ヘルスケアITの世界市場 (~2030年):ソリューション・サービス・エンドユーザー (病院・外来手術センター・薬局・保険支払者) 別

Healthcare IT Market by Solution, Service, End User (Hospital, ASC, Pharmacy, Payer) - Global Forecast to 2030- 発行日

- ページ情報

- 英文 691 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 2057476

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

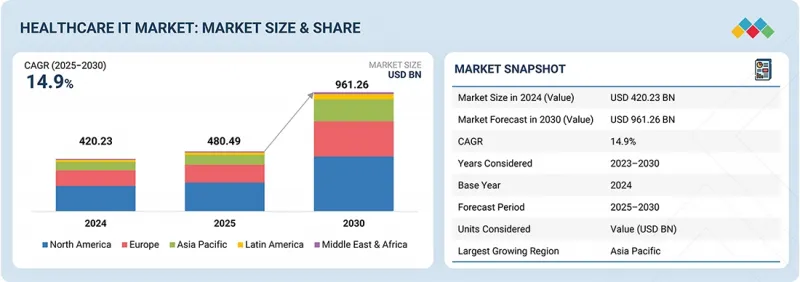

世界のヘルスケアITの市場規模は、2025年の4,804億9,000万米ドルから、2030年には9,612億6,000万米ドルに達すると予測されており、2025年から2030年までのCAGRは14.9%となる見込みです。

技術革新ソリューションの広範な導入が、ヘルスケアIT市場の成長を加速させています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2024年~2030年 |

| 基準年 | 2024 |

| 予測期間 | 2025年~2030年 |

| 単位 | 金額 (米ドル) |

| セグメント | ソリューション・サービス、コンポーネント、エンドユーザー |

| 対象地域 | 北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカ |

2024年8月に発表されたHealthcare誌の記事によると、AIを活用した臨床意思決定支援システムは、腫瘍専門医がエビデンスに基づく治療法を選択する際の支援を行っています。AIの導入により、診断精度が10~15%向上したことが判明しました。さらに、電子カルテ (EHR) の導入拡大がデータのアクセス性を向上させ、高度なヘルスケアITソリューションへの需要を牽引しています。

「遠隔医療ソリューションセグメントは、臨床ヘルスケアIT市場において最大のセグメントになると予測されています」

臨床HCITの分析によると、遠隔医療ソリューションは、一時的・限定的な医療サービスにとどまらず、現在では主流の医療提供モデルの一部として定着しつつあり、予測期間を通じて主要なセグメントとなる見込みです。世界保健機関 (WHO) が提唱した「Global Strategy on Digital Health (2020~2025) 」をはじめ、「Slaintecare Action Plan」、「HSE Corporate Plan」、「Healthy Ireland Actions」などのデジタルヘルス関連の政府主導施策が、特に地域医療、慢性疾患管理、ケアパスウェイ分野におけるテレヘルスソリューションの導入を後押ししています。 また、高齢化の進展に伴い、複数の併存疾患を抱えやすい高齢者のケア負荷が増大しています。こうした患者には継続的なケアが必要であるため、テレヘルスソリューションの導入が全体的に拡大しており、医療システムが人材不足、コスト増加、医療提供能力の不足といった課題に直面する中、この分野は今後も堅調な成長が期待されています。

「エンドユーザー別では、医療提供者のセグメントが2024年に最大の規模を示しました。」

医療提供者は、人材確保の課題を抱えながらも、デジタル化された個別化医療サービスに対する高い需要に対応しなければなりません。同時に、医療システムは、患者の獲得、積極的なケアへの関与、地域社会への貢献を推進しようと努めています。また、財政的に持続可能な価値に基づくケアと人口健康管理という長期的なビジョンを達成するには、患者と従業員の体験を向上させつつ、医療提供者本来の業務である「ケア」に集中できるようにする医療情報技術ソリューションが必要です。これらのことから、患者ケアを改善しつつ業務効率を高めるヘルスケアITソリューションへの需要が高まっています。

「予測期間中、アジア太平洋地域が最も高い成長率を記録する見込みです。」

アジア太平洋市場の成長は、主に医療インフラの改善、技術ソリューションの導入、HCITソリューションの導入に向けた政府の取り組みといった要因によって牽引されています。例えばインドでは、病院認定機関であるNational Accreditation Board for Hospitals (NABH) が、病院情報システム (HIS) および電子診療記録 (EMR) に関する基準やガイドラインを策定したことで、ヘルスケアITソリューションへの需要が大きく高まっています。病院情報システム (HIS) および電子カルテ (EMR) に関する基準とガイドラインを策定するための、国立病院認定委員会 (NABH) による最近の取り組みが、ヘルスケア技術ソリューションへの需要を大幅に牽引しています。2023年9月に導入されたこれらのデジタルヘルス基準に対して、すでに275の病院が認証申請を行い、そのうち100の病院が認証を取得しています。このような規制・制度面での後押しは、ヘルスケアIT市場の成長を促進するだけでなく、高度なデジタルインフラを活用した医療提供体制の構築を通じて、インドの医療サービス全体の高度化にも貢献すると期待されています。

当レポートでは、世界のヘルスケアITの市場を調査し、市場概要、市場成長への各種影響因子の分析、技術・特許の動向、法規制環境、ケーススタディ、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズとホワイトスペース

- 関連市場・異業種との分野横断的機会

- ティア1/2/3企業による戦略的な動き

第5章 業界動向

- ポーターのファイブフォース分析

- マクロ経済指標

- GDPの動向と予測

- 世界のヘルスケアIT業界の動向

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 主な会議およびイベント

- 顧客の事業に影響を与える動向/ディスラプション

- 投資と資金調達のシナリオ

- ケーススタディ分析

- 2025年の米国関税の影響- ヘルスケアIT市場

第6章 技術、特許、デジタル技術、AIの導入による戦略的ディスラプション

- 主要な新興技術

- AIと機械学習

- クラウドコンピューティング

- ビッグデータ&アナリティクス

- 相互運用性および医療情報交換プラットフォーム

- アプリ対応の患者ポータル

- 補完技術

- 医療IoT

- ブロックチェーン

- スマート病院インフラ

- ロボティックプロセスオートメーション

- 隣接技術

- 仮想現実 (VR)・拡張現実 (AR)

- エッジコンピューティング

- 医療ロボット

- 技術/製品ロードマップ

- 特許分析

- 将来の応用

- AIを活用した臨床意思決定支援

- 精密医療とゲノミクスの統合

- 遠隔患者モニタリングとバーチャルケア

- ヘルスケアIT市場における生成AIの影響

第7章 規制状況

- 地域の規制および遵守事項

第8章 顧客情勢と購買行動

- 意思決定プロセス

- ステークホルダーと購入評価基準

- 導入における障壁と内部課題

- 様々なエンドユーザー産業におけるアンメットニーズ

- 市場収益性

第9章 ヘルスケアIT市場:ソリューション・サービス別

- 医療提供者向けソリューション

- 臨床HCITソリューション

- 非臨床ヘルスケアITソリューション

- 医療保険支払者向けソリューション

- 請求管理

- 人口保健管理

- 薬局監査および分析

- 顧客関係管理

- 不正分析ソリューション

- プロバイダーネットワーク管理

- HCITアウトソーシングサービス

- ITインフラ管理

- 支払者向けHCITアウトソーシングサービス

- プロバイダー向けHCITアウトソーシングサービス

- 運用HCITアウトソーシングサービス

第10章 ヘルスケアIT市場:コンポーネント別

- サービス

- ソフトウェア

- ハードウェア

第11章 ヘルスケアIT市場:エンドユーザー別

- 医療提供者

- 病院

- 外来診療センター (外来患者向け施設)

- 在宅医療サービス機関および介護付き住宅施設

- 診断・画像診断センター

- 薬局

- 医療保険支払者

- 公的支払者

- 民間支払者

- ライフサイエンス産業

第12章 ヘルスケアIT市場:地域別

- 北米

- マクロ経済見通し

- 米国

- カナダ

- 欧州

- マクロ経済見通し

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他

- アジア太平洋

- マクロ経済見通し

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- その他

- ラテンアメリカ

- マクロ経済見通し

- ブラジル

- メキシコ

- その他

- 中東・アフリカ

- マクロ経済見通し

- GCC諸国

- 南アフリカ

- その他

第13章 競合情勢

- 概要

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- ブランド比較

- 評価と財務指標

- 企業評価マトリックス:主要企業

- 企業評価マトリックス:スタートアップ/中小企業

- 競合シナリオ

第14章 企業プロファイル

- 主要企業

- OPTUM, INC.

- COGNIZANT

- KONINKLIJKE PHILIPS N.V.

- DELL INC.

- GE HEALTHCARE

- ORACLE

- EPIC SYSTEMS CORPORATION

- VERADIGM LLC

- SAS INSTITUTE INC.

- NUANCE COMMUNICATIONS, INC. (MICROSOFT)

- WIPRO

- ECLINICALWORKS

- INOVALON

- INFOR (KOCH INDUSTRIES)

- CONIFER HEALTH SOLUTIONS, LLC.

- SOLVENTUM

- MERATIVE

- INTERSYSTEMS CORPORATION

- SALESFORCE, INC.

- CITIUSTECH INC

- その他の企業

- CONDUENT, INC.

- CARESTREAM HEALTH

- PRACTICE FUSION, INC.

- TATA CONSULTANCY SERVICES LIMITED

- ELSEVIER

- MEDEANALYTICS, INC.

- MEDECISION

- SURGICAL INFORMATION SYSTEMS

- CHARTIS

- CLEARWAVE CORPORATION

第15章 調査手法

第16章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 691 Pages

- 納期

- 即納可能