|

|

市場調査レポート

商品コード

1718871

海底断熱材の世界市場:タイプ別、充填材タイプ別、用途別、地域別 - 2030年までの予測Subsea Thermal Insulation Materials Market by Type, Filler Type, Application, and Region - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 海底断熱材の世界市場:タイプ別、充填材タイプ別、用途別、地域別 - 2030年までの予測 |

|

出版日: 2025年04月29日

発行: MarketsandMarkets

ページ情報: 英文 298 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

海底断熱材の市場規模は、2025年の2億5,670万米ドルから2030年には3億1,660万米ドルに達すると予測され、予測期間中のCAGRは4.3%になるとみられています。

エネルギー企業は、海洋深海環境への事業シフトをますます進めており、海底パイプラインの正確な熱管理が必要となっています。これは、生産継続に重大なリスクをもたらすハイドレート形成を抑制するために極めて重要です。このような厳しい条件下で安全かつ効率的な操業を行うには、過酷な水中環境に耐える信頼性の高い断熱材を使用する必要があります。材料科学と断熱技術の開発により、過酷な海底条件に耐えうる高性能材料が開発されました。このような技術強化は、安全機構を改善するだけでなく、水中施設の運用寿命を延ばすことにもつながります。海洋探査・生産活動が世界的に拡大する中、これらの技術革新は予測期間中の市場成長を推進する上で極めて重要です。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2023年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 検討単位 | 金額(100万米ドル)数量(トン) |

| セグメント | タイプ別、充填材タイプ別、用途別、地域別 |

| 対象地域 | 北米、アジア太平洋、欧州、中東・アフリカ、南米 |

ポリプロピレンは、特に深海用途において、その優れた性能特性と費用対効果に牽引され、市場で2番目に高い成長率を記録すると予測されています。このポリマーは、断熱性と機械的強度の優れたバランスを示すと同時に、耐吸水性を発揮するため、極寒・高圧環境下での海底パイプラインや機器の保護に適しています。経済的にも、ポリプロピレンは高級断熱材に代わる競争力のある選択肢を提供します。石油・ガスの海洋事業がより深海まで拡大するにつれ、厳しい性能基準を満たす信頼性とコスト効率の両方を備えた絶縁ソリューションが急務となっています。この動向は、業界におけるポリプロピレンの需要を大幅に高めると予想されます。

パイプインパイプ(PiP)用途は、特に深海や超深海用途に適しており、その優れた熱効率に起因して、市場内で2番目に急成長しているセグメントになると予測されています。PiPシステムには同軸設計が採用されており、太い内管が細い外管に包まれ、断熱材が環状空間を満たしています。この構成により、広範な海底パイプラインの流体温度が効果的に維持され、ハイドレートやワックス析出による流れの乱れのリスクが大幅に低減されます。PiP断熱システムに対する需要の高まりは、信頼性の高い高性能断熱ソリューションが必要とされる、より過酷な環境への業界の拡大が主な要因となっています。

ガラス微小球は、その卓越した軽量化可能性、優れた断熱特性、優れた圧縮強度により、深海や超深海用途に適しているため、市場を独占すると予測されています。海底分野では、この小さなガラス球が、断熱コーティングからの熱損失を最小限に抑え、高圧水中環境における石油・ガスパイプラインや機器の運転温度を維持する上で重要な役割を果たしています。

中東・アフリカは、深海・超深海地域での石油・ガス探査活動の加速に牽引され、海底断熱材の2番目に急成長する市場として浮上しています。アンゴラ、ナイジェリア、ナミビアのような国々は、これまで未開拓だった油層にアクセスするためにオフショア・プロジェクト開発への取り組みを強化しており、サウジアラビアとUAEは生産能力を強化するためにオフショア事業を拡大しています。海底プロジェクトがますます課題となっている水深まで進むにつれて、パイプラインの最適な性能を確保するための効果的な断熱材に対する需要が大幅に高まっています。沖合鉱区の発見が強化され、アフリカの海洋地帯への外国投資が増加したことで、海底インフラ開発の大幅な進歩への道が開かれつつあります。現在進行中の地域パイプライン構想や、暑い気候や過酷な水中条件に耐えられるよう調整された断熱ソリューションへのニーズが、中東・アフリカ全域の海底断熱材に対する市場の堅調な需要を牽引しています。この探査活動と技術革新の融合は、同地域の海底材料市場にとって極めて重要な瞬間です。

本調査には、海底断熱材市場におけるこれら主要企業の企業プロファイル、最近の動向、主要市場戦略など、詳細な競合分析が含まれています。

当レポートでは、世界の海底断熱材市場について調査し、同市場をタイプ(ポリウレタン、ポリプロピレン、シリコーンゴム、エポキシ、エアロゲル、EPDM、その他のタイプ)、充填剤タイプ(ガラス微小球、その他の充填剤タイプ)、用途(パイプインパイプ、直接断熱&パイプカバー、機器、フィールドジョイント、その他の用途)、地域(アジア太平洋、北米、欧州、南米、中東&アフリカ)に基づいて分類しています。当レポートの調査範囲は、海底断熱材市場の成長に影響を与える促進要因・抑制要因・課題・機会に関する詳細情報を網羅しています。主要業界プレイヤーの詳細な分析により、事業概要、提供製品、海底断熱材市場に関連する提携、拡張、買収などの主要戦略に関する洞察を提供しています。

レポート購入の理由

当レポートは、海底断熱材市場全体とサブセグメントの収益数の最も近い近似値に関する情報を市場リーダー/新規参入者に提供します。当レポートは、利害関係者が競合情勢を理解し、事業をより良く位置づけるための考察を深め、適切な市場参入戦略を計画するのに役立ちます。当レポートは、利害関係者が市場の鼓動を理解し、主要市場促進要因・抑制要因・課題・機会に関する情報を提供するのに役立ちます。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 顧客ビジネスに影響を与える動向/混乱

- エコシステム分析

- バリューチェーン分析

- 規制状況

- 価格分析

- 貿易分析

- 技術分析

- 特許分析

- ケーススタディ分析

- 2025年~2026年の主な会議とイベント

- AI/生成AIが海底断熱材市場に与える影響

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- マクロ経済分析

- 2025年の米国関税が海底断熱材市場に与える影響

第6章 海底断熱材市場(タイプ別)

- イントロダクション

- ポリウレタン

- ポリプロピレン

- シリコンゴム

- エポキシ

- エアロゲル

- その他

第7章 海底断熱材市場(充填材タイプ別)

- イントロダクション

- ガラスマイクロスフィア

- その他

第8章 海底断熱材市場(用途別)

- イントロダクション

- パイプインパイプ

- 直接断熱材とパイプカバー

- 装置

- フィールドジョイント

- その他

第9章 海底断熱材市場(地域別)

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他

- 欧州

- ロシア

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- その他

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他

- 南米

- ブラジル

- アルゼンチン

- その他

第10章 競合情勢

- イントロダクション

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- 企業評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:中小企業、2024年

- 競合シナリオ

第11章 企業プロファイル

- 主要参入企業

- ASPEN AEROGELS, INC.

- CABOT CORPORATION

- AIS

- KINGSPAN GROUP

- TENARIS S.A.

- VIPO AS

- BALMORAL GROUP

- PERMA-PIPE INTERNATIONAL HOLDINGS, INC.

- LFM ENERGY

- BEERENBERG GROUP

- その他の企業

- ENGINEERED SYNTACTIC SYSTEMS

- V.I.P. VERNICIATURA INDUSTRIALE PESARESE SRL

- DOW

- SIAO PETROLEO S.A.

- ACOUSTIC POLYMERS LTD.

- AKZONOBEL N.V.

- HUNTSMAN INTERNATIONAL LLC

- BASF SE

- ROCKWOOL GROUP

- EXXON MOBIL CORPORATION

- WACKER CHEMIE AG

- THERMAL MITIGATION TECHNOLOGIES, LLC

- エンドユーザー

- SAIPEM SPA

- SUBSEA 7 S.A.

- TECHNIPFMC PLC

- MCDERMOTT

- BAKER HUGHES COMPANY

- HALLIBURTON

- NOV INC.

- PRYSMIAN GROUP

- JOHN WOOD GROUP PLC

- ONESUBSEA

- SAPURA ENERGY BERHAD

- FUGRO

- ENBRIDGE INC.

- L&T ENERGY HYDROCARBON(LTEH)

- OCEANEERING INTERNATIONAL, INC.

第12章 隣接市場と関連市場

第13章 付録

List of Tables

- TABLE 1 ROLES OF COMPANIES IN SUBSEA THERMAL INSULATION MATERIALS ECOSYSTEM

- TABLE 2 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 3 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 4 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 5 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 6 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 7 INDICATIVE PRICING ANALYSIS OF SUBSEA THERMAL INSULATION MATERIALS OFFERED BY KEY PLAYERS, BY APPLICATION, 2024 (USD/TON)

- TABLE 8 AVERAGE SELLING PRICE TREND OF SUBSEA THERMAL INSULATION MATERIALS, BY REGION, 2021-2024 (USD/TON)

- TABLE 9 IMPORT DATA RELATED TO HS CODE 392690-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 10 EXPORT DATA RELATED TO HS CODE 392690-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 11 SUBSEA THERMAL INSULATION MATERIALS MARKET: LIST OF KEY PATENTS, 2020-2024

- TABLE 12 SUBSEA THERMAL INSULATION MATERIALS MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 13 SUBSEA THERMAL INSULATION MATERIALS MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 14 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY APPLICATIONS

- TABLE 15 KEY BUYING CRITERIA FOR MAJOR APPLICATIONS

- TABLE 16 GLOBAL GDP GROWTH PROJECTION, BY REGION, 2021-2028 (USD TRILLION)

- TABLE 17 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 18 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 19 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 20 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 21 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE (EPDM), 2023-2030 (USD THOUSAND)

- TABLE 22 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE (EPDM), 2023-2030 (TONS)

- TABLE 23 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (USD THOUSAND)

- TABLE 24 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (TONS)

- TABLE 25 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

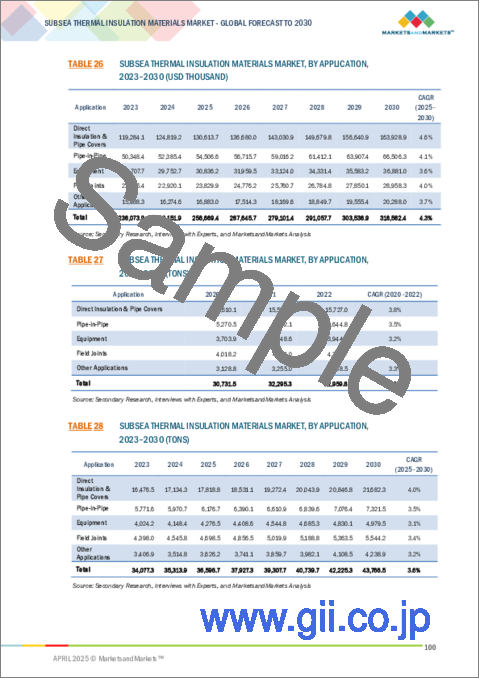

- TABLE 26 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 27 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 28 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 29 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY REGION, 2020-2022 (USD THOUSAND)

- TABLE 30 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY REGION, 2023-2030 (USD THOUSAND)

- TABLE 31 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY REGION, 2020-2022 (TONS)

- TABLE 32 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY REGION, 2023-2030 (TONS)

- TABLE 33 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (USD THOUSAND)

- TABLE 34 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (USD THOUSAND)

- TABLE 35 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (TONS)

- TABLE 36 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (TONS)

- TABLE 37 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 38 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 39 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 40 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 41 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (USD THOUSAND)

- TABLE 42 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (TONS)

- TABLE 43 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 44 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 45 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 46 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 47 US: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 48 US: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 49 US: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 50 US: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 51 US: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 52 US: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 53 US: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 54 US: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 55 CANADA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 56 CANADA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 57 CANADA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 58 CANADA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 59 CANADA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 60 CANADA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 61 CANADA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 62 CANADA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 63 MEXICO: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 64 MEXICO: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 65 MEXICO: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 66 MEXICO: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 67 MEXICO: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 68 MEXICO: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 69 MEXICO: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 70 MEXICO: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 71 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (USD THOUSAND)

- TABLE 72 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (USD THOUSAND)

- TABLE 73 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (TONS)

- TABLE 74 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (TONS)

- TABLE 75 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 76 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 77 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 78 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 79 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (USD THOUSAND)

- TABLE 80 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (TONS)

- TABLE 81 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 82 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 83 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 84 ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 85 CHINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 86 CHINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 87 CHINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 88 CHINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 89 CHINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 90 CHINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 91 CHINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 92 CHINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 93 INDIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 94 INDIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 95 INDIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 96 INDIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 97 INDIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 98 INDIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 99 INDIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 100 INDIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 101 JAPAN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 102 JAPAN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 103 JAPAN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 104 JAPAN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 105 JAPAN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 106 JAPAN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 107 JAPAN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 108 JAPAN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 109 SOUTH KOREA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 110 SOUTH KOREA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 111 SOUTH KOREA SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 112 SOUTH KOREA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 113 SOUTH KOREA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 114 SOUTH KOREA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 115 SOUTH KOREA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 116 SOUTH KOREA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 117 REST OF ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 118 REST OF ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 119 REST OF ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 120 REST OF ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 121 REST OF ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 122 REST OF ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 123 REST OF ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 124 REST OF ASIA PACIFIC: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 125 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (USD THOUSAND)

- TABLE 126 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (USD THOUSAND)

- TABLE 127 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (TONS)

- TABLE 128 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (TONS)

- TABLE 129 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 130 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 131 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 132 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 133 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (USD THOUSAND)

- TABLE 134 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (TONS)

- TABLE 135 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 136 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 137 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 138 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 139 RUSSIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 140 RUSSIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 141 RUSSIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 142 RUSSIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 143 RUSSIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 144 RUSSIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 145 RUSSIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 146 RUSSIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 147 GERMANY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 148 GERMANY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 149 GERMANY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 150 GERMANY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 151 GERMANY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 152 GERMANY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 153 GERMANY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 154 GERMANY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 155 FRANCE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 156 FRANCE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 157 FRANCE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 158 FRANCE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 159 FRANCE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 160 FRANCE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 161 FRANCE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 162 FRANCE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 163 UK: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 164 UK: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 165 UK: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 166 UK: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 167 UK: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 168 UK: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 169 UK: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 170 UK: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 171 SPAIN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 172 SPAIN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 173 SPAIN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 174 SPAIN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 175 SPAIN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 176 SPAIN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 177 SPAIN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 178 SPAIN: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 179 ITALY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 180 ITALY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 181 ITALY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 182 ITALY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 183 ITALY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 184 ITALY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 185 ITALY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 186 ITALY: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 187 REST OF EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 188 REST OF EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 189 REST OF EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 190 REST OF EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 191 REST OF EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 192 REST OF EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 193 REST OF EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 194 REST OF EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 195 MIDDLE EAST AND AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (USD THOUSAND)

- TABLE 196 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (USD THOUSAND)

- TABLE 197 MIDDLE EAST AND AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (TONS)

- TABLE 198 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (TONS)

- TABLE 199 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 200 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 201 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 202 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 203 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (USD THOUSAND)

- TABLE 204 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (TONS)

- TABLE 205 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 206 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 207 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 208 MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 209 GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 210 GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 211 GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 212 GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 213 GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 214 GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 215 GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 216 GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 217 SAUDI ARABIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 218 SAUDI ARABIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 219 SAUDI ARABIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 220 SAUDI ARABIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 221 SAUDI ARABIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 222 SAUDI ARABIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 223 SAUDI ARABIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 224 SAUDI ARABIA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 225 UAE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 226 UAE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 227 UAE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 228 UAE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 229 UAE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 230 UAE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 231 UAE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 232 UAE: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 233 REST OF GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 234 REST OF GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 235 REST OF GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 236 REST OF GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 237 REST OF GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 238 REST OF GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 239 REST OF GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 240 REST OF GCC COUNTRIES: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 241 SOUTH AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 242 SOUTH AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 243 SOUTH AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 244 SOUTH AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 245 SOUTH AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 246 SOUTH AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 247 SOUTH AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 248 SOUTH AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 249 REST OF MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 250 REST OF MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 251 REST OF MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 252 REST OF MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 253 REST OF MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 254 REST OF MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 255 REST OF MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 256 REST OF MIDDLE EAST & AFRICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 257 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (USD THOUSAND)

- TABLE 258 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (USD THOUSAND)

- TABLE 259 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2020-2022 (TONS)

- TABLE 260 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY, 2023-2030 (TONS)

- TABLE 261 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 262 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 263 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 264 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 265 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (USD THOUSAND)

- TABLE 266 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE, 2023-2030 (TONS)

- TABLE 267 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 268 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 269 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 270 SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 271 BRAZIL: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 272 BRAZIL: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 273 BRAZIL: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 274 BRAZIL: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 275 BRAZIL: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 276 BRAZIL: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 277 BRAZIL: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 278 BRAZIL: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 279 ARGENTINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 280 ARGENTINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 281 ARGENTINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 282 ARGENTINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 283 ARGENTINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 284 ARGENTINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 285 ARGENTINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 286 ARGENTINA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 287 REST OF SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (USD THOUSAND)

- TABLE 288 REST OF SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (USD THOUSAND)

- TABLE 289 REST OF SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2020-2022 (TONS)

- TABLE 290 REST OF SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE, 2023-2030 (TONS)

- TABLE 291 REST OF SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (USD THOUSAND)

- TABLE 292 REST OF SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (USD THOUSAND)

- TABLE 293 REST OF SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2020-2022 (TONS)

- TABLE 294 REST OF SOUTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION, 2023-2030 (TONS)

- TABLE 295 SUBSEA THERMAL INSULATION MATERIALS MARKET: OVERVIEW OF KEY STRATEGIES ADOPTED BY MAJOR PLAYERS, 2019-2025

- TABLE 296 SUBSEA THERMAL INSULATION MATERIALS MARKET: DEGREE OF COMPETITION, 2024

- TABLE 297 SUBSEA THERMAL INSULATION MATERIALS MARKET: REGION FOOTPRINT

- TABLE 298 SUBSEA THERMAL INSULATION MATERIALS MARKET: TYPE FOOTPRINT

- TABLE 299 SUBSEA THERMAL INSULATION MATERIALS MARKET: FILLER TYPE FOOTPRINT

- TABLE 300 SUBSEA THERMAL INSULATION MATERIALS MARKET: APPLICATION FOOTPRINT

- TABLE 301 SUBSEA THERMAL INSULATION MATERIALS MARKET: DETAILED LIST OF KEY SMES

- TABLE 302 SUBSEA THERMAL INSULATION MATERIALS MARKET: COMPETITIVE BENCHMARKING OF KEY SMES

- TABLE 303 SUBSEA THERMAL INSULATION MATERIALS MARKET: DEALS, JANUARY 2019-APRIL 2025

- TABLE 304 SUBSEA THERMAL INSULATION MATERIALS MARKET: EXPANSIONS, JANUARY 2019-APRIL 2025

- TABLE 305 ASPEN AEROGELS, INC.: COMPANY OVERVIEW

- TABLE 306 ASPEN AEROGELS, INC.: PRODUCTS OFFERED

- TABLE 307 CABOT CORPORATION: COMPANY OVERVIEW

- TABLE 308 CABOT CORPORATION: PRODUCTS OFFERED

- TABLE 309 AIS: COMPANY OVERVIEW

- TABLE 310 AIS: PRODUCTS OFFERED

- TABLE 311 AIS: DEALS

- TABLE 312 AIS: EXPANSIONS

- TABLE 313 KINGSPAN GROUP: COMPANY OVERVIEW

- TABLE 314 KINGSPAN GROUP: PRODUCTS OFFERED

- TABLE 315 KINGSPAN GROUP: DEALS

- TABLE 316 TENARIS S.A.: COMPANY OVERVIEW

- TABLE 317 TENARIS S.A.: PRODUCTS OFFERED

- TABLE 318 TENARIS S.A.: DEALS

- TABLE 319 VIPO AS: COMPANY OVERVIEW

- TABLE 320 VIPO AS: PRODUCTS OFFERED

- TABLE 321 VIPO AS: DEALS

- TABLE 322 BALMORAL GROUP: COMPANY OVERVIEW

- TABLE 323 BALMORAL GROUP: PRODUCTS OFFERED

- TABLE 324 BALMORAL GROUP: EXPANSIONS

- TABLE 325 PERMA-PIPE INTERNATIONAL HOLDINGS, INC.: COMPANY OVERVIEW

- TABLE 326 PERMA-PIPE INTERNATIONAL HOLDINGS, INC.: PRODUCTS OFFERED

- TABLE 327 PERMA-PIPE INTERNATIONAL HOLDINGS, INC.: EXPANSIONS

- TABLE 328 LFM ENERGY: COMPANY OVERVIEW

- TABLE 329 LFM ENERGY: PRODUCTS OFFERED

- TABLE 330 BEERENBERG GROUP: COMPANY OVERVIEW

- TABLE 331 BEERENBERG GROUP: PRODUCTS OFFERED

- TABLE 332 BEERENBERG GROUP: DEALS

- TABLE 333 ENGINEERED SYNTACTIC SYSTEMS: COMPANY OVERVIEW

- TABLE 334 V.I.P. VERNICIATURA INDUSTRIALE PESARESE SRL: COMPANY OVERVIEW

- TABLE 335 DOW: COMPANY OVERVIEW

- TABLE 336 SIAO PETROLEO S.A.: COMPANY OVERVIEW

- TABLE 337 ACOUSTIC POLYMERS LTD.: COMPANY OVERVIEW

- TABLE 338 AKZONOBEL N.V.: COMPANY OVERVIEW

- TABLE 339 HUNTSMAN INTERNATIONAL LLC: COMPANY OVERVIEW

- TABLE 340 BASF SE: COMPANY OVERVIEW

- TABLE 341 ROCKWOOL GROUP: COMPANY OVERVIEW

- TABLE 342 EXXON MOBIL CORPORATION: COMPANY OVERVIEW

- TABLE 343 WACKER CHEMIE AG: COMPANY OVERVIEW

- TABLE 344 THERMAL MITIGATION TECHNOLOGIES, LLC: COMPANY OVERVIEW

- TABLE 345 SAIPEM SPA: COMPANY OVERVIEW

- TABLE 346 SUBSEA 7 S.A.: COMPANY OVERVIEW

- TABLE 347 TECHNIPFMC PLC: COMPANY OVERVIEW

- TABLE 348 MCDERMOTT: COMPANY OVERVIEW

- TABLE 349 BAKER HUGHES COMPANY: COMPANY OVERVIEW

- TABLE 350 HALLIBURTON: COMPANY OVERVIEW

- TABLE 351 NOV INC.: COMPANY OVERVIEW

- TABLE 352 PRYSMIAN GROUP: COMPANY OVERVIEW

- TABLE 353 JOHN WOOD GROUP PLC: COMPANY OVERVIEW

- TABLE 354 ONESUBSEA: COMPANY OVERVIEW

- TABLE 355 SAPURA ENERGY BERHAD: COMPANY OVERVIEW

- TABLE 356 FUGRO: COMPANY OVERVIEW

- TABLE 357 ENBRIDGE INC.: COMPANY OVERVIEW

- TABLE 358 L&T ENERGY HYDROCARBON (LTEH): COMPANY OVERVIEW

- TABLE 359 OCEANEERING INTERNATIONAL, INC.: COMPANY OVERVIEW

- TABLE 360 OFFSHORE PIPELINE MARKET, BY DIAMETER, 2018-2020 (USD MILLION)

- TABLE 361 OFFSHORE PIPELINE MARKET, BY DIAMETER, 2021-2027 (USD MILLION)

- TABLE 362 OFFSHORE PIPELINE MARKET, BY LINE TYPE, 2018-2020 (USD MILLION)

- TABLE 363 OFFSHORE PIPELINE MARKET, BY LINE TYPE, 2021-2027 (USD MILLION)

- TABLE 364 OFFSHORE PIPELINE MARKET, BY PRODUCT, 2018-2020 (USD MILLION)

- TABLE 365 OFFSHORE PIPELINE MARKET, BY PRODUCT, 2021-2027 (USD MILLION)

- TABLE 366 OFFSHORE PIPELINE MARKET, BY REGION, 2018-2020 (USD MILLION)

- TABLE 367 OFFSHORE PIPELINE MARKET, BY REGION, 2021-2027 (USD MILLION)

- TABLE 368 OFFSHORE PIPELINE MARKET, BY REGION, 2018-2020 (KILOMETERS)

- TABLE 369 OFFSHORE PIPELINE MARKET, BY REGION, 2021-2027 (KILOMETERS)

- TABLE 370 OFFSHORE PIPELINE MARKET, BY REGION, 2018-2020 (USD MILLION)

- TABLE 371 OFFSHORE PIPELINE MARKET, BY REGION, 2021-2027 (USD MILLION)

List of Figures

- FIGURE 1 SUBSEA THERMAL INSULATION MATERIALS MARKET: SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 SUBSEA THERMAL INSULATION MATERIALS MARKET: RESEARCH DESIGN

- FIGURE 3 BREAKDOWN OF INTERVIEWS WITH EXPERTS

- FIGURE 4 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 6 SUBSEA THERMAL INSULATION MATERIALS MARKET: SUPPLY-SIDE ANALYSIS

- FIGURE 7 SUBSEA THERMAL INSULATION MATERIALS MARKET: DATA TRIANGULATION

- FIGURE 8 POLYURETHANE SEGMENT TO HOLD MAJOR SHARE OF SUBSEA THERMAL INSULATION MATERIALS MARKET IN 2025

- FIGURE 9 DIRECT INSULATION & PIPER COVERS TO BE FASTEST-GROWING SEGMENT IN SUBSEA THERMAL INSULATION MATERIALS MARKET DURING FORECAST PERIOD

- FIGURE 10 GLASS MICROSPHERES SEGMENT TO RECORD HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 11 ASIA PACIFIC TO REGISTER FASTEST-GROWTH IN SUBSEA THERMAL INSULATION MATERIALS MARKET DURING FORECAST PERIOD

- FIGURE 12 RISING DEMAND FROM RENEWABLE OFFSHORE ENERGY PROJECTS TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

- FIGURE 13 POLYURETHANE SEGMENT AND REST OF EUROPE HELD LARGEST SHARES OF EUROPEAN SUBSEA THERMAL INSULATION MATERIALS MARKET IN 2024

- FIGURE 14 POLYURETAHNE SEGMENT TO ACCOUNT FOR LARGEST SHARE OF SUBSEA THERMAL INSULATION MATERIALS MARKET IN 2030

- FIGURE 15 DIRECT INSULATION & PIPE COVERS SEGMENT TO ACCOUNT FOR LARGEST SHARE OF SUBSEA THERMAL INSULATION MATERIALS MARKET IN 2030

- FIGURE 16 GLASS MICROSPHERES SEGMENT TO ACCOUNT FOR LARGER SHARE OF SUBSEA THERMAL INSULATION MATERIALS MARKET IN 2030

- FIGURE 17 COUNTRIES IN REST OF ASIA PACIFIC TO REGISTER HIGHEST CAGRS IN SUBSEA THERMAL INSULATION MATERIALS MARKET DURING FORECAST PERIOD

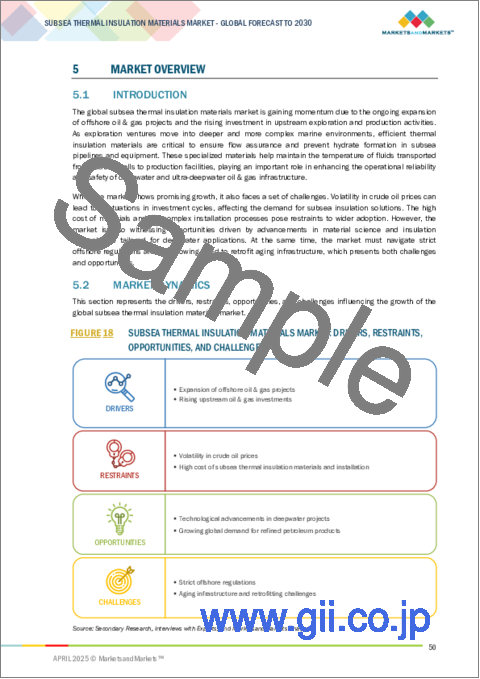

- FIGURE 18 SUBSEA THERMAL INSULATION MATERIALS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 19 NUMBER OF OIL & GAS EXTRACTION PROJECTS, BY REGION, 2016-2024

- FIGURE 20 OIL & GAS DISCOVERIES (MILLION BARRELS OF OIL EQUIVALENT), BY COUNTRY, 2023 & 2024

- FIGURE 21 EXTRACTABLE OIL & GAS VOLUMES FROM DISCOVERIES, APPROVALS, AND STARTUP (BBOE), 2024

- FIGURE 22 TEN-YEAR AVERAGE OF OFFSHORE DISCOVERY SHARE (PERCENTAGE OF TOTAL COUNT), 1950-2020

- FIGURE 23 UPSTREAM OIL & GAS CAPEX FORECAST, 2019-2030 (USD BILLION-NOMINAL)

- FIGURE 24 CRUDE OIL PRICES, 1968-2024 (USD/BARREL)

- FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 SUBSEA THERMAL INSULATION MATERIALS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 27 SUBSEA THERMAL INSULATION MATERIALS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 28 AVERAGE SELLING PRICE TREND OF SUBSEA THERMAL INSULATION MATERIALS OFFERED BY KEY PLAYERS, BY APPLICATION, 2024 (USD/TON)

- FIGURE 29 AVERAGE SELLING PRICE TREND OF SUBSEA THERMAL INSULATION MATERIALS, BY REGION, 2021-2024 (USD/TON)

- FIGURE 30 IMPORT DATA FOR HS CODE 392690-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 31 EXPORT DATA FOR HS CODE 392690-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 32 LIST OF MAJOR PATENTS APPLIED AND GRANTED RELATED TO SUBSEA THERMAL INSULATION MATERIALS, 2015-2024

- FIGURE 33 MAJOR PATENTS APPLIED AND GRANTED RELATED TO SUBSEA THERMAL INSULATION MATERIALS, BY COUNTRY/REGION, 2015-2024

- FIGURE 34 SUBSEA THERMAL INSULATION MATERIALS MARKET: IMPACT OF AI/GEN AI

- FIGURE 35 SUBSEA THERMAL INSULATION MATERIALS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 36 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY APPLICATIONS

- FIGURE 37 KEY BUYING CRITERIA FOR MAJOR APPLICATIONS

- FIGURE 38 POLYURETHANE SEGMENT TO HOLD LARGEST MARKET SHARE IN 2025

- FIGURE 39 GLASS MICROSPHERES SEGMENT TO HOLD LARGER MARKET SHARE IN 2025

- FIGURE 40 DIRECT INSULATION & PIPE COVERS SEGMENT TO HOLD LARGEST MARKET SHARE IN 2025

- FIGURE 41 SAUDI ARABIA TO BE FASTEST-GROWING MARKET FOR SUBSEA THERMAL INSULATION MATERIALS DURING FORECAST PERIOD

- FIGURE 42 EUROPE TO ACCOUNT FOR LARGEST SHARE OF SUBSEA THERMAL INSULATION MARKET IN 2025

- FIGURE 43 NORTH AMERICA: SUBSEA THERMAL INSULATION MATERIALS MARKET SNAPSHOT

- FIGURE 44 EUROPE: SUBSEA THERMAL INSULATION MATERIALS MARKET SNAPSHOT

- FIGURE 45 SUBSEA THERMAL INSULATION MATERIALS MARKET: REVENUE ANALYSIS OF TOP FOUR PLAYERS, 2020-2024 (USD BILLION)

- FIGURE 46 SUBSEA THERMAL INSULATION MATERIALS MARKET SHARE ANALYSIS, 2024

- FIGURE 47 SUBSEA THERMAL INSULATION MATERIALS MARKET: COMPANY VALUATION (USD BILLION), 2025

- FIGURE 48 SUBSEA THERMAL INSULATION MATERIALS MARKET: FINANCIAL MATRIX (EV/EBITDA), 2025

- FIGURE 49 SUBSEA THERMAL INSULATION MATERIALS MARKET: YEAR-TO-DATE PRICE AND FIVE-YEAR STOCK BETA, 2025

- FIGURE 50 SUBSEA THERMAL INSULATION MATERIALS MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 51 SUBSEA THERMAL INSULATION MATERIALS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 52 SUBSEA THERMAL INSULATION MATERIALS MARKET: COMPANY FOOTPRINT

- FIGURE 53 SUBSEA THERMAL INSULATION MATERIALS MARKET: COMPANY EVALUATION MATRIX (SMES), 2024

- FIGURE 54 ASPEN AEROGELS, INC.: COMPANY SNAPSHOT

- FIGURE 55 CABOT CORPORATION: COMPANY SNAPSHOT

- FIGURE 56 KINGSPAN GROUP: COMPANY SNAPSHOT

- FIGURE 57 TENARIS S.A.: COMPANY SNAPSHOT

- FIGURE 58 PERMA-PIPE INTERNATIONAL HOLDINGS, INC.: COMPANY SNAPSHOT

The subsea thermal insulation materials market is expected to reach USD 316.6 million by 2030 from USD 256.7 million in 2025, at a CAGR of 4.3% during the forecast period. Energy companies are increasingly shifting their operations to deepwater offshore environments, necessitating precise thermal management of subsea pipelines. This is crucial to mitigate hydrate formation, which poses a significant risk to production continuity. Conducting safe and efficient operations in these challenging conditions demands the use of reliable thermal insulation materials that can withstand extreme underwater environments. Advancements in materials science and insulation technologies have led to the development of high-performance materials capable of enduring harsh subsea conditions. These technological enhancements not only improve safety mechanisms but also extend the operational lifespan of underwater installations. As offshore exploration and production activities expand globally, these innovations are pivotal in driving market growth during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) Volume (Tons) |

| Segments | Type, Filler Type, Application, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

"Polypropylene to be second fastest-growing segment in subsea thermal insulation materials market"

Polypropylene is projected to experience the second-highest growth rate in the market, driven by its superior performance attributes and cost-effectiveness, particularly in deepwater applications. This polymer exhibits an exceptional balance of thermal insulation and mechanical strength while demonstrating resistance to water absorption, making it suitable for subsea pipeline and equipment protection under extremely cold and high-pressure environments. Economically, polypropylene offers a competitive alternative to higher-end insulation materials. As offshore oil and gas ventures extend into greater depths, there is a pressing need for both reliable and cost-efficient insulation solutions that meet stringent performance criteria. This trend is anticipated to significantly enhance the demand for polypropylene in the industry.

"Pipe-in-pipe to be second fastest-growing segment in subsea thermal insulation materials market"

The pipe-in-pipe (PiP) application is projected to be the second fastest-growing segment within the market, attributed to its superior thermal efficiency, which is particularly suited for deepwater and ultra-deepwater applications. The PiP system incorporates a co-axial design where a larger inner pipe is encased by a smaller outer pipe, with insulation material filling the annular space. This configuration effectively preserves fluid temperatures across extensive subsea pipelines, significantly reducing the risk of flow disruption caused by hydrates and wax deposition. The escalating demand for PiP insulation systems is primarily driven by the industry's expansion into harsher environments that necessitate dependable, high-performance insulation solutions.

"Glass microspheres to be largest segment in subsea thermal insulation materials market"

Glass microspheres are projected to dominate the market due to their exceptional weight-saving potential, superior thermal insulation characteristics, and impressive compressive strength, making them well-suited for deepwater and ultra-deepwater applications. In the subsea sector, these small glass spheres play a crucial role in minimizing heat loss from insulation coatings, helping sustain the operational temperatures of oil and gas pipelines and equipment in high-pressure underwater environments.

"Middle East & Africa to be second fastest-growing regional market for subsea thermal insulation materials"

The Middle East & Africa is emerging as the second fastest-growing market for subsea thermal insulation materials, driven by accelerating oil & gas exploration activities in deep and ultra-deep offshore regions. Countries like Angola, Nigeria, and Namibia are intensifying their offshore project development efforts to access previously untapped reservoirs, while Saudi Arabia and the UAE are expanding their offshore operations to enhance production capabilities. As subsea projects progress into increasingly challenging water depths, the demand for effective insulation materials to ensure optimal pipeline performance has risen substantially. The enhancement of offshore field discoveries and increased foreign investment in Africa's maritime zones are paving the way for significant advancements in subsea infrastructure development. Ongoing regional pipeline initiatives and the need for insulation solutions tailored to endure hot climates and extreme underwater conditions are driving robust market demand for subsea thermal insulation materials across the Middle East & Africa. This convergence of exploration activity and technological innovation marks a pivotal moment for the subsea materials market in the region.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Aspen Aerogels, Inc. (US), Cabot Corporation (US), AIS (UK), Tenaris S.A. (Luxembourg), Vipo AS (Norway), and Kingspan Group (Ireland), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the subsea thermal insulation materials market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the subsea thermal insulation materials market based on type (polyurethane, polypropylene, silicone rubber, epoxy, aerogel, EPDM, and other types), filler type (glass microspheres and other filler types), application (pipe-in-pipe, direct insulation & pipe covers, equipment, field joints, and other applications), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the subsea thermal insulation materials market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, expansions, and acquisitions, associated with the subsea thermal insulation materials market.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall subsea thermal insulation materials market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (Expansion of offshore oil & gas projects), restraints (Volatility in crude oil prices), opportunities (Technological advancements in deepwater projects), and challenges (Aging infrastructure and retrofitting challenges).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the subsea thermal insulation materials market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the subsea thermal insulation materials market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the subsea thermal insulation materials market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Aspen Aerogels, Inc. (US), Cabot Corporation (US), AIS (UK), Tenaris S.A. (Luxembourg), Vipo AS (Norway), and Kingspan Group (Ireland).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 BASE NUMBER CALCULATION

- 2.3.1 SUPPLY-SIDE ANALYSIS

- 2.4 MARKET FORECAST APPROACH

- 2.4.1 SUPPLY SIDE

- 2.4.2 DEMAND SIDE

- 2.5 DATA TRIANGULATION

- 2.6 FACTOR ANALYSIS

- 2.7 RESEARCH ASSUMPTIONS

- 2.8 RESEARCH LIMITATIONS

- 2.9 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SUBSEA THERMAL INSULATION MATERIALS MARKET

- 4.2 EUROPE SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE AND COUNTRY

- 4.3 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE

- 4.4 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION

- 4.5 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE

- 4.6 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Expansion of offshore oil & gas projects

- 5.2.1.2 Rising upstream oil & gas investments

- 5.2.2 RESTRAINTS

- 5.2.2.1 Volatility in crude oil prices

- 5.2.2.2 High cost of subsea thermal insulation materials and installation

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Technological advancements in deepwater projects

- 5.2.3.2 Growing global demand for refined petroleum products

- 5.2.4 CHALLENGES

- 5.2.4.1 Strict offshore regulations

- 5.2.4.2 Aging infrastructure and retrofitting challenges

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 REGULATORY LANDSCAPE

- 5.6.1 REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- 5.6.2 KEY REGULATIONS

- 5.6.2.1 ISO 12736 wet thermal insulation systems

- 5.6.2.2 ISO 9001:2015

- 5.6.2.3 ISO 14001

- 5.6.2.4 ISO 45001:2018

- 5.6.2.5 API RP 17A

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION, 2024

- 5.7.2 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2024

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 392690)

- 5.8.2 EXPORT SCENARIO (HS CODE 392690)

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Different approaches for insulated flowline in deepwater operations

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Electrically heat-traced flowline (EHTF) technology

- 5.9.2.2 Direct electrical heating (DEH) technology

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Pipeline bundle technology

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.10.1 INTRODUCTION

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 SUBSEA INSULATION FOR HTHP SURF STRUCTURES IN BRAZIL

- 5.11.2 ENHANCEMENT OF OFFSHORE PIPELINE THERMAL PERFORMANCE THROUGH SUPER-INSULATION ASSESSMENT

- 5.11.3 REMOTE APPLICATION OF NEXT-GENERATION SUBSEA MANIFOLD INSULATION IN AUSTRALIA

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 IMPACT OF AI/GEN AI ON SUBSEA THERMAL INSULATION MATERIALS MARKET

- 5.13.1 INTRODUCTION

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF SUPPLIERS

- 5.14.4 BARGAINING POWER OF BUYERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 MACROECONOMIC ANALYSIS

- 5.16.1 INTRODUCTION

- 5.16.2 GDP TRENDS AND FORECASTS

- 5.17 IMPACT OF 2025 US TARIFF ON SUBSEA THERMAL INSULATION MATERIALS MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.3.1 Increased raw material costs

- 5.17.3.2 Increased manufacturing costs and supply chain challenges

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 US

- 5.17.4.2 Europe

6 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY TYPE

- 6.1 INTRODUCTION

- 6.2 POLYURETHANE

- 6.2.1 CORROSION PROTECTION AND LONG SERVICE LIFE IN OFFSHORE APPLICATIONS TO DRIVE DEMAND

- 6.3 POLYPROPYLENE

- 6.3.1 MULTILAYER CONFIGURATIONS AND EXCELLENT PERFORMANCE IN OFFSHORE PIPELINE PROJECTS TO PROPEL MARKET

- 6.4 SILICONE RUBBER

- 6.4.1 INNOVATIONS IN SILICONE RUBBER FOR SUBSEA APPLICATIONS TO FUEL DEMAND

- 6.5 EPOXY

- 6.5.1 HIGH DURABILITY AND PERFORMANCE IN DEEPWATER OIL & GAS THERMAL INSULATION TO FUEL MARKET GROWTH

- 6.6 AEROGEL

- 6.6.1 GROWING ROLE OF AEROGEL IN SUBSEA THERMAL INSULATION TO DRIVE MARKET

- 6.7 OTHER TYPES

- 6.8 USE OF DICYCLOPENTADIENE (DCPD)

- 6.8.1 DICYCLOPENTADIENE IN SUBSEA APPLICATIONS

7 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY FILLER TYPE

- 7.1 INTRODUCTION

- 7.2 GLASS MICROSPHERES

- 7.2.1 ADVANCEMENTS IN HOLLOW GLASS MICROSPHERE TECHNOLOGY FOR SUBSEA APPLICATIONS TO DRIVE MARKET

- 7.3 OTHER FILLER TYPES

8 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 PIPE-IN-PIPE

- 8.2.1 INCREASE IN DEEPWATER AND ULTRA-DEEPWATER PROJECTS TO DRIVE MARKET

- 8.3 DIRECT INSULATION & PIPE COVERS

- 8.3.1 RISING DEMAND FOR INNOVATIVE WET INSULATION MATERIALS TO PROPEL MARKET

- 8.4 EQUIPMENT

- 8.4.1 GROWING DEMAND FOR PROTECTING SUBSEA COMPONENTS TO DRIVE MARKET

- 8.5 FIELD JOINTS

- 8.5.1 ABILITY TO PROTECT PIPELINES AGAINST CORROSION, UV EXPOSURE, AND MECHANICAL STRESSES TO DRIVE DEMAND

- 8.6 OTHER APPLICATIONS

9 SUBSEA THERMAL INSULATION MATERIALS MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 US

- 9.2.1.1 Expanding offshore operations in Gulf of America to propel market

- 9.2.2 CANADA

- 9.2.2.1 Growing offshore oil production to drive market

- 9.2.3 MEXICO

- 9.2.3.1 Booming oil & gas industry to fuel demand

- 9.2.1 US

- 9.3 ASIA PACIFIC

- 9.3.1 CHINA

- 9.3.1.1 Increased production targets and deepwater projects of CNOOC to drive demand

- 9.3.2 INDIA

- 9.3.2.1 Rising offshore domestic oil & gas production while decreasing dependency on energy imports to drive market

- 9.3.3 JAPAN

- 9.3.3.1 Ongoing technological advancements and strategic investments to create growth opportunities

- 9.3.4 SOUTH KOREA

- 9.3.4.1 Rising investments in development of advanced materials and technologies to propel market

- 9.3.5 REST OF ASIA PACIFIC

- 9.3.1 CHINA

- 9.4 EUROPE

- 9.4.1 RUSSIA

- 9.4.1.1 Expanding energy industry to drive demand

- 9.4.2 GERMANY

- 9.4.2.1 Stringent environmental regulations and sustainability goals to fuel demand

- 9.4.3 FRANCE

- 9.4.3.1 Commitment to sustainable energy practices and stringent environmental regulations to boost demand

- 9.4.4 UK

- 9.4.4.1 New offshore developments and energy security initiatives to fuel market growth

- 9.4.5 SPAIN

- 9.4.5.1 Booming energy industry to drive demand

- 9.4.6 ITALY

- 9.4.6.1 Advancing offshore energy landscape to accelerate demand

- 9.4.7 REST OF EUROPE

- 9.4.1 RUSSIA

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 GCC COUNTRIES

- 9.5.1.1 Saudi Arabia

- 9.5.1.1.1 Vision 2030 to drive market

- 9.5.1.2 UAE

- 9.5.1.2.1 Expanding offshore oil & gas industry to drive market

- 9.5.1.3 Rest of GCC Countries

- 9.5.1.1 Saudi Arabia

- 9.5.2 SOUTH AFRICA

- 9.5.2.1 Growing focus on offshore oil & gas exploration and expansion of subsea infrastructure to propel market

- 9.5.3 REST OF MIDDLE EAST & AFRICA

- 9.5.1 GCC COUNTRIES

- 9.6 SOUTH AMERICA

- 9.6.1 BRAZIL

- 9.6.1.1 Dominance of offshore oil & gas industry to drive market

- 9.6.2 ARGENTINA

- 9.6.2.1 Growing offshore oil exploration to fuel demand

- 9.6.3 REST OF SOUTH AMERICA

- 9.6.1 BRAZIL

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 10.3 REVENUE ANALYSIS

- 10.4 MARKET SHARE ANALYSIS

- 10.5 COMPANY VALUATION AND FINANCIAL METRICS

- 10.6 BRAND/PRODUCT COMPARISON

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.7.5.1 Company footprint

- 10.7.5.2 Region footprint

- 10.7.5.3 Type footprint

- 10.7.5.4 Filler type footprint

- 10.7.5.5 Application footprint

- 10.8 COMPANY EVALUATION MATRIX: SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING: SMES, 2024

- 10.8.5.1 Detailed list of key SMEs

- 10.8.5.2 Competitive benchmarking of key SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 DEALS

- 10.9.2 EXPANSIONS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 ASPEN AEROGELS, INC.

- 11.1.1.1 Business overview

- 11.1.1.2 Products offered

- 11.1.1.3 MnM view

- 11.1.1.3.1 Key strengths/Right to win

- 11.1.1.3.2 Strategic choices

- 11.1.1.3.3 Weaknesses/Competitive threats

- 11.1.2 CABOT CORPORATION

- 11.1.2.1 Business overview

- 11.1.2.2 Products offered

- 11.1.2.3 MnM view

- 11.1.2.3.1 Key strengths/Right to win

- 11.1.2.3.2 Strategic choices

- 11.1.2.3.3 Weaknesses/Competitive threats

- 11.1.3 AIS

- 11.1.3.1 Business overview

- 11.1.3.2 Products offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Deals

- 11.1.3.3.2 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths/Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses/Competitive threats

- 11.1.4 KINGSPAN GROUP

- 11.1.4.1 Business overview

- 11.1.4.2 Products offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Deals

- 11.1.4.4 MnM view

- 11.1.4.4.1 Key strengths/Right to win

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses/Competitive threats

- 11.1.5 TENARIS S.A.

- 11.1.5.1 Business overview

- 11.1.5.2 Products offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Deals

- 11.1.5.4 MnM view

- 11.1.5.4.1 Key strengths/Right to win

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses/Competitive threats

- 11.1.6 VIPO AS

- 11.1.6.1 Business overview

- 11.1.6.2 Products offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Deals

- 11.1.6.4 MnM view

- 11.1.7 BALMORAL GROUP

- 11.1.7.1 Business overview

- 11.1.7.2 Products offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Expansions

- 11.1.7.4 MnM view

- 11.1.8 PERMA-PIPE INTERNATIONAL HOLDINGS, INC.

- 11.1.8.1 Business overview

- 11.1.8.2 Products offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Expansions

- 11.1.8.4 MnM view

- 11.1.9 LFM ENERGY

- 11.1.9.1 Business overview

- 11.1.9.2 Products offered

- 11.1.9.3 MnM view

- 11.1.10 BEERENBERG GROUP

- 11.1.10.1 Business overview

- 11.1.10.2 Products offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Deals

- 11.1.10.4 MnM view

- 11.1.1 ASPEN AEROGELS, INC.

- 11.2 OTHER PLAYERS

- 11.2.1 ENGINEERED SYNTACTIC SYSTEMS

- 11.2.2 V.I.P. VERNICIATURA INDUSTRIALE PESARESE SRL

- 11.2.3 DOW

- 11.2.4 SIAO PETROLEO S.A.

- 11.2.5 ACOUSTIC POLYMERS LTD.

- 11.2.6 AKZONOBEL N.V.

- 11.2.7 HUNTSMAN INTERNATIONAL LLC

- 11.2.8 BASF SE

- 11.2.9 ROCKWOOL GROUP

- 11.2.10 EXXON MOBIL CORPORATION

- 11.2.11 WACKER CHEMIE AG

- 11.2.12 THERMAL MITIGATION TECHNOLOGIES, LLC

- 11.3 END USERS

- 11.3.1 SAIPEM SPA

- 11.3.2 SUBSEA 7 S.A.

- 11.3.3 TECHNIPFMC PLC

- 11.3.4 MCDERMOTT

- 11.3.5 BAKER HUGHES COMPANY

- 11.3.6 HALLIBURTON

- 11.3.7 NOV INC.

- 11.3.8 PRYSMIAN GROUP

- 11.3.9 JOHN WOOD GROUP PLC

- 11.3.10 ONESUBSEA

- 11.3.11 SAPURA ENERGY BERHAD

- 11.3.12 FUGRO

- 11.3.13 ENBRIDGE INC.

- 11.3.14 L&T ENERGY HYDROCARBON (LTEH)

- 11.3.15 OCEANEERING INTERNATIONAL, INC.

12 ADJACENT AND RELATED MARKET

- 12.1 INTRODUCTION

- 12.2 OFFSHORE PIPELINE MARKET

- 12.2.1 MARKET DEFINITION

- 12.2.2 MARKET OVERVIEW

- 12.2.3 OFFSHORE PIPELINE MARKET, BY DIAMETER

- 12.2.4 OFFSHORE PIPELINE MARKET, BY LINE TYPE

- 12.2.5 OFFSHORE PIPELINE MARKET, BY PRODUCT

- 12.2.6 OFFSHORE PIPELINE MARKET, BY REGION

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS