|

|

市場調査レポート

商品コード

1364958

ライフサイエンス機器市場:技術別(分光、顕微鏡、クロマトグラフィー(HPLC、GC、TLC)、PCR、免疫測定、シークエンシング、フローサイトメトリー、ラボオートメーション、マイクロアレイ、電気泳動、インキュベーター、遠心分離機)-2030年までの世界予測Life Science Equipment Market by Technology (Spectroscopy, Microscopy, Chromatography (HPLC, GC, TLC), PCR, Immunoassay, Sequencing, Flow Cytometry, Lab Automation, Microarray, Electrophoresis, Incubator, Centrifuge) End User - Global Forecast to 2030 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| ライフサイエンス機器市場:技術別(分光、顕微鏡、クロマトグラフィー(HPLC、GC、TLC)、PCR、免疫測定、シークエンシング、フローサイトメトリー、ラボオートメーション、マイクロアレイ、電気泳動、インキュベーター、遠心分離機)-2030年までの世界予測 |

|

出版日: 2023年10月17日

発行: Meticulous Research

ページ情報: 英文 686 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

ライフサイエンス機器市場:技術別(分光、顕微鏡、クロマトグラフィー(HPLC、GC、TLC)、PCR、免疫測定、シークエンシング、フローサイトメトリー、ラボオートメーション、マイクロアレイ、電気泳動、インキュベーター、遠心分離機)エンドユーザー別-2030年までの世界予測

ライフサイエンス機器市場は、2023年から2030年までのCAGRが6.2%で、2030年には922億1,000万米ドルに達すると予測されます。

広範な1次調査と2次調査を経て、本レポートはライフサイエンス機器市場の詳細な分析を提供しています。また、ライフサイエンス機器市場の主要促進要因・市場抑制要因・課題・機会に関する洞察も提供しています。ライフサイエンス機器市場の成長は、製薬・バイオテクノロジー研究開発費の増加、ライフサイエンス研究開発を支援する政府の取り組み、慢性疾患や感染症の流行増加、環境汚染を抑制するための取り組みの拡大が原動力となっています。しかし、新興国では先端機器のコストが高く、資金やインフラの制約があるため、同市場の成長は抑制されています。

さらに、ゲノミクスとプロテオミクスの成長、個別化医療に対する意識の高まりと採用の拡大、ライフサイエンス業界における自動化とデジタル化の進展、食品の安全性と品質への注目の高まりは、この市場で事業を展開するプレーヤーに成長機会をもたらしています。しかし、高度な検査機器の操作に必要な熟練した専門家の不足やデータセキュリティの懸念は、市場利害関係者にとって大きな課題となっています。

本レポートに含まれる技術のうち、2023年の予測期間中に最も高いCAGRを記録すると予測されるのはシーケンシング分野です。高収率でエラーのないスループットを生成するシーケンス技術の能力、臨床および研究環境におけるこの技術の統合の拡大、製品提供の拡大および改善を目的としたシーケンス機器メーカー間のパートナーシップおよびコラボレーションの増加は、このセグメントの成長に寄与する要因の一部です。

本レポートに含まれるエンドユーザーのうち、2023年には製薬・バイオテクノロジー産業セグメントがライフサイエンス機器市場で最大のシェアを占めると推定されます。この大きな市場セグメントシェアは、個別化医療への注目の高まり、生物製剤やバイオシミラーを対象とした調査件数の増加、製薬・バイオテクノロジー企業とCRO間の協力関係の拡大が主な要因です。

ライフサイエンス機器市場の地域別シナリオの詳細分析では、5つの主要地域(北米、地域別市場、アジア太平洋、ラテンアメリカ、中東・アフリカ)の詳細な質的・量的洞察と各地域の主要国のカバレッジを提供しています。2023年には、北米がライフサイエンス機器市場で最大のシェアを占め、次いで欧州、アジア太平洋、ラテンアメリカ、中東&アフリカが続くと推定されます。バイオシミラーやジェネリック医薬品の多くの承認につながる慢性疾患や感染症の高い流行、先端技術の高い採用率、確立されたヘルスケアシステム、ライフサイエンス研究への資金提供活動の活発化などが、この市場の最大シェアを支える要因となっています。

調査範囲:

ライフサイエンス機器市場の技術別評価

- 分光法

- 分子分光法

- 紫外可視分光法

- 核磁気共鳴(NMR)

- 近赤外(NIR)分光法

- 赤外(IR)分光法

- ラマン分光法

- ポラリメーターと屈折計

- 蛍光・発光分光法

- その他の分子分光学技術

注:その他の分子分光テクノロジー分野には、ラマン分光法、エリプソメトリー、色計測が含まれます。

- 質量分析

- 四重極LC/MS

- 飛行時間型LC/MS(Q-TOF &LC-TOF)

- ガスクロマトグラフ質量分析計(GC/MS)

- フーリエ変換質量分析(FT/MS)

- マトリックス支援レーザー脱離イオン化飛行時間質量分析法(MALDI-TOF MS)

- ポータブルおよびインフィールド質量分析法

- タンデム質量分析(MS/MS)

- イオントラップ質量分析(LC/MS)

- 原子分光法

- 原子吸光分光法(AAS)

- 蛍光X線(XRF)分光法

- X線回折(XRD)分光法

- その他の原子分光技術

注)その他の原子分光技術には、誘導結合プラズマ(ICP)分光法、グロー放電分光法、アーク/スパーク発光分光法が含まれます。

- 分光学ソフトウェア

- 顕微鏡

- 電子顕微鏡

- 光学顕微鏡

- 走査型プローブ顕微鏡

- その他の顕微鏡

- 顕微鏡ソフトウェア

- クロマトグラフィー

- 高速液体クロマトグラフィー(HPLC)

- ガスクロマトグラフ(GC)

- 低圧液体クロマトグラフィー(LPLC)

- フラッシュクロマトグラフィー

- 薄層クロマトグラフィー(TLC)

- イオンクロマトグラフィー

- 超臨界流体クロマトグラフィー(SFC)

- クロマトグラフィーソフトウェア

- ラボオートメーション

- 自動ワークステーション

- ロボットシステム

- 自動保管・検索システム(ASRS)

- ラボ自動化ソフトウェア

- 免疫測定アナライザー

- 化学発光免疫測定装置

- 蛍光免疫測定

- ラジオイムノアッセイ(RIA)

- 比色免疫測定

- その他の免疫測定分析装置

- 免疫測定ソフトウェア

- PCR法

- RT-PCR

- コンベンショナルPCR

- デジタルPCR

- PCRソフトウェア

- シーケンス

- フローサイトメトリー

- セルベースフローサイトメーター

- ビーズベースフローサイトメーター

- フローサイトメトリーソフトウェア

- インキュベーター

- マイクロアレイ

- DNAマイクロアレイ

- タンパク質マイクロアレイ

- 組織アレイ

- その他のマイクロアレイ

- マイクロアレイソフトウェア

注:その他のマイクロアレイには、糖鎖マイクロアレイ、炭水化物マイクロアレイ、化合物マイクロアレイが含まれます。

- 遠心分離機

- 遠心機、タイプ別

- デバイス

- 多目的遠心機

- 微量遠心機

- 小型遠心機

- 超遠心機

- その他の遠心分離機

- 遠心分離機アクセサリー

- モデル別遠心機

- 卓上型遠心分離機

- 床置き型遠心分離機

- 遠心分離機:用途別

- 調査用途

- ゲノミクス

- 微生物学

- セロミクス

- プロテオミクス

- 臨床応用

- 診断学

- 血液処理とスクリーニング

- その他のアプリケーション

- 電気泳動

- ゲル電気泳動

- キャピラリー電気泳動

- ゲル文書化システムとソフトウェア

- その他の機器

注:その他の機器セグメントには、オートクレーブ、スターラー&シェーカー、ミキサー、バス、ホットプレート、オーブン&ファーネス、天秤が含まれます。

ライフサイエンス機器市場の評価-エンドユーザー別

- 製薬およびバイオテクノロジー産業

- 学術・研究機関

- 病院および診断研究所

- 分析試験所

- 農業および食品産業

- 法医学研究所

- その他のエンドユーザー

注:その他のエンドユーザーには、血液バンク、化粧品、化学、石油・ガス、エレクトロニクス・半導体、自動車、航空宇宙、セラミック、プラスチック、ゴム、塗料・コーティングなどの産業が含まれます。

ライフサイエンス機器市場の評価-地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- スイス

- その他欧州(RoE)

- アジア太平洋(APAC)

- 中国

- 日本

- インド

- 韓国

- APACのその他諸国(RoAPAC)

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ(RoLATAM)

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東とアフリカ(RoMEA)

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場

- 概要

- 市場成長への影響要因

- 市場力学の影響分析

- 要因分析

- ライフサイエンス機器市場規制分析

- 概要

- 北米

- 欧州

- アジア太平洋

- 中国

- 日本

- インド

- ラテンアメリカ

- 中東・アフリカ

- 価格分析

- 産業と技術動向

- ラボラトリーオートメーションとロボティクスの採用増加

- 高速液体クロマトグラフィー(HPLC)の技術進歩:UPLC、自動化、小型化

- ライフサイエンス業界におけるバイオインフォマティクス・ソリューションとサービスの採用増加

- クラウド接続されたラボ用機器を使用したライフサイエンス研究所のラボダウンタイムの最小化

- ポーターのファイブフォース分析

第5章 ライフサイエンス機器市場の技術別評価

- 概要

- 分光法

- 分子分光学

- 紫外可視分光法

- 核磁気共鳴(NMR)

- 近赤外(NIR)分光法

- 赤外(IR)分光法

- ラマン分光法

- ポラリメーターと屈折計

- 蛍光・発光分光法

- その他の分子分光学技術

- 質量分析

- 四重極LC/MS

- 飛行時間型LC/MS(Q-TOF &LC-TOF)

- ガスクロマトグラフ質量分析計(GC/MS)

- フーリエ変換質量分析(FT/MS)

- マトリックス支援レーザー脱離イオン化飛行時間質量分析法(MALDI-TOF MS)

- ポータブルおよびインフィールド質量分析法

- タンデム質量分析(MS/MS)

- イオントラップ質量分析(LC/MS)

- 原子分光法

- 原子吸光分光法(AAS)

- 蛍光X線(XRF)分光法

- X線回折(XRD)分光法

- その他の原子分光学技術

- 分光学ソフトウェア

- 分子分光学

- 顕微鏡

- 電子顕微鏡

- 光学顕微鏡

- 走査型プローブ顕微鏡

- その他の顕微鏡

- 顕微鏡ソフトウェア

- クロマトグラフィー

- 高速液体クロマトグラフィー(HPLC)

- ガスクロマトグラフ(GC)

- 低圧液体クロマトグラフィー(LPLC)

- フラッシュクロマトグラフィー

- 薄層クロマトグラフィー(TLC)

- イオンクロマトグラフィー

- 超臨界流体クロマトグラフィー(SFC)

- クロマトグラフィーソフトウェア

- ラボオートメーション

- 自動ワークステーション

- ロボットシステム

- 自動保管・検索システム(ASRS)

- ラボ自動化ソフトウェア

- 免疫測定アナライザー

- 化学発光免疫測定装置

- 蛍光免疫測定

- ラジオイムノアッセイ(RIA)

- 比色免疫測定

- その他の免疫測定分析装置

- 免疫測定ソフトウェア

- PCR法

- RT-PCR

- コンベンショナルPCR

- デジタルPCR

- PCRソフトウェア

- シーケンス

- フローサイトメトリー

- セルベースフローサイトメーター

- ビーズベースフローサイトメーター

- フローサイトメトリーソフトウェア

- インキュベーター

- マイクロアレイ

- DNAマイクロアレイ

- タンパク質マイクロアレイ

- 組織アレイ

- その他のマイクロアレイ

- マイクロアレイソフトウェア

- 遠心分離機

- 遠心機,タイプ別

- デバイス

- 多目的遠心機

- 微量遠心機

- 小型遠心機

- 超遠心機

- その他の遠心分離機

- 遠心分離機アクセサリー

- デバイス

- モデル別遠心機

- 卓上型遠心分離機

- 床置き型遠心分離機

- 遠心分離機:用途別

- 調査用途

- ゲノミクス

- 微生物学

- セロミクス

- プロテオミクス

- 臨床応用

- 診断学

- 血液処理とスクリーニング

- その他のアプリケーション

- 調査用途

- 遠心機,タイプ別

- 電気泳動

- ゲル電気泳動

- キャピラリー電気泳動

- ゲル文書化システムとソフトウェア

- その他の機器

第6章 ライフサイエンス機器のエンドユーザー別市場評価

- 概要

- 製薬・バイオ産業

- 学術・研究機関

- 病院・診断研究所

- 分析試験所

- 農業・食品産業

- 法医学研究所

- その他のエンドユーザー

第7章 ライフサイエンス機器市場の地域別評価

- 概要

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- スイス

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東とアフリカ

第8章 競合分析

- 概要

- 主要成長戦略

- 競合ベンチマーキング

- 競合ダッシュボード

- 業界リーダー

- 市場差別化要因

- 先行企業

- 新興企業

- 市場シェア分析(2022年)

- Thermo Fisher Scientific Inc.(U.S.)

- Danaher Corporation(U.S.)

- Agilent Technologies, Inc.(U.S.)

- F. Hoffmann-la Roche AG(Switzerland)

- Shimadzu Corporation(Japan)

第9章 企業プロファイル(企業概要、財務概要、製品ポートフォリオ、戦略的展開、SWOT分析)

- Thermo Fisher Scientific Inc.

- Agilent Technologies, Inc.

- Danaher Corporation

- F. Hoffmann LA-Roche AG

- Shimadzu Corporation

- Becton, Dickinson, and Company

- Bio-Rad Laboratories, Inc.

- PerkinElmer, Inc.

- Waters Corporation

- Bruker Corporation

- Siemens Heathineers

- Eppendorf SE

- Sartorius AG

- Qiagen N.V.

第10章 付録

List of Tables

- Table 1 ISO Compliance Regulations

- Table 2 GMP Regulations for the Life Sciences Industry

- Table 3 Key FDA Regulations for the Life Sciences Industry

- Table 4 Laws Regulating the Life Sciences Industry In India

- Table 5 Pricing of Life Sciences And Laboratory Equipment

- Table 6 Global Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

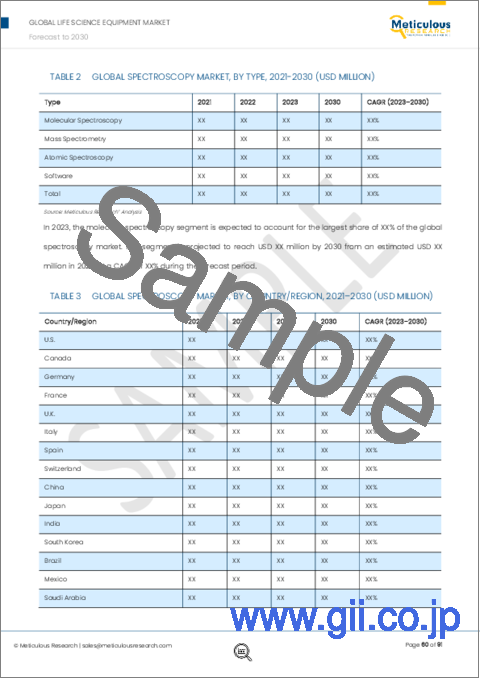

- Table 7 Global Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 8 Global Spectroscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 9 Global Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 10 Global Molecular Spectroscopy Market, by Country/Region, 2021-2030, (USD Million)

- Table 11 Global UV/VIS Spectroscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 12 Global Nuclear Magnetic Resonance (NMR) Spectroscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 13 Global Near-Infrared (NIR) Spectroscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 14 Global Infrared (IR) Spectroscopy Market, by Country/Region, 2021-2030, (USD Million)

- Table 15 Global Raman Spectroscopy Market, by Country/Region, 2021-2030, (USD Million)

- Table 16 Global Polarimeters And Refractometers Market, by Country/Region, 2021-2030 (USD Million)

- Table 17 Global Fluorescence & Luminescence Spectroscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 18 Global Other Molecular Spectroscopy Technologies Market, by Country/Region, 2021-2030 (USD Million)

- Table 19 Application Areas Of Mass Spectrometry

- Table 20 Global Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 21 Global Mass Spectrometry Market, by Country/Region, 2021-2030 (USD Million)

- Table 22 Comparison Between Scan And Sim Mode

- Table 23 Global Quadrupole LC/MS Market, by Country/Region, 2021-2030 (USD Million)

- Table 24 Global Time-Of-Flight LC/MS (Q-ToF & LC-ToF) Market, by Country/Region, 2021-2030 (USD Million)

- Table 25 Global Gas Chromatography-Mass Spectrometry (GC/MS) Market, by Country/Region, 2021-2030 (USD Million)

- Table 26 Global Fourier Transform Mass Spectrometry (FT/MS) Market, by Country/Region, 2021-2030 (USD Million)

- Table 27 Global Matrix-Assisted Laser Desorption/Ionization-Time Of Flight Mass Spectrometry (Maldi-ToF MS) Market, by Country/Region, 2021-2030 (USD Million)

- Table 28 Global Portable And In-Field Mass Spectrometry Market, by Country/Region, 2021-2030 (USD Million)

- Table 29 Global Tandem Mass Spectrometry (MS/MS) Market, by Country/Region, 2021-2030 (USD Million)

- Table 30 Global Ion Trap Mass Spectrometry (LC/MS) Market, by Country/Region, 2021-2030 (USD Million)

- Table 31 Global Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 32 Global Atomic Spectroscopy Market, by Country/Region, 2021-2030, (USD Million)

- Table 33 Global Atomic Absorbance Spectroscopy (AAS) Market, by Country/Region, 2021-2030 (USD Million)

- Table 34 Global X-Ray Fluorescence (XRF) Spectroscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 35 Global X-Ray Diffraction (XRD) Spectroscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 36 Global Other Atomic Spectroscopy Technologies Market, by Country/Region, 2021-2030 (USD Million)

- Table 37 Global Spectroscopy Software Market, by Country/Region, 2021-2030, (USD Million)

- Table 38 Global Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 39 Global Microscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 40 Global Electron Microscopy Market, by Country/Region, 2021-2030, (USD Million)

- Table 41 Global Optical Microscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 42 Global Scanning Probe Microscopy Market, by Country/Region, 2021-2030, (USD Million)

- Table 43 Global Other Microscopy Market, by Country/Region, 2021-2030 (USD Million)

- Table 44 Global Microscopy Software Market, by Country/Region, 2021-2030, (USD Million)

- Table 45 Global Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 46 Global Chromatography Market, by Country/Region, 2021-2030 (USD Million)

- Table 47 Global High-Performance Liquid Chromatography (HPLC) Market, by Country/Region, 2021-2030 (USD Million)

- Table 48 Global Gas Chromatography (GC) Market, by Country/Region, 2021-2030, (USD Million)

- Table 49 Global Low-Pressure Liquid Chromatography (LPLC) Market, by Country/Region, 2021-2030 (USD Million)

- Table 50 Global Flash Chromatography Market, by Country/Region, 2021-2030, (USD Million)

- Table 51 Global Thin Layer Chromatography (TLC) Market, by Country/Region, 2021-2030 (USD Million)

- Table 52 Global Ion Chromatography Market, by Country/Region, 2021-2030 (USD Million)

- Table 53 Global Supercritical Fluid Chromatography (SFC) Market, by Country/Region, 2021-2030 (USD Million)

- Table 54 Global Chromatography Software Market, by Country/Region, 2021-2030, (USD Million)

- Table 55 Global Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 56 Global Lab Automation Market, by Country/Region, 2021-2030 (USD Million)

- Table 57 Global Automated Workstations Market, by Country/Region, 2021-2030, (USD Million)

- Table 58 Global Robotic Systems Market, by Country/Region, 2021-2030 (USD Million)

- Table 59 Global Automated Storage And Retrieval Systems Market, by Country/Region, 2021-2030 (USD Million)

- Table 60 Global Lab Automation Software Market, by Country/Region, 2021-2030, (USD Million)

- Table 61 Global Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 62 Global Immunoassay Analyzers Market, by Country/Region, 2021-2030, (USD Million)

- Table 63 Global Chemiluminescence Immunoassay Market, by Country/Region, 2021-2030 (USD Million)

- Table 64 Global Fluorescence Immunoassay Market, by Country/Region, 2021-2030, (USD Million)

- Table 65 Global Radioimmunoassay Market, by Country/Region, 2021-2030 (USD Million)

- Table 66 Global Colorimetric Immunoassay Market, by Country/Region, 2021-2030, (USD Million)

- Table 67 Global Other Immunoassay Analyzers Market, by Country/Region, 2021-2030 (USD Million)

- Table 68 Global Immunoassay Software Market, by Country/Region, 2021-2030, (USD Million)

- Table 69 Global PCR Market, by Type, 2021-2030 (USD Million)

- Table 70 Global PCR Market, by Country/Region, 2021-2030 (USD Million)

- Table 71 Global RT-PCR Market, by Country/Region, 2021-2030 (USD Million)

- Table 72 Global Conventional PCR Market, by Country/Region, 2021-2030 (USD Million)

- Table 73 Global Digital PCR Market, by Country/Region, 2021-2030 (USD Million)

- Table 74 Global PCR Software Market, by Country/Region, 2021-2030 (USD Million)

- Table 75 Global Sequencing Market, by Country/Region, 2021-2030 (USD Million)

- Table 76 Global Flow Cytometry Market, by Type, 2021-2030 (USD Million)

- Table 77 Global Flow Cytometry Market, by Country/Region, 2021-2030 (USD Million)

- Table 78 Global Cell-Based Flow Cytometers Market, by Country/Region, 2021-2030, (USD Million)

- Table 79 Global Bead-Based Flow Cytometers Market, by Country/Region, 2021-2030, (USD Million)

- Table 80 Global Flow Cytometry Software Market, by Country/Region, 2021-2030, (USD Million)

- Table 81 Global Life Science Equipment Market for Incubators, by Country/Region, 2021-2030 (USD Million)

- Table 82 Global Microarray Market, by Type, 2021-2030 (USD Million)

- Table 83 Global Microarray Market, by Country/Region, 2021-2030 (USD Million)

- Table 84 Global DNA Microarrays Market, by Country/Region, 2021-2030 (USD Million)

- Table 85 Global Protein Microarray Market, by Country/Region, 2021-2030 (USD Million)

- Table 86 Global Tissue Array (TMA) Market, by Country/Region, 2021-2030 (USD Million)

- Table 87 Global Other Microarrays Market, by Country/Region, 2021-2030 (USD Million)

- Table 88 Global Microarray Software Market, by Country/Region, 2021-2030 (USD Million)

- Table 89 Global Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 90 Global Centrifuges Market, by Country/Region, 2021-2030 (USD Million)

- Table 91 Global Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 92 Global Centrifuge Devices Market, by Country/Region, 2021-2030 (USD Million)

- Table 93 Global Multipurpose Centrifuges Market, by Country/Region, 2021-2030, (USD Million)

- Table 94 Global Microcentrifuges Market By Country/Region, 2021-2030 (USD Million)

- Table 95 Global Mini-Centrifuges Market, by Country/Region, 2021-2030 (USD Million)

- Table 96 Global Ultracentrifuges Market, by Country/Region, 2021-2030 (USD Million)

- Table 97 Leukemia: Estimated Number of New Cases Worldwide, 2020 Vs. 2030

- Table 98 Global Other Centrifuges Market, by Country/Region, 2021-2030 (USD Million)

- Table 99 Global Centrifuge Accessories Market, by Country/Region, 2021-2030, (USD Million)

- Table 100 Global Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 101 Global Benchtop Centrifuges Market, by Country/Region, 2021-2030, (USD Million)

- Table 102 Global Floor-Standing Centrifuges Market, by Country/Region, 2021-2030, (USD Million)

- Table 103 Global Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 104 Global Centrifuges Market for Research Application, by Type, 2021-2030, (USD Million)

- Table 105 Global Centrifuges Market for Research Applications, by Country/Region, 2021-2030 (USD Million)

- Table 106 Global Centrifuges Market for Genomics, by Country/Region, 2021-2030, (USD Million)

- Table 107 Global Centrifuges Market for Microbiology, by Country/Region, 2021-2030 (USD Million)

- Table 108 Global Centrifuges Market for Cellomics, by Country/Region, 2021-2030

- Table 109 Global Centrifuges Market for Proteomics, by Country/Region, 2021-2030, (USD Million)

- Table 110 Global Centrifuges Market for Clinical Application, by Type, 2021-2030, (USD Million)

- Table 111 Global Centrifuges Market for Clinical Application, by Country/Region, 2021-2030 (USD Million)

- Table 112 Global Centrifuges Market for Diagnostics, by Country/Region, 2021-2030, (USD Million)

- Table 113 Global Centrifuges Market for Blood Processing And Screening, by Country/Region, 2021-2030 (USD Million)

- Table 114 Global Centrifuges Market for Other Applications, by Country/Region, 2021-2030 (USD Million)

- Table 115 Global Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 116 Global Electrophoresis Market, by Country/Region, 2021-2030 (USD Million)

- Table 117 Global Gel Electrophoresis Market, by Country/Region, 2021-2030 (USD Million)

- Table 118 Global Capillary Electrophoresis Market, by Country/Region, 2021-2030, (USD Million)

- Table 119 Global Gel Documentation System And Software Market, by Country/Region, 2021-2030 (USD Million)

- Table 120 Global Life Science Equipment Market for Other Equipment, by Country/Region, 2021-2030 (USD Million)

- Table 121 Global Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 122 Global Life Science Equipment Market for Pharmaceutical & Biotechnology Industry, by Country/Region, 2021-2030 (USD Million)

- Table 123 Global Life Science Equipment Market for Academic & Research Institutes, by Country/Region, 2021-2030 (USD Million)

- Table 124 Global Life Science Equipment Market for Hospitals & Diagnostic Laboratories, by Country/Region, 2021-2030 (USD Million)

- Table 125 Global Life Science Equipment Market for Analytical Testing Laboratories, by Country/Region, 2021-2030 (USD Million)

- Table 126 Global Life Science Equipment Market for Agriculture & Food Industry, by Country/Region, 2021-2030 (USD Million)

- Table 127 Global Life Science Equipment Market for Forensic Laboratories, by Country/Region, 2021-2030 (USD Million)

- Table 128 Global Life Science Equipment Market for Other End Users, by Country/Region, 2021-2030 (USD Million)

- Table 129 Global Life Science Equipment Market, by Country/Region, 2021-2030 (USD Million)

- Table 130 North America: Life Science Equipment Market, by Country, 2021-2030 (USD Million)

- Table 131 North America: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 132 North America: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 133 North America: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 134 North America: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 135 North America: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 136 North America: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 137 North America: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 138 North America: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 139 North America: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 140 North America: PCR Market, by Type, 2021-2030 (USD Million)

- Table 141 North America: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 142 North America: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 143 North America: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 144 North America: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 145 North America: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 146 North America: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 147 North America: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 148 North America: Centrifuges Clinical Application Market, by Type, 2021-2030, (USD Million)

- Table 149 North America: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 150 North America: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 151 U.S.: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 152 U.S.: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 153 U.S.: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 154 U.S.: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 155 U.S.: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 156 U.S.: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 157 U.S.: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 158 U.S.: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 159 U.S.: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 160 U.S.: PCR Market, by Type, 2021-2030 (USD Million)

- Table 161 U.S.: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 162 U.S.: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 163 U.S.: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 164 U.S.: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 165 U.S.: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 166 U.S.: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 167 U.S.: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 168 U.S.: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 169 U.S.: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 170 U.S.: Life Science Equipment Market, by End User, 2021-2030, (USD Million)

- Table 171 Canada: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 172 Canada: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 173 Canada: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 174 Canada: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 175 Canada: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 176 Canada: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 177 Canada: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 178 Canada: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 179 Canada: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 180 Canada: PCR Market, by Type, 2021-2030 (USD Million)

- Table 181 Canada: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 182 Canada: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 183 Canada: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 184 Canada: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 185 Canada: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 186 Canada: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 187 Canada: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 188 Canada: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 189 Canada: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 190 Canada: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 191 Europe: Life Science Equipment Market, by Country/Region, 2021-2030 (USD Million)

- Table 192 Europe: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 193 Europe: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 194 Europe: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 195 Europe: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 196 Europe: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 197 Europe: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 198 Europe: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 199 Europe: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 200 Europe: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 201 Europe: PCR Market, by Type, 2021-2030 (USD Million)

- Table 202 Europe: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 203 Europe: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 204 Europe: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 205 Europe: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 206 Europe: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 207 Europe: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 208 Europe: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 209 Europe: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 210 Europe: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 211 Europe: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 212 Germany: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 213 Germany: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 214 Germany: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 215 Germany: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 216 Germany: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 217 Germany: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 218 Germany: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 219 Germany: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 220 Germany: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 221 Germany: PCR Market, by Type, 2021-2030 (USD Million)

- Table 222 Germany: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 223 Germany: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 224 Germany: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 225 Germany: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 226 Germany: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 227 Germany: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 228 Germany: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 229 Germany: Centrifuges Clinical Application Market, by Type, 2021-2030, (USD Million)

- Table 230 Germany: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 231 Germany: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 232 France: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 233 France: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 234 France: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 235 France: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 236 France: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 237 France: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 238 France: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 239 France: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 240 France: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 241 France: PCR Market, by Type, 2021-2030 (USD Million)

- Table 242 France: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 243 France: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 244 France: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 245 France: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 246 France: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 247 France: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 248 France: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 249 France: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 250 France: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 251 France: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 252 U.K.: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 253 U.K.: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 254 U.K.: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 255 U.K.: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 256 U.K.: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 257 U.K.: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 258 U.K.: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 259 U.K.: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 260 U.K.: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 261 U.K.: PCR Market, by Type, 2021-2030 (USD Million)

- Table 262 U.K.: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 263 U.K.: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 264 U.K.: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 265 U.K.: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 266 U.K.: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 267 U.K.: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 268 U.K.: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 269 U.K.: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 270 U.K.: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 271 U.K.: Life Science Equipment Market, by End User, 2021-2030, (USD Million)

- Table 272 Italy: Food And Agriculture Products Exported To The U.S. In 2021 (USD Million)

- Table 273 Italy: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 274 Italy: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 275 Italy: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 276 Italy: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 277 Italy: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 278 Italy: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 279 Italy: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 280 Italy: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 281 Italy: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 282 Italy: PCR Market, by Type, 2021-2030 (USD Million)

- Table 283 Italy: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 284 Italy: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 285 Italy: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 286 Italy: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 287 Italy: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 288 Italy: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 289 Italy: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 290 Italy: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 291 Italy: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 292 Italy: Life Science Equipment Market, by End User, 2021-2030, (USD Million)

- Table 293 Spain: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 294 Spain: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 295 Spain: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 296 Spain: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 297 Spain: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 298 Spain: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 299 Spain: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 300 Spain: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 301 Spain: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 302 Spain: PCR Market, by Type, 2021-2030 (USD Million)

- Table 303 Spain: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 304 Spain: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 305 Spain: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 306 Spain: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 307 Spain: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 308 Spain: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 309 Spain: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 310 Spain: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 311 Spain: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 312 Spain: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 313 Switzerland: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 314 Switzerland: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 315 Switzerland: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 316 Switzerland: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 317 Switzerland: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 318 Switzerland: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 319 Switzerland: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 320 Switzerland: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 321 Switzerland: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 322 Switzerland: PCR Market, by Type, 2021-2030 (USD Million)

- Table 323 Switzerland: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 324 Switzerland: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 325 Switzerland: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 326 Switzerland: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 327 Switzerland: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 328 Switzerland: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 329 Switzerland: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 330 Switzerland: Centrifuges Clinical Application Market, by Type, 2021-2030, (USD Million)

- Table 331 Switzerland: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 332 Switzerland: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 333 Pharmaceutical Micro Indicators, 2020 (USD Million)

- Table 334 Rest of Europe: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 335 Rest of Europe: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 336 Rest of Europe: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 337 Rest of Europe: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 338 Rest of Europe: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 339 Rest of Europe: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 340 Rest of Europe: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 341 Rest of Europe: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 342 Rest of Europe: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 343 Rest of Europe: PCR Market, by Type, 2021-2030 (USD Million)

- Table 344 Rest of Europe: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 345 Rest of Europe: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 346 Rest of Europe: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 347 Rest of Europe: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 348 Rest of Europe: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 349 Rest of Europe: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 350 Rest of Europe: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 351 Rest of Europe: Centrifuges Clinical Application Market, by Type, 2021-2030, (USD Million)

- Table 352 Rest of Europe: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 353 Rest of Europe: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 354 Asia-Pacific: Life Science Equipment Market, by Country, 2021-2030 (USD Million)

- Table 355 Asia-Pacific: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 356 Asia-Pacific: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 357 Asia-Pacific: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 358 Asia-Pacific: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 359 Asia-Pacific: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 360 Asia-Pacific: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 361 Asia-Pacific: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 362 Asia-Pacific: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 363 Asia-Pacific: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 364 Asia-Pacific: PCR Market, by Type, 2021-2030 (USD Million)

- Table 365 Asia-Pacific: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 366 Asia-Pacific: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 367 Asia-Pacific: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 368 Asia-Pacific: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 369 Asia-Pacific: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 370 Asia-Pacific: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 371 Asia-Pacific: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 372 Asia-Pacific: Centrifuges Clinical Application Market, by Type, 2021-2030, (USD Million)

- Table 373 Asia-Pacific: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 374 Asia-Pacific: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 375 China: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 376 China: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 377 China: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 378 China: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 379 China: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 380 China: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 381 China: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 382 China: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 383 China: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 384 China: PCR Market, by Type, 2021-2030 (USD Million)

- Table 385 China: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 386 China: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 387 China: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 388 China: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 389 China: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 390 China: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 391 China: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 392 China: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 393 China: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 394 China: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 395 Japan: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 396 Japan: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 397 Japan: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 398 Japan: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 399 Japan: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 400 Japan: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 401 Japan: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 402 Japan: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 403 Japan: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 404 Japan: PCR Market, by Type, 2021-2030 (USD Million)

- Table 405 Japan: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 406 Japan: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 407 Japan: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 408 Japan: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 409 Japan: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 410 Japan: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 411 Japan: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 412 Japan: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 413 Japan: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 414 Japan: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 415 India: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 416 India: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 417 India: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 418 India: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 419 India: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 420 India: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 421 India: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 422 India: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 423 India: PCR Market, by Type, 2021-2030 (USD Million)

- Table 424 India: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 425 India: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 426 India: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 427 India: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 428 India: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 429 India: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 430 India: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 431 India: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 432 India: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 433 India: Life Science Equipment Market, by End User, 2021-2030, (USD Million)

- Table 434 South Korea: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 435 South Korea: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 436 South Korea: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 437 South Korea: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 438 South Korea: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 439 South Korea: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 440 South Korea: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 441 South Korea: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 442 South Korea: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 443 South Korea: PCR Market, by Type, 2021-2030 (USD Million)

- Table 444 South Korea: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 445 South Korea: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 446 South Korea: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 447 South Korea: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 448 South Korea: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 449 South Korea: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 450 South Korea: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 451 South Korea: Centrifuges Clinical Application Market, by Type, 2021-2030, (USD Million)

- Table 452 South Korea: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 453 South Korea: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 454 Estimated Number Of New Cancer Cases, by Country, 2020 Vs. 2030

- Table 455 Rest of Asia-Pacific: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 456 Rest of Asia-Pacific: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 457 Rest of Asia-Pacific: Molecular Spectroscopy Market, by Type, 2021-2030, (USD Million)

- Table 458 Rest of Asia-Pacific: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 459 Rest of Asia-Pacific: Atomic Spectroscopy Market, by Type, 2021-2030, (USD Million)

- Table 460 Rest of Asia-Pacific: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 461 Rest of Asia-Pacific: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 462 Rest of Asia-Pacific: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 463 Rest of Asia-Pacific: Immunoassay Analyzers Market, by Type, 2021-2030, (USD Million)

- Table 464 Rest of Asia-Pacific: PCR Market, by Type, 2021-2030 (USD Million)

- Table 465 Rest of Asia-Pacific: Flow Cytometry Market, by Technology, 2021-2030, (USD Million)

- Table 466 Rest of Asia-Pacific: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 467 Rest of Asia-Pacific: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 468 Rest of Asia-Pacific: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 469 Rest of Asia-Pacific: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 470 Rest of Asia-Pacific: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 471 Rest of Asia-Pacific: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 472 Rest of Asia-Pacific: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 473 Rest of Asia-Pacific: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 474 Rest of Asia-Pacific: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 475 Latin America: Life Science Equipment Market, by Country, 2021-2030 (USD Million)

- Table 476 Latin America: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 477 Latin America: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 478 Latin America: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 479 Latin America: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 480 Latin America: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 481 Latin America: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 482 Latin America: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 483 Latin America: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 484 Latin America: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 485 Latin America: PCR Market, by Type, 2021-2030 (USD Million)

- Table 486 Latin America: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 487 Latin America: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 488 Latin America: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 489 Latin America: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 490 Latin America: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 491 Latin America: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 492 Latin America: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 493 Latin America: Centrifuges Clinical Application Market, by Type, 2021-2030, (USD Million)

- Table 494 Latin America: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 495 Latin America: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 496 Brazil: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 497 Brazil: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 498 Brazil: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 499 Brazil: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 500 Brazil: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 501 Brazil: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 502 Brazil: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 503 Brazil: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 504 Brazil: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 505 Brazil: PCR Market, by Type, 2021-2030 (USD Million)

- Table 506 Brazil: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 507 Brazil: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 508 Brazil: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 509 Brazil: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 510 Brazil: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 511 Brazil: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 512 Brazil: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 513 Brazil: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 514 Brazil: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 515 Brazil: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 516 Mexico: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 517 Mexico: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 518 Mexico: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 519 Mexico: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 520 Mexico: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 521 Mexico: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 522 Mexico: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 523 Mexico: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 524 Mexico: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 525 Mexico: PCR Market, by Type, 2021-2030 (USD Million)

- Table 526 Mexico: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 527 Mexico: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 528 Mexico: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 529 Mexico: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 530 Mexico: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 531 Mexico: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 532 Mexico: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 533 Mexico: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 534 Mexico: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 535 Mexico: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 536 Rest of Latin America: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 537 Rest of Latin America: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 538 Rest of Latin America: Molecular Spectroscopy Market, by Type, 2021-2030, (USD Million)

- Table 539 Rest of Latin America: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 540 Rest of Latin America: Atomic Spectroscopy Market, by Type, 2021-2030, (USD Million)

- Table 541 Rest of Latin America: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 542 Rest of Latin America: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 543 Rest of Latin America: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 544 Rest of Latin America: Immunoassay Analyzers Market, by Type, 2021-2030, (USD Million)

- Table 545 Rest of Latin America: PCR Market, by Type, 2021-2030 (USD Million)

- Table 546 Rest of Latin America: Flow Cytometry Market, by Technology, 2021-2030, (USD Million)

- Table 547 Rest of Latin America: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 548 Rest of Latin America: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 549 Rest of Latin America: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 550 Rest of Latin America: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 551 Rest of Latin America: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 552 Rest of Latin America: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 553 Rest of Latin America: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 554 Rest of Latin America: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 555 Rest of Latin America: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 556 Middle East & Africa: Life Science Equipment Market, by Country/Region, 2021-2030 (USD Million)

- Table 557 Middle East & Africa: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 558 Middle East & Africa: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 559 Middle East & Africa: Molecular Spectroscopy Market, by Type, 2021-2030, (USD Million)

- Table 560 Middle East & Africa: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 561 Middle East & Africa: Atomic Spectroscopy Market, by Type, 2021-2030, (USD Million)

- Table 562 Middle East & Africa: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 563 Middle East & Africa: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 564 Middle East & Africa: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 565 Middle East & Africa: Immunoassay Analyzers Market, by Type, 2021-2030, (USD Million)

- Table 566 Middle East & Africa: PCR Market, by Type, 2021-2030 (USD Million)

- Table 567 Middle East & Africa: Flow Cytometry Market, by Technology, 2021-2030, (USD Million)

- Table 568 Middle East & Africa: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 569 Middle East & Africa: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 570 Middle East & Africa: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 571 Middle East & Africa: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 572 Middle East & Africa: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 573 Middle East & Africa: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 574 Middle East & Africa: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 575 Middle East & Africa: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 576 Middle East & Africa: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 577 Saudi Arabia: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 578 Saudi Arabia: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 579 Saudi Arabia: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 580 Saudi Arabia: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 581 Saudi Arabia: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 582 Saudi Arabia: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 583 Saudi Arabia: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 584 Saudi Arabia: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 585 Saudi Arabia: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 586 Saudi Arabia: PCR Market, by Type, 2021-2030 (USD Million)

- Table 587 Saudi Arabia: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 588 Saudi Arabia: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 589 Saudi Arabia: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 590 Saudi Arabia: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 591 Saudi Arabia: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 592 Saudi Arabia: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 593 Saudi Arabia: Centrifuges Research Application Market, by Type, 2021-2030, (USD Million)

- Table 594 Saudi Arabia: Centrifuges Clinical Application Market, by Type, 2021-2030, (USD Million)

- Table 595 Saudi Arabia: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 596 Saudi Arabia: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 597 UAE: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 598 UAE: Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 599 UAE: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 600 UAE: Mass Spectrometry Market, by Type, 2021-2030 (USD Million)

- Table 601 UAE: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 602 UAE: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 603 UAE: Chromatography Market, by Type, 2021-2030 (USD Million)

- Table 604 UAE: Lab Automation Market, by Type, 2021-2030 (USD Million)

- Table 605 UAE: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 606 UAE: PCR Market, by Type, 2021-2030 (USD Million)

- Table 607 UAE: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 608 UAE: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 609 UAE: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 610 UAE: Centrifuge Devices Market, by Type, 2021-2030 (USD Million)

- Table 611 UAE: Centrifuges Market, by Model, 2021-2030 (USD Million)

- Table 612 UAE: Centrifuges Market, by Application, 2021-2030 (USD Million)

- Table 613 UAE: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 614 UAE: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 615 UAE: Electrophoresis Market, by Type, 2021-2030 (USD Million)

- Table 616 UAE: Life Science Equipment Market, by End User, 2021-2030, (USD Million)

- Table 617 Rest of Middle East & Africa: Life Science Equipment Market, by Technology, 2021-2030 (USD Million)

- Table 618 Rest of Middle East & Africa: Spectroscopy Market, by Type, 2021-2030, (USD Million)

- Table 619 Rest of Middle East & Africa: Molecular Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 620 Rest of Middle East & Africa: Mass Spectrometry Market, by Type, 2021-2030, (USD Million)

- Table 621 Rest of Middle East & Africa: Atomic Spectroscopy Market, by Type, 2021-2030 (USD Million)

- Table 622 Rest of Middle East & Africa: Microscopy Market, by Type, 2021-2030 (USD Million)

- Table 623 Rest of Middle East & Africa: Chromatography Market, by Type, 2021-2030, (USD Million)

- Table 624 Rest of Middle East & Africa: Lab Automation Market, by Type, 2021-2030, (USD Million)

- Table 625 Rest of Middle East & Africa: Immunoassay Analyzers Market, by Type, 2021-2030 (USD Million)

- Table 626 Rest of Middle East & Africa: PCR Market, by Type, 2021-2030 (USD Million)

- Table 627 Rest of Middle East & Africa: Flow Cytometry Market, by Technology, 2021-2030 (USD Million)

- Table 628 Rest of Middle East & Africa: Microarray Market, by Type, 2021-2030 (USD Million)

- Table 629 Rest of Middle East & Africa: Centrifuges Market, by Type, 2021-2030 (USD Million)

- Table 630 Rest of Middle East & Africa: Centrifuge Devices Market, by Type, 2021-2030, (USD Million)

- Table 631 Rest of Middle East & Africa: Centrifuges Market, by Model, 2021-2030, (USD Million)

- Table 632 Rest of Middle East & Africa: Centrifuges Market, by Application, 2021-2030, (USD Million)

- Table 633 Rest of Middle East & Africa: Centrifuges Research Application Market, by Type, 2021-2030 (USD Million)

- Table 634 Rest of Middle East & Africa: Centrifuges Clinical Application Market, by Type, 2021-2030 (USD Million)

- Table 635 Rest of Middle East & Africa: Electrophoresis Market, by Type, 2021-2030, (USD Million)

- Table 636 Rest of Middle East & Africa: Life Science Equipment Market, by End User, 2021-2030 (USD Million)

- Table 637 Recent Developments, by Company, 2020-2023)

Life Science Equipment Market By Technology (Spectroscopy, Microscopy, Chromatography (HPLC, GC, TLC), PCR, Immunoassay, Sequencing, Flow Cytometry, Lab Automation, Microarray, Electrophoresis, Incubator, Centrifuge) End User- Global Forecast to 2030

The life science equipment market is expected to reach $92.21 billion by 2030, at a CAGR of 6.2% from 2023 to 2030.

After extensive primary and secondary research, the report provides an in-depth analysis of the life science equipment market. The report also provides insights into the key drivers, restraints, challenges, and opportunities in the life science equipment market. The growth of the life science equipment market is driven by the increasing pharmaceutical and biotech R&D expenditures, government initiatives supporting life sciences R&D, the increasing prevalence of chronic and infectious diseases, and growth in initiatives to control environmental pollution. However, the high costs of advanced equipment and funding and infrastructure limitations in developing countries restrain the growth of this market.

Furthermore, the growth in genomics and proteomics, the increasing awareness and growing adoption of personalized medicines, increasing automation and digitalization in the life sciences industry, and the increasing focus on food safety and quality are generating growth opportunities for the players operating in this market. However, the lack of skilled professionals required for operating advanced laboratory equipment and data security concerns are major challenges for market stakeholders.

Among the technologies included in the report, in 2023, the sequencing segment is projected to register the highest CAGR during the forecast period. The capability of sequencing technology to generate high-yield error-free throughput, the growing integration of this technology in clinical and research settings, and increasing partnerships and collaborations among sequencing instrument manufacturers to expand and improve product offerings are some of the factors contributing to the growth of the segment.

Among the end users included in the report, in 2023, the pharmaceutical and biotechnology industry segment is estimated to account for the largest share of the life science equipment market. The large market segment share is majorly attributed to the increased attention towards personalized medicine, growth in the number of research studies covering biologics and biosimilars, and growing collaborations among pharmaceutical & biotechnology companies and CROs.

An in-depth analysis of the geographical scenario of the life science equipment market provides detailed qualitative and quantitative insights into the five major geographies (North America, Europe, Asia-Pacific, Latin America, the Middle East & Africa) along with the coverage of major countries in each region. In 2023, North America is estimated to account for the largest share of the life science equipment market, followed by Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The high prevalence of chronic and infectious diseases leading to a large number of approvals of biosimilars and generics, high adoption of advanced technologies, a well-established healthcare system, and increased funding activities for life science research are some of the factors supporting the largest share of this market.

The key players operating in the life science equipment market are Agilent Technologies, Inc. (U.S.), Becton, Dickinson, and Company (U.S.), Bio-Rad Laboratories, Inc. (U.S.), Danaher Corporation (U.S.), F. Hoffmann LA-Roche AG (Switzerland), PerkinElmer, Inc. (U.S.), Thermo Fisher Scientific, Inc. (U.S.), Waters Corporation (U.S.), Bruker Corporation (U.S.), Shimadzu Corporation (Japan), Siemens Healthineers AG (Germany), Eppendorf SE (Germany), Sartorius AG (Germany), and Qiagen N.V. (Netherlands).

Scope of the Report:

Life Science Equipment Market Assessment-by Technology

- Spectroscopy

- Molecular Spectroscopy

- UV/Vis Spectroscopy

- Nuclear Magnetic Resonance (NMR)

- Near-Infrared (NIR) Spectroscopy

- Infrared (IR) Spectroscopy

- Raman Spectroscopy

- Polarimeters and Refractometers

- Fluorescence & Luminescence Spectroscopy

- Other Molecular Spectroscopy Technologies

Note: Other molecular spectroscopy technologies segment includes Raman spectroscopy, ellipsometry, and color measurement.

- Mass Spectrometry

- Quadrupole LC/MS

- Time of Flight LC/MS (Q-TOF & LC-TOF)

- Gas Chromatography-Mass Spectrometry (GC/MS)

- Fourier Transform Mass Spectrometry (FT/MS)

- Matrix-Assisted Laser Desorption/Ionization-Time of Flight Mass Spectroscopy (MALDI-TOF MS)

- Portable and In-Field Mass Spectroscopy

- Tandem Mass Spectroscopy (MS/MS)

- Ion Trap Mass Spectroscopy (LC/MS)

- Atomic Spectroscopy

- Atomic Absorbance Spectroscopy (AAS)

- X-Ray Fluorescence (XRF) Spectroscopy

- X-Ray Diffraction (XRD) Spectroscopy

- Other Atomic Spectroscopy Technologies

Note: Other atomic spectroscopy technologies segment includes inductively coupled plasma (ICP) spectroscopy, glow discharge spectroscopy, and arc/spark optical emission spectroscopy.

- Spectroscopy Software

- Microscopy

- Electron Microscopy

- Optical Microscopy

- Scanning Probe Microscopy

- Other Microscopy

- Microscopy Software

- Chromatography

- High-Performance Liquid Chromatography (HPLC)

- Gas Chromatography (GC)

- Low Pressure Liquid Chromatography (LPLC)

- Flash Chromatography

- Thin Layer Chromatography (TLC)

- Ion Chromatography

- Supercritical Fluid Chromatography (SFC)

- Chromatography Software

- Lab Automation

- Automated Workstations

- Robotic Systems

- Automated Storage and Retrieval Systems (ASRS)

- Lab Automation Software

- Immunoassay Analyzers

- Chemiluminescence Immunoassay

- Fluorescence Immunoassay

- Radioimmunoassay (RIA)

- Colorimetric Immunoassay

- Other Immunoassay Analyzers

- Immunoassay Software

- PCR

- RT-PCR

- Conventional PCR

- Digital PCR

- PCR Software

- Sequencing

- Flow Cytometry

- Cell-Based Flow Cytometers

- Bead-Based Flow Cytometers

- Flow Cytometry Software

- Incubators

- Microarray

- DNA Microarrays

- Protein Microarray

- Tissue Array

- Other Microarrays

- Microarray Software

Note: Other microarrays segment includes glycan microarray, carbohydrate microarray, and chemical compounds microarray.

- Centrifuges

- Centrifuges, by Type

- Devices

- Multipurpose Centrifuges

- Microcentrifuges

- Mini-centrifuges

- Ultracentrifuges

- Other Centrifuges

- Centrifuge Accessories

- Centrifuges, by Model

- Benchtop Centrifuges

- Floor-standing Centrifuges

- Centrifuges, by Application

- Research Applications

- Genomics

- Microbiology

- Cellomics

- Proteomics

- Clinical Applications

- Diagnostics

- Blood Processing and Screening

- Other Applications

- Electrophoresis

- Gel Electrophoresis

- Capillary Electrophoresis

- Gel Documentation Systems and Software

- Other Equipment

Note: Other equipment segment includes autoclaves, stirrers & shakers, mixers, baths, hot plates, ovens & furnaces, and balances.

Life Science Equipment Market Assessment -by End User

- Pharmaceutical and Biotechnology Industry

- Academic & Research Institutes

- Hospitals and Diagnostic Laboratories

- Analytical Testing Laboratories

- Agriculture and Food Industry

- Forensic Laboratories

- Other End Users

Note: Other end users include blood banks and industries, such as cosmetics, chemicals, oil & gas, electronics & semiconductors, automotive, aerospace, ceramics, plastics, rubber, and paints & coatings.

Life Science Equipment Market Assessment -by Geography

- North America

- U.S.

- Canada

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Switzerland

- Rest of Europe (RoE)

- Asia-Pacific (APAC)

- China

- Japan

- India

- South Korea

- Rest of APAC (RoAPAC)

- Latin America

- Brazil

- Mexico

- Rest of LATAM (RoLATAM)

- Middle East & Africa

- Saudi Arabia

- UAE

- Rest of Middle East & Africa (RoMEA)

TABLE OF CONTENTS

1. Introduction

- 1.1. Market Definition & Scope

- 1.2. Market Ecosystem

- 1.3. Currency And Limitations

- 1.4. Key Stakeholders

2. Research Methodology

- 2.1. Research Approach

- 2.2. Process of Data Collection and Validation

- 2.2.1. Secondary Research

- 2.2.2. Primary Research/Interviews with Key Opinion Leaders from the Industry

- 2.3. Market Sizing and Forecasting

- 2.3.1. Market Size Estimation Approach

- 2.3.2. Growth Forecast Approach

- 2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

- 4.1. Overview

- 4.2. Factors Affecting Market Growth

- 4.2.1. Impact Analysis Of Market Dynamics

- 4.2.2. Factor Analysis

- 4.3. Life Science Equipment Market: Regulatory Analysis

- 4.3.1. Overview

- 4.3.2. North America

- 4.3.3. Europe

- 4.3.4. Asia-Pacific

- 4.3.4.1. China

- 4.3.4.2. Japan

- 4.3.4.3. India

- 4.3.5. Latin America

- 4.3.6. Middle East & Africa

- 4.4. Pricing Analysis

- 4.5. Industry & Technology Trends

- 4.5.1. Increased Adoption Of Laboratory Automation And Robotics

- 4.5.2. Technological Advancements In High-Performance Liquid Chromatography (HPLC): UPLC, Automation, And Miniaturization

- 4.5.3. Increased Adoption Of Bioinformatics Solutions And Services In The Life Sciences Industry

- 4.5.4. Life Sciences Laboratories' Laboratory Downtime Minimization Using Cloud-Connected Laboratory Instruments

- 4.6. Porter's Five Forces Analysis

- 4.6.1. Bargaining Power Of Buyers

- 4.6.2. Bargaining Power Of Suppliers

- 4.6.3. Threat Of Substitutes

- 4.6.4. Threat Of New Entrants

- 4.6.5. Degree Of Competition

5. Life Science Equipment Market Assessment-by Technology

- 5.1. Overview

- 5.2. Spectroscopy

- 5.2.1. Molecular Spectroscopy

- 5.2.1.1. UV/Vis Spectroscopy

- 5.2.1.2. Nuclear Magnetic Resonance (NMR)

- 5.2.1.3. Near-Infrared (NIR) Spectroscopy

- 5.2.1.4. Infrared (IR) Spectroscopy

- 5.2.1.5. Raman Spectroscopy

- 5.2.1.6. Polarimeters and Refractometers

- 5.2.1.7. Fluorescence & Luminescence Spectroscopy

- 5.2.1.8. Other Molecular Spectroscopy Technologies

- 5.2.2. Mass Spectrometry

- 5.2.2.1. Quadrupole LC/MS

- 5.2.2.2. Time of Flight LC/MS (Q-TOF & LC-TOF)

- 5.2.2.3. Gas Chromatography-Mass Spectrometry (GC/MS)

- 5.2.2.4. Fourier Transform Mass Spectrometry (FT/MS)

- 5.2.2.5. Matrix-Assisted Laser Desorption/Ionization-Time of Flight Mass Spectroscopy (MALDI-TOF MS)

- 5.2.2.6. Portable and In-Field Mass Spectroscopy

- 5.2.2.7. Tandem Mass Spectroscopy (MS/MS)

- 5.2.2.8. Ion Trap Mass Spectroscopy (LC/MS)

- 5.2.3. Atomic Spectroscopy

- 5.2.3.1. Atomic Absorbance Spectroscopy (AAS)

- 5.2.3.2. X-Ray Fluorescence (XRF) Spectroscopy

- 5.2.3.3. X-Ray Diffraction (XRD) Spectroscopy

- 5.2.3.4. Other Atomic Spectroscopy Technologies

- 5.2.4. Spectroscopy Software

- 5.2.1. Molecular Spectroscopy

- 5.3. Microscopy

- 5.3.1. Electron Microscopy

- 5.3.2. Optical Microscopy

- 5.3.3. Scanning Probe Microscopy

- 5.3.4. Other Microscopy

- 5.3.5. Microscopy Software

- 5.4. Chromatography

- 5.4.1. High-Performance Liquid Chromatography (HPLC)

- 5.4.2. Gas Chromatography (GC)

- 5.4.3. Low Pressure Liquid Chromatography (LPLC)

- 5.4.4. Flash Chromatography

- 5.4.5. Thin Layer Chromatography (TLC)

- 5.4.6. Ion Chromatography

- 5.4.7. Supercritical Fluid Chromatography (SFC)

- 5.4.8. Chromatography Software

- 5.5. Lab Automation

- 5.5.1. Automated Workstations

- 5.5.2. Robotic Systems

- 5.5.3. Automated Storage and Retrieval Systems (ASRS)

- 5.5.4. Lab Automation Software

- 5.6. Immunoassay Analyzers