ポリ乳酸の世界市場:グレード別、原材料別、用途別、最終用途産業別、地域別 - 2030年までの予測

Polylactic Acid Market by Grade, Application, End-use Industry, Raw Material, and Region - Global Forecast to 2030- 発行日

- ページ情報

- 英文 268 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1798377

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

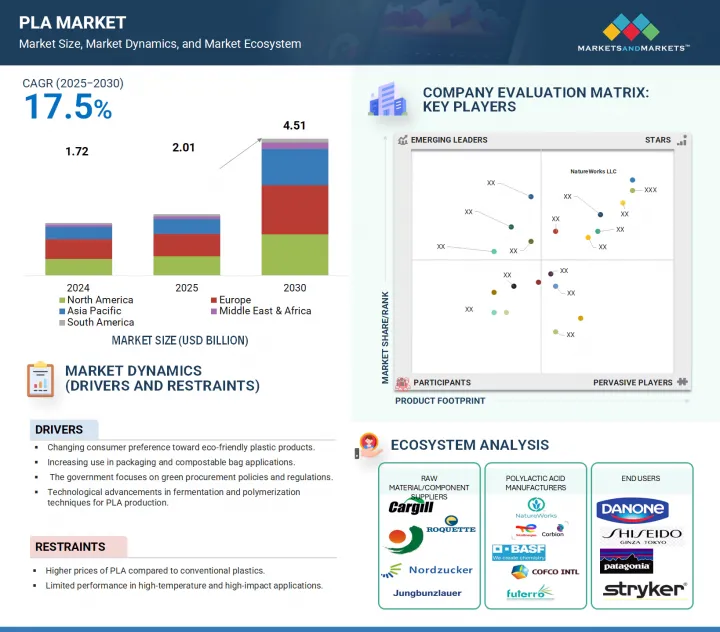

世界のポリ乳酸(PLA)の市場規模は、2025年の20億1,000万米ドルから2030年には45億1,000万米ドルに拡大し、予測期間のCAGRは17.5%になると予想されています。

この成長の多くは、食品・飲料分野における堆肥化可能なパッケージングに対する需要の増加と、特にアジア太平洋、欧州、北米地域における新しい大規模な工業用PLA生産工場の立ち上がりによるものです。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2023年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 検討単位 | 金額(100万/10億米ドル)数量(KT) |

| セグメント | グレード別、原材料別、用途別、最終用途産業別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

さらに、耐熱性やケミカルリサイクルが可能なPLAの開発が進んでおり、自動車、エレクトロニクス、耐久消費財などの用途で、より幅広い市場開拓の機会が生まれています。バイオ精製工場への投資、原料の多様化、持続可能なパッケージングを開発するブランドによるコミットメントに支えられ、市場開拓の見通しは引き続き明るいです。バイオ医療機器市場、複合材料、低炭素製造システムにおける新たな用途も、長期的な成長機会をもたらすと思われます。

フィルムとシートの用途分野は、PLA市場で2番目に急成長するセグメントとなる見込みです。PLAフィルムは、その優れた透明性、密封性、用途によっては生分解性により、フレキシブル食品包装、農業用マルチフィルム、パーソナルケア用包装材、さまざまなラベル用途など、さまざまな用途に使用されています。この市場セグメントでは、従来の多層プラスチックフィルムからの世界のシフトと、認証された堆肥化可能な包装製品に対する需要の高まりにより、PLAベースのフィルムを代替品として採用することが容易になっています。堆肥化可能なパッケージングにおける世界のイニシアチブを支援したプロジェクトでは、ウェイト・トゥ・ラミネート、サーモシール、コーティング用途、および持続可能な製品を積極的に追求するその他のセグメントで、PLAベースのフィルムの使用が増加していることを示しています。

押出グレードのPLAセグメントは、包装、建築、消費者用途におけるバイオベースのシート、フィルム、プロファイルの需要増加により、2024年のPLA市場で2番目に急成長するセグメントとなっています。PLAは、標準的な押出装置を利用できること、耐熱性、機械的安定性が向上していることから、硬質・軟質のいずれのアプローチにおいても、従来のポリマーに代わる有力な代替品と考えられています。クラムシェル容器、ブリスターパック、ラミネート材料、その他のパッケージング製品、特に成形性、透明性、堆肥化性が必要な場合に有効な代替品としての利用が増加しているため、押出成形分野はさらに進展しています。食品包装や工業用シート市場がより持続可能な素材へとシフトする中、押出グレードのPLAセグメントは安価な代替品を提供すると同時に、大規模で効率的な加工を実現し、環境への全体的な影響を軽減します。共押出や多層PLA構造などの他の革新は、このセグメントの国際的な足跡を増やすのに役立つと思われます。

コーンスターチセグメントは、2024年にサトウキビに次いで2番目に急成長したPLA原料供給源です。トウモロコシデンプンは、特に北米、欧州、中国において、乳酸発酵のための最も顕著で容易に入手可能な原料であり続けています。強力なサプライチェーン、競争力のある価格、高い発酵可能糖分という利点があり、大規模なPLA生産にとって魅力的です。トウモロコシを原料とするPLAの市場開拓は、特にトウモロコシの加工インフラが確立している新興国市場における、生分解性パッケージングや農業用フィルムに対する消費者や規制当局の需要の増加によって支えられています。さらに、非遺伝子組み換えの畑のトウモロコシを発酵させ、より炭素効率の高い生産方法を開発する研究が進行中であることから、持続可能性に対する認識が高まり、トウモロコシデンプンのマーケティング見通しが向上する可能性が高いです。

中東・アフリカは、2024年にPLA地域市場の中で2番目に急成長すると予想されています。プラスチック汚染に対する意識の高まり、バイオベースの代替パッケージングの採用、持続可能な開発目標(SDGs)に向けた同地域の推進が開発の原動力となっています。中東・アフリカの各国政府は使い捨てプラスチックを削減するための法律を導入しており、同地域で事業を展開する多国籍FMCG企業は持続可能性の誓約のためにPLAベースの材料にシフトしています。さらに、湾岸諸国、南アフリカ、北アフリカ諸国の食品包装、消費財、農業セクターの拡大は、PLA採用の有望な基盤となっています。この地域はまた、バイオマス資源へのコスト競争力のあるアクセスを提供し、グリーンテクノロジーとバイオベース産業への海外直接投資を誘致しており、PLA市場の成長をさらに促進しています。

