スマートホームの世界市場:住居タイプ別、プロトコルおよび通信技術別、製品タイプ別、設置タイプ別、制御インターフェース別、エンドユーザー別、用途別、地域別 - 2032年までの予測

Smart Home Market By Product (Lighting Control, Smart Speaker, Entertainment and Other Controls, Smart Kitchen, HVAC Control, Security & Access Control, Home Healthcare, Home Appliances), Offering (Behavioral, Proactive) - Global Forecast to 2032- 発行日

- ページ情報

- 英文 390 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 2011927

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

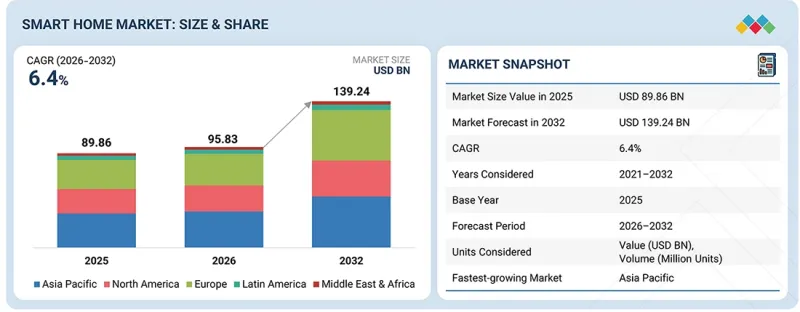

世界のスマートホームの市場規模は、2026年の958億3,000万米ドルから、2032年までに1,392億4,000万米ドルに達すると予測されており、CAGRは6.4%となる見込みです。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2021年~2032年 |

| 基準年 | 2024年 |

| 予測期間 | 2026年~2032年 |

| 対象単位 | 金額(10億米ドル) |

| セグメント | 住居タイプ別、プロトコルおよび通信技術別、製品タイプ別、設置タイプ別、制御インターフェース別、エンドユーザー別、用途別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

スマートホーム市場は、インターネット普及率の向上、コネクテッドデバイスの導入拡大、そして省エネかつ安全な住宅環境への関心の高まりを背景に、着実な成長を遂げています。先進国および新興国の住宅所有者は、利便性の向上、家庭内の安全性の確保、エネルギー消費の最適化を図るため、スマートホームソリューションへの投資を進めています。ブロードバンドインフラの拡充、スマート住宅開発、デジタルライフスタイルの動向が、統合型ホームオートメーションシステムへの需要をさらに加速させています。AIを活用した分析技術、IoTセンサー、音声制御プラットフォーム、クラウドベースのホームマネジメントシステムの進歩により、システムの相互運用性が向上し、ユーザー体験が向上するとともに、リアルタイムの監視と自動化が可能になっています。住宅のデジタル化が進み続ける中、拡張性が高く、信頼性があり、統合されたスマートホームエコシステムへの需要は、予測期間を通じて着実に増加すると見込まれています。

スマートキッチンセグメントは、コネクテッド家電の普及拡大と利便性を重視した家庭内オートメーションへの需要の高まりを背景に、予測期間中にスマートホーム市場で最も急速な成長を記録すると見込まれています。スマート冷蔵庫、コネクテッドオーブン、インテリジェント食器洗い機、音声対応調理アシスタントに対する消費者の嗜好の高まりが、住宅における製品の普及を加速させています。IoT対応家電、省エネ技術、アプリベースの遠隔モニタリングの進歩により、キッチン環境におけるユーザーの制御性、安全性、およびエネルギー効率の最適化が向上しています。消費者が統合された自動化された調理体験をますます求める中、メーカーはAIを活用した機能や相互運用性への投資を進めており、スマートキッチンセグメントは最も急速に成長する製品タイプとして位置づけられています。

販売チャネル別に見ると、メーカーがブランドウェブサイト、直営店、認定設置ネットワークを通じて消費者と直接関わるケースが増加しているため、スマートホーム市場において直販セグメントが圧倒的なシェアを占めると予想されます。消費者への直接販売戦略により、企業は価格設定の主導権を維持し、顧客エンゲージメントを強化し、設置からアフターサービスまで一貫したサポートを提供することが可能になります。カスタマイズされたスマートホームソリューションや専門的なシステム統合への需要が高まる中、直販チャネルはバンドル販売や技術的専門知識を通じて、より大きな価値を提供しています。ブランドのエコシステムに対する消費者の信頼が高まるにつれ、スマートホーム市場において、直接販売は引き続き主要な流通チャネルであり続けると予測されています。

