ブロックチェーンの世界市場:オファリング別、プロバイダー別、タイプ別、展開モード別、組織規模別、業界別、地域別 - 2031年までの予測

Blockchain Market by Offering (Middleware/Web3 Infrastructure, Platforms, Services), Provider (Application, Infrastructure, Middleware), Type (Public, Private, Hybrid, Consortium), Deployment Mode, Vertical, and Region - Global Forecast to 2031- 発行日

- ページ情報

- 英文 556 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 2072268

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

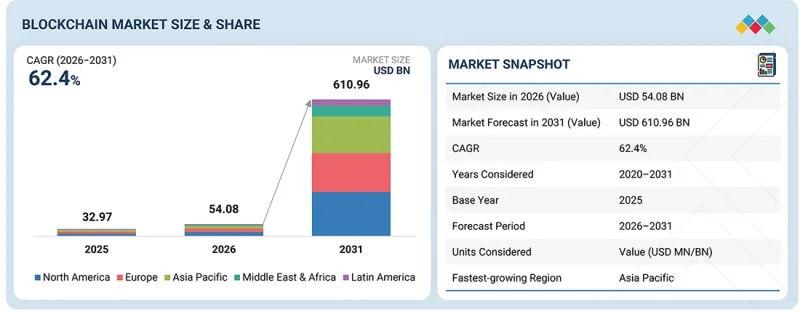

ブロックチェーンの市場規模は、2026年の540億8,000万米ドルから、2031年までに6,109億6,000万米ドルに達すると予測されており、予測期間中のCAGRは62.4%となる見込みです。

この市場は、金融サービス、医療、政府、および企業環境において、安全なデジタルID認証、プライバシーを保護したデータ共有、および規制に準拠した認証に対するニーズの高まりによって牽引されています。組織では、ID詐欺の削減、オンボーディングプロセスの効率化、信頼性の高いデジタルインタラクションの実現を目的として、ブロックチェーンベースの分散型ID(DID)フレームワークや検証可能な資格情報を導入する動きがますます広がっています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2020年~2031年 |

| 基準年 | 2025年 |

| 予測期間 | 2026年~2031年 |

| 算定単位 | 金額(10億米ドル) |

| セグメント | オファリング別、プロバイダー別、タイプ別、展開モード別、組織規模別、業界別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、中東・アフリカ、ラテンアメリカ |

自己主権型アイデンティティ(SSI)、ゼロ知識証明(ZKP)、相互運用可能な認証基準の進展により、導入がさらに加速しています。一方、政府主導のデジタルアイデンティティ構想や、セキュアなAI対応デジタルサービスへの需要の高まりが、引き続き市場の拡大を支えています。

「予測期間中、プロフェッショナルサービスセグメントが最も高いCAGRを記録する見込み」

サービス別に見ると、ブロックチェーン戦略、コンサルティング、実装、統合、およびスマートコントラクト開発における専門的なノウハウへの需要が高まっていることから、予測期間中、ブロックチェーン市場においてプロフェッショナルサービスセグメントが最も高いCAGRを記録すると予想されます。BFSI、政府、小売・Eコマース、ヘルスケア、サプライチェーンの各業界の企業がブロックチェーンの導入を加速させるにつれ、使用事例の評価、適切なブロックチェーンプラットフォームの選定、規制順守の確保、およびブロックチェーンと既存のエンタープライズシステムとの統合を行うためのプロフェッショナルサービスが必要とされています。トークン化、デジタルID、分散型アプリケーション(dApps)、クロスチェーン相互運用性の複雑化が進んでいることも、アドバイザリー、セキュリティ監査、導入サービスへの需要をさらに後押ししています。さらに、組織は、導入リスクの低減、投資収益率(ROI)の最適化、および企業規模でのブロックチェーン変革イニシアチブの加速を図るため、ブロックチェーンコンサルティング会社やシステムインテグレーターへの依存度を高めています。

「2026年には、プライベートブロックチェーンセグメントがブロックチェーン市場で最大のシェアを占める見込み」

タイプ別では、プライベートブロックチェーンセグメントが2026年に最大の市場シェアを占めると予測されています。これは、データプライバシー、セキュリティ、ガバナンス、および規制遵守に関する企業の要件と強く合致しているためです。BFSI(銀行・金融・保険)、政府機関、医療、小売・Eコマース、サプライチェーンなどの分野における組織は、参加者のアクセスや取引の検証に対する管理を維持しつつ、機密情報を安全に共有するために、許可型ブロックチェーンネットワークをますます好むようになっています。プライベートブロックチェーンは、パブリックネットワークよりも高いスループット、低いレイテンシー、優れたスケーラビリティを提供するため、国境を越えた決済、デジタルID、貿易金融、資産のトークン化、サプライチェーンのトレーサビリティといった、ミッションクリティカルなエンタープライズアプリケーションに最適です。Hyperledger Fabric、R3 Corda、Cantonといったエンタープライズプラットフォームの採用拡大に加え、主要ベンダーによるBlockchain-as-a-Service(BaaS)やデジタル資産インフラへの投資増加により、プライベートブロックチェーンセグメントの優位性は引き続き強まっています。

「2026年から2031年にかけて、アジア太平洋地域のブロックチェーン市場において、韓国が最も高い成長率を記録する見込み」

国別に見ると、デジタルイノベーションに対する政府の強力な支援、デジタル決済技術の広範な普及、そして先進的なICTインフラを背景に、予測期間中、韓国がブロックチェーン市場において最も高い成長率を示すと予想されます。Web3エコシステムの育成、デジタル資産のイノベーション、およびブロックチェーンを活用した公共サービスへの注力が、企業によるブロックチェーンの導入を加速させています。金融機関は、決済、資産のトークン化、デジタルID管理の分野で、ブロックチェーンの活用をますます模索しています。さらに、メタバースプラットフォーム、ゲームアプリケーション、分散型技術への投資拡大が、ブロックチェーンソリューションの新たな使用事例を生み出しています。技術的に先進的な韓国の消費者層に加え、安全で透明性の高いデジタル取引への需要の高まりが、市場の成長を後押しし続けています。大手テクノロジー企業の存在と活発なスタートアップエコシステムが、ブロックチェーンのイノベーションと商用化をさらに後押ししています。

ブロックチェーン市場の主要ベンダーには、OVHcloud(フランス)、AWS(米国)、IBM(米国)、Oracle(米国)、Huawei(中国)、Accenture(アイルランド)、TCS(インド)、Google(米国)、Alibaba Cloud(中国)、Microsoft(米国)、SAP(ドイツ)、HPE(米国)、Tencent Cloud(中国)、Wipro(インド)、Infosys(インド)、Lumen Technologies(米国)、DigitalOcean(米国)、VMware(米国)、Linode(Akamai)(米国)、Applied Blockchain(英国)、Consensys(米国)、Contabo(ドイツ)、LeewayHertz(米国)、Vultr(米国)、CloudSigma(スイス)、MEVSPACE(ポーランド)、Scaleway(フランス)、Kaleido(米国)、Chainlink Labs(米国)、Alchemy(米国)、Blockdaemon(米国)、Qubetics(ベリーズ)、CoreWeave(米国)、Hetzner(ドイツ)、T-Cloud Public(ドイツ)、Exoscale(スイス)、UpCloud(フィンランド)、TeraSwitch(米国)、Latitude.sh(ブラジル)、Limestone Networks(米国)、Allnodes(米国)、Cherry Servers(リトアニア)。本調査では、ブロックチェーン市場の主要参入企業に関する詳細な競合分析、各社の企業プロファイル、最近の動向、および主要な市場戦略を網羅しています。

調査範囲

当レポートでは、ブロックチェーン市場をセグメンテーションし、オファリング別、プロバイダー別、タイプ別、展開モード別、組織規模別、業界別、ならびに地域別に分析しています。

また、本調査では、市場の主要参入企業に関する詳細な競合分析、各社の企業プロファイル、製品および事業提供に関する主な観察事項、最近の動向、ならびに主要な市場戦略についても取り上げています。

当レポートを購入する主なメリット

当レポートは、ブロックチェーン市場全体およびそのサブセグメントにおける売上高の最も正確な推計値に関する情報を提供することで、市場をリードする企業や新規参入企業の皆様を支援します。当レポートは、利害関係者の方が競合情勢を理解し、自社のビジネスをより良い位置づけに導き、適切な市場参入戦略を策定するための貴重な洞察を得るのに役立ちます。また、当レポートは、利害関係者の方が市場の動向を把握するのに役立ち、主要な市場促進要因、市場抑制要因、課題、および機会に関する情報を提供します。

当レポートでは、以下のポイントに関する洞察を提供しています:

- 主要な促進要因(実世界資産のトークン化、プライベートおよびパーミッション型ブロックチェーンを通じた企業での導入、Blockchain-as-a-Service(BaaS)およびクラウドの導入、小売、サプライチェーン管理(SCM)、銀行業務における安全かつ透明性の高い取引への需要の高まり)、制約要因(地域ごとに変化し、断片化している規制状況、大規模導入におけるスケーラビリティとパフォーマンスの制限)、機会(ブロックチェーンプラットフォームおよびサービスに関連する政府主導の取り組みの増加、ブロックチェーンと人工知能およびモノのインターネット(IoT)との融合、分散型IDおよびデジタルIDソリューションの採用拡大、分散型金融(DeFi)の成長と従来の金融システムとの統合)、ならびに課題(ブロックチェーンエコシステムにおけるセキュリティ上の脆弱性、プライバシーに関する懸念、および鍵管理上の課題、ブロックチェーンおよびWeb3に関する専門的な技術的ノウハウの不足)

- 製品開発/イノベーション:ブロックチェーン市場における今後の技術、研究開発活動、新製品、およびサービス立ち上げに関する詳細な洞察

- 市場開発:収益性の高い市場に関する包括的な情報--当レポートでは、さまざまな地域にわたるブロックチェーン市場を分析しています

- 市場の多様化:ブロックチェーン市場における新製品・サービス、未開拓地域、最近の動向、および投資に関する網羅的な情報

- 競合分析:ブロックチェーン市場における主要企業(AWS(米国)、IBM(米国)、OVHcloud(フランス)、Huawei(中国)、Oracle(米国)、Accenture(アイルランド)など)の市場シェア、成長戦略、およびサービス提供内容に関する詳細な評価

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズと未開拓分野

- 相互接続された市場と異業種間の機会

- ティア1/2/3参入企業による戦略的な動き

第5章 業界動向

- ポーターの5つの競争要因分析

- マクロ経済指標

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 貿易分析

- 2026年の主要な会議およびイベント

- 顧客企業のビジネスに影響を与える動向と変化

- 投資と資金調達のシナリオ

- 事例研究分析

- 2025年の米国関税がブロックチェーン市場に与える影響

第6章 技術進歩、AIによる影響、特許、イノベーション、そして将来の応用

- 技術分析

- 技術/製品ロードマップ

- ブロックチェーン技術の実装

- 中央集権型/許可型ブロックチェーンと分散型/許可不要型ブロックチェーンの比較

- 特許分析

- 将来の応用

- AI/生成AIがブロックチェーン市場に与える影響

- 成功事例と実世界での応用例

第7章 規制状況

- 地域規制および遵守事項

- 規制機関、政府機関、その他の組織

- 業界標準

第8章 消費者の状況と購買行動

- 意思決定プロセス

- 主要利害関係者と購入基準

- 導入における障壁と内部課題

- 様々な最終用途産業におけるアンメットニーズ

第9章 ブロックチェーン市場(オファリング別)

- インフラストラクチャー

- プラットフォーム

- ミドルウェア/Web3インフラストラクチャ

- サービス

第10章 ブロックチェーン市場(プロバイダー別)

- アプリケーションプロバイダー

- インフラストラクチャプロバイダー

- ミドルウェアプロバイダー

第11章 ブロックチェーン市場(タイプ別)

- パブリック

- プライベート

- ハイブリッド

- コンソーシアム

第12章 ブロックチェーン市場(展開モード別)

- オンプレミス

- クラウド

- ハイブリッド

第13章 ブロックチェーン市場(組織規模別)

- 中小企業

- 大企業

第14章 ブロックチェーン市場(業界別)

- 輸送・物流

- 農業・食品

- 製造業

- エネルギー・公益事業

- ヘルスケア・ライフサイエンス

- メディア、広告、エンターテインメント

- 銀行・金融サービス

- 保険

- IT・通信

- 小売業・Eコマース

- 政府

- 不動産・建設

- その他

第15章 ブロックチェーン市場(地域別)

- 北米

- 北米:ブロックチェーン市場促進要因

- 米国

- カナダ

- 欧州

- 欧州:ブロックチェーン市場促進要因

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- スイス

- オランダ

- その他

- アジア太平洋

- アジア太平洋:ブロックチェーン市場促進要因

- 中国

- 日本

- オーストラリア

- シンガポール

- インド

- 韓国

- その他

- 中東・アフリカ

- 中東・アフリカ:ブロックチェーン市場促進要因

- 湾岸協力会議(GCC)

- 南アフリカ

- その他

- ラテンアメリカ

- ラテンアメリカ:ブロックチェーン市場促進要因

- ブラジル

- メキシコ

- その他

第16章 競合情勢

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- ブランド/製品比較

- 企業評価と財務指標

- 企業評価マトリックス:主要企業、2025年

- 企業評価マトリックス:スタートアップ/中小企業、2025年

- 企業評価マトリックス:ブロックチェーンホスティングインフラストラクチャ市場(主要企業)、2025年

- 競合シナリオと動向

第17章 企業プロファイル

- 主要参入企業

- AWS

- IBM

- ORACLE

- HUAWEI

- ACCENTURE

- OVHCLOUD

- TCS

- ALIBABA

- MICROSOFT

- SAP

- HPE

- HETZNER

- TERASWITCH

- その他の企業

- TENCENT CLOUD

- WIPRO

- INFOSYS

- LUMEN TECHNOLOGIES

- DIGITALOCEAN

- VMWARE

- AKAMAI TECHNOLOGIES

- APPLIED BLOCKCHAIN

- CONSENSYS

- CONTABO

- LEEWAYHERTZ

- VULTR

- CLOUDSIGMA

- MEVSPACE

- SCALEWAY

- KALEIDO

- CHAINLINK LABS

- ALCHEMY

- BLOCKDAEMON

- QUBETICS

- COREWEAVE

- T CLOUD PUBLIC

- EXOSCALE

- UPCLOUD

- LATITUDE.SH

- LIMESTONE NETWORKS

- ALLNODES

- CHERRY SERVERS

第18章 調査手法

第19章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 556 Pages

- 納期

- 即納可能