|

|

市場調査レポート

商品コード

1773185

ヘルスケアディスペンシングシステムの世界市場:タイプ別、材料別、用途別、エンドユーザー別、地域別 - 2030年までの予測Healthcare Dispensing Systems Market by Type (Automatic, Manual, Dispensing Component, Control System), Material (Reagent, Antibody, Powder), Application (Drug Delivery, Microfluidics), End User (Hospital, Pharmacy) & Region - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ヘルスケアディスペンシングシステムの世界市場:タイプ別、材料別、用途別、エンドユーザー別、地域別 - 2030年までの予測 |

|

出版日: 2025年07月18日

発行: MarketsandMarkets

ページ情報: 英文 406 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

ヘルスケアディスペンシングシステムの市場規模は、予測期間中に6.3%のCAGRで拡大し、2025年の46億1,000万米ドルから2030年には62億7,000万米ドルに達すると予測されています。

ライフサイエンスや臨床における精度、自動化、効率化の要求の高まりは、製薬会社やバイオテクノロジー会社をハイスループットスクリーニングや個別化医療へとシフトさせる原動力となっています。その結果、正確で汚染のないリキッドハンドリングシステムに対するニーズが高まっています。高度な分注システム、高コスト、他のラボシステムとの統合問題に対する懸念は、予測期間中、ヘルスケア分注システム市場の成長をある程度妨げる可能性があります。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2024年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2024年~2030年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント | タイプ別、材料別、用途別、エンドユーザー別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、中東・アフリカ、ラテンアメリカ |

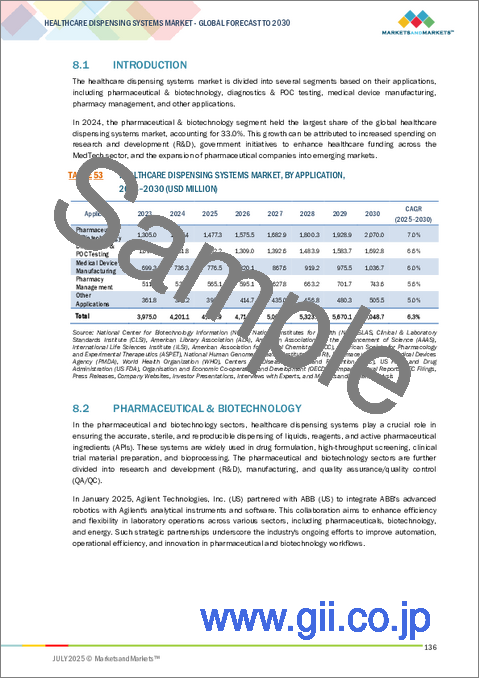

用途別では、ヘルスケアディスペンシングシステム市場は、製薬・バイオテクノロジー、診断・ポイントオブケア検査管理、医療機器製造、薬局管理、その他に区分されます。このうち、診断・ポイントオブケア検査管理は、迅速かつ分散化された検査に対する需要の高まりと、疾病の早期発見に対する世界の関心の高まりによって、最も急速に成長している分野です。このセグメントには、ラテラルフローアッセイ(LFA)、PCRおよびNAAT検査、ELISA、マイクロアレイ、マイクロ流体デバイスなどが含まれ、それぞれ試薬とサンプルの正確で反復可能な分注を必要とします。分子診断の拡大、感染症サーベイランスの増加、コンパクトでハイスループットな検査プラットフォームの利用可能性の拡大が成長の原動力となっています。一貫性のある診断結果を出すための精度、スピード、自動化の必要性から、ばらつきを抑え、トレーサビリティを確保し、検査キットの大量生産をサポートする自動分注システムが広く採用されています。

材料別では、ヘルスケア分注システム市場は液体、粉末、顆粒、凍結乾燥材料、その他に区分されます。このうち、液体分野は診断、製薬、研究用途で重要な役割を果たすため、予測期間中に最も速い速度で成長すると予測されています。液体分注システムは、ハイスループット環境において試薬、緩衝液、生物学的サンプル、薬剤製剤を正確に取り扱うために不可欠です。その精度、スピード、自動化システムとの互換性は、臨床診断(ELISA、PCRなど)、医薬品研究開発、ポイントオブケア検査ワークフローにおいて不可欠なものとなっています。検査量の拡大、生物製剤の製造、個別化医療を背景とした自動リキッドハンドリングに対する需要の高まりが、採用を大幅に後押ししています。さらに、非接触およびチップレス分注技術の進歩により、より高い精度と汚染の最小化が可能になり、厳格な品質管理を必要とするアプリケーションをサポートしています。自動化、デジタル化、スループット最適化がヘルスケアとラボのオペレーションを再構築し続ける中、液体分注システムは、多様なエンドユーザー・セグメントにおいて、拡張性があり、効率的で、コンプライアンスに準拠した液体ハンドリング・ソリューションを提供する、傑出した技術として台頭しています。

世界のヘルスケアディスペンシングシステム市場は5つの主要地域(北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカ)に区分されます。2024年には、アジア太平洋が予測期間中にヘルスケアディスペンシングシステムで最も速い成長を記録すると予想されています。この急成長の主な要因は、中国、インド、韓国、シンガポールなどの国々における政府資金の増加、医薬品・診断薬製造の継続的拡大、自動化技術の採用などです。さらに、有利な製造政策、医療技術・バイオテクノロジー部門への外国直接投資の増加、臨床研究活動の活発化により、ハイスループット自動分注ソリューションに対する強い需要が生まれています。医療へのアクセス性と効率性の向上への注力と相まって、これらの要因はアジア太平洋におけるヘルスケアディスペンシングシステム市場の成長を大きく促進すると予想されます。

当レポートでは、世界のヘルスケアディスペンシングシステム市場について調査し、タイプ別、材料別、用途別、エンドユーザー別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 顧客のビジネスに影響を与える動向/混乱

- 業界動向

- エコシステム分析

- バリューチェーン分析

- 技術分析

- 規制分析

- 価格分析

- ポーターのファイブフォース分析

- 特許分析

- 主要な利害関係者と購入基準

- エンドユーザー分析

- 2025年~2026年の主な会議とイベント

- ケーススタディ分析

- 貿易分析

- 投資と資金調達のシナリオ

- 2025年の米国関税がヘルスケアディスペンシングシステム市場に与える影響

第6章 ヘルスケアディスペンシングシステム市場(タイプ別)

- イントロダクション

- 自動ディスペンシングシステム

- 半自動ディスペンシングシステム

- スタンドアロン/手動ディスペンシングシステム

- OEM/ディスペンシングコンポーネント

第7章 ヘルスケアディスペンシングシステム市場(材料別)

- イントロダクション

- 液体

- 粉末、顆粒、凍結乾燥物

- その他

第8章 ヘルスケアディスペンシングシステム市場(用途別)

- イントロダクション

- 医薬品・バイオテクノロジー

- 診断・POC検査

- 医療機器製造

- 薬局経営

- その他

第9章 ヘルスケアディスペンシングシステム市場(エンドユーザー別)

- イントロダクション

- ヘルスケア提供者

- 製薬・バイオテクノロジー企業

- 医療技術企業

- その他

第10章 ヘルスケアディスペンシングシステム市場(地域別)

- イントロダクション

- 北米

- 北米のマクロ経済見通し

- 米国

- カナダ

- 欧州

- 欧州のマクロ経済見通し

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他

- アジア太平洋

- アジア太平洋のマクロ経済見通し

- 中国

- 日本

- インド

- その他

- ラテンアメリカ

- ラテンアメリカのマクロ経済見通し

- ブラジル

- メキシコ

- その他

- 中東・アフリカ

- 中東・アフリカのマクロ経済見通し

- GCC諸国

- その他

第11章 競合情勢

- 概要

- 主要参入企業の戦略/強み

- 収益分析、2020年~2024年

- 市場シェア分析、2024年

- 主要市場プレーヤーのランキング

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業、2024年

- 企業評価と財務指標

- ブランド/製品比較

- 競合シナリオ

第12章 企業プロファイル

- 主要参入企業

- NORDSON CORPORATION

- AGILENT TECHNOLOGIES, INC.

- DANAHER CORPORATION

- THERMO FISHER SCIENTIFIC INC.

- BIODOT

- FISNAR

- PARKER-HANNIFIN CORPORATION

- BDTRONIC

- HAMILTON COMPANY

- GRACO INC.

- REVVITY, INC.

- HARRO HOFLIGER VERPACKUNGSMASCHINEN GMBH

- TECAN TRADING AG

- IVEK CORPORATION

- IMAGENE TECHNOLOGY INC.

- QIAGEN

- BRAND GMBH+CO KG

- ASCENTIAL TECHNOLOGIES

- LGC BIOSEARCH TECHNOLOGIES

- GILSON INCORPORATED

- その他の企業

- CLAREMONT BIOSOLUTIONS, LLC

- GUANGZHOU ASCEND PRECISION MACHINERY CO., LTD.

- RADETEC PTY LTD.

- BAODING CHUANGRUI PRECISION PUMP CO., LTD.

- ELVEFLOW

第13章 付録

List of Tables

- TABLE 1 EXCHANGE RATES UTILIZED FOR CONVERSION TO USD

- TABLE 2 HEALTHCARE DISPENSING SYSTEMS MARKET: FACTOR ANALYSIS

- TABLE 3 HEALTHCARE DISPENSING SYSTEMS MARKET: RISK ASSESSMENT

- TABLE 4 HEALTHCARE DISPENSING SYSTEMS MARKET: MARKET DYNAMICS

- TABLE 5 HEALTHCARE DISPENSING SYSTEMS MARKET: ROLE IN ECOSYSTEM

- TABLE 6 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 REGULATORY SCENARIO OF NORTH AMERICA

- TABLE 12 REGULATORY SCENARIO OF EUROPE

- TABLE 13 REGULATORY SCENARIO OF ASIA PACIFIC

- TABLE 14 REGULATORY SCENARIO OF MIDDLE EAST & AFRICA

- TABLE 15 REGULATORY SCENARIO OF LATIN AMERICA

- TABLE 16 INDICATIVE PRICING FOR HEALTHCARE DISPENSING SYSTEMS MARKET, BY PRODUCT (2024)

- TABLE 17 INDICATIVE PRICING OF HEALTHCARE DISPENSING SYSTEMS, BY REGION, 2024

- TABLE 18 HEALTHCARE DISPENSING SYSTEMS MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 19 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR PRODUCTS, BY END USER (%)

- TABLE 20 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR HEALTHCARE DISPENSING SYSTEMS FOR KEY END USERS

- TABLE 21 UNMET NEEDS IN HEALTHCARE DISPENSING SYSTEMS MARKET

- TABLE 22 END-USER EXPECTATIONS IN HEALTHCARE DISPENSING SYSTEMS MARKET

- TABLE 23 LIST OF KEY CONFERENCES & EVENTS IN HEALTHCARE DISPENSING SYSTEMS MARKET, JANUARY 2025-DECEMBER 2026

- TABLE 24 CASE STUDY 1: AUTOMATING BIOREACTOR WORKFLOWS WITH CELLEXUS & WATSON-MARLOW PUMPS

- TABLE 25 CASE STUDY 2: REDUCING MEDICATION RE-DISPENSES THROUGH BARCODE-ENABLED DISPENSING SYSTEM INTEGRATION AT A U.S. HEALTH SYSTEM

- TABLE 26 CASE STUDY 3: SCALING PRESCRIPTION FULFILLMENT WITH AN AUTOMATED DISPENSING SYSTEM FOR HIGH-VOLUME PHARMACY OPERATIONS

- TABLE 27 IMPORT SCENARIO FOR PUMPS FOR LIQUIDS, WHETHER OR NOT FITTED WITH A MEASURING DEVICE [EXCL. (HS CODE 8413)], BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 28 EXPORT SCENARIO FOR PUMPS FOR LIQUIDS, WHETHER OR NOT FITTED WITH A MEASURING DEVICE [EXCL. (HS CODE 8413)], BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 29 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 30 HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 31 HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (THOUSAND UNITS)

- TABLE 32 AUTOMATIC DISPENSING SYSTEMS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 33 SEMI-AUTOMATIC DISPENSING SYSTEMS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 34 STANDALONE/MANUAL DISPENSING SYSTEMS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 35 OEM/DISPENSING COMPONENTS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 36 OEM/DISPENSING COMPONENTS MARKET FOR PUMPS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 37 OEM/DISPENSING COMPONENTS MARKET FOR VALVES & NOZZLES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 38 OEM/DISPENSING COMPONENTS MARKET FOR CONTROL SYSTEMS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 39 OTHER OEM/DISPENSING COMPONENTS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 40 HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 41 HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 42 HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 43 HEALTHCARE DISPENSING SYSTEMS MARKET FOR REAGENTS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 44 HEALTHCARE DISPENSING SYSTEMS MARKET FOR BUFFERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 45 HEALTHCARE DISPENSING SYSTEMS MARKET FOR ANTIBODIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 46 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OTHER LIQUIDS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 47 HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 48 HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 49 HEALTHCARE DISPENSING SYSTEMS MARKET FOR CAKES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 50 HEALTHCARE DISPENSING SYSTEMS MARKET FOR LYOBEADS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 51 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OTHER POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 52 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OTHER MATERIALS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 53 HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 54 HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 55 HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 56 HEALTHCARE DISPENSING SYSTEMS MARKET FOR R&D APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 57 HEALTHCARE DISPENSING SYSTEMS MARKET FOR MANUFACTURING & QA/QC APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 58 HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY REGION, 2022-2030 (USD MILLION)

- TABLE 59 HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 60 HEALTHCARE DISPENSING SYSTEMS MARKET FOR LATERAL FLOW ASSAYS & RAPID TESTS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 61 HEALTHCARE DISPENSING SYSTEMS MARKET FOR PCR & NUCLEIC ACID TESTS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 62 HEALTHCARE DISPENSING SYSTEMS MARKET FOR IMMUNOASSAYS & ELISA TESTS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 63 HEALTHCARE DISPENSING SYSTEMS MARKET FOR MICROARRAYS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 64 HEALTHCARE DISPENSING SYSTEMS MARKET FOR IMMUNOBLOTS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 65 HEALTHCARE DISPENSING SYSTEMS MARKET FOR MICROFLUIDICS & LAB-ON-A-CHIP TESTS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 66 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OTHER DIAGNOSTICS & POC TESTING APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 67 HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 68 HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 69 HEALTHCARE DISPENSING SYSTEMS MARKET FOR DRUG DELIVERY DEVICES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 70 HEALTHCARE DISPENSING SYSTEMS MARKET FOR IMPLANTABLE MEDICAL DEVICES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 71 HEALTHCARE DISPENSING SYSTEMS MARKET FOR SURGICAL INSTRUMENTS & WOUND CARE DEVICES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 72 HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTIC TEST KIT MANUFACTURING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 73 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OTHER MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 74 HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACY MANAGEMENT APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 75 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OTHER APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 76 HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 77 HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 78 HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 79 HEALTHCARE DISPENSING SYSTEMS MARKET FOR HOSPITALS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 80 HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTIC LABS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 81 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OUTPATIENT SETTINGS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 82 HEALTHCARE DISPENSING SYSTEMS MARKET FOR HOME HEALTHCARE, LONG-TERM CARE, AND ASSISTED LIVING FACILITIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 83 HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 84 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OTHER HEALTHCARE PROVIDERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 85 HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 86 HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDTECH COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 87 HEALTHCARE DISPENSING SYSTEMS MARKET FOR OTHER END USERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 88 HEALTHCARE DISPENSING SYSTEMS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 89 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 90 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 91 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 92 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 93 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 94 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 95 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 96 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 97 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 98 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 99 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 100 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 101 US: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 102 US: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 103 US: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 104 US: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 105 US: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 106 US: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 107 US: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 108 US: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 109 US: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 110 US: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 111 US: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 112 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 113 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 114 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 115 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 116 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 117 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 118 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 119 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 120 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 121 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 122 CANADA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 123 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 124 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 125 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 126 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 127 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 128 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 129 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 130 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 131 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 132 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 133 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 134 EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 135 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 136 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 137 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 138 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 139 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 140 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 141 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 142 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 143 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 144 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 145 GERMANY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 146 UK: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 147 UK: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 148 UK: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 149 UK: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 150 UK: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 151 UK: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 152 UK: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 153 UK: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 154 UK: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 155 UK: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 156 UK: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 157 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 158 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 159 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 160 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 161 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 162 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 163 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 164 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 165 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 166 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 167 FRANCE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 168 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 169 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 170 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 171 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 172 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 173 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 174 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 175 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 176 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 177 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 178 ITALY: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 179 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 180 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 181 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 182 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 183 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 184 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 185 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 186 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 187 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 188 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 189 SPAIN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 190 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 191 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 192 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 193 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 194 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 195 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 196 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 197 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 198 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 199 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 200 REST OF EUROPE: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 201 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 202 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 203 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 204 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 205 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 206 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 207 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 208 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 209 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 210 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 211 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 212 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 213 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 214 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 215 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 216 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 217 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 218 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 219 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 220 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 221 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 222 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 223 CHINA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 224 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 225 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 226 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 227 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 228 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 229 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 230 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 231 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 232 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 233 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 234 JAPAN: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 235 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 236 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 237 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 238 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 239 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 240 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 241 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 242 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 243 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 244 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 245 INDIA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 246 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 247 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 248 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 249 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 250 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 251 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 252 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 253 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 254 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 255 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 256 REST OF ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 257 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 258 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 259 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 260 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 261 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 262 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 263 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 264 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 265 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 266 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 267 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 268 LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 269 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 270 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 271 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 272 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 273 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 274 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 275 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 276 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 277 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 278 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 279 BRAZIL: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 280 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 281 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 282 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 283 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 284 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 285 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 286 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 287 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 288 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 289 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 290 MEXICO: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 291 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 292 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 293 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 294 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 295 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 296 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 297 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 298 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 299 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 300 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 301 REST OF LATIN AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 302 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 303 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 304 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 305 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 306 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 307 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 308 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 309 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 310 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 311 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 312 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 313 MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 314 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 315 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 316 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 317 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 318 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 319 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 320 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 321 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 322 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 323 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 324 GCC COUNTRIES: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 325 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 326 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR OEM/DISPENSING COMPONENTS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 327 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2023-2030 (USD MILLION)

- TABLE 328 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR LIQUIDS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 329 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR POWDERS, GRANULES, AND LYOPHILIZED MATERIALS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 330 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 331 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 332 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR DIAGNOSTICS & POC TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 333 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR MEDICAL DEVICE MANUFACTURING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 334 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 335 REST OF MIDDLE EAST & AFRICA: HEALTHCARE DISPENSING SYSTEMS MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 336 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN HEALTHCARE DISPENSING SYSTEMS MARKET, JANUARY 2022-JUNE 2025

- TABLE 337 HEALTHCARE DISPENSING SYSTEMS MARKET: DEGREE OF COMPETITION

- TABLE 338 HEALTHCARE DISPENSING SYSTEMS MARKET: REGION FOOTPRINT

- TABLE 339 HEALTHCARE DISPENSING SYSTEMS MARKET: TYPE FOOTPRINT

- TABLE 340 HEALTHCARE DISPENSING SYSTEMS MARKET: MATERIAL FOOTPRINT

- TABLE 341 HEALTHCARE DISPENSING SYSTEMS MARKET: APPLICATION FOOTPRINT

- TABLE 342 HEALTHCARE DISPENSING SYSTEMS MARKET: END-USER FOOTPRINT

- TABLE 343 HEALTHCARE DISPENSING SYSTEMS MARKET: DETAILED LIST OF KEY STARTUP/SME PLAYERS

- TABLE 344 HEALTHCARE DISPENSING SYSTEMS MARKET: COMPETITIVE BENCHMARKING OF KEY EMERGING PLAYERS/STARTUPS, BY REGION

- TABLE 345 HEALTHCARE DISPENSING SYSTEMS MARKET: COMPETITIVE BENCHMARKING OF KEY EMERGING PLAYERS/STARTUPS, BY TYPE

- TABLE 346 HEALTHCARE DISPENSING SYSTEMS MARKET: PRODUCT LAUNCHES, JANUARY 2022-JULY 2025

- TABLE 347 HEALTHCARE DISPENSING SYSTEMS MARKET: DEALS, JANUARY 2022-JULY 2025

- TABLE 348 HEALTHCARE DISPENSING SYSTEMS MARKET: EXPANSIONS, JANUARY 2022-MAY 2025

- TABLE 349 NORDSON CORPORATION: COMPANY OVERVIEW

- TABLE 350 NORDSON CORPORATION: PRODUCTS OFFERED

- TABLE 351 NORDSON CORPORATION: PRODUCT LAUNCHES, JANUARY 2022-MAY 2025

- TABLE 352 NORDSON CORPORATION: DEALS, JANUARY 2022-MAY 2025

- TABLE 353 NORDSON CORPORATION: EXPANSIONS, JANUARY 2022-MAY 2025

- TABLE 354 AGILENT TECHNOLOGIES, INC.: COMPANY OVERVIEW

- TABLE 355 AGILENT TECHNOLOGIES, INC.: PRODUCTS OFFERED

- TABLE 356 AGILENT TECHNOLOGIES, INC.: PRODUCT LAUNCHES, JANUARY 2022-MAY 2025

- TABLE 357 AGILENT TECHNOLOGIES, INC.: DEALS, JANUARY 2022-MAY 2025

- TABLE 358 DANAHER CORPORATION: COMPANY OVERVIEW

- TABLE 359 DANAHER CORPORATION: PRODUCTS OFFERED

- TABLE 360 DANAHER CORPORATION: DEALS, JANUARY 2022-MAY 2025

- TABLE 361 THERMO FISHER SCIENTIFIC INC.: COMPANY OVERVIEW

- TABLE 362 THERMO FISHER SCIENTIFIC INC.: PRODUCTS OFFERED

- TABLE 363 THERMO FISHER SCIENTIFIC INC.: EXPANSIONS, JANUARY 2022-MAY 2025

- TABLE 364 BIODOT: COMPANY OVERVIEW

- TABLE 365 BIODOT: PRODUCTS OFFERED

- TABLE 366 BIODOT: PRODUCT LAUNCHES, JANUARY 2022- MAY 2025

- TABLE 367 BIODOT: DEALS, JANUARY 2022- MAY 2025

- TABLE 368 FISNAR: COMPANY OVERVIEW

- TABLE 369 FISNAR: PRODUCTS OFFERED

- TABLE 370 PARKER-HANNIFIN CORPORATION: COMPANY OVERVIEW

- TABLE 371 PARKER-HANNIFIN CORPORATION: PRODUCTS OFFERED

- TABLE 372 BDTRONIC: COMPANY OVERVIEW

- TABLE 373 BDTRONIC: PRODUCTS OFFERED

- TABLE 374 HAMILTON COMPANY: COMPANY OVERVIEW

- TABLE 375 HAMILTON COMPANY: PRODUCTS OFFERED

- TABLE 376 HAMILTON COMPANY: PRODUCT LAUNCHES, JANUARY 2022-MAY 2025

- TABLE 377 HAMILTON COMPANY: DEALS, JANUARY 2022-MAY 2025

- TABLE 378 GRACO INC.: COMPANY OVERVIEW

- TABLE 379 GRACO INC.: PRODUCTS OFFERED

- TABLE 380 GRACO INC.: PRODUCT LAUNCHES, JANUARY 2022-MAY 2025

- TABLE 381 REVVITY, INC.: COMPANY OVERVIEW

- TABLE 382 REVVITY, INC.: PRODUCTS OFFERED

- TABLE 383 HARRO HOFLIGER VERPACKUNGSMASCHINEN GMBH: COMPANY OVERVIEW

- TABLE 384 HARRO HOFLIGER VERPACKUNGSMASCHINEN GMBH: PRODUCTS OFFERED

- TABLE 385 HARRO HOFLIGER VERPACKUNGSMASCHINEN GMBH: DEALS, JANUARY 2022-MAY 2025

- TABLE 386 TECAN TRADING AG: COMPANY OVERVIEW

- TABLE 387 TECAN TRADING AG: PRODUCTS OFFERED

- TABLE 388 IVEK CORPORATION: COMPANY OVERVIEW

- TABLE 389 IVEK CORPORATION: PRODUCTS OFFERED

- TABLE 390 IMAGENE TECHNOLOGY INC.: COMPANY OVERVIEW

- TABLE 391 IMAGENE TECHNOLOGY INC.: PRODUCTS OFFERED

- TABLE 392 QIAGEN: COMPANY OVERVIEW

- TABLE 393 QIAGEN: PRODUCTS OFFERED

- TABLE 394 BRAND GMBH + CO KG: COMPANY OVERVIEW

- TABLE 395 BRAND GMBH + CO KG: PRODUCTS OFFERED

- TABLE 396 ASCENTIAL TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 397 ASCENTIAL TECHNOLOGIES: PRODUCTS OFFERED

- TABLE 398 ASCENTIAL TECHNOLOGIES: EXPANSIONS, JANUARY 2022-MAY 2025

- TABLE 399 ASCENTIAL TECHNOLOGIES: OTHER DEVELOPMENTS, JANUARY 2022-MAY 2025

- TABLE 400 LGC BIOSEARCH TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 401 LGC BIOSEARCH TECHNOLOGIES: PRODUCTS OFFERED

- TABLE 402 LGC BIOSEARCH TECHNOLOGIES: DEALS, JANUARY 2022-MAY 2025

- TABLE 403 GILSON INCORPORATED: COMPANY OVERVIEW

- TABLE 404 GILSON INCORPORATED: PRODUCTS OFFERED

- TABLE 405 CLAREMONT BIOSOLUTIONS, LLC: COMPANY OVERVIEW

- TABLE 406 GUANGZHOU ASCEND PRECISION MACHINERY CO., LTD.: COMPANY OVERVIEW

- TABLE 407 RADETEC PTY LTD.: COMPANY OVERVIEW

- TABLE 408 BAODING CHUANGRUI PRECISION PUMP CO., LTD.: COMPANY OVERVIEW

- TABLE 409 ELVEFLOW: COMPANY OVERVIEW

List of Figures

- FIGURE 1 HEALTHCARE DISPENSING SYSTEMS MARKET SEGMENTATION & REGIONAL SCOPE

- FIGURE 2 RESEARCH DESIGN

- FIGURE 3 PRIMARY SOURCES

- FIGURE 4 INSIGHTS FROM INDUSTRY EXPERTS

- FIGURE 5 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 6 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 7 HEALTHCARE DISPENSING SYSTEMS MARKET: SUPPLY-SIDE MARKET ESTIMATION

- FIGURE 8 HEALTHCARE DISPENSING SYSTEMS MARKET: REVENUE ESTIMATION APPROACH

- FIGURE 9 BOTTOM-UP APPROACH: END-USER SPENDING ON HEALTHCARE DISPENSING SYSTEMS

- FIGURE 10 CAGR PROJECTIONS FROM ANALYSIS OF DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES (2025-2030)

- FIGURE 11 HEALTHCARE DISPENSING SYSTEMS MARKET: CAGR PROJECTIONS

- FIGURE 12 TOP-DOWN APPROACH

- FIGURE 13 DATA TRIANGULATION METHODOLOGY

- FIGURE 14 HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE, 2025 VS. 2030 (USD MILLION)

- FIGURE 15 HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL, 2025 VS. 2030 (USD MILLION)

- FIGURE 16 HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION, 2025 VS. 2030 (USD MILLION)

- FIGURE 17 HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER, 2025 VS. 2030 (USD MILLION)

- FIGURE 18 HEALTHCARE DISPENSING SYSTEMS MARKET: GEOGRAPHICAL SNAPSHOT

- FIGURE 19 GROWING FOCUS ON AUTOMATION DISPENSING AND FAVORABLE GOVERNMENT SUPPORT AND FUNDING TO DRIVE MARKET

- FIGURE 20 NORTH AMERICA TO DOMINATE HEALTHCARE DISPENSING SYSTEMS MARKET DURING FORECAST PERIOD

- FIGURE 21 PHARMACEUTICAL COMPANIES IN NORTH AMERICA ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 22 CHINA TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 23 EMERGING ECONOMIES TO REGISTER HIGHER GROWTH RATES DURING FORECAST PERIOD

- FIGURE 24 HEALTHCARE DISPENSING SERVICES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 25 HEALTHCARE DISPENSING SYSTEMS MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 26 HEALTHCARE DISPENSING SYSTEMS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 27 HEALTHCARE DISPENSING SYSTEMS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 28 HEALTHCARE DISPENSING SYSTEMS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 29 GLOBAL PATENTS GRANTED IN HEALTHCARE DISPENSING SYSTEMS MARKET, 2015-2024

- FIGURE 30 JURISDICTION ANALYSIS: TOP APPLICANT COUNTRIES FOR "REAGENT DISPENSING SYSTEMS" PATENTS (JANUARY 2015-JUNE 2025)

- FIGURE 31 MAJOR PATENTS IN HEALTHCARE DISPENSING SYSTEMS MARKET (JANUARY 2015-JUNE 2025)

- FIGURE 32 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR END USERS

- FIGURE 33 KEY BUYING CRITERIA FOR TOP END USERS

- FIGURE 34 HEALTHCARE DISPENSING SYSTEMS MARKET: IMPORT SCENARIO FOR HS CODE 8413, 2020-2024

- FIGURE 35 HEALTHCARE DISPENSING SYSTEMS MARKET: EXPORT SCENARIO FOR HS CODE 8413, 2020-2024

- FIGURE 39 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET SNAPSHOT

- FIGURE 40 ASIA PACIFIC: HEALTHCARE DISPENSING SYSTEMS MARKET SNAPSHOT

- FIGURE 41 REVENUE ANALYSIS OF KEY PLAYERS IN HEALTHCARE DISPENSING SYSTEMS MARKET, 2020-2024 (USD MILLION)

- FIGURE 42 MARKET SHARE ANALYSIS OF KEY PLAYERS IN HEALTHCARE DISPENSING SYSTEMS MARKET (2024)

- FIGURE 43 RANKING OF KEY PLAYERS IN HEALTHCARE DISPENSING SYSTEMS MARKET, 2024

- FIGURE 44 HEALTHCARE DISPENSING SYSTEMS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 45 HEALTHCARE DISPENSING SYSTEMS MARKET: COMPANY FOOTPRINT

- FIGURE 46 HEALTHCARE DISPENSING SYSTEMS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 47 EV/EBITDA OF KEY VENDORS, 2024

- FIGURE 48 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND A 5-YEAR STOCK BETA OF HEALTHCARE DISPENSING SYSTEM VENDORS, 2024

- FIGURE 49 HEALTHCARE DISPENSING SYSTEMS MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 50 NORDSON CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 51 AGILENT TECHNOLOGIES, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 52 DANAHER CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 53 THERMO FISHER SCIENTIFIC INC.: COMPANY SNAPSHOT

- FIGURE 54 PARKER-HANNIFIN CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 55 GRACO INC.: COMPANY SNAPSHOT (2024)

- FIGURE 56 REVVITY, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 57 TECAN TRADING AG: COMPANY SNAPSHOT (2024)

- FIGURE 58 QIAGEN: COMPANY SNAPSHOT (2024)

The healthcare dispensing systems market is projected to reach USD 6.27 billion by 2030 from USD 4.61 billion in 2025, at a CAGR of 6.3% during the forecast period. The growing demand for precision, automation, and efficiency in life sciences and clinical applications drives pharmaceutical and biotechnology companies to shift toward high-throughput screening and personalized medicine. As a result, there is a rising need for accurate and contamination-free liquid handling systems. Concerns about advanced dispensing systems, high costs, and integration issues with other laboratory systems can hinder the growth of the healthcare dispensing systems market to some extent over the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2024-2030 |

| Units Considered | Value (USD billion) |

| Segments | Type, Dispensing Material, Application, End User, and Region |

| Regions covered | North America, Europe, APAC, MEA, LATAM |

"Diagnostic & Point-of-care testing management is the fastest growing application segment in the healthcare dispensing systems market during the forecast period."

By application, the healthcare dispensing systems market is segmented into pharmaceutical & biotechnology, diagnostic & point-of-care testing management, medical device manufacturing, pharmacy management, and other applications. Among these, the diagnostic & point-of-care testing management is the fastest-growing segment, driven by the increasing demand for rapid, decentralized testing and the global focus on early disease detection. This segment covers applications such as lateral flow assays (LFAs), PCR and NAAT tests, ELISA, microarrays, and microfluidic devices, each requiring accurate and repeatable dispensing of reagents and samples. Growth is fueled by the expansion of molecular diagnostics, rising infectious disease surveillance, and the growing availability of compact, high-throughput testing platforms. The need for precision, speed, and automation in producing consistent diagnostic results has led to the widespread adoption of automated dispensing systems that reduce variability, ensure traceability, and support large-scale manufacturing of test kits.

"Liquids are the fastest growing segment in the healthcare dispensing systems market, by dispensing material, during the forecast period."

By dispensing material, the healthcare dispensing systems market is segmented into liquids; powders, granules, lyophilized materials; and other dispensing materials. Among these, the liquid segment is projected to grow at the fastest rate during the forecast period due to its critical role in diagnostic, pharmaceutical, and research applications. Liquid dispensing systems are essential for accurately handling reagents, buffers, biological samples, and drug formulations in high-throughput environments. Their precision, speed, and compatibility with automated systems make them indispensable in clinical diagnostics (e.g., ELISA, PCR), pharmaceutical R&D, and point-of-care testing workflows. The increasing demand for automated liquid handling, driven by expanding test volumes, biologics manufacturing, and personalized medicine, has significantly boosted adoption. Additionally, advancements in non-contact and tipless dispensing technologies have enabled greater accuracy and minimized contamination, supporting applications that require stringent quality control. As automation, digitalization, and throughput optimization continue to reshape healthcare and laboratory operations, liquid dispensing systems emerge as a prominent technology, providing scalable, efficient, and compliant fluid handling solutions across diverse end users segments.

"The Asia Pacific region is expected to register the highest growth rate in the healthcare dispensing systems market during the forecast period."

The global healthcare dispensing systems market is segmented into five major regions: North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2024, the Asia Pacific is expected to register the fastest growth in healthcare dispensing systems during the forecast period. This surge is primarily attributed to increased government funding, ongoing expansion in pharmaceutical and diagnostic manufacturing, and the adoption of automation technologies in countries such as China, India, South Korea, and Singapore. Additionally, favorable manufacturing policies, rising foreign direct investment in medtech and biotech sectors, and increased clinical research activity are creating strong demand for high-throughput, automated dispensing solutions. Combined with a focus on improving healthcare accessibility and efficiency, these factors are expected to significantly drive the growth of the healthcare dispensing systems market in Asia Pacific.

The breakdown of primary participants is as mentioned below:

- By Company Type - Tier 1 (41%), Tier 2 (31%), and Tier 3 (28%)

- By Designation - C-level Executives (44%), Director-level (31%), and Others (25%)

- By Region - North America (45%), Europe (28%), Asia Pacific (20%), Latin America (4%), Middle East & Africa (3%)

Key Players

The prominent players in this market are Nordson Corporation (US), DH Life Sciences, LLC (US), ABB (Switzerland), Fisnar (US), PARKER HANNIFIN CORP (US), BioDot (US), Thermo Fisher Scientific Inc. (US), bdtronic (Germany), Agilent Technologies, Inc. (US), Hamilton Company (US), Graco Inc. (US), Imagene Technology Inc (US), Harro Hofliger Verpackungsmaschinen GmbH (Germany), Tecan Trading AG (Switzerland), IVEK Corporation (US), Perkinelmer (US), QIAGEN (Germany), Coperion GmbH (Germany), Ascential Technologies (US), and and LGC Biosearch Technologies (UK). Players adopted organic as well as inorganic growth strategies such as product launches and enhancements, and investments, partnerships, collaborations, joint ventures, funding, acquisition, expansions, agreements, contracts, and alliances to increase their offerings, cater to the unmet needs of customers, increase their profitability, and expand their presence in the global market.

Research Coverage

- The report studies the healthcare dispensing systems market based on type, dispensing material, application, end user, and region.

- The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting market growth.

- The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

- The report studies micro-markets with respect to their growth trends, prospects, and contributions to the total healthcare dispensing systems market.

- The report forecasts the revenue of market segments with respect to five major regions.

Reasons to Buy the Report

The report can help established firms, as well as new entrants/smaller firms, gauge the pulse of the market, which, in turn, would help them garner a greater share. Firms purchasing the report could use one or a combination of the five strategies mentioned below.

This report provides insights into the following pointers:

- Analysis of key drivers (increasing demand for automation and precision in pharmaceutical and diagnostic workflows, rising adoption of point-of-care and decentralized testing platforms, growing need for high-throughput testing solutions in response to global health challenges, ongoing advancements in liquid handling and non-contact dispensing technologies, expansion of R&D and manufacturing infrastructure by biotech and medtech companies, supportive government initiatives for domestic manufacturing, and the push for digital transformation in clinical laboratories), restraints (high capital investment for advanced dispensing systems, limited adoption in low-resource settings, and technical complexity requiring skilled personnel), opportunities (rising outsourcing of diagnostic manufacturing to contract service providers, increasing investments in personalized medicine and biologics requiring precise micro dispensing, rapid growth in Asia Pacific healthcare infrastructure, demand for integrated cloud-based dispensing systems, and increased use of modular systems in flexible lab automation environments), and challenges (stringent regulatory validation processes, interoperability issues between dispensing systems and lab information systems, supply chain disruptions affecting critical dispensing components, and resistance from traditional labs in adopting automated workflows) influencing the growth of healthcare dispensing systems market).

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the healthcare dispensing systems market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of healthcare dispensing systems across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the healthcare dispensing systems market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the healthcare dispensing systems market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primary sources

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.4.1 MARKET SIZING ASSUMPTIONS

- 2.4.2 OVERALL STUDY ASSUMPTIONS

- 2.5 RISK ASSESSMENT

- 2.6 RESEARCH LIMITATIONS

- 2.6.1 METHODOLOGY-RELATED LIMITATIONS

- 2.6.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 HEALTHCARE DISPENSING SYSTEMS MARKET OVERVIEW

- 4.2 HEALTHCARE DISPENSING SYSTEMS MARKET, BY REGION

- 4.3 NORTH AMERICA: HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER & REGION

- 4.4 HEALTHCARE DISPENSING SYSTEMS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.5 HEALTHCARE DISPENSING SYSTEMS MARKET: DEVELOPED VS. EMERGING ECONOMIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.1.1 DRIVERS

- 5.1.1.1 Innovation in artificial intelligence and robotic systems

- 5.1.1.2 Biotech and medtech R&D expansion

- 5.1.1.3 Workflow optimization and lab digitization

- 5.1.1.4 Government incentives for advanced manufacturing

- 5.1.2 RESTRAINTS

- 5.1.2.1 High cost of healthcare dispensing systems

- 5.1.2.2 Regulatory and validation burdens

- 5.1.2.3 Limited infrastructure in emerging markets

- 5.1.3 OPPORTUNITIES

- 5.1.3.1 Growing demand from emerging biotech hubs

- 5.1.3.2 Growing partnerships and collaborations

- 5.1.3.3 Increasing healthcare spending across regions

- 5.1.4 CHALLENGES

- 5.1.4.1 System integration challenges with existing laboratory infrastructure

- 5.1.4.2 Shortage of skilled workforce for operating advanced labs

- 5.1.1 DRIVERS

- 5.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.3 INDUSTRY TRENDS

- 5.3.1 AUTOMATION AND ROBOTICS ADOPTION

- 5.3.2 AI AND MACHINE LEARNING INTEGRATION

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 KEY TECHNOLOGIES

- 5.6.1.1 Non-contact dispensing technologies

- 5.6.1.2 Pressure-based microfluidic dispensing

- 5.6.1.3 Robotic automation & vision systems

- 5.6.2 COMPLEMENTARY TECHNOLOGIES

- 5.6.2.1 Laboratory information management systems (LIMS)

- 5.6.2.2 Computer-aided design and manufacturing (CAD/CAM) systems

- 5.6.3 ADJACENT TECHNOLOGIES

- 5.6.3.1 Digital twin technology

- 5.6.3.2 3D printing in healthcare dispensing ecosystems

- 5.6.3.3 AI-driven predictive maintenance for dispensing systems

- 5.6.1 KEY TECHNOLOGIES

- 5.7 REGULATORY ANALYSIS

- 5.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.7.2 REGULATORY ANALYSIS

- 5.7.2.1 North America

- 5.7.2.2 Europe

- 5.7.2.3 Asia Pacific

- 5.7.2.4 Middle East & Africa

- 5.7.2.5 Latin America

- 5.8 PRICING ANALYSIS

- 5.8.1 INDICATIVE PRICING FOR HEALTHCARE DISPENSING SYSTEMS, BY PRODUCT (2024)

- 5.8.2 INDICATIVE PRICING FOR HEALTHCARE DISPENSING SYSTEMS MARKET, BY REGION, 2024

- 5.9 PORTER'S FIVE FORCES ANALYSIS

- 5.9.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.9.2 BARGAINING POWER OF BUYERS

- 5.9.3 THREAT OF SUBSTITUTES

- 5.9.4 THREAT OF NEW ENTRANTS

- 5.9.5 BARGAINING POWER OF SUPPLIERS

- 5.10 PATENT ANALYSIS

- 5.10.1 PATENT PUBLICATION TRENDS FOR HEALTHCARE DISPENSING SYSTEMS MARKET

- 5.10.2 JURISDICTION ANALYSIS: TOP APPLICANT COUNTRIES FOR HEALTHCARE DISPENSING SYSTEMS MARKET

- 5.10.3 MAJOR PATENTS IN HEALTHCARE DISPENSING SYSTEMS MARKET

- 5.11 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.11.2 KEY BUYING CRITERIA

- 5.12 END-USER ANALYSIS

- 5.12.1 UNMET NEEDS

- 5.12.2 END-USER EXPECTATIONS

- 5.13 KEY CONFERENCES & EVENTS, 2025-2026

- 5.14 CASE STUDY ANALYSIS

- 5.15 TRADE ANALYSIS

- 5.15.1 IMPORT SCENARIO (HS CODE 8413)

- 5.15.2 EXPORT SCENARIO (HS CODE 8413)

- 5.16 INVESTMENT & FUNDING SCENARIO

- 5.17 IMPACT OF 2025 US TARIFFS ON HEALTHCARE DISPENSING SYSTEMS MARKET

- 5.17.1 KEY TARIFF RATES

- 5.17.2 PRICE IMPACT ANALYSIS

- 5.17.3 IMPACT ON COUNTRY/REGION

- 5.17.3.1 US

- 5.17.3.2 Europe

- 5.17.3.3 APAC

- 5.17.4 IMPACT ON END-USE INDUSTRIES

6 HEALTHCARE DISPENSING SYSTEMS MARKET, BY TYPE

- 6.1 INTRODUCTION

- 6.2 AUTOMATIC DISPENSING SYSTEMS

- 6.2.1 GROWING DEMAND FOR PRECISION, STERILITY, AND LAB AUTOMATION TO BOOST ADOPTION OF AUTOMATIC DISPENSING SYSTEMS

- 6.3 SEMI-AUTOMATIC DISPENSING SYSTEMS

- 6.3.1 RISING R&D AND MID-VOLUME LAB DEMAND TO DRIVE DEMAND FOR COST-EFFECTIVE SEMI-AUTOMATED DISPENSING SYSTEMS

- 6.4 STANDALONE/MANUAL DISPENSING SYSTEMS

- 6.4.1 VITAL ROLE OF MANUAL DISPENSING TOOLS IN LOW-RESOURCE, HIGH-CUSTOMIZATION LAB SETTINGS TO SUPPORT MARKET GROWTH

- 6.5 OEM/DISPENSING COMPONENTS

- 6.5.1 PUMPS

- 6.5.1.1 Ability of precision pumps to power sterile, compliant fluid handling across healthcare workflows to drive growth

- 6.5.2 VALVES & NOZZLES

- 6.5.2.1 Ability of valves & nozzles to enable precision, contamination-free fluid control in automated dispensing to boost market

- 6.5.3 CONTROL SYSTEMS

- 6.5.3.1 Ability of control systems to drive intelligent, compliant automation in healthcare dispensing to contribute to growth

- 6.5.4 OTHER OEM COMPONENTS

- 6.5.1 PUMPS

7 HEALTHCARE DISPENSING SYSTEMS MARKET, BY MATERIAL

- 7.1 INTRODUCTION

- 7.2 LIQUIDS

- 7.2.1 REAGENTS

- 7.2.1.1 Growing automation needs in diagnostics, genomics, and biomanufacturing to boost demand for reagent dispensing systems

- 7.2.2 BUFFERS

- 7.2.2.1 High demand for scalable, validated workflows in biologics and diagnostics to boost market for buffer dispensing systems

- 7.2.3 ANTIBODIES

- 7.2.3.1 Rising demand for ultra-precise diagnostic and therapeutic applications to boost demand for antibody dispensing systems

- 7.2.4 OTHER LIQUIDS

- 7.2.1 REAGENTS

- 7.3 POWDERS, GRANULES, AND LYOPHILIZED MATERIALS

- 7.3.1 CAKES

- 7.3.1.1 Growing demand for high-precision injectable and diagnostic products to boost market for lyophilized cake dispensing

- 7.3.2 LYOBEADS

- 7.3.2.1 Ability of lyobeads to power cold chain-free diagnostics and therapeutics to drive growth

- 7.3.3 OTHER POWDERS, GRANULES, AND LYOPHILIZED MATERIALS

- 7.3.1 CAKES

- 7.4 OTHER MATERIALS

8 HEALTHCARE DISPENSING SYSTEMS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 PHARMACEUTICAL & BIOTECHNOLOGY

- 8.2.1 R&D

- 8.2.1.1 Pivotal role of R&D in precise dispensing systems to support growth

- 8.2.2 MANUFACTURING & QA/QC

- 8.2.2.1 Advancing quality control with intelligent dispensing in pharma & biotech manufacturing to fuel growth

- 8.2.1 R&D

- 8.3 DIAGNOSTICS & POC TESTING

- 8.3.1 LATERAL FLOW ASSAYS & RAPID TESTS

- 8.3.1.1 Ability of these tests to enable scalable production with precision dispensing systems to boost market

- 8.3.2 PCR & NUCLEIC ACID TESTS

- 8.3.2.1 Ability of dispensing systems to advance PCR & NAAT efficiency to fuel growth

- 8.3.3 IMMUNOASSAYS & ELISA TESTS

- 8.3.3.1 Ability of automated dispensing systems to power high-throughput immunoassays to propel growth

- 8.3.4 MICROARRAYS

- 8.3.4.1 High-density assay precision with advanced dispensing systems to drive demand

- 8.3.5 IMMUNOBLOTS

- 8.3.5.1 Growing need to automate immunoblot workflows to drive market

- 8.3.6 MICROFLUIDICS & LAB-ON-A-CHIP TESTS

- 8.3.6.1 Advantages of dispensing systems in microfluidic and lab-on-a-chip technologies to support market

- 8.3.7 OTHER DIAGNOSTICS & POC TESTING APPLICATIONS

- 8.3.1 LATERAL FLOW ASSAYS & RAPID TESTS

- 8.4 MEDICAL DEVICE MANUFACTURING

- 8.4.1 DRUG DELIVERY DEVICES

- 8.4.1.1 Advantages such as precision filling and coating with advanced dispensing systems to boost market

- 8.4.2 IMPLANTABLE MEDICAL DEVICES

- 8.4.2.1 Growing need for dispensing of coatings, drug layers, and biocompatible materials to support market

- 8.4.3 SURGICAL INSTRUMENTS & WOUND CARE DEVICES

- 8.4.3.1 Ability of dispensing systems to drive quality and sterility in surgical and wound care devices to fuel growth

- 8.4.4 DIAGNOSTIC TEST KIT MANUFACTURING

- 8.4.4.1 Vital role of dispensing technologies in supporting medical-grade devices to drive growth

- 8.4.5 OTHER MEDICAL DEVICE MANUFACTURING APPLICATIONS

- 8.4.1 DRUG DELIVERY DEVICES

- 8.5 PHARMACY MANAGEMENT

- 8.5.1 INCREASING INTEGRATION OF DISPENSING SYSTEMS IN PHARMACY MANAGEMENT TO DRIVE GROWTH

- 8.6 OTHER APPLICATIONS

9 HEALTHCARE DISPENSING SYSTEMS MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 HEALTHCARE PROVIDERS

- 9.2.1 HOSPITALS

- 9.2.1.1 High test volumes and strong push for automation to boost market growth

- 9.2.2 DIAGNOSTIC LABS

- 9.2.2.1 Need for precise, high-throughput dispensing in clinical testing to drive demand in diagnostic labs

- 9.2.3 OUTPATIENT SETTINGS

- 9.2.3.1 Need for patient safety in outpatient settings to boost segmental growth

- 9.2.4 HOME HEALTHCARE, LONG-TERM CARE, AND ASSISTED LIVING FACILITIES

- 9.2.4.1 Need to support decentralized, high-throughput care and ensure regulatory compliance to boost adoption

- 9.2.5 PHARMACIES

- 9.2.5.1 Growing need for technology to assist with faster prescription filling and medication dispensing to drive market growth

- 9.2.6 OTHER HEALTHCARE PROVIDERS

- 9.2.1 HOSPITALS

- 9.3 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 9.3.1 GROWING IMPORTANCE OF AUTOMATION TO ENHANCE DRUG DEVELOPMENT SPEED AND ACCURACY TO BOOST DEMAND

- 9.4 MEDTECH COMPANIES

- 9.4.1 GROWING ADOPTION OF PRECISION DISPENSING SYSTEMS TO SUPPORT DEVICE MINIATURIZATION

- 9.5 OTHER END USERS

10 HEALTHCARE DISPENSING SYSTEMS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 US to dominate North American healthcare dispensing systems market

- 10.2.3 CANADA

- 10.2.3.1 Strong demand for pharmacy automation to propel market

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 Germany to dominate European healthcare dispensing systems market during forecast period

- 10.3.3 UK

- 10.3.3.1 Strong support for life science R&D and well-developed infrastructure to aid market

- 10.3.4 FRANCE

- 10.3.4.1 Increasing investment in R&D and funding for life sciences to drive growth

- 10.3.5 ITALY

- 10.3.5.1 Advancements in laboratory systems to drive growth

- 10.3.6 SPAIN

- 10.3.6.1 Expanding medical diagnostics research to propel market growth

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 CHINA

- 10.4.2.1 China to grow at highest growth rate during forecast period

- 10.4.3 JAPAN

- 10.4.3.1 Japan to dominate Asia Pacific healthcare dispensing systems market

- 10.4.4 INDIA

- 10.4.4.1 Expansion of biotech sector, coupled with supportive government policies, to fuel market growth

- 10.4.5 REST OF ASIA

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.5.2 BRAZIL

- 10.5.2.1 Growing public and private initiatives supporting scientific research to drive growth

- 10.5.3 MEXICO

- 10.5.3.1 Thriving pharmaceutical industry to drive market

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 10.6.2 GCC COUNTRIES

- 10.6.2.1 Improvements in healthcare infrastructure to support market growth

- 10.6.3 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 RANKING OF KEY MARKET PLAYERS

- 11.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.6.1 STARS

- 11.6.2 EMERGING LEADERS

- 11.6.3 PERVASIVE PLAYERS

- 11.6.4 PARTICIPANTS

- 11.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.6.5.1 Company footprint

- 11.6.5.2 Region footprint

- 11.6.5.3 Type footprint

- 11.6.5.4 Material footprint

- 11.6.5.5 Application footprint

- 11.6.5.6 End-user footprint

- 11.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 RESPONSIVE COMPANIES

- 11.7.3 DYNAMIC COMPANIES

- 11.7.4 STARTING BLOCKS

- 11.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.7.5.1 Detailed list of key startups/SMEs

- 11.7.5.2 Competitive benchmarking of startups/SMEs

- 11.8 COMPANY VALUATION & FINANCIAL METRICS

- 11.9 BRAND/PRODUCT COMPARISON

- 11.10 COMPETITIVE SCENARIO

- 11.10.1 PRODUCT LAUNCHES

- 11.10.2 DEALS

- 11.10.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 NORDSON CORPORATION

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.3.3 Expansions

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses & competitive threats

- 12.1.2 AGILENT TECHNOLOGIES, INC.

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses & competitive threats

- 12.1.3 DANAHER CORPORATION

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses & competitive threats

- 12.1.4 THERMO FISHER SCIENTIFIC INC.

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Expansions

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses & competitive threats

- 12.1.5 BIODOT

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win