交通安全の世界市場:オファリング別、展開モデル別、実施タイプ別、データタイプ別、用途別、エンドユーザー別、地域別 - 2030年までの予測

Road Safety Market by Offering (Traffic Control, ANPR, ALPR, Incident Response, Enforcement, Smart Signals, RSUS, Sensors, Cameras, AI, ML, Analytics), Application (Accident Prevention, Work Zone Safety, Violation Management) - Global Forecast to 2030- 発行日

- ページ情報

- 英文 380 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1797405

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

交通安全の市場規模は急速に拡大しており、2025年の66億9,000万米ドルから2030年には123億9,000万米ドルに拡大すると予測され、予測期間中のCAGRは13.1%になるとみられています。

事故コストを削減し、資産を保護して規制に準拠するため、フリート事業者は現在、交通安全に注力しています。その結果、ドライバーの行動監視、AIダッシュカム、テレマティクス、さらには疲労検知ソリューションなどの技術の採用率が急速に高まっています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 検討単位 | 米ドル(100万米ドル) |

| セグメント | オファリング別、展開モデル別、実施タイプ別、データタイプ別、用途別、エンドユーザー別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、中東・アフリカ、ラテンアメリカ |

高度な安全技術へのアクセスとともに、業務用車両は現在、ドライバーの説明責任の向上、保険料の割引、全体的な効率レベルの向上といった恩恵を受けています。その結果、フリート向けに調整された交通安全ソリューションに対する需要が高まり、交通安全市場全体の成長と革新を促進しています。

交通安全技術には大きな改善の可能性があるが、監視方法の機密性やデータ管理に関するリスクに対する懸念が高まっており、市場拡大の大きな抑制要因となっています。AIを搭載したカメラ、自動ナンバープレート認識、ドライバー監視システムの普及により、公共の監視やデータプライバシーに関する懸念の検討が進んでいます。

政府機関や自治体は交通安全ソリューションを広く採用しています。彼らは意識向上プログラムから包括的な安全インフラや取締りシステムの管理・展開まで、すべてを監督する上で大きな役割を果たしています。彼らは交通安全市場において極めて重要であり、規制と安全政策の実施者として機能しています。資金を提供し、プログラムを開発することで、彼らは公共の安全に大きな影響を与えることができます。政府機関や自治体は法律の遵守を取り締まり、インフラ整備の予算を配分する責任を負っています。

道路上の信号や標識の管理、赤信号やスピード違反取り締まりのためのカメラの配備、AIを使った違反撲滅、リアルタイムの交通管理システムの導入などを行っています。2024年11月、カナダのブランプトン市はJenoptikと協力し、スクールゾーンの遵守率を向上させるため、180台以上の自動速度取締カメラを導入しました。

事故検知・対応部門は交通安全市場の重要な部分であり、負傷者、死亡者、交通障害を最小限に抑えるため、交通事故を迅速に検知し、緊急サービスに迅速に通知することに重点を置いています。事故検知・対応分野は、道路の安全性を高め、事故や危険な状況での対応時間を短縮する方法で、スマート監視、通信インフラ、自動応答を統合しています。

このセグメントは、緊急サービスが文書を分析し、早期介入によってリスクを軽減できるようにすることで、交通事故死者数を減らすことを目的としています。交通事故死者数を減らすことで、事故検知・対応セグメントは事故による遅延や渋滞も減らし、最終的には交通効率全体を向上させる。さらに、この分野はビジョン・ゼロ、インテリジェント交通システム(ITS)、自律走行車の準備という目標に大きく貢献し、世界の交通安全エコシステムの中で高成長分野となっています。

北米は現在、交通安全市場で最大の市場シェアを占めていますが、これはデジタル技術の普及、スマートインフラ技術、大手交通安全ベンダーの存在などが背景にあります。北米政府はビジョン・ゼロ、米国交通安全戦略(NRSS)、カナダの交通安全戦略2025など、より安全な道路利用者、より安全な車両、よりスマートなインフラに優先順位を置くさまざまなプログラムを導入しています。米国運輸省もまた、AIベースの取締りプログラムの実施、自動速度カメラの配備、スマート信号機と歩行者保護装置の設置に50億米ドルを投じる「Safe Streets and Roads for All(SS4A)」プログラムによって、交通安全の革新を奨励しています。

アジア太平洋は世界の交通安全情勢の中で最も急成長している地域として浮上しています。都市化が進み、自動車保有率が上昇し、交通事故死を抑制したいという政府の意向が高まっているからです。これに伴い、インド、中国、日本、韓国、オーストラリアは、インテリジェント交通システム(ITS)、進化するスマートシティプログラム、交通取締り技術への大規模投資で先頭を走っています。

当レポートでは、世界の交通安全市場について調査し、オファリング別、展開モデル別、実施タイプ別、データタイプ別、用途別、エンドユーザー別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要と業界動向

- イントロダクション

- 市場力学

- 2025年の米国関税が交通安全市場に与える影響

- 交通安全ソリューションの進化

- サプライチェーン分析

- 生成AIが交通安全市場に与える影響

- エコシステム分析

- 投資情勢と資金調達シナリオ

- ケーススタディ分析

- 技術分析

- 関税と規制状況

- 貿易分析

- 特許分析

- 価格分析

- 主要な会議とイベント(2025年~2026年)

- ポーターのファイブフォース分析

- 購入者に影響を与える動向と混乱

- 主要な利害関係者と購入基準

- 技術ロードマップ

- パートナーシップとエコシステム戦略

- 利害関係者にとっての戦略的必須事項

第6章 交通安全市場(オファリング別)

- イントロダクション

- ソリューション

- サービス

第7章 交通安全市場(展開モデル別)

- イントロダクション

- 固定設備

- 移動式/トレーラー搭載型システム

- ポータブル/一時的なソリューション

- クラウドベースのプラットフォーム

第8章 交通安全市場(実施タイプ別)

- イントロダクション

- 自動

- 手動

- ハイブリッド

第9章 交通安全市場(データタイプ別)

- イントロダクション

- ビデオと画像

- センサーデータ

- 統合ビッグデータ

第10章 交通安全市場(用途別)

- イントロダクション

- 違反管理

- トラフィック最適化

- 事故防止

- 緊急対応

- 運転者行動モニタリング

- 啓発・トレーニング

- 歩行者・VRUの保護

- 作業区域の安全管理

- 保険リスク評価

第11章 交通安全市場(エンドユーザー別)

- イントロダクション

- 政府と地方自治体

- 高速道路当局

- 法執行機関

- 民間の通行料金徴収業者

- スマートシティインテグレーター

- 建設会社

- その他

第12章 交通安全市場(地域別)

- イントロダクション

- 北米

- 北米:交通安全市場促進要因

- 北米:マクロ経済見通し

- 米国

- カナダ

- 欧州

- 欧州:交通安全市場促進要因

- 欧州:マクロ経済見通し

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他

- アジア太平洋

- アジア太平洋:交通安全市場の牽引役

- アジア太平洋:マクロ経済見通し

- 中国

- 日本

- インド

- オーストラリアとニュージーランド

- ASEAN

- 韓国

- その他

- 中東・アフリカ

- 中東・アフリカ:交通安全市場促進要因

- 中東・アフリカ:マクロ経済見通し

- サウジアラビア

- アラブ首長国連邦(UAE)

- 南アフリカ

- カタール

- その他

- ラテンアメリカ

- ラテンアメリカ:交通安全市場促進要因

- ラテンアメリカ:マクロ経済見通し

- ブラジル

- メキシコ

- アルゼンチン

- その他

第13章 競合情勢

- 概要

- 主要参入企業の戦略/強み、2022年~2025年

- 収益分析、2020年~2024年

- 市場シェア分析、2024年

- 製品比較分析

- 企業評価と財務指標

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業(ハードウェア)、2024年

- 企業評価マトリックス:スタートアップ/中小企業(ソフトウェア)、2024年

- 競合シナリオと動向

第14章 企業プロファイル

- 主要参入企業

- JENOPTIK

- KAPSCH TRAFFICCOM

- SENSYS GATSO GROUP

- VERRA MOBILITY

- TELEDYNE FLIR

- MOTOROLA SOLUTIONS

- IDEMIA

- SWARCO

- VITRONIC

- SIEMENS

- CONDUENT

- CUBIC CORPORATION

- DAHUA TECHNOLOGY

- LASER TECHNOLOGIES

- その他の企業

- TRAFFIC MANAGEMENT TECHNOLOGIES

- TRIFOIL

- KRIA

- SYNTELL

- TRUVELO

- CLEARVIEW INTELLIGENCE

- SIMICON

- FRED ENGINEERING

- KODIAK ROBOTICS

- HUMANISING AUTONOMY

- VEBITS AI

- CONNECTED WISE LLC

- SAFEROAD

- LIVEROAD ANALYTICS

- VIVACITY

- NOTRAFFIC

- VALERANN

- ACUSENSUS

第15章 隣接市場と関連市場

第16章 付録

図表

List of Tables

- TABLE 1 UNITED STATES DOLLAR EXCHANGE RATE, 2020-2024

- TABLE 2 FACTOR ANALYSIS

- TABLE 3 GLOBAL ROAD SAFETY MARKET SIZE AND GROWTH RATE, 2020-2024 (USD MILLION, Y-O-Y %)

- TABLE 4 GLOBAL ROAD SAFETY MARKET SIZE AND GROWTH RATE, 2025-2030 (USD MILLION, Y-O-Y %)

- TABLE 5 US: ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 6 EXPECTED CHANGE IN PRICES AND LIKELY IMPACT ON END-USE MARKET DUE TO TARIFF IMPACT

- TABLE 7 ROAD SAFETY MARKET: ECOSYSTEM

- TABLE 8 TARIFF RELATED TO ELECTRICAL SIGNALING, SAFETY, AND TRAFFIC CONTROL EQUIPMENT

- TABLE 9 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 EXPORT DATA FOR HS CODE 853080 - ELECTRICAL SIGNALING AND TRAFFIC CONTROL EQUIPMENT, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 14 IMPORT DATA FOR HS CODE 853080 - ELECTRICAL SIGNALING AND TRAFFIC CONTROL EQUIPMENT, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 15 PATENTS FILED, 2016-2025

- TABLE 16 LIST OF TOP PATENTS IN ROAD SAFETY MARKET, 2024-2025

- TABLE 17 PRICING DATA OF ROAD SAFETY MARKET, BY OFFERING

- TABLE 18 PRICING DATA OF ROAD SAFETY MARKET, BY APPLICATION

- TABLE 19 ROAD SAFETY MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

- TABLE 20 ROAD SAFETY MARKET: PORTER'S FIVE FORCES MODEL

- TABLE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- TABLE 22 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- TABLE 23 PARTNERSHIP TYPE AND STRATEGIC VALUE

- TABLE 24 STRATEGIC IMPERATIVES FOR STAKEHOLDERS

- TABLE 25 ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 26 ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 27 ROAD SAFETY MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 28 ROAD SAFETY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 29 ROAD SAFETY MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 30 ROAD SAFETY MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 31 ENFORCEMENT SOLUTIONS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 32 ENFORCEMENT SOLUTIONS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33 ALPR/ANPR: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 34 ALPR/ANPR: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 35 INCIDENT DETECTION AND RESPONSE: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 36 INCIDENT DETECTION AND RESPONSE: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37 TRAFFIC MONITORING & CONTROL: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 38 TRAFFIC MONITORING & CONTROL: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 39 PEDESTRIAN SAFETY: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 40 PEDESTRIAN SAFETY: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 41 ROAD SAFETY MARKET, BY COMPONENT, 2020-2024 (USD MILLION)

- TABLE 42 ROAD SAFETY MARKET, BY COMPONENT, 2025-2030 (USD MILLION)

- TABLE 43 HARDWARE: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 44 HARDWARE: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 45 SOFTWARE: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 46 SOFTWARE: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 47 ROAD SAFETY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 48 ROAD SAFETY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 49 PROFESSIONAL SERVICES: ROAD SAFETY MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 50 PROFESSIONAL SERVICES: ROAD SAFETY MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 51 CONSULTING: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 52 CONSULTING: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 53 SYSTEM INTEGRATION: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 54 SYSTEM INTEGRATION: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 55 TRAINING: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 56 TRAINING: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 57 ROAD SAFETY AUDITS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 58 ROAD SAFETY AUDITS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 59 MANAGED SERVICES: ROAD SAFETY MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 60 MANAGED SERVICES: ROAD SAFETY MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 61 OUTSOURCED OPERATIONS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 62 OUTSOURCED OPERATIONS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 63 SYSTEM MAINTENANCE: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 64 SYSTEM MAINTENANCE: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 65 ANALYTICS-AS-A-SERVICE: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 66 ANALYTICS-AS-A-SERVICE: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 67 BACK-OFFICE PROCESSING: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 68 BACK-OFFICE PROCESSING: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 69 ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2020-2024 (USD MILLION)

- TABLE 70 ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 71 FIXED INSTALLATIONS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 72 FIXED INSTALLATIONS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 73 MOBILE/TRAILER-MOUNTED SYSTEMS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 74 MOBILE/TRAILER-MOUNTED SYSTEMS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 75 PORTABLE/TEMPORARY SOLUTIONS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 76 PORTABLE/TEMPORARY SOLUTIONS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 77 CLOUD-BASED PLATFORMS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 78 CLOUD-BASED PLATFORMS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 79 ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 80 ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 81 AUTOMATED ENFORCEMENT: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 82 AUTOMATED ENFORCEMENT: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 83 MANUAL ENFORCEMENT: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 84 MANUAL ENFORCEMENT: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 85 HYBRID ENFORCEMENT: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 86 HYBRID ENFORCEMENT: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 87 ROAD SAFETY MARKET, BY DATA TYPE, 2020-2024 (USD MILLION)

- TABLE 88 ROAD SAFETY MARKET, BY DATA TYPE, 2025-2030 (USD MILLION)

- TABLE 89 VIDEO & IMAGE: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 90 VIDEO & IMAGE: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 91 SENSOR DATA: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 92 SENSOR DATA: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 93 INTEGRATED BIG DATA: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 94 INTEGRATED BIG DATA: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 95 ROAD SAFETY MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 96 ROAD SAFETY MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 97 VIOLATION MANAGEMENT: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 98 VIOLATION MANAGEMENT: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 99 TRAFFIC OPTIMIZATION: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 100 TRAFFIC OPTIMIZATION: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 101 ACCIDENT PREVENTION: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 102 ACCIDENT PREVENTION: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 103 EMERGENCY RESPONSE: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 104 EMERGENCY RESPONSE: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 105 DRIVER BEHAVIOR MONITORING: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 106 DRIVER BEHAVIOR MONITORING: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 107 PUBLIC AWARENESS/TRAINING: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 108 PUBLIC AWARENESS/TRAINING: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 109 PEDESTRIAN & VRU PROTECTION: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 110 PEDESTRIAN & VRU PROTECTION: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 111 WORK ZONE SAFETY MANAGEMENT: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 112 WORK ZONE SAFETY MANAGEMENT: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 113 INSURANCE RISK ASSESSMENT: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 114 INSURANCE RISK ASSESSMENT: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 115 ROAD SAFETY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 116 ROAD SAFETY MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 117 GOVERNMENT & MUNICIPALITIES: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 118 GOVERNMENT & MUNICIPALITIES: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 119 HIGHWAY AUTHORITIES: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 120 HIGHWAY AUTHORITIES: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 121 LAW ENFORCEMENT AGENCIES: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 122 LAW ENFORCEMENT AGENCIES: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 123 PRIVATE TOLL OPERATORS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 124 PRIVATE TOLL OPERATORS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 125 SMART CITY INTEGRATORS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 126 SMART CITY INTEGRATORS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 127 CONSTRUCTION COMPANIES: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 128 CONSTRUCTION COMPANIES: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 129 OTHER END USERS: ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 130 OTHER END USERS: ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 131 ROAD SAFETY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 132 ROAD SAFETY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 133 NORTH AMERICA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 134 NORTH AMERICA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 135 NORTH AMERICA: ROAD SAFETY MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 136 NORTH AMERICA: ROAD SAFETY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 137 NORTH AMERICA: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 138 NORTH AMERICA: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 139 NORTH AMERICA: ROAD SAFETY MARKET, BY COMPONENT, 2020-2024 (USD MILLION)

- TABLE 140 NORTH AMERICA: ROAD SAFETY MARKET, BY COMPONENT, 2025-2030 (USD MILLION)

- TABLE 141 NORTH AMERICA: ROAD SAFETY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 142 NORTH AMERICA: ROAD SAFETY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 143 NORTH AMERICA: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 144 NORTH AMERICA: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 145 NORTH AMERICA: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2020-2024 (USD MILLION)

- TABLE 146 NORTH AMERICA: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2025-2030 (USD MILLION)

- TABLE 147 NORTH AMERICA: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2020-2024 (USD MILLION)

- TABLE 148 NORTH AMERICA: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 149 NORTH AMERICA: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 150 NORTH AMERICA: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 151 NORTH AMERICA: ROAD SAFETY MARKET, BY DATA TYPE, 2020-2024 (USD MILLION)

- TABLE 152 NORTH AMERICA: ROAD SAFETY MARKET, BY DATA TYPE, 2025-2030 (USD MILLION)

- TABLE 153 NORTH AMERICA: ROAD SAFETY MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 154 NORTH AMERICA: ROAD SAFETY MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 155 NORTH AMERICA: ROAD SAFETY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 156 NORTH AMERICA: ROAD SAFETY MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 157 NORTH AMERICA: ROAD SAFETY MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 158 NORTH AMERICA: ROAD SAFETY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 159 US: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 160 US: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 161 CANADA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 162 CANADA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 163 EUROPE: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 164 EUROPE: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 165 EUROPE: ROAD SAFETY MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 166 EUROPE: ROAD SAFETY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 167 EUROPE: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 168 EUROPE: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 169 EUROPE: ROAD SAFETY MARKET, BY COMPONENT, 2020-2024 (USD MILLION)

