|

市場調査レポート

商品コード

1435215

工業用塩:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Industrial Salts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 工業用塩:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

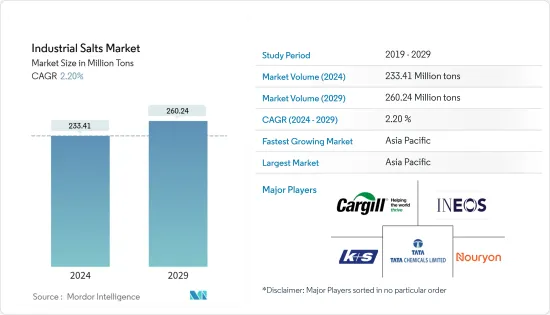

工業用塩の市場規模は、2024年に2億3,341万トンと推定され、2029年までに2億6,024万トンに達すると予測されており、予測期間(2024年から2029年)中に2.20%のCAGRで成長すると予想されます。

2020年の市場は、新型コロナウイルス感染症(COVID-19)によって悪影響を受けました。工業用塩は、塩素や苛性ソーダなどの化学物質の製造に使用されます。パンデミックのシナリオにより、政府が課したロックダウン中、化学製造部門は一時的に停止し、その結果、化学処理に必要な原材料の需要の減少につながりました。さらに、工業用塩は製紙の際にも消費されます。欧州製紙産業連盟(CEPA)によると、Cepi加盟国の紙と板紙の生産量は2020年に前年比5%減少しました。これは主に新型コロナウイルス感染症(COVID-19)のパンデミックによる世界の需要の影響を受け、マイナスになったことによる。調査対象市場の需要に影響を与えます。しかし、個人の衛生と清潔な環境を考慮して、生産時に工業用塩を原料として使用する石鹸や洗剤の使用量が大幅に増加しており、それが工業用塩市場の需要を刺激しています。

主なハイライト

- 短期的には、化学処理および水処理用途のための工業用塩の需要の増加が市場の成長を促進すると予想されます。

- その一方で、環境保護庁(EPA)によって課された厳しい規制が市場の成長を妨げると予想されます。

- 用途別では、ソーダ灰、苛性ソーダ、塩素の製造での使用量が増加しているため、化学処理セグメントが市場を独占すると予想されています。

- アジア太平洋地域は世界中の市場を独占しており、中国やインドなどの国々からの消費が最大となっています。

工業用塩市場動向

化学品処理用途の需要増加

- 工業用塩は、従来の採掘、天日蒸発、真空蒸発により岩塩または天然塩水から製造されます。

- 化学処理用途は、工業用塩の総需要の50%以上を占めています。工業用塩は、大量に入手可能で費用対効果が高いため、塩素、ソーダ灰、苛性ソーダの製造に広く使用されています。

- 費用対効果の高い代替品が存在しないため、工業用塩は二塩化エチレンなどの製品を製造する塩素アルカリプロセスで積極的に使用されており、工業用塩の需要が刺激されています。

- 米国化学評議会によると、米国の化学産業の年間生産成長率は、2021年に前年比約12.3%増加する可能性があります。化学設備投資の総額は、2021年までに前年比15.7%の成長率で335億米ドルに増加すると見込まれており、これにより工業用塩の市場需要が刺激されることが予想されます。

- 工業用塩は、ポリ塩化ビニル、石鹸、洗剤、除草剤、殺虫剤などのプラスチックの製造に使用されます。また、二酸化チタンなどの無機化学物質の製造にも使用され、工業用塩市場の成長を促進します。

- ランドリーケア部門も、洗剤、石鹸、その他のランドリーケア製品の製造のために工業用塩を消費します。米国のランドリーケア市場は2019年に約128億米ドルと評価され、2020年には約131億米ドルに達し、成長率は約2%で、調査対象市場の需要を刺激しました。

- したがって、前述の要因は今後数年間で市場に大きな影響を与えると予想されます。

アジア太平洋地域が市場を独占

- アジア太平洋地域は、この地域での工業化の進展により、予測期間中に工業用塩の市場を独占すると予想されます。中国、インド、日本などの国々では、化学加工産業での工業用塩の使用により、工業用塩の需要が増加しています。

- 2019年の日本の化学産業の規模は約2,000億米ドルで、前年比約2.5%の成長率であり、これが工業用塩の市場需要を刺激しています。

- 工業用塩は、豪雪国の道路を除雪するための除氷に広く使用されています。工業用塩の除氷特性は、氷の再形成を一定期間遅らせるのにも役立ちます。

- 水処理プラントでは、水の軟化と浄化のプロセスに工業用塩が使用されます。インドや中国などの国では、多くの水処理プロジェクトが建設されており、予測期間中に工業用塩の成長を促進する可能性があります。

- プラスチック部門では、工業用塩を使用してポリ塩化ビニル(PVC)を製造しています。PVCは、建設業界で配管、PVCボードなどのさまざまな用途に広く使用されています。中国は2019年の市場規模が1兆929億米ドルで建設業界をリードし、前年比14.71%の成長率を記録しました。

- また、国内の新築総戸数は2019年に約1億2,755万平方メートル、2020年には約1億1,374万平方メートルに達し、減少率は約10.5%となった。これにより、PVC製建材の消費量が減少し、工業用塩市場の需要が刺激されました。

- アジア太平洋地域で事業を展開している主要企業には、カーギル社、K+S Aktiengesellschaft、Tata Chemicals Ltdなどがあります。

- したがって、前述の要因は今後数年間で市場に大きな影響を与えると予想されます。

工業用塩業界の概要

工業用塩市場は細分化されており、上位5社が市場のわずかなシェアを占めています。市場の主要企業には、Cargill Incorporated、K+S Aktiengesellschaft、Tata Chemicals Ltd、INEOS、およびNouryonなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 化学処理における需要の増加

- 水処理分野での需要拡大

- 抑制要因

- 厳しい政府規制

- COVID-19の影響による不利な状況

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 由来

- 岩塩

- 天然塩水

- 製造プロセス

- 天日乾燥

- 真空蒸発

- 従来型採掘

- 用途

- 化学処理

- 水処理

- 除氷

- 農業

- 食品加工

- 石油・ガス

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Archean Group

- Cargill Incorporated

- Compass Minerals

- Delmon Group of Companies

- Dominion Salt Limited

- Donald Brown Group

- Exportadora de Sal de CV

- INEOS

- K+S Aktiengesellschaft

- MITSUI & CO. LTD

- Morton Salt Inc.

- Nouryon

- Rio Tinto

- Salins IAA

- Tata Chemicals Ltd

第7章 市場機会と今後の動向

The Industrial Salts Market size is estimated at 233.41 Million tons in 2024, and is expected to reach 260.24 Million tons by 2029, growing at a CAGR of 2.20% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. Industrial salts are used to produce chemicals like chlorine and caustic soda. Owing to the pandemic scenario, the chemical manufacturing units were on a temporary halt during the government-imposed lockdown, thus leading to a decrease in the demand for raw material needed in chemical processing. Furthermore, industrial salts are also consumed in paper manufacturing. According to the CONFEDERATION OF EUROPEAN PAPER INDUSTRIES (CEPA), the paper and board production by Cepi member countries decreased by 5% in 2020 compared to the previous year, mainly due to global demand impacted by the COVID-19 pandemic, which in turn negatively impacts the demand for the studied market. However, the usage of soaps and detergents that use industrial salts as a raw material during production has significantly increased during this situation, considering the personal hygiene and clean surrounding, which in turn stimulates the demand for the industrial salts market.

Key Highlights

- Over the short term, the increasing demand for industrial salts for chemical processing and water treatment applications is expected to drive the market's growth.

- On the flip side, strict regulations imposed by the environmental protection agency (EPA) are expected to hinder the growth of the market.

- By application, the chemical processing segment is expected to dominate the market, owing to the increasing usage in manufacturing soda ash, caustic soda, and chlorine.

- The Asia-Pacific region dominated the market across the world, with the largest consumption from countries such as China and India.

Industrial Salts Market Trends

Increasing Demand from Chemicals Processing Application

- Industrial salts are manufactured from rock salt or natural brine by conventional mining, solar evaporation, and vacuum evaporation.

- Chemical processing applications account for over 50% of the total industrial salts demand. Industrial salts are widely used for manufacturing chlorine, soda ash, and caustic soda, owing to their availability in large quantities and cost-effectiveness.

- Due to the lack of cost-effective substitutes, industrial salts are actively used in the chloralkali process to manufacture products such as ethylene dichloride, which is stimulating the demand for industrial salts.

- According to the American Chemistry Council, the annual production growth of the chemical industry in the United States is likely to rise by about 12.3% in 2021 compared to the previous year. The total chemical capital expenditure is likely to rise to USD 33.5 billion by 2021, with a growth rate of 15.7% compared to the previous year, which in turn is expected to stimulate the market demand for industrial salts.

- Industrial salts are used in the production of plastics, including polyvinyl chloride, soaps, detergents, herbicides, and pesticides. It is also used in the production of inorganic chemicals like titanium dioxide, enhancing the growth of the industrial salts market.

- The laundry care segment also consumes industrial salts for manufacturing detergents, soaps, and other laundry care products. The US laundry care market was valued at about USD 12.8 billion in 2019 and reached about USD 13.1 billion in 2020, with a growth rate of about 2%, stimulating the demand for the studied market.

- Therefore, the aforementioned factors are expected to significantly impact the market in the coming years.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for industrial salts during the forecast period, owing to the growing industrialization in the region. In countries like China, India, and Japan, due to the usage of industrial salts in the chemicals processing industry, the demand for industrial salts has been increasing.

- The Japanese chemical industry was valued at about USD 200 billion in 2019, with a growth rate of about 2.5% compared to the previous year, which in turn stimulates the market demand for industrial salts.

- Industrial salts are widely used for de-icing for clearing roadways in countries with heavy snowfall. De-icing property of industrial salts also helps to delay the reformation of ice for a certain period of time.

- In water treatment plants, industrial salts are used for the water softening and purification process. In countries like India and China, many water treatment projects are being constructed, which is likely to help stimulate the growth of industrial salts over the forecast period.

- The plastic segment uses industrial salts to produce polyvinyl chloride (PVC), which are widely used in the construction industry for different applications, including piping, PVC boards, and others. China was leading the construction industry with market size of USD 1,092.9 billion in 2019, registering a growth rate of 14.71% compared to the previous year.

- Furthermore, the total new construction in Japan accounted for about 127.55 million sq. m in 2019 and reached about 113.74 million sq. m in 2020, with a decline rate of about 10.5%. This led to a decrease in consumption of PVC-made construction materials, in turn stimulating the demand for the industrial salts market.

- Some major companies operating in the Asia-Pacific region include Cargill Incorporated, K+S Aktiengesellschaft, and Tata Chemicals Ltd.

- Therefore, the aforementioned factors are expected to significantly impact the market in the coming years.

Industrial Salts Industry Overview

The industrial salts market is fragmented, with the top five players accounting for a marginal share of the market. Some key players in the market include Cargill Incorporated, K+S Aktiengesellschaft, Tata Chemicals Ltd, INEOS, and Nouryon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand in Chemical Processing

- 4.1.2 Growing Demand from Water Treatment

- 4.2 Restraints

- 4.2.1 Stringent Government Regulations

- 4.2.2 Unfavorable Conditions Arising due to the Impact of COVID-19

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Source

- 5.1.1 Rock Salt

- 5.1.2 Natural Brine

- 5.2 Manufacturing Process

- 5.2.1 Solar Evaporation

- 5.2.2 Vacuum Evaporation

- 5.2.3 Conventional Mining

- 5.3 Application

- 5.3.1 Chemical Processing

- 5.3.2 Water Treatment

- 5.3.3 De-icing

- 5.3.4 Agriculture

- 5.3.5 Food Processing

- 5.3.6 Oil and Gas

- 5.3.7 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Archean Group

- 6.4.2 Cargill Incorporated

- 6.4.3 Compass Minerals

- 6.4.4 Delmon Group of Companies

- 6.4.5 Dominion Salt Limited

- 6.4.6 Donald Brown Group

- 6.4.7 Exportadora de Sal de CV

- 6.4.8 INEOS

- 6.4.9 K+S Aktiengesellschaft

- 6.4.10 MITSUI & CO. LTD

- 6.4.11 Morton Salt Inc.

- 6.4.12 Nouryon

- 6.4.13 Rio Tinto

- 6.4.14 Salins IAA

- 6.4.15 Tata Chemicals Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements to Produce High Purity Salts

- 7.2 Other Opportunities