|

市場調査レポート

商品コード

1689878

包装用フォーム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Packaging Foams - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 包装用フォーム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

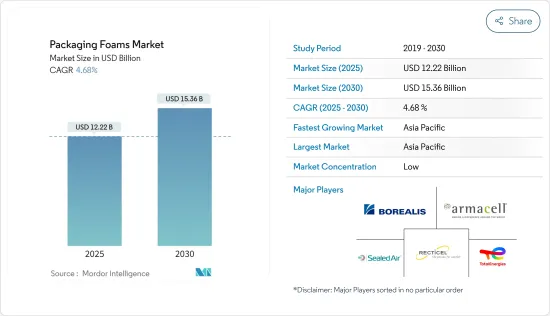

包装用フォーム市場規模は2025年に122億2,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは4.68%で、2030年には153億6,000万米ドルに達すると予測されています。

COVID-19は2020年の世界経済にマイナスの影響を与えました。サプライチェーンに支障をきたし、包装部門などいくつかの産業部門に影響を与えました。ロックダウンとシャットダウンは、シャッター、国際的なサプライチェーン、および様々な分野にわたって大幅に購入小売事業の行動を変更しました。しかし、2021年後半に規制が解除された後、消費者はオンラインショッピングや輸送活動の増加により、食料品やその他の食品をオンラインで注文することが増えているため、利便性への需要が高まり、業界は回復を示しました。

主なハイライト

- 短期的には、工業包装業界からの需要増が市場成長の主な要因です。

- しかし、環境に優しい代替品として成形パルプが入手可能であることが、予測期間中に対象産業の成長を抑制すると予想される主な要因です。

- とはいえ、環境に優しい包装用発泡体への要求の高まりは、近いうちに世界市場に有利な成長機会を生み出す可能性が高いです。

- アジア太平洋は包装用フォームの世界市場を独占すると予測されており、中国やインドなどの国々で市場用途が増加していることから、予測期間中に最も急成長する市場になると推定・予測されています。

包装用フォーム市場の動向

工業包装分野からの需要の増加

- 包装用フォームは一般的に箱の緩衝材として使用されており、このパッケージングソリューションは汎用性が高く、カスタマイズできることで知られています。

- フォームは、工業製品、家電製品、自動車など、最適な保護と耐久性が最優先される様々な包装用途や産業で使用されています。

- 自動車部品は取り扱いが難しく、保管や輸送の際に特に注意が必要な部品もあります。これは、いくつかの部品、特に内装やエンジンの部品が入り組んでいるためです。

- 世界の自動車産業は調査期間中に大きな成長を記録しました。OICAによると、2021年の自動車生産台数は8,014万5,988台で、2020年と比較して3%の成長率を記録しました。アジア太平洋地域は、2021年の生産台数が4,673万2,785台で、世界の自動車市場で最も高いシェアを占めています。

- 国勢調査局によると、米国の小売eコマース売上高は2,659億米ドルで、2022年第2四半期から3.0%増加した(+-0.5%)。

- 欧州のeコマース産業は、2021年末時点で7兆7,180億ユーロ(7兆9,023億2,000万米ドル)と評価され、昨年の状況と比較して13%の増加を記録しました。この地域の主な貢献は北欧で、eコマース総額の86%を占めています。

- さらに、ミリタリーフォーム包装は、商業用包装よりも細部にまで気を配る必要があります。内容物が繊細であるため、軍事用貨物の膨大な割合が慎重な梱包と取り扱いを必要としています。軍用品は頻繁に世界中を移動するため、安全な輸送を確保するために高品質の防衛用発泡梱包を使用する必要があります。

- このように、輸送とeコマース産業の成長は、包装セクターの飛躍的な成長につながり、また、グリーン包装の意識の高まりと使用から支援を受けています。従って、これらの動向は、予測される数年間において、包装用発泡スチロール市場に潜在的にプラスの影響を与えると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋が世界の包装用発泡スチロール市場を独占している主な理由は、物流における包装需要の増加、工業および自動車製造の増加、その他の製造事業によるものです。

- 中国は、世界、特にアジア太平洋の包装用発泡体市場に大きく貢献している国の一つです。飲食品、自動車、エレクトロニクス、パーソナルケア、製薬産業の成長が市場の成長を後押しすると期待されています。

- 中国は世界最大の食品産業の一つです。中国国家統計局によると、2021年、中国の食品産業は約6,187億人民元(863億3,000万米ドル)の総利益を生み出しました。このうち、食品製造業は約1,654億人民元(230億8,000万米ドル)の利益に貢献しました。

- 経済産業省(日本)によれば、2021年の日本のエレクトロニクス産業の総生産額は約10兆9,500億円(800億米ドル)で、前年比110%です。さらに、2021年の電子機器輸出総額は10兆8,200億円(790億米ドル)に達し、2021年12月だけで1兆400億円(76億米ドル)に達するため、この地域の包装用発泡体には莫大な需要がもたらされます。

- 韓国のeコマース市場は年間920億米ドルを超えています。建設と投資の波は、GIC、APG、アンジェロ・ゴードン、ウォーバーグ・ピンカス、ブラックストーンなどの国際的な投資家から大きな関心と資本を引き寄せています。韓国はまた、アジア太平洋で第4位のサードパーティ・ロジスティクス(3PL)市場であり、年率8%近い成長率で、日本、オーストラリア、シンガポールよりも速いペースで成長しています。

- 従って、アジア太平洋地域で包装産業が急成長しているため、包装用フォームの需要も予測期間中に急速に増加すると予想されます。

包装用フォーム業界の概要

包装用フォーム市場は、その性質上、部分的に断片化されています。主な企業は、Borealis AG、Sealed AIR、Armacell、TotalEnergies、Recticel NV/SAなどである(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 包装業界からの需要増加

- 抑制要因

- グリーン代替品としての成形パルプ

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 素材

- ポリスチレン

- ポリウレタン

- ポリオレフィン

- その他の素材

- 構造

- 柔軟

- 硬質

- 用途

- 食品包装

- 工業包装

- 輸送

- 電気・電子

- パーソナルケア

- 医薬品

- その他の産業用包装

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Armacell

- Atlas Roofing Corporation

- Borealis AG

- Drew Foam

- Foamcraft Inc.

- TotalEnergies

- Huntington Solutions

- Recticel

- Sealed Air

- Williams Foam

- Zotefoams PLC

第7章 市場機会と今後の動向

- 環境に優しい包装用発泡体への要求の高まり

The Packaging Foams Market size is estimated at USD 12.22 billion in 2025, and is expected to reach USD 15.36 billion by 2030, at a CAGR of 4.68% during the forecast period (2025-2030).

COVID-19 had a negative impact on the global economy in 2020. It affected several industrial sectors such as the packaging sector by hindering their supply chain. The lockdown and shutdown have changed the behavior of retail business shuttered, international supply chains, and purchase significantly across various sectors. However, the industry witnessed a recovery, with the growing demand for convenience as consumers are increasingly ordering groceries and other food products online owing to increased online shopping and transportation activities after the lifting of restrictions in the second half of 2021.

Key Highlights

- Over the short term, the rising demand from the industrial packaging industries is a major factor driving the growth of the market studied.

- However, the availability of molded pulp as a green alternative is a key factor anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the growing quest for eco-friendly packaging foam is likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific is expected to dominate the global packaging foams market, and it is also estimated to be the fastest-growing market over the forecast period due to the increasing market applications in countries such as China and India.

Packaging Foam Market Trends

Increasing Demand from the Industrial Packaging Sector

- Packaging foam is commonly used as a cushioning material for boxes, and this packaging solution is known for its versatility and ability to be customized.

- Foams are used in a wide variety of packaging applications and industries including industrial goods, consumer electronics, automotive, and other applications where optimum protection and durability are overriding considerations.

- Automotive spares are difficult to handle, and some parts necessitate extra caution during storage and transportation. This is due to the intricate nature of some parts, particularly those in the interior and engine.

- The global automotive industry registered huge growth in the studied period. According to OICA, the total number of vehicles produced in 2021 was 80,145,988 and witnessed a growth rate of 3% compared to 2020. The Asia-Pacific region holds the highest production share in the global automotive market with 46,732,785 units in 2021.

- According to the Census Bureau, United States retail e-commerce sales amounted to USD 265.9 billion, an increase of 3.0 percent (+-0.5%) from the second quarter of 2022.

- The European e-commerce industry was valued at EUR 7718 billion (USD 7,902.32 billion) at the end of 2021, registering an increase of 13 % as compared to the situation last year. The major contribution in the region comes from Northern Europe, which accounts for 86% of the total e-commerce value.

- Moreover, Military foam packaging necessitates a higher level of attention to detail than commercial packaging. Because of the sensitive contents, a huge proportion of military cargo requires careful packing and handling. Military equipment is frequently moved around the world, which necessitates the use of high-quality defense foam packaging to ensure safe shipping.

- Thus, the growth in transportation and e-commerce industries has led to the exponential growth of the packaging sector, also taking support from the rising awareness and use of green packaging. Therefore, these trends are expected to have a potentially positive impact on the packaging foam market in the forecast years.

Asia-Pacific to Dominate the Market

- Asia-Pacific dominated the global packaging foams market primarily due to the growing demand for packaging in logistics, the growing industrial and automotive manufacturing and other manufacturing operations.

- China is one of the major contributors to the packaging foams markets globally, especially in Asia-Pacific. The growing food and beverages, automotive, electronics, personal care, and pharmaceutical industry are expected to boost the growth of the market.

- China has one of the largest food industries in the world. As per the National Bureau of Statistics of China, in 2021, the food industry in China generated a total profit of about CNY 618.7 billion (USD 86.33 billion). The food manufacturing industry contributed approximately CNY 165.4 billion (USD 23.08 billion) to the total profits.

- As per METI (Japan), the total production value of the electronics industry in Japan is around JPY 10.95 trillion (USD 80 billion) in 2021, which is 110% of the production value compared to the last year. Furthermore, the total electronics exports in 2021 amount to JPY 10.82 trillion (USD 79 billion) with JPY 1.04 trillion (USD 7.6 billion) in December 2021 alone, thus providing huge demand for packaging foams in the region.

- The South Korean e-commerce market stands at over USD 92 billion per annum. A wave of building and investment has been drawing significant interest and capital from international investors, including GIC, APG, Angelo Gordon, Warburg Pincus, and Blackstone. South Korea is also the 4th-largest third-party logistics (3PL) market in Asia-Pacific and is growing at an annual rate of nearly 8%, faster than Japan, Australia, and Singapore.

- Hence, owing to the rapidly growing packaging industry in the Asia-Pacific region, the demand for packaging foams is also expected to increase rapidly over the forecast period.

Packaging Foam Industry Overview

The packaging foams market is partially fragmented in nature. The major companies include (not in any particular order) Borealis AG, Sealed AIR, Armacell, TotalEnergies, and Recticel NV/SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Packaging Industry

- 4.2 Restraints

- 4.2.1 Molded Pulp as a Green Alternative

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material

- 5.1.1 Polystyrene

- 5.1.2 Polyurethane

- 5.1.3 Polyolefin

- 5.1.4 Other Materials

- 5.2 Structure

- 5.2.1 Flexible

- 5.2.2 Rigid

- 5.3 Application

- 5.3.1 Food Packaging

- 5.3.2 Industrial Packaging

- 5.3.2.1 Transportation

- 5.3.2.2 Electrical and Electronics

- 5.3.2.3 Personal Care

- 5.3.2.4 Pharmaceutical

- 5.3.2.5 Other Industrial Packaging

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East & Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Armacell

- 6.4.2 Atlas Roofing Corporation

- 6.4.3 Borealis AG

- 6.4.4 Drew Foam

- 6.4.5 Foamcraft Inc.

- 6.4.6 TotalEnergies

- 6.4.7 Huntington Solutions

- 6.4.8 Recticel

- 6.4.9 Sealed Air

- 6.4.10 Williams Foam

- 6.4.11 Zotefoams PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Quest for Eco-friendly Packaging Foam