北米は、高いインターネット普及率、コネクテッド技術の早期導入、およびホームオートメーションのメリットに対する消費者の高い認識に牽引され、2026年にはスマートホーム市場で最大のシェアを占めると予測されています。同地域は、先進的なデジタルインフラ、スマートデバイスの広範な普及、そして主要テクノロジープロバイダーの強力な存在感という恩恵を受けています。省エネ住宅、スマートセキュリティシステム、音声対応オートメーションソリューションへの需要の高まりが、米国およびカナダ全域での市場拡大を後押しし続けています。住宅分野のデジタルトランスフォーメーションが加速する中、北米は世界のスマートホーム市場において主導的な地位を維持すると予想されます。

スマートホーム市場は、Johnson Controls Inc.(アイルランド)、Honeywell International Inc.(米国)、Schneider Electric(フランス)、Siemens(ドイツ)、ASSA ABLOY(スウェーデン)、Amazon.com, Inc.(米国)、Apple Inc.(米国)、ADT(米国)、Robert Bosch(ドイツ)、ABB(スイス)など、数社の世界的に確立された企業が支配しています。本調査では、スマートホーム市場におけるこれらの主要企業について、企業プロファイル、最近の動向、および主要な市場戦略を含む詳細な競合分析を行っています。

調査範囲

当レポートでは、スマートホーム市場をセグメント化し、製品タイプ、設置形態、販売チャネル、提供サービス、および地域別に市場規模を予測しています。また、市場の成長に影響を与える促進要因、抑制要因、機会、課題について包括的な分析を提供しています。当レポートは、市場の定性的および定量的両面の側面を網羅しています。

当レポートを購入する理由:

当レポートは、スマートホーム市場全体および関連セグメントのおおよその売上高データを提供することで、この市場のリーダーや新規参入企業を支援します。当レポートは、利害関係者が競合情勢を理解し、市場での地位を強化し、効果的な市場参入戦略を策定するための深い洞察を得るのに役立ちます。また、当レポートは利害関係者が市場の動向を把握するのに役立ち、主要な促進要因、抑制要因、機会、課題に関する情報を提供します。

当レポートでは、以下のポイントに関する洞察を提供します:

- 主要な促進要因の分析(インターネットユーザーの増加とスマートデバイスの普及拡大、新興国における可処分所得の増加、遠隔地におけるホームモニタリングの重要性の高まり、省エネおよび低炭素排出志向のソリューションへの需要の高まり、一般市民の間での安全性、セキュリティ、利便性に関する懸念)。制約要因(必要性よりも利便性を重視する市場、既存のスマートデバイス利用者における切り替えコストの高さ、セキュリティおよびプライバシー侵害に関連する問題)、機会(グリーンビルディングを促進する好意的な政府規制、データ接続技術を内蔵した照明コントローラーの採用、スマートホームへの電力線通信技術の統合)、課題(異種システム間の連携の難しさ、機能の限定、オープンスタンダードの欠如、デバイスの誤動作リスク)

- 製品開発/イノベーション:スマートホーム市場における今後の技術、研究開発活動、および製品発売に関する詳細な洞察

- 市場開発:様々な地域におけるスマートホーム市場の分析を通じた、収益性の高い市場に関する包括的な情報

- 市場の多様化:スマートホーム市場における新製品、未開拓地域、最近の動向、および投資に関する網羅的な情報

- 競合分析:Johnson Controls Inc.(アイルランド)、Honeywell International Inc.(米国)、Schneider Electric(フランス)、Siemens(ドイツ)、ASSA ABLOY(スウェーデン)、Amazon.com, Inc.(米国)、Apple Inc.(米国)、ADT(米国)、Robert Bosch(ドイツ)、ABB(スイス)など、スマートホーム市場における主要企業の市場シェア、成長戦略、サービス提供内容に関する詳細な評価

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 相互接続された市場と異業種間の機会

- ティア1/2/3企業による戦略的な動き

第5章 業界動向

- ポーターの5つの競争要因分析

- マクロ経済見通し

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 貿易分析

- 2026年~2027年の主な会議およびイベント

- 顧客ビジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ

- 事例研究分析

- 米国関税がスマートホーム市場に与える影響

第6章 技術進歩、AIによる影響、特許、イノベーション

- 主要技術

- 補完的技術

- 技術/製品ロードマップ

- 特許分析

- AIがスマートホーム市場に与える影響

第7章 規制状況

- 地域規制およびコンプライアンス

- 規制機関、政府機関、その他の組織

- 法律および指令

- 業界標準

- 地域規制

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 購買プロセスに関わる主要な利害関係者とその評価基準

- 導入における障壁と内部課題

- 様々なエンドユーザーのアンメットニーズ

- 市場収益性

第9章 スマートホームインフラストラクチャで使用される技術

- IoT接続

- AIと機械学習

- 音声認識

- コンピュータビジョン

- エッジコンピューティング

第10章 スマートホーム市場(住居タイプ別)

- 一戸建て住宅

- 集合住宅

- ヴィラ/高級住宅

第11章 スマートホーム市場(プロトコルおよび通信技術別)

- 有線

- 無線

第12章 スマートホーム市場(製品タイプ別)

- スマート照明ソリューション

- スマートセキュリティ&アクセス制御システム

- スマートHVACソリューション

- スマートエンターテイメントおよびその他のシステム

- スマートヘルスケアソリューション

- スマートキッチン家電

- スマートホームガジェット

- スマート家具

第13章 スマートホーム市場(設置タイプ別)

- 新規設置

- 改修設置

第14章 スマートホーム市場(制御インターフェース別)

- スマートフォン/タブレット用アプリケーション

- 音声アシスタント

- 壁パネルとスイッチ

- ウェアラブル

第15章 スマートホーム市場(エンドユーザー別)

- 個人住宅所有者

- 住宅建設業者および開発業者

- 賃貸住宅のオーナーおよび運営者

第16章 スマートホーム市場(用途別)

- 安全とセキュリティ

- 快適さと利便性

- エネルギー管理

- エンターテインメント

- 健康とウェルネス

- その他

第17章 スマートホーム市場(地域別)

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- 北欧諸国

- その他

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- シンガポール

- オーストラリア

- 東南アジア

- その他

- 南米

- ブラジル

- アルゼンチン

- その他

- 中東・アフリカ

- 南アフリカ

- GCC諸国

- その他

第18章 競合情勢

- 概要

- 主要参入企業の競争戦略/強み、2022年9月~2026年2月

- 市場シェア分析、2025年

- 収益分析、2021年~2025年

- 企業評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要企業、2025年

- 企業評価マトリックス:スタートアップ/中小企業、2025年

- 競合シナリオ

第19章 企業プロファイル

- 主要参入企業

- JOHNSON CONTROLS

- SCHNEIDER ELECTRIC

- SIEMENS

- HONEYWELL INTERNATIONAL INC.

- ASSA ABLOY

- ADT

- ROBERT BOSCH GMBH

- ABB

- APPLE INC.

- AMAZON.COM, INC.

- SIGNIFY HOLDING

- ACUITY INC.

- LEGRAND

- DAIKIN INDUSTRIES LTD.

- CARRIER

- その他の企業

- PANASONIC HOLDINGS CORPORATION

- ZUMTOBEL GROUP

- EMERSON ELECTRIC CO.

- AMS-OSRAM AG

- RESIDEO TECHNOLOGIES INC.

- SAMSUNG

- SONY GROUP CORPORATION

- OOMA, INC.

- WOZART TECHNOLOGIES PRIVATE LIMITED

- AXIS COMMUNICATIONS AB

- COMCAST

- ECOBEE

- CRESTRON ELECTRONICS, INC.

- SIMPLISAFE, INC.

- SAVANT SYSTEMS, INC

- SMARTFROG LTD.

- LG ELECTRONICS

- LUTRON

- HANGZHOU HIKVISION DIGITAL TECHNOLOGIES

- WIPRO LIGHTING

- INTER IKEA SYSTEMS B.V.

- LENNOX INTERNATIONAL INC.

- U-TEC GROUP INC.

- ALARM.COM

- HAVELLS INDIA LTD.

第20章 調査手法

第21章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 390 Pages

- 納期

- 即納可能