|

|

市場調査レポート

商品コード

1198022

ポリエチレンワックス市場- 成長、動向、予測(2023年-2028年)Polyethylene Wax Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ポリエチレンワックス市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年01月23日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

ポリエチレンワックスの市場は、予測期間中、世界的に約4%のCAGRで成長すると予想されています。

ポリ塩化ビニル加工におけるポリエチレンワックスの使用量の増加とその他の要因が、市場の成長を促進しています。一方、原料コストの変動やCOVID-19の発生による不利な条件が、市場の成長を妨げています。

主なハイライト

- ポリエチレンワックス市場は、プラスチック分野からの需要増加により、予測期間中に成長すると予想されます。

- アジア太平洋地域は最大の市場であり、中国、インド、日本などの国々での消費増加により、予測期間中に最も急速に成長する市場となる見込みです。

ポリエチレンワックスの市場動向

プラスチック産業からの需要拡大

- ポリエチレンワックスは、その優れた特性からプラスチック製造に広く使用されており、予測期間中に急成長すると見込まれています。

- ポリエチレンワックスは、主にエチレンの直接高圧重合、高分子量ポリエチレン樹脂の熱分解、低分子ワックスの精製などの工程で製造されています。

- ポリエチレンワックスは、プラスチックの製造工程で広く使用されており、その粘着防止特性により、潤滑性が向上します。また、粘度や融点を調整することで潤滑性を高めたり、フィラーの分散性を向上させる効果もあります。また、プラスチックの耐熱性を向上させ、熱安定性を高める効果もあります。

- プラスチックは私たちの日常生活に欠かせないものとなっており、自動車や包装などさまざまな産業でプラスチックに対する需要が高まっていることから、予測期間中、ポリエチレンワックスの市場を牽引するものと期待されています。

アジア太平洋地域が市場を独占

- インドや中国などの国々からプラスチック・ゴム、塗料・コーティング、接着剤などの需要が増加していることから、アジア太平洋地域が予測期間中にポリエチレンワックスの市場を独占すると予想されます。

- 2019年だけでも、中国は約7500万トンのプラスチックを生産しており、これは世界の総プラスチック生産量の約20%にあたります。プラスチックは、軽量で耐久性があるため、主に包装産業で使用されています。eコマース市場の拡大は、プラスチック消費全体の約30%を占めるプラスチックの需要を牽引することが期待されます。プラスチック産業の成長は、ポリエチレンワックスの市場を牽引すると予想されます。

- 繊維分野では、ポリエチレンワックスから作られたエマルションが、柔軟性を向上させ、酸に対する耐性を提供し、生地の黄変や色調変化を解消しています。

- 繊維省年次報告書2018-19によると、インドの繊維産業は、金額ベースで産業生産高の7%、インドのGDPの2%、同国の輸出収益の15%に寄与しています。現在、インドには世界最大級の若年層が存在し、人口の半数が25歳以下です。この若い層が衣料品の最大の消費者であり、予測期間中、市場を牽引することが期待されます。

- さらに、中国の国家発展改革委員会は、2019年の最初の11ヶ月間のアパレルおよびニットウェアの国内売上高は約1724億米ドルであり、2018年の同時期と比較して前年同期比で約3%の成長であったと述べています。

- 塗料・コーティングでは、ポリエチレンワックスはより良い撥水性を提供し、沈降防止特性を向上させ、耐摩耗性を提供します。中国やインドなどの国々で建設部門が拡大していることが、市場を牽引すると予想されます。

- 前述の要因は、政府の支援と相まって、予測期間中にアジア太平洋地域でポリエチレンワックスの需要が増加する要因となっています。

ポリエチレンワックス市場の競合他社分析

ポリエチレンワックスの世界市場は部分的に断片化されており、プレーヤーが占めるシェアはごくわずかです。少数の企業は、Clariant、BASF SE、MITSUI CHEMICALS AMERICA, INC、DEUREX AG、SCG Chemicalsを含みます。

その他の特典

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 塩化ビニル樹脂加工におけるポリエチレンワックスの使用増加

- その他の促進要因

- 抑制要因

- 不安定な原料コスト

- COVID-19の発生による不利な状況

- 産業バリューチェーン分析

- ポーターズファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

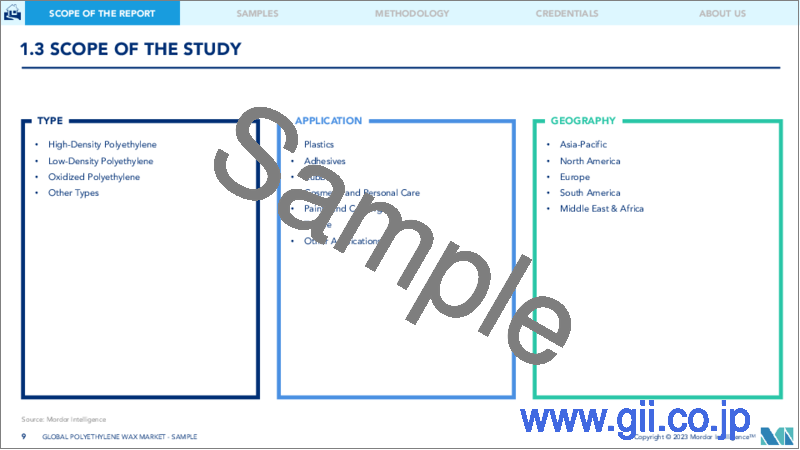

第5章 市場セグメンテーション

- 種類

- 高密度ポリエチレン

- 低密度ポリエチレン

- 酸化ポリエチレン

- その他

- 用途

- プラスチック

- 粘着剤

- ゴム

- 化粧品

- 塗料・コーティング

- 繊維

- その他

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米地域

- 中東地域

- サウジアラビア

- 南アフリカ共和国

- その他の中東地域

- アジア太平洋地域

第6章 競合情勢

- M&A、合弁事業、提携、契約

- 市場シェア(%)/ランキング分析

- 主要なプレーヤーが採用する戦略

- 企業プロファイル

- BASF SE

- Carmel Industries

- Cerax

- Clariant

- DEUREX AG

- Marcus Oil

- MITSUI CHEMICALS AMERICA, INC

- Pishro Chem Co.LTD

- Repsol

- SANYO CHEMICAL, LTD

- SAVITA

- SCG Chemicals Co., Ltd.

- SQIWAX

- WIWAX

- WSD Chemical limited

第7章 市場機会と今後の動向

- 新興国におけるプラスチックの需要拡大

- その他のビジネスチャンス

The market for polyethylene wax is expected to grow at a CAGR of about 4% globally during the forecast period. Increasing usage of polyethylene wax in polyvinyl chloride processing coupled with other drivers are driving the market growth. On the flip side, volatile raw material costs, and unfavorable conditions arising due to the COVID-19 outbreak are hindering the growth of the market.

Key Highlights

- The polyethylene wax market is expected to grow during the forecast period owing to the increasing demand from the plastics segment.

- Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

Polyethylene Wax Market Trends

Growing Demand from the Plastics Industry

- Polyethylene wax is widely used in the plastics manufacturing owing to its superior characteristics and is expected to grow rapidly during the forecast period.

- Polyethylene waxes are mainly manufactured using one of the following processes direct high-pressure polymerization of ethylene, thermal degradation of high molecular weight polyethylene resins and refining low polymer wax.

- Polyethylene waxes are widely used in plastics manufacturing owing to its anti-sticking properties. Additionally, they also provide more lubrication by modifying viscosity or melt point and improve the dispersion of fillers during plastics manufacturing. They improve plastic's resistance to heat and increase thermal stability.

- Plastics have become an integral part of our daily life, the growing demand for plastics from various industries such as automotive and packaging is expected to drive the market for polyethylene wax during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for polyethylene wax during the forecast period as a result of the increase in demand for plastics & rubber, paints & coatings and adhesives from countries like India and China.

- In 2019 alone, China produced about 75 million tons of plastic which are about 20% of the total world's plastic production. Plastic is mainly used in the packaging industry for its light-weight and durability. The increasing e-commerce market is expected to drive the demand for plastics which accounts for around 30% of total plastics consumption. The growing plastics industry is expected to drive the market for polyethylene wax.

- In the textile sector, emulsions made from polyethylene wax improve softening and provide resistance against acids and eliminate yellowing & color change of fabrics.

- As per the Ministry of Textiles annual report 2018-19, India's textile industry contributes to 7% of industry output in value terms, 2% of India's GDP and 15% of the country's export earnings. Currently, India has one of the world's largest young population and half of the population is under 25. This young group is the largest consumer of apparels and is expected to drive the market during the forecast period.

- Furthermore, China's National Development and Reform Commission, stated that the domestic sales of apparel and knitwear stood at around USD 172.4 billion for the first 11 months of 2019, which represents growth of about 3% Y-o-Y over same time period in 2018.

- In paints & coatings, polyethylene wax provides better water repellency, improves anti-settling properties and provides abrasion resistance. The growing construction sector in countries like China and India is expected to drive the market.

- The aforementioned factors, coupled with government support, are contributing to the increasing demand for polyethylene wax in the Asia-Pacific region during the forecast period.

Polyethylene Wax Market Competitor Analysis

The global polyethylene wax market is partially fragmented with players accounting for a marginal share of the market. Few companies include Clariant, BASF SE, MITSUI CHEMICALS AMERICA, INC, DEUREX AG and SCG Chemicals Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Polyethylene Wax in Poly Vinyl Chloride Processing

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatile Raw Material Costs

- 4.2.2 Unfavorable Conditions Arising Due to COVID-19 Outbreak

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 High Density Polyethylene

- 5.1.2 Low Density Polyethylene

- 5.1.3 Oxidized Polyethylene

- 5.1.4 Others

- 5.2 Application

- 5.2.1 Plastics

- 5.2.2 Adhesives

- 5.2.3 Rubber

- 5.2.4 Cosmetics

- 5.2.5 Paints & Coatings

- 5.2.6 Textile

- 5.2.7 Others

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Carmel Industries

- 6.4.3 Cerax

- 6.4.4 Clariant

- 6.4.5 DEUREX AG

- 6.4.6 Marcus Oil

- 6.4.7 MITSUI CHEMICALS AMERICA, INC

- 6.4.8 Pishro Chem Co.LTD

- 6.4.9 Repsol

- 6.4.10 SANYO CHEMICAL, LTD

- 6.4.11 SAVITA

- 6.4.12 SCG Chemicals Co., Ltd.

- 6.4.13 SQIWAX

- 6.4.14 WIWAX

- 6.4.15 WSD Chemical limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand for Plastics From Emerging Economies

- 7.2 Other Opportunities