|

|

市場調査レポート

商品コード

1526810

作動油の世界市場:販売場所別、基油別、用途別、最終用途産業別、地域別 - 2029年までの予測Hydraulic Fluids Market by Base Oil (Mineral Oil, Synthetic Oil), Point of Sale (OEM and Aftermarket), Application (Mobile Equipment), End-use Industry (Construction, Agriculture, Transportation, Metal & Mining), and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 作動油の世界市場:販売場所別、基油別、用途別、最終用途産業別、地域別 - 2029年までの予測 |

|

出版日: 2024年07月30日

発行: MarketsandMarkets

ページ情報: 英文 299 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

作動油の市場規模は、2024年の87億米ドルから2029年には102億米ドルに成長し、CAGRは3.2%になると予測されています。

中東・アフリカとアジア太平洋における産業成長の高まり、最終用途産業における自動化の進展、加工食品需要の高まりが、作動油市場を牽引しています。また、鉱物油ベースの潤滑油に関連する健康被害への意識が高まるにつれ、合成潤滑油やバイオベースの潤滑油の代替品への要望が高まっています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2018年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 対象ユニット | 数量(キロトン)および金額(100万米ドル) |

| セグメント | 販売場所別、基油別、用途別、最終用途産業別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

作動油市場の最大の用途はモバイル機器です。油圧産業は、金属・鉱業、農業、建設、発電、セメント製造など、あらゆる産業に広がっています。これらの産業では、掘削機、ローダー、トラクター、クレーン、フォークリフトなど、さまざまな移動機械が主に使用されています。これらの機械はすべて、動力伝達と制御に不可欠な油圧システムを動力源としています。世界のインフラプロジェクト、ビル建設作業、農業省力化機械の応用の拡大が、移動機械における作動油の需要拡大の主な要因となっています。

金属・鉱業は、円滑な操業とメンテナンスのために様々な機器に幅広く依存しているため、作動油市場において2番目に大きなエンドユーザー産業となっています。これらの機器には、掘削機、ダンプトラック、クレーン、破砕機などが含まれます。金属・鉱業は様々な重機械や機器に大きく依存しており、過酷な条件下で効率的に稼動するためには継続的な潤滑が必要です。継続的な操業、安全への懸念、世界の金属需要により、金属・鉱業は依然として作動油の使用量第2位のセクターです。

予測期間中、中東・アフリカは2番目に急成長する市場と予想されており、石油化学および下流産業も同様に中東・アフリカの作動油市場を促進すると期待されています。これは主に、鉱業、石油探査産業、自動車、農業における工業化とインフラ整備の高まりによるものです。さらに、これらの地域では、インフラ整備や都市化に対する関心が高まっており、そのため機械や設備に使用される作動油の需要が高まり、2024年から2029年の予測期間中に市場が拡大することが予想されます。

当レポートでは、世界の作動油市場について調査し、販売場所別、基油別、用途別、最終用途産業別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- ポーターのファイブフォース分析

- マクロ経済指標

第6章 業界の動向

- 主な利害関係者と購入基準

- サプライチェーン分析

- エコシステム分析/市場マップ

- ケーススタディ分析

- 規制状況

- 技術分析

- 顧客ビジネスに影響を与える動向/混乱

- 貿易分析

- 2024年~2025年の主な会議とイベント

- 価格分析

- 投資と資金調達のシナリオ

- 特許分析

第7章 作動油市場(販売場所別)

- イントロダクション

- メーカー

- アフターマーケット

第8章 作動油市場(基油別)

- イントロダクション

- 鉱油

- 合成油

- バイオベースオイル

第9章 作動油市場(用途別)

- イントロダクション

- 移動機器

- 産業機器

第10章 作動油市場(最終用途産業別)

- イントロダクション

- 建設

- 金属・鉱業

- 農業

- 石油ガス

- 輸送

- セメント生産

- 食品加工

- 発電

- その他

第11章 作動油市場(地域別)

- イントロダクション

- アジア太平洋

- 欧州

- 北米

- 中東・アフリカ

- 南米

第12章 競合情勢

- イントロダクション

- 主要参入企業の戦略

- 収益分析

- 市場シェア分析

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 企業価値評価と財務指標

- ブランド/製品比較分析

- 競争状況と動向

第13章 企業プロファイル

- 主要参入企業

- EXXON MOBIL CORPORATION

- TOTALENERGIES SE

- SHELL PLC

- CHEVRON CORPORATION

- BP P.L.C.

- FUCHS SE

- CHINA PETROLEUM & CHEMICAL CORPORATION

- ENEOS HOLDINGS, INC.

- IDEMITSU KOSAN CO., LTD.

- PETROCHINA COMPANY LIMITED

- その他の企業

- PETROLIAM NASIONAL BERHAD(PETRONAS)

- LUKOIL

- PT PERTAMINA(PERSERO)

- INDIAN OIL CORPORATION LIMITED

- HINDUSTAN PETROLEUM CORPORATION LIMITED

- PHILLIPS 66

- PETROLEO BRASILEIRO S.A.(PETROBRAS)

- BALMER LAWRIE & CO. LTD.

- PJSC ROSNEFT OIL COMPANY

- LUBRI-LAB INC.

- CALUMET SPECIALTY PRODUCTS PARTNERS, L.P.

- CITGO PETROLEUM CORPORATION

- HARRISON MANUFACTURING PTY LIMITED

- NYCO

- PENRITE OIL

第14章 隣接市場と関連市場

第15章 付録

List of Tables

- TABLE 1 HYDRAULIC FLUIDS MARKET: RISK ASSESSMENT

- TABLE 2 INDUSTRIAL GROWTH RATE OF COUNTRIES IN ASIA PACIFIC, 2023

- TABLE 3 TOP FIVE MOTOR VEHICLE PRODUCERS IN ASIA PACIFIC, 2023

- TABLE 4 CRUDE OIL PRICE TREND (2019-2022)

- TABLE 5 HYDRAULIC FLUIDS MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 GDP TRENDS AND FORECAST OF MAJOR ECONOMIES, 2021-2029 (USD BILLION)

- TABLE 7 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES (%)

- TABLE 8 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

- TABLE 9 HYDRAULIC FLUIDS MARKET: ROLE IN ECOSYSTEM

- TABLE 10 NORTH AMERICA: REGULATIONS FOR HYDRAULIC FLUIDS

- TABLE 11 EUROPE: REGULATIONS FOR HYDRAULIC FLUIDS

- TABLE 12 ASIA PACIFIC: REGULATIONS FOR HYDRAULIC FLUIDS

- TABLE 13 MIDDLE EAST & AFRICA: REGULATIONS FOR HYDRAULIC FLUIDS

- TABLE 14 SOUTH AMERICA: REGULATIONS FOR HYDRAULIC FLUIDS

- TABLE 15 IMPORT OF HYDRAULIC FLUIDS, BY REGION, 2018-2022 (USD BILLION)

- TABLE 16 EXPORT OF HYDRAULIC FLUIDS, BY REGION, 2018-2022 (USD BILLION)

- TABLE 17 HYDRAULIC FLUIDS MARKET: KEY CONFERENCES & EVENTS, 2024-2025

- TABLE 18 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR TOP THREE BASE OIL TYPES (USD/KG)

- TABLE 19 AVERAGE SELLING PRICE TREND OF HYDRAULIC FLUIDS, BY REGION, 2022-2029 (USD/KG)

- TABLE 20 PATENT STATUS: PATENT APPLICATIONS, LIMITED PATENTS, AND GRANTED PATENTS

- TABLE 21 MAJOR PATENTS FOR HYDRAULIC FLUIDS

- TABLE 22 PATENTS BY HALLIBURTON ENERGY SERVICES, INC.

- TABLE 23 PATENTS BY SAUDI ARABIAN OIL COMPANY

- TABLE 24 TOP 10 PATENT OWNERS IN US, 2013-2023

- TABLE 25 HYDRAULIC FLUIDS MARKET, BY POINT OF SALE, 2018-2022 (USD MILLION)

- TABLE 26 HYDRAULIC FLUIDS MARKET, BY POINT OF SALE, 2023-2029 (USD MILLION)

- TABLE 27 HYDRAULIC FLUIDS MARKET, BY POINT OF SALE, 2018-2022 (KILOTON)

- TABLE 28 HYDRAULIC FLUIDS MARKET, BY POINT OF SALE, 2023-2029 (KILOTON)

- TABLE 29 BASE OIL DESCRIPTION, BY CATEGORY

- TABLE 30 HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 31 HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 32 HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 33 HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 34 MINERAL OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 35 MINERAL OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 36 MINERAL OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 37 MINERAL OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 38 SYNTHETIC OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 39 SYNTHETIC OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 40 SYNTHETIC OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 41 SYNTHETIC OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 42 BIO-BASED OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 43 BIO-BASED OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 44 BIO-BASED OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 45 BIO-BASED OIL: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 46 HYDRAULIC FLUIDS MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 47 HYDRAULIC FLUIDS MARKET, BY APPLICATION, 2023-2029 (USD MILLION)

- TABLE 48 HYDRAULIC FLUIDS MARKET, BY APPLICATION, 2018-2022 (KILOTON)

- TABLE 49 HYDRAULIC FLUIDS MARKET, BY APPLICATION, 2023-2029 (KILOTON)

- TABLE 50 HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 51 HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 52 HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 53 HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 54 CONSTRUCTION: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 55 CONSTRUCTION: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 56 CONSTRUCTION: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 57 CONSTRUCTION: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 58 METAL & MINING: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 59 METAL & MINING: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 60 METAL & MINING: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 61 METAL & MINING: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 62 AGRICULTURE: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 63 AGRICULTURE: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 64 AGRICULTURE: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 65 AGRICULTURE: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 66 OIL & GAS: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 67 OIL & GAS: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 68 OIL & GAS: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 69 OIL & GAS: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 70 TRANSPORTATION: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 71 TRANSPORTATION: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 72 TRANSPORTATION: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 73 TRANSPORTATION: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 74 CEMENT PRODUCTION: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 75 CEMENT PRODUCTION: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 76 CEMENT PRODUCTION: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 77 CEMENT PRODUCTION: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 78 FOOD PROCESSING: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 79 FOOD PROCESSING: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 80 FOOD PROCESSING: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 81 FOOD PROCESSING: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 82 POWER GENERATION: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 83 POWER GENERATION: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 84 POWER GENERATION: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 85 POWER GENERATION: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 86 OTHER END-USE INDUSTRIES: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 87 OTHER END-USE INDUSTRIES: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 88 OTHER END-USE INDUSTRIES: HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 89 OTHER END-USE INDUSTRIES: HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 90 HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 91 HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 92 HYDRAULIC FLUIDS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 93 HYDRAULIC FLUIDS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 94 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 95 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 96 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 97 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 98 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 99 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 100 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 101 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 102 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 103 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (USD MILLION)

- TABLE 104 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 105 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (KILOTON)

- TABLE 106 CHINA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 107 CHINA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 108 CHINA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 109 CHINA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 110 INDIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 111 INDIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 112 INDIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 113 INDIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 114 JAPAN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 115 JAPAN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 116 JAPAN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 117 JAPAN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 118 SOUTH KOREA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 119 SOUTH KOREA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 120 SOUTH KOREA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 121 SOUTH KOREA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 122 AUSTRALIA & NEW ZEALAND: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 123 AUSTRALIA & NEW ZEALAND: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 124 AUSTRALIA & NEW ZEALAND: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 125 AUSTRALIA & NEW ZEALAND: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 126 THAILAND: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 127 THAILAND: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 128 THAILAND: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 129 THAILAND: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 130 INDONESIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 131 INDONESIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 132 INDONESIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 133 INDONESIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 134 EUROPE: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 135 EUROPE: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 136 EUROPE: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 137 EUROPE: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 138 EUROPE: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 139 EUROPE: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 140 EUROPE: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 141 EUROPE: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 142 EUROPE: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 143 EUROPE: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (USD MILLION)

- TABLE 144 EUROPE: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 145 EUROPE: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (KILOTON)

- TABLE 146 RUSSIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 147 RUSSIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 148 RUSSIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 149 RUSSIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 150 GERMANY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 151 GERMANY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 152 GERMANY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 153 GERMANY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 154 UK: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 155 UK: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 156 UK: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 157 UK: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 158 FRANCE: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 159 FRANCE: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 160 FRANCE: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 161 FRANCE: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 162 ITALY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 163 ITALY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 164 ITALY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 165 ITALY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 166 SPAIN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 167 SPAIN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 168 SPAIN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 169 SPAIN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 170 TURKEY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 171 TURKEY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 172 TURKEY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 173 TURKEY: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 174 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 175 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 176 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 177 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 178 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 179 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 180 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 181 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 182 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 183 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (USD MILLION)

- TABLE 184 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 185 NORTH AMERICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (KILOTON)

- TABLE 186 US: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 187 US: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 188 US: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 189 US: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 190 CANADA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 191 CANADA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 192 CANADA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 193 CANADA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 194 MEXICO: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 195 MEXICO: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 196 MEXICO: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 197 MEXICO: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 198 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 199 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 200 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 201 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 202 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 203 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 204 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 205 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 206 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 207 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (USD MILLION)

- TABLE 208 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 209 MIDDLE EAST & AFRICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (KILOTON)

- TABLE 210 SAUDI ARABIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 211 SAUDI ARABIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 212 SAUDI ARABIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 213 SAUDI ARABIA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 214 SOUTH AFRICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 215 SOUTH AFRICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 216 SOUTH AFRICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 217 SOUTH AFRICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 218 IRAN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 219 IRAN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 220 IRAN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 221 IRAN: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 222 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 223 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 224 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 225 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 226 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 227 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 228 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 229 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 230 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 231 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (USD MILLION)

- TABLE 232 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 233 SOUTH AMERICA: HYDRAULIC FLUIDS MARKET, BY COUNTRY, 2023-2029 (KILOTON)

- TABLE 234 BRAZIL: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 235 BRAZIL: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 236 BRAZIL: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 237 BRAZIL: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 238 ARGENTINA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 239 ARGENTINA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (USD MILLION)

- TABLE 240 ARGENTINA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 241 ARGENTINA: HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY, 2023-2029 (KILOTON)

- TABLE 242 OVERVIEW OF STRATEGIES ADOPTED BY KEY HYDRAULIC FLUID MANUFACTURERS

- TABLE 243 HYDRAULIC FLUIDS MARKET: DEGREE OF COMPETITION

- TABLE 244 HYDRAULIC FLUIDS MARKET: REGION FOOTPRINT

- TABLE 245 HYDRAULIC FLUIDS MARKET: BASE OIL FOOTPRINT

- TABLE 246 HYDRAULIC FLUIDS MARKET: APPLICATION FOOTPRINT

- TABLE 247 HYDRAULIC FLUIDS MARKET: POINT OF SALE FOOTPRINT

- TABLE 248 HYDRAULIC FLUIDS MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 249 HYDRAULIC FLUIDS MARKET: PRODUCT LAUNCHES, JANUARY 2019-JUNE 2024

- TABLE 250 HYDRAULIC FLUIDS MARKET: DEALS, JANUARY 2019-JUNE 2024

- TABLE 251 HYDRAULIC FLUIDS MARKET: EXPANSION, JANUARY 2019-JUNE 2024

- TABLE 252 EXXON MOBIL CORPORATION: COMPANY OVERVIEW

- TABLE 253 EXXON MOBIL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 254 EXXON MOBIL CORPORATION: PRODUCT LAUNCHES

- TABLE 255 EXXON MOBIL CORPORATION: DEALS

- TABLE 256 EXXON MOBIL CORPORATION: EXPANSIONS

- TABLE 257 TOTALENERGIES SE: COMPANY OVERVIEW

- TABLE 258 TOTALENERGIES SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 259 TOTALENERGIES SE: PRODUCT LAUNCHES

- TABLE 260 TOTALENERGIES SE: DEALS

- TABLE 261 TOTALENERGIES SE: EXPANSIONS

- TABLE 262 SHELL PLC: COMPANY OVERVIEW

- TABLE 263 SHELL PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 264 SHELL PLC: PRODUCT LAUNCHES

- TABLE 265 SHELL PLC: DEALS

- TABLE 266 SHELL PLC: EXPANSIONS

- TABLE 267 CHEVRON CORPORATION: COMPANY OVERVIEW

- TABLE 268 CHEVRON CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 269 CHEVRON CORPORATION: DEALS

- TABLE 270 CHEVRON CORPORATION: EXPANSIONS

- TABLE 271 BP P.L.C.: COMPANY OVERVIEW

- TABLE 272 BP P.L.C.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 273 BP P.L.C.: EXPANSIONS

- TABLE 274 FUCHS SE: COMPANY OVERVIEW

- TABLE 275 FUCHS SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 276 FUCHS SE: DEALS

- TABLE 277 FUCHS SE: EXPANSIONS

- TABLE 278 CHINA PETROLEUM & CHEMICAL CORPORATION: COMPANY OVERVIEW

- TABLE 279 CHINA PETROLEUM & CHEMICAL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 280 CHINA PETROLEUM & CHEMICAL CORPORATION: DEALS

- TABLE 281 CHINA PETROLEUM & CHEMICAL CORPORATION: EXPANSIONS

- TABLE 282 ENEOS HOLDINGS, INC.: COMPANY OVERVIEW

- TABLE 283 ENEOS HOLDINGS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 284 ENEOS HOLDINGS, INC.: DEALS

- TABLE 285 ENEOS HOLDINGS, INC.: EXPANSIONS

- TABLE 286 IDEMITSU KOSAN CO., LTD.: COMPANY OVERVIEW

- TABLE 287 IDEMITSU KOSAN CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 288 IDEMITSU KOSAN CO., LTD.: DEALS

- TABLE 289 IDEMITSU KOSAN CO., LTD.: EXPANSIONS

- TABLE 290 PETROCHINA COMPANY LIMITED: COMPANY OVERVIEW

- TABLE 291 PETROCHINA COMPANY LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 292 PETROCHINA COMPANY LIMITED: DEALS

- TABLE 293 PETROLIAM NASIONAL BERHAD (PETRONAS): COMPANY OVERVIEW

- TABLE 294 LUKOIL: COMPANY OVERVIEW

- TABLE 295 PT PERTAMINA (PERSERO): COMPANY OVERVIEW

- TABLE 296 INDIAN OIL CORPORATION LIMITED: COMPANY OVERVIEW

- TABLE 297 HINDUSTAN PETROLEUM CORPORATION LIMITED: COMPANY OVERVIEW

- TABLE 298 PHILLIPS 66: COMPANY OVERVIEW

- TABLE 299 PETROLEO BRASILEIRO S.A. (PETROBRAS): COMPANY OVERVIEW

- TABLE 300 BALMER LAWRIE & CO. LTD.: COMPANY OVERVIEW

- TABLE 301 PJSC ROSNEFT OIL COMPANY: COMPANY OVERVIEW

- TABLE 302 LUBRI-LAB INC.: COMPANY OVERVIEW

- TABLE 303 CALUMET SPECIALTY PRODUCTS PARTNERS, L.P.: COMPANY OVERVIEW

- TABLE 304 CITGO PETROLEUM CORPORATION: COMPANY OVERVIEW

- TABLE 305 HARRISON MANUFACTURING PTY LIMITED: COMPANY OVERVIEW

- TABLE 306 NYCO: COMPANY OVERVIEW

- TABLE 307 PENRITE OIL: COMPANY OVERVIEW

- TABLE 308 INDUSTRIAL LUBRICANTS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 309 INDUSTRIAL LUBRICANTS MARKET, BY REGION, 2023-2029 (USD MILLION)

- TABLE 310 INDUSTRIAL LUBRICANTS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 311 INDUSTRIAL LUBRICANTS MARKET, BY REGION, 2023-2029 (KILOTON)

- TABLE 312 ASIA PACIFIC: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 313 ASIA PACIFIC: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 314 ASIA PACIFIC: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 315 ASIA PACIFIC: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 316 NORTH AMERICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 317 NORTH AMERICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 318 NORTH AMERICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 319 NORTH AMERICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 320 EUROPE: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 321 EUROPE: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 322 EUROPE: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 323 EUROPE: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 324 MIDDLE EAST & AFRICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 325 MIDDLE EAST & AFRICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 326 MIDDLE EAST & AFRICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 327 MIDDLE EAST & AFRICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

- TABLE 328 SOUTH AMERICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (USD MILLION)

- TABLE 329 SOUTH AMERICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (USD MILLION)

- TABLE 330 SOUTH AMERICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2018-2022 (KILOTON)

- TABLE 331 SOUTH AMERICA: INDUSTRIAL LUBRICANTS MARKET, BY BASE OIL, 2023-2029 (KILOTON)

List of Figures

- FIGURE 1 HYDRAULIC FLUIDS MARKET SEGMENTATION

- FIGURE 2 HYDRAULIC FLUIDS MARKET: RESEARCH DESIGN

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE): COLLECTIVE SHARE OF MAJOR PLAYERS

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2 (SUPPLY SIDE): COLLECTIVE REVENUE OF ALL PRODUCTS (BOTTOM-UP)

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 3 - BOTTOM UP (DEMAND SIDE): PRODUCTS SOLD

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 7 HYDRAULIC FLUIDS MARKET: DATA TRIANGULATION

- FIGURE 8 MARKET GROWTH PROJECTION FROM SUPPLY SIDE

- FIGURE 9 MARKET GROWTH PROJECTION FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES

- FIGURE 10 AFTERMARKET SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 11 SYNTHETIC OIL TO BE FASTEST-GROWING BASE OIL SEGMENT DURING FORECAST PERIOD

- FIGURE 12 CONSTRUCTION INDUSTRY TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 13 ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARE IN 2023

- FIGURE 14 HYDRAULIC FLUIDS MARKET TO WITNESS STEADY GROWTH DURING FORECAST PERIOD

- FIGURE 15 CHINA AND MINERAL OIL SEGMENT LED MARKET IN 2023

- FIGURE 16 ASIA PACIFIC TO BE LARGEST MARKET FOR HYDRAULIC FLUIDS DURING FORECAST PERIOD

- FIGURE 17 CONSTRUCTION END-USE INDUSTRY ACCOUNTED FOR LARGEST MARKET SHARE IN 2023

- FIGURE 18 INDIA PROJECTED TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 19 FACTORS GOVERNING HYDRAULIC FLUIDS MARKET

- FIGURE 20 HYDRAULIC FLUIDS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

- FIGURE 22 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

- FIGURE 23 HYDRAULIC FLUIDS MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 24 HYDRAULIC FLUIDS MARKET: ECOSYSTEM ANALYSIS/MARKET MAP

- FIGURE 25 HYDRAULIC FLUIDS MARKET: FUTURE REVENUE MIX

- FIGURE 26 HYDRAULIC FLUIDS IMPORT, BY KEY COUNTRY (2018-2022)

- FIGURE 27 HYDRAULIC FLUIDS EXPORT, BY KEY COUNTRY (2018-2022)

- FIGURE 28 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR TOP THREE BASE OIL TYPES

- FIGURE 29 AVERAGE SELLING PRICE TREND OF HYDRAULIC FLUIDS, BY REGION (2022-2029)

- FIGURE 30 PATENTS REGISTERED, 2013-2023

- FIGURE 31 LIST OF MAJOR PATENTS FOR HYDRAULIC FLUIDS

- FIGURE 32 LEGAL STATUS OF PATENTS FILED FOR HYDRAULIC FLUIDS

- FIGURE 33 MAXIMUM PATENTS FILED IN JURISDICTION OF US

- FIGURE 34 AFTERMARKET SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 35 SYNTHETIC OIL-BASED HYDRAULIC FLUIDS TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 36 MOBILE EQUIPMENT SEGMENT TO BE LARGEST APPLICATION OF HYDRAULIC FLUIDS DURING FORECAST PERIOD

- FIGURE 37 CONSTRUCTION END-USE INDUSTRY TO LEAD HYDRAULIC FLUIDS MARKET DURING FORECAST PERIOD

- FIGURE 38 ASIA PACIFIC TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 39 ASIA PACIFIC: HYDRAULIC FLUIDS MARKET SNAPSHOT

- FIGURE 40 EUROPE: HYDRAULIC FLUIDS MARKET SNAPSHOT

- FIGURE 41 NORTH AMERICA: HYDRAULIC FLUIDS MARKET SNAPSHOT

- FIGURE 42 REVENUE ANALYSIS OF KEY COMPANIES (2019-2023)

- FIGURE 43 SHELL PLC DOMINATED HYDRAULIC FLUIDS MARKET IN 2023

- FIGURE 44 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- FIGURE 45 HYDRAULIC FLUIDS MARKET: COMPANY FOOTPRINT

- FIGURE 46 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- FIGURE 47 COMPANY VALUATION AND FINANCIAL METRICS OF KEY PLAYERS

- FIGURE 48 EV/EBITDA OF KEY PLAYERS

- FIGURE 49 EXXON MOBIL CORPORATION: COMPANY SNAPSHOT

- FIGURE 50 TOTALENERGIES SE: COMPANY SNAPSHOT

- FIGURE 51 SHELL PLC: COMPANY SNAPSHOT

- FIGURE 52 CHEVRON CORPORATION: COMPANY SNAPSHOT

- FIGURE 53 BP P.L.C.: COMPANY SNAPSHOT

- FIGURE 54 FUCHS SE: COMPANY SNAPSHOT

- FIGURE 55 CHINA PETROLEUM & CHEMICAL CORPORATION: COMPANY SNAPSHOT

- FIGURE 56 ENEOS HOLDINGS, INC.: COMPANY SNAPSHOT

- FIGURE 57 IDEMITSU KOSAN CO., LTD.: COMPANY SNAPSHOT

- FIGURE 58 PETROCHINA COMPANY LIMITED: COMPANY SNAPSHOT

In terms of value, the hydraulic fluids market is estimated to grow from USD 8.7 billion in 2024 to USD 10.2 billion by 2029, at a CAGR of 3.2%. The rising industrial growth in the Middle East & Africa and Asia Pacific, growing automating in end-use industries, mounting demand from for processed foods are driving the hydraulic fluids market. Also, as individuals become more conscious of the probable health hazards linked to mineral oil based lubricants, there is an growing desire for synthetic and bio-based lubricant alternatives.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2018-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Volume (Kiloton) and Value (USD Million) |

| Segments | Base Oil Type, Point of Sale, Application, By End-use Industry, and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

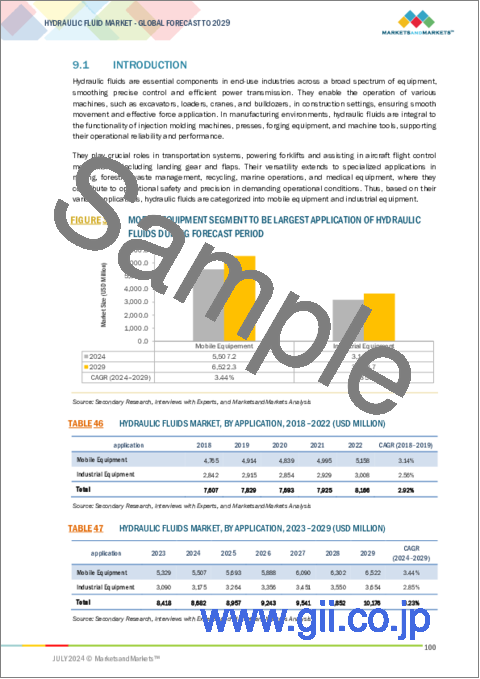

"Mobile Equipment was the largest application of hydraulic fluids market, in terms of value, in 2023."

Mobile equipment is the largest application of hydraulic fluids market. The hydraulic industry has spread to the whole set of industries from the metal & mining, agriculture, construction, power generation, cement production, and others. These industries are mostly using various mobile machinery such as excavators, loaders, tractors, cranes, forklifts, and others. All of these machines are powered by hydraulic systems, which are essential for power transmission and control. The growth of infrastructure projects, building construction operations, and the application of agricultural labor-saving machinery worldwide are the major factors behind the growing demand for hydraulic fluids in the mobile equipment.

"Metal & mining was the second largest end-use industry of the hydraulic fluids market, in terms of value, in 2023."

Metal & mining stands as the second largest end-user industry in the hydraulic fluids market due to its extensive reliance on various equipments for smooth operation and maintenance. These equipments includes excavators, dump trucks, cranes, crushers, and others. The metal & mining industry is heavily relies on various heavy machinery and equipment, which require continuous lubrication to operate efficiently in harsh conditions. With continuous operations, safety concerns, and a global metal demand, metal & mining remains a second largest sector for hydraulic fluids usage.

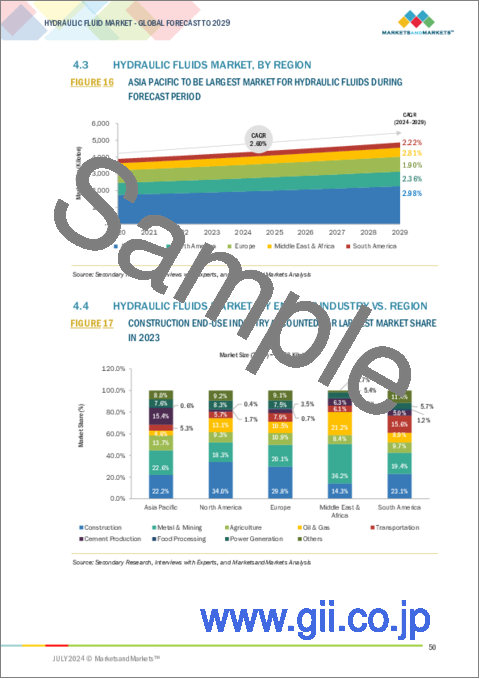

"The Middle East & AFrica is projected to be the second fastest-growing region, during the forecast period in the hydraulic fluids market."

Petrochemical and downstream industries are equally expected to foster the hydraulic fluids market in the Middle East and Africa as it is expected to be the second fastest growing market during forecast period. This mainly because of the rising industrialization and infrastructure development in mining, oil exploration industries, automobiles and agriculture. Moreover, from these regions, there is the increasing interest in infrastructural development and urbanization and hence, the subsequent demand for hydraulic fluids to be used in the machinery and equipments would enable the market expand in during forecast period 2024 to 2029..

- By Company Type: Tier 1 - 69%, Tier 2 - 23%, and Tier 3 - 8%

- By Designation: C-Level - 23%, Director Level - 37%, and Others - 40%

- By Region: North America - 24%, Europe - 40%, Asia Pacific - 17%, South America - 7%, Middle East & Africa - 12%,

The key players profiled in the report include Shell plc (UK), Exxon Mobil Corporation (US), BP p.l.c. (UK), Chevron Corporation (US), TotalEnergies SE (France), FUCHS SE (Germany), PetroChina Company Limited (China), ENEOS Holdings, Inc. (Japan), China Petroleum & Chemical Corporation (China), Idemitsu Kosan Co., Ltd. (Japan), and among others.

Research Coverage

This report segments the market for hydraulic fluids based on base oil type, point of sale, application, end-use industry, and region and provides estimations of volume (Kiloton) and value (USD Million) for the overall market size across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, services, and key strategies, associated with the market for hydraulic fluids.

Reasons to Buy this Report

This research report is focused on various levels of analysis - industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the hydraulic fluids market; high-growth regions; and market drivers, restraints, and opportunities.

The report provides insights on the following pointers:

- Market Penetration: Comprehensive information on hydraulic fluids offered by top players in the global market

- Analysis of key drives: (growing automating in end-use industries, mounting demand from for processed foods, rising industrial growth in the Middle East & Africa and Asia Pacific, and increasing demand from mining, construction, agriculture and marine industries), restraints (Swing towards synthetic lubricants, high price of bio-based and synthetic lubricants), opportunities (Mounting demand for bio-based lubricants, and increasing demand for renewable energy), and challenges (Escalating raw material prices) influencing the growth of hydraulic fluids market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the hydraulic fluids market

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for hydraulic fluids across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global hydraulic fluids market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the hydraulic fluids market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 HYDRAULIC FLUIDS MARKET: INCLUSIONS & EXCLUSIONS

- 1.2.2 HYDRAULIC FLUIDS MARKET: MARKET DEFINITIONS & INCLUSIONS, BY BASE OIL

- 1.2.3 HYDRAULIC FLUIDS MARKET: MARKET DEFINITIONS & INCLUSIONS, BY POINT OF SALE

- 1.2.4 HYDRAULIC FLUIDS MARKET: MARKET DEFINITIONS & INCLUSIONS, BY APPLICATION

- 1.2.5 HYDRAULIC FLUIDS MARKET: MARKET DEFINITIONS & INCLUSIONS, BY END-USE INDUSTRY

- 1.3 STUDY SCOPE

- 1.3.1 REGIONS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.3.4 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 RECESSION IMPACT

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary participants

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of interviews with experts

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 GROWTH FORECAST

- 2.4.1 SUPPLY SIDE

- 2.4.2 DEMAND SIDE

- 2.5 IMPACT OF RECESSION

- 2.6 ASSUMPTIONS

- 2.7 LIMITATIONS

- 2.8 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HYDRAULIC FLUIDS MARKET

- 4.2 ASIA PACIFIC HYDRAULIC FLUIDS MARKET, BY BASE OIL AND COUNTRY

- 4.3 HYDRAULIC FLUIDS MARKET, BY REGION

- 4.4 HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY VS. REGION

- 4.5 HYDRAULIC FLUIDS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Massive industrial growth in Asia Pacific and Middle East & Africa

- 5.2.1.2 Growth of automotive industry in Asia Pacific

- 5.2.1.3 Increasing demand for hydraulic fluids in mining and construction sectors

- 5.2.1.4 Rising use of automation in various end-use industries

- 5.2.1.5 Growing demand for processed food

- 5.2.2 RESTRAINTS

- 5.2.2.1 Shift toward synthetic lubricants

- 5.2.2.2 High cost of synthetic & bio-based hydraulic fluids and stringent environmental regulations

- 5.2.2.3 Technological advancements in hybrid vehicles

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing demand for bio-based hydraulic fluids

- 5.2.3.2 Pressing need for semi-synthetic hydraulic fluids

- 5.2.3.3 Availability of zinc-free (ashless) hydraulic fluids

- 5.2.3.4 Rising demand for renewable energy

- 5.2.4 CHALLENGES

- 5.2.4.1 Volatile crude oil prices

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF SUBSTITUTES

- 5.3.2 THREAT OF NEW ENTRANTS

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 MACROECONOMIC INDICATORS

- 5.4.1 GDP TRENDS AND FORECAST FOR MAJOR ECONOMIES

6 INDUSTRY TRENDS

- 6.1 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.1.2 BUYING CRITERIA

- 6.2 SUPPLY CHAIN ANALYSIS

- 6.2.1 RAW MATERIAL SUPPLIERS

- 6.2.2 MANUFACTURERS

- 6.2.3 DISTRIBUTORS

- 6.2.4 END-USE INDUSTRIES

- 6.3 ECOSYSTEM ANALYSIS/MARKET MAP

- 6.4 CASE STUDY ANALYSIS

- 6.4.1 REDUCING OPERATING COSTS OF INJECTION MOLDING MACHINE USING HYDRAULIC FLUIDS

- 6.4.2 UPGRADING PERFORMANCE POTENTIAL OF INJECTION MOLDING MACHINES USING HYDRAULIC FLUIDS

- 6.4.3 SAVING ENERGY BY USING HYDRO-CRACKED BASE OIL FOR HYDRAULIC OILS

- 6.5 REGULATORY LANDSCAPE

- 6.5.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.6 TECHNOLOGY ANALYSIS

- 6.6.1 KEY TECHNOLOGY

- 6.6.1.1 Ester in hydraulic fluid

- 6.6.1.2 Central hydraulic fluid

- 6.6.1.3 Re-refining

- 6.6.1.4 Nanotechnology

- 6.6.2 COMPLEMENTARY TECHNOLOGY

- 6.6.2.1 SO2 scrubbing system

- 6.6.1 KEY TECHNOLOGY

- 6.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.7.1 REVENUE SHIFT & NEW REVENUE POCKETS IN HYDRAULIC FLUIDS MARKET

- 6.8 TRADE ANALYSIS

- 6.8.1 IMPORT SCENARIO

- 6.8.2 EXPORT SCENARIO

- 6.9 KEY CONFERENCES & EVENTS IN 2024-2025

- 6.10 PRICING ANALYSIS

- 6.10.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY BASE OIL TYPE

- 6.10.2 AVERAGE SELLING PRICE TREND, BY REGION

- 6.11 INVESTMENT AND FUNDING SCENARIO

- 6.12 PATENT ANALYSIS

- 6.12.1 APPROACH

- 6.12.2 DOCUMENT TYPES

- 6.12.3 TOP APPLICANTS

- 6.12.4 LEGAL STATUS

- 6.12.5 JURISDICTION ANALYSIS

7 HYDRAULIC FLUIDS MARKET, BY POINT OF SALE

- 7.1 INTRODUCTION

- 7.2 OEM

- 7.3 AFTERMARKET

8 HYDRAULIC FLUIDS MARKET, BY BASE OIL

- 8.1 INTRODUCTION

- 8.2 MINERAL OIL

- 8.2.1 LOW COST TO BOOST DEMAND FOR MINERAL OIL-BASED HYDRAULIC FLUIDS

- 8.3 SYNTHETIC OIL

- 8.3.1 SURGE IN INDUSTRIAL ACTIVITIES TO INCREASE DEMAND FOR HIGH-PERFORMANCE HYDRAULIC FLUIDS

- 8.3.2 POLYALPHAOLEFINS

- 8.3.3 POLYALKYLENE GLYCOLS

- 8.3.4 ESTERS

- 8.3.5 GROUP III

- 8.4 BIO-BASED OIL

- 8.4.1 RISING AWARENESS ABOUT BIO-BASED HYDRAULIC FLUIDS TO FUEL DEMAND

9 HYDRAULIC FLUIDS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 MOBILE EQUIPMENT

- 9.3 INDUSTRIAL EQUIPMENT

10 HYDRAULIC FLUIDS MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 CONSTRUCTION

- 10.2.1 RISING DEMAND IN CONSTRUCTION EQUIPMENT TO DRIVE MARKET

- 10.3 METAL & MINING

- 10.3.1 SURGE IN METAL PRODUCTION AND MINING ACTIVITIES TO BOOST MARKET

- 10.4 AGRICULTURE

- 10.4.1 GROWING GLOBAL FOOD DEMAND TO INCREASE NEED FOR HYDRAULIC FLUIDS

- 10.5 OIL & GAS

- 10.5.1 NEED FOR LONG-TERM STABILITY AND SMOOTH FUNCTIONING OF MACHINERY TO FUEL MARKET

- 10.6 TRANSPORTATION

- 10.6.1 GROWTH OF MARINE AND AVIATION INDUSTRIES TO DRIVE MARKET

- 10.6.2 MARINE

- 10.6.3 AVIATION

- 10.6.4 AUTOMOTIVE

- 10.7 CEMENT PRODUCTION

- 10.7.1 SURGE IN CONSTRUCTION ACTIVITIES TO DRIVE MARKET

- 10.8 FOOD PROCESSING

- 10.8.1 RISING AWARENESS ABOUT FOOD SAFETY TO DRIVE MARKET

- 10.9 POWER GENERATION

- 10.9.1 INCREASING USE OF RENEWABLE SOURCES FOR POWER GENERATION TO DRIVE MARKET

- 10.10 OTHER END-USE INDUSTRIES

11 HYDRAULIC FLUIDS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC

- 11.2.1 RECESSION IMPACT

- 11.2.2 CHINA

- 11.2.2.1 Increasing population and rapid industrialization to drive market

- 11.2.3 INDIA

- 11.2.3.1 Growing construction industry to boost market

- 11.2.4 JAPAN

- 11.2.4.1 Government's fiscal support for technological developments to drive market

- 11.2.5 SOUTH KOREA

- 11.2.5.1 Increasing demand from transportation end-use industry to drive market

- 11.2.6 AUSTRALIA & NEW ZEALAND

- 11.2.6.1 Growth of mining industry to drive demand for hydraulic fluids

- 11.2.7 THAILAND

- 11.2.7.1 Viable economic policies to drive market

- 11.2.8 INDONESIA

- 11.2.8.1 Established crude oil and mining sectors to boost market

- 11.3 EUROPE

- 11.3.1 RECESSION IMPACT

- 11.3.2 RUSSIA

- 11.3.2.1 Capacity expansion for producing crude oil products to boost market

- 11.3.3 GERMANY

- 11.3.3.1 Growth of food processing industry to boost market

- 11.3.4 UK

- 11.3.4.1 Government plans for infrastructure spending to drive market

- 11.3.5 FRANCE

- 11.3.5.1 Presence of established international companies to boost demand for hydraulic fluids

- 11.3.6 ITALY

- 11.3.6.1 Growth of manufacturing industry to fuel demand for hydraulic fluids

- 11.3.7 SPAIN

- 11.3.7.1 Rising demand for hydraulic fluids in energy and agriculture sector to drive market

- 11.3.8 TURKEY

- 11.3.8.1 Increase in automotive sales to boost market

- 11.4 NORTH AMERICA

- 11.4.1 RECESSION IMPACT

- 11.4.2 US

- 11.4.2.1 Strong industrial infrastructure and increasing environmental awareness to drive market

- 11.4.3 CANADA

- 11.4.3.1 Growth of automotive industry to drive market

- 11.4.4 MEXICO

- 11.4.4.1 Booming industrialization and rising population to increase demand for hydraulic fluids

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 RECESSION IMPACT

- 11.5.2 GCC COUNTRIES

- 11.5.2.1 Saudi Arabia

- 11.5.2.1.1 Growing oil & gas sector to drive market

- 11.5.2.1 Saudi Arabia

- 11.5.3 SOUTH AFRICA

- 11.5.3.1 Demand for platinum to boost market

- 11.5.4 IRAN

- 11.5.4.1 Rapid growth in industrial sectors to propel market

- 11.6 SOUTH AMERICA

- 11.6.1 RECESSION IMPACT

- 11.6.2 BRAZIL

- 11.6.2.1 Rapidly expanding economy stimulated by increasing investments to drive market

- 11.6.3 ARGENTINA

- 11.6.3.1 Developing mining industry to drive market

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Base oil footprint

- 12.5.5.4 Application footprint

- 12.5.5.5 Point of Sale footprint

- 12.5.5.6 End-use industry footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

- 12.6.5.1 Hydraulic fluids market: Key startups/SMEs

- 12.6.5.2 Hydraulic fluids market: Competitive benchmarking of key startups/SMEs

- 12.7 COMPANY VALUATION AND FINANCIAL METRICS

- 12.8 BRAND/PRODUCT COMPARISON ANALYSIS

- 12.9 COMPETITIVE SITUATION AND TRENDS

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY COMPANIES

- 13.1.1 EXXON MOBIL CORPORATION

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 TOTALENERGIES SE

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 SHELL PLC

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 CHEVRON CORPORATION

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Deals

- 13.1.4.3.2 Expansions

- 13.1.4.4 MnM View

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 BP P.L.C.

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Expansions

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 FUCHS SE

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Deals

- 13.1.6.3.2 Expansions

- 13.1.7 CHINA PETROLEUM & CHEMICAL CORPORATION

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.7.3.2 Expansions

- 13.1.8 ENEOS HOLDINGS, INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Deals

- 13.1.8.3.2 Expansions

- 13.1.9 IDEMITSU KOSAN CO., LTD.

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Deals

- 13.1.9.3.2 Expansions

- 13.1.10 PETROCHINA COMPANY LIMITED

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Deals

- 13.1.1 EXXON MOBIL CORPORATION

- 13.2 OTHER PLAYERS

- 13.2.1 PETROLIAM NASIONAL BERHAD (PETRONAS)

- 13.2.2 LUKOIL

- 13.2.3 PT PERTAMINA (PERSERO)

- 13.2.4 INDIAN OIL CORPORATION LIMITED

- 13.2.5 HINDUSTAN PETROLEUM CORPORATION LIMITED

- 13.2.6 PHILLIPS 66

- 13.2.7 PETROLEO BRASILEIRO S.A. (PETROBRAS)

- 13.2.8 BALMER LAWRIE & CO. LTD.

- 13.2.9 PJSC ROSNEFT OIL COMPANY

- 13.2.10 LUBRI-LAB INC.

- 13.2.11 CALUMET SPECIALTY PRODUCTS PARTNERS, L.P.

- 13.2.12 CITGO PETROLEUM CORPORATION

- 13.2.13 HARRISON MANUFACTURING PTY LIMITED

- 13.2.14 NYCO

- 13.2.15 PENRITE OIL

14 ADJACENT & RELATED MARKETS

- 14.1 INTRODUCTION

- 14.2 LIMITATIONS

- 14.3 INDUSTRIAL LUBRICANTS MARKET

- 14.3.1 MARKET DEFINITION

- 14.3.2 MARKET OVERVIEW

- 14.4 INDUSTRIAL LUBRICANTS MARKET, BY REGION

- 14.4.1 ASIA PACIFIC

- 14.4.2 NORTH AMERICA

- 14.4.3 EUROPE

- 14.4.4 MIDDLE EAST & AFRICA

- 14.4.5 SOUTH AMERICA

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS