|

|

市場調査レポート

商品コード

1426163

自動車用燃料電池の世界市場:車両タイプ別、コンポーネント別、燃料タイプ別、水素燃料ポイント別、走行距離別、出力別、容量別、特殊車両タイプ別、地域別 - 予測(~2030年)Automotive Fuel Cell Market by Vehicle Type (Buses, Trucks, LCVs, Passenger Cars), Component, Fuel Type, Hydrogen Fuel Points, Operating Miles, Power, Capacity, Specialized Vehicle Type and Region - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用燃料電池の世界市場:車両タイプ別、コンポーネント別、燃料タイプ別、水素燃料ポイント別、走行距離別、出力別、容量別、特殊車両タイプ別、地域別 - 予測(~2030年) |

|

出版日: 2024年02月12日

発行: MarketsandMarkets

ページ情報: 英文 331 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界の自動車用燃料電池の市場規模は、2024年の2億米ドルから2030年までに21億米ドルに達し、CAGRで48.0%の成長が予測されています。

低排出ガス車に対する需要の増加や、グリーンモビリティに対する需要の増加といったパラメーターが、市場を牽引します。さらに、水素駆動技術の進歩と燃料電池技術に対する政府の支援が、この市場に新たな機会を生み出す見込みです。市場におけるゼロエミッション車への需要の増加と政府の強力な支援により、多くの主要OEMがFCEVの研究開発に投資しています。水素燃料電池は、この数十年で急成長している技術です。多くの新しい技術開発が行われ、市場において自動車用燃料電池の需要を高めています。従来のEVとは異なり、FCEVは長距離走行が可能であり、長距離のEV通勤に使用されることが多いです。Toyota、Hyundai、Hondaのような企業は、過去20年間この技術開発をリードしてきました。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2024年~2030年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2030年 |

| 単位 | 10億米ドル |

| セグメント | タイプ、コンポーネント、燃料タイプ、水素燃料ポイント、走行距離、容量、容量、特殊車両タイプ、地域 |

| 対象地域 | アジアオセアニア、欧州、北米、その他の地域 |

「水素がFCEVでもっとも一般的に使用される燃料となります。」

水素は私たちの環境に自然に存在し、水(H2O)、炭化水素(例:メタン - CH4)、有機物のようなさまざまな形態で貯蔵されていますが、燃料として使用するために効率的に取り出すという点では課題があります。水素は、多様な国産の資源に由来する実行可能な代替燃料として脚光を浴びています。水素輸送市場は初期段階にありますが、政府と産業の共同活動は、クリーンで費用対効果が高く、安全な水素の生産と流通を実現することに集中しています。水素燃料電池は、水素の化学エネルギーを利用して電気を発生させ、使用時の副生成物は水だけです。一般的に自動車用に利用されているPEM燃料電池は、水素、メタノール、エタノールなどの燃料に対応しています。水素は、自動車用燃料電池にとってもっともクリーンな燃料オプションとして突出しています。現在、水素燃料電池車の需要は限られていますが、その主な理由はグリーン水素の供給が限られていることと、水素生産に化石燃料を使用していることです。この取り組みにより、各国での水素ステーションの設置が進み、生産が拡大すれば、水素燃料電池車の需要も増加すると予測されます。燃料としての水素の普及を妨げている課題は貯蔵です。水素は密度が低いため、化石燃料のように簡単に貯蔵できず、貯蔵前に圧縮と冷却が必要です。米国では、高温の水蒸気と天然ガスを組み合わせて水素を取り出す水蒸気改質が、依然として水素生産の主流となっています。風力や太陽光のような再生可能エネルギーを利用することで、その他のエネルギー生産形態に伴う有害な排出を軽減できるという利点があります。このため、貯蔵用の特殊なタンクが必要となり、自動車用途に水素燃料電池を使用する際のコストをさらに押し上げる要因となっています。目標は、燃料電池電気自動車(FCEV)への水素の普及を促進することです。現在、小型FCEVはわずかな量で徐々に消費者市場に参入しており、当初は国内と世界の特定地域のみです。さらに、水素市場は、バス、マテリアルハンドリング機器(フォークリフトなど)、GSE、中型・大型トラック、船舶、定置用途などのさまざまなセグメントで有望な成長を示しています。水素生産は大気環境に影響を与える排出ガスを発生させる可能性がありますが、水素で走るFCEVからの排気は水蒸気と暖かい空気だけであり、ゼロエミッション車に分類されることに注意しなければなりません。これは、小売消費者への小型車の購入や、カリフォルニア州での中型・大型バスとトラックの初期展開で具体化されており、北東部の州でも車両が利用できるようになる予定です。

当レポートでは、世界の自動車用燃料電池市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 自動車用燃料電池市場の企業にとって魅力的な機会

- 自動車用燃料電池市場:車両タイプ別

- 自動車用燃料電池市場:水素燃料ポイント別

- 自動車用燃料電池市場:容量別

- 自動車用燃料電池市場:コンポーネント別

- 自動車用燃料電池市場:走行距離別

- 自動車用燃料電池市場:地域別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 既存の/今後のFCEVモデル

- ケーススタディ分析

- 特許分析

- エコシステム分析

- 水素燃料サプライヤー

- Tier Iサプライヤー(燃料電池、関連部品メーカー)

- OEM

- サプライチェーン分析

- 燃料電池の価格設定の分析

- 顧客のビジネスに影響を与える動向と混乱

- 自動車セグメントにおける水素技術の展開のロードマップ

- 主要OEMによるFCEV発売予定

- 水素燃料自動車エコシステムにおけるステークホルダーの計画

- ビジネスモデル

- 技術分析

- 直接水素化ホウ素燃料電池

- 燃料電池ハイブリッド電気自動車

- 水素ICE

- 非貴金属触媒燃料電池

- パッケージ燃料電池システムモジュール

- 液体水素有機水素キャリアー

- 炭酸塩超構造固体燃料電池

- 規制情勢

- 北米

- 欧州

- アジアのオセアニア

- 規制機関、政府機関、その他の組織

- 主な会議とイベント(2024年~2025年)

- 主なステークホルダーと購入基準

- LCV

- バス

- トラック

- 購入プロセスにおける主なステークホルダー

- 購入基準

第6章 自動車用燃料電池市場:コンポーネント別

- イントロダクション

- 経営データ

- 燃料スタック

- 燃料プロセッサー

- パワーコンディショナー

- エアコンプレッサー

- 加湿器

- 重要考察

第7章 自動車用燃料電池市場:燃料タイプ別

- イントロダクション

- 水素

- メタノール

- エタノール

- 重要考察

第8章 自動車用燃料電池市場:水素燃料ポイント別

- イントロダクション

- 経営データ

- アジアオセアニア

- 欧州

- 北米

- 重要考察

第9章 自動車用燃料電池市場:走行距離別

- イントロダクション

- 経営データ

- 0~250マイル

- 251~500マイル

- 500マイル超

- 重要考察

第10章 自動車用燃料電池市場:容量別

- イントロダクション

- 経営データ

- 150KW未満

- 150~250KW

- 250KW超

- 重要考察

第11章 自動車用燃料電池市場:推進別

- イントロダクション

- 経営データ

- FCHEV

- FCEV

- 重要考察

第12章 自動車用燃料電池市場:特殊車両タイプ別

- イントロダクション

- マテリアルハンドリング車両

- 冷蔵トラック用補助電源ユニット

- 重要考察

第13章 自動車用燃料電池市場:車両タイプ別

- イントロダクション

- 経営データ

- 乗用車

- LCV

- バス

- トラック

- 重要考察

第14章 自動車用燃料電池市場:地域別

- イントロダクション

- アジアオセアニア

- 中国

- 日本

- 韓国

- オーストラリア

- インド

- 欧州

- ベルギー

- デンマーク

- フランス

- ドイツ

- イタリア

- オランダ

- ノルウェー

- スウェーデン

- スペイン

- スイス

- 英国

- 北米

- カナダ

- メキシコ

- 米国

第15章 競合情勢

- 概要

- 市場ランキング分析

- 主要企業の戦略(2020年~2023年)