対象企業:NatureWorks LLC(米国)、TotalEnergies Corbion(オランダ)、BASF SE(ドイツ)、COFCO(中国)、Futerro(ベルギー)、Danimer Scientific(米国)、東レ株式会社(日本)、Evonik Industries(ドイツ)、三菱化学株式会社(日本)、株式会社ユニチカ(日本)を対象とします。

本調査には、PLA市場におけるこれら主要企業の企業プロファイル、最近の動向、主な市場戦略など、詳細な競合分析が含まれています。

調査対象

この調査レポートは、PLA市場をグレード(熱成形グレード、射出成形グレード、押出成形グレード、ブロー成形グレード)、用途(硬質熱成形品、フィルム&シート、ボトル)、最終用途産業(包装、消費財、農業、繊維、バイオ医療)、原料(サトウキビ、コーンスターチ、キャッサバ、サトウキビ)、地域(アジア太平洋、北米、欧州、南米、中東&アフリカ)に基づいて分類しています。本レポートの調査範囲には、PLA市場の成長に影響を与える促進要因・市場抑制要因・課題・機会に関する詳細情報が含まれています。主要な業界プレイヤーの包括的な分析により、事業概要、提供製品、PLA市場に関連する提携、契約、製品発売、事業拡大、買収などの主要戦略に関する洞察を提供します。さらに、PLA業界のエコシステムにおける新興新興企業の競合分析も掲載しています。

当レポートは、PLA市場全体とそのサブセグメントの収益推計値を市場リーダーや新規参入者に提供します。本レポートは、利害関係者が競合情勢を理解し、事業のポジショニングについてより良い考察を得、適切な市場開拓戦略を策定するのに役立ちます。また、利害関係者が市場の鼓動を理解し、市場促進要因・課題に関する情報を提供するのにも役立ちます。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- ポリ乳酸市場における魅力的な機会

- ポリ乳酸市場(グレード別)

- ポリ乳酸市場(原材料別)

- ポリ乳酸市場(用途別)

- ポリ乳酸市場(最終用途産業別)

- ポリ乳酸市場(国別)

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ポーターのファイブフォース分析

- バリューチェーン分析

- 特許分析

- 価格分析

- ポリ乳酸の平均販売価格(地域別、2022年~2030年)

- ポリ乳酸の平均販売価格(グレード別、2022年~2030年)

- ポリ乳酸の平均販売価格(最終用途産業別、2024年)

- 2024年における市場上位3社別平均販売価格

- ポリ乳酸の製造方法

- 原材料分析

- エコシステム/市場マッピング

- ケーススタディ

- 規制状況

- 貿易分析

- 顧客ビジネスに影響を与える動向/混乱

- 2025年~2026年の主な会議とイベント

- 購入決定に影響を与える主な要因

- 技術分析

第6章 ポリ乳酸市場(グレード別)

- イントロダクション

- 熱成形

- 射出成形

- 押出

- ブロー成形

- その他

第7章 ポリ乳酸市場(原材料別)

- イントロダクション

- サトウキビ

- コーンスターチ

- キャッサバ

- サトウダイコン

- その他

第8章 ポリ乳酸市場(用途別)

- イントロダクション

- 硬質熱成形品

- フィルムとシート

- ボトル

- その他

第9章 ポリ乳酸市場(最終用途産業別)

- イントロダクション

- 包装

- 消費財

- 農業

- 繊維

- バイオメディカル

- その他

第10章 ポリ乳酸市場(地域別)

- イントロダクション

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- その他

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他

第11章 競合情勢

- 概要

- 主要参入企業の戦略

- 市場シェア分析

- 収益分析

- 企業評価と財務指標

- 製品/ブランド比較

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業、2024年

- 競合シナリオ

第12章 企業プロファイル

- 主要参入企業

- NATUREWORKS LLC

- TOTALENERGIES CORBION

- BASF SE

- COFCO

- FUTERRO

- DANIMER SCIENTIFIC

- TORAY INDUSTRIES, INC.

- EVONIK INDUSTRIES

- MITSUBISHI CHEMICAL GROUP CORPORATION

- UNITIKA LTD.

- その他の企業

- BIOWORKS CORPORATION

- ADBIOPLASTICS

- MUSASHINO CHEMICAL LABORATORY, LTD.

- HANGZHOU PEIJIN CHEMICAL CO.,LTD.

- AKRO-PLASTIC GMBH

- FUJIAN GREENJOY BIOMATERIAL CO., LTD.

- PLAMFG

- FKUR

- OTTO CHEMIE PVT. LTD.

- RAGHAV POLYMERS

- VAISHNAVI BIO TECH

- HENAN SINOWIN CHEMICAL INDUSTRY CO., LTD.

- EMNANDI BIOPLASTICS

- UNILONG INDUSTRY CO., LTD.

- PRAJ INDUSTRIES

第13章 付録

図表

List of Tables

- TABLE 1 POLYLACTIC ACID MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 ADVERSE HEALTH EFFECTS DUE TO USE OF CONVENTIONAL PLASTICS

- TABLE 3 PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 TOTAL NUMBER OF PATENTS

- TABLE 5 TOP TEN PATENT OWNERS

- TABLE 6 ECOSYSTEM

- TABLE 7 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 IMPORT DATA FOR HS CODE 390770-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024

- TABLE 9 EXPORT DATA FOR HS CODE 390770-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024

- TABLE 10 DETAILED LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 11 POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (USD MILLION)

- TABLE 12 POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (USD MILLION)

- TABLE 13 POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (KILOTON)

- TABLE 14 POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (KILOTON)

- TABLE 15 POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (USD MILLION)

- TABLE 16 POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (USD MILLION)

- TABLE 17 POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (KILOTON)

- TABLE 18 POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (KILOTON)

- TABLE 19 POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 20 POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 21 POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 22 POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 23 POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 24 POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 25 POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 26 POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 27 POLYLACTIC ACID MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 28 POLYLACTIC ACID MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 29 POLYLACTIC ACID MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 30 POLYLACTIC ACID MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 31 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 32 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 33 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 34 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 35 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 36 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 37 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 38 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 39 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (USD MILLION)

- TABLE 40 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (USD MILLION)

- TABLE 41 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (KILOTON)

- TABLE 42 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (KILOTON)

- TABLE 43 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (USD MILLION)

- TABLE 44 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (USD MILLION)

- TABLE 45 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (KILOTON)

- TABLE 46 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (KILOTON)

- TABLE 47 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 48 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 49 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 50 ASIA PACIFIC: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 51 CHINA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 52 CHINA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 53 CHINA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 54 CHINA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 55 INDIA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 56 INDIA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 57 INDIA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 58 INDIA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 59 JAPAN: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 60 JAPAN: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 61 JAPAN: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 62 JAPAN: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 63 SOUTH KOREA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 64 SOUTH KOREA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 65 SOUTH KOREA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 66 SOUTH KOREA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 67 REST OF ASIA PACIFIC: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 68 REST OF ASIA PACIFIC: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 69 REST OF ASIA PACIFIC: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 70 REST OF ASIA PACIFIC: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 71 EUROPE: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 72 EUROPE: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 73 EUROPE: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 74 EUROPE: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 75 EUROPE: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 76 EUROPE: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 77 EUROPE: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 78 EUROPE: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 79 EUROPE: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (USD MILLION)

- TABLE 80 EUROPE: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (USD MILLION)

- TABLE 81 EUROPE: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (KILOTON)

- TABLE 82 EUROPE: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (KILOTON)

- TABLE 83 EUROPE: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (USD MILLION)

- TABLE 84 EUROPE: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (USD MILLION)

- TABLE 85 EUROPE: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (KILOTON)

- TABLE 86 EUROPE: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (KILOTON)

- TABLE 87 EUROPE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 88 EUROPE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 89 EUROPE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 90 EUROPE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 91 GERMANY: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 92 GERMANY: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 93 GERMANY POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 94 GERMANY POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 95 UK: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 96 UK: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 97 UK: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 98 UK: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 99 FRANCE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 100 FRANCE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 101 FRANCE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 102 FRANCE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 103 ITALY: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 104 ITALY: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 105 ITALY: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 106 ITALY: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 107 SPAIN: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 108 SPAIN: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 109 SPAIN: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 110 SPAIN: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 111 REST OF EUROPE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 112 REST OF EUROPE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 113 REST OF EUROPE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 114 REST OF EUROPE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 115 NORTH AMERICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 116 NORTH AMERICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 117 NORTH AMERICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 118 NORTH AMERICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 119 NORTH AMERICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 120 NORTH AMERICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 121 NORTH AMERICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 122 NORTH AMERICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 123 NORTH AMERICA: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (USD MILLION)

- TABLE 124 NORTH AMERICA: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (USD MILLION)

- TABLE 125 NORTH AMERICA: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (KILOTON)

- TABLE 126 NORTH AMERICA: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (KILOTON)

- TABLE 127 NORTH AMERICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (USD MILLION)

- TABLE 128 NORTH AMERICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (USD MILLION)

- TABLE 129 NORTH AMERICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (KILOTON)

- TABLE 130 NORTH AMERICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (KILOTON)

- TABLE 131 NORTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 132 NORTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 133 NORTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 134 NORTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 135 US: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 136 US: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 137 US: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 138 US: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 139 CANADA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 140 CANADA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 141 CANADA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 142 CANADA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 143 MEXICO: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 144 MEXICO: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 145 MEXICO: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 146 MEXICO: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 147 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 148 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 149 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 150 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 151 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 152 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 153 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 154 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 155 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (USD MILLION)

- TABLE 156 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (USD MILLION)

- TABLE 157 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (KILOTON)

- TABLE 158 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (KILOTON)

- TABLE 159 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (USD MILLION)

- TABLE 160 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (USD MILLION)

- TABLE 161 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (KILOTON)

- TABLE 162 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (KILOTON)

- TABLE 163 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 164 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 165 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 166 SOUTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 167 BRAZIL: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 168 BRAZIL: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 169 BRAZIL: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 170 BRAZIL: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 171 REST OF SOUTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 172 REST OF SOUTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 173 REST OF SOUTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 174 REST OF SOUTH AMERICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 175 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 176 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 177 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 178 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 179 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 180 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 181 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 182 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 183 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (USD MILLION)

- TABLE 184 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (USD MILLION)

- TABLE 185 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY GRADE, 2022-2024 (KILOTON)

- TABLE 186 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY GRADE, 2025-2030 (KILOTON)

- TABLE 187 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (USD MILLION)

- TABLE 188 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (USD MILLION)

- TABLE 189 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2022-2024 (KILOTON)

- TABLE 190 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY RAW MATERIAL, 2025-2030 (KILOTON)

- TABLE 191 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 192 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 193 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 194 MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 195 SAUDI ARABIA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 196 SAUDI ARABIA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 197 SAUDI ARABIA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 198 SAUDI ARABIA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 199 UAE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 200 UAE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 201 UAE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 202 UAE: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 203 REST OF MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (USD MILLION)

- TABLE 204 REST OF MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 205 REST OF MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2022-2024 (KILOTON)

- TABLE 206 REST OF MIDDLE EAST & AFRICA: POLYLACTIC ACID MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 207 POLYLACTIC ACID MARKET: OVERVIEW OF MAJOR STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2020-JUNE 2025

- TABLE 208 POLYLACTIC ACID MARKET: DEGREE OF COMPETITION, 2024

- TABLE 209 POLYLACTIC ACID MARKET: REGION FOOTPRINT

- TABLE 210 POLYLACTIC ACID MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 211 POLYLACTIC ACID MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 212 POLYLACTIC ACID MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 213 POLYLACTIC ACID MARKET: PRODUCT LAUNCHES, JANUARY 2020-JUNE 2025

- TABLE 214 POLYLACTIC ACID MARKET: DEALS, JANUARY 2020-JUNE 2025

- TABLE 215 POLYLACTIC ACID MARKET: EXPANSIONS, JANUARY 2020-JUNE 2025

- TABLE 216 NATUREWORKS LLC : COMPANY OVERVIEW

- TABLE 217 NATUREWORKS LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 218 NATUREWORKS LLC: PRODUCT LAUNCHES, JANUARY 2020-JUNE 2025

- TABLE 219 NATUREWORKS LLC: DEALS, JANUARY 2020-JUNE 2025

- TABLE 220 NATUREWORKS LLC: EXPANSIONS, JANUARY 2020-JUNE 2025

- TABLE 221 TOTALENERGIES CORBION: COMPANY OVERVIEW

- TABLE 222 TOTALENERGIES CORBION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 223 TOTALENERGIES CORBION: PRODUCT LAUNCHES, JANUARY 2020-JUNE 2025

- TABLE 224 TOTALENERGIES CORBION: DEALS, JANUARY 2020-JUNE 2025

- TABLE 225 TOTALENERGIES CORBION: EXPANSIONS, JANUARY 2020-JUNE 2025

- TABLE 226 BASF SE: COMPANY OVERVIEW

- TABLE 227 BASF SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 228 BASF SE: DEALS, JANUARY 2020-JUNE 2025

- TABLE 229 BASF SE: EXPANSIONS, JANUARY 2020-JUNE 2025

- TABLE 230 COFCO: COMPANY OVERVIEW

- TABLE 231 COFCO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 232 FUTERRO: COMPANY OVERVIEW

- TABLE 233 FUTERRO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 234 FUTERRO: EXPANSIONS, JANUARY 2020-JUNE 2025

- TABLE 235 DANIMER SCIENTIFIC: COMPANY OVERVIEW

- TABLE 236 DANIMER SCIENTIFIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 DANIMER SCIENTIFIC: DEALS, JANUARY 2020-JUNE 2025

- TABLE 238 DANIMER SCIENTIFIC: EXPANSIONS, JANUARY 2020-JUNE 2025

- TABLE 239 TORAY INDUSTRIES, INC.: COMPANY OVERVIEW

- TABLE 240 TORAY INDUSTRIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 DANIMER SCIENTIFIC: PRODUCT LAUNCHES, JANUARY 2020-JUNE 2025

- TABLE 242 EVONIK INDUSTRIES: COMPANY OVERVIEW

- TABLE 243 EVONIK INDUSTRIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 244 EVONIK INDUSTRIES: PRODUCT LAUNCHES, JANUARY 2020-JUNE 2025

- TABLE 245 EVONIK INDUSTRIES: DEALS, JANUARY 2020-JUNE 2025

- TABLE 246 MITSUBISHI CHEMICAL GROUP CORPORATION: COMPANY OVERVIEW

- TABLE 247 MITSUBISHI CHEMICAL GROUP CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 248 UNITIKA LTD.: COMPANY OVERVIEW

- TABLE 249 UNITIKA LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 250 BIOWORKS CORPORATION: COMPANY OVERVIEW

- TABLE 251 ADBIOPLASTICS: COMPANY OVERVIEW

- TABLE 252 MUSASHINO CHEMICAL LABORATORY, LTD. : COMPANY OVERVIEW

- TABLE 253 HANGZHOU PEIJIN CHEMICAL CO.,LTD.: COMPANY OVERVIEW

- TABLE 254 AKRO-PLASTIC GMBH: COMPANY OVERVIEW

- TABLE 255 FUJIAN GREENJOY BIOMATERIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 256 PLAMFG: COMPANY OVERVIEW

- TABLE 257 FKUR: COMPANY OVERVIEW

- TABLE 258 OTTO CHEMIE PVT. LTD.: COMPANY OVERVIEW

- TABLE 259 RAGHAV POLYMERS: COMPANY OVERVIEW

- TABLE 260 VAISHNAVI BIO TECH: COMPANY OVERVIEW

- TABLE 261 HENAN SINOWIN CHEMICAL INDUSTRY CO.,LTD.: COMPANY OVERVIEW

- TABLE 262 EMNANDI BIOPLASTICS: COMPANY OVERVIEW

- TABLE 263 UNILONG INDUSTRY CO., LTD.: COMPANY OVERVIEW

- TABLE 264 PRAJ INDUSTRIES: COMPANY OVERVIEW

List of Figures

- FIGURE 1 POLYLACTIC ACID MARKET: SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 POLYLACTIC ACID MARKET: RESEARCH DESIGN

- FIGURE 3 POLYLACTIC ACID MARKET: BOTTOM-UP APPROACH

- FIGURE 4 POLYLACTIC ACID MARKET: TOP-DOWN APPROACH

- FIGURE 5 POLYLACTIC ACID MARKET: DATA TRIANGULATION

- FIGURE 6 THERMOFORMING GRADE TO LEAD POLYLACTIC ACID MARKET DURING FORECAST PERIOD

- FIGURE 7 SUGARCANE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 8 RIGID THERMOFORMS APPLICATION TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 9 PACKAGING INDUSTRY TO DOMINATE OVERALL POLYLACTIC ACID MARKET BETWEEN 2025 AND 2030

- FIGURE 10 EUROPE LED POLYLACTIC ACID MARKET IN 2024

- FIGURE 11 ASIA PACIFIC OFFERS ATTRACTIVE OPPORTUNITIES IN POLYLACTIC ACID MARKET DURING FORECAST PERIOD

- FIGURE 12 THERMOFORMING GRADE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 13 SUGARCANE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 14 RIGID THERMOFORMS APPLICATION TO WITNESS HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 15 PACKAGING SEGMENT TO LEAD MARKET BY 2030

- FIGURE 16 MARKET IN JAPAN TO REGISTER HIGHEST CAGR FROM 2025 TO 2030

- FIGURE 17 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN POLYLACTIC ACID MARKET

- FIGURE 18 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 19 OVERVIEW OF POLYLACTIC ACID MARKET VALUE CHAIN

- FIGURE 20 TOTAL NUMBER OF PATENTS DURING LAST 10 YEARS

- FIGURE 21 PATENT ANALYSIS, BY LEGAL STATUS

- FIGURE 22 TOP JURISDICTIONS FOR POLYLACTIC ACID PATENTS

- FIGURE 23 TOP 10 COMPANIES/APPLICANTS WITH HIGHEST NUMBER OF PATENTS

- FIGURE 24 AVERAGE SELLING PRICE, BY REGION, 2022-2030 (USD/KG)

