|

|

市場調査レポート

商品コード

1655430

AIビジョンの世界市場 (~2029年):ビジョンソフトウェア (API・SDK)・ビジョンプラットフォーム・行動分析・OCR・空間分析・画像認識・ヒートマップ分析・機械学習・ディープラーニング・CNN・生成AI別AI Vision Market by Vision Software (API, SDK), Vision Platform, Behavioral Analysis, Optical Character Recognition, Spatial Analysis, Image Recognition, Heatmap Analysis, Machine Learning, Deep Learning, CNN, Generative AI - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| AIビジョンの世界市場 (~2029年):ビジョンソフトウェア (API・SDK)・ビジョンプラットフォーム・行動分析・OCR・空間分析・画像認識・ヒートマップ分析・機械学習・ディープラーニング・CNN・生成AI別 |

|

出版日: 2025年02月01日

発行: MarketsandMarkets

ページ情報: 英文 250 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

AIビジョンの市場規模は、2024年の148億5,000万米ドルから、予測期間中は23.7%のCAGRで推移し、2029年には430億2,000万米ドルの規模に成長すると予測されています。

AIビジョン市場は、クラウドコンピューティング、機械学習 (ML)、ディープラーニングの高い導入率により、加速度的な成長を遂げています。エッジコンピューティングの進歩は、自動車や製造業におけるリアルタイム分析の需要を押し上げています。一方で、同市場は、法的リスクや風評リスク、保証されたレベルの精度を生み出すために必要なデータの質といった課題に直面しています。そのため、AIの次世代ビジョンソリューションへの統合が、小売、製造、ヘルスケアなど、さまざまな業界に新たな事業機会をもたらし、市場を推進しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020-2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024-2029年 |

| 単位 | 金額 (米ドル) |

| セグメント別 | 提供区分・サービスタイプ・技術・運用モード・産業・地域別 |

| 対象地域 | 北米・欧州・アジア太平洋・その他の地域 |

"産業別では、ヘルスケアの部門が予測期間中の市場をリードする見込み"

AIビジョンは、全方位的な診断精度、個別化された治療計画、継続的な患者モニタリングのサポート、迅速な意思決定を提供することで、ヘルスケア産業に影響を与えます。AIビジョンは効率を改善し、病院のコストを削減します。医療の専門家は、癌の検出や手術支援などの重要な作業においてAIビジョンへの依存を高めており、これらの技術に対する需要は今後も伸び続けると思われます。

"ビジョンソフトウェアの部門が市場で2番目に高いCAGRで成長する見込み"

ビジョンソフトウェアは、ヘルスケア、製造、小売など、さまざまな産業でのスケーラブルで効率的なAIソリューションに対する需要の高まりに対応するため、大幅な成長が見込まれています。AIや機械学習の継続的な進歩に伴い、これらのツールは小売業における顧客追跡や製造業における業務効率の向上などのタスクに不可欠なものとなりつつあります。企業が戦略的な意思決定に視覚データを活用することをますます目指すようになるにつれ、ビジョンソフトウェアの採用は拡大し続け、AIビジョン市場の重要な構成要素としての役割を確固たるものにしていくと思われます。

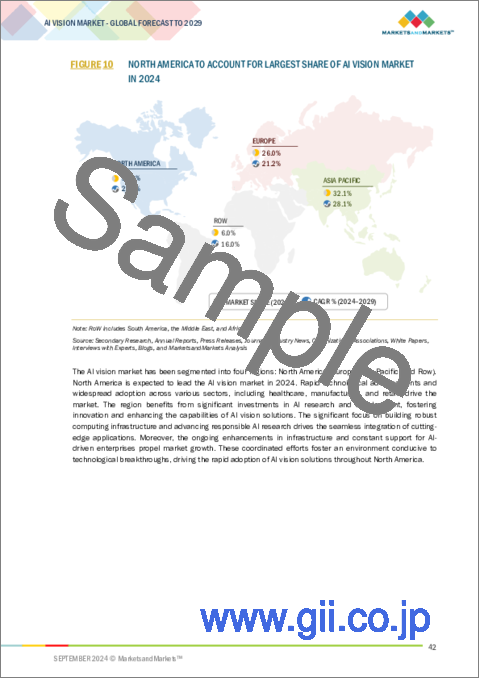

"北米が2番目の市場シェアを占めると予測"

技術の進歩が進み、ヘルスケア、製造業、小売業で大幅な導入が進んでいることから、北米はAIビジョン市場で第2位にランクされています。Microsoft Corporation (米国) 、NVIDIA Corporation (米国) 、Alphabet, Inc (米国) などの大手技術企業が市場を牽引しています。同時に、AIの研究開発に対する政府の資金援助も、この業界に提供される追加的な支援となっています。カナダは、コンピューティングインフラと責任あるAI研究能力の向上に注力しており、この地域の強みに拍車をかけています。メキシコは継続的にインフラをアップグレードし、AIに関わるビジネスを支援しようとしています。これらすべての要因が組み合わさることで、イノベーションを促進し、北米全域でAIビジョンソリューションの統合を確実にするダイナミックな環境が強化されています。

当レポートでは、世界のAIビジョンの市場を調査し、市場概要、市場成長への各種影響因子の分析、技術・特許の動向、法規制環境、ケーススタディ、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- バリューチェーン分析

- エコシステム分析

- 顧客の事業に影響を与える動向/ディスラプション

- 価格分析

- 技術分析

- ポーターのファイブフォース分析

- 主なステークホルダーと購入基準

- ケーススタディ分析

- 投資と資金調達のシナリオ

- 貿易分析

- 特許分析

- 主な会議とイベント

- 規制状況

第6章 AIビジョンのユースケース

- 自動運転車

- 拡張現実デバイス

- ロボットビジョンシステム

- 3Dプリンター

- 医療画像ソリューション

- 交通監視システム

- 自動ナンバープレート認識システム

- セキュリティおよび監視システム

- デジタル資産管理ソリューション

第7章 AIビジョン市場:提供区分別

- ビジョンプラットフォーム

- ビジョンソフトウェア

- API

- ソフトウェア開発キット

- カスタムソリューション

第8章 AIビジョン市場:サービスタイプ別

- 行動分析

- 顔認識

- OCR

- 空間分析

- モーション検出

- 侵入検知

- 周囲監視

- 画像認識

- ヒートマップ分析

- 群衆密度分析

第9章 AIビジョン市場:技術別

- 機械学習

- ディープラーニング

- 畳み込みニューラルネットワーク

- 生成AI

第10章 AIビジョン市場:運用モード別

- エッジ推論

- クラウドベース学習

第11章 AIビジョン市場:産業別

- 輸送・物流

- 小売

- ヘルスケア

- 製造

- 農業

- 石油・ガス

- 建設

- その他

第12章 AIビジョン市場:地域別

- 北米

- マクロ経済要因

- 米国

- カナダ

- メキシコ

- 欧州

- マクロ経済要因

- ドイツ

- 英国

- フランス

- イタリア

- その他

- アジア太平洋

- マクロ経済要因

- 中国

- 日本

- 韓国

- その他

- その他の地域

- マクロ経済要因

- 中東

- アフリカ

- 南米

第13章 競合情勢

- 概要

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- 企業価値評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要企業

- 企業評価マトリックス:スタートアップ/中小企業

- 競合シナリオ

第14章 企業プロファイル

- 主要企業

- NVIDIA CORPORATION

- MICROSOFT CORPORATION

- INTEL CORPORATION

- ALPHABET INC.

- AMAZON.COM, INC.

- IBM

- ORACLE

- COGNEX CORPORATION

- QUALCOMM TECHNOLOGIES, INC.

- STMICROELECTRONICS

- AVNET, INC.

- AVEVA GROUP LIMITED

- その他の企業

- SYMPHONYAI

- APERA AI

- CHOOCH

- IRONYUN INC.

- KYUNGWOO SYSTECH, INC.

- LANDINGAI

- ML6

- OPENSISTEMAS

- ROBOVISION BV

- SENSETIME

- SEVENLAB

- SOLOMON TECHNOLOGY CORPORATION

- VISO.AI

- ZEBRA TECHNOLOGIES

- AI VISION TECHNOLOGIES LLC

- HELLBENDER

- MVISION AI

第15章 付録

List of Tables

- TABLE 1 REPORT LIMITATIONS AND ASSOCIATED RISKS

- TABLE 2 ROLE OF COMPANIES IN AI VISION ECOSYSTEM

- TABLE 3 AVERAGE SELLING PRICE TREND OF VISION PLATFORM OFFERINGS OF KEY PLAYERS, BY FEATURE, 2023

- TABLE 4 AVERAGE SELLING PRICE TREND OF VISION PLATFORMS OFFERED BY KEY PLAYERS, 2023

- TABLE 5 AI VISION MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 VERTICALS

- TABLE 7 KEY BUYING CRITERIA FOR TOP 3 VERTICALS

- TABLE 8 IMPORT SCENARIO FOR HS CODE 852580-COMPLIANT PRODUCTS, BY COUNTRY, 2019-20203 (USD MILLION)

- TABLE 9 EXPORT SCENARIO FOR HS CODE 852580-COMPLIANT PRODUCTS, BY COUNTRY, 2019-20203 (USD MILLION)

- TABLE 10 AI VISION MARKET: PATENTS, 2020-2024

- TABLE 11 AI VISION MARKET: MAJOR CONFERENCES AND EVENTS, 2024-2026

- TABLE 12 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 MAJOR STANDARDS AND REGULATIONS IN NORTH AMERICA

- TABLE 17 MAJOR STANDARDS AND REGULATIONS IN EUROPE

- TABLE 18 MAJOR STANDARDS AND REGULATIONS IN ASIA PACIFIC

- TABLE 19 MAJOR STANDARDS AND REGULATIONS IN ROW

- TABLE 20 AI VISION MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 21 AI VISION MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 22 VISION PLATFORMS: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 23 VISION PLATFORMS: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 24 VISION SOFTWARE: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 25 VISION SOFTWARE: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 26 VISION SOFTWARE: AI VISION MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 27 VISION SOFTWARE: AI VISION MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 28 CUSTOM SOLUTIONS: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 29 CUSTOM SOLUTIONS: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 30 AI VISION MARKET, BY SERVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 31 AI VISION MARKET, BY SERVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 32 SPATIAL ANALYSIS: AI VISION MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 33 SPATIAL ANALYSIS: AI VISION MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 34 AI VISION MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 35 AI VISION MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 36 MACHINE LEARNING: AI VISION MARKET, BY TECHNOLOGY TYPE, 2020-2023 (USD MILLION)

- TABLE 37 MACHINE LEARNING: AI VISION MARKET, BY TECHNOLOGY TYPE, 2024-2029 (USD MILLION)

- TABLE 38 MACHINE LEARNING: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 39 MACHINE LEARNING: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 40 DEEP LEARNING: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 41 DEEP LEARNING: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 42 CONVOLUTIONAL NEURAL NETWORKS: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 43 CONVOLUTIONAL NEURAL NETWORKS: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 44 GENERATIVE AI: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 45 GENERATIVE AI: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 46 AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 47 AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 48 EDGE INFERENCING: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 49 EDGE INFERENCING: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 50 EDGE INFERENCING: AI VISION MARKET IN NORTH AMERICA, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 51 EDGE INFERENCING: AI VISION MARKET IN NORTH AMERICA, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 52 EDGE INFERENCING: AI VISION MARKET IN EUROPE, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 53 EDGE INFERENCING: AI VISION MARKET IN EUROPE, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 54 EDGE INFERENCING: AI VISION MARKET IN ASIA PACIFIC, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 55 EDGE INFERENCING: AI VISION MARKET IN ASIA PACIFIC, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 56 EDGE INFERENCING: AI VISION MARKET IN ROW, BY REGION, 2020-2023 (USD MILLION)

- TABLE 57 EDGE INFERENCING: AI VISION MARKET IN ROW, BY REGION, 2024-2029 (USD MILLION)

- TABLE 58 CLOUD-BASED LEARNING: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 59 CLOUD-BASED LEARNING: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 60 CLOUD-BASED LEARNING: AI VISION MARKET IN NORTH AMERICA, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 61 CLOUD-BASED LEARNING: AI VISION MARKET IN NORTH AMERICA, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 62 CLOUD-BASED LEARNING: AI VISION MARKET IN EUROPE, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 63 CLOUD-BASED LEARNING: AI VISION MARKET IN EUROPE, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 64 CLOUD-BASED LEARNING: AI VISION MARKET IN ASIA PACIFIC, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 65 CLOUD-BASED LEARNING: AI VISION MARKET IN ASIA PACIFIC, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 66 CLOUD-BASED LEARNING: AI VISION MARKET IN ROW, BY REGION, 2020-2023 (USD MILLION)

- TABLE 67 CLOUD-BASED LEARNING: AI VISION MARKET IN ROW, BY REGION, 2024-2029 (USD MILLION)

- TABLE 68 AI VISION MARKET, BY VERTICAL, 2020-2023 (USD MILLION)

- TABLE 69 AI VISION MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 70 TRANSPORTATION & LOGISTICS: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 71 TRANSPORTATION & LOGISTICS: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 72 RETAIL: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 73 RETAIL: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 74 HEALTHCARE: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 75 HEALTHCARE: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 76 MANUFACTURING: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 77 MANUFACTURING: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 78 AGRICULTURE: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 79 AGRICULTURE: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 80 OIL & GAS: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 81 OIL & GAS: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 82 CONSTRUCTION: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 83 CONSTRUCTION: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 84 OTHER VERTICALS: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 85 OTHER VERTICALS: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 86 AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 87 AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 88 NORTH AMERICA: AI VISION MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 89 NORTH AMERICA: AI VISION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 90 NORTH AMERICA: AI VISION MARKET, BY VERTICAL, 2020-2023 (USD MILLION)

- TABLE 91 NORTH AMERICA: AI VISION MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 92 NORTH AMERICA: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 93 NORTH AMERICA: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 94 NORTH AMERICA: AI VISION MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 95 NORTH AMERICA: AI VISION MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 96 NORTH AMERICA: AI VISION MARKET FOR MACHINE LEARNING, BY TECHNOLOGY TYPE, 2020-2023 (USD MILLION)

- TABLE 97 NORTH AMERICA: AI VISION MARKET FOR MACHINE LEARNING, BY TECHNOLOGY TYPE, 2024-2029 (USD MILLION)

- TABLE 98 NORTH AMERICA: AI VISION MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 99 NORTH AMERICA: AI VISION MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 100 US: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 101 US: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 102 CANADA: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 103 CANADA: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 104 MEXICO: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 105 MEXICO: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 106 EUROPE: AI VISION MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 107 EUROPE: AI VISION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 108 EUROPE: AI VISION MARKET, BY VERTICAL, 2020-2023 (USD MILLION)

- TABLE 109 EUROPE: AI VISION MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 110 EUROPE: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 111 EUROPE: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 112 EUROPE: AI VISION MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 113 EUROPE: AI VISION MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 114 EUROPE: AI VISION MARKET FOR MACHINE LEARNING, BY TECHNOLOGY TYPE, 2020-2023 (USD MILLION)

- TABLE 115 EUROPE: AI VISION MARKET FOR MACHINE LEARNING, BY TECHNOLOGY TYPE, 2024-2029 (USD MILLION)

- TABLE 116 EUROPE: AI VISION MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 117 EUROPE: AI VISION MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 118 GERMANY: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 119 GERMANY: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 120 UK: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 121 UK: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 122 FRANCE: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 123 FRANCE: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 124 ITALY: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 125 ITALY: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 126 REST OF EUROPE: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 127 REST OF EUROPE: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 128 ASIA PACIFIC: AI VISION MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 129 ASIA PACIFIC: AI VISION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 130 ASIA PACIFIC: AI VISION MARKET, BY VERTICAL, 2020-2023 (USD MILLION)

- TABLE 131 ASIA PACIFIC: AI VISION MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 132 ASIA PACIFIC: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 133 ASIA PACIFIC: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 134 ASIA PACIFIC: AI VISION MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 135 ASIA PACIFIC: AI VISION MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 136 ASIA PACIFIC: AI VISION MARKET FOR MACHINE LEARNING, BY TECHNOLOGY TYPE, 2020-2023 (USD MILLION)

- TABLE 137 ASIA PACIFIC: AI VISION MARKET FOR MACHINE LEARNING, BY TECHNOLOGY TYPE, 2024-2029 (USD MILLION)

- TABLE 138 ASIA PACIFIC: AI VISION MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 139 ASIA PACIFIC: AI VISION MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 140 CHINA: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 141 CHINA: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 142 JAPAN: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 143 JAPAN: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 144 SOUTH KOREA: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 145 SOUTH KOREA: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 146 REST OF ASIA PACIFIC: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 147 REST OF ASIA PACIFIC: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 148 ROW: AI VISION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 149 ROW: AI VISION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 150 ROW: AI VISION MARKET, BY VERTICAL, 2020-2023 (USD MILLION)

- TABLE 151 ROW: AI VISION MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 152 ROW: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 153 ROW: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 154 ROW: AI VISION MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 155 ROW: AI VISION MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 156 ROW: AI VISION MARKET FOR MACHINE LEARNING, BY TECHNOLOGY TYPE, 2020-2023 (USD MILLION)

- TABLE 157 ROW: AI VISION MARKET, FOR MACHINE LEARNING, BY TECHNOLOGY TYPE, 2024-2029 (USD MILLION)

- TABLE 158 ROW: AI VISION MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 159 ROW: AI VISION MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 160 MIDDLE EAST: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 161 MIDDLE EAST: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 162 AFRICA: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 163 AFRICA: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 164 SOUTH AMERICA: AI VISION MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 165 SOUTH AMERICA: AI VISION MARKET, BY MODE OF OPERATION, 2024-2029 (USD MILLION)

- TABLE 166 OVERVIEW OF STRATEGIES ADOPTED BY MAJOR COMPANIES, 2021-2024

- TABLE 167 AI VISION MARKET: DEGREE OF COMPETITION, 2023

- TABLE 168 AI VISION MARKET: MODE OF OPERATION FOOTPRINT

- TABLE 169 AI VISION MARKET: TECHNOLOGY FOOTPRINT

- TABLE 170 AI VISION MARKET: OFFERING FOOTPRINT

- TABLE 171 AI VISION MARKET: VERTICAL FOOTPRINT

- TABLE 172 AI VISION MARKET: REGION FOOTPRINT

- TABLE 173 AI VISION MARKET: LIST OF KEY STARTUPS/SMES

- TABLE 174 AI VISION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 175 AI VISION MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, JANUARY 2021-JANUARY 2025

- TABLE 176 AI VISION MARKETS MARKET: DEALS, JANUARY 2021-JANUARY 2024

- TABLE 177 NVIDIA CORPORATION: COMPANY OVERVIEW

- TABLE 178 NVIDIA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 179 NVIDIA CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 180 NVIDIA CORPORATION: DEALS

- TABLE 181 MICROSOFT CORPORATION: COMPANY OVERVIEW

- TABLE 182 MICROSOFT CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 183 MICROSOFT CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 184 MICROSOFT CORPORATION: DEALS

- TABLE 185 MICROSOFT CORPORATION: EXPANSIONS

- TABLE 186 INTEL CORPORATION: COMPANY OVERVIEW

- TABLE 187 INTEL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 188 INTEL CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 189 ALPHABET INC.: COMPANY OVERVIEW

- TABLE 190 ALPHABET INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 191 AMAZON.COM, INC.: COMPANY OVERVIEW

- TABLE 192 AMAZON.COM, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 193 AMAZON.COM, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 194 AMAZON.COM, INC.: DEALS

- TABLE 195 IBM: COMPANY OVERVIEW

- TABLE 196 IBM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 197 IBM: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 198 ORACLE: COMPANY OVERVIEW

- TABLE 199 ORACLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 200 ORACLE: DEALS

- TABLE 201 COGNEX CORPORATION: COMPANY OVERVIEW

- TABLE 202 COGNEX CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 203 COGNEX CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 204 QUALCOMM TECHNOLOGIES, INC.: COMPANY OVERVIEW

- TABLE 205 QUALCOMM TECHNOLOGIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 206 STMICROELECTRONICS: COMPANY OVERVIEW

- TABLE 207 STMICROELECTRONICS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 208 STMICROELECTRONICS: DEALS

- TABLE 209 AVNET, INC.: COMPANY OVERVIEW

- TABLE 210 AVNET, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 211 AVNET, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 212 AVEVA GROUP LIMITED: COMPANY OVERVIEW

- TABLE 213 AVEVA GROUP LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 214 AVEVA GROUP LIMITED: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 215 SYMPHONYAI: COMPANY OVERVIEW

- TABLE 216 APERA AI: COMPANY OVERVIEW

- TABLE 217 CHOOCH: COMPANY OVERVIEW

- TABLE 218 IRONYUN INC.: COMPANY OVERVIEW

- TABLE 219 KYUNGWOO SYSTECH, INC.: COMPANY OVERVIEW

- TABLE 220 LANDINGAI: COMPANY OVERVIEW

- TABLE 221 ML6: COMPANY OVERVIEW

- TABLE 222 OPENSISTEMAS: COMPANY OVERVIEW

- TABLE 223 ROBOVISION BV: COMPANY OVERVIEW

- TABLE 224 SENSETIME: COMPANY OVERVIEW

- TABLE 225 SEVENLAB: COMPANY OVERVIEW

- TABLE 226 SOLOMON TECHNOLOGY CORPORATION: COMPANY OVERVIEW

- TABLE 227 VISO.AI: COMPANY OVERVIEW

- TABLE 228 ZEBRA TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 229 AI VISION TECHNOLOGIES LLC: COMPANY OVERVIEW

- TABLE 230 HELLBENDER: COMPANY OVERVIEW

- TABLE 231 MVISION AI: COMPANY OVERVIEW

List of Figures

- FIGURE 1 AI VISION MARKET: RESEARCH DESIGN

- FIGURE 2 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2 (SUPPLY-SIDE)-IDENTIFICATION OF REVENUE GENERATED BY COMPANIES FROM SALES OF AI VISION SOLUTIONS

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 6 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 7 VISION PLATFORMS SEGMENT TO LEAD AI VISION MARKET FROM 2024 TO 2029

- FIGURE 8 IMAGE RECOGNITION SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE THROUGHOUT FORECAST PERIOD

- FIGURE 9 HEALTHCARE SEGMENT TO COMMAND AI VISION MARKET BETWEEN 2024 AND 2029

- FIGURE 10 NORTH AMERICA TO ACCOUNT FOR LARGEST SHARE OF AI VISION MARKET IN 2024

- FIGURE 11 INTEGRATION OF AI WITH CLOUD AND EDGE COMPUTING TECHNOLOGIES ACROSS INDUSTRIES TO BOOST AI VISION PLATFORM ADOPTION

- FIGURE 12 US AND MANUFACTURING VERTICAL TO HOLD LARGEST SHARE OF NORTH AMERICAN AI VISION MARKET IN 2024

- FIGURE 13 HEALTHCARE VERTICAL TO ACCOUNT FOR LARGEST SHARE OF AI VISION MARKET IN ASIA PACIFIC THROUGHOUT FORECAST PERIOD

- FIGURE 14 CHINA TO EXHIBIT HIGHEST CAGR IN GLOBAL AI VISION MARKET FROM 2024 TO 2029

- FIGURE 15 AI VISION MARKET DYNAMICS: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 16 IMPACT OF DRIVERS ON AI VISION MARKET

- FIGURE 17 IMPACT OF RESTRAINTS ON AI VISION MARKET

- FIGURE 18 IMPACT OF OPPORTUNITIES ON AI VISION MARKET

- FIGURE 19 IMPACT OF CHALLENGES ON AI VISION MARKET

- FIGURE 20 VALUE CHAIN ANALYSIS: AI VISION MARKET

- FIGURE 21 AI VISION ECOSYSTEM PARTICIPANTS

- FIGURE 22 TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

- FIGURE 23 AVERAGE SELLING PRICE TREND OF VISION PLATFORMS OFFERED BY KEY PLAYERS

- FIGURE 24 PORTER'S FIVE FORCES ANALYSIS: AI VISION MARKET

- FIGURE 25 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 VERTICALS

- FIGURE 26 KEY BUYING CRITERIA FOR TOP 3 VERTICALS

- FIGURE 27 FUNDS GATHERED BY COMPANIES IN AI VISION MARKET

- FIGURE 28 IMPORT DATA FOR HS CODE 852580-COMPLIANT PRODUCTS FOR TOP 5 COUNTRIES, 2019-20203

- FIGURE 29 EXPORT DATA FOR HS CODE 852580-COMPLIANT PRODUCTS FOR TOP 5 COUNTRIES, 2019-2023

- FIGURE 30 NUMBER OF PATENTS APPLIED AND GRANTED, 2014-2024

- FIGURE 31 VISION PLATFORMS SEGMENT TO DOMINATE AI VISION MARKET THROUGHOUT FORECAST PERIOD

- FIGURE 32 IMAGE RECOGNITION TO CAPTURE LARGEST MARKET SHARE THROUGHOUT FORECAST PERIOD

- FIGURE 33 MACHINE LEARNING TO CAPTURE LARGER SHARE OF AI VISION MARKET DURING FORECAST PERIOD

- FIGURE 34 CLOUD-BASED LEARNING SEGMENT TO HOLD LARGER SHARE OF AI VISION MARKET DURING FORECAST PERIOD

- FIGURE 35 HEALTHCARE TO HOLD LARGEST SHARE OF AI VISION MARKET IN 2029

- FIGURE 36 ASIA PACIFIC TO DOMINATE AI VISION MARKET DURING FORECAST PERIOD

- FIGURE 37 NORTH AMERICA: AI VISION MARKET SNAPSHOT

- FIGURE 38 EUROPE: AI VISION MARKET SNAPSHOT

- FIGURE 39 ASIA PACIFIC: AI VISION MARKET SNAPSHOT

- FIGURE 40 REVENUE ANALYSIS OF KEY PLAYERS IN AI VISION MARKET, 2019-2023

- FIGURE 41 MARKET SHARE ANALYSIS OF MAJOR PLAYERS, 2023

- FIGURE 42 COMPANY VALUATION, JUNE 2024

- FIGURE 43 FINANCIAL METRICS (EV/EBITDA), 2023

- FIGURE 44 BRAND/PRODUCT COMPARISON

- FIGURE 45 AI VISION MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 46 AI VISION MARKET: COMPANY FOOTPRINT

- FIGURE 47 AI VISION MARKET: COMPANY EVALUATION MATRIX (SMES/STARTUPS), 2023

- FIGURE 48 NVIDIA CORPORATION: COMPANY SNAPSHOT

- FIGURE 49 MICROSOFT CORPORATION: COMPANY SNAPSHOT

- FIGURE 50 INTEL CORPORATION: COMPANY SNAPSHOT

- FIGURE 51 ALPHABET INC.: COMPANY SNAPSHOT

- FIGURE 52 AMAZON.COM, INC.: COMPANY SNAPSHOT

- FIGURE 53 IBM: COMPANY SNAPSHOT

- FIGURE 54 ORACLE: COMPANY SNAPSHOT

- FIGURE 55 COGNEX CORPORATION: COMPANY SNAPSHOT

- FIGURE 56 QUALCOMM TECHNOLOGIES, INC.: COMPANY SNAPSHOT

- FIGURE 57 STMICROELECTRONICS: COMPANY