- 企業の評価マトリクス

- 企業フットプリント(燃料電池メーカー)(2023年)

- 企業の用途フットプリント(燃料電池メーカー)(2023年)

- 企業の地域フットプリント(燃料電池メーカー)(2023年)

- スタートアップの評価マトリクス

- 競合シナリオ

第16章 企業プロファイル

- 主要企業(OEM)

- TOYOTA MOTOR CORPORATION

- HYUNDAI GROUP

- HONDA

- GENERAL MOTORS

- STELLANTIS

- 主要企業(燃料電池プロバイダー)

- BALLARD POWER SYSTEMS

- HYSTER-YALE

- PLUG POWER

- CUMMINS

- DOOSAN GROUP

- ADVENT TECHNOLOGIES HOLDINGS

- ITM POWER

- CERES POWER

- NEDSTACK

- PROTON MOTOR POWER SYSTEMS

- TOSHIBA

- POWERCELL AB

- その他の企業

- PANASONIC

- TORAY INDUSTRIES

- SUNRISE POWER CO. LTD

- BOSCH

- INTELLIGENT ENERGY

- SYMBIO

- ELRINGKLINGER AG

- SWISS HYDROGEN POWER

- DANA INCORPORATED

- FUEL CELL SYSTEM MANUFACTURING LLC

- VOLKSWAGEN AG

- DAIMLER

- RIVERSIMPLE

- SAIC MOTORS

- VAN HOOL

- MEBIUS FUEL CELL

- HYDRA ENERGY CORPORATION

- ISUZU MOTORS

- FORD MOTOR COMPANY

- FUELCELL ENERGY

- BLOOM ENERGY

- SUNFIRE

- IONOMR INNOVATIONS

- BRAMBLE ENERGY

第17章 MARKETSANDMARKETSによる推奨事項

- 日本、韓国、中国は自動車用燃料電池市場の焦点国

- FCEVの市場を押し上げる技術の進歩

- 結論

第18章 付録

The global automotive fuel cell market is projected to grow from USD 0.2 billion in 2024 to USD 2.1 billion by 2030, at a CAGR of 48.0%. Parameters such as an increase in demand for low emission vehicles and an increase in demand for green mobility will drive the market. In addition, the advancements in hydrogen-powered technology, paired with government support for fuel cell technology, will create new opportunities for this market. Increasing demand for zero-emission vehicles in the market and strong government support has led to many top OEMs invest in the R&D of FCEVs. Hydrogen fuel cells have thus become a fast-growing technology in the past decades. Many new technological developments have taken place, which have increased the demand for automobile fuel cells in the market. Unlike traditional EVs, FCEVs can be used for much longer distances and are often used in long-distance EV commuting. Companies like Toyota, Hyundai, and Honda have been leading the development of this technology for the last two decades.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2023 |

| Forecast Period | 2024-2030 |

| Units Considered | Value (USD Billion) |

| Segments | Type (Buses, Trucks, LCVs, Passenger Cars), Component, Fuel Type, Hydrogen Fuel Points, Operating Miles, Power, Capacity, Specialized Vehicle Type and Region |

| Regions covered | Asia Oceania, Europe, North America, and RoW |

" Hydrogen will be the most commonly used fuel in FCEVs."

Hydrogen, naturally occurring in our environment and stored in various forms such as water (H2O), hydrocarbons (e.g., methane - CH4), and organic matter, presents a challenge in terms of efficiently extracting it for use as a fuel. Hydrogen is gaining prominence as a viable alternative fuel derived from diverse domestic resources. Although the hydrogen transportation market is in its early stages, joint efforts from both government and industry are concentrated on achieving clean, cost-effective, and secure hydrogen production and distribution. Hydrogen fuel cells harness the chemical energy of hydrogen to generate electricity, with water being the sole by-product of usage. PEM fuel cells, commonly utilized for automotive purposes, are compatible with fuels like hydrogen, methanol, and ethanol. Hydrogen stands out as the cleanest fuel option for fuel cells in automotive applications. Despite the current limited demand for hydrogen fuel cell vehicles, primarily due to a constrained supply of green hydrogen and the use of fossil fuels in hydrogen production, countries worldwide are initiating green hydrogen projects for various applications. This initiative is expected to boost demand for hydrogen fuel cell vehicles as production scales up, accompanied by the establishment of hydrogen stations across countries. Storage poses a challenge hindering the widespread adoption of hydrogen as a fuel. Due to its low density, hydrogen cannot be stored as easily as fossil fuels and requires compression and cooling before storage. Steam reforming remains the dominant method for hydrogen production in the United States, involving the high-temperature combination of steam with natural gas to extract hydrogen. Alternatively, hydrogen can be produced from water through electrolysis, a more energy-intensive process that offers the advantage of using renewable energy sources such as wind or solar, thereby mitigating harmful emissions associated with other energy production forms. This necessitates specific tanks for storage purposes, further contributing to the cost of using hydrogen fuel cells for automotive applications. The goal is to facilitate the widespread adoption of hydrogen in Fuel Cell Electric Vehicles (FCEVs). Currently, light-duty FCEVs are gradually entering the consumer market in limited quantities, initially in specific regions both domestically and globally. Moreover, the hydrogen market is exhibiting promising growth in various sectors, including buses, material handling equipment (e.g., forklifts), ground support equipment, medium- and heavy-duty trucks, marine vessels, and stationary applications. While hydrogen production may generate emissions affecting air quality, it is crucial to note that the exhaust from an FCEV running on hydrogen comprises only water vapor and warm air, classifying it as a zero-emission vehicle. This has materialized in the introduction of light-duty vehicles to retail consumers and the initial deployment of medium- and heavy-duty buses and trucks in California, with plans for fleet availability expanding to northeastern states..

"North America to have rapid fuel cell demand growth during the forecast period."

North America has emerged as one of the fastest growing market in fuel cell development, spearheaded by acclaimed companies like Ballard Power (Canada), Plug Power (LIS), and Fuel Cell Energy (US). The US and Canada are actively promoting the growth of Fuel Cell Electric Vehicles (FCEVs), particularly in the commercial vehicle sector. Government support includes performance testing for fuel cell Heavy Commercial Vehicles (HCVs) and buses, with key players like Ballard Power Systems, Hyster-Yale, Plug Power, Cummins, Advent Technologies Holdings, and BorgWarner contributing to the region's competitive market. The United States is committed to decarbonizing its power sector by 2035, aiming for a 50-52% reduction in carbon emissions compared to 2005 levels and achieving net-zero emissions by 2050. Each fuel cell bus in operation in the US has the potential to annually reduce carbon emissions by 100 tons and eliminate the need for 9,000 gallons of fuel, resulting in significant cost savings of over USD 37,000 per vehicle compared to diesel-fueled buses. Recognizing the importance of fuel cell technology in its national energy strategy, the US government has proposed a USD 2 billion investment in technologies, including fuel cells, to reduce dependence on fossil fuels. California, at the forefront of automotive legislation for emissions reduction, has established hydrogen refueling stations, and the H2USA project aims to advance hydrogen infrastructure, preparing for the widespread adoption of FCEVs. The US Department of Energy's investment of USD 52.5 million in 31 projects supports the advancement of clean hydrogen technologies and the Hydrogen Energy Earthshot initiative, targeting 700,000 jobs and $140 billion in revenue by 2030. However, the US goal of producing green hydrogen at $1 per kilogram by 2031 may be optimistic, with blue hydrogen and naturally extracted hydrogen gaining attention on political agendas worldwide. Simultaneously, the California Air Resources Board (CARB) is championing zero-emissions vehicles, opening the door for more hydrogen fuel cell vehicles. North America's prowess in fuel cell technology innovation is attributed to government policies promoting low-emission technologies, business-friendly environments, lower taxes, and incentives for fuel cell vehicle users, fostering significant growth in the automotive fuel cell market.Canada is also taking steps to reduce carbon emissions, with the City of Toronto planning to convert 50% of its fleets to Electric Vehicles (EVs), including a substantial portion designated for long-distance travel using FCEVs. Provinces like BC and Quebec are incentivizing Zero-Emission Vehicle (ZEV) purchases, implementing regulations, and deploying hydrogen fueling infrastructure to promote the adoption of FCEVs.

In-depth interviews were conducted with CEOs, managers, and executives from various key organizations operating in this market.

- By Respondent Type - OEMs - 24% , Tier I - 67% , Tier II & III - 9%

- By Designation - C- level Executives - 33% , Managers - 52% , Executives - 15%

- By Region - North America - 28%, Asia Oceania - 38%,Europe - 34%

Research Coverage:

The report covers the automotive fuel cell market, in terms of vehicle type (Passenger Cars , LCV,Bus, Truck), Component (fuel cell stack, fuel processor, power conditioner, air compressor, humidifier), by specialised vehicle type (Material Handling Vehicle, Auxilary Power Unit or Refrigerated Truck), H2 fuel station (Asia Oceania, Europe, and North America), power output (<150kW, 150-250 Kw, >250kw), operating miles (0-250 miles, 250-500 miles, and above 500 miles), propulsion (FCEV,FCHEV), fuel type (Methanol, Ethanol, and others), region (Asia Oceania, Europe, and North America). It covers the competitive landscape and company profiles of the major automotive fuel cell market ecosystem players.

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall automotive fuel cell market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

- The report also helps stakeholders understand the current and future pricing trends of different automotive fuel cell systems based on their capacity.

The report provides insight on the following pointers:

- Analysis of key drivers (better fuel efficiency and increased driving range, rapid increase in investment and development for green hydrogen production, fast refuelling, reduced Oil dependency, lower emissions compared to other vehicles), restraints (highly flammable, hard to detect hydrogen leakage, high initial investment or hydrogen refuelling infrastructure, lower efficiency compared to BEV's and HEVs), challenges (rising demand for fuel cell vehicles in automotive and transportation sector, fuel cell vans to be an emerging opportunity for OEMs, government initiatives pertaining to hydrogen infrastructure ), and opportunities (high vehicle costs, insufficient hydrogen infrastructure, fast growing demand for BEVS and HEVs), influencing the growth of the authentication and brand protection market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the automotive fuel cell market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the automotive fuel cell market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the automotive fuel cell market.

- Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players Ballard Power Systems (Canada), Hyster-Yale (US), Plug Power(US) ITM Power(UK) and Cummins (US), among others in automotive fuel cell market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- TABLE 1 AUTOMOTIVE FUEL CELL MARKET DEFINITION, BY COMPONENT

- TABLE 2 AUTOMOTIVE FUEL CELL MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 3 AUTOMOTIVE FUEL CELL MARKET DEFINITION, BY SPECIALIZED VEHICLE TYPE

- TABLE 4 AUTOMOTIVE FUEL CELL MARKET DEFINITION, BY POWER OUTPUT

- TABLE 5 AUTOMOTIVE FUEL CELL MARKET DEFINITION, BY OPERATING MILES

- TABLE 6 AUTOMOTIVE FUEL CELL MARKET DEFINITION, BY PROPULSION

- TABLE 7 AUTOMOTIVE FUEL CELL MARKET DEFINITION, BY FUEL TYPE

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- TABLE 8 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- FIGURE 1 AUTOMOTIVE FUEL CELL MARKET SEGMENTATION

- 1.3.1 REGIONS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 9 CURRENCY EXCHANGE RATES

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 AUTOMOTIVE FUEL CELL MARKET: RESEARCH DESIGN

- FIGURE 3 RESEARCH DESIGN MODEL

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews: demand and supply sides

- 2.1.2.2 Key industry insights and breakdown of primary interviews

- FIGURE 4 KEY INDUSTRY INSIGHTS

- FIGURE 5 BREAKDOWN OF PRIMARY INTERVIEWS

- 2.1.2.3 List of primary participants

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 6 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 7 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 8 TOP-DOWN APPROACH

- FIGURE 9 AUTOMOTIVE FUEL CELL MARKET ESTIMATION NOTES

- FIGURE 10 RESEARCH DESIGN AND METHODOLOGY: DEMAND SIDE

- 2.3 DATA TRIANGULATION

- FIGURE 11 DATA TRIANGULATION

- FIGURE 12 MARKET GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES

- 2.4 FACTOR ANALYSIS

- FIGURE 13 FACTOR ANALYSIS FOR MARKET SIZING: DEMAND AND SUPPLY SIDES

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

- FIGURE 14 AUTOMOTIVE FUEL CELL MARKET OVERVIEW

- FIGURE 15 AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (USD MILLION)

- FIGURE 16 PASSENGER CAR TO BE LARGEST VEHICLE TYPE DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE FUEL CELL MARKET

- FIGURE 17 GROWING DEMAND FOR ALTERNATIVE ZERO-EMISSION TRANSPORT OPTIONS TO DRIVE MARKET

- 4.2 AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE

- FIGURE 18 PASSENGER CAR TO BE LARGEST VEHICLE TYPE DURING 2024-2030

- 4.3 AUTOMOTIVE FUEL CELL MARKET, BY HYDROGEN FUEL POINTS

- FIGURE 19 ASIA OCEANIA TO BE FASTEST-GROWING SEGMENT DURING 2024-2030

- 4.4 AUTOMOTIVE FUEL CELL MARKET, BY POWER OUTPUT

- FIGURE 20 150-250 KW POWER OUTPUT TO GROW RAPIDLY DURING FORECAST PERIOD

- 4.5 AUTOMOTIVE FUEL CELL MARKET, BY COMPONENT

- FIGURE 21 FUEL STACK COMPONENT TO LEAD MARKET DURING FORECAST PERIOD

- 4.6 AUTOMOTIVE FUEL CELL MARKET, BY OPERATING MILES

- FIGURE 22 251-500 MILES SEGMENT TO LEAD MARKET DURING 2024-2030

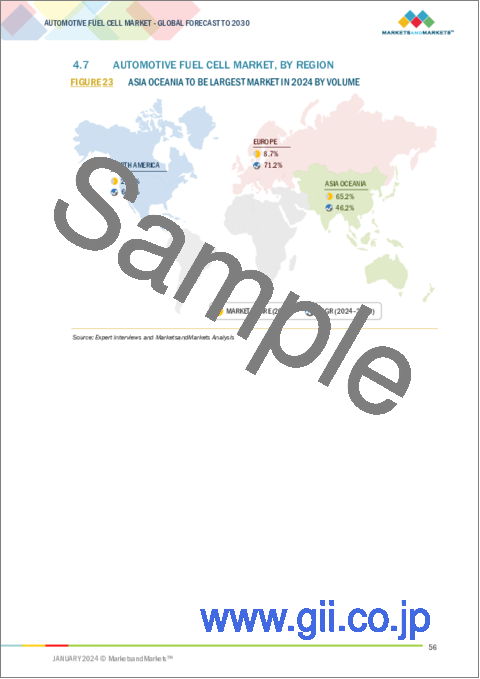

- 4.7 AUTOMOTIVE FUEL CELL MARKET, BY REGION

- FIGURE 23 ASIA OCEANIA TO BE LARGEST MARKET IN 2024 BY VOLUME

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- FIGURE 24 HYDROGEN FUEL CELL ELECTRIC VEHICLE SYSTEM

- 5.2 MARKET DYNAMICS

- FIGURE 25 AUTOMOTIVE FUEL CELL MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Better fuel efficiency and driving range than ICE vehicles

- FIGURE 26 NATURAL GAS REQUIRED TO PROPEL BEV TO 300 MILES VS. FCEV TRAVELING 300 MILES

- TABLE 10 ATTRIBUTES OF FCEV VS. ADVANCED BEV FOR 200-MILE AND 300-MILE RANGE

- 5.2.1.2 Growing investment in green hydrogen production

- FIGURE 27 NUMBER OF HYDROGEN FUEL STATIONS IN US (2017-2022)

- 5.2.1.3 Fast refueling

- TABLE 11 ZERO-EMISSION LIGHT-DUTY VEHICLE REFERENCE COMPARISON: BEV CHARGING VS. FCEV HYDROGEN FUELING

- 5.2.1.4 Reduced oil dependency

- FIGURE 28 LIQUID OIL CONSUMPTION (MILLION BARRELS PER DAY), 2017-2022

- TABLE 12 US: GASOLINE AVERAGE PRICING TREND (2018-2024)

- 5.2.1.5 Lower emissions than other vehicles

- 5.2.2 RESTRAINTS

- 5.2.2.1 High flammability

- FIGURE 29 COMPARISON OF AUTOIGNITION TEMPERATURES OF VARIOUS FUELS

- 5.2.2.2 Hard to detect hydrogen leakages

- 5.2.2.3 High initial investments in hydrogen fueling infrastructure

- FIGURE 30 DISPENSED FUEL COST BUILDUP FOR FUTURE TRANSPORTATION FUELS

- FIGURE 31 INITIAL INVESTMENT IN INFRASTRUCTURE FOR VARIOUS FUELS

- FIGURE 32 COMPARISON OF BEV AND FCEV

- 5.2.2.4 Lower efficiency than BEVs and HEVs

- FIGURE 33 GLOBAL ELECTRIC VEHICLE SALES, 2019-2023

- FIGURE 34 COMPARISON OF HYDROGEN AND ELECTRIC VEHICLE DRIVE

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising demand for fuel cell vehicles in automotive & transportation sector

- 5.2.3.1.1 Fuel cell commercial freight truck developments

- 5.2.3.1 Rising demand for fuel cell vehicles in automotive & transportation sector

- TABLE 13 FUEL CELL COMMERCIAL FREIGHT TRUCK DEVELOPMENTS

- 5.2.3.1.2 Fuel-cell buses worldwide, 2023

- FIGURE 35 OPERATED FUEL CELL BUSES, 2023

- 5.2.3.2 Growth potential of fuel cell vans for OEMs

- 5.2.3.3 Government initiatives promoting hydrogen infrastructure

- FIGURE 36 GOVERNMENT-LED HYDROGEN HUB INITIATIVES IN US AND CANADA

- 5.2.3.4 Development of mobile and community hydrogen fueling systems

- FIGURE 37 MOBILE HYDROGEN-REFUELING STATIONS IN JAPAN

- 5.2.4 CHALLENGES

- 5.2.4.1 High vehicle costs

- FIGURE 38 COST OF FUEL CELL STACK FOR PRODUCTION VOLUME OF 1,000 UNITS/YEAR VS. 500,000 UNITS/YEAR

- 5.2.4.2 Lack of proper hydrogen infrastructure

- FIGURE 39 HYDROGEN INFRASTRUCTURE MAINTENANCE COSTS, BY COMPONENT

- 5.2.4.3 Rising demand for BEVs and HEVs

- TABLE 14 AUTOMOTIVE FUEL CELL MARKET: IMPACT OF MARKET DYNAMICS

- 5.3 EXISTING AND UPCOMING FCEV MODELS

- TABLE 15 EXISTING AND UPCOMING PASSENGER CAR FCEV MODELS

- TABLE 16 EXISTING AND UPCOMING COMMERCIAL FCEV MODELS

- 5.4 CASE STUDY ANALYSIS

- 5.4.1 CASE STUDY 1: BALLARD FUEL CELL ZERO-EMISSION BUSES IN LONDON

- 5.4.2 CASE STUDY 2: BALLARD FUEL CELL ZERO-EMISSION TRUCKS IN SHANGHAI

- 5.4.3 CASE STUDY 3: NON-PRECIOUS METAL CATALYST BY BALLARD

- 5.4.4 CASE STUDY 4: FUEL CELL ZERO-EMISSION BUSES BY BALLARD

- 5.4.5 CASE STUDY 5: FUEL-CELL BUSES FOR CITY TRANSIT IN FRANCE

- 5.5 PATENT ANALYSIS

- FIGURE 40 NUMBER OF PUBLISHED AUTOMOTIVE FUEL CELL PATENTS (2019-2023)

- FIGURE 41 TOP PATENT APPLICANTS

- TABLE 17 IMPORTANT PATENT REGISTRATIONS RELATED TO AUTOMOTIVE FUEL CELL MARKET

- 5.6 ECOSYSTEM ANALYSIS

- FIGURE 42 AUTOMOTIVE FUEL CELL MARKET: ECOSYSTEM ANALYSIS

- 5.6.1 HYDROGEN FUEL SUPPLIERS

- 5.6.2 TIER I SUPPLIERS (FUEL CELL AND RELATED COMPONENT PRODUCERS)

- 5.6.3 OEMS

- TABLE 18 AUTOMOTIVE FUEL CELL MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- 5.7 SUPPLY CHAIN ANALYSIS

- FIGURE 43 AUTOMOTIVE FUEL CELL MARKET: SUPPLY CHAIN ANALYSIS

- 5.8 FUEL CELL PRICING ANALYSIS

- TABLE 19 AUTOMOTIVE FUEL CELL STACK PRICE: REGIONAL PRICE TREND, 2020 VS. 2022

- 5.8.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY VEHICLE TYPE

- TABLE 20 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY VEHICLE TYPE

- FIGURE 44 FUEL CELL SYSTEM COST, 2006-2025

- FIGURE 45 FUEL CELL SYSTEM AND FUEL CELL STACK COST

- 5.9 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 46 AUTOMOTIVE FUEL CELL MARKET: NEW REVENUE SOURCES

- TABLE 21 FUEL CELL BUS SALES AND UPCOMING PROJECTS

- 5.10 ROADMAP OF DEPLOYMENT OF HYDROGEN TECHNOLOGY IN AUTOMOTIVE SECTOR

- 5.11 FCEV LAUNCH SCHEDULED BY MAJOR OEMS

- FIGURE 47 LAUNCH OF HYDROGEN MODELS

- 5.11.1 HYDROGEN FUEL CELL VEHICLES TO GAIN MOMENTUM ACROSS DIVERSE LANDSCAPES

- 5.12 STAKEHOLDERS' PLAN IN HYDROGEN-FUELED VEHICLE ECOSYSTEM

- 5.13 BUSINESS MODELS

- FIGURE 48 BUSINESS MODELS IN AUTOMOTIVE FUEL CELL MARKET

- 5.14 TECHNOLOGY ANALYSIS

- 5.14.1 DIRECT BOROHYDRIDE FUEL CELL

- FIGURE 49 DIRECT BOROHYDRIDE FUEL CELL WORKING

- 5.14.2 FUEL CELL HYBRID ELECTRIC VEHICLE

- 5.14.3 HYDROGEN INTERNAL COMBUSTION ENGINE

- 5.14.4 NON-PRECIOUS METAL CATALYST-BASED FUEL CELL

- 5.14.5 PACKAGED FUEL CELL SYSTEM MODULE

- FIGURE 50 TOYOTA'S NEW PACKAGED FUEL CELL SYSTEM MODULE

- 5.14.6 HYDROGENIOUS LIQUID ORGANIC HYDROGEN CARRIER

- 5.14.7 CARBONATE-SUPERSTRUCTURED SOLID FUEL CELL

- 5.15 REGULATORY LANDSCAPE

- 5.15.1 NORTH AMERICA

- TABLE 22 NORTH AMERICA: POLICIES & INITIATIVES SUPPORTING HYDROGEN-POWERED VEHICLES & HYDROGEN INFRASTRUCTURE

- 5.15.2 EUROPE

- TABLE 23 EUROPE: POLICIES & INITIATIVES SUPPORTING HYDROGEN-POWERED VEHICLES & HYDROGEN INFRASTRUCTURE

- 5.15.3 ASIA OCEANIA

- TABLE 24 ASIA OCEANIA: POLICIES & INITIATIVES SUPPORTING HYDROGEN-POWERED VEHICLES & HYDROGEN INFRASTRUCTURE

- 5.15.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 25 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 ASIA OCEANIA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.16 KEY CONFERENCES AND EVENTS IN 2024-2025

- TABLE 28 KEY CONFERENCES AND EVENTS, 2024-2025

- 5.17 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.17.1 LCV

- 5.17.2 BUS

- 5.17.3 TRUCK

- 5.17.4 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 51 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- TABLE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS (%)

- 5.17.5 BUYING CRITERIA

- FIGURE 52 KEY BUYING CRITERIA FOR AUTOMOTIVE FUEL CELL MARKET

- TABLE 30 KEY BUYING CRITERIA FOR FUEL CELL VEHICLE TYPES

6 AUTOMOTIVE FUEL CELL MARKET, BY COMPONENT

- 6.1 INTRODUCTION

- FIGURE 53 AUTOMOTIVE FUEL CELL MARKET, BY COMPONENT, 2024-2030 (USD MILLION)

- TABLE 31 AUTOMOTIVE FUEL CELL MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 32 AUTOMOTIVE FUEL CELL MARKET, BY COMPONENT, 2024-2030 (USD MILLION)

- 6.2 OPERATIONAL DATA

- TABLE 33 POPULAR FUEL CELL PROVIDERS WORLDWIDE

- FIGURE 54 FUEL CELL POWERTRAIN

- 6.3 FUEL STACK

- 6.3.1 STRINGENT EMISSION REGULATIONS AND GOVERNMENT INCENTIVES TO DRIVE MARKET

- TABLE 34 FUEL STACK: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 35 FUEL STACK: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.4 FUEL PROCESSOR

- 6.4.1 RAPID GROWTH OF FUEL CELL TECHNOLOGIES IN ASIA OCEANIA AND NORTH AMERICA TO DRIVE MARKET

- TABLE 36 FUEL PROCESSOR: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 37 FUEL PROCESSOR: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.5 POWER CONDITIONER

- 6.5.1 PRESENCE OF LEADING FCEV MANUFACTURERS IN ASIA OCEANIA TO DRIVE MARKET

- TABLE 38 POWER CONDITIONER: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 39 POWER CONDITIONER: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.6 AIR COMPRESSOR

- 6.6.1 GROWING ADOPTION OF FUEL CELL BUSES IN NORTH AMERICA TO DRIVE MARKET

- TABLE 40 AIR COMPRESSOR: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 41 AIR COMPRESSOR: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.7 HUMIDIFIER

- 6.7.1 INCREASING DEMAND FOR FCEVS IN EUROPE TO DRIVE MARKET

- TABLE 42 HUMIDIFIER: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 43 HUMIDIFIER: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.8 KEY PRIMARY INSIGHTS

7 AUTOMOTIVE FUEL CELL MARKET, BY FUEL TYPE

- 7.1 INTRODUCTION

- TABLE 44 COMPARISON OF FUEL TYPES USED IN FUEL CELLS AND LITHIUM-ION BATTERIES

- 7.2 HYDROGEN

- 7.3 METHANOL

- 7.4 ETHANOL

- 7.5 KEY PRIMARY INSIGHTS

8 AUTOMOTIVE FUEL CELL MARKET, BY HYDROGEN FUEL POINTS

- 8.1 INTRODUCTION

- FIGURE 55 INFRASTRUCTURE COST COMPARISON FOR FCEV AND BEV

- FIGURE 56 AUTOMOTIVE HYDROGEN FUEL POINTS MARKET, BY REGION, 2024-2030 (UNITS)

- TABLE 45 HYDROGEN FUEL POINTS: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (UNITS)

- TABLE 46 HYDROGEN FUEL POINTS: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (UNITS)

- 8.2 OPERATIONAL DATA

- TABLE 47 NUMBER OF HYDROGEN FUEL POINTS, BY COUNTRY (DECEMBER 2023)

- 8.3 ASIA OCEANIA

- TABLE 48 ASIA OCEANIA: AUTOMOTIVE HYDROGEN FUEL POINTS MARKET, BY COUNTRY, 2020-2023 (UNITS)

- TABLE 49 ASIA OCEANIA: AUTOMOTIVE HYDROGEN FUEL POINTS MARKET, BY COUNTRY, 2024-2030 (UNITS)

- 8.4 EUROPE

- TABLE 50 EUROPE: AUTOMOTIVE HYDROGEN FUEL POINTS MARKET, BY COUNTRY, 2020-2023 (UNITS)

- TABLE 51 EUROPE: AUTOMOTIVE HYDROGEN FUEL POINTS MARKET, BY COUNTRY, 2024-2030 (UNITS)

- 8.5 NORTH AMERICA

- TABLE 52 NORTH AMERICA: AUTOMOTIVE HYDROGEN FUEL POINTS MARKET, BY COUNTRY, 2020-2023 (UNITS)

- TABLE 53 NORTH AMERICA: AUTOMOTIVE HYDROGEN FUEL POINTS MARKET, BY COUNTRY, 2024-2030 (UNITS)

- 8.6 KEY PRIMARY INSIGHTS

9 AUTOMOTIVE FUEL CELL MARKET, BY OPERATING MILES

- 9.1 INTRODUCTION

- FIGURE 57 AUTOMOTIVE FUEL CELL MARKET, BY OPERATING MILES, 2024-2030 (THOUSAND UNITS)

- TABLE 54 AUTOMOTIVE FUEL CELL MARKET, BY OPERATING MILES, 2020-2023 (THOUSAND UNITS)

- TABLE 55 AUTOMOTIVE FUEL CELL MARKET, BY OPERATING MILES, 2024-2030 (THOUSAND UNITS)

- 9.2 OPERATIONAL DATA

- TABLE 56 POPULAR FCEVS WORLDWIDE, BY OPERATING MILES

- 9.3 0-250 MILES

- 9.3.1 NORTH AMERICA AND ASIA OCEANIA TO DRIVE MARKET

- TABLE 57 0-250 MILES: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 58 0-250 MILES: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 9.4 251-500 MILES

- 9.4.1 CONSIDERABLE RANGE ACHIEVABLE ON SINGLE FUELING TO DRIVE MARKET

- TABLE 59 BESTSELLING FCEVS WITH 251-500 MILES RANGE

- TABLE 60 251-500 MILES: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 61 251-500 MILES: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 9.5 ABOVE 500 MILES

- 9.5.1 RESILIENCE IN DIFFERENT LOAD CYCLES TO DRIVE MARKET

- TABLE 62 ABOVE 500 MILES: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 63 ABOVE 500 MILES: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 9.6 KEY PRIMARY INSIGHTS

10 AUTOMOTIVE FUEL CELL MARKET, BY POWER OUTPUT

- 10.1 INTRODUCTION

- FIGURE 58 AUTOMOTIVE FUEL CELL MARKET, BY POWER OUTPUT, 2024-2030 (THOUSAND UNITS)

- TABLE 64 AUTOMOTIVE FUEL CELL MARKET, BY POWER OUTPUT, 2020-2023 (THOUSAND UNITS)

- TABLE 65 AUTOMOTIVE FUEL CELL MARKET, BY POWER OUTPUT, 2024-2030 (THOUSAND UNITS)

- 10.2 OPERATIONAL DATA

- TABLE 66 POPULAR FCEVS WORLDWIDE, BY POWER OUTPUT

- 10.3 <150 KW

- 10.3.1 GROWING DEMAND FOR FUEL CELL PASSENGER CARS TO DRIVE MARKET

- TABLE 67 <150 KW: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 68 <150 KW: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 10.4 150-250 KW

- 10.4.1 GROWING DEMAND FOR HEAVY-DUTY TRUCKS AND BUSES TO DRIVE MARKET

- TABLE 69 150-250 KW: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 70 150-250 KW: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 10.5 >250 KW

- 10.5.1 HIGH DEMAND FOR LONG-HAUL TRUCKING TO DRIVE MARKET

- TABLE 71 >250 KW: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 72 >250 KW: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 10.6 KEY PRIMARY INSIGHTS

11 AUTOMOTIVE FUEL CELL MARKET, BY PROPULSION

- 11.1 INTRODUCTION

- FIGURE 59 AUTOMOTIVE FUEL CELL MARKET, BY PROPULSION, 2024-2030 (THOUSAND UNITS)

- TABLE 73 AUTOMOTIVE FUEL CELL MARKET, BY PROPULSION, 2020-2023 (THOUSAND UNITS)

- TABLE 74 AUTOMOTIVE FUEL CELL MARKET, BY PROPULSION, 2024-2030 (THOUSAND UNITS)

- 11.2 OPERATIONAL DATA

- TABLE 75 POPULAR FCEV AND FCHEV MODEL LAUNCHES

- 11.3 FCHEV

- 11.3.1 SMOOTH POWER DELIVERY REDUCING STRESS ON FUEL CELLS TO DRIVE MARKET

- 11.4 FCEV

- 11.4.1 HIGH DEMAND FOR SUSTAINABLE AND ZERO-EMISSION TRANSPORTATION TO DRIVE MARKET

- 11.5 KEY PRIMARY INSIGHTS

12 AUTOMOTIVE FUEL CELL MARKET, BY SPECIALIZED VEHICLE TYPE

- 12.1 INTRODUCTION

- 12.2 MATERIAL HANDLING VEHICLE

- TABLE 76 COMPARISON OF POLYMER ELECTROLYTE MEMBRANE (PEM) FUEL CELL AND BATTERY-POWERED FORKLIFTS AND PALLET JACKS

- 12.3 AUXILIARY POWER UNIT FOR REFRIGERATED TRUCKS

- 12.4 KEY PRIMARY INSIGHTS

13 AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE

- 13.1 INTRODUCTION

- TABLE 77 TABLE OF COMPARISON OF DIFFERENT TYPES OF HYDROGEN VEHICLES

- FIGURE 60 AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (THOUSAND UNITS)

- TABLE 78 AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 79 AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (THOUSAND UNITS)

- 13.2 OPERATIONAL DATA

- TABLE 80 POTENTIAL MARKET FOR NEW ZERO-EMISSION BUSES PER YEAR ACROSS EUROPE

- 13.3 PASSENGER CAR

- 13.3.1 GROWING ENVIRONMENTAL CONCERNS, STRICTER EMISSION REGULATIONS, AND ADVANCEMENTS IN TECHNOLOGY TO DRIVE MARKET

- TABLE 81 PASSENGER CAR: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 82 PASSENGER CAR: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 13.4 LCV

- 13.4.1 RISING DEMAND FOR LAST MILE DELIVERY TO DRIVE MARKET

- TABLE 83 LCV: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 84 LCV: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 13.5 BUS

- 13.5.1 SURGING URBAN AIR QUALITY CONCERNS AND RAPID REFUELING ADVANCEMENTS TO DRIVE MARKET

- TABLE 85 EXAMPLES OF BUS DEPLOYMENT PROJECTS

- TABLE 86 BUS: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 87 BUS: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 13.6 TRUCK

- 13.6.1 EXPANDING HYDROGEN INFRASTRUCTURE AND INCREASING GOVERNMENT INCENTIVES TO DRIVE MARKET

- TABLE 88 OVERVIEW OF VEHICLE WEIGHT CLASSES

- TABLE 89 MASS DIFFERENCE BETWEEN BASELINE VEHICLE AND ITS FUEL CELL TRUCK VERSION

- TABLE 90 DEMONSTRATION PROJECTS/DEPLOYMENT OF FUEL CELL TRUCKS

- TABLE 91 MAJOR FUEL CELL TRUCK PROTOTYPES

- TABLE 92 POWERTRAIN BENCHMARKING FOR TRUCKS >12 TONS

- TABLE 93 TRUCK: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 94 TRUCK: AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- 13.7 KEY PRIMARY INSIGHTS

14 AUTOMOTIVE FUEL CELL MARKET, BY REGION

- 14.1 INTRODUCTION

- FIGURE 61 AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (USD MILLION)

- TABLE 95 AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 96 AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (USD MILLION)

- TABLE 97 AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 98 AUTOMOTIVE FUEL CELL MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 99 STEPS TAKEN BY MAJOR COUNTRIES TO BOOST AUTOMOTIVE FUEL CELL MARKET

- 14.2 ASIA OCEANIA

- FIGURE 62 ASIA OCEANIA: AUTOMOTIVE FUEL CELL MARKET SNAPSHOT

- TABLE 100 ASIA OCEANIA AUTOMOTIVE FUEL CELL MARKET: UPCOMING PROJECTS

- TABLE 101 ASIA OCEANIA: AUTOMOTIVE FUEL CELL MARKET, BY COUNTRY, 2020-2023 (THOUSAND UNITS)

- TABLE 102 ASIA OCEANIA: AUTOMOTIVE FUEL CELL MARKET, BY COUNTRY, 2024-2030 (THOUSAND UNITS)

- 14.2.1 CHINA

- 14.2.1.1 Emphasis on utilizing industrial by-product hydrogen to drive market

- TABLE 103 CHINA: TARGETS, VISIONS, AND PROJECTIONS

- TABLE 104 CHINA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 105 CHINA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.2.2 JAPAN

- 14.2.2.1 Plans to increase production of hydrogen to drive market

- TABLE 106 JAPAN: TARGETS, VISIONS, AND PROJECTIONS

- TABLE 107 JAPAN: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 108 JAPAN: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.2.3 SOUTH KOREA

- 14.2.3.1 Transition to hydrogen economy to drive market

- TABLE 109 SOUTH KOREA: TARGETS, VISIONS, AND PROJECTIONS

- TABLE 110 SOUTH KOREA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 111 SOUTH KOREA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.2.4 AUSTRALIA

- 14.2.4.1 Government investment in hydrogen ecosystem to drive market

- TABLE 112 AUSTRALIA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 113 AUSTRALIA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.2.5 INDIA

- 14.2.5.1 Initiatives by government for green transportation to drive market

- TABLE 114 INDIA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 115 INDIA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3 EUROPE

- TABLE 116 EUROPE: RELEVANT EXPERIENCE/PRODUCTS OF OEMS

- TABLE 117 EUROPE: TARGETS, VISIONS, AND PROJECTIONS

- FIGURE 63 EUROPE: AUTOMOTIVE FUEL CELL MARKET, 2024-2030 (THOUSAND UNITS)

- TABLE 118 EUROPEAN AUTOMOTIVE FUEL CELL MARKET: ONGOING PROJECTS

- TABLE 119 EUROPE: AUTOMOTIVE FUEL CELL MARKET, BY COUNTRY, 2020-2023 (THOUSAND UNITS)

- TABLE 120 EUROPE: AUTOMOTIVE FUEL CELL MARKET, BY COUNTRY, 2024-2030 (THOUSAND UNITS)

- 14.3.1 BELGIUM

- 14.3.1.1 Tax incentives to drive market

- TABLE 121 BELGIUM: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 122 BELGIUM: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.2 DENMARK

- 14.3.2.1 Investments in hydrogen infrastructure to drive market

- TABLE 123 DENMARK: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 124 DENMARK: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.3 FRANCE

- 14.3.3.1 Presence of major OEM fleets to drive market

- TABLE 125 FRANCE: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 126 FRANCE: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.4 GERMANY

- 14.3.4.1 Fast-paced developments in hydrogen infrastructure to drive market

- TABLE 127 GERMANY: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 128 GERMANY: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.5 ITALY

- 14.3.5.1 Focus on developing fuel cell technology to drive market

- TABLE 129 ITALY: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 130 ITALY: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.6 NETHERLANDS

- 14.3.6.1 Dutch Hydrogen Coalition to drive market

- TABLE 131 NETHERLANDS: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 132 NETHERLANDS: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.7 NORWAY

- 14.3.7.1 Robust fueling infrastructure plans to drive market

- TABLE 133 NORWAY: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 134 NORWAY: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.8 SWEDEN

- 14.3.8.1 Advancement in fuel cells to drive market

- TABLE 135 SWEDEN: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 136 SWEDEN: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.9 SPAIN

- 14.3.9.1 Government plans and investments to drive market

- TABLE 137 SPAIN: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 138 SPAIN: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.10 SWITZERLAND

- 14.3.10.1 Ending tax exemption for electric cars to drive market

- TABLE 139 SWITZERLAND: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 140 SWITZERLAND: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.3.11 UK

- 14.3.11.1 Plan for zero-emission public transport to drive market

- TABLE 141 UK: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 142 UK: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.4 NORTH AMERICA

- FIGURE 64 NORTH AMERICA: AUTOMOTIVE FUEL CELL MARKET SNAPSHOT

- TABLE 143 NORTH AMERICAN AUTOMOTIVE FUEL CELL MARKET: UPCOMING PROJECTS

- TABLE 144 NORTH AMERICA: AUTOMOTIVE FUEL CELL MARKET, BY COUNTRY, 2020-2023 (THOUSAND UNITS)

- TABLE 145 NORTH AMERICA: AUTOMOTIVE FUEL CELL MARKET, BY COUNTRY, 2024-2030 (THOUSAND UNITS)

- 14.4.1 CANADA

- 14.4.1.1 Inclusion of benefits in tax credit to drive market

- TABLE 146 CANADA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 147 CANADA: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.4.2 MEXICO

- 14.4.2.1 Shift to zero-emission transport alternative to drive market

- TABLE 148 MEXICO: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 149 MEXICO: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

- 14.4.3 US

- 14.4.3.1 Government investment in green hydrogen to drive market

- TABLE 150 US: TARGETS, VISIONS, AND PROJECTIONS

- TABLE 151 US: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2020-2023 (UNITS)

- TABLE 152 US: AUTOMOTIVE FUEL CELL MARKET, BY VEHICLE TYPE, 2024-2030 (UNITS)

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 MARKET RANKING ANALYSIS

- FIGURE 65 AUTOMOTIVE FUEL CELL MARKET RANKING ANALYSIS (OEMS), 2023

- FIGURE 66 AUTOMOTIVE FUEL CELL MARKET RANKING ANALYSIS (COMPONENT PROVIDERS), 2023

- 15.3 KEY PLAYERS' STRATEGIES, 2020-2023

- TABLE 153 KEY PLAYERS' STRATEGIES, 2020-2023

- FIGURE 67 REVENUE ANALYSIS OF TOP PUBLIC/LISTED PLAYERS IN AUTOMOTIVE FUEL CELL MARKET DURING LAST 5 YEARS

- 15.4 COMPANY EVALUATION MATRIX

- 15.4.1 STARS

- 15.4.2 EMERGING LEADERS

- 15.4.3 PERVASIVE PLAYERS

- 15.4.4 PARTICIPANTS

- FIGURE 68 AUTOMOTIVE FUEL CELL MARKET: COMPANY EVALUATION MATRIX (TOP COMPONENT PROVIDERS), 2023

- 15.5 COMPANY FOOTPRINT (FUEL CELL MANUFACTURERS), 2023

- TABLE 154 AUTOMOTIVE FUEL CELL MARKET: COMPANY FOOTPRINT

- 15.6 COMPANY APPLICATION FOOTPRINT (FUEL CELL MANUFACTURERS), 2023

- TABLE 155 AUTOMOTIVE FUEL CELL MARKET: COMPANY APPLICATION FOOTPRINT

- 15.7 COMPANY REGIONAL FOOTPRINT (FUEL CELL MANUFACTURERS), 2023

- TABLE 156 AUTOMOTIVE FUEL CELL MARKET: REGIONAL FOOTPRINT

- FIGURE 69 AUTOMOTIVE FUEL CELL MARKET: COMPANY EVALUATION MATRIX (OEMS), 2023

- 15.8 STARTUP EVALUATION MATRIX

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- FIGURE 70 AUTOMOTIVE FUEL CELL MARKET: START-UP MATRIX, 2023

- 15.8.5 COMPETITIVE BENCHMARKING

- TABLE 157 LIST OF KEY STARTUPS/SMES

- TABLE 158 COMPETITIVE BENCHMARKING OF START-UPS/SMES

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 DEALS

- TABLE 159 AUTOMOTIVE FUEL CELL MARKET: DEALS, 2020-2023

- 15.9.2 PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 160 AUTOMOTIVE FUEL CELL MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, 2020-2023

- 15.9.3 EXPANSIONS

- TABLE 161 AUTOMOTIVE FUEL CELL MARKET: EXPANSIONS, 2020-2023

16 COMPANY PROFILES

(Business overview, Products offered, Recent developments & MnM View)**

- 16.1 KEY PLAYERS (OEMS)

- 16.1.1 TOYOTA MOTOR CORPORATION

- TABLE 162 TOYOTA MOTOR CORPORATION: COMPANY OVERVIEW

- FIGURE 71 TOYOTA MOTOR CORPORATION: COMPANY SNAPSHOT

- FIGURE 72 TOYOTA MOTOR CORPORATION: GLOBAL DATA BY REGION

- TABLE 163 TOYOTA MOTOR CORPORATION: PRODUCTS OFFERED

- TABLE 164 TOYOTA MOTOR CORPORATION: PRODUCT DEVELOPMENTS

- TABLE 165 TOYOTA MOTOR CORPORATION: DEALS

- TABLE 166 TOYOTA MOTOR CORPORATION: EXPANSIONS

- 16.1.2 HYUNDAI GROUP

- TABLE 167 HYUNDAI GROUP: COMPANY OVERVIEW

- FIGURE 73 HYUNDAI GROUP: COMPANY SNAPSHOT

- TABLE 168 HYUNDAI GROUP: PRODUCTS OFFERED

- TABLE 169 HYUNDAI GROUP: PRODUCT LAUNCHES

- TABLE 170 HYUNDAI GROUP: DEALS

- 16.1.3 HONDA

- TABLE 171 HONDA: COMPANY OVERVIEW

- FIGURE 74 HONDA: COMPANY SNAPSHOT

- TABLE 172 HONDA: PRODUCTS OFFERED

- TABLE 173 HONDA: PRODUCT DEVELOPMENTS

- TABLE 174 HONDA: DEALS

- 16.1.4 GENERAL MOTORS

- TABLE 175 GENERAL MOTORS: COMPANY OVERVIEW

- FIGURE 75 GENERAL MOTORS: COMPANY SNAPSHOT

- FIGURE 76 GENERAL MOTORS: FUEL CELL MANUFACTURING CAPACITY

- TABLE 176 GENERAL MOTORS: DEALS

- 16.1.5 STELLANTIS

- TABLE 177 STELLANTIS: COMPANY OVERVIEW

- FIGURE 77 STELLANTIS: COMPANY SNAPSHOT

- TABLE 178 STELLANTIS: PRODUCTS OFFERED

- TABLE 179 STELLANTIS: PRODUCT LAUNCHES

- TABLE 180 STELLANTIS: DEALS

- TABLE 181 STELLANTIS: EXPANSIONS

- 16.2 KEY PLAYERS (FUEL CELL PROVIDERS)

- 16.2.1 BALLARD POWER SYSTEMS

- TABLE 182 BALLARD POWER SYSTEMS: COMPANY OVERVIEW

- FIGURE 78 BALLARD POWER SYSTEMS: COMPANY SNAPSHOT

- FIGURE 79 BALLARD POWER SYSTEMS: MACRO LANDSCAPE

- TABLE 183 BALLARD POWER SYSTEMS: FUEL CELL STACK

- FIGURE 80 BALLARD POWER SYSTEMS: FUTURE PLANS

- FIGURE 81 BALLARD POWER SYSTEMS: STATIONARY POWER GENERATION WITH HYDROGEN FUEL CELLS

- TABLE 184 BALLARD POWER SYSTEMS: PRODUCTS OFFERED

- TABLE 185 BALLARD POWER SYSTEMS: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 186 BALLARD POWER SYSTEMS: DEALS

- TABLE 187 BALLARD POWER SYSTEMS: EXPANSIONS

- 16.2.2 HYSTER-YALE

- FIGURE 82 HYSTER-YALE'S SUBSIDIARY NUVERA AT A GLANCE

- TABLE 188 HYSTER-YALE: COMPANY OVERVIEW

- FIGURE 83 HYSTER-YALE: COMPANY SNAPSHOT

- TABLE 189 HYSTER-YALE: PRODUCTS OFFERED

- TABLE 190 HYSTER-YALE: PRODUCT DEVELOPMENTS

- TABLE 191 HYSTER-YALE: DEALS

- TABLE 192 HYSTER-YALE: EXPANSIONS

- 16.2.3 PLUG POWER

- TABLE 193 PLUG POWER: COMPANY OVERVIEW

- FIGURE 84 PLUG POWER: COMPANY SNAPSHOT

- TABLE 194 PLUG POWER: OPERATIONAL CHARACTERISTICS OF EV CHARGERS FOR LIGHT-DUTY VEHICLES

- TABLE 195 PLUG POWER: PRODUCTS OFFERED

- TABLE 196 PLUG POWER: PRODUCT DEVELOPMENTS

- TABLE 197 PLUG POWER: DEALS

- TABLE 198 PLUG POWER: OTHER DEVELOPMENTS

- 16.2.4 CUMMINS

- FIGURE 85 CUMMINS: PARTICIPATION IN HYDROGEN ECONOMY

- TABLE 199 CUMMINS: COMPANY OVERVIEW

- FIGURE 86 CUMMINS: COMPANY SNAPSHOT

- FIGURE 87 CUMMINS: SALES FOR ENGINE SEGMENT

- TABLE 200 CUMMINS: PRODUCTS OFFERED

- TABLE 201 CUMMINS: PRODUCT PORTFOLIO

- TABLE 202 CUMMINS: PRODUCT DEVELOPMENTS

- TABLE 203 CUMMINS: DEALS

- TABLE 204 CUMMINS: OTHER DEVELOPMENTS

- 16.2.5 DOOSAN GROUP

- TABLE 205 DOOSAN GROUP: COMPANY OVERVIEW

- FIGURE 88 DOOSAN GROUP: COMPANY SNAPSHOT

- TABLE 206 DOOSAN GROUP: PRODUCTS OFFERED

- TABLE 207 DOOSAN GROUP: PRODUCT DEVELOPMENTS

- TABLE 208 DOOSAN GROUP: DEALS

- TABLE 209 DOOSAN GROUP: OTHER DEVELOPMENTS

- 16.2.6 ADVENT TECHNOLOGIES HOLDINGS

- TABLE 210 ADVENT TECHNOLOGIES HOLDINGS: COMPANY OVERVIEW

- FIGURE 89 ADVENT TECHNOLOGIES HOLDINGS: COMPANY SNAPSHOT

- FIGURE 90 ADVENT TECHNOLOGIES HOLDINGS: OFFERINGS

- TABLE 211 ADVENT TECHNOLOGIES HOLDINGS: PRODUCTS OFFERED

- TABLE 212 ADVENT TECHNOLOGIES HOLDINGS: DEALS

- 16.2.7 ITM POWER

- TABLE 213 ITM POWER: COMPANY OVERVIEW

- FIGURE 91 ITM POWER: COMPANY SNAPSHOT

- FIGURE 92 ITM POWER: KEY PARTNERSHIPS

- TABLE 214 ITM POWER: PRODUCTS OFFERED

- TABLE 215 ITM POWER: DEALS

- TABLE 216 ITM POWER: OTHER DEVELOPMENTS

- 16.2.8 CERES POWER

- FIGURE 93 CERES POWER: PROGRESS WITH KEY COMMERCIAL PARTNERSHIP

- TABLE 217 CERES POWER: COMPANY OVERVIEW

- FIGURE 94 CERES POWER: COMPANY SNAPSHOT

- TABLE 218 CERES POWER: PRODUCTS OFFERED

- TABLE 219 CERES POWER: PRODUCT DEVELOPMENTS

- TABLE 220 CERES POWER: DEALS

- TABLE 221 CERES POWER: EXPANSIONS

- 16.2.9 NEDSTACK

- TABLE 222 NEDSTACK: COMPANY OVERVIEW

- TABLE 223 NEDSTACK: PRODUCTS OFFERED

- TABLE 224 NEDSTACK: DEALS

- 16.2.10 PROTON MOTOR POWER SYSTEMS

- TABLE 225 PROTON MOTOR POWER SYSTEMS: COMPANY OVERVIEW

- FIGURE 95 PROTON MOTOR POWER SYSTEMS: COMPANY SNAPSHOT

- TABLE 226 PROTON MOTOR POWER SYSTEMS: PRODUCTS OFFERED

- TABLE 227 PROTON MOTOR POWER SYSTEMS: PRODUCT DEVELOPMENTS

- TABLE 228 PROTON MOTOR POWER SYSTEMS: DEALS

- 16.2.11 TOSHIBA

- TABLE 229 TOSHIBA: COMPANY OVERVIEW

- FIGURE 96 TOSHIBA: COMPANY SNAPSHOT

- FIGURE 97 TOSHIBA: CYBER PHYSICAL SYSTEMS (CPS) TECHNOLOGY

- TABLE 230 TOSHIBA: PRODUCTS OFFERED

- TABLE 231 TOSHIBA: DEALS

- TABLE 232 TOSHIBA: OTHER DEVELOPMENTS

- 16.2.12 POWERCELL AB

- TABLE 233 POWERCELL AB: COMPANY OVERVIEW

- FIGURE 98 POWERCELL AB: COMPANY SNAPSHOT

- TABLE 234 POWERCELL AB: PRODUCTS OFFERED

- TABLE 235 POWERCELL AB: DEALS

- *Details on Business overview, Products offered, Recent developments & MnM View might not be captured in case of unlisted companies.

- 16.3 OTHER PLAYERS

- 16.3.1 PANASONIC

- 16.3.2 TORAY INDUSTRIES

- 16.3.3 SUNRISE POWER CO. LTD

- 16.3.4 BOSCH

- 16.3.5 INTELLIGENT ENERGY

- 16.3.6 SYMBIO

- 16.3.7 ELRINGKLINGER AG

- 16.3.8 SWISS HYDROGEN POWER

- 16.3.9 DANA INCORPORATED

- 16.3.10 FUEL CELL SYSTEM MANUFACTURING LLC

- 16.3.11 VOLKSWAGEN AG

- 16.3.12 DAIMLER

- 16.3.13 RIVERSIMPLE

- 16.3.14 SAIC MOTORS

- 16.3.15 VAN HOOL

- 16.3.16 MEBIUS FUEL CELL

- 16.3.17 HYDRA ENERGY CORPORATION

- 16.3.18 ISUZU MOTORS

- 16.3.19 FORD MOTOR COMPANY

- 16.3.20 FUELCELL ENERGY

- 16.3.21 BLOOM ENERGY

- 16.3.22 SUNFIRE

- 16.3.23 IONOMR INNOVATIONS

- 16.3.24 BRAMBLE ENERGY

17 RECOMMENDATIONS BY MARKETSANDMARKETS

- 17.1 JAPAN, SOUTH KOREA, AND CHINA ARE KEY FOCUS COUNTRIES FOR AUTOMOTIVE FUEL CELL MARKET

- 17.2 TECHNOLOGICAL ADVANCEMENTS TO BOOST MARKET FOR FCEVS

- 17.3 CONCLUSION

18 APPENDIX

- 18.1 KEY INSIGHTS OF INDUSTRY EXPERTS

- 18.2 DISCUSSION GUIDE

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.4.1 AUTOMOTIVE FUEL CELL MARKET, BY PROPULSION AT COUNTRY LEVEL

- 18.4.2 AUTOMOTIVE FUEL CELL MARKET, ADDITIONAL COUNTRIES (UP TO 3)

- 18.4.3 PROFILING OF ADDITIONAL MARKET PLAYERS (UP TO 3)

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS