|

|

市場調査レポート

商品コード

1796198

種子応用技術市場/SATの世界市場:技術別、機能別、作物タイプ別、地域別 - 2030年までの予測Seed Technologies Market/ SAT Market by Function (Seed Protection, Seed Enhancement, and Precision Seeding), Technology, Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables), and Region - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 種子応用技術市場/SATの世界市場:技術別、機能別、作物タイプ別、地域別 - 2030年までの予測 |

|

出版日: 2025年08月06日

発行: MarketsandMarkets

ページ情報: 英文 551 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

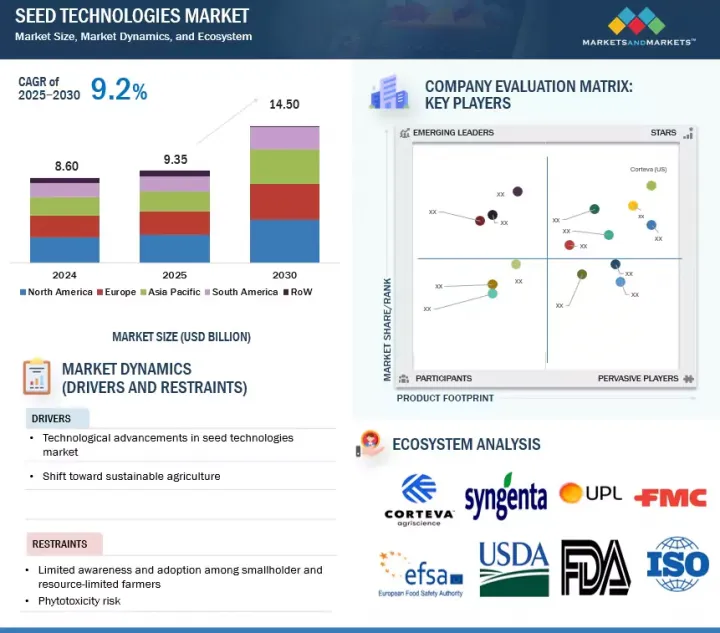

世界の種子応用技術の市場規模は2025年に93億5,000万米ドルと推定され、予測期間中のCAGRは9.2%と見込まれており、2030年には145億米ドルに達すると予測されています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2025年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 検討単位 | 金額(米ドル)および数量(KT) |

| セグメント別 | 技術別、機能別、作物タイプ別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、南米、RoW |

種子応用技術市場は、作物の高収量化ニーズの高まり、害虫・病害圧力の増大、製剤・送達技術の進歩によって牽引されています。高価値のハイブリッド種子や遺伝子組み換え種子の採用が増加しているため、保護および性能向上種子処理の需要が拡大しています。

さらに、政府の好意的な政策やインセンティブに支えられた持続可能な農業への世界のシフトが、生物学的種子処理剤の使用を加速させています。商業的農業とデジタル農業の拡大は、市場の効率と作物保護を強化しています。主な動向は、環境に優しい生物学的および微生物ベースの種子処理剤の使用の増加であり、規制当局や消費者からの持続可能性の要求と一致しています。

しかし、新興国市場の零細農家では、種子コーティング技術の利点が証明されているにもかかわらず、その認知度や利用しやすさが限られているため、普及が妨げられており、市場の成長を抑制しています。

種子コーティング技術は、種子性能の向上、ハンドリングの改善、作物保護剤および栄養剤の標的への送達に対する需要の増加により、著しい成長を示すと予測されます。これらの技術には、種子の周囲に均一な層を形成するポリマー、着色剤、ミネラル、有効成分の塗布が含まれ、流動性、単一性、機械的および精密農業システムにおける植え付け精度を向上させる。野菜、トウモロコシ、穀物などの高価値作物でコーティング種子の採用が増加していることに加え、生物刺激剤や微生物接種剤を含む生物学的コーティングの受け入れが拡大していることも、市場の拡大をさらに後押ししています。

さらに、種子コーティングは自動種子処理装置や植え付け装置との互換性を提供し、圃場でのばらつきや人件費を削減します。ポリマー製剤と放出制御型コーティングの革新も、保存期間と処理効力の向上につながるため、支持を集めています。農家が投入効率と均一な作物の出穂を優先する傾向が強まるなか、種子コーティング技術は先進国市場と新興国市場で広く採用される見込みです。

穀物・穀類は、その広大な世界的栽培面積と食糧安全保障における重要な役割によって、種子応用技術市場の作物タイプセグメントで最大のシェアを占めています。トウモロコシ、小麦、米、大麦などの作物は多くの地域で主食であり、初期段階の害虫や病害の圧力に非常に敏感であるため、種子応用ソリューションの最有力候補となっています。農家は、苗の活力を高め、均一な出穂を確保し、土壌伝染性の病原菌や害虫から守るために、化学的・生物学的治療を含む種子施用技術に依存しています。

特にトウモロコシでは、高収量品種や遺伝子組み換え品種が広く採用されているため、効果的な種子保護の必要性がさらに高まっています。さらに、製剤技術の進歩や、大規模機械化農業システムへの種子施用製品の統合により、主要穀物生産地域全体でその使用が強化されています。政府の支援政策と主要農薬・種子企業の存在が、このセグメントにおける穀物・穀物市場の地位強化に寄与しています。

北米は、先進的な農法の普及、主要な業界プレイヤーの存在、遺伝子組み換え種子や高価値種子の高い使用率に支えられ、予測期間中、世界の種子応用技術市場で最大のシェアを占めると予想されます。同地域の治療市場は確立されており、市場成長に寄与しています。トウモロコシ、ダイズ、カノーラは、種子保護・強化ソリューションの旺盛な需要を牽引しています。さらに、北米は精密農業や総合的害虫管理などの技術革新でリードしており、市場での優位性をさらに強めています。

対照的に、アジア太平洋は、食糧需要の増加、急速な人口増加、インド、中国、東南アジア諸国における農業の近代化に牽引され、予測期間中、種子応用技術の市場として最も急成長すると予測されます。農家の意識の高まり、持続可能な農業を支援する政府の取り組み、ハイブリッド種子の採用拡大が、種子処理市場の需要を加速しています。さらに、商業的農業の拡大、農業投入物へのアクセスの改善、世界の種子応用技術企業からの投資の増加が、この地域全体の市場成長を促進すると予想されます。

当レポートでは、世界の種子応用技術市場/SAT市場について調査し、技術別、機能別、作物タイプ別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 種子応用技術市場の参入企業にとって魅力的な機会

- 北米:種子応用技術市場(機能別・国別)

- 国別種子応用技術市場

- 種子応用技術市場(技術別・地域別)

- 種子応用技術市場(機能別・地域別)

- 作物タイプ別・地域別種子応用技術市場

第5章 市場概要

- イントロダクション

- マクロ経済指標

- 主要な商業用種子生産の成長

- 高価値作物の市場需要の増加

- 有機農業の実践の成長

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

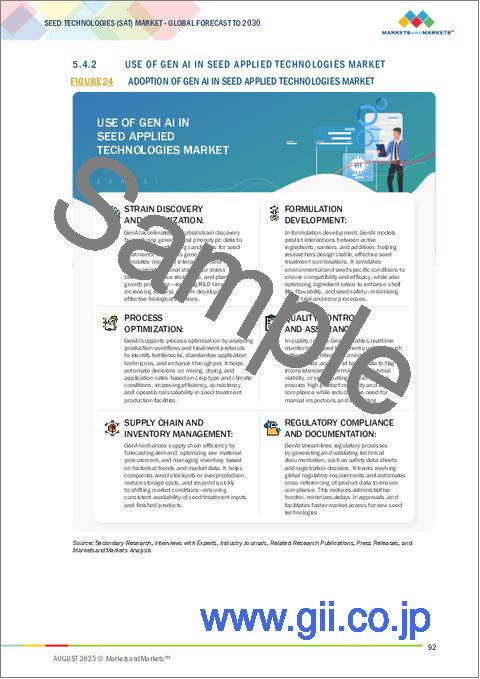

- AI/生成AIが種子応用技術市場に与える影響

- イントロダクション

- 種子応用技術市場におけるGEN AIの活用

- ケーススタディ分析

第6章 業界動向

- イントロダクション

- 2025年の米国関税の影響- 種子応用技術市場

- イントロダクション

- 主要関税率

- 価格影響分析

- 国/地域への影響

- 最終用途産業への影響

- バリューチェーン分析

- 貿易分析

- 技術分析

- 価格分析

- エコシステム分析

- 顧客ビジネスに影響を与える動向/混乱

- 特許分析

- 2025年~2026年の主な会議とイベント

- 規制状況

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- 投資と資金調達のシナリオ

- ケーススタディ分析

- BIOWEGとバイエルが持続可能な農業のための生分解性種子コーティングの開発で提携

- ボレガード社がセルロースベースの生分解性種子コーティングを発表

- キンゼの真のスピードイノベーション:高速での精密植栽を再定義

- AGCOの戦略的飛躍:トリンブルAGとの合弁事業を通じて精密農業を推進

第7章 種子応用技術市場(技術別)

- イントロダクション

- 種子コーティング

- 種子処理

- 種子ペレット化

- 種子の準備と調整

- 種子の消毒

- 精密播種

第8章 種子応用技術市場(機能別)

- イントロダクション

- 種子保護

- 種子の強化

- 精密播種

第9章 種子応用技術市場(作物タイプ別)

- イントロダクション

- 油糧種子と豆類

- 穀物

- 果物と野菜

- その他の作物

第10章 種子応用技術市場(地域別)

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- ドイツ

- スペイン

- イタリア

- 英国

- その他

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリアとニュージーランド

- その他

- 南米

- ブラジル

- アルゼンチン

- その他

- その他の地域

- アフリカ

- 中東

第11章 競合情勢

- 概要

- 主要参入企業の戦略/強み

- 収益分析、2020年~2024年

- 市場シェア分析、2024年

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業、2024年

- 企業評価と財務指標

- ブランド/製品比較

- 競合シナリオと動向

第12章 企業プロファイル

- 主要参入企業

- BASF SE

- CORTEVA

- SYNGENTA

- BAYER AG

- UPL

- FMC CORPORATION

- SUMITOMO CHEMICAL CO., LTD.

- CRODA INTERNATIONAL PLC

- NUFARM

- NOVONESIS GROUP

- SYENSQO

- AGCO CORPORATION

- DEERE & COMPANY

- KINZE MANUFACTURING

- GERMAINS SEED TECHNOLOGY

- その他の企業(スタートアップ/中小企業)

- VERDESIAN LIFE SCIENCES

- ANDERMATT GROUP AG

- NAIO TECHNOLOGY INC.

- IPL BIOLOGICALS

- AGRILIFE

- ROVENSA NEXT

- BIONEMA

- BIOCONSORTIA

- NORDIA MICROBES A/S

- APHEA.BIO

第13章 隣接市場と関連市場

第14章 付録

List of Tables

- TABLE 1 SEED APPLIED TECHNOLOGIES MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 USD EXCHANGE RATES CONSIDERED, 2020-2024

- TABLE 3 SEED APPLIED TECHNOLOGIES MARKET SNAPSHOT, 2025 VS. 2030

- TABLE 4 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 5 EXPORT VALUE OF HS CODE 3808, BY KEY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 6 IMPORT VALUE OF HS CODE 3808, BY KEY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 7 AVERAGE SELLING PRICE TREND OF SEED APPLIED TECHNOLOGIES, BY FUNCTION, 2020-2024 (USD/KG)

- TABLE 8 AVERAGE SELLING PRICE TREND, BY REGION, 2020-2024 (USD/KG)

- TABLE 9 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY FUNCTION, 2024 (USD/KG)

- TABLE 10 SEED APPLIED TECHNOLOGIES MARKET: ROLE OF PLAYERS IN ECOSYSTEM

- TABLE 11 KEY PATENTS PERTAINING TO SEED APPLIED TECHNOLOGIES, 2015-2025

- TABLE 12 SEED APPLIED TECHNOLOGIES MARKET: CONFERENCES AND EVENTS, 2025-2026

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 SOUTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 REST OF WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 PORTER'S FIVE FORCES IMPACT ON SEED APPLIED TECHNOLOGIES MARKET

- TABLE 19 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY FUNCTION

- TABLE 20 KEY BUYING CRITERIA, BY FUNCTION

- TABLE 21 SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 22 SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 23 SEED COATING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 24 SEED COATING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 25 SEED COATING: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 26 SEED COATING: SEED APPLIED TECHNOLOGIES, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 27 SEED DRESSING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 28 SEED DRESSING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 29 SEED DRESSING: SEED APPLIED TECHNOLOGIES, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 30 SEED DRESSING: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 31 SEED PELLETING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 32 SEED PELLETING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33 SEED PELLETING: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 34 SEED PELLETING: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 35 SEED PRIMING & CONDITIONING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 36 SEED PRIMING & CONDITIONING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37 SEED PRIMING & CONDITIONING: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 38 SEED PRIMING & CONDITIONING: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 39 SEED DISINFECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 40 SEED DISINFECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 41 SEED DISINFECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 42 SEED DISINFECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 43 PRECISION SEEDING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 44 PRECISION SEEDING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 45 PRECISION SEEDING: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 46 PRECISION SEEDING: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 47 SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 48 SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 49 SEED APPLIED TECHNOLOGIES MARKET, (SEED PROTECTION), BY FUNCTION, 2020-2024 (KILOTON)

- TABLE 50 SEED APPLIED TECHNOLOGIES MARKET, (SEED PROTECTION), BY FUNCTION, 2025-2030 (KILOTON)

- TABLE 51 SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION FUNCTION, 2020-2024 (USD MILLION)

- TABLE 52 SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION FUNCTION, 2025-2030 (USD MILLION)

- TABLE 53 SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION FUNCTION, 2020-2024 (KILOTON)

- TABLE 54 SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION FUNCTION, 2025-2030 (KILOTON)

- TABLE 55 CHEMICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 56 CHEMICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 57 CHEMICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (KILOTON)

- TABLE 58 CHEMICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 59 CHEMICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 60 CHEMICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 61 CHEMICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 62 CHEMICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 63 INSECTICIDE SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 64 INSECTICIDE SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 65 FUNGICIDE SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 66 FUNGICIDE SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 67 KEY NEMATICIDE BRANDS OF TOP GLOBAL COMPANIES

- TABLE 68 NEMATICIDES & OTHERS SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 69 NEMATICIDES & OTHERS SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 70 BIOLOGICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 71 BIOLOGICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 72 BIOLOGICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (KILOTON)

- TABLE 73 BIOLOGICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 74 BIOLOGICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 75 BIOLOGICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 76 BIOLOGICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 77 BIOLOGICAL SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 78 BIOINSECTICIDE SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 79 BIOINSECTICIDE SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 80 BIOFUNGICIDE SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 81 BIOFUNGICIDE SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 82 BIONEMATICIDES & OTHERS SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 83 BIONEMATICIDES & OTHERS SEED PROTECTION: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

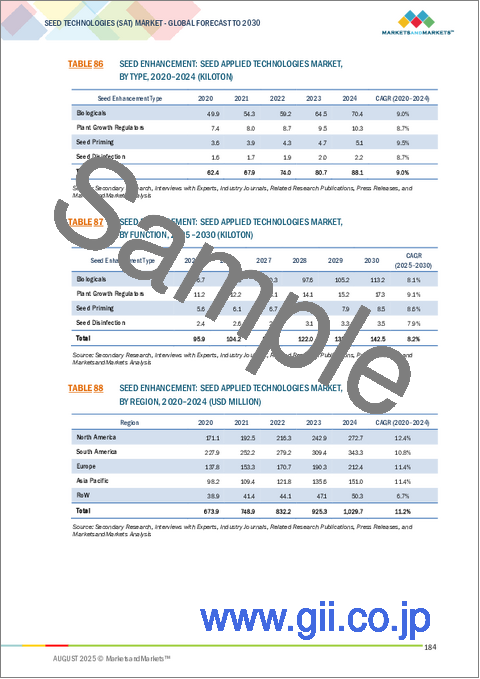

- TABLE 84 SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 85 SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 86 SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (KILOTON)

- TABLE 87 SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (KILOTON)

- TABLE 88 SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 89 SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 90 SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 91 SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 92 BIOLOGICAL SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 93 BIOLOGICAL SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 94 BIOLOGICAL SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (KILOTON)

- TABLE 95 BIOLOGICAL SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 96 BIOFERTILIZER SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 97 BIOFERTILIZER SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 98 BIOSTIMULANT SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 99 BIOSTIMULANT SEED ENHANCEMENT: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 100 PLANT GROWTH REGULATORS: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 101 PLANT GROWTH REGULATORS: SEED APPLIED TECHNOLOGIES MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 102 PRECISION SEEDING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 103 PRECISION SEEDING: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 104 SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 105 SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 106 SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (KILOTON)

- TABLE 107 SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (KILOTON)

- TABLE 108 OILSEED & PULSES: SEED APPLIED TECHNOLOGIES MARKET, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 109 OILSEED & PULSES: SEED APPLIED TECHNOLOGIES MARKET, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 110 OILSEED & PULSES: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 111 OILSEED & PULSES: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 112 OILSEED & PULSES: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 113 OILSEED & PULSES: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 114 APPLICATION AREAS OF SOYBEAN

- TABLE 115 CEREALS & GRAINS: SEED APPLIED TECHNOLOGIES MARKET, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 116 CEREALS & GRAINS: SEED APPLIED TECHNOLOGIES MARKET, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 117 CEREALS & GRAINS: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 118 CEREALS & GRAINS: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 119 CEREALS & GRAINS: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 120 CEREALS & GRAINS: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 121 FRUITS & VEGETABLES: SEED APPLIED TECHNOLOGIES MARKET, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 122 FRUITS & VEGETABLES: SEED APPLIED TECHNOLOGIES MARKET, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 123 FRUITS & VEGETABLES: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 124 FRUITS & VEGETABLES: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 125 FRUITS & VEGETABLES: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 126 FRUITS & VEGETABLES: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 127 OTHER CROP TYPES: SEED APPLIED TECHNOLOGIES MARKET, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 128 OTHER CROP TYPES: SEED APPLIED TECHNOLOGIES MARKET, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 129 OTHER CROPS: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 130 OTHER CROPS: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 131 OTHER CROPS: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 132 OTHER CROPS: SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 133 SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 134 SEED APPLIED TECHNOLOGIES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 135 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 136 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 137 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 138 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 139 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 140 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 141 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 142 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 143 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY INSECTICIDE TYPE, 2020-2024 (USD MILLION)

- TABLE 144 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY INSECTICIDE TYPE, 2025-2030 (USD MILLION)

- TABLE 145 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNGICIDE TYPE, 2020-2024 (USD MILLION)

- TABLE 146 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNGICIDE TYPE, 2025-2030 (USD MILLION)

- TABLE 147 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY NEMATICIDE & OTHERS TYPE, 2020-2024 (USD MILLION)

- TABLE 148 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY NEMATICIDE & OTHERS TYPE, 2025-2030 (USD MILLION)

- TABLE 149 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 150 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 151 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOINSECTICIDE SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 152 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOINSECTICIDE SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 153 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFUNGICIDE SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 154 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFUNGICIDE SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 155 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIONEMATICIDES & OTHER SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 156 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIONEMATICIDES & OTHER SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 157 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 158 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 159 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL TYPE, 2020-2024 (USD MILLION)

- TABLE 160 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL TYPE, 2025-2030 (USD MILLION)

- TABLE 161 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFERTILIZER SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 162 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFERTILIZER SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 163 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOSTIMULANT SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 164 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOSTIMULANT SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 165 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY PLANT GROWTH REGULATOR SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 166 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY PLANT GROWTH REGULATOR SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 167 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 168 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 169 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS & PULSES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 170 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS & PULSES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 171 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 172 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 173 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 174 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 175 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 176 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 177 NORTH AMERICA: SEED APPLIED TCHNOLOGIES MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 178 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 179 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED COATING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 180 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED COATING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 181 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DRESSING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 182 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DRESSING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 183 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PELLETING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 184 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PELLETING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 185 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PRIMING & CONDITIONING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 186 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PRIMING & CONDITIONING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 187 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DISINFECTION TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 188 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DISINFECTION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 189 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY PRECISION SEEDING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 190 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY PRECISION SEEDING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 191 US: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 192 US: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 193 US: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 194 US: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 195 US: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 196 US: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 197 US: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 198 US: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 199 US: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 200 US: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 201 US: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 202 US: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 203 US: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 204 US: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 205 US: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 206 US: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 207 US: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 208 US: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 209 US: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 210 US: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 211 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 212 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 213 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 214 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 215 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 216 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 217 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 218 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 219 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 220 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 221 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 222 CANADA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 223 CANADA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 224 CANADA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 225 CANADA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 226 CANADA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 227 CANADA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 228 CANADA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 229 CANADA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 230 CANADA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 231 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 232 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 233 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 234 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 235 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 236 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 237 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 238 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 239 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 240 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 241 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 242 MEXICO: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 243 MEXICO: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 244 MEXICO: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 245 MEXICO: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 246 MEXICO: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 247 MEXICO: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 248 MEXICO: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 249 MEXICO: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 250 MEXICO: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 251 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 252 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 253 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 254 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 255 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 256 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 257 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 258 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 259 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY INSECTICIDE TYPE, 2020-2024 (USD MILLION)

- TABLE 260 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY INSECTICIDE TYPE, 2025-2030 (USD MILLION)

- TABLE 261 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY FUNGICIDE TYPE, 2020-2024 (USD MILLION)

- TABLE 262 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY FUNGICIDE TYPE, 2025-2030 (USD MILLION)

- TABLE 263 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY NEMATICIDE & OTHERS TYPE, 2020-2024 (USD MILLION)

- TABLE 264 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY NEMATICIDE & OTHERS TYPE, 2025-2030 (USD MILLION)

- TABLE 265 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 266 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 267 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOINSECTICIDE SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 268 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOINSECTICIDE SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 269 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFUNGICIDE SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 270 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFUNGICIDE SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 271 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIONEMATICIDES & OTHER SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 272 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIONEMATICIDES & OTHER SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 273 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 274 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 275 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL TYPE, 2020-2024 (USD MILLION)

- TABLE 276 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL TYPE, 2025-2030 (USD MILLION)

- TABLE 277 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFERTILIZER SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 278 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFERTILIZER SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 279 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOSTIMULANT SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 280 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOSTIMULANT SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 281 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY PLANT GROWTH REGULATOR SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 282 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY PLANT GROWTH REGULATOR SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 283 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 284 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 285 EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 286 EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 287 EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 288 EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 289 EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 290 EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 291 EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 292 EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 293 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 294 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 295 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED COATING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 296 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED COATING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 297 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DRESSING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 298 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DRESSING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 299 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PELLETING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 300 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PELLETING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 301 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PRIMING & CONDITIONING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 302 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PRIMING & CONDITIONING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 303 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DISINFECTION TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 304 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DISINFECTION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 305 EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY PRECISION SEEDING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 306 EUROPE: PRECISION SEEDING MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 307 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 308 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 309 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 310 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 311 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 312 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 313 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 314 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 315 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 316 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 317 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 318 FRANCE: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 319 FRANCE: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP, 2020-2024 (USD MILLION)

- TABLE 320 FRANCE: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 321 FRANCE: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 322 FRANCE: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 323 FRANCE: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 324 FRANCE: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 325 FRANCE: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 326 FRANCE: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 327 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 328 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 329 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 330 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 331 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 332 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 333 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 334 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 335 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 336 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 337 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 338 GERMANY: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 339 GERMANY: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 340 GERMANY: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 341 GERMANY: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 342 GERMANY: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 343 GERMANY: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 344 GERMANY: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 345 GERMANY: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 346 GERMANY: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 347 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 348 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 349 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 350 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 351 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 352 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 353 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 354 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 355 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 356 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 357 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 358 SPAIN: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 359 SPAIN: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 360 SPAIN: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 361 SPAIN: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 362 SPAIN: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 363 SPAIN: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 364 SPAIN: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 365 SPAIN: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 366 SPAIN: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 367 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 368 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 369 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 370 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 371 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 372 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 373 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 374 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 375 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 376 ITALY: SEED ENHANCEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 377 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 378 ITALY: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 379 ITALY: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 380 ITALY: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 381 ITALY: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 382 ITALY: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 383 ITALY: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 384 ITALY: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 385 ITALY: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 386 ITALY: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 387 UK: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 388 UK: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 389 UK: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 390 UK: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 391 UK: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 392 UK: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 393 UK: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 394 UK: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 395 UK: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 396 UK: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 397 UK: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 398 UK: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 399 UK: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 400 UK: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 401 UK: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 402 UK: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 403 UK: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 404 UK: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 405 UK: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 406 UK: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 407 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 408 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 409 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 410 REST OF EUROPE: SEED PROTECTION MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 411 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 412 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 413 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 414 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 415 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 416 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 417 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 418 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 419 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 420 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 421 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 422 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 423 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 424 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 425 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 426 REST OF EUROPE: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 427 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 428 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 429 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 430 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 431 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 432 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 433 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 434 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 435 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY INSECTICIDE TYPE, 2020-2024 (USD MILLION)

- TABLE 436 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY INSECTICIDE TYPE, 2025-2030 (USD MILLION)

- TABLE 437 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY FUNGICIDE TYPE, 2020-2024 (USD MILLION)

- TABLE 438 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY FUNGICIDE TYPE, 2025-2030 (USD MILLION)

- TABLE 439 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY NEMATICIDE & OTHERS TYPE, 2020-2024 (USD MILLION)

- TABLE 440 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY NEMATICIDE & OTHERS TYPE, 2025-2030 (USD MILLION)

- TABLE 441 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 442 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 443 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOINSECTICIDE SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 444 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOINSECTICIDE SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 445 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFUNGICIDE SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 446 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFUNGICIDE SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 447 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIONEMATICIDES & OTHER SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 448 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIONEMATICIDES & OTHER SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 449 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 450 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 451 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL TYPE, 2020-2024 (USD MILLION)

- TABLE 452 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL TYPE, 2025-2030 (USD MILLION)

- TABLE 453 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFERTILIZER SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 454 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFERTILIZER SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 455 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOSTIMULANT SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 456 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOSTIMULANT SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 457 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY PLANT GROWTH REGULATOR SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 458 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY PLANT GROWTH REGULATOR SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 459 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 460 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 461 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 462 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 463 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 464 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 465 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 466 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 467 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 468 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 469 ASIA PACIFIC: SEED APPLIED TCHNOLOGIES MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 470 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 471 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED COATING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 472 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED COATING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 473 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DRESSING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 474 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DRESSING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 475 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PELLETING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 476 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PELLETING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 477 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PRIMING & CONDITIONING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 478 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PRIMING & CONDITIONING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 479 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DISINFECTION TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 480 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DISINFECTION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 481 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY PRECISION SEEDING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 482 ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY PRECISION SEEDING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 483 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 484 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 485 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 486 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 487 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 488 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 489 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 490 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 491 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 492 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 493 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 494 CHINA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 495 CHINA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 496 CHINA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 497 CHINA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 498 CHINA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 499 CHINA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 500 CHINA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 501 CHINA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 502 CHINA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 503 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 504 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 505 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 506 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 507 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 508 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 509 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 510 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 511 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 512 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 513 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 514 INDIA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 515 INDIA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 516 INDIA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 517 INDIA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 518 INDIA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 519 INDIA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 520 INDIA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 521 INDIA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 522 INDIA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 523 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 524 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 525 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 526 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 527 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 528 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 529 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 530 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 531 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 532 JAPAN: SEED ENHANCEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 533 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 534 JAPAN: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 535 JAPAN: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 536 JAPAN: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 537 JAPAN: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 538 JAPAN: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 539 JAPAN: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 540 JAPAN: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 541 JAPAN: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 542 JAPAN: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 543 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 544 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 545 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 546 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 547 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 548 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 549 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 550 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 551 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 552 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 553 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 554 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 555 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 556 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 557 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 558 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 559 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 560 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 561 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 562 AUSTRALIA & NEW ZEALAND: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 563 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 564 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 565 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 566 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 567 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 568 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 569 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 570 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 571 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 572 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 573 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 574 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 575 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 576 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 577 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 578 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 579 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 580 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 581 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 582 REST OF ASIA PACIFIC: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 583 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 584 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 585 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 586 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 587 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 588 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 589 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 590 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 591 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY INSECTICIDE TYPE, 2020-2024 (USD MILLION)

- TABLE 592 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY INSECTICIDE TYPE, 2025-2030 (USD MILLION)

- TABLE 593 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNGICIDE TYPE, 2020-2024 (USD MILLION)

- TABLE 594 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNGICIDE TYPE, 2025-2030 (USD MILLION)

- TABLE 595 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY NEMATICIDE & OTHERS TYPE, 2020-2024 (USD MILLION)

- TABLE 596 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY NEMATICIDE & OTHERS TYPE, 2025-2030 (USD MILLION)

- TABLE 597 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 598 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 599 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOINSECTICIDE SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 600 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOINSECTICIDE SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 601 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFUNGICIDE SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 602 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFUNGICIDE SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 603 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIONEMATICIDES & OTHER SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 604 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIONEMATICIDES & OTHER SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 605 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 606 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 607 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL TYPE, 2020-2024 (USD MILLION)

- TABLE 608 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL TYPE, 2025-2030 (USD MILLION)

- TABLE 609 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFERTILIZER SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 610 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOFERTILIZER SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 611 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOSTIMULANT SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 612 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY BIOSTIMULANT SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 613 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY PLANT GROWTH REGULATOR SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 614 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY PLANT GROWTH REGULATOR SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 615 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 616 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 617 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 618 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 619 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 620 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 621 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 622 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 623 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 624 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET IN OTHER CROP TYPES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 625 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 626 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 627 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED COATING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 628 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED COATING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 629 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DRESSING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 630 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DRESSING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 631 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PELLETING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 632 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PELLETING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 633 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PRIMING & CONDITIONING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 634 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PRIMING & CONDITIONING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 635 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DISINFECTION TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 636 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY SEED DISINFECTION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 637 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY PRECISION SEEDING TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 638 SOUTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY PRECISION SEEDING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 639 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2020-2024 (USD MILLION)

- TABLE 640 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION, 2025-2030 (USD MILLION)

- TABLE 641 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 642 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 643 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 644 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY CHEMICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 645 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2020-2024 (USD MILLION)

- TABLE 646 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY BIOLOGICAL SEED PROTECTION TYPE, 2025-2030 (USD MILLION)

- TABLE 647 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2020-2024 (USD MILLION)

- TABLE 648 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY SEED ENHANCEMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 649 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2020-2024 (USD MILLION)

- TABLE 650 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE, 2025-2030 (USD MILLION)

- TABLE 651 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS & PULSES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 652 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET IN OILSEEDS & PULSES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 653 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 654 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET IN CEREALS & GRAINS, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)

- TABLE 655 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2020-2024 (USD MILLION)

- TABLE 656 BRAZIL: SEED APPLIED TECHNOLOGIES MARKET IN FRUITS & VEGETABLES, BY CROP SUB-TYPE, 2025-2030 (USD MILLION)