軍用プラットフォームの世界市場:タイプ別、技術別、顧客別、地域別 - 予測(~2032年)

Military Platforms Market by Type (Fighter, Transport, Special Mission, Helicopter, MBT, APC, IFV, MRAP, Aircraft Carrier, Destroyer, Submarine, Corvette, Frigate, Patrol Vessel), Technology (Legacy, Next-Gen), Customer, Region - Global Forecast To 2032- 発行日

- ページ情報

- 英文 466 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1963144

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

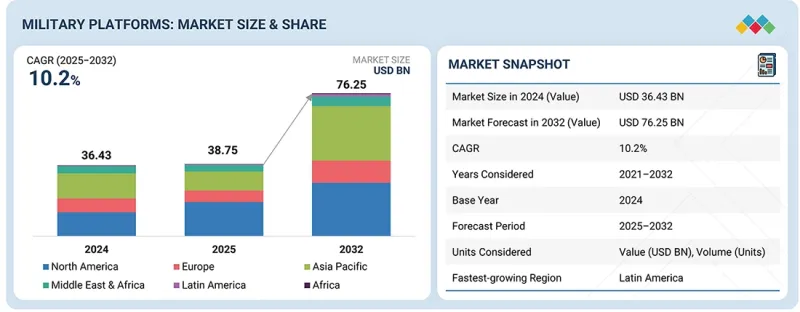

世界の軍用プラットフォームの市場規模は、2025年の387億5,000万米ドルから2032年までに約762億5,000万米ドルに達すると予測され、予測期間にCAGRで約10.2%の成長が見込まれています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2021年~2032年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2032年 |

| 単位 | 10億米ドル |

| セグメント | タイプ、技術、地域 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

市場の成長は、主に進行中の防衛近代化活動、老朽化した陸上・海上・航空プラットフォームの更新、高性能軍用システムへの持続的な投資によって促進されています。艦隊の急速な拡大というよりも、プラットフォームの複雑化、単価の上昇、主要な防衛軍全体における先進のミッションシステム、生存性機能、相互運用性要件の統合によって成長が形作られています。

「タイプ別では、軍用艦船が予測期間にもっとも高い成長率を示す見込みです。」

海上保安、沿岸監視、排他的経済水域(EEZ)保護への注目の高まりにより、軍用哨戒艇がプラットフォームカテゴリの中でもっとも速い成長を記録すると予測されます。海軍は非対称的脅威、海上国境取締、海賊行為、密輸、グレーゾーン作戦への対応のため、沿岸哨戒艦、高速哨戒艇、沿岸警備プラットフォームの優先度をますます高めています。

大型の水上戦闘艦と比較し、哨戒艇は建造期間が短く、調達・運用コストが低く、運用上の可用性が高いため、艦隊の迅速な拡充に有利です。特に新興海軍勢力は、高価な主力艦の財政的・兵站的負荷を伴わずに海上プレゼンスを強化するために、哨戒艇への投資を加速させています。この運用上の重要性、手頃な価格、拡張性の組み合わせが、哨戒艇の力強い成長見通しを支えています。

「技術別では、旧式プラットフォームが予測期間に最大の市場シェアを占めると見込まれます。」

旧式軍用プラットフォームは、広範な展開、運用成熟度、確立された業界エコシステムに支えられ、市場で最大のシェアを維持すると予測されます。防衛機関は、実績ある性能、予測可能なライフサイクルコスト、既存インフラやドクトリンとの互換性から、旧式の航空機・車両・艦艇への依存を続けています。このセグメントにおける支出は、抜本的な再設計ではなく、主にアビオニクスのアップグレード、推進システムの改良、構造補強、ミッションシステムの強化といった段階的な近代化に充てられています。旧式プラットフォームは、堅牢なグローバルサプライチェーンと長期的な維持管理フレームワークの恩恵も受けており、技術的リスクを低減し、高い稼働率を保証しています。次世代の先進プラットフォームが戦略的な注目を集めている一方で、旧式システムは即応態勢と戦力継続性の維持において依然として中核的役割を担っており、軍用プラットフォーム市場全体における支配的な地位を確固たるものとしています。

「ラテンアメリカが予測期間にもっとも高い成長率を示す見込みです。」

ラテンアメリカは、比較的低いベースからの防衛投資の増加と、艦隊の更新と近代化への注目の高まりにより、2025年~2032年に軍用プラットフォーム市場でもっとも速い成長を記録すると予測されます。同地域の成長は、作戦準備態勢の向上と既存アセットの耐用年数延長を目的とした、軍用車両、航空機、海上プラットフォームの選択的調達によって支えられています。大規模な防衛市場と比較するとプラットフォーム全体の数量は依然として限定的ですが、支出強度の向上と近代化が主導する調達により、地域全体での金額成長、部門横断的な運用上の採用、そして無人能力開発に対する政府の強い重視が促進されています。

当レポートでは、世界の軍用プラットフォーム市場について調査分析し、主な促進要因と抑制要因、製品開発とイノベーション、競合情勢に関する知見を提供しています。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要な知見

- 軍用プラットフォーム市場の企業にとって魅力的な機会

- 軍用プラットフォーム市場:タイプ別

- 軍用プラットフォーム市場:技術別

- 軍用プラットフォーム市場:顧客別

第4章 市場の概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズとホワイトスペース

- 限られたアップグレードの柔軟性とモジュール統合

- 業界の拡張性と急増する生産能力

- ライフサイクル上の可用性と維持の柔軟性

- 相互接続された市場と部門横断的な機会

- 民間航空宇宙、商業航空

- 陸上輸送、重工業、自動車システム

- 商船建造、オフショアインフラ

- Tier 1/2/3企業の戦略的動き

- 総所有コスト

- 軍用艦船の総所有コスト

- 軍用車両の総所有コスト

- 軍用航空機の総所有コスト

- ビジネスモデル

- 軍用艦船:ビジネスモデル

- 軍用車両:ビジネスモデル

- 軍用航空機:ビジネスモデル

- 部品表

- 軍用艦船の部品表

- 軍用車両の部品表

- 軍用航空機の部品表

- 機体・構造材料

- 推進システム

- アビオニクス・電子機器

- 兵器システム

- センサー・電力システム

- 着陸装置・油圧システム

- その他のシステム

- 投資と資金調達のシナリオ

第5章 業界動向

- マクロ経済の見通し

- 北米

- 欧州

- アジア太平洋

- 中東

- その他の地域

- バリューチェーン分析

- エコシステム分析

- 著名企業

- 民間企業・中小企業

- エンドユーザー

- 価格設定の分析

- 貿易分析

- 艦船:輸入シナリオ(HSコード89)

- 艦船:輸出シナリオ(HSコード89)

- 軍用車両:輸出シナリオ(HSコード8710)

- 軍用車両:輸入シナリオ(HSコード8710)

- 軍用航空機:輸入シナリオ(HSコード8802)

- 軍用航空機:輸出シナリオ(HSコード8802)

- カスタマービジネスに影響を与える動向と混乱

- ケーススタディ分析

- 2025年の米国関税の影響

- 主な関税率

- 価格の影響の分析

- 国/地域への影響

- さまざまなプラットフォームへの影響

第6章 顧客情勢と購買行動

- 意思決定プロセス

- バイヤーのステークホルダーと購入評価基準

- 採用障壁と内部課題

- さまざまな最終用途産業のアンメットニーズ

第7章 持続可能性と規制情勢

- 地域の規制とコンプライアンス

- 規制機関、政府機関、その他の組織

- 業界標準

- 持続可能性への取り組み

- 炭素の影響の削減

- エコ用途

- 認証、ラベル、環境基準

第8章 技術の進歩、AIによる影響、特許、イノベーション、将来の用途

- 主要技術

- 先進の推進・動力システム

- ネットワーク中心の指揮・統制・通信システム

- 先進のセンサーとセンサーフュージョン

- デジタルアーキテクチャとオープンシステム

- 補完技術

- 分散型測位・航法・タイミング(PNT)システム

- 大容量オンボードデータストレージ・エッジ処理

- 先進の電力管理とエネルギー配分

- テクノロジーロードマップ

- 軍用艦船

- 軍用車両

- 軍用航空機

- 特許分析

- 将来の用途

- AI/生成AIの影響

- 主なユースケースと市場の将来性

- ベストプラクティス

- AI導入のケーススタディ

- 相互接続されたエコシステムと市場企業への影響

- AI/生成AI導入に対するクライアントの準備状況

- メガトレンドの影響

- ビッグデータと海洋インテリジェンスプラットフォーム

- クラウドとエッジコンピューティングの統合

- 生成AIとデジタルツインエコシステム

- IoT対応の防衛接続性

第9章 軍用プラットフォーム市場:プラットフォームタイプ別

- 軍用航空機

- 軍用艦船

- 軍用車両

第10章 軍用プラットフォーム市場:顧客別

- 陸軍

- 海軍

- 空軍

第11章 軍用プラットフォーム市場:技術別

- 旧式

- 次世代

第12章 軍用プラットフォーム市場:地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- アジア太平洋

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アフリカ

- 中東

- GCC

- イスラエル

- トルコ

第13章 競合情勢

- 主要参入企業の戦略/強み(2021年~2025年)

- 収益分析

- 市場シェア分析

- ブランド/製品の比較

- 企業の評価と財務指標

- 企業の評価マトリクス:主要企業(2024年)

- 軍用航空機市場

- 軍用車両市場

- 軍用艦船市場

- 企業の概要:主要企業

- 企業の評価マトリクス:スタートアップ/中小企業(2024年)

- 競合シナリオ

第14章 企業プロファイル

- 主要企業

- BAE SYSTEMS

- LOCKHEED MARTIN

- HUNTINGTON INGALLS INDUSTRIES(HII)

- BOEING

- RHEINMETALL AG

- GENERAL DYNAMICS CORPORATION

- TEXTRON INC.

- SAAB AB

- LEONARDO S.P.A.

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- FINCANTIERI S.P.A.

- HD HYUNDAI HEAVY INDUSTRIES CO., LTD.

- HANWHA OCEAN CO., LTD.

- NAVAL GROUP

- RTX

- ST ENGINEERING

- THALES

- NORTHROP GRUMMAN

- ISRAEL AEROSPACE INDUSTRIES

- DASSAULT AVIATION

- AIRBUS

- その他の企業

- KALYANI STRATEGIC SYSTEMS LTD.

- MAHINDRA EMIRATES VEHICLE ARMOURING FZ LLC

- TATA ADVANCED SYSTEMS LIMITED

- INKAS ARMORED VEHICLE MANUFACTURING

- STREIT GROUP

- ARQUUS

- IVECO DEFENSE VEHICLES

- BRODOSPLIT SHIPYARD

- SEDEF SHIPBUILDING INC.

- DE HAVILLAND AIRCRAFT OF CANADA LIMITED

第15章 調査手法

第16章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 466 Pages

- 納期

- 即納可能