- TABLE 170 EUROPE: ROAD SAFETY MARKET, BY COMPONENT, 2025-2030 (USD MILLION)

- TABLE 171 EUROPE: ROAD SAFETY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 172 EUROPE: ROAD SAFETY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 173 EUROPE: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 174 EUROPE: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 175 EUROPE: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2020-2024 (USD MILLION)

- TABLE 176 EUROPE: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2025-2030 (USD MILLION)

- TABLE 177 EUROPE: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2020-2024 (USD MILLION)

- TABLE 178 EUROPE: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 179 EUROPE: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 180 EUROPE: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 181 EUROPE: ROAD SAFETY MARKET, BY DATA TYPE, 2020-2024 (USD MILLION)

- TABLE 182 EUROPE: ROAD SAFETY MARKET, BY DATA TYPE, 2025-2030 (USD MILLION)

- TABLE 183 EUROPE: ROAD SAFETY MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 184 EUROPE: ROAD SAFETY MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 185 EUROPE: ROAD SAFETY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 186 EUROPE: ROAD SAFETY MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 187 EUROPE: ROAD SAFETY MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 188 EUROPE: ROAD SAFETY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 189 UK: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 190 UK: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 191 GERMANY: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 192 GERMANY: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 193 FRANCE: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 194 FRANCE: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 195 ITALY: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 196 ITALY: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 197 SPAIN: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 198 SPAIN: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 199 REST OF EUROPE: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 200 REST OF EUROPE: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 201 ASIA PACIFIC: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 202 ASIA PACIFIC: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 203 ASIA PACIFIC: ROAD SAFETY MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 204 ASIA PACIFIC: ROAD SAFETY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 205 ASIA PACIFIC: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 206 ASIA PACIFIC: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 207 ASIA PACIFIC: ROAD SAFETY MARKET, BY COMPONENT, 2020-2024 (USD MILLION)

- TABLE 208 ASIA PACIFIC: ROAD SAFETY MARKET, BY COMPONENT, 2025-2030 (USD MILLION)

- TABLE 209 ASIA PACIFIC: ROAD SAFETY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 210 ASIA PACIFIC: ROAD SAFETY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 211 ASIA PACIFIC: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 212 ASIA PACIFIC: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 213 ASIA PACIFIC: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2020-2024 (USD MILLION)

- TABLE 214 ASIA PACIFIC: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2025-2030 (USD MILLION)

- TABLE 215 ASIA PACIFIC: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2020-2024 (USD MILLION)

- TABLE 216 ASIA PACIFIC: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 217 ASIA PACIFIC: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 218 ASIA PACIFIC: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 219 ASIA PACIFIC: ROAD SAFETY MARKET, BY DATA TYPE, 2020-2024 (USD MILLION)

- TABLE 220 ASIA PACIFIC: ROAD SAFETY MARKET, BY DATA TYPE, 2025-2030 (USD MILLION)

- TABLE 221 ASIA PACIFIC: ROAD SAFETY MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 222 ASIA PACIFIC: ROAD SAFETY MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 223 ASIA PACIFIC: ROAD SAFETY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 224 ASIA PACIFIC: ROAD SAFETY MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 225 ASIA PACIFIC: ROAD SAFETY MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 226 ASIA PACIFIC: ROAD SAFETY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 227 CHINA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 228 CHINA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 229 JAPAN: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 230 JAPAN: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 231 INDIA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 232 INDIA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 233 AUSTRALIA & NEW ZEALAND: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 234 AUSTRALIA & NEW ZEALAND: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 235 ASEAN: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 236 ASEAN: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 237 SOUTH KOREA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 238 SOUTH KOREA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 239 REST OF ASIA PACIFIC: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 240 REST OF ASIA PACIFIC: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 241 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 242 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 243 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 244 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 245 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 246 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 247 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY COMPONENT, 2020-2024 (USD MILLION)

- TABLE 248 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY COMPONENT, 2025-2030 (USD MILLION)

- TABLE 249 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 250 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 251 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 252 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 253 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2020-2024 (USD MILLION)

- TABLE 254 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2025-2030 (USD MILLION)

- TABLE 255 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2020-2024 (USD MILLION)

- TABLE 256 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 257 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 258 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 259 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY DATA TYPE, 2020-2024 (USD MILLION)

- TABLE 260 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY DATA TYPE, 2025-2030 (USD MILLION)

- TABLE 261 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 262 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 263 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 264 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 265 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 266 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 267 SAUDI ARABIA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 268 SAUDI ARABIA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 269 UAE: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 270 UAE: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 271 SOUTH AFRICA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 272 SOUTH AFRICA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 273 QATAR: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 274 QATAR: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 275 REST OF MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 276 REST OF MIDDLE EAST & AFRICA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 277 LATIN AMERICA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 278 LATIN AMERICA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 279 LATIN AMERICA: ROAD SAFETY MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 280 LATIN AMERICA: ROAD SAFETY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 281 LATIN AMERICA: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 282 LATIN AMERICA: ROAD SAFETY MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 283 LATIN AMERICA: ROAD SAFETY MARKET, BY COMPONENT, 2020-2024 (USD MILLION)

- TABLE 284 LATIN AMERICA: ROAD SAFETY MARKET, BY COMPONENT, 2025-2030 (USD MILLION)

- TABLE 285 LATIN AMERICA: ROAD SAFETY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 286 LATIN AMERICA: ROAD SAFETY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 287 LATIN AMERICA: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 288 LATIN AMERICA: ROAD SAFETY MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 289 LATIN AMERICA: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2020-2024 (USD MILLION)

- TABLE 290 LATIN AMERICA: ROAD SAFETY MARKET, BY MANAGED SERVICE, 2025-2030 (USD MILLION)

- TABLE 291 LATIN AMERICA: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2020-2024 (USD MILLION)

- TABLE 292 LATIN AMERICA: ROAD SAFETY MARKET, BY DEPLOYMENT MODEL, 2025-2030 (USD MILLION)

- TABLE 293 LATIN AMERICA: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 294 LATIN AMERICA: ROAD SAFETY MARKET, BY ENFORCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 295 LATIN AMERICA: ROAD SAFETY MARKET, BY DATA TYPE, 2020-2024 (USD MILLION)

- TABLE 296 LATIN AMERICA: ROAD SAFETY MARKET, BY DATA TYPE, 2025-2030 (USD MILLION)

- TABLE 297 LATIN AMERICA: ROAD SAFETY MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 298 LATIN AMERICA: ROAD SAFETY MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 299 LATIN AMERICA: ROAD SAFETY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 300 LATIN AMERICA: ROAD SAFETY MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 301 LATIN AMERICA: ROAD SAFETY MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 302 LATIN AMERICA: ROAD SAFETY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 303 BRAZIL: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 304 BRAZIL: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 305 MEXICO: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 306 MEXICO: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 307 ARGENTINA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 308 ARGENTINA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 309 REST OF LATIN AMERICA: ROAD SAFETY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 310 REST OF LATIN AMERICA: ROAD SAFETY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 311 OVERVIEW OF STRATEGIES ADOPTED BY KEY ROAD SAFETY VENDORS, 2022-2025

- TABLE 312 ROAD SAFETY MARKET: DEGREE OF COMPETITION

- TABLE 313 REGIONAL FOOTPRINT (13 COMPANIES), 2024

- TABLE 314 OFFERING FOOTPRINT (13 COMPANIES), 2024

- TABLE 315 APPLICATION FOOTPRINT (13 COMPANIES), 2024

- TABLE 316 END USER FOOTPRINT (13 COMPANIES), 2024

- TABLE 317 ROAD SAFETY MARKET: KEY STARTUPS/SMES, 2024

- TABLE 318 ROAD SAFETY MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (HARDWARE)

- TABLE 319 ROAD SAFETY MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (SOFTWARE)

- TABLE 320 ROAD SAFETY MARKET: PRODUCT LAUNCHES AND ENHANCEMENTS, 2022-2025

- TABLE 321 ROAD SAFETY MARKET: DEALS, 2022-2025

- TABLE 322 JENOPTIK: COMPANY OVERVIEW

- TABLE 323 JENOPTIK: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 324 JENOPTIK: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 325 KAPSCH TRAFFICCOM: COMPANY OVERVIEW

- TABLE 326 KAPSCH TRAFFICCOM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 327 KAPSCH TRAFFICCOM: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 328 KAPSCH TRAFFICCOM: DEALS

- TABLE 329 SENSYS GATSO GROUP: COMPANY OVERVIEW

- TABLE 330 SENSYS GATSO GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 331 SENSYS GATSO: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 332 SENSYS GATSO GROUP: DEALS

- TABLE 333 VERRA MOBILITY: COMPANY OVERVIEW

- TABLE 334 VERRA MOBILITY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 335 VERRA MOBILITY: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 336 VERRA MOBILITY: DEALS

