|

|

市場調査レポート

商品コード

1606234

煙感知器の世界市場:感知器タイプ別、電源別 - 予測(~2029年)Smoke Detector Market by Detector Type (Photoelectric Smoke Detectors, Ionization, Dual-sensor Smoke Detectors, Aspirating, Duct Smoke Detectors, Beam Detectors), Power Source (Wired Smoke Detectors, Wireless Smoke Detectors) - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 煙感知器の世界市場:感知器タイプ別、電源別 - 予測(~2029年) |

|

出版日: 2024年11月28日

発行: MarketsandMarkets

ページ情報: 英文 265 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界の煙感知器の市場規模は、2024年までに26億8,000万米ドル、2029年までに37億6,000万米ドルに達すると予測され、成長率は7.0%です。

主な促進要因は、住宅、商業、工業部門における火災安全意識の高まり、各セグメントで実施されている厳格な火災安全規制、スマート煙感知器とloT接続の新動向などです。無線煙感知器の使用の増加や世界の建設活動の増加が、煙感知器市場の需要をさらに押し上げています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 単位 | 10億米ドル |

| セグメント | 感知器タイプ、電源、サービス、最終用途産業、地域 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

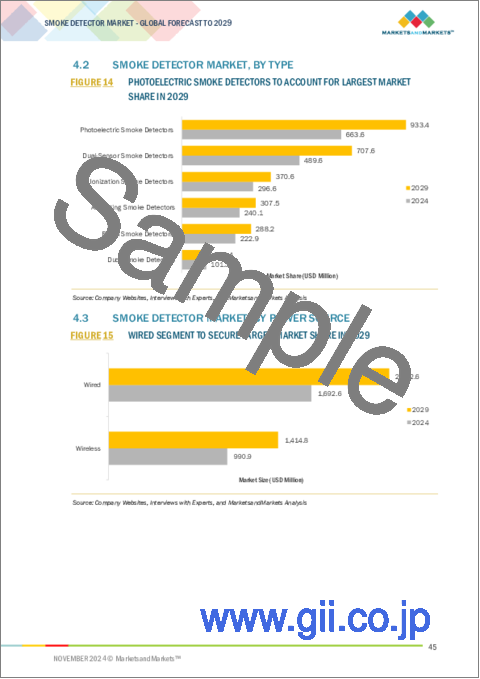

「予測期間に有線煙感知器が大きな市場シェアを維持します。」

有線煙感知器は主にその高い信頼性と一貫性により、予測期間に煙感知器市場で大きな市場シェアを維持する見込みです。有線煙感知器は通常、建物の電気システムにハードワイヤーで接続されるため、電池に頼ることなく継続的に機能し、商業、工業、大規模住宅用途で普及しています。有線煙感知器にはバックアップ電源設備があるため、停電時の安全性が確保されます。ビルオートメーションシステムや厳しい火災安全を求めるシステム内での統合が容易になり、厳しい火災感知ニーズがある危険な環境での需要が高まります。

「光電式煙感知器が火災感知能力の強化により最大の市場シェアを占めます。」

予測期間に光電式煙感知器が最大の市場シェアを占めると予測されます。光電式煙感知器は、住宅や商業施設で一般的な、ゆっくりとくすぶり続ける火災の感知に優れています。光電式煙感知器は、光に反応するセンサーを使って煙の粒子を検出するため、イオン化式煙感知器よりも火災の早期発見において信頼性が高いです。火災安全に対する意識が高まり、規制や規制が厳しくなり、新築だけでなく改築にも広く応用されるようになったことで、その使用は増加しています。光電技術の進歩は効率と信頼性を向上させるため、市場においてより恒久的な存在となっています。

「予測期間に工業部門が最大の市場シェアを占める見込み」

工業部門が煙感知器市場を独占すると予測されます。これは主に、火災が財産に深刻な損害を与え、生産を停止させ、さらには人命の損失につながる可能性がある工業施設がもっとも重要であるためです。工業施設に煙感知器の設置を義務付ける政府の厳しい規制が、この市場を牽引しています。また、可燃性物質を扱う工業プロセスでは、信頼性が高く精巧な煙感知器を必要とする複雑性が増しているため、工業市場は特に高性能ソリューションにとって、主要部門であり続けています。

「規制遵守と技術の進歩により北米が煙感知器市場で最大のシェアを獲得します。」

北米は、厳しい火災安全規制、火災リスク意識の高まり、技術の高い採用率に後押しされ、予測期間を通じて煙感知器市場をリードします。北米では住宅や商業施設の建設が活発化しており、信頼性の高い煙感知ソリューションの需要が高まっています。建物に煙感知器を設置する政府の取り組みや建築基準法が市場の成長を支えています。有名メーカーの存在や、スマートシステムや相互接続システムなどの煙感知技術の絶え間ない革新が北米を煙感知器市場の主要地域としており、さまざまな用途で多くの安全対策が確保されています。

当レポートでは、世界の煙感知器市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 煙感知機市場で活動する企業にとって魅力的な機会

- 煙感知機市場:タイプ別

- 煙感知機市場:電源別

- 煙感知機市場:サービス別

- 煙感知機市場:エンドユーザー別

- 北米の煙感知器市場:エンドユーザー別、国別

- 煙感知機市場:国別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 主要企業が提供する光電式煙感知器の参考価格(2023年)

- 煙感知器の平均販売価格の動向:タイプ別(2020年~2023年)

- 光電式煙感知器の平均販売価格の動向:地域別(2020年~2023年)

- 顧客ビジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ

- 技術分析

- 主要技術

- 隣接技術

- 補完技術

- ポーターのファイブフォース分析

- 主なステークホルダーと購入基準

- ケーススタディ分析

- 貿易分析

- 輸入シナリオ(HSコード8531)

- 輸出シナリオ(HSコード8531)

- 特許分析

- 主な会議とイベント(2025年~2026年)

- 規制情勢

- 規制機関、政府機関、その他の組織

- 標準

- 規制

- 煙感知機市場に対するAIの影響

- イントロダクション

- 煙感知機市場に対するAIの影響

- 主なユースケースと市場の可能性

第6章 煙感知器の流通チャネル

- イントロダクション

- オンライン

- オフライン

第7章 煙感知機市場:提供別

- イントロダクション

- 製品

- サービス

第8章 煙感知機市場:タイプ別

- イントロダクション

- 光電式煙感知器

- イオン化式煙感知器

- デュアルセンサー煙感知器

- ビーム煙感知器

- 吸引式煙感知器

- ダクト煙感知器

第9章 煙感知機市場:サービス別

- イントロダクション

- エンジニアリングサービス

- 設置・設計サービス

- メンテナンスサービス

- マネージドサービス

- その他のサービス

第10章 煙感知機市場:電源別

- イントロダクション

- 有線と無線の煙感知システムの比較

- 有線

- 無線

第11章 煙感知機市場:エンドユーザー別

- イントロダクション

- 商業

- 学術機関・機関

- 小売

- 医療

- ホスピタリティ

- BFSI

- 政府機関・オフィスビル

- 住宅

- 工業

- 石油・ガス、鉱業

- 輸送・ロジスティクス

- IT・通信

- 製造

- エネルギー・電力

- 医薬品

- その他の産業

第12章 煙感知機市場:地域別

- イントロダクション

- 北米

- 北米のマクロ経済の見通し

- 米国

- カナダ

- メキシコ

- 欧州

- 欧州のマクロ経済の見通し

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- アジア太平洋のマクロ経済の見通し

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- その他のアジア太平洋

- その他の地域

- その他の地域のマクロ経済の見通し

- 中東

- 南米

- アフリカ

第13章 競合情勢

- イントロダクション

- 主要参入企業の戦略/強み(2021年~2024年)

- 収益分析(2019年~2023年)

- 市場シェア分析(2023年)

- 企業の評価と財務指標(2024年)

- ブランド/製品の比較

- 企業の評価マトリクス:主要企業(2023年)

- 企業の評価マトリクス:スタートアップ/中小企業(2023年)

- 競合シナリオ

第14章 企業プロファイル

- 主要企業

- HONEYWELL INTERNATIONAL INC.

- JOHNSON CONTROLS INC.

- SIEMENS

- ROBERT BOSCH GMBH

- HOCHIKI CORPORATION

- CARRIER

- GENTEX CORPORATION

- RESIDEO TECHNOLOGIES INC.

- MIRCOM GROUP OF COMPANIES

- SCHNEIDER ELECTRIC

- ABB

- EMERSON ELECTRIC CO.

- EATON

- SECOM CO., LTD.

- その他の企業

- APOLLO FIRE DETECTORS

- FIKE

- CEASEFIRE INDUSTRIES PVT. LTD.

- SECURITON AG

- UNIVERSAL SECURITY INSTRUMENTS, INC.

- HEKATRON VERTRIEBS GMBH

- NETATMO

- ORR PROTECTION

- RAVEL GROUP OF COMPANIES

- GUARDIAN PROTECTION

- VIKING GROUP INC.

- VECTOR SECURITY, INC.

第15章 付録

List of Tables

- TABLE 1 SMOKE DETECTOR MARKET: RESEARCH ASSUMPTION

- TABLE 2 SMOKE DETECTOR MARKET: RISK ANALYSIS

- TABLE 3 SMOKE DETECTOR MARKET: ECOSYSTEM

- TABLE 4 INDICATIVE PRICING OF PHOTOELECTRIC SMOKE DETECTORS OFFERED BY KEY PLAYERS, 2023 (USD)

- TABLE 5 AVERAGE SELLING PRICE TREND OF SMOKE DETECTORS, BY TYPE, 2020-2023 (USD)

- TABLE 6 AVERAGE SELLING PRICE TREND OF PHOTOELECTRIC SMOKE DETECTORS, BY REGION, 2020-2023 (USD)

- TABLE 7 SMOKE DETECTOR MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 8 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS (%)

- TABLE 9 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- TABLE 10 IMPORT SCENARIO FOR HS CODE 8531-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 11 EXPORT SCENARIO FOR HS CODE 8531-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 12 LIST OF APPLIED/GRANTED PATENTS RELATED TO SMOKE DETECTOR MARKET, 2022-2024

- TABLE 13 SMOKE DETECTOR MARKET: LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 14 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 SMOKE DETECTOR MARKET: STANDARDS

- TABLE 19 SMOKE DETECTOR MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 20 SMOKE DETECTOR MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 21 SMOKE DETECTOR MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 22 SMOKE DETECTOR MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 23 SMOKE DETECTOR MARKET, BY TYPE, 2020-2023 (MILLION UNITS)

- TABLE 24 SMOKE DETECTOR MARKET, BY TYPE, 2024-2029 (MILLION UNITS)

- TABLE 25 PHOTOELECTRIC SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 26 PHOTOELECTRIC SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 27 IONIZATION SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 28 IONIZATION SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 29 DUAL-SENSOR SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 30 DUAL-SENSOR SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 31 BEAM SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 32 BEAM SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 33 ASPIRATING SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 34 ASPIRATING SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 35 DUCT SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 36 DUCT SMOKE DETECTORS: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 37 SMOKE DETECTOR MARKET, BY SERVICE, 2020-2023 (USD MILLION)

- TABLE 38 SMOKE DETECTOR MARKET, BY SERVICE, 2024-2029 (USD MILLION)

- TABLE 39 SERVICE: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 40 SERVICE: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 41 WIRED VS. WIRELESS SMOKE DETECTORS

- TABLE 42 SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 43 SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 44 WIRED: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 45 WIRED: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 46 WIRED: SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 47 WIRED: SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 48 WIRELESS: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 49 WIRELESS: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 50 WIRELESS: SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 51 WIRELESS: SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 52 SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 53 SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 54 COMMERCIAL: SMOKE DETECTOR MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 55 COMMERCIAL: SMOKE DETECTOR MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 56 SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2020-2023 (USD MILLION)

- TABLE 57 SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2024-2029 (USD MILLION)

- TABLE 58 COMMERCIAL: SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 59 COMMERCIAL: SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 60 COMMERCIAL: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 61 COMMERCIAL: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 62 COMMERCIAL: SMOKE DETECTOR MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 63 COMMERCIAL: SMOKE DETECTOR MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 64 COMMERCIAL: SMOKE DETECTOR MARKET FOR ACADEMIA & INSTITUTIONAL, BY REGION, 2020-2023 (USD MILLION)

- TABLE 65 COMMERCIAL: SMOKE DETECTOR MARKET FOR ACADEMIA & INSTITUTIONAL, BY REGION, 2024-2029 (USD MILLION)

- TABLE 66 COMMERCIAL: SMOKE DETECTOR MARKET FOR RETAIL, BY REGION, 2020-2023 (USD MILLION)

- TABLE 67 COMMERCIAL: SMOKE DETECTOR MARKET FOR RETAIL, BY REGION, 2024-2029 (USD MILLION)

- TABLE 68 COMMERCIAL: SMOKE DETECTOR MARKET FOR HEALTHCARE, 2020-2023 (USD MILLION)

- TABLE 69 COMMERCIAL: SMOKE DETECTOR MARKET FOR HEALTHCARE, BY REGION, 2024-2029 (USD MILLION)

- TABLE 70 COMMERCIAL: SMOKE DETECTOR MARKET FOR HOSPITALITY, 2020-2023 (USD MILLION)

- TABLE 71 COMMERCIAL: SMOKE DETECTOR MARKET FOR HOSPITALITY, 2024-2029 (USD MILLION)

- TABLE 72 COMMERCIAL: SMOKE DETECTOR MARKET FOR BFSI, BY REGION, 2020-2023 (USD MILLION)

- TABLE 73 COMMERCIAL: SMOKE DETECTOR MARKET FOR BFSI, BY REGION, 2024-2029 (USD MILLION)

- TABLE 74 COMMERCIAL: SMOKE DETECTOR MARKET FOR GOVERNMENT & OFFICE BUILDINGS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 75 COMMERCIAL: SMOKE DETECTOR MARKET FOR GOVERNMENT & OFFICE BUILDINGS, BY REGION, 2024-2029 (USD MILLION)

- TABLE 76 RESIDENTIAL: SMOKE DETECTOR MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 77 RESIDENTIAL: SMOKE DETECTOR MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 78 RESIDENTIAL: SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 79 RESIDENTIAL: SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 80 RESIDENTIAL: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 81 RESIDENTIAL SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 82 RESIDENTIAL: SMOKE DETECTOR MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 83 RESIDENTIAL: SMOKE DETECTOR MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 84 INDUSTRIAL: SMOKE DETECTOR MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 85 INDUSTRIAL: SMOKE DETECTOR MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 86 SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2020-2023 (USD MILLION)

- TABLE 87 SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2024-2029 (USD MILLION)

- TABLE 88 INDUSTRIAL: SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 89 INDUSTRIAL: SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 90 INDUSTRIAL: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 91 INDUSTRIAL: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 92 INDUSTRIAL: SMOKE DETECTOR MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 93 INDUSTRIAL SMOKE DETECTOR MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 94 INDUSTRIAL: SMOKE DETECTOR MARKET FOR OIL& GAS AND MINING, BY REGION, 2020-2023 (USD MILLION)

- TABLE 95 INDUSTRIAL: SMOKE DETECTOR MARKET FOR OIL& GAS AND MINING, BY REGION, 2024-2029 (USD MILLION)

- TABLE 96 INDUSTRIAL: SMOKE DETECTOR MARKET FOR TRANSPORTATION & LOGISTICS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 97 INDUSTRIAL: SMOKE DETECTOR MARKET FOR TRANSPORTATION & LOGISTICS, BY REGION, 2024-2029 (USD MILLION)

- TABLE 98 INDUSTRIAL: SMOKE DETECTOR MARKET FOR IT & TELECOMMUNICATIONS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 99 INDUSTRIAL: SMOKE DETECTOR MARKET FOR IT & TELECOMMUNICATIONS, BY REGION, 2024-2029 (USD MILLION)

- TABLE 100 INDUSTRIAL: SMOKE DETECTOR MARKET FOR MANUFACTURING, BY REGION, 2020-2023 (USD MILLION)

- TABLE 101 INDUSTRIAL: SMOKE DETECTOR MARKET FOR MANUFACTURING, BY REGION, 2024-2029 (USD MILLION)

- TABLE 102 INDUSTRIAL: SMOKE DETECTOR MARKET FOR ENERGY & POWER, BY REGION, 2020-2023 (USD MILLION)

- TABLE 103 INDUSTRIAL: SMOKE DETECTOR MARKET FOR ENERGY & POWER, BY REGION, 2024-2029 (USD MILLION)

- TABLE 104 INDUSTRIAL: SMOKE DETECTOR MARKET FOR PHARMACEUTICALS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 105 INDUSTRIAL: SMOKE DETECTOR MARKET FOR PHARMACEUTICALS, BY REGION, 2024-2029 (USD MILLION)

- TABLE 106 OTHER INDUSTRIES: SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 107 OTHER INDUSTRIES: SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 108 SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 109 SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 110 NORTH AMERICA: SMOKE DETECTOR MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 111 NORTH AMERICA: SMOKE DETECTOR MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 112 NORTH AMERICA: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 113 NORTH AMERICA: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 114 NORTH AMERICA: SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2020-2023 (USD MILLION)

- TABLE 115 NORTH AMERICA: SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2024-2029 (USD MILLION)

- TABLE 116 NORTH AMERICA: SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2020-2023 (USD MILLION)

- TABLE 117 NORTH AMERICA: SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2024-2029 (USD MILLION)

- TABLE 118 NORTH AMERICA: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 119 NORTH AMERICA: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 120 US: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 121 US: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 122 CANADA: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 123 CANADA: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 124 EUROPE: SMOKE DETECTOR MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 125 EUROPE: SMOKE DETECTOR MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 126 EUROPE: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 127 EUROPE: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 128 EUROPE: SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2020-2023 (USD MILLION)

- TABLE 129 EUROPE: SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2024-2029 (USD MILLION)

- TABLE 130 EUROPE: SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2020-2023 (USD MILLION)

- TABLE 131 EUROPE: SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2024-2029 (USD MILLION)

- TABLE 132 EUROPE: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 133 EUROPE: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 134 UK: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 135 UK: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 136 GERMANY: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 137 GERMANY: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 138 FRANCE: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 139 FRANCE: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 140 REST OF EUROPE: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 141 REST OF EUROPE: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 142 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 143 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 144 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 145 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 146 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2020-2023 (USD MILLION)

- TABLE 147 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2024-2029 (USD MILLION)

- TABLE 148 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2020-2023 (USD MILLION)

- TABLE 149 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2024-2029 (USD MILLION)

- TABLE 150 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 151 ASIA PACIFIC: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 152 ROW: SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 153 ROW: SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 154 ROW: SMOKE DETECTOR MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 155 ROW: SMOKE DETECTOR MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 156 ROW: SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2020-2023 (USD MILLION)

- TABLE 157 ROW: SMOKE DETECTOR MARKET, BY COMMERCIAL END USER, 2024-2029 (USD MILLION)

- TABLE 158 ROW: SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2020-2023 (USD MILLION)

- TABLE 159 ROW: SMOKE DETECTOR MARKET, BY INDUSTRIAL END USER, 2024-2029 (USD MILLION)

- TABLE 160 ROW: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2020-2023 (USD MILLION)

- TABLE 161 ROW: SMOKE DETECTOR MARKET, BY POWER SOURCE, 2024-2029 (USD MILLION)

- TABLE 162 MIDDLE EAST: SMOKE DETECTOR MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 163 MIDDLE EAST: SMOKE DETECTOR MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 164 GCC: SMOKE DETECTOR MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 165 GCC: SMOKE DETECTOR MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 166 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN SMOKE DETECTOR MARKET, 2021-2024

- TABLE 167 SMOKE DETECTOR MARKET: DEGREE OF COMPETITION

- TABLE 168 SMOKE DETECTOR MARKET: REGION FOOTPRINT

- TABLE 169 SMOKE DETECTOR MARKET: POWER SOURCE FOOTPRINT

- TABLE 170 SMOKE DETECTOR MARKET: TYPE FOOTPRINT

- TABLE 171 SMOKE DETECTOR MARKET: END USER FOOTPRINT

- TABLE 172 SMOKE DETECTOR MARKET: DETAILED LIST OF KEY STARTUP/SMES

- TABLE 173 SMOKE DETECTOR MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 174 SMOKE DETECTOR MARKET: PRODUCT LAUNCHES, JANUARY 2021-NOVEMBER 2024

- TABLE 175 SMOKE DETECTOR MARKET: DEALS, JANUARY 2021-NOVEMBER 2024

- TABLE 176 SMOKE DETECTOR MARKET: OTHER DEVELOPMENTS, JANUARY 2021-NOVEMBER 2024

- TABLE 177 HONEYWELL INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 178 HONEYWELL INTERNATIONAL INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 179 HONEYWELL INTERNATIONAL INC.: PRODUCT LAUNCHES

- TABLE 180 HONEYWELL INTERNATIONAL INC.: EXPANSIONS

- TABLE 181 JOHNSON CONTROLS INC.: COMPANY OVERVIEW

- TABLE 182 JOHNSON CONTROLS INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 183 JOHNSON CONTROLS INC.: PRODUCT LAUNCHES

- TABLE 184 SIEMENS: COMPANY OVERVIEW

- TABLE 185 SIEMENS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 186 SIEMENS: PRODUCT LAUNCHES

- TABLE 187 SIEMENS: DEALS

- TABLE 188 ROBERT BOSCH GMBH: COMPANY OVERVIEW

- TABLE 189 ROBERT BOSCH GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 190 HOCHIKI CORPORATION: COMPANY OVERVIEW

- TABLE 191 HOCHIKI CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 192 CARRIER: COMPANY OVERVIEW

- TABLE 193 CARRIER: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 194 CARRIER: PRODUCT LAUNCHES

- TABLE 195 CARRIER: DEALS

- TABLE 196 CARRIER: OTHER DEVELOPMENTS

- TABLE 197 GENTEX CORPORATION: COMPANY OVERVIEW

- TABLE 198 GENTEX CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 199 RESIDEO TECHNOLOGIES INC.: COMPANY OVERVIEW

- TABLE 200 RESIDEO TECHNOLOGIES INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 201 RESIDEO TECHNOLOGIES INC.: PRODUCT LAUNCHES

- TABLE 202 RESIDEO TECHNOLOGIES INC.: DEALS

- TABLE 203 MIRCOM GROUP OF COMPANIES: COMPANY OVERVIEW

- TABLE 204 MIRCOM GROUP OF COMPANIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 205 MIRCOM GROUP OF COMPANIES: PRODUCT LAUNCHES

- TABLE 206 SCHNEIDER ELECTRIC: COMPANY OVERVIEW

- TABLE 207 SCHNEIDER ELECTRIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 208 ABB: COMPANY OVERVIEW

- TABLE 209 ABB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 210 EMERSON ELECTRIC CO.: COMPANY OVERVIEW

- TABLE 211 EMERSON ELECTRIC CO.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 212 EMERSON ELECTRIC CO.: EXPANSIONS

- TABLE 213 EATON: COMPANY OVERVIEW

- TABLE 214 EATON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 215 SECOM CO., LTD.: COMPANY OVERVIEW

- TABLE 216 SECOM CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

List of Figures

- FIGURE 1 SMOKE DETECTOR MARKET: SEGMENTATION

- FIGURE 2 SMOKE DETECTOR MARKET: RESEARCH DESIGN

- FIGURE 3 SMOKE DETECTOR MARKET: RESEARCH APPROACH

- FIGURE 4 SMOKE DETECTOR MARKET: BOTTOM-UP APPROACH

- FIGURE 5 SMOKE DETECTOR MARKET: TOP-DOWN APPROACH

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH (SUPPLY-SIDE): REVENUE GENERATED THROUGH SALES OF SMOKE DETECTOR PRODUCTS/SERVICES

- FIGURE 7 DATA TRIANGULATION

- FIGURE 8 DUAL-SENSOR SMOKE DETECTORS TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 9 WIRED SMOKE DETECTORS TO HOLD LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 10 MAINTENANCE SERVICES SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 11 INDUSTRIAL SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 12 ASIA PACIFIC TO EXHIBIT HIGHEST CAGR IN SMOKE DETECTOR MARKET DURING FORECAST PERIOD

- FIGURE 13 GROWING INITIATIVES AND SUPPORT FROM VARIOUS GOVERNMENT BODIES EXPECTED TO DRIVE MARKET

- FIGURE 14 PHOTOELECTRIC SMOKE DETECTORS TO ACCOUNT FOR LARGEST MARKET SHARE IN 2029

- FIGURE 15 WIRED SEGMENT TO SECURE LARGER MARKET SHARE IN 2029

- FIGURE 16 MAINTENANCE SERVICES TO HOLD LARGEST SHARE OF SMOKE DETECTOR MARKET IN 2029

- FIGURE 17 INDUSTRIAL SEGMENT TO HOLD LARGEST SHARE OF SMOKE DETECTOR MARKET IN 2029

- FIGURE 18 INDUSTRIAL SEGMENT AND US TO HOLD LARGEST SHARES OF SMOKE DETECTOR MARKET IN 2029

- FIGURE 19 INDIA TO EXHIBIT HIGHEST CAGR IN GLOBAL SMOKE DETECTOR MARKET DURING FORECAST PERIOD

- FIGURE 20 SMOKE DETECTOR MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 21 SMOKE DETECTOR MARKET: IMPACT ANALYSIS OF DRIVERS

- FIGURE 22 SMOKE DETECTOR MARKET: IMPACT ANALYSIS OF RESTRAINTS

- FIGURE 23 SMOKE DETECTOR MARKET: IMPACT ANALYSIS OF OPPORTUNITIES

- FIGURE 24 SMOKE DETECTOR MARKET: IMPACT ANALYSIS OF CHALLENGES

- FIGURE 25 SMOKE DETECTOR MARKET: VALUE CHAIN ANALYSIS

- FIGURE 26 SMOKE DETECTOR MARKET: ECOSYSTEM ANALYSIS

- FIGURE 27 INDICATIVE PRICING OF PHOTOELECTRIC SMOKE DETECTORS OFFERED BY KEY PLAYERS, 2023

- FIGURE 28 AVERAGE SELLING PRICE TREND OF SMOKE DETECTORS, BY TYPE, 2020-2023

- FIGURE 29 AVERAGE SELLING PRICE TREND OF PHOTOELECTRIC SMOKE DETECTORS BY REGION, 2020-2023

- FIGURE 30 TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

- FIGURE 31 INVESTMENT AND FUNDING SCENARIO

- FIGURE 32 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 33 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- FIGURE 34 KEY BUYING CRITERIA FOR TOP THREE END USERS

- FIGURE 35 IMPORT DATA FOR HS CODE 8531-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023

- FIGURE 36 EXPORT DATA FOR HS CODE 8531-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023

- FIGURE 37 SMOKE DETECTOR MARKET: PATENT ANALYSIS, 2014-2023

- FIGURE 38 KEY AI USE CASES IN SMOKE DETECTOR MARKET

- FIGURE 39 SMOKE DETECTOR MARKET, BY DISTRIBUTION CHANNEL

- FIGURE 40 SMOKE DETECTOR MARKET, BY TYPE

- FIGURE 41 DUAL-SENSOR SMOKE DETECTOR MARKET TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 42 SMOKE DETECTOR MARKET, BY SERVICE

- FIGURE 43 MAINTENANCE SERVICES TO DOMINATE SMOKE DETECTOR MARKET IN 2029

- FIGURE 44 SMOKE DETECTOR MARKET, BY POWER SOURCE

- FIGURE 45 WIRED SEGMENT TO HOLD LARGEST SHARE OF SMOKE DETECTOR MARKET DURING FORECAST PERIOD

- FIGURE 46 SMOKE DETECTOR MARKET, BY END USER

- FIGURE 47 INDUSTRIAL SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 48 SMOKE DETECTOR MARKET, BY REGION

- FIGURE 49 SMOKE DETECTOR MARKET IN INDIA TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 50 NORTH AMERICA TO HOLD LARGEST SHARE OF SMOKE DETECTOR MARKET DURING FORECAST PERIOD

- FIGURE 51 NORTH AMERICA: SMOKE DETECTOR MARKET SNAPSHOT

- FIGURE 52 US TO DOMINATE SMOKE DETECTOR MARKET IN NORTH AMERICA THROUGHOUT FORECAST PERIOD

- FIGURE 53 EUROPE: SMOKE DETECTOR MARKET SNAPSHOT

- FIGURE 54 GERMANY TO BE FASTEST-GROWING MARKET IN EUROPE DURING FORECAST PERIOD

- FIGURE 55 ASIA PACIFIC: SMOKE DETECTOR MARKET SNAPSHOT

- FIGURE 56 CHINA TO DOMINATE ASIA PACIFIC MARKET THROUGHOUT FORECAST PERIOD

- FIGURE 57 MIDDLE EAST TO DOMINATE MARKET IN ROW THROUGHOUT FORECAST PERIOD

- FIGURE 58 SMOKE DETECTOR MARKET: REVENUE ANALYSIS OF FOUR KEY PLAYERS, 2019-2023

- FIGURE 59 SMOKE DETECTOR MARKET SHARE ANALYSIS, 2023

- FIGURE 60 COMPANY VALUATION (USD MILLION), 2024

- FIGURE 61 FINANCIAL METRICS (EV/EBITDA), 2024

- FIGURE 62 BRAND/PRODUCT COMPARISON

- FIGURE 63 SMOKE DETECTOR MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 64 COMPANY FOOTPRINT

- FIGURE 65 SMOKE DETECTOR MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- FIGURE 66 HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

- FIGURE 67 JOHNSON CONTROLS INC.: COMPANY SNAPSHOT

- FIGURE 68 SIEMENS: COMPANY SNAPSHOT

- FIGURE 69 ROBERT BOSCH GMBH: COMPANY SNAPSHOT

- FIGURE 70 HOCHIKI CORPORATION: COMPANY SNAPSHOT

- FIGURE 71 CARRIER: COMPANY SNAPSHOT

- FIGURE 72 GENTEX CORPORATION: COMPANY SNAPSHOT

- FIGURE 73 RESIDEO TECHNOLOGIES INC.: COMPANY SNAPSHOT

- FIGURE 74 SCHNEIDER ELECTRIC: COMPANY SNAPSHOT

- FIGURE 75 ABB: COMPANY SNAPSHOT

- FIGURE 76 EMERSON ELECTRIC CO.: COMPANY SNAPSHOT

- FIGURE 77 EATON: COMPANY SNAPSHOT

- FIGURE 78 SECOM CO., LTD.: COMPANY SNAPSHOT

The global Smoke Detectors market is projected to reach USD 2.68 billion by 2024 and USD 3.76 billion by 2029, growing at a rate of 7.0%. Key drivers include growing fire safety awareness in residential, commercial, and industrial sectors, stringent fire safety regulations implemented in every segment, and emerging trend of smart smoke detectors and loT connectivity. The increasing use of wireless smoke detectors and increasing construction activities across the globe has further driven the demand in the smoke detector market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Detector Type, Power Source, Service, End-Use Industry and Region |

| Regions covered | North America, Europe, APAC, RoW |

" Wired smoke detectors to maintain significant market share during the forecast period."

Wired smoke detectors is anticipated to hold a significant market share in the smoke detector market during the forecast period, mainly due to their high reliability and consistency. The wired smoke detectors are usually hardwired into a building's electrical system so that they function continuously without relying on batteries, which makes them popular in commercial, industrial, and large residential applications. With the presence of a backup power facility with smoke detectors that are wired, it presents safety factors in the context of power failure. Integration becomes easy within building automation systems and severe fire safety requirement systems that increase demand in hazardous environments with stringent fire detection needs.

"Photoelectric smoke detectors to hold largest market share due to enhanced fire detection capabilities."

Photoelectric smoke detectors are expected to hold the largest market share during the forecast period. They outperform in detection of slow, smoldering fires that are generally common in residential and commercial settings. These detectors detect smoke particles using light-sensitive sensors, making them relatively more reliable in detecting fires early than ionization detectors. Increased awareness of fire safety, more stringent rules and regulations, and the vast applications in new construction as well as retrofitting, has seen an increase in its use. Advancements in photoelectric technology improve the efficiency and reliability, therefore making them a more permanent player in the market.

"Industrial segment is expected to hold largest market share during the forecast period."

The industrial sector is expected to dominate the smoke detector market. This is mainly because industrial facilities are of utmost importance, where fire can cause severe damage to property, halt production, and even result in loss of life. Severe government regulations that require the installation of smoke detectors in industrial facilities are driving this market. There is also increased complexity in industrial processes requiring reliable and sophisticated smoke detectors to be deployed in dealing with flammable materials, thus making the industrial market remain a leading sector, especially for high-performance solutions.

"North America is set to capture largest market share in smoke detector market driven by regulatory compliance and technological advancements."

North America will lead the smoke detector market throughout the forecast period, as propelled by strict fire safety rules, raised fire risk awareness, and a high adoption rate of technology. Intensified home and commercial construction in North America has raised the demand for reliable smoke detection solutions throughout the region. Government initiatives and building codes to install smoke detectors in buildings support the growth of the market. The existence of prominent manufacturers and constant innovation in smoke detection technologies, such as smart and interconnected systems, make North America a leading region in the smoke detector market, thus ensuring more safety measures in various applications.

Breakdown of primaries

A variety of executives from key organizations operating in the smoke detectors market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 -40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: C-level Executives - 35%, Directors - 40%, and Others - 25%

- By Region: North America - 35%, Europe - 25%, Asia Pacific - 32%, and RoW - 8%

Major players profiled in this report are as follows: Johnson Controls (Ireland), Robert Bosch GmbH (Germany), Hochiki Corporation (Japan), Siemens (Germany), and Honeywell International Inc. (US) and others. These leading companies possess a wide portfolio of products, establishing a prominent presence in established as well as emerging markets.

The study provides a detailed competitive analysis of these key players in the smoke detectors market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

In this report, the smoke detectors market has been segmented based on power source, type, enduser and region. The power source segment consists of wired and wireless smoke detector. The type segment consists of photoelectric, ionization, dual, beam, aspirating and duct smoke detectors. The enduser segment consists of residential, commercial and industrial sectors. The market has been segmented into four regions-North America, Asia Pacific, Europe, and RoW.

Reasons to buy the report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the sub-segments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the smoke detectors market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

- Analysis of key drivers (Rising initiatives and support for smoke detectors from government bodies, Increased fire-related expenditure of various enterprises and rise in deaths & loss of properties, Advantages of the technological innovations and Increasing population and rapid urbanization), restraints (High replacing costs associated with replacing traditional smoke detectors with smart smoke detectors, Installation challenges of smoke detectors) opportunities (Smart smoke detectors to capture the market in coming years, Increasing installation of smoke detectors in buses, coaches, and specialty vehicles, Growing awareness of fire safety), and challenges (Difficulties in disposing off smoke detectors, Incidence of false alarms) influencing the growth of the smoke detectors market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the smoke detectors market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the smoke detectors market across varied regions.

- Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the smoke detectors market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Johnson Controls (Ireland), Robert Bosch GmbH (Germany), Hochiki Corporation (Japan), Siemens (Germany), and Honeywell International Inc. (US) and others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY AND PRIMARY RESEARCH

- 2.1.2 SECONDARY DATA

- 2.1.2.1 List of major secondary sources

- 2.1.2.2 Key data from secondary sources

- 2.1.3 PRIMARY DATA

- 2.1.3.1 Primary interviews with experts

- 2.1.3.2 Key primary interview participants

- 2.1.3.3 Key data from primary sources

- 2.1.3.4 Key industry insights

- 2.1.3.5 Breakdown of primaries

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

- 2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS OPERATING IN SMOKE DETECTOR MARKET

- 4.2 SMOKE DETECTOR MARKET, BY TYPE

- 4.3 SMOKE DETECTOR MARKET, BY POWER SOURCE

- 4.4 SMOKE DETECTOR MARKET, BY SERVICE

- 4.5 SMOKE DETECTOR MARKET, BY END USER

- 4.6 SMOKE DETECTOR MARKET IN NORTH AMERICA, BY END USER AND COUNTRY

- 4.7 SMOKE DETECTOR MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising initiatives and support for smoke detectors from government bodies

- 5.2.1.2 Increased fire-related expenditure of various enterprises

- 5.2.1.3 Advancements in sensor technology

- 5.2.1.4 Growing population and rapid urbanization

- 5.2.2 RESTRAINTS

- 5.2.2.1 High costs associated with replacing traditional with smart smoke detectors

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing adoption of smart smoke detectors

- 5.2.3.2 Surging installation of smoke detectors in buses, coaches, and specialty vehicles

- 5.2.3.3 Growing awareness of fire safety

- 5.2.4 CHALLENGES

- 5.2.4.1 Difficulties in disposing of smoke detectors

- 5.2.4.2 Incidence of false alarms

- 5.2.4.3 Installation challenges of smoke detectors in existing buildings

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING OF PHOTOELECTRIC SMOKE DETECTORS OFFERED BY KEY PLAYERS, 2023

- 5.5.2 AVERAGE SELLING PRICE TREND OF SMOKE DETECTORS, BY TYPE, 2020-2023

- 5.5.3 AVERAGE SELLING PRICE TREND OF PHOTOELECTRIC SMOKE DETECTORS, BY REGION, 2020-2023

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7 INVESTMENT AND FUNDING SCENARIO

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 IoT-enabled smoke detector systems

- 5.8.2 ADJACENT TECHNOLOGIES

- 5.8.2.1 Smart home integration

- 5.8.3 COMPLEMENTARY TECHNOLOGIES

- 5.8.3.1 Video image smoke and flame detection systems

- 5.8.3.2 Artificial intelligence

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PORTER'S FIVE FORCES ANALYSIS

- 5.9.1 BARGAINING POWER OF SUPPLIERS

- 5.9.2 BARGAINING POWER OF BUYERS

- 5.9.3 THREAT OF NEW ENTRANTS

- 5.9.4 THREAT OF SUBSTITUTES

- 5.9.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.10.2 BUYING CRITERIA

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 EAST COAST MUSEUM ADOPTS JOHNSON CONTROLS' FIRE DETECTION SYSTEM TO QUICKLY RESPOND TO EMERGENCIES

- 5.11.2 CASA SOLLIEVO BIMBI USES BOSCH SECURITY AND SAFETY SYSTEMS' INTEGRATED FIRE AND VOICE EVACUATION SOLUTION TO IMPROVE EMERGENCY RESPONSE TIMES

- 5.11.3 JOHNSON CONTROLS INC. HELPS MAJOR PACIFIC NORTHWEST AIRPORT ENHANCE FIRE SAFETY AND CUT COSTS USING 4100 ES SYSTEM

- 5.11.4 DOHA MTERO ADDRESSES RIGOROUS SAFETY AND EFFICIENCY REQUIREMENTS WITH HONEYWELL INTERNATIONAL INC.'S ADVANCED FIRE SAFETY SOLUTIONS

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT SCENARIO (HS CODE 8531)

- 5.12.2 EXPORT SCENARIO (HS CODE 8531)

- 5.13 PATENT ANALYSIS

- 5.14 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.15 REGULATORY LANDSCAPE

- 5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15.2 STANDARDS

- 5.15.3 REGULATIONS

- 5.16 IMPACT OF AI ON SMOKE DETECTOR MARKET

- 5.16.1 INTRODUCTION

- 5.16.2 AI IMPACT ON SMOKE DETECTOR MARKET

- 5.16.3 TOP USE CASES AND MARKET POTENTIAL

6 DISTRIBUTION CHANNELS OF SMOKE DETECTORS

- 6.1 INTRODUCTION

- 6.2 ONLINE

- 6.3 OFFLINE

7 SMOKE DETECTOR MARKET, BY OFFERING

- 7.1 INTRODUCTION

- 7.2 PRODUCTS

- 7.2.1 GROWING AWARENESS OF LIFE SAFETY TO BOOST DEMAND

- 7.3 SERVICES

- 7.3.1 STRINGENT GOVERNMENT REGULATIONS AND BUILDING CODES TO INCREASE DEMAND

8 SMOKE DETECTOR MARKET, BY TYPE

- 8.1 INTRODUCTION

- 8.2 PHOTOELECTRIC SMOKE DETECTORS

- 8.2.1 INCREASING USE IN COMMERCIAL SPACE TO FUEL MARKET GROWTH

- 8.3 IONIZATION SMOKE DETECTORS

- 8.3.1 ABILITY TO DETECT VISIBLE AND INVISIBLE COMBUSTION PRODUCTS TO BOOST DEMAND

- 8.4 DUAL-SENSOR SMOKE DETECTORS

- 8.4.1 GROWING DEPLOYMENT TO REDUCE FALSE ALARMS AND IMPROVE SAFETY TO PROPEL MARKET

- 8.5 BEAM SMOKE DETECTORS

- 8.5.1 LOWER INSTALLATION AND MAINTENANCE COSTS TO DRIVE ADOPTION

- 8.5.2 REFLECTED BEAM SMOKE DETECTORS

- 8.5.3 RECEIVER-TRANSMITTER/OPTICAL BEAM SMOKE DETECTORS

- 8.6 ASPIRATING SMOKE DETECTORS

- 8.6.1 QUICK INSTALLATION AND EASY COMMISSIONING TO SPIKE DEMAND

- 8.7 DUCT SMOKE DETECTORS

- 8.7.1 ENHANCING FIRE SAFETY IN HVAC SYSTEMS TO BOOST DEMAND

9 SMOKE DETECTOR MARKET, BY SERVICE

- 9.1 INTRODUCTION

- 9.2 ENGINEERING SERVICES

- 9.2.1 INTEGRATION OF FIRE SAFETY SERVICES IN NEW CONSTRUCTIONS AND RENOVATIONS TO AUGMENT MARKET GROWTH

- 9.3 INSTALLATION & DESIGN SERVICES

- 9.3.1 LIFE SAFETY AND PROPERTY PROTECTION TO DRIVE MARKET

- 9.4 MAINTENANCE SERVICES

- 9.4.1 SURGING NEED FOR ROUTINE INSPECTIONS AND TESTING TO SPIKE DEMAND

- 9.5 MANAGED SERVICES

- 9.5.1 NEED TO REDUCE RISKS ASSOCIATED WITH FIRE HAZARDS AND DAMAGE TO PROPEL MARKET

- 9.6 OTHER SERVICES

10 SMOKE DETECTOR MARKET, BY POWER SOURCE

- 10.1 INTRODUCTION

- 10.2 COMPARISON OF WIRED AND WIRELESS SMOKE DETECTOR SYSTEMS

- 10.3 WIRED

- 10.3.1 RELIABILITY AND CONTINUOUS POWER SUPPLY TO DRIVE MARKET

- 10.4 WIRELESS

- 10.4.1 EASE OF INSTALLATION AND FLEXIBILITY TO FUEL DEMAND

11 SMOKE DETECTOR MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 COMMERCIAL

- 11.2.1 ACADEMIA & INSTITUTIONAL

- 11.2.1.1 Stricter government regulations and building codes to augment market growth

- 11.2.2 RETAIL

- 11.2.2.1 Presence of combustible materials in retail stores to propel market growth

- 11.2.3 HEALTHCARE

- 11.2.3.1 Increasing fire incidents in healthcare facilities to drive adoption

- 11.2.4 HOSPITALITY

- 11.2.4.1 Strengthening fire safety protocols with enhanced smoke detection systems in hotels to spike demand

- 11.2.5 BFSI

- 11.2.5.1 Rising focus on enhancing operational resilience to spur demand

- 11.2.6 GOVERNMENT & OFFICE BUILDINGS

- 11.2.6.1 Emphasis on protecting staff and assets to support market growth

- 11.2.1 ACADEMIA & INSTITUTIONAL

- 11.3 RESIDENTIAL

- 11.3.1 GOVERNMENT-LED INITIATIVES AND IMPLEMENTATION OF LAWS AND BUILDING CODES TO BOOST DEMAND

- 11.4 INDUSTRIAL

- 11.4.1 OIL & GAS AND MINING

- 11.4.1.1 Pressing need to improve industrial plant safety to drive adoption

- 11.4.2 TRANSPORTATION & LOGISTICS

- 11.4.2.1 Growing need for prompt and efficient handling of fire emergencies to fuel demand

- 11.4.3 IT & TELECOMMUNICATIONS

- 11.4.3.1 Enforcement of robust fire safety measures to accelerate market growth

- 11.4.4 MANUFACTURING

- 11.4.4.1 Implementation of comprehensive smoke detection solutions to support market growth

- 11.4.5 ENERGY & POWER

- 11.4.5.1 Heightened risk of fire due to flammable materials to spur demand

- 11.4.6 PHARMACEUTICALS

- 11.4.6.1 Strong demand for fire protection systems to ensure operational continuity to fuel market growth

- 11.4.7 OTHER INDUSTRIES

- 11.4.1 OIL & GAS AND MINING

12 SMOKE DETECTOR MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 Presence of prominent market players and strict regulations to drive adoption

- 12.2.3 CANADA

- 12.2.3.1 Government-led initiatives boosting adoption of smoke detectors to propel market growth

- 12.2.4 MEXICO

- 12.2.4.1 Pressing need to increase investment in residential and corporate fire prevention to foster market growth

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 UK

- 12.3.2.1 Continuous expansion and renovation of hospitality sector to contribute to market growth

- 12.3.3 GERMANY

- 12.3.3.1 Surging adoption of photoelectric and dual-sensor smoke detectors to fuel market growth

- 12.3.4 FRANCE

- 12.3.4.1 Mandates pertaining to compulsory installation of smoke detectors in residential homes to fuel market growth

- 12.3.5 ITALY

- 12.3.5.1 Raising awareness and enforcing smoke detector regulations to drive market

- 12.3.6 SPAIN

- 12.3.6.1 Stringent fire safety standards to accelerate demand

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 Growing government initiatives to enforce installations of fire protection systems to spur demand

- 12.4.3 JAPAN

- 12.4.3.1 Government efforts to enhance public awareness of fire safety measures to support market growth

- 12.4.4 SOUTH KOREA

- 12.4.4.1 Awareness about fire prevention and safety regulations among citizens to spike demand

- 12.4.5 INDIA

- 12.4.5.1 Rising awareness and safety regulations to drive adoption

- 12.4.6 AUSTRALIA

- 12.4.6.1 Stringent regulations and a strong emphasis on fire safety to drive market

- 12.4.7 REST OF ASIA PACIFIC

- 12.5 ROW

- 12.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 12.5.2 MIDDLE EAST

- 12.5.2.1 Urbanization and enhanced fire safety regulations to support market growth

- 12.5.2.2 GCC countries

- 12.5.2.2.1 Saudi Arabia

- 12.5.2.2.1.1 Rapid urbanization with significant construction activity to boost demand

- 12.5.2.2.2 UAE

- 12.5.2.2.2.1 Stringent fire safety regulations to drive market

- 12.5.2.2.3 Rest of GCC countries

- 12.5.2.2.1 Saudi Arabia

- 12.5.2.3 Rest of Middle East

- 12.5.3 SOUTH AMERICA

- 12.5.3.1 Increasing adoption of smoke detectors in multiple sectors to drive market

- 12.5.4 AFRICA

- 12.5.4.1 Growing urbanization and improved standard of living to spur demand

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 STRATEGIES ADOPTED BY KEY PLAYERS/RIGHT TO WIN, 2021-2024

- 13.3 REVENUE ANALYSIS, 2019-2023

- 13.4 MARKET SHARE ANALYSIS, 2023

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS, 2024

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 13.7.1 EMERGING LEADERS

- 13.7.2 STARS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Power source footprint

- 13.7.5.4 Type footprint

- 13.7.5.5 End user footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 HONEYWELL INTERNATIONAL INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 JOHNSON CONTROLS INC.

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 SIEMENS

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 ROBERT BOSCH GMBH

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Key strengths

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses and competitive threats

- 14.1.5 HOCHIKI CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 MnM view

- 14.1.5.3.1 Key strengths

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses and competitive threats

- 14.1.6 CARRIER

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.3.2 Deals

- 14.1.6.3.3 Other developments

- 14.1.7 GENTEX CORPORATION

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.8 RESIDEO TECHNOLOGIES INC.

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.3.2 Deals

- 14.1.9 MIRCOM GROUP OF COMPANIES

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches

- 14.1.10 SCHNEIDER ELECTRIC

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.11 ABB

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.12 EMERSON ELECTRIC CO.

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Expansions

- 14.1.13 EATON

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Solutions/Services offered

- 14.1.14 SECOM CO., LTD.

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Solutions/Services offered

- 14.1.1 HONEYWELL INTERNATIONAL INC.

- 14.2 OTHER PLAYERS

- 14.2.1 APOLLO FIRE DETECTORS

- 14.2.2 FIKE

- 14.2.3 CEASEFIRE INDUSTRIES PVT. LTD.

- 14.2.4 SECURITON AG

- 14.2.5 UNIVERSAL SECURITY INSTRUMENTS, INC.

- 14.2.6 HEKATRON VERTRIEBS GMBH

- 14.2.7 NETATMO

- 14.2.8 ORR PROTECTION

- 14.2.9 RAVEL GROUP OF COMPANIES

- 14.2.10 GUARDIAN PROTECTION

- 14.2.11 VIKING GROUP INC.

- 14.2.12 VECTOR SECURITY, INC.

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS