|

|

市場調査レポート

商品コード

2034862

電気自動車向けワイヤレス充電の世界市場:充電システム別、充電タイプ別、用途別、コンポーネント別、電源供給範囲別、推進方式別、車両タイプ別、地域別 - 2032年までの予測Wireless Charging Market for Electric Vehicles by Charging System (Inductive, Capacitive, Magnetic Power Transfer), Propulsion, Charging Type (Stationary, Dynamic Wireless Charging), Component, Power Supply, and Vehicle Type - Global Forecast to 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 電気自動車向けワイヤレス充電の世界市場:充電システム別、充電タイプ別、用途別、コンポーネント別、電源供給範囲別、推進方式別、車両タイプ別、地域別 - 2032年までの予測 |

|

出版日: 2026年05月04日

発行: MarketsandMarkets

ページ情報: 英文 250 Pages

納期: 即納可能

|

概要

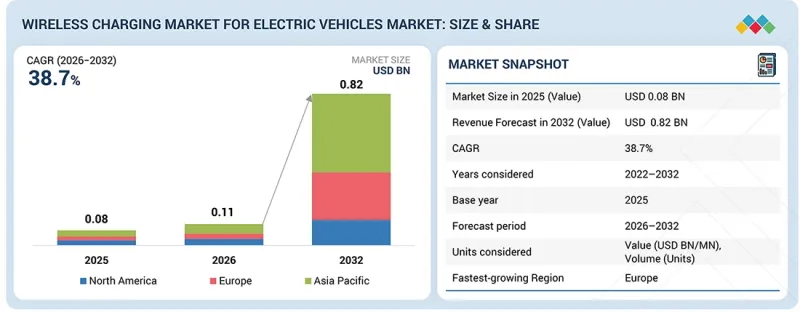

電気自動車向けワイヤレス充電の市場規模は、2026年の1億1,000万米ドルから2032年までに8億2,000万米ドルに達すると予測されており、CAGRは38.7%となる見込みです。

この成長は、EVの普及拡大と、充電の利便性向上への関心の高まりに支えられています。自動車メーカー各社は、技術プロバイダーとの提携を背景に、ワイヤレス充電を車両プラットフォームに組み込むことを検討しています。ワイヤレス充電は自動的なエネルギー転送を可能にし、ケーブルへの依存を減らし、特に都市部やフリート用途において利便性を向上させます。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2026年~2032年 |

| 基準年 | 2025年 |

| 予測期間 | 2026年~2032年 |

| 対象単位 | 10億米ドル |

| セグメント | 充電システム別、充電タイプ別、用途別、コンポーネント別、電源供給範囲別、推進方式別、車両タイプ別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州 |

誘導充電システム、位置合わせ、および標準化の進展により、システムの性能が向上し、初期段階での導入が促進されています。車両とインフラ間の統合が進むにつれ、利用頻度の高い使用事例において、ワイヤレス充電が徐々に普及していくと予想されます。

「充電システム別では、誘導電力伝送が最大のセグメントになると予想されます。」

誘導電力伝送は、EVのワイヤレス充電において最も広く採用されている方式です。これは電磁誘導の原理に基づいており、地上の送信パッドと車両に搭載された受信パッドの間で電力が伝送されます。誘導式システムは、SAE J2954などの標準化の取り組みに支えられ、住宅、職場、公共の充電環境の各所で導入が進んでいます。現代自動車、ボルボ・グループ、BMW、トヨタなどの自動車メーカーや、アプティブ(Aptiv)やマーレ(Mahle)といったティア1サプライヤーは、誘導充電を車両プラットフォームに統合する取り組みを進めています。例えば、2026年3月、Electreon(Electreon)は、公共交通機関やフリート用途向けに、米国ミシガン州での誘導充電の展開を拡大しました。それ以前の2025年6月には、ENRXがボルボ・グループと提携し、電気バスやトラック向けの誘導充電を展開し、機会充電をサポートしました。誘導電力伝送の主な利点には、安定した電力伝送、統合の容易さ、およびシステムの複雑さの低減が含まれます。誘導電力伝送の効率は通常90~95%の範囲にあり、エネルギー損失の低減と安定した充電性能を実現します。これらの要因が誘導電力伝送の普及を後押しし、市場における主要技術としての地位を確立しています。

「充電方式別では、固定式ワイヤレス充電が最大のセグメントになると予想されています。」

固定式ワイヤレス充電は、住宅、職場、公共の駐車場環境における自動充電の実用的なソリューションとして注目を集めています。誘導電力伝送に基づくこのシステムは、地面に設置された充電パッドと車両に搭載された受信機との間でエネルギーを伝送します。これにより、駐車中に手動操作なしで充電が可能となり、利便性が向上し、プラグインシステムへの依存度が低減されます。この技術は、一定期間車両が静止した状態にある乗用車やフリート用途に最適です。この技術は安定した充電をサポートし、ユーザー体験を向上させ、物理的なコネクタに伴う摩耗や損傷を軽減します。自動車メーカー(OEM)やワイヤレス充電プロバイダーは、これらのシステムを車両プラットフォームや駐車インフラに統合することに注力しています。2026年3月、WiTricityはシーメンスと協力し、スケーラブルなインフラ統合に焦点を当て、住宅用およびフリート用駐車アプリケーションにおける固定式ワイヤレス充電ソリューションの展開を推進しました。システムの効率性と標準化が進むにつれ、固定式ワイヤレス充電は主要な使用事例においてより広く採用されることが期待されています。

「予測期間中、欧州が最も急速に成長する市場になると予想されています。」

欧州の自動車業界では、欧州連合(EU)が定めた厳格な排出ガス規制と明確な脱炭素化目標に支えられ、ゼロエミッションモビリティへの強力な移行が進んでいます。欧州各国は、インセンティブ、インフラ投資、政策支援を通じてEVの普及を積極的に推進しており、ワイヤレス充電技術にとって好ましい環境を作り出しています。ワイヤレス充電への需要は、プレミアムEVの台頭や、ユーザーの利便性および先進的な車両機能への注目が高まっていることも後押ししています。OEMや技術プロバイダーは、地域標準や相互運用性の要件に準拠しつつ、ワイヤレス充電を次世代車両プラットフォームに統合するために協力しています。この地域の主要企業には、ドイツのIPT Technology GmbHやRobert Bosch GmbH、欧州の複数の市場で事業を展開するElectreon、そしてノルウェーのENRXなどが挙げられます。2025年4月、Electreon社はドイツにおけるワイヤレス充電道路プロジェクトを拡大し、公共交通機関向け誘導充電インフラの展開を支援しました。これらのソリューションは、特に公共交通機関やフリート用途において、パイロットプロジェクトや初期の商用プロジェクトを通じて導入が進められています。スマートシティやコネクテッドインフラへの投資が増加する中、欧州はEV向けワイヤレス充電の普及を推進する上で中心的な役割を果たすと予想されます。

電気自動車向けワイヤレス充電市場は、Electreon(イスラエル)、Witricity(米国)、ENRX(ノルウェー)、HEVO Inc.(米国)、Plugless Power Inc.(米国)といった老舗企業が主導しています。これらの企業は、工場出荷時統合型システムから高出力のフリート向けインフラに至るまで、ワイヤレス充電ソリューションを開発・供給しています。

調査範囲:

本調査では、電気自動車向けワイヤレス充電市場を、充電システム(誘導電力伝送、磁気電力伝送、導電電力伝送)、推進方式(BEV、PHEV)、充電タイプ(定置型ワイヤレス充電、動的ワイヤレス充電)、構成部品(ベース充電パッド、電力制御ユニット、車両用充電パッド)、電力供給(<3.7 kW, 3.8-7.7 kW, 7.8-11 kW,>11 kW)、および車種(乗用車、商用車)別に分析しています。また、ワイヤレス充電エコシステムにおける主要企業の競合情勢や企業プロファイルについても網羅しています。

当レポートの主なメリット:

当レポートは、市場リーダーおよび新規参入企業に対し、電気自動車向けワイヤレス充電市場全体およびそのサブセグメントにおける売上高の最も正確な推計値を提供します。これにより、利害関係者は競合情勢を理解し、自社のビジネスをより効果的に位置づけ、適切な市場参入戦略を策定するための洞察を得ることができます。また、当レポートは利害関係者が市場の動向を把握するのを支援し、主要な市場促進要因、制約、課題、および機会に関する情報を提供します。

当レポートでは、以下の点について洞察を提供します:

- 主要な促進要因(ワイヤレス充電エコシステムへのOEMの参入拡大、自動・スマート駐車システムとのワイヤレス充電の統合、排出ガスゼロかつ持続可能な電気モビリティに対する政府の強力な支援)、制約要因(車載ワイヤレス充電システムの統合に伴う高コストと複雑さ、従来の有線充電ソリューションと比較したエネルギー伝送効率の低さ)、機会(スマートシティインフラにおけるワイヤレス充電の採用拡大、ダイナミックワイヤレス充電技術への投資増加、利用頻度の高い電気自動車フリート運用におけるシームレスな充電の可能性)、および市場の成長に影響を与える課題(標準化された車両統合フレームワークの欠如、公共ワイヤレス充電インフラの設置・導入コストの高さ)

- 製品開発/イノベーション:市場における今後の技術、研究開発活動、新製品の発売に関する詳細な洞察

- 市場開発:収益性の高い市場に関する包括的な情報―当レポートでは、様々な地域にわたる市場を分析しています

- 市場の多様化:市場における新製品、未開拓地域、最近の動向、および投資に関する網羅的な情報

- 競合分析:Electreon(イスラエル)、Witricity(米国)、ENRX(ノルウェー)、HEVO Inc.(米国)、Plugless Power Inc.(米国)などの主要企業の市場シェア、成長戦略、サービス提供内容に関する詳細な評価

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 価格分析

- エコシステム分析

- バリューチェーン分析

- 事例研究分析

- 投資と資金調達のシナリオ

- 特許分析

- 技術分析

- 市場構造と競争上の優先事項

- ワイヤレスEV充電インフラと統合における依存関係

- 投資および設備投資分析

- 規制概要

- 2026年~2027年の主な会議およびイベント

- 世界の電気自動車動向

- 主要な利害関係者と購入基準

- 顧客ビジネスに影響を与える動向/混乱

- OEM分析

第5章 電気自動車向けワイヤレス充電市場(充電システム別)

- 磁気動力伝達

- 誘導電力伝送

- 容量性電力伝送

- 主要な洞察

第6章 電気自動車向けワイヤレス充電市場(充電方式別)

- 据え置き型ワイヤレス充電

- ダイナミックワイヤレス充電

- 主要な洞察

第7章 電気自動車向けワイヤレス充電市場(用途別)

- 家庭用充電ユニット

- 商用充電ステーション

- 主要な洞察

第8章 電気自動車向けワイヤレス充電市場(コンポーネント別)

- ベース充電パッド

- 電源制御ユニット

- 車両用充電パッド

- 主要な洞察

第9章 電気自動車向けワイヤレス充電市場(電源供給範囲別)

- 3.7kW未満

- 3.7~7.7kW

- 7.8~11kW

- 11kW以上

- 主要な洞察

第10章 電気自動車向けワイヤレス充電市場(推進方式別)

- BEV

- PHEV

- 主要な洞察

第11章 電気自動車向けワイヤレス充電市場(車両タイプ別)

- 乗用車

- 商用車

- 主要な洞察

第12章 電気自動車向けワイヤレス充電市場(地域別)

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- 欧州

- フランス

- ドイツ

- オランダ

- ノルウェー

- スペイン

- スウェーデン

- スイス

- 英国

- 北米

- カナダ

- 米国

第13章 競合情勢

- 主要参入企業の戦略/強み、2022年~2025年

- 市場シェア分析、2025年

- 収益分析、2021年~2025年

- 企業評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要企業、2026年

- 企業評価マトリックス:スタートアップ/中小企業、2026年

- 競合シナリオ

第14章 企業プロファイル

- 主要参入企業

- ELECTREON

- WITRICITY AI TECH, LLC

- ENRX

- HEVO INC.

- PLUGLESS POWER INC.

- MITSUBISHI ELECTRIC CORPORATION

- TGOOD ELECTRIC CO., LTD.

- TOYOTA MOTOR CORPORATION

- ROBERT BOSCH GMBH

- CONTINENTAL AG

- TOSHIBA CORPORATION

- HELLA GMBH & CO. KGAA

- その他の企業

- IDEANOMICS INC.

- VOLTERIO GMBH

- MOJO MOBILITY INC.

- BMW

- FORTUM CORPORATION

- HYUNDAI MOTOR COMPANY

- PULS GMBH

- DAIHEN CORPORATION

- VIE GROUP CO., LTD.

- IPT TECHNOLOGY GMBH

- EASELINK GMBH

- MAHLE GMBH

- NISSAN MOTOR CO., LTD.