- TABLE 337 TELEDYNE FLIR: COMPANY OVERVIEW

- TABLE 338 TELEDYNE FLIR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 339 TELEDYNE FLIR: PRODUCT LAUNCH AND ENHANCEMENTS

- TABLE 340 TELEDYNE FLIR: DEALS

- TABLE 341 MOTOROLA SOLUTIONS: COMPANY OVERVIEW

- TABLE 342 MOTOROLA SOLUTIONS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 343 MOTOROLA SOLUTIONS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 344 MOTOROLA SOLUTIONS: DEALS

- TABLE 345 IDEMIA: COMPANY OVERVIEW

- TABLE 346 IDEMIA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 347 IDEMIA: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 348 IDEMIA: DEALS

- TABLE 349 SWARCO: COMPANY OVERVIEW

- TABLE 350 SWARCO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 351 SWARCO: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 352 SWARCO: DEALS

- TABLE 353 VITRONIC: COMPANY OVERVIEW

- TABLE 354 VITRONIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 355 VITRONIC: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 356 SIEMENS: COMPANY OVERVIEW

- TABLE 357 SIEMENS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 358 SIEMENS: DEALS

- TABLE 359 CONDUENT: COMPANY OVERVIEW

- TABLE 360 CONDUENT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 361 CONDUENT: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 362 CONDUENT: DEALS

- TABLE 363 CUBIC CORPORATION: COMPANY OVERVIEW

- TABLE 364 CUBIC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 365 CUBIC: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 366 CUBIC CORPORATION: DEALS

- TABLE 367 TRAFFIC MANAGEMENT MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 368 TRAFFIC MANAGEMENT MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 369 TRAFFIC MANAGEMENT MARKET, BY AREA OF APPLICATION, 2019-2023 (USD MILLION)

- TABLE 370 TRAFFIC MANAGEMENT MARKET, BY AREA OF APPLICATION, 2024-2029 (USD MILLION)

- TABLE 371 TRAFFIC MANAGEMENT MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 372 TRAFFIC MANAGEMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 373 TRAFFIC MANAGEMENT MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 374 TRAFFIC MANAGEMENT MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 375 SMART TRANSPORTATION MARKET, BY TRANSPORTATION MODE, 2018-2022 (USD MILLION)

- TABLE 376 SMART TRANSPORTATION MARKET, BY TRANSPORTATION MODE, 2023-2028 (USD MILLION)

- TABLE 377 ROADWAY: SMART TRANSPORTATION MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 378 ROADWAY: SMART TRANSPORTATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 379 RAILWAY: SMART TRANSPORTATION MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 380 RAILWAY: SMART TRANSPORTATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 381 AIRWAY: SMART TRANSPORTATION MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 382 AIRWAY: SMART TRANSPORTATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 383 MARITIME: SMART TRANSPORTATION MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 384 MARITIME: SMART TRANSPORTATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 385 SMART TRANSPORTATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 386 SMART TRANSPORTATION MARKET, BY REGION, 2023-2028 (USD MILLION)

List of Figures

- FIGURE 1 ROAD SAFETY MARKET: RESEARCH DESIGN

- FIGURE 2 ROAD SAFETY MARKET: DATA TRIANGULATION

- FIGURE 3 ROAD SAFETY MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 1, BOTTOM-UP (SUPPLY-SIDE): REVENUE FROM SOLUTIONS AND SERVICES IN ROAD SAFETY MARKET

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 2, BOTTOM-UP (SUPPLY-SIDE): COLLECTIVE REVENUE FROM KEY COMPANIES IN ROAD SAFETY MARKET

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 3, BOTTOM-UP (SUPPLY-SIDE): COLLECTIVE REVENUE FROM BUSINESS UNITS (BUS) OF KEY VENDORS IN ROAD SAFETY MARKET

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 4, BOTTOM-UP (DEMAND-SIDE): SHARE OF ROAD SAFETY THROUGH OVERALL IT SPENDING ON ROAD SAFETY SOLUTIONS

- FIGURE 8 AUTOMATED ENFORCEMENT SEGMENT TO HOLD LARGEST MARKET SIZE IN 2025

- FIGURE 9 VIDEO & IMAGE SEGMENT TO HOLD LARGEST MARKET SHARE IN 2025

- FIGURE 10 SOLUTIONS SEGMENT TO HOLD LARGEST MARKET SHARE IN 2025

- FIGURE 11 SMART CITY INTEGRATORS TO WITNESS HIGHEST GROWTH RATE IN END USER SEGMENT DURING FORECAST PERIOD

- FIGURE 12 ASIA PACIFIC TO REGISTER FASTEST GROWTH BETWEEN 2025 AND 2030

- FIGURE 13 ACCELERATING DIGITAL INFRASTRUCTURE AND ROAD SAFETY MANDATE ACROSS ASIA PACIFIC TO DRIVE ROAD SAFETY MARKET GROWTH

- FIGURE 14 DRIVER BEHAVIOR MONITORING SEGMENT TO ACCOUNT FOR HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 15 VIDEO & IMAGE AND AUTOMATED ENFORCEMENT TO BE LARGEST SHAREHOLDERS IN NORTH AMERICAN ROAD SAFETY MARKET IN 2025

- FIGURE 16 NORTH AMERICA TO HOLD LARGEST MARKET SHARE IN 2025

- FIGURE 17 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: ROAD SAFETY MARKET

- FIGURE 18 ROAD SAFETY MARKET EVOLUTION

- FIGURE 19 ROAD SAFETY MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 20 MARKET POTENTIAL OF GENERATIVE AI IN ENHANCING ROAD SAFETY

- FIGURE 21 KEY PLAYERS IN ROAD SAFETY MARKET ECOSYSTEM

- FIGURE 22 ROAD SAFETY MARKET: INVESTMENT LANDSCAPE AND FUNDING SCENARIO

- FIGURE 23 ELECTRICAL SIGNALING AND TRAFFIC CONTROL EQUIPMENT EXPORT, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 24 ELECTRICAL SIGNALING AND TRAFFIC CONTROL EQUIPMENT IMPORT, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 25 NUMBER OF PATENTS GRANTED IN LAST 10 YEARS, 2016-2025

- FIGURE 26 REGIONAL ANALYSIS OF PATENTS GRANTED, 2016-2025

- FIGURE 27 ROAD SAFETY MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 28 TRENDS IMPACTING CUSTOMERS: ROAD SAFETY MARKET

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- FIGURE 30 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- FIGURE 31 SERVICES SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 32 COMPONENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 33 INCIDENT DETECTION & RESPONSE SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 34 SOFTWARE SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 35 MANAGED SERVICES SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 36 TRAINING SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 37 ANALYTICS-AS-A-SERVICE TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 38 CLOUD-BASED PLATFORMS SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 39 AUTOMATED ENFORCEMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 40 INTEGRATED BIG DATA TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 41 DRIVER BEHAVIOR MONITORING TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 42 SMART CITY INTEGRATORS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 43 NORTH AMERICA TO BE LARGEST REGIONAL MARKET DURING FORECAST PERIOD

- FIGURE 44 INDIA TO WITNESS FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 45 NORTH AMERICA: MARKET SNAPSHOT

- FIGURE 46 ASIA PACIFIC: MARKET SNAPSHOT

- FIGURE 47 TOP FIVE PUBLIC PLAYERS IN ROAD SAFETY MARKET, 2020-2024 (USD MILLION)

- FIGURE 48 SHARE OF LEADING COMPANIES IN ROAD SAFETY MARKET, 2024

- FIGURE 49 PRODUCT COMPARATIVE ANALYSIS (HARDWARE) (ROAD SAFETY)

- FIGURE 50 PRODUCT COMPARATIVE ANALYSIS (SOFTWARE) (ROAD SAFETY)

- FIGURE 51 FINANCIAL METRICS OF KEY VENDORS

- FIGURE 52 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 53 ROAD SAFETY MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 54 COMPANY FOOTPRINT (13 COMPANIES), 2024

- FIGURE 55 ROAD SAFETY MARKET: COMPANY EVALUATION MATRIX HARDWARE (STARTUPS/SMES), 2024

- FIGURE 56 ROAD SAFETY MARKET: COMPANY EVALUATION MATRIX SOFTWARE (STARTUPS/SMES), 2024

- FIGURE 57 JENOPTIK: COMPANY SNAPSHOT

- FIGURE 58 KAPSCH TRAFFICCOM: COMPANY SNAPSHOT

- FIGURE 59 SENSYS GATSO GROUP: COMPANY SNAPSHOT

- FIGURE 60 MOTOROLA SOLUTIONS: COMPANY SNAPSHOT

- FIGURE 61 SIEMENS: COMPANY SNAPSHOT

- FIGURE 62 CONDUENT: COMPANY SNAPSHOT

目次

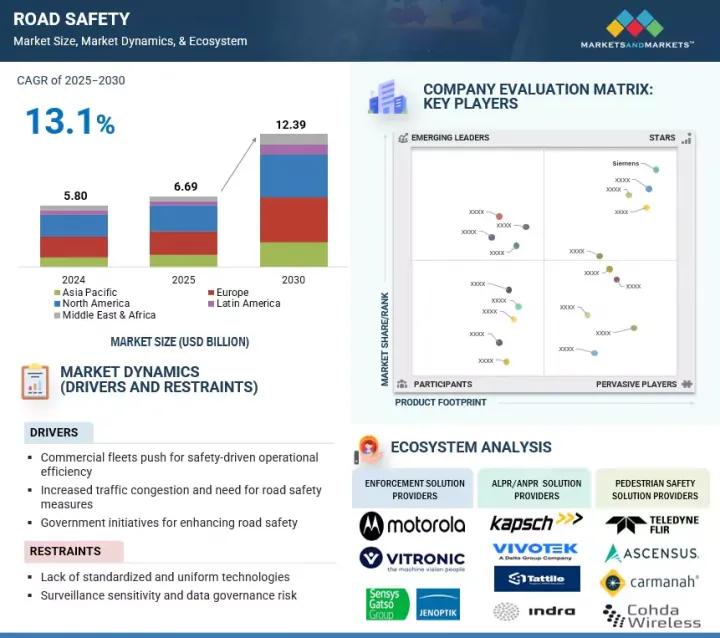

The road safety market is expanding rapidly, with a projected market size rising from USD 6.69 billion in 2025 to USD 12.39 billion by 2030, at a CAGR of 13.1% during the forecast period. To reduce accident costs and to protect assets and comply with regulations, fleet operators are now focusing on road safety. This is resulting in the rapid adoption rates of technologies such as the monitoring of driver behavior, AI dashcams, telematics, and even fatigue detection solutions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD (Million) |

| Segments | Offering, Deployment Model, Data Type, Enforcement Type, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

Along with access to advanced safety technologies, the commercial fleet now benefits from improved driver accountability, insurance discounts, and overall higher efficiency levels. Consequently, the demand for road safety solutions tailored to fleets is rising, driving growth and innovation across the road safety market.

Although road safety technologies have great potential for improvement, rising worries about the sensitivity of surveillance methods and risks related to data management pose significant restraints to market expansion. The widespread use of AI-powered cameras, automatic license plate recognition, and driver monitoring systems has led to increased examination of public surveillance and data privacy concerns.

"By end user, government & municipalities segment will likely hold the largest market share during the forecast period"

Government agencies and municipalities widely adopt road safety solutions. They play a major role in overseeing everything from awareness programs to managing and deploying comprehensive safety infrastructure and enforcement systems. They are crucial in the road safety market, acting as regulators and implementers of safety policies. By providing funding and developing programs, they can significantly influence public safety. Government agencies and municipalities are responsible for enforcing compliance with legislation and also allocating budgets for infrastructure improvements.

They manage traffic signals and signs on roadways, deploy cameras for red light and speed enforcement, combat violations using AI, and implement real-time traffic management systems. In November 2024, the city of Brampton in Canada worked with Jenoptik to deploy over 180 automated speed enforcement cameras to improve the compliance rate in school zones.

"By solution type, incident detection & response to account for the fastest growth rate during the forecast period"

The incident detection and response segment is a key part of the road safety market, focusing on quickly detecting traffic incidents and promptly notifying emergency services to minimize injuries, fatalities, and traffic disruptions. The incident detection and response segment integrates smart surveillance, communications infrastructure, and automated responses in a way that increases the safety of roadways and decreases response time in accidents or dangerous situations.

This segment aims to reduce road fatalities by enabling emergency services to analyze documentation and mitigate risks through early intervention. By decreasing road fatalities, the incident detection and response segment will also lessen delays and congestion caused by accidents, ultimately improving overall traffic efficiency. Additionally, this segment contributes significantly to the goals of Vision Zero, intelligent transport systems (ITS), and the readiness for autonomous vehicles, making it a high-growth area within the global road safety ecosystem.

"North America leads in market share while Asia Pacific emerges as the fastest-growing region in the road safety market"

North America currently holds the largest market share in the road safety market, driven by widespread digital adoption, smart infrastructure technologies, and the presence of major road safety vendors. North American governments are introducing various programs, such as Vision Zero, the U.S. National Roadway Safety Strategy (NRSS), and Canada's Road Safety Strategy 2025, that focus their priorities on safer road users, safer vehicles, and smarter infrastructure. The U.S. Department of Transportation is also encouraging innovation in road safety with its Safe Streets and Roads for All (SS4A) program, which is backed by USD 5 billion to implement AI-based enforcement programs, deploy automated speed cameras, and install smart traffic signals and pedestrian protections.

The Asia Pacific region is emerging as the fastest-growing region in the global road safety landscape, as it continues to urbanize, with increasing motorization rates and increased government desire to curb road traffic fatalities. In line with this, India, China, Japan, South Korea, and Australia are leading the way with their large investments into intelligent transportation systems (ITS), evolving smart city programs, and traffic enforcement technologies.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the road safety market.

- By Company: Tier I - 34%, Tier II - 43%, and Tier III - 23%

- By Designation: C-Level Executives - 50%, D-Level Executives -30%, and others - 20%

- By Region: North America - 30%, Europe - 30%, Asia Pacific - 25%, Middle East & Africa - 10%, and Latin America - 5%

The report profiles key players in the road safety market, including JENOPTIK (Germany), Kapsch TrafficCom (Austria), Sensys Gatso Group (Sweden), IDEMIA (France), Teledyne FLIR (US), Motorola Solutions (US), Verra Mobility (US), SWARCO (Austria), Siemens (Germany), Cubic Corporation (US), Conduent (US), VITRONIC (Germany), Dahua Technology (China), Laser Technology (US), Traffic Management Technology (South Africa), Truvelo (UK), Kria (Italy), Syntell (South Africa), Clearview Intelligence (UK), Simicon (Russia), FRED Engineering (Italy), Kodiak Robotics (US), Humanising Autonomy (UK), Vebit AI (US), Connected Wise LLC (US), Saferoad (Germany), LiveRoad Analytics (US), Acusensus (Australia), Valerann (UK), NoTraffic (Israel), and Vivacity (UK).

Research Coverage

This research report categorizes the road safety market based on offering [solution (type {enforcement solution, incident detection and response, ALPR/ANPR, traffic monitoring & control, pedestrian safety}, and component {hardware and software}) and services], deployment model (fixed installation, mobile/trailer-mounted systems, portable/temporary solutions, and cloud-based platforms), data type (video & image, sensor data and integrated big data), enforcement type (automated, manual, or hybrid), application (violation management, traffic optimization, accident prevention, emergency response, and public awareness & training, pedestrian & VRU protection, work zone safety management, insurance risk assessment), end user (government & municipalities, highway authorities, law enforcement agencies, private toll operators, smart city integrators, construction companies, others {fleet operators and insurance providers}) and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the road safety market. A detailed analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, and mergers and acquisitions; and recent developments associated with the road safety market. Competitive analysis of upcoming startups in the road safety market ecosystem was also covered in this report.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall road safety market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to improve their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (commercial fleets push for safety-driven operational efficiency, Enforcement to improve compliance with governments, the adoption of digitalization and technologies in the road safety market, government initiatives for enhancing road safety, urban surge fuels smart road safety revolution amid rising traffic risks), restraints (Lack of standardized and uniform technologies, data privacy and surveillance concerns hinder adoption of road safety technologies), opportunities (improved intelligent transportation systems for road safety, integration of AI and predictive analytics in traffic management systems, growth evolving 5G technology and transformation of road safety systems), and challenges (Digital reluctance and fragmentation in legacy fleet segments, infrastructure gaps and budget constraints limit road safety technology deployment)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the road safety market

- Market Development: Comprehensive information about lucrative markets - the report analyses the road safety market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the road safety market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like JENOPTIK (Germany), Kapsch TrafficCom (Austria), Sensys Gatso Group (Sweden), IDEMIA (France), Teledyne FLIR (US), Motorola Solutions (US), Verra Mobility (US), SWARCO (Austria), Siemens (Germany), Cubic Corporation (US), Conduent (US), VITRONIC (Germany), Dahua Technology (China), Laser Technology (US), Traffic Management Technology (South Africa), Truvelo (UK), Kria (Italy), Syntell (South Africa), Clearview Intelligence (UK), Simicon (Russia), FRED Engineering (Italy), Kodiak Robotics (US), Humanising Autonomy (UK), Vebit AI (US), Connected Wise LLC (US), Saferoad (Germany), LiveRoad Analytics (US), Acusensus (Australia), Valerann (UK), NoTraffic (Israel), and Vivacity (UK)

The report also helps stakeholders understand the pulse of the road safety market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION AND SCOPE

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary participants

- 2.1.2.2 Breakdown of primaries

- 2.1.2.3 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN ROAD SAFETY MARKET

- 4.2 ROAD SAFETY MARKET: TOP THREE APPLICATIONS

- 4.3 NORTH AMERICA: ROAD SAFETY MARKET, BY DATA TYPE AND ENFORCEMENT TYPE

- 4.4 ROAD SAFETY MARKET, BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Urban surge fuels smart road safety revolution amid rising traffic risks

- 5.2.1.2 Commercial fleets push for safety-driven operational efficiency

- 5.2.1.3 Enforcement to improve compliance with governments

- 5.2.1.4 Adoption of digitalization and technologies in road safety market

- 5.2.1.5 Government initiatives for enhancing road safety

- 5.2.2 RESTRAINTS

- 5.2.2.1 Lack of standardized and uniform technologies

- 5.2.2.2 Data privacy and surveillance concerns hinder adoption of road safety technologies

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Improved intelligent transportation systems for road safety

- 5.2.3.2 Integration of AI and predictive analytics in traffic management systems

- 5.2.3.3 Evolving 5g technology and transformation of road safety systems

- 5.2.4 CHALLENGES

- 5.2.4.1 Infrastructure gaps and budget constraints limit road safety technology deployment

- 5.2.4.2 Digital reluctance and fragmentation in legacy fleet segments

- 5.2.1 DRIVERS

- 5.3 IMPACT OF 2025 US TARIFF ON ROAD SAFETY MARKET

- 5.3.1 INTRODUCTION

- 5.3.2 KEY TARIFF RATES

- 5.3.3 PRICE IMPACT ANALYSIS

- 5.3.3.1 Strategic shifts and emerging trends

- 5.3.4 IMPACT ON COUNTRY/REGION

- 5.3.4.1 US

- 5.3.4.1.1 Strategic shifts and key observations

- 5.3.4.2 Europe

- 5.3.4.2.1 Strategic shifts and key observations

- 5.3.4.3 Asia Pacific

- 5.3.4.3.1 Strategic shifts and key observations

- 5.3.4.1 US

- 5.3.5 IMPACT ON END-USE INDUSTRIES

- 5.3.5.1 Government and municipalities

- 5.3.5.2 Highway authorities

- 5.3.5.3 Law enforcement agencies

- 5.3.5.4 Private toll operators

- 5.3.5.5 Smart city integrator

- 5.3.5.6 Construction companies

- 5.4 EVOLUTION OF ROAD SAFETY SOLUTIONS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 IMPACT OF GENERATIVE AI ON ROAD SAFETY MARKET

- 5.6.1 TOP USE CASES & MARKET POTENTIAL

- 5.6.1.1 Key use cases

- 5.6.2 TRAFFIC INCIDENT REPORTING AND DOCUMENTATION

- 5.6.3 SYNTHETIC DATA GENERATION FOR TRAINING AI MODELS

- 5.6.4 PREDICTIVE VIOLATION & ACCIDENT RISK MODELING

- 5.6.5 AUTOMATED PUBLIC AWARENESS CAMPAIGNS

- 5.6.6 LAW ENFORCEMENT SUPPORT

- 5.6.7 INFRASTRUCTURE DESIGN & SIMULATION

- 5.6.1 TOP USE CASES & MARKET POTENTIAL

- 5.7 ECOSYSTEM ANALYSIS

- 5.7.1 ROAD SAFETY MARKET: SOLUTION TYPE

- 5.7.1.1 Enforcement solution

- 5.7.1.2 ALPR/ANPR (automatic number plate recognition)

- 5.7.1.3 Incident detection & response

- 5.7.1.4 Traffic monitoring & control

- 5.7.1.5 Pedestrian safety solutions

- 5.7.1 ROAD SAFETY MARKET: SOLUTION TYPE

- 5.8 INVESTMENT LANDSCAPE AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 USE CASE 1: SIEMENS HELPED YUNEX TRAFFIC WITH ADAPTIVE TRAFFIC CONTROL AND MANAGEMENT, HIGHWAY, AND TUNNEL AUTOMATION AS WELL AS SMART SOLUTIONS FOR V2X AND ROAD USER CHARGING (TOLLING)

- 5.9.2 USE CASE 2: MOTOROLA SOLUTIONS HELPED VICTORIA POLICE WITH NUMBER PLATE RECOGNITION WITH ANPR TECHNOLOGY

- 5.9.3 USE CASE 3: CONDUENT AND HAYDEN AI ANNOUNCED TECHNOLOGY PARTNERSHIP TO IMPROVE BUS LANE PERFORMANCE AND TRAFFIC SAFETY

- 5.9.4 USE CASE 4: SWARCO ROAD MARKING SYSTEMS AND ISAC GMBH MEASURED DETECTABILITY OF ROAD MARKINGS

- 5.9.5 CASE STUDY 6: DATA COLLECTION LIMITED ENHANCED ROAD INFRASTRUCTURE MANAGEMENT WITH TELEDYNE FLIR IMAGING SOLUTIONS

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 Artificial intelligence (AI)

- 5.10.1.2 Internet of things (IoT)

- 5.10.1.3 Geographic information systems (GIS)

- 5.10.1.4 Automatic number plate recognition (ANPR)

- 5.10.1.5 Vehicle-to-infrastructure (V2I) and vehicle-to-everything (V2X)

- 5.10.2 COMPLEMENTARY TECHNOLOGIES

- 5.10.2.1 Big data and analytics

- 5.10.2.2 Edge computing

- 5.10.2.3 5G

- 5.10.3 ADJACENT TECHNOLOGIES

- 5.10.3.1 Advanced traffic management systems (ATMS)

- 5.10.3.2 Smart city solutions

- 5.10.3.3 Blockchain

- 5.10.1 KEY TECHNOLOGIES

- 5.11 TARIFF AND REGULATORY LANDSCAPE

- 5.11.1 TARIFF RELATED TO ROAD SAFETY SOLUTIONS

- 5.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.3 KEY REGULATIONS

- 5.11.3.1 North America

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.3.4 Middle East & Africa

- 5.11.3.5 Latin America

- 5.12 TRADE ANALYSIS

- 5.12.1 EXPORT SCENARIO OF ELECTRICAL SIGNALING AND TRAFFIC CONTROL EQUIPMENT (HS CODE 853080)

- 5.12.2 IMPORT SCENARIO OF ELECTRICAL SIGNALING AND TRAFFIC CONTROL EQUIPMENT (HS CODE 853080)

- 5.13 PATENT ANALYSIS

- 5.13.1 METHODOLOGY

- 5.13.2 PATENTS FILED, BY DOCUMENT TYPE

- 5.13.3 INNOVATION AND PATENT APPLICATIONS

- 5.14 PRICING ANALYSIS

- 5.14.1 AVERAGE SELLING PRICE OF OFFERING, BY KEY PLAYER, 2025

- 5.14.2 INDICATIVE PRICING, BY APPLICATION, 2025

- 5.15 KEY CONFERENCES AND EVENTS (2025-2026)

- 5.16 PORTER'S FIVE FORCES ANALYSIS

- 5.16.1 THREAT OF NEW ENTRANTS

- 5.16.2 THREAT OF SUBSTITUTES

- 5.16.3 BARGAINING POWER OF BUYERS

- 5.16.4 BARGAINING POWER OF SUPPLIERS

- 5.16.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.17 TRENDS AND DISRUPTIONS IMPACTING BUYERS

- 5.18 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.18.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.18.2 BUYING CRITERIA

- 5.19 TECHNOLOGY ROADMAP

- 5.19.1 ROAD SAFETY TECHNOLOGY ROADMAP TILL 2030

- 5.19.1.1 Short-term roadmap (2024-2026)

- 5.19.1.2 Mid-term roadmap (2026-2028)

- 5.19.1.3 Long-term roadmap (2028-2030)

- 5.19.1 ROAD SAFETY TECHNOLOGY ROADMAP TILL 2030

- 5.20 PARTNERSHIP & ECOSYSTEM STRATEGIES

- 5.20.1 PARTNERSHIP & ECOSYSTEM STRATEGIES

- 5.21 STRATEGIC IMPERATIVES FOR STAKEHOLDERS

- 5.21.1 STRATEGIC IMPERATIVES FOR STAKEHOLDERS

6 ROAD SAFETY MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: ROAD SAFETY MARKET DRIVERS

- 6.2 SOLUTION

- 6.2.1 ENABLING SAFER ROADS THROUGH END-TO-END INTELLIGENT TRAFFIC ENFORCEMENT AND MANAGEMENT SOLUTIONS

- 6.2.2 SOLUTION TYPE

- 6.2.2.1 Enforcement solutions

- 6.2.2.1.1 Red light enforcement

- 6.2.2.1.2 Speed enforcement systems

- 6.2.2.1.3 Seat belt & mobile phone enforcement

- 6.2.2.1.4 DUI enforcement

- 6.2.2.1.5 Temporary speed enforcement

- 6.2.2.2 ALPR/ANPR

- 6.2.2.2.1 Fixed ALPR systems

- 6.2.2.2.2 Mobile ALPR systems

- 6.2.2.2.3 Portable ALPR

- 6.2.2.2.4 ALPR analytics

- 6.2.2.3 Incident detection and response

- 6.2.2.3.1 Violation detection

- 6.2.2.3.2 Accident detection

- 6.2.2.3.3 Emergency vehicle preemption and notification

- 6.2.2.3.4 Congestion/Queue detection

- 6.2.2.3.5 Driver behavior monitoring systems

- 6.2.2.4 Traffic monitoring & control

- 6.2.2.4.1 Smart traffic signals

- 6.2.2.4.2 Variable message signs

- 6.2.2.4.3 Road weather information systems (RWIS)

- 6.2.2.4.4 Dynamic lane management

- 6.2.2.5 Pedestrian safety

- 6.2.2.5.1 Smart crosswalks

- 6.2.2.5.2 VRU detection

- 6.2.2.5.3 Pedestrian alert system

- 6.2.2.1 Enforcement solutions

- 6.2.3 COMPONENT

- 6.2.3.1 Hardware

- 6.2.3.1.1 Cameras

- 6.2.3.1.2 Sensors

- 6.2.3.1.3 Smart signs & signals

- 6.2.3.1.4 Roadside units (RSUS)

- 6.2.3.1.5 Other hardware

- 6.2.3.2 Software

- 6.2.3.2.1 Violation detection engines

- 6.2.3.2.2 AI/ML analytics platform

- 6.2.3.2.3 LPR/OCR recognition software

- 6.2.3.2.4 Command & simulation tools

- 6.2.3.2.5 Other software

- 6.2.3.1 Hardware

- 6.3 SERVICES

- 6.3.1 OFFER PROFESSIONAL AND MANAGED SERVICES FOR INSTALLATION, COMMISSIONING, CALIBRATION, AND FUNCTIONAL TESTING OF CRITICAL ROAD SAFETY EQUIPMENT

- 6.3.2 PROFESSIONAL SERVICES

- 6.3.2.1 Consulting

- 6.3.2.2 System integration

- 6.3.2.3 Training

- 6.3.2.4 Road safety audits

- 6.3.3 MANAGED SERVICES

- 6.3.3.1 Outsourced operations

- 6.3.3.2 System maintenance

- 6.3.3.3 Analytics-as-a-service

- 6.3.3.4 Back-office processing

7 ROAD SAFETY MARKET, BY DEPLOYMENT MODEL

- 7.1 INTRODUCTION

- 7.1.1 DEPLOYMENT MODEL: ROAD SAFETY MARKET DRIVERS

- 7.2 FIXED INSTALLATIONS

- 7.2.1 ESTABLISHING LONG-TERM AND HIGH-ACCURACY ROAD SAFETY INFRASTRUCTURE AT CRITICAL TRAFFIC ZONES

- 7.3 MOBILE/TRAILER-MOUNTED SYSTEMS

- 7.3.1 DEPLOYING SEMI-PERMANENT AND RELOCATABLE TRAFFIC MONITORING UNITS FOR FLEXIBLE AND TARGETED COVERAGE

- 7.4 PORTABLE/TEMPORARY SOLUTIONS

- 7.4.1 UTILIZING LIGHTWEIGHT AND RAPIDLY DEPLOYABLE ENFORCEMENT TOOLS FOR SHORT-DURATION OR ON-DEMAND TRAFFIC SAFETY OPERATIONS

- 7.5 CLOUD-BASED PLATFORMS

- 7.5.1 IMPLEMENTING CENTRALIZED AND SCALABLE CLOUD-BASED PLATFORMS TO MANAGE, PROCESS, AND ANALYZE ROAD SAFETY DATA IN REAL-TIME

8 ROAD SAFETY MARKET, BY ENFORCEMENT TYPE

- 8.1 INTRODUCTION

- 8.1.1 ENFORCEMENT TYPE: ROAD SAFETY MARKET DRIVERS

- 8.2 AUTOMATED ENFORCEMENT

- 8.2.1 DEPLOYING INTELLIGENT TECHNOLOGY-DRIVEN SYSTEMS TO ENABLE CONTINUOUS, UNBIASED, AND FULLY AUTOMATED ENFORCEMENT OF TRAFFIC VIOLATIONS ACROSS DIVERSE ENVIRONMENTS

- 8.3 MANUAL ENFORCEMENT

- 8.3.1 CONDUCTING FIELD-LEVEL ENFORCEMENT OPERATIONS THROUGH HUMAN INTERVENTION TO ENSURE REGULATORY COMPLIANCE AND ADDRESS SITUATIONAL ROAD SAFETY CHALLENGES

- 8.4 HYBRID ENFORCEMENT

- 8.4.1 ENSURE RELIABLE, FLEXIBLE, AND REAL-TIME AI DELIVERY WITH ADVANCED MODEL DEPLOYMENT AND SERVING FUNCTIONALITIES

9 ROAD SAFETY MARKET, BY DATA TYPE

- 9.1 INTRODUCTION

- 9.1.1 DATA TYPE: ROAD SAFETY MARKET DRIVERS

- 9.2 VIDEO & IMAGE

- 9.2.1 HARNESSING REAL-TIME AND HIGH-RESOLUTION VISUAL EVIDENCE THROUGH AI-ENABLED CAMERA NETWORKS TO AUTOMATE VIOLATION DETECTION AND ENHANCE INCIDENT TRACEABILITY IN TRAFFIC ECOSYSTEMS

- 9.3 SENSOR DATA

- 9.3.1 CONDUCTING DEPLOYING HIGH-PRECISION ROADWAY AND ROADSIDE SENSORS TO CAPTURE REAL-TIME VEHICLE AND TRAFFIC BEHAVIOR DATA FOR CONTINUOUS, NON-VISUAL MONITORING

- 9.4 INTEGRATED BIG DATA

- 9.4.1 AGGREGATING CROSS-DOMAIN AND MULTI-SOURCE DATASETS INTO SCALABLE PLATFORMS TO ENABLE PREDICTIVE ROAD SAFETY INTELLIGENCE, OPTIMIZE ENFORCEMENT STRATEGIES

10 ROAD SAFETY MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.1.1 APPLICATION: ROAD SAFETY MARKET DRIVERS

- 10.2 VIOLATION MANAGEMENT

- 10.2.1 IMPLEMENTING INTELLIGENT ROAD SAFETY SOLUTIONS TO AUTOMATE VIOLATION DETECTION AND STREAMLINE CITATION PROCESSING FOR SAFER ROAD NETWORKS

- 10.3 TRAFFIC OPTIMIZATION

- 10.3.1 USING DATA-DRIVEN CONTROL STRATEGIES AND REAL-TIME OPTIMIZATION TECHNOLOGIES WILL REDUCE CONGESTION AND ENHANCE MOBILITY ACROSS URBAN ROAD NETWORKS

- 10.4 ACCIDENT PREVENTION

- 10.4.1 DEPLOYING PREDICTIVE ANALYTICS AND ENVIRONMENTAL SENSING TECHNOLOGIES TO IDENTIFY RISK ZONES AND IMPLEMENT PROACTIVE MEASURES

- 10.5 EMERGENCY RESPONSE

- 10.5.1 ENABLING ACCELERATED INCIDENT DETECTION AND REAL-TIME COORDINATION OF EMERGENCY SERVICES TO REDUCE RESPONSE TIME

- 10.6 DRIVER BEHAVIOR MONITORING

- 10.6.1 LEVERAGING IN-VEHICLE ANALYTICS AND SENSOR FUSION TO TRACK AND CORRECT UNSAFE DRIVING BEHAVIORS FOR LONG-TERM BEHAVIORAL CHANGE AND CRASH REDUCTION

- 10.7 PUBLIC AWARENESS/TRAINING

- 10.7.1 PROMOTING ROAD SAFETY CULTURE THROUGH IMMERSIVE AWARENESS PROGRAMS AND STRUCTURED TRAINING

- 10.8 PEDESTRIAN & VRU PROTECTION

- 10.8.1 INTEGRATING SMART INFRASTRUCTURE AND DETECTION SYSTEMS TO SAFEGUARD PEDESTRIANS AND VULNERABLE ROAD USERS THROUGH REAL-TIME ALERTS

- 10.9 WORK ZONE SAFETY MANAGEMENT

- 10.9.1 ENHANCING SAFETY IN ACTIVE WORK ZONES BY DEPLOYING CONNECTED ENFORCEMENT SYSTEMS AND DYNAMIC WARNINGS TO PREVENT COLLISIONS AND PROTECT ROAD CREWS

- 10.10 INSURANCE RISK ASSESSMENT

- 10.10.1 UTILIZING BEHAVIORAL ANALYTICS AND TELEMATICS TO ACCURATELY ASSESS DRIVER RISK PROFILES AND INFORM DYNAMIC, USAGE-BASED INSURANCE AND SAFETY STRATEGIES