- FIGURE 25 AVERAGE SELLING PRICE, BY GRADE, 2022-2030 (USD/KG)

- FIGURE 26 AVERAGE SELLING PRICE, BY END-USE INDUSTRY, 2024 (USD/KG)

- FIGURE 27 AVERAGE SELLING PRICE, BY TOP THREE MARKET PLAYERS, 2024 (USD/KG)

- FIGURE 28 ECOSYSTEM MAPPING

- FIGURE 29 TRENDS IN POLYLACTIC ACID MARKET

- FIGURE 30 THERMOFORMING GRADE TO BE LARGEST SEGMENT OF POLYLACTIC ACID MARKET

- FIGURE 31 SUGARCANE TO BE LEADING RAW MATERIAL SEGMENT OF POLYLACTIC ACID MARKET DURING FORECAST PERIOD

- FIGURE 32 RIGID THERMOFORMS TO BE LARGEST SEGMENT OF POLYLACTIC ACID MARKET

- FIGURE 33 PACKAGING END-USE INDUSTRY TO LEAD OVERALL POLYLACTIC ACID MARKET

- FIGURE 34 ASIA PACIFIC: POLYLACTIC ACID MARKET SNAPSHOT

- FIGURE 35 EUROPE: POLYLACTIC ACID MARKET SNAPSHOT

- FIGURE 36 POLYLACTIC ACID MARKET SHARE ANALYSIS, 2024

- FIGURE 37 POLYLACTIC ACID MARKET: REVENUE ANALYSIS OF KEY COMPANIES IN LAST FOUR YEARS, 2020-2023 (USD BILLION)

- FIGURE 38 POLYLACTIC ACID MARKET: COMPANY VALUATION, 2024 (USD BILLION)

- FIGURE 39 POLYLACTIC ACID MARKET: FINANCIAL MATRIX: EV/EBITDA RATIO, 2024

- FIGURE 40 POLYLACTIC ACID MARKET: YEAR-TO-DATE PRICE AND FIVE-YEAR STOCK BETA, 2024

- FIGURE 41 POLYLACTIC ACID MARKET: PRODUCT/BRAND COMPARISON

- FIGURE 42 POLYLACTIC ACID MARKET: COMPANY EVALUATION MATRIX, KEY PLAYERS, 2024

- FIGURE 43 POLYLACTIC ACID MARKET: COMPANY FOOTPRINT

- FIGURE 44 POLYLACTIC ACID MARKET: COMPANY EVALUATION MATRIX, STARTUPS/SMES, 2024

- FIGURE 45 BASF SE: COMPANY SNAPSHOT

- FIGURE 46 DANIMER SCIENTIFIC: COMPANY SNAPSHOT

- FIGURE 47 TORAY INDUSTRIES, INC.: COMPANY SNAPSHOT

- FIGURE 48 EVONIK INDUSTRIES: COMPANY SNAPSHOT

- FIGURE 49 MITSUBISHI CHEMICAL GROUP CORPORATION: COMPANY SNAPSHOT

- FIGURE 50 UNITIKA LTD.: COMPANY SNAPSHOT

目次

The global PLA market is expected to increase from USD 2.01 billion in 2025 to USD 4.51 billion by 2030, translating into a CAGR of 17.5% over the forecast period. Much of this growth can be attributed to increasing demand for compostable packaging in the food and beverage sector, along with the rise of new large-scale industrial PLA production plants, particularly in the Asia Pacific, Europe, and North America regions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million / Billion) Volume (KT) |

| Segments | Application, Grade, End-use Industry, Raw Material, and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

Additionally, ongoing developments of PLA that are heat-resistant or can be chemically recycled are opening up broader market opportunities for applications in automotive, electronics, and durable goods. The market outlook remains positive, supported by investments in bio-refineries, diversification of feedstocks, and commitments by brands to develop sustainable packaging. Emerging applications in the biomedical device market, composites, and low-carbon manufacturing systems will also present long-term growth opportunities perspective.

"Films & Sheets to Be Second Fastest-Growing Segment in the PLA Market"

The films and sheets application area is expected to be the second-fastest growing segment in the PLA market. PLA films are used in various applications, including flexible food packaging, agricultural mulch films, personal care wrappers, and different labeling uses due to their excellent transparency, sealability, and, for some applications, biodegradability. Within this market segment, it has become easier to adopt PLA-based film as a replacement because of the global shift away from traditional multilayer plastic films and the increasing demand for certified compostable packaging products. Projects that have supported global initiatives in compostable packaging show a rising use of PLA-based films in waiting-to-laminate, thermo-sealing, coating applications, and other segments actively pursuing sustainability products.

"Extrusion grade to be second fastest-growing segment in PLA market"

The extrusion grade PLA segment was the second fastest-growing segment in the PLA market in 2024, due to the increased demand for bio-based sheets, films, and profiles in packaging, construction, and consumer applications. PLA is considered a viable alternative to conventional polymers, in both rigid and flexible approaches, given that PLA can utilize standard extrusion equipment, improvements in thermal resistance, and mechanical stability. The extrusion segment is further advancing due to its increased use as a viable alternative for clamshell containers, blister packs, laminated materials, and other packaging products, especially where formability, clarity, and compostability are necessary. As the food packaging and industrial sheets market shifted toward more sustainable materials, the extrusion grade PLA segment offers inexpensive alternatives, while also offering large-scale, efficient processing, and reducing the overall impact on the environment. Other innovations, such as co-extrusion and multilayer PLA structures, will help increase the segment's footprint internationally.

"The corn starch segment was the second fastest-growing segment of PLA market in 2024."

The corn starch segment was the second-fastest growing source of PLA raw material in 2024, following sugarcane. Corn starch remains the most prominent and readily available feedstock for the fermentation of lactic acid, especially in North America, Europe, and China. It benefits from a strong supply chain, competitive prices, and high fermentable sugar content, making it attractive for large-scale PLA production. Growth in corn-based PLA is supported by increasing consumer and regulatory demand for biodegradable packaging and agricultural films, particularly in developed markets with well-established corn processing infrastructure. Additionally, ongoing research into fermenting non-GMO field corn and developing more carbon-efficient production methods will likely enhance perceptions of sustainability and improve marketing prospects for corn starch.

"Middle East & Africa to be second fastest-growing regional market for PLA"

The Middle East & Africa is anticipated to be the second fastest-growing regional PLA market in 2024. Growth is being driven by increasing awareness of plastic pollution, adoption of bio-based packaging alternatives, and the region's push toward sustainable development goals (SDGs). Governments in the Middle East & Africa are introducing legislation to reduce single-use plastics, and multinational FMCG companies operating in the region are shifting to PLA-based materials for their sustainability pledges. Additionally, the expansion of food packaging, consumer goods, and agriculture sectors across Gulf nations, South Africa, and North African countries provides a promising foundation for PLA adoption. The region also offers cost-competitive access to biomass resources and is attracting foreign direct investment in green technology and bio-based industries, further fueling its PLA market growth.

By Company Type: Tier 1: 23%, Tier 2: 42%, and Tier 3: 35%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: NatureWorks LLC (US), TotalEnergies Corbion (Netherlands), BASF SE (Germany), COFCO (China), Futerro (Belgium), Danimer Scientific (US), TORAY INDUSTRIES, INC. (Japan), Evonik Industries (Germany), Mitsubishi Chemical Group Corporation (Japan), and UNITIKA LTD. (Japan) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the PLA market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the PLA market based on grade (thermoforming grade, injection molding grade, extrusion grade, blow molding grade), application (rigid thermoforms, films & sheets, bottles), end-use industry (packaging, consumer goods, agricultural, textile, bio-medical), raw material (sugarcane, corn starch, cassava, sugarbeet), and region (Asia Pacific, North America, Europe, South America, Middle East & Africa). The report's scope includes detailed information on the drivers, restraints, challenges, and opportunities impacting the growth of the PLA market. A comprehensive analysis of key industry players provides insights into their business overview, products offered, and key strategies such as partnerships, agreements, product launches, expansions, and acquisitions related to the PLA market. Additionally, this report features a competitive analysis of emerging startups in the PLA industry ecosystem.

Reasons to Buy the Report

The report will provide market leaders and new entrants with estimates of revenue figures for the overall PLA market and its subsegments. This report will help stakeholders understand the competitive landscape, gain better insights into positioning their businesses, and develop appropriate go-to-market strategies. It will also help stakeholders understand the market's pulse and offer information on key drivers, restraints, and challenges opportunities.

The report provides insights into the following points:

- Assessment of primary drivers (changing consumer preference toward eco-friendly plastic products, Increasing use in packaging and compostable bag applications, government focus on green procurement policies and regulations, technological advancements in fermentation and polymerization techniques for PLA production) restraints (higher prices of PLA than conventional plastics and limited performance in high-temperature and high-impact applications), opportunities (development of new end-use applications, High growth potential in emerging economies of Asia Pacific, versatility of PLA in multiple sectors such as 3D printing, agriculture, and textiles), and challenges (lower thermal stability and mechanical performance compared to traditional plastics, competition from other biodegradable or recycled plastics and High production costs and complexity in scaling up).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the PLA market.

- Market Development: Comprehensive information about profitable markets-the report analyzes the PLA market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the PLA market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as NatureWorks LLC (US), TotalEnergies Corbion (Netherlands) , BASF SE (Germany), COFCO (China), Futerro (Belgium), Danimer Scientific (US), TORAY INDUSTRIES, INC. (Japan), Evonik Industries (Germany), Mitsubishi Chemical Group Corporation (Japan), and UNITIKA LTD. (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of interviews with experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 GROWTH RATE ASSUMPTIONS/FORECAST

- 2.5.1 SUPPLY SIDE

- 2.5.2 DEMAND SIDE

- 2.6 RISK ASSESSMENT

- 2.7 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POLYLACTIC ACID MARKET

- 4.2 POLYLACTIC ACID MARKET, BY GRADE

- 4.3 POLYLACTIC ACID MARKET, BY RAW MATERIAL

- 4.4 POLYLACTIC ACID MARKET, BY APPLICATION

- 4.5 POLYLACTIC ACID MARKET, BY END-USE INDUSTRY

- 4.6 POLYLACTIC ACID MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Changing consumer preference toward eco-friendly plastic products

- 5.2.1.2 Increasing use in packaging and compostable bag applications

- 5.2.1.3 Government focus on green procurement policies and regulations

- 5.2.1.4 Technological advancements in fermentation and polymerization processes of PLA

- 5.2.2 RESTRAINTS

- 5.2.2.1 Higher prices of PLA compared to conventional plastics

- 5.2.2.2 Limited performance in high-temperature and high-impact applications

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Development of new end-use applications

- 5.2.3.2 High growth potential in emerging countries of Asia Pacific

- 5.2.3.3 Versatility of PLA in 3D printing, agriculture, and textile sectors

- 5.2.4 CHALLENGES

- 5.2.4.1 Lower thermal stability and mechanical performance compared to traditional plastics

- 5.2.4.2 Competition from other biodegradable or recycled plastics

- 5.2.4.3 Expensive and complex production process

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 BARGAINING POWER OF SUPPLIERS

- 5.3.2 BARGAINING POWER OF BUYERS

- 5.3.3 THREAT OF SUBSTITUTES

- 5.3.4 THREAT OF NEW ENTRANTS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 VALUE CHAIN ANALYSIS

- 5.4.1 RAW MATERIAL SUPPLIERS

- 5.4.2 MANUFACTURERS

- 5.4.3 DISTRIBUTORS

- 5.4.4 END-CONSUMERS

- 5.4.5 SUPPLIERS OF POLYLACTIC ACID MANUFACTURING EQUIPMENT

- 5.5 PATENT ANALYSIS

- 5.5.1 METHODOLOGY

- 5.5.2 PATENTS GRANTED WORLDWIDE, 2015-2024

- 5.5.3 PATENT PUBLICATION TRENDS

- 5.5.4 INSIGHTS

- 5.5.5 LEGAL STATUS OF PATENTS

- 5.5.6 JURISDICTION-WISE PATENT ANALYSIS

- 5.5.7 TOP COMPANIES/APPLICANTS

- 5.5.8 TOP 10 PATENT OWNERS (US) DURING LAST 10 YEARS

- 5.6 PRICE ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF POLYLACTIC ACID, BY REGION, 2022-2030

- 5.6.2 AVERAGE SELLING PRICE OF POLYLACTIC ACID, BY GRADE, 2022-2030

- 5.6.3 AVERAGE SELLING PRICE OF POLYLACTIC ACID, BY END-USE INDUSTRY, 2024

- 5.6.4 AVERAGE SELLING PRICE, BY TOP THREE MARKET PLAYERS, 2024

- 5.7 MANUFACTURING PROCESS OF POLYLACTIC ACID

- 5.7.1 RAW MATERIAL PREPARATION

- 5.7.2 LACTIDE PRODUCTION

- 5.7.3 LACTIDE PURIFICATION

- 5.7.4 LACTIDE DEPOLYMERIZATION

- 5.7.5 POLYMERIZATION CONTROL

- 5.7.6 POLYMER PURIFICATION AND PROCESSING

- 5.7.7 POST-PROCESSING AND FINISHING

- 5.7.8 PRODUCT MANUFACTURING

- 5.8 RAW MATERIAL ANALYSIS

- 5.8.1 STARCH

- 5.8.2 TAPIOCA ROOT

- 5.8.3 WOOD CHIPS

- 5.8.4 SUGARCANE

- 5.9 ECOSYSTEM/MARKET MAPPING

- 5.10 CASE STUDIES

- 5.10.1 TOTALENERGIES CORBION IMPROVES ENVIRONMENTAL FOOTPRINT WITH LUMINY RECYCLED PLAOVERVIEW

- 5.10.2 NATUREWOKS LLC HELPS SHANGHAI TUOZHUO IN IMPROVING PERFORMANCE AND REDUCING COST AND MAINTENANCE OF WOOD MOLDS FOR METAL CASTING

- 5.10.3 NATUREWORKS LLC PROVIDES INGEO POLYLACTIC ACID FILAMENT TO EARL E. BAKKEN MEDICAL DEVICE CENTER TO STREAMLINE ITS 3D PROTOTYPING

- 5.11 REGULATORY LANDSCAPE

- 5.11.1 NORTH AMERICA

- 5.11.1.1 US

- 5.11.1.2 Canada

- 5.11.2 ASIA PACIFIC

- 5.11.3 EUROPE

- 5.11.1 NORTH AMERICA

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT-EXPORT SCENARIO OF POLYLACTIC ACID MARKET (HS CODE 390770)

- 5.13 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.14 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.15 KEY FACTORS AFFECTING BUYING DECISIONS

- 5.15.1 PRICE

- 5.15.2 SUSTAINABILITY

- 5.15.3 PERFORMANCE

- 5.15.4 AVAILABILITY

- 5.15.5 REGULATIONS

- 5.15.6 BRAND REPUTATION

- 5.15.7 MARKET TRENDS

- 5.15.8 APPLICATION

- 5.16 TECHNOLOGY ANALYSIS

- 5.16.1 NANOCELLULOSE-PLA NANOCOMPOSITES

- 5.16.2 DEVELOPMENT OF STEREO-COMPLEX PLA FOR HEAT-RESISTANT APPLICATIONS

- 5.16.3 GRAPHENE-REINFORCED PLA FOR HIGH-STRENGTH AND CONDUCTIVE APPLICATIONS

6 POLYLACTIC ACID MARKET, BY GRADE

- 6.1 INTRODUCTION

- 6.2 THERMOFORMING

- 6.2.1 PROCESSING CHARACTERISTICS COMPARABLE TO CONVENTIONAL PLASTICS TO BOOST MARKET

- 6.3 INJECTION MOLDING

- 6.3.1 EXCELLENT MELT FLOW AND SUITABILITY FOR COMPLEX AND DETAILED MOLD DESIGNS TO PROPEL MARKET

- 6.4 EXTRUSION

- 6.4.1 GOOD PROCESSIBILITY, MECHANICAL STRENGTH, THERMAL STABILITY, AND LOW ENVIRONMENTAL IMPACT TO DRIVE MARKET

- 6.5 BLOW MOLDING

- 6.5.1 DEMAND FOR HIGH PRODUCTION VOLUMES AND LOW UNIT COST TO BOOST GROWTH

- 6.6 OTHER GRADES

7 POLYLACTIC ACID MARKET, BY RAW MATERIAL

- 7.1 INTRODUCTION

- 7.2 SUGARCANE

- 7.2.1 HIGH SUCROSE CONTENT, AVAILABILITY, AND SUSTAINABILITY TO BOOST MARKET

- 7.3 CORN STARCH

- 7.3.1 WIDE AVAILABILITY AS MOST CULTIVATED CROP GLOBALLY TO FUEL GROWTH

- 7.4 CASSAVA

- 7.4.1 RESILIENCE AND LESS REQUIREMENT OF WATER AND AGRICULTURAL INPUTS TO PROPEL GROWTH

- 7.5 SUGAR BEET

- 7.5.1 CARBON SEQUESTRATION, REDUCED WATER USAGE, , AND POTENTIAL FOR CROP ROTATION, ENHANCING SOIL FERTILITY TO DRIVE MARKET

- 7.6 OTHER RAW MATERIALS

8 POLYLACTIC ACID MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 RIGID THERMOFORMS

- 8.2.1 HIGH-VOLUME PRODUCTION OF PLASTIC PARTS TO DRIVE GROWTH

- 8.3 FILMS & SHEETS

- 8.3.1 DEMAND FOR PRODUCTION OF SPECIAL LINERS, WASTE MANAGEMENT SHEETS, AGRICULTURAL APPLICATIONS, AND RETAIL AND CONVENIENCE BAGS TO BOOST GROWTH

- 8.4 BOTTLES

- 8.4.1 FEWER FOSSIL FUEL RESOURCES AND PLANT-BASED CHEMICAL SYNTHESIS PROCESS TO DRIVE MARKET

- 8.5 OTHER APPLICATIONS

9 POLYLACTIC ACID MARKET, BY END-USE INDUSTRY

- 9.1 INTRODUCTION

- 9.2 PACKAGING

- 9.2.1 HIGH DURABILITY AND IMPERMEABILITY OF WATER TO BOOST GROWTH

- 9.2.2 FOOD PACKAGING

- 9.2.3 NON-FOOD PACKAGING

- 9.3 CONSUMER GOODS

- 9.3.1 VERSATILITY AND COST-EFFECTIVENESS TO SUPPORT MARKET GROWTH

- 9.3.2 ELECTRICAL APPLIANCES

- 9.3.3 DOMESTIC APPLIANCES

- 9.4 AGRICULTURAL

- 9.4.1 REGENERATIVE AGRICULTURAL PRACTICES AND REDUCED SOIL POLLUTION TO PROPEL MARKET

- 9.4.2 PLANTER BOXES

- 9.4.3 TAPES & MULCH FILMS

- 9.4.4 NETTING

- 9.5 TEXTILE

- 9.5.1 GROWING DEMAND FOR APPAREL, HOME TEXTILES, AND NONWOVEN FABRICS TO BOOST MARKET

- 9.5.2 DIAPERS AND WIPES

- 9.5.3 FEMALE HYGIENE

- 9.5.4 PERSONAL CARE, CLOTHES, DISPOSABLE GARMENTS, MEDICAL & HEALTHCARE, AND OTHER TEXTILES

- 9.6 BIO-MEDICAL

- 9.6.1 BIODEGRADABILITY, BIOCOMPATIBILITY, AND SAFE ABSORPTION BY HUMAN BODY TO DRIVE GROWTH

- 9.6.2 MEDICAL PLATES AND SCREWS

- 9.6.3 IMPLANTS

- 9.7 OTHER END-USE INDUSTRIES

10 POLYLACTIC ACID MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 ASIA PACIFIC

- 10.2.1 CHINA

- 10.2.1.1 Rising industrial investments and strong government mandates to boost market

- 10.2.2 INDIA

- 10.2.2.1 Stricter plastic waste laws, domestic push for bioplastics, and NGO engagement to boost market

- 10.2.3 JAPAN

- 10.2.3.1 Research on development of better polylactic acid grades to drive market

- 10.2.4 SOUTH KOREA

- 10.2.4.1 Government policies to support market growth

- 10.2.5 REST OF ASIA PACIFIC

- 10.2.1 CHINA

- 10.3 EUROPE

- 10.3.1 GERMANY

- 10.3.1.1 Ban on conventional plastics to drive market

- 10.3.2 UK

- 10.3.2.1 Stringent regulations on single-use plastics and rising domestic production capacity to drive market growth

- 10.3.3 FRANCE

- 10.3.3.1 Government initiatives to promote use of bioplastics to drive demand

- 10.3.4 ITALY

- 10.3.4.1 Demand from food packaging industry to drive demand

- 10.3.5 SPAIN

- 10.3.5.1 Rising public awareness and regulatory measures to boost market

- 10.3.6 REST OF EUROPE

- 10.3.1 GERMANY

- 10.4 NORTH AMERICA

- 10.4.1 US

- 10.4.1.1 Shift toward sustainable packaging to drive market growth

- 10.4.2 CANADA

- 10.4.2.1 Stringent environmental regulations and circular economy initiatives to propel growth

- 10.4.3 MEXICO

- 10.4.3.1 Strategic manufacturing and export hub to support market growth

- 10.4.1 US

- 10.5 SOUTH AMERICA

- 10.5.1 BRAZIL

- 10.5.1.1 Abundance of raw materials to fuel market

- 10.5.2 REST OF SOUTH AMERICA

- 10.5.1 BRAZIL

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 SAUDI ARABIA

- 10.6.1.1 Stringent anti-plastic regulations and circular economy efforts to fuel market

- 10.6.2 UAE

- 10.6.2.1 Focus on medical innovation, circular economy, and healthcare expansion to boost market

- 10.6.3 REST OF MIDDLE EAST & AFRICA

- 10.6.1 SAUDI ARABIA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES

- 11.3 MARKET SHARE ANALYSIS

- 11.4 REVENUE ANALYSIS

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.6 PRODUCT/BRAND COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 End-use industry footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 NATUREWORKS LLC

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.3.3 Expansions

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 TOTALENERGIES CORBION

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Deals

- 12.1.2.3.3 Expansions

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 BASF SE

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Deals

- 12.1.3.3.2 Expansions

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 COFCO

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 MnM view

- 12.1.4.3.1 Right to win

- 12.1.4.3.2 Strategic choices

- 12.1.4.3.3 Weaknesses and competitive threats

- 12.1.5 FUTERRO

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Expansions

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 DANIMER SCIENTIFIC

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Deals

- 12.1.6.3.2 Expansions

- 12.1.6.4 MnM view

- 12.1.7 TORAY INDUSTRIES, INC.

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches

- 12.1.7.4 MnM view

- 12.1.8 EVONIK INDUSTRIES

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches

- 12.1.8.3.2 Deals

- 12.1.8.4 MnM view

- 12.1.9 MITSUBISHI CHEMICAL GROUP CORPORATION

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 MnM view

- 12.1.10 UNITIKA LTD.

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 MnM view

- 12.1.1 NATUREWORKS LLC

- 12.2 OTHER PLAYERS

- 12.2.1 BIOWORKS CORPORATION

- 12.2.2 ADBIOPLASTICS

- 12.2.3 MUSASHINO CHEMICAL LABORATORY, LTD.

- 12.2.4 HANGZHOU PEIJIN CHEMICAL CO.,LTD.

- 12.2.5 AKRO-PLASTIC GMBH

- 12.2.6 FUJIAN GREENJOY BIOMATERIAL CO., LTD.

- 12.2.7 PLAMFG

- 12.2.8 FKUR

- 12.2.9 OTTO CHEMIE PVT. LTD.

- 12.2.10 RAGHAV POLYMERS

- 12.2.11 VAISHNAVI BIO TECH

- 12.2.12 HENAN SINOWIN CHEMICAL INDUSTRY CO., LTD.

- 12.2.13 EMNANDI BIOPLASTICS

- 12.2.14 UNILONG INDUSTRY CO., LTD.

- 12.2.15 PRAJ INDUSTRIES

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 268 Pages

- 納期

- 即納可能