|

市場調査レポート

商品コード

1406569

子宮筋腫核出術:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Myomectomy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 子宮筋腫核出術:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

子宮筋腫核出術市場は、2024年の6億4,000万米ドルから2029年には9億3,000万米ドルに成長し、予測期間(2024年~2029年)のCAGRは8.1%を記録すると予測されています。

COVID-19の大流行が子宮筋腫核出術市場に与えた影響は大きいです。世界中でCOVID-19患者が急増したため、ヘルスケアサービスはCOVID-19に苦しむ患者にリソースを振り向けた。パンデミック時の患者管理のためのガイドラインや勧告が提供されました。その結果、病院は緊急処置を優先し、子宮筋腫摘出手術などの選択的処置を遅らせたり延期したりすることになり、何カ月も手術を待つ患者の滞留を招いた。例えば、Lancet Rheumatology誌が2021年2月に発表した論文によると、パンデミックの初期には、多くの国がCOVID-19患者の治療に人員とリソースを割くために、緊急ではない外科手術をすべてキャンセルするという必要な決定を下し、選択的手術の待ち時間の延長は、パンデミック中にヘルスケアシステムが直面した大きな問題の一つに過ぎなかった。しかし、パンデミックの状況が正常に戻ったため、子宮筋腫摘出術は徐々に回復すると予想され、本調査の予測期間中、市場は安定した成長が見込まれます。

子宮筋腫を患う患者数の増加が、子宮筋腫核出術市場の成長に寄与する主要因になると予測されています。2022年7月にInternational Journal of Reproduction, Contraception, Obstetrics, and Gynecologyによって発表された記事によると、子宮筋腫の発生率は31~40歳に最も多く、約34.9%であることを示す研究がインドで実施されました。子宮筋腫で最もよく観察される症状は、腹部のしこり(41%)と異常子宮出血(24.1%)でした。粘膜下筋腫の有病率は38.6%、硬膜内筋腫19.3%、粘膜下ポリープ14.5%、実生筋腫13.9%、漿膜下筋腫10.2%でした。さらに、合併症の減少や入院期間の短縮による低侵襲外科手術の増加が、市場の成長につながると予想されています。また、質の高い効率的な治療を提供するためのロボット手術や腹腔鏡支援手術の増加などの技術的進歩も、子宮筋腫核出術市場の成長に寄与する可能性があります。

2021年12月にMISジャーナルが発表した記事によると、子宮筋腫は一般的な子宮の良性平滑筋腫瘍と考えられており、閉経までの女性のほぼ70%が罹患しています。子宮筋腫の危険因子には、民族性、分娩数、初潮の早さ、閉経の遅さ、家族歴、肥満、高血圧などがあります。子宮筋腫があっても生命を脅かすことはほとんどないです。しかし、異常出血、骨盤痛、尿路障害など、生活の質に影響する症状を伴うことが多いです。また、ロボット筋腫核出術は、開腹手術に比べて出血量が少なく、合併症が少なく、入院期間が短いなど、子宮筋腫核出術には多くの利点があると記事は述べています。また、手首で操作する器具、三次元的な視野、正しい手術手技を取り入れることの利点も、大規模で多数の症例におけるロボット支援アプローチの利点を強調しています。このように、子宮筋腫の負担が大きく、技術的に進歩した子宮筋腫核出術の利点が増加していることも、市場の成長を後押しすると予想されます。

したがって、子宮筋腫の有病率の上昇や技術的に進歩した子宮筋腫核出術の利点の増加といった上記の要因は、市場成長を後押しすると予想されます。しかし、新しい医療機器のコスト高や手術に伴う合併症が、調査対象市場の成長を制限する可能性があります。

子宮筋腫核出術市場の動向

予測期間中、腹腔鏡セグメントが大きな市場シェアを占める見込み

腹腔鏡下子宮筋腫核出術は、外科医がおへそまたはその近くを小さく切開する手術法です。その後、腹腔鏡を挿入します。腹腔鏡とは、カメラを取り付けた細いチューブのことです。腹腔鏡下子宮筋腫核出術には、出血量が少ない、入院期間が短い、回復が早い、術後の合併症や癒着形成率が低いなどの利点があります。このように、腹腔鏡下子宮筋腫核出術の利点の増加は、同分野の成長を後押しすると予想されます。さらに、子宮筋腫の有病率の増加や、腹腔鏡筋腫核出術の技術的進歩の高まりも、セグメントの成長を押し上げると予想されています。

2022年9月にPubMed Centralが発表した論文によると、腹腔鏡下子宮筋腫摘出術は子宮筋腫摘出の一般的な手技の1つです。また、包括的なリハビリテーション看護と組み合わせた腹腔鏡下子宮筋腫摘出術は、子宮筋腫患者の術後のストレス状態を効果的に軽減し、患者の満足度を向上させ、有害感情を軽減し、リハビリテーションを促進することが示されたという研究結果も発表されています。このように、腹腔鏡下子宮筋腫核出術の利点の増加は、同分野の成長を促進する主な要因となっています。

さらに、子宮筋腫の有病率の上昇は、市場の成長を促進する主な要因です。例えば、英国NHSが2022年9月に更新したデータによると、子宮筋腫は一般的であり、約3人に2人の女性が人生のある時点で少なくとも1つの筋腫を発症しており、30~50歳の女性に最も多く発症しています。このように、子宮筋腫の有病率の高さは、本調査の予測期間中、腹腔鏡下子宮筋腫核出術の採用を後押しすると予想されます。さらに、泌尿器科疾患に関する調査の増加も予測期間中のセグメント成長を後押しすると予想されています。

したがって、腹腔鏡下子宮筋腫核出術の利点の増加、泌尿器科疾患に関する研究の増加、子宮筋腫の有病率の上昇といった上述の要因は、予測期間中のセグメント成長を高めると予想されます。

予測期間中、北米が子宮筋腫核出術市場で大きなシェアを占める見込み

北米は、子宮筋腫の有病率の上昇と筋腫核出術の技術的進歩により、予測期間にわたって筋腫核出術市場で大きなシェアを占めると予想されます。

米国女性健康局が2021年2月に更新したデータによると、女性の約20%から80%が50歳になるまでに子宮筋腫を発症すると推定されています。子宮筋腫は40代から50代前半の女性に多いといわれ、筋腫のある女性すべてに症状があるわけではないが、症状がある女性は筋腫を生きづらいと感じていることが多いです。このように、米国では子宮筋腫の負担が大きいため、市場の成長が期待されています。

さらに、2022年12月にTaylor &Francis Onlineが発表した記事によると、子宮筋腫(UF)は子宮の非がん性増殖といわれ、米国では2,600万人以上の女性の生活に影響を与えています。子宮筋腫は症状を伴わないこともあるが、その存在が外科的治療につながる女性もいます。したがって、子宮筋腫の有病率の高さが市場の成長を後押しすると予想されます。

したがって、子宮筋腫の有病率の上昇などの上記の要因は、予測期間にわたって同地域の市場成長を高めると予想されます。

子宮筋腫核出術産業の概要

子宮筋腫核出術市場は依然として競争が激しく、大手企業が市場を独占しています。技術の進歩や製品の革新は、市場内で競争する企業に新たな機会を提供すると思われます。腹腔鏡やロボット支援による子宮筋腫核出術は、従来の方法よりも優れているため、市場の成長を促進する可能性があります。主な企業としては、Medtronic PLC、Stryker Corporation、ConMed Corporation、INSIGHTEC Ltd、CooperSurgical Inc.、Hologic Inc.、KARL STORZ SE &Co.KG、B Braun、Richard Wolf Medical Instruments、Minerva Surgical Inc.

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 子宮筋腫に苦しむ患者数の増加

- 低侵襲手術の増加

- 技術の進歩

- 市場抑制要因

- 医療機器の高コスト

- 手術に伴う合併症

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- 腹腔鏡

- 腹腔鏡

- 子宮鏡下

- ロボット

- 製品別

- 腹腔鏡パワーモルセレーター

- ハーモニックメス

- 腹腔鏡シーラー

- その他の製品

- エンドユーザー別

- クリニック/病院

- 外来手術センター

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 世界のその他の地域

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic PLC

- Stryker Corporation

- ConMed Corporation

- INSIGHTEC Ltd

- CooperSurgical Inc.

- Hologic Inc.

- Intuitive Surgical Inc.

- KARL STORZ SE & Co. KG

- B Braun SE

- Richard Wolf Medical Instruments

- Minerva Surgical Inc.

第7章 市場機会と今後の動向

The myomectomy market is expected to grow from USD 0.64 billion in 2024 to USD 0.93 billion by 2029, registering a CAGR of 8.1% over the forecast period (2024-2029).

The impact of the COVID-19 pandemic was significant on the myomectomy market. With the surge of COVID-19 cases worldwide, healthcare services diverted their resources toward patients suffering from COVID-19. Guidelines and recommendations were provided for the management of patients during the pandemic. This resulted in hospitals prioritizing emergency procedures and delaying or postponing elective procedures, such as myomectomy surgery, leading to a backlog of patients waiting for their surgeries for months. For instance, according to an article published by the Lancet Rheumatology in February 2021, during the initial pandemic, many countries made the necessary decision to cancel all non-emergency surgical procedures to free up personnel and resources to care for patients with COVID-19 and extended wait times for elective surgeries was but one of the big problems that healthcare systems faced during the pandemic. However, as the pandemic conditions have returned to normal, myomectomy procedures are expected to recover gradually, and the market is expected to have stable growth during the forecast period of the study.

An increase in the number of patients suffering from uterine fibroids is anticipated to be the key factor contributing to the growth of the myomectomy market. According to an article published by the International Journal of Reproduction, Contraception, Obstetrics, and Gynecology in July 2022, a study was conducted in India which showed that the incidence of fibroids is most common in 31-40 years of age, which is around 34.9%. The most commonly observed symptom for uterine fibroids was abdominal lump (41%) and abnormal uterine bleeding (24.1%). The prevalence of submucosal fibroids was 38.6%, intramural fibroids 19.3%, submucosal polyp 14.5%, seedling fibroid 13.9%, and subserosal fibroid 10.2%. Additionally, a rise in minimally invasive surgical procedures due to fewer complications and reduced hospital stays is anticipated to grow the market. Technological advancements, such as the rise in robotic and laparoscopic-assisted surgeries to deliver quality and efficient treatment, may also contribute to the growth of the myomectomy market.

According to an article published by MIS Journal in December 2021, uterine fibroids are considered a common benign smooth muscle tumor of the uterus that affects almost 70% of women until menopause. Risk factors of uterine fibroids include ethnicity, parity, early menarche, late menopause, family history, obesity, and hypertension. The presence of uterine fibroids is rarely life-threatening. Still, they are often associated with symptoms affecting the quality of life, such as abnormal bleeding, pelvic pain, and urinary tract problems. The article also stated that robotic myomectomy has many advantages in uterine fibroid removal, such as lower blood loss, fewer complications, and shorter hospital stays over open surgery. The advantages of the wristed instruments, three-dimensional vision, and the incorporation of correct surgical techniques also emphasize the benefits of the robotic-assisted approach in large and numerous cases. Thus, the high burden of uterine fibroids and the increasing advantages of technologically advanced myomectomy procedures are also expected to boost market growth.

Hence, the factors above, such as the rising prevalence of uterine fibroids and the increasing advantages of technologically advanced myomectomy procedures, are expected to boost the market growth. However, the higher costs of new medical devices and complications associated with the procedure might restrict the growth of the studied market.

Myomectomy Market Trends

Laparoscopic Segment is Expected to Hold a Significant Market Share over the Forecast Period

Laparoscopic myomectomy is a surgical procedure where the surgeon makes a small incision in or near the belly button. Then a laparoscope is inserted, a narrow tube fitted with a camera into the abdomen. Laparoscopic myomectomy has several advantages such as less blood loss, shorter hospital stays, faster recovery, and lower complications and adhesion formation rates after surgery. Thus, the increasing advantages of laparoscopic myomectomy are expected to boost segment growth. Moreover, the increasing prevalence of uterine fibroids and the rising technological advancements in the laparoscopic myomectomy procedure are also expected to boost segment growth.

According to an article published by PubMed Central in September 2022, laparoscopic myomectomy is one of the common procedures for uterine fibroids removal. Also, the article stated that a study showed that laparoscopic myomectomy combined with comprehensive rehabilitation nursing effectively reduced the postoperative stress state of patients with uterine fibroids, improved patient satisfaction, reduced adverse emotions, and promoted rehabilitation. Thus, the increasing advantages of laparoscopic myomectomy are a major factor driving the segment growth.

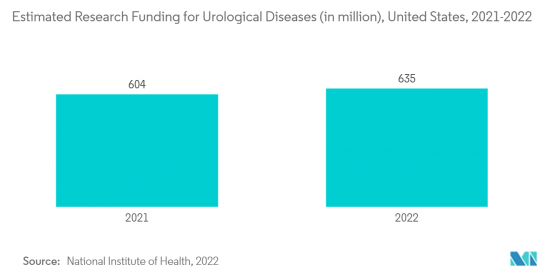

Furthermore, the rising prevalence of uterine fibroids is a major factor driving the market's growth. For instance, according to the data updated by the United Kingdom NHS in September 2022, uterine fibroids were common, with around 2 in 3 women developing at least 1 fibroid at some point in their life, and they most often occured in women aged 30 to 50. Thus, the high prevalence of uterine fibroids is expected to boost the adoption of laparoscopic myomectomy during the forecast period of the study. Moreover, the increasing research on urological diseases is also expected to boost segment growth in the forecast period.

Hence, the abovementioned factors such as the increasing advantages of laparoscopic myomectomy, the increasing research on urological diseases, and the rising prevalence of uterine fibroids are expected to enhance the segment growth over the forecast period.

North America is Expected to Hold a Significant Share in the Myomectomy Market Over the Forecast Period

North America is expected to hold a significant share of the myomectomy market over the forecast period due to the rising prevalence of uterine fibroid and technological advancements in myomectomy procedures.

According to the data updated by the United States Office on Women's Health in February 2021, it was estimated that about 20 percent to 80 percent of women developed fibroids by the time they reached age 50. Uterine fibroids are said to be most common in women in their 40s and early 50s, and not all women with fibroids have symptoms, but women who do have symptoms often find fibroids hard to live with. Thus, the high burden of uterine fibroids in the United States is expected to boost market growth.

Furthermore, according to an article published by Taylor & Francis Online in December 2022, uterine fibroids (UF) were said to be noncancerous growths of the uterus and impact the livelihood of over 26 million women in the United States. Although UF may not have accompanying symptoms, their presence leads to surgical treatment for some women. Thus, the high prevalence of uterine fibroids is expected to boost market growth.

Hence, the abovementioned factors, such as the rising prevalence of uterine fibroids, are expected to enhance the market growth in the region over the forecast period.

Myomectomy Industry Overview

The myomectomy market remains highly competitive, with major players dominating the market. Technological advancements and product innovations will likely provide new opportunities for the players to compete within the market. The rise in laparoscopic and robotic-assisted myomectomy procedures due to their advantages over traditional methods may drive the market's growth. Some of the major players include Medtronic PLC, Stryker Corporation, ConMed Corporation, INSIGHTEC Ltd, CooperSurgical Inc., Hologic Inc., KARL STORZ SE & Co. KG, B Braun, Richard Wolf Medical Instruments, and Minerva Surgical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Number of Patients Suffering from Uterine Fibroids

- 4.2.2 Rise in Minimally Invasive Procedures

- 4.2.3 Technological Advancements

- 4.3 Market Restraints

- 4.3.1 High Cost of Medical Devices

- 4.3.2 Complications Associated with the Procedure

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Abdominal

- 5.1.2 Laparoscopic

- 5.1.3 Hysteroscopic

- 5.1.4 Robotic

- 5.2 By Product

- 5.2.1 Laparoscopic Power Morcellators

- 5.2.2 Harmonic Scalpel

- 5.2.3 Laparoscopic Sealer

- 5.2.4 Other Products

- 5.3 By End User

- 5.3.1 Clinics/Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic PLC

- 6.1.2 Stryker Corporation

- 6.1.3 ConMed Corporation

- 6.1.4 INSIGHTEC Ltd

- 6.1.5 CooperSurgical Inc.

- 6.1.6 Hologic Inc.

- 6.1.7 Intuitive Surgical Inc.

- 6.1.8 KARL STORZ SE & Co. KG

- 6.1.9 B Braun SE

- 6.1.10 Richard Wolf Medical Instruments

- 6.1.11 Minerva Surgical Inc.