11 ROAD SAFETY MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.1.1 END USER: ROAD SAFETY MARKET DRIVERS

- 11.2 GOVERNMENT & MUNICIPALITIES

- 11.2.1 GOVERNMENTS AND MUNICIPALITIES LEAD ROAD SAFETY EFFORTS THROUGH FUNDING, REGULATION, AND SMART CITY INITIATIVES

- 11.3 HIGHWAY AUTHORITIES

- 11.3.1 HIGHWAY AUTHORITIES ADOPT SMART INFRASTRUCTURE TO ENSURE SAFETY ON HIGH-SPEED ROAD NETWORKS

- 11.4 LAW ENFORCEMENT AGENCIES

- 11.4.1 LAW ENFORCEMENT AGENCIES EMBRACE SURVEILLANCE AND ANALYTICS TO MONITOR AND CONTROL TRAFFIC VIOLATIONS

- 11.5 PRIVATE TOLL OPERATORS

- 11.5.1 TOLL OPERATORS INVEST IN INTELLIGENT SYSTEMS TO ENSURE SAFE, EFFICIENT, AND COMPLIANT ROAD USAGE

- 11.6 SMART CITY INTEGRATORS

- 11.6.1 SMART CITY INTEGRATORS EMBED ROAD SAFETY WITHIN BROADER URBAN DIGITAL INFRASTRUCTURE

- 11.7 CONSTRUCTION COMPANIES

- 11.7.1 CONSTRUCTION FIRMS IMPLEMENT SAFETY PROTOCOLS AND TECHNOLOGIES ACROSS ROAD DEVELOPMENT PHASES

- 11.8 OTHER END USERS

12 ROAD SAFETY MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 NORTH AMERICA: ROAD SAFETY MARKET DRIVERS

- 12.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 12.2.3 US

- 12.2.3.1 Institutionalized cross-sector data integration and predictive enforcement to scale vision zero across diverse urban and rural mobility ecosystems

- 12.2.4 CANADA

- 12.2.4.1 Align safety modernization with climate goals through municipal co-funding, open data mandates, and community-based AI enforcement

- 12.3 EUROPE

- 12.3.1 EUROPE: ROAD SAFETY MARKET DRIVERS

- 12.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 12.3.3 UK

- 12.3.3.1 UK's nationwide deployment of AI-powered speed enforcement, smart crossings, and connected mobility zones to drive toward zero fatalities

- 12.3.4 GERMANY

- 12.3.4.1 Germany scaling road safety through V2X integration, dynamic lane controls, and urban zero-vision zones

- 12.3.5 FRANCE

- 12.3.5.1 France's tech-driven road safety surge expanding autonomous radar networks, smart signage, and urban speed harmonization

- 12.3.6 ITALY

- 12.3.6.1 Italy building safer streets through urban ITS deployment, smart crosswalks, and behavioral analytics to protect vulnerable road users

- 12.3.7 SPAIN

- 12.3.7.1 Spain's smart enforcement strategy scaling intelligent cameras, real-time incident detection, and speed harmonization for safer mobility

- 12.3.8 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 ASIA PACIFIC: ROAD SAFETY MARKET DRIVER

- 12.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 12.4.3 CHINA

- 12.4.3.1 China scales AI-driven enforcement in tier 2/3 cities

- 12.4.4 JAPAN

- 12.4.4.1 Japan deploying smart crosswalks with embedded led alerts and pedestrian protection systems

- 12.4.5 INDIA

- 12.4.5.1 Accelerating road safety transformation through data-driven enforcement and public-private innovation

- 12.4.6 AUSTRALIA & NEW ZEALAND

- 12.4.6.1 Pioneering smart safety through predictive analytics and digital infrastructure for zero fatality roads

- 12.4.7 ASEAN

- 12.4.7.1 Unlocking scalable road safety through regional standards and smart mobility innovation

- 12.4.8 SOUTH KOREA

- 12.4.8.1 Korea driving Vision Zero through AI-powered pedestrian safety and urban intelligence

- 12.4.9 REST OF ASIA PACIFIC

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 MIDDLE EAST & AFRICA: ROAD SAFETY MARKET DRIVERS

- 12.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 12.5.3 SAUDI ARABIA

- 12.5.3.1 Drive holistic integration of AI, infrastructure, and enforcement under Vision 2030 mobility goals

- 12.5.4 UNITED ARAB EMIRATES (UAE)

- 12.5.4.1 Expand interoperable urban safety platforms leveraging AI, V2X, and municipal data integration

- 12.5.5 SOUTH AFRICA

- 12.5.5.1 Expansion of multi-layered safety programs integrating enforcement, education, and urban design in high-risk zones

- 12.5.6 QATAR

- 12.5.6.1 Leveraging world cup infrastructure legacy to build scalable, high-compliance smart enforcement mode

- 12.5.7 REST OF MIDDLE EAST & AFRICA

- 12.6 LATIN AMERICA

- 12.6.1 LATIN AMERICA: ROAD SAFETY MARKET DRIVERS

- 12.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 12.6.3 BRAZIL

- 12.6.3.1 Modernizing legacy enforcement networks through regionalized, data-centric road safety platforms

- 12.6.4 MEXICO

- 12.6.4.1 Expansion of municipal safety intelligence systems to address VRU vulnerability and informal transit risks

- 12.6.5 ARGENTINA

- 12.6.5.1 Strengthening of data-driven enforcement and crash analytics amid institutional decentralization

- 12.6.6 REST OF LATIN AMERICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 13.3 REVENUE ANALYSIS, 2020-2024

- 13.4 MARKET SHARE ANALYSIS, 2024

- 13.4.1 MARKET RANKING ANALYSIS

- 13.5 PRODUCT COMPARATIVE ANALYSIS

- 13.5.1 PRODUCT COMPARATIVE ANALYSIS, BY HARDWARE (ROAD SAFETY)

- 13.5.1.1 TruSpeed Laser (Laser Technology)

- 13.5.1.2 Redflex RadarCam (Traffic Management Technologies)

- 13.5.1.3 Enforcer Portable System (Trifoil Group)

- 13.5.1.4 Camera-based Speed System (Syntell)

- 13.5.1.5 Gatso T-Series (Sensys Gatso Group)

- 13.5.2 PRODUCT COMPARATIVE ANALYSIS, BY SOFTWARE (ROAD SAFETY)

- 13.5.2.1 TRIPS platform (Fred Engineering)

- 13.5.2.2 Behavior AI (Humanising Autonomy)

- 13.5.2.3 SafeCam AI (Vebits AI)

- 13.5.2.4 SmartMobility Suite (Connected Wise)

- 13.5.2.5 LiveRoad Insights (LiveRoad Analytics)

- 13.5.1 PRODUCT COMPARATIVE ANALYSIS, BY HARDWARE (ROAD SAFETY)

- 13.6 COMPANY VALUATION AND FINANCIAL METRICS

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.7.5.1 Company footprint

- 13.7.5.2 Regional footprint

- 13.7.5.3 Offering footprint

- 13.7.5.4 Application footprint

- 13.7.5.5 End user footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES (HARDWARE), 2024

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES (SOFTWARE), 2024

- 13.9.1 PROGRESSIVE COMPANIES

- 13.9.2 RESPONSIVE COMPANIES

- 13.9.3 DYNAMIC COMPANIES

- 13.9.4 STARTING BLOCKS

- 13.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.9.5.1 Detailed list of key startups/SMEs

- 13.9.5.2 Competitive benchmarking of key startups/SMEs (hardware)

- 13.9.5.3 Competitive benchmarking of key startups/SMEs (software)

- 13.10 COMPETITIVE SCENARIO AND TRENDS

- 13.10.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 13.10.2 DEALS

14 COMPANY PROFILES

- 14.1 MAJOR PLAYERS

- 14.1.1 JENOPTIK

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches and enhancements

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths/Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 KAPSCH TRAFFICCOM

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches and enhancements

- 14.1.2.3.2 Deals

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths/Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 SENSYS GATSO GROUP

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches and enhancements

- 14.1.3.3.2 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths/Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 VERRA MOBILITY

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches and enhancements

- 14.1.4.3.2 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths/Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 TELEDYNE FLIR

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches and enhancements

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 MOTOROLA SOLUTIONS

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches and enhancements

- 14.1.6.3.2 Deals

- 14.1.7 IDEMIA

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches and enhancements

- 14.1.7.3.2 Deals

- 14.1.8 SWARCO

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches and enhancements

- 14.1.8.3.2 Deals

- 14.1.9 VITRONIC

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches and enhancements

- 14.1.10 SIEMENS

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.11 CONDUENT

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches and enhancements

- 14.1.11.3.2 Deals

- 14.1.12 CUBIC CORPORATION

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Product launches and enhancements

- 14.1.12.3.2 Deals

- 14.1.13 DAHUA TECHNOLOGY

- 14.1.14 LASER TECHNOLOGIES

- 14.1.1 JENOPTIK

- 14.2 OTHER PLAYERS

- 14.2.1 TRAFFIC MANAGEMENT TECHNOLOGIES

- 14.2.2 TRIFOIL

- 14.2.3 KRIA

- 14.2.4 SYNTELL

- 14.2.5 TRUVELO

- 14.2.6 CLEARVIEW INTELLIGENCE