|

|

市場調査レポート

商品コード

1660557

ポリマー積層造形の世界市場:市場規模、シェア、予測、動向分析:オファリング別、技術別、エンドユーザー別、地域別-2031年までの予測Polymer Additive Manufacturing Market Size, Share, Forecast, & Trends Analysis by Offering, Technology, End User - Global Forecast to 2031 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ポリマー積層造形の世界市場:市場規模、シェア、予測、動向分析:オファリング別、技術別、エンドユーザー別、地域別-2031年までの予測 |

|

出版日: 2025年01月22日

発行: Meticulous Research

ページ情報: 英文 199 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界のポリマー積層造形の市場規模は、2023年に119億5,000万米ドルとなりました。同市場は、2024年の135億5,000万米ドルから2031年には361億9,000万米ドルに達すると予測され、2024年から2031年までの予測期間中のCAGRは15.1%となる見込みです。

同市場の成長は、コスト効率と材料廃棄物の削減、カスタマイズと設計の柔軟性、リードタイムの短縮、人件費の削減、持続可能性と環境への影響など、ポリマー積層造形が提供する特典によってもたらされます。さらに、カスタマイズとパーソナライゼーション、サプライチェーンの弾力性とオンデマンド生産、材料廃棄物の削減とコスト効率、バイオプリンティングとヘルスケアにおける進歩、コラボレーションと業界パートナーシップは、市場成長の機会を生み出すと期待されています。

タイプ別では、2024年にサービス分野がポリマー積層造形市場で最大のシェアを占めました。このセグメントの市場シェアが大きいのは、主に航空宇宙、ヘルスケア、自動車などの産業で専門的でカスタマイズされた製品が必要とされていることと、多額の設備投資をせずに生産をアウトソーシングできることによるものです。

技術別では、2024年に溶融積層造形(FDM)分野がポリマー積層造形市場で最大のシェアを占めました。このセグメントの市場シェアが大きいのは、主に低コスト、使いやすさ、汎用性によるもので、新興企業、中小企業、教育に最適です。ラピッドプロトタイピング、機能テスト、少量生産での利用が広がっていることが、このセグメントの大きなシェアをさらに支えています。

エンドユーザー別では、2024年に消費者製品分野がポリマー積層造形市場で最大のシェアを占めました。このセグメントの大幅な市場シェアは主に、パーソナライゼーション、ラピッドプロトタイピング、少量生産、オンデマンド生産、カスタマイズされた少量生産の高品質アイテムのための高性能で持続可能な材料の革新に対する需要の高まりによるものです。

当レポートでは、世界のポリマー積層造形市場について調査し、市場の現状とともに、オファリング別、技術別、エンドユーザー別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の洞察

- 概要

- 市場の成長に影響を与える要因

- 促進要因

- 抑制要因

- 機会

- 主な動向

第5章 ポリマー積層造形市場の評価、オファリング別

- 概要

- サービス

- ハードウェア

- ソフトウェア

- 材料

第6章 ポリマー積層造形市場の評価、技術別

- 概要

- 熱溶解積層法(FDM)

- 選択的レーザー焼結(SLS)

- ステレオリソグラフィー(SLA)

- ポリジェット

- デジタル光処理(DLP)

- マルチジェットフュージョン

- バインダージェッティング

- その他

第7章 ポリマー積層造形市場の評価、エンドユーザー別

- 概要

- 消費財

- ヘルスケア

- 自動車

- 一般製造業

- エレクトロニクス・半導体

- 航空宇宙・防衛

- 化学品・材料

- エネルギー・石油・ガス

- その他

第8章 ポリマー積層造形市場の評価、地域別

- 概要

- 北米

- 米国

- カナダ

- アジア太平洋

- 中国

- 日本

- インド

- その他

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他

- 中東・アフリカ

- ラテンアメリカ

第9章 競合分析

- 概要

- 主な成長戦略

- 競合ベンチマーキング

- 競合ダッシュボード

第10章 企業プロファイル(事業概要、財務概要、製品ポートフォリオ、戦略開発、SWOT分析)

- Stratasys, Ltd.

- 3D Systems Corporation

- EOS GmbH

- Materialise NV

- voxeljet AG

- Markforged Holding Corporation

- Proto Labs, Inc.

- Autodesk, Inc.

- 3Dceram

- Dassault Systemes SE

- Formlabs Inc.

- Shapeways Holdings, Inc.

第11章 付録

LIST OF TABLES

- Table 1 Global Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 2 Global Polymer Additive Manufacturing Services Market, by Country/Region, 2022-2031 (USD Million)

- Table 3 Global Polymer Additive Manufacturing Hardware Market, by Country/Region, 2022-2031 (USD Million)

- Table 4 Global Polymer Additive Manufacturing Software Market, by Country/Region, 2022-2031 (USD Million)

- Table 5 Global Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 6 Global Polymer Additive Manufacturing Materials Market, by Country/Region, 2022-2031 (USD Million)

- Table 7 Global Photopolymers (Resins)-Based Polymer Additive Manufacturing Market, by Country/Region, 2022-2031 (USD Million)

- Table 8 Global Polylactic Acid (PLA)- Based Polymer Additive Manufacturing Market, by Country/Region, 2022-2031 (USD Million)

- Table 9 Global Polyamide (Nylon)- Based Polymer Additive Manufacturing Market, by Country/Region, 2022-2031 (USD Million)

- Table 10 Global Acrylonitrile Butadiene Styrene (ABS)- Based Polymer Additive Manufacturing Market, by Country/Region, 2022-2031 (USD Million)

- Table 11 Global Polycarbonate (PC)- Based Polymer Additive Manufacturing Market, by Country/Region, 2022-2031 (USD Million)

- Table 12 Global Thermoplastic Polyurethane (TPU)- Based Polymer Additive Manufacturing Market, by Country/Region, 2022-2031 (USD Million)

- Table 13 Global Other Polymer Additive Manufacturing Materials Market, by Country/Region, 2022-2031 (USD Million)

- Table 14 Global Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 15 Global Polymer Additive Manufacturing Market for Fused Deposition Modeling (FDM), by Country/Region, 2022-2031 (USD Million)

- Table 16 Global Polymer Additive Manufacturing Market for Selective Laser Sintering (SLS), by Country/Region, 2022-2031 (USD Million)

- Table 17 Global Polymer Additive Manufacturing Market for Stereolithography (SLA), by Country/Region, 2022-2031 (USD Million)

- Table 18 Global Polymer Additive Manufacturing Market for Polyjet, by Country/Region, 2022-2031 (USD Million)

- Table 19 Global Polymer Additive Manufacturing Market for Digital Light Processing (DLP), by Country/Region, 2022-2031 (USD Million)

- Table 20 Global Polymer Additive Manufacturing Market for Multi Jet Fusion (MJF), by Country/Region, 2022-2031 (USD Million)

- Table 21 Global Polymer Additive Manufacturing Market for Binder Jetting, by Country/Region, 2022-2031 (USD Million)

- Table 22 Global Polymer Additive Manufacturing Market for Other Polymer Technologies, by Country/Region, 2022-2031 (USD Million)

- Table 23 Global Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 24 Global Polymer Additive Manufacturing Market for Consumer Products, by Country/Region, 2022-2031 (USD Million)

- Table 25 Global Polymer Additive Manufacturing Market for Healthcare, by Country/Region, 2022-2031 (USD Million)

- Table 26 Global Polymer Additive Manufacturing Market for Automotive, by Country/Region, 2022-2031 (USD Million)

- Table 27 Global Polymer Additive Manufacturing Market for General Manufacturing, by Country/Region, 2022-2031 (USD Million)

- Table 28 Global Polymer Additive Manufacturing Market for Electronics & Semiconductors, by Country/Region, 2022-2031 (USD Million)

- Table 29 Global Polymer Additive Manufacturing Market for Aerospace & Defense, by Country/Region, 2022-2031 (USD Million)

- Table 30 Global Polymer Additive Manufacturing Market for Chemicals & Materials, by Country/Region, 2022-2031 (USD Million)

- Table 31 Global Polymer Additive Manufacturing Market for Energy and Oil & Gas, by Country/Region, 2022-2031 (USD Million)

- Table 32 Global Polymer Additive Manufacturing Market for Other End Users, by Country/Region, 2022-2031 (USD Million)

- Table 33 Global Polymer Additive Manufacturing Market, by Region, 2022-2031 (USD Million)

- Table 34 North America: Polymer Additive Manufacturing Market, by Country, 2022-2031 (USD Million)

- Table 35 North America: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 36 North America: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 37 North America: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 38 North America: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 39 U.S.: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 40 U.S.: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 41 U.S.: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 42 U.S.: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 43 Canada: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 44 Canada: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 45 Canada: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 46 Canada: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 47 Asia-Pacific: Polymer Additive Manufacturing Market, by Country/ Region, 2022-2031 (USD Million)

- Table 48 Asia-Pacific: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 49 Asia-Pacific: Polymer Additive Manufacturing Materials Market, by Type,2022-2031 (USD Million)

- Table 50 Asia-Pacific: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 51 Asia-Pacific: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 52 China: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 53 China: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 54 China: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 55 China: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 56 Japan: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 57 Japan: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 58 Japan: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 59 Japan: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 60 India: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 61 India: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 62 India: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 63 India: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 64 Rest of Asia-Pacific: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 65 Rest of Asia-Pacific: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 66 Rest of Asia-Pacific: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 67 Rest of Asia-Pacific: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 68 Europe: Polymer Additive Manufacturing Market, by Country/Region, 2022-2031 (USD Million)

- Table 69 Europe: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 70 Europe: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 71 Europe: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 72 Europe: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 73 Germany: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 74 Germany: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 75 Germany: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 76 Germany: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 77 U.K.: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 78 U.K.: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 79 U.K.: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 80 U.K.: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 81 France: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 82 France: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 83 France: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 84 France: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 85 Italy: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 86 Italy: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 87 Italy: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 88 Italy: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 89 Spain: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 90 Spain: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 91 Spain: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 92 Spain: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 93 Rest of Europe: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 94 Rest of Europe: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 95 Rest of Europe: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 96 Rest of Europe: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 97 Middle East & Africa: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 98 Middle East & Africa: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 99 Middle East & Africa: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 100 Middle East & Africa: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

- Table 101 Latin America: Polymer Additive Manufacturing Market, by offering, 2022-2031 (USD Million)

- Table 102 Latin America: Polymer Additive Manufacturing Materials Market, by Type, 2022-2031 (USD Million)

- Table 103 Latin America: Polymer Additive Manufacturing Market, by Technology, 2022-2031 (USD Million)

- Table 104 Latin America: Polymer Additive Manufacturing Market, by End User, 2022-2031 (USD Million)

LIST OF FIGURES

- Figure 1 Research Process

- Figure 2 Secondary Sources Referenced for This Study

- Figure 3 Primary Research Techniques

- Figure 4 Key Executives Interviewed

- Figure 5 Breakdown of Primary Interviews (Supply-Side & Demand-Side)

- Figure 6 Market Sizing and Growth Forecast Approach

- Figure 7 In 2024, the Services Segment is Expected to Dominate the Market

- Figure 8 In 2024, the Fused Deposition Modeling Segment is Expected to Dominate the Market

- Figure 9 In 2024, the Consumer Products Segment is Expected to Dominate the Market

- Figure 10 North America Dominates the Overall Polymer Additive Manufacturing Market

- Figure 11 Impact Analysis of Market Dynamics

- Figure 12 Global Polymer Additive Manufacturing Market, by Offering, 2024 Vs. 2031 (USD Million)

- Figure 13 Global Polymer Additive Manufacturing Market, by Technology, 2024 Vs. 2031 (USD Million)

- Figure 14 Global Polymer Additive Manufacturing Market, by End User, 2024 Vs. 2031 (USD Million)

- Figure 15 Global Polymer Additive Manufacturing Market, by Region, 2024 Vs. 2031 (USD Million)

- Figure 16 North America: Polymer Additive Manufacturing Market Snapshot

- Figure 17 Asia-Pacific: Polymer Additive Manufacturing Market Snapshot

- Figure 18 Europe: Polymer Additive Manufacturing Market Snapshot

- Figure 19 Middle East & Africa: Polymer Additive Manufacturing Market Snapshot

- Figure 20 Latin America: Polymer Additive Manufacturing Market Snapshot

- Figure 21 Key Growth Strategies Adopted by Leading Players, 2021-2024

- Figure 22 Polymer Additive Manufacturing Market: Competitive Benchmarking, by Offering

- Figure 23 Polymer Additive Manufacturing Market: Competitive Benchmarking, by Geography

- Figure 24 Competitive Dashboard: Polymer Additive Manufacturing Market

- Figure 25 Stratasys, Ltd.: Financial Snapshot (2023)

- Figure 26 3D Systems Corporation: Financial Overview (2023)

- Figure 27 Materialise NV: Financial Snapshot (2023)

- Figure 28 voxeljet AG: Financial Snapshot (2022)

- Figure 29 Markforged Holding Corporation: Financial Snapshot (2023)

- Figure 30 Proto Labs, Inc.: Financial Snapshot (2023)

- Figure 31 Autodesk, Inc.: Financial Snapshot (2024)

- Figure 32 Dassault Systemes SE: Financial Overview (2023)

Polymer Additive Manufacturing Market Size, Share, Forecast, & Trends Analysis by Offering (Hardware, Materials, Services), Technology (FDM, SLA, SLS, Polyjet, Binder Jetting), End User (Consumer, Electronics, Healthcare, Automotive, Aerospace & Defense)-Global Forecast to 2031

The Polymer Additive Manufacturing Market was valued at $11.95 billion in 2023. This market is expected to reach $36.19 billion by 2031 from an estimated $13.55 billion in 2024, at a CAGR of 15.1% during the forecast period from 2024 to 2031.

Succeeding extensive secondary and primary research and in-depth analysis of the market scenario, the report comprises the analysis of key industry drivers, restraints, challenges, and opportunities. The growth of this market is driven by the benefits offered by polymer additive manufacturing such as cost efficiency and reduction in material waste; customization and design flexibility; reduction in lead time; lower labor costs; and sustainability and environmental impact. Moreover, customization and personalization; supply chain resilience and on-demand production; reduced material waste and cost-efficiency; advancements in bioprinting and healthcare; and collaborations and industry partnerships are expected to create market growth opportunities,

The polymer additive manufacturing market is characterized by a moderately competitive scenario due to the presence of many large and small-sized global, regional, and local players. The key players operating in the polymer additive manufacturing market are Stratasys, Ltd. (U.S.), 3D Systems Corporation (U.S.), EOS GmbH (Germany), Materialise NV (Belgium), voxeljet AG (Germany), Markforged Holding Corporation (U.S.), Proto Labs, Inc. (U.S.), Autodesk, Inc. (U.S.), 3Dceram (France), Dassault Systemes SE (France), Formlabs Inc. (U.S.), and Shapeways Holdings, Inc. (U.S.).

The polymer additive manufacturing market is segmented based on offering, technology, and end user. The report also evaluates industry competitors and analyzes the polymer additive manufacturing market at the regional and country levels.

By type, in 2024, the services segment accounted for the largest share of the polymer additive manufacturing market. The substantial market share of this segment is primarily due to the need for specialized, customized products in industries like aerospace, healthcare, and automotive, along with the ability to outsource production without significant capital investment.

By technology, in 2024, the fused deposition modeling (FDM) segment accounted for the largest share of the polymer additive manufacturing market. The large market share of this segment is primarily due to its low cost, ease of use, and versatility, making it ideal for startups, small businesses, and education. Its widespread use in rapid prototyping, functional testing, and low-volume production is further supporting the large share of this segment

By end user, in 2024, the consumer products segment accounted for the largest share of the polymer additive manufacturing market. The substantial market share of this segment is primarily due to the growing demand for personalization, rapid prototyping, small-batch and on-demand production, and innovations in high-performance and sustainable materials for customized, low-volume, high-quality items.

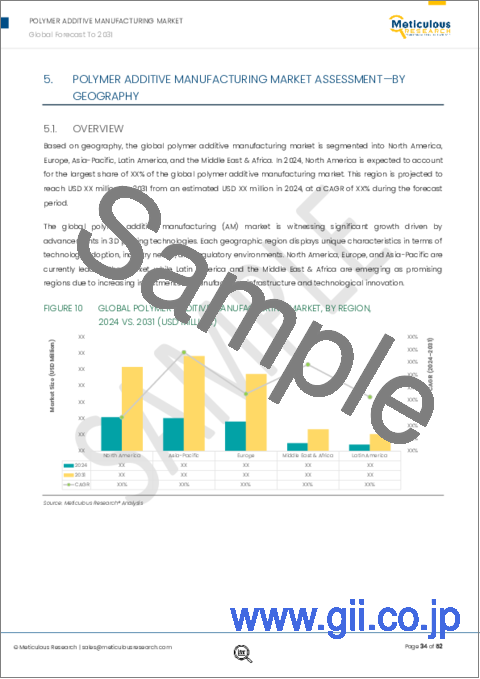

This research report analyzes major geographies and provides a comprehensive analysis of North America (U.S., Canada), Asia-Pacific (China, Japan, India, and Rest of Asia-Pacific), Europe (Germany, U.K., France, Italy, Spain, and Rest of Europe), the Middle East & Africa, and Latin America.

By geography, North America holds the largest share in the polymer additive manufacturing market, driven by strong industrial adoption, technological innovation, and a well-established manufacturing ecosystem. The region is home to key players in the additive manufacturing industry, including manufacturers of advanced 3D printers, materials, and software solutions. This concentration of expertise facilitates rapid technological advancements and widespread adoption across industries, particularly in automotive, aerospace, and healthcare.

Key Questions Answered in the Report-

- What is the value of revenue generated by the sale of polymer additive manufacturing related products and services?

- At what rate is the global demand for polymer additive manufacturing products and services projected to grow for the next five to seven years?

- What is the historical market size and growth rate for the polymer additive manufacturing market?

- What are the major factors impacting the growth of this market at global and regional levels?

- What are the major opportunities for existing players and new entrants in the market?

- Which product offering, technology, and end user segments create major traction for the manufacturers in this market?

- What are the key geographical trends in this market? Which regions/countries are expected to offer significant growth opportunities for the manufacturers operating in the polymer additive manufacturing market?

- Who are the major players in the polymer additive manufacturing market? What are their specific product offerings in this market?

- What recent developments have taken place in the polymer additive manufacturing market? What impact have these strategic developments created on the market?

TABLE OF CONTENTS

1. Introduction

- 1.1. Market Definition & Scope

- 1.2. Market Ecosystem

- 1.3. Currency & Limitations

- 1.4. Key Stakeholders

2. Research Methodology

- 2.1. Research Approach

- 2.2. Process of Data Collection and Validation

- 2.2.1. Secondary Research

- 2.2.2. Primary Research/Interviews with Key Opinion Leaders of the Industry

- 2.3. Market Sizing and forecasting

- 2.3.1. Market Size Estimation Approach

- 2.3.2. Growth forecast Approach

- 2.3.3. Market Share Analysis

- 2.4. Assumptions for the Study

3. Executive Summary

- 3.1. Overview

- 3.2. Segment Analysis

- 3.2.1. Polymer Additive Manufacturing Market, by offering

- 3.2.2. Polymer Additive Manufacturing Market, by Technology

- 3.2.3. Polymer Additive Manufacturing Market, by End User

- 3.3. Polymer Additive Manufacturing Market-Regional Analysis

- 3.4. Competitive Landscape & Market Competitors

4. Market Insights

- 4.1. Overview

- 4.2. Factors Affecting Market Growth

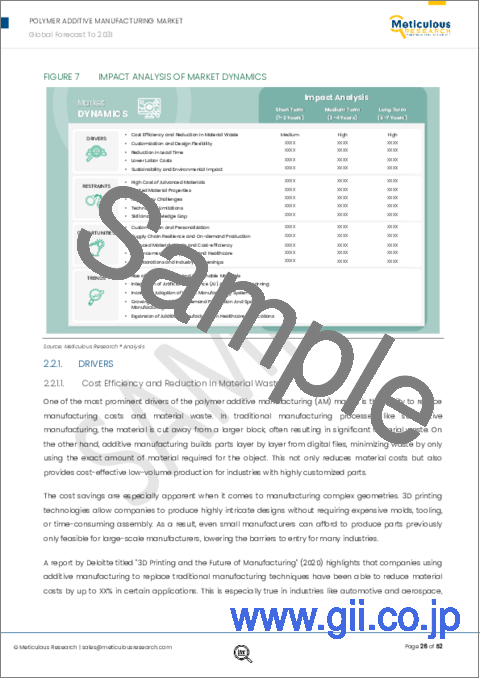

- 4.2.1. Drivers

- 4.2.1.1. Cost Efficiency and Reduction in Material Waste

- 4.2.1.2. Customization and Design Flexibility

- 4.2.1.3. Reduction in Lead Time

- 4.2.1.4. Lower Labor Costs

- 4.2.1.5. Sustainability and Environmental Impact

- 4.2.2. Restraints

- 4.2.2.1. High Cost of Advanced Materials

- 4.2.2.2. Limited Material Properties

- 4.2.2.3. Regulatory Challenges

- 4.2.2.4. Technology Limitations

- 4.2.2.5. Skill and Knowledge Gap

- 4.2.3. Opportunities

- 4.2.3.1. Customization and Personalization

- 4.2.3.2. Supply Chain Resilience and On-demand Production

- 4.2.3.3. Reduced Material Waste and Cost-efficiency

- 4.2.3.4. Advancements in Bioprinting and Healthcare

- 4.2.3.5. Collaborations and Industry Partnerships

- 4.2.4. Key Trends

- 4.2.4.1. Rise of Biodegradable and Sustainable Materials

- 4.2.4.2. Integration of Artificial Intelligence (Ai) and Machine Learning

- 4.2.4.3. Increased Adoption of Hybrid Manufacturing Systems

- 4.2.4.4. Growing Demand for On-demand Production and Spare Parts Manufacturing

- 4.2.4.5. Expansion of Additive Manufacturing in Healthcare Applications

- 4.2.1. Drivers

5. Polymer Additive Manufacturing Market Assessment-by offering

- 5.1. Overview

- 5.2. Services

- 5.3. Hardware

- 5.4. Software

- 5.5. Materials

- 5.5.1. Photopolymers (Resins)

- 5.5.2. Polylactic Acid (PLA)

- 5.5.3. Polyamide (Nylon)

- 5.5.4. Acrylonitrile Butadiene Styrene (ABS)

- 5.5.5. Polycarbonate (PC)

- 5.5.6. Thermoplastic Polyurethane (TPU)

- 5.5.7. Other Polymer Materials

6. Polymer Additive Manufacturing Market Assessment-by Technology

- 6.1. Overview

- 6.2. Fused Deposition Modeling (FDM)

- 6.3. Selective Laser Sintering (SLS)

- 6.4. Stereolithography (SLA)

- 6.5. Polyjet

- 6.6. Digital Light Processing (DLP)

- 6.7. Multi Jet Fusion

- 6.8. Binder Jetting

- 6.9. Other Polymer Technologies

7. Polymer Additive Manufacturing Market Assessment-by End User

- 7.1. Overview

- 7.2. Consumer Products

- 7.3. Healthcare

- 7.4. Automotive

- 7.5. General Manufacturing

- 7.6. Electronics & Semiconductors

- 7.7. Aerospace & Defense

- 7.8. Chemicals & Materials

- 7.9. Energy and Oil & Gas

- 7.10. Other End Users

8. Polymer Additive Manufacturing Market Assessment-by Geography

- 8.1. Overview

- 8.2. North America

- 8.2.1. U.S.

- 8.2.2. Canada

- 8.3. Asia-Pacific

- 8.3.1. China

- 8.3.2. Japan

- 8.3.3. India

- 8.3.4. Rest of Asia-Pacific

- 8.4. Europe

- 8.4.1. Germany

- 8.4.2. U.K.

- 8.4.3. France

- 8.4.4. Italy

- 8.4.5. Spain

- 8.4.6. Rest of Europe

- 8.5. Middle East & Africa

- 8.6. Latin America

9. Competition Analysis

- 9.1. Overview

- 9.2. Key Growth Strategies

- 9.3. Competitive Benchmarking

- 9.4. Competitive Dashboard

- 9.4.1. Industry Leaders

- 9.4.2. Market Differentiators

- 9.4.3. Vanguards

- 9.4.4. Emerging Companies

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, and SWOT Analysis*)

- 10.1. Stratasys, Ltd.

- 10.2. 3D Systems Corporation

- 10.3. EOS GmbH

- 10.4. Materialise NV

- 10.5. voxeljet AG

- 10.6. Markforged Holding Corporation

- 10.7. Proto Labs, Inc.

- 10.8. Autodesk, Inc.

- 10.9. 3Dceram

- 10.10. Dassault Systemes SE

- 10.11. Formlabs Inc.

- 10.12. Shapeways Holdings, Inc.

11. Appendix

- 11.1. Available Customization

- 11.2. Related Reports