|

市場調査レポート

商品コード

1406064

フッ素系界面活性剤 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測Fluorosurfactant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| フッ素系界面活性剤 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

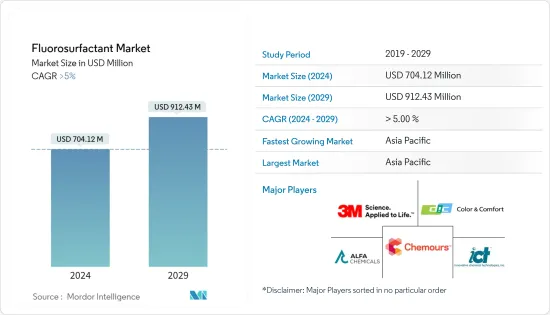

フッ素系界面活性剤市場規模は、2024年に7億412万米ドルと推定され、2029年には9億1,243万米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは5%以上で成長すると予測されます。

フッ素系界面活性剤市場は、塗料やコーティング剤、洗剤などの業界が封じ込め対策や経済的混乱のために生産の遅れを余儀なくされたため、生産と移動の減速があり、COVID-19の流行によってマイナスの影響を受けました。現在、市場はパンデミックから回復しています。市場は2022年にパンデミック以前の水準に達し、今後も安定した成長が見込まれます。

フッ素系界面活性剤市場は、塗料・コーティング業界からの需要増加により、予測期間中に成長すると予想されます。

その反面、炭化水素系やシリコン系の界面活性剤と比較すると価格が高いことが、市場の成長を妨げています。

さらに、フッ素系界面活性剤は、腐食性の化学薬品に対する高い安定性、高い絶縁耐力などのため、電子塗料に使用されており、予測期間中に市場機会を生み出すと予測されています。

アジア太平洋地域は、中国、インド、日本などの国々からの消費が最も多く、世界全体で市場を独占しています。

フッ素系界面活性剤の市場動向

塗料・コーティング業界からの需要拡大

- フッ素系界面活性剤は、疎水性部分と親水性部分を持つ両親媒性分子です。疎水性の尾部はフルオロカーボンであり、親水性の部分は電荷に基づいて特徴付けられます。

- 界面活性剤はしばしば界面活性剤と呼ばれ、液体と気体の間、液体と固体の間、あるいは混じり合わない二つの相の間の表面張力を低下させる。これにより塗膜の表面張力が低下し、より滑らかで優れた仕上がりが得られます。

- フッ素界面活性剤は、顔料と基材の濡れ性とレベリング性を向上させ、高いオープンタイムを提供します。フッ素の電気陰性度が高く、フッ素と炭素原子の結合が非常に安定しているため、フッ素系界面活性剤は他の界面活性剤よりも安定性が高く、様々な条件に適しており、好まれています。

- 米国国勢調査局によると、2022年の民間建設額は1兆4,342億米ドルで、2021年の1兆2,795億米ドルを11.7%上回った。2022年の住宅建設支出は8,991億米ドルで、2021年の7,937億米ドルから13.3%増加しました。このように、建設活動の拡大が市場の成長を促進すると予想されます。

- さらに、中国の塗料・コーティング産業は過去30年間、数量成長率で世界のその他の地域を上回ってきました。この間の急速な都市化は、建設活動の増加により、国内の建築塗料セクターを新たな高みへと押し上げました。

- 中国国家統計局によると、中国の建設生産高は2022年にピークを迎え、その額は約31兆2,000億人民元(~4兆6,100億米ドル)に達します。その結果、こうした要因が市場の需要を増加させる傾向にあります。

- さらに、ドイツは欧州最大の建設産業を抱えています。同国の建設業界は緩やかな成長を続けており、その主な要因は新設住宅建設件数の増加です。同国には欧州大陸最大の建築ストックがあり、当面はこの傾向が続くと予想されます。ドイツは、持続可能なエネルギーシステムへの移行を進める一環として、2050年までにほぼ気候変動に左右されない建築ストックを持つことを目指しています。

- 上記のような要因から、同市場は予測期間中に急成長すると予想されます。

市場を独占するアジア太平洋地域

- アジア太平洋地域は、中国、インド、日本などの国々からの需要の増加により、予測期間中にフッ素系界面活性剤市場を独占すると予想されます。

- フッ素系界面活性剤は、塗料やコーティング産業で広く使用されています。アジア太平洋地域の建築・建設における塗料・コーティング需要の増加が市場を牽引すると予想されます。

- 中国は、eコマースやオフィススペースの需要増加などにより、広大な建設部門を擁しています。このため、中国では商業建設が増加しています。例えば、中国はショッピングセンター建設に関する主要国のひとつです。中国には約4,000のショッピングセンターがあり、2025年までにさらに7,000がオープンすると推定されています。これにより、予測期間中の市場成長を支えています。

- さらに、インドは商業セクターを拡大しています。同国では複数のプロジェクトが進行しています。例えば、2022年第1四半期に9億米ドル相当のCommerzIII商業オフィス複合施設の建設が開始されました。このプロジェクトでは、ムンバイのゴレガオンに、許容床面積2,60,128平方メートルの43階建ての商業オフィス複合施設を建設します。このプロジェクトは2027年第4四半期に完成する予定で、予測期間中の市場成長に寄与します。

- 塗料・コーティング以外にも、フッ素系界面活性剤は石油・ガス分野で広く使用されています。石油天然ガス省(インド)によると、同国の石油製品の生産量は2022年に2億5,430万トンを超え、2021年の2億3,350万トンと比べて8%以上増加しました。このことは、市場の成長を支えることになると思われます。

- 上記のすべての要因が、予測期間中のアジア太平洋地域のフッ素系界面活性剤市場の成長を促進すると思われます。

フッ素系界面活性剤産業の概要

フッ素系界面活性剤市場は、その性質上、部分的に断片化されています。調査対象市場の主要企業(順不同)には、3M、Innovative Chemical Technologies、DIC CORPORATION、The Chemours Company、Alfa Chemicalsなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 塗料・コーティング業界からの需要の高まり

- 油田におけるフッ素系界面活性剤の用途拡大

- その他の促進要因

- 抑制要因

- 他の界面活性剤に比べて高価格

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模)

- タイプ

- アニオン

- カチオン

- 非イオン

- 両性

- 用途

- 塗料・コーティング剤

- 洗剤・洗浄剤

- 石油・ガス

- 難燃剤

- 接着剤

- その他の用途(自動車、エレクトロニクスなど)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Alfa Chemicals

- CYTONIX

- DIC CORPORATION

- DYNAX

- Innovative Chemical Technologies

- MAFLON S.p.A.

- Merck KGaA

- TCI EUROPE N.V.

- The Chemours Company

第7章 市場機会と今後の動向

- エレクトロニクス分野におけるフッ素系界面活性剤の使用増加

- その他の機会

The Fluorosurfactant Market size is estimated at USD 704.12 million in 2024, and is expected to reach USD 912.43 million by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The fluorosurfactant market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as paints and coatings, detergents, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The fluorosurfactant market is expected to grow during the forecast period owing to the increasing demand from the paints and coatings industry.

On the flip side, higher price when compared to hydrocarbon and silicone-based surfactants, is hindering the market growth.

Further, the use of fluorosurfactants in electronic coatings, owing to their high stability to aggressive chemicals, high dielectric strength, etc., is predicted to generate a market opportunity during the forecast period.

Asia-Pacific region dominates the market across the globe, with the largest consumption from countries such as China, India, and Japan.

Fluorosurfactant Market Trends

Growing Demand from the Paints and Coatings Industry

- Fluorosurfactants are amphiphilic molecules that have hydrophobic and hydrophilic parts. The hydrophobic tail is a fluorocarbon, and the hydrophilic part is characterized based on charge.

- Surfactants, often called surface-active agents, lower the surface tension between a liquid and a gas, or between a liquid and a solid, or between two immiscible phases. This lowers the surface tension of a coating, thus offering a smoother and excellent finish.

- Fluorosurfactant improves pigment and substrate wetting and leveling characteristics and provides high open time. Because of the high electronegativity of fluorine and the highly stable bond between fluorine and carbon atoms, fluorosurfactants are more stable, suitable for various conditions, and are more favored than other surfactants.

- In the United States, according to the US Census Bureau, the value of private construction in 2022 stood at USD 1,434.2 billion, 11.7% higher than USD 1,279.5 billion in 2021. Residential construction spending in 2022 was USD 899.1 billion, up 13.3% from USD 793.7 billion in 2021. Thus, the growing construction activities are anticipated to fuel the market growth.

- Further, China's paints and coating industry has outperformed the rest of the world in terms of volume growth over the last 30 years. Rapid urbanization during this time has boosted the domestic architectural coating sector to new heights owing to increasing construction activities.

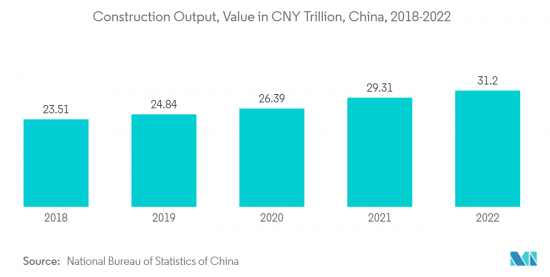

- According to the National Bureau of Statistics of China, China's construction output peaked in 2022 at a value of about CNY 31.20 (~USD 4.61 trillion). As a result, these factors tend to increase the market demand.

- Moreover, Germany has the largest construction industry in Europe. The country's construction industry has been growing slowly, which is majorly driven by the increasing number of new residential construction activities. The country is home to the continent's largest building stock and is expected to continue in the foreseeable future. Germany aims to have an almost climate-neutral building stock by 2050 as part of its ongoing transition to a sustainable energy system.

- Owing to all the factors mentioned above, its market is expected to grow rapidly over the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for fluorosurfactants during the forecast period due to an increase in demand from countries like China, India, and Japan.

- Fluorosurfactants are widely used in the paints and coatings industry. The increase in demand for paints and coatings in building and construction in the Asia-Pacific region is expected to drive the market.

- China hosts a vast construction sector owing to the rising demand from e-commerce, office space requirements, etc. This has resulted in increased commercial construction in China. For example, China is one of the leading countries concerning the construction of shopping centers. China has almost 4,000 shopping centers, while 7,000 more are estimated to be open by 2025. Thereby supporting the market growth during the forecast period.

- Furthermore, India is expanding its commercial sector. Several projects have been going on in the country. For instance, the CommerzIII Commercial Office Complex construction worth USD 900 million started in Q1 2022. The project involves the construction of a 43-story commercial office complex with a permissible floor area of 2,60,128 square meters in Goregaon, Mumbai. The project is expected to be completed in Q4 2027, thus benefitting the market growth during the forecast period.

- Apart from paints and coatings, fluorosurfactants are widely used in the oil and gas sector. According to the Ministry of Petroleum and Natural Gas (India), the production volume of petroleum products in the country was more than 254.3 million metric tons in 2022, reflecting an increase of more than 8% compared to 233.5 million metric tons in 2021. This, in turn, is likely to support the market growth.

- All the factors mentioned above are likely to fuel the growth of the Asia-Pacific fluorosurfactants market over the forecast period.

Fluorosurfactant Industry Overview

The fluorosurfactant market is partially fragmented in nature. The major players in the studied market (not in any particular order) include 3M, Innovative Chemical Technologies, DIC CORPORATION, The Chemours Company, and Alfa Chemicals, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand From the Paints and Coatings Industry

- 4.1.2 Increasing Application of Flurosurfactants in Oil Field

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Higher Price Compared to Other Surfactants

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Anionic

- 5.1.2 Cationic

- 5.1.3 Non-ionic

- 5.1.4 Amphoteric

- 5.2 Application

- 5.2.1 Paints and Coatings

- 5.2.2 Detergents and Cleaning Agents

- 5.2.3 Oil and Gas

- 5.2.4 Flame Retardants

- 5.2.5 Adhesives

- 5.2.6 Other Applications (Automotive, Electronics, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Alfa Chemicals

- 6.4.3 CYTONIX

- 6.4.4 DIC CORPORATION

- 6.4.5 DYNAX

- 6.4.6 Innovative Chemical Technologies

- 6.4.7 MAFLON S.p.A.

- 6.4.8 Merck KGaA

- 6.4.9 TCI EUROPE N.V.

- 6.4.10 The Chemours Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Use of Fluorosurfactants in Electronics Sector

- 7.2 Other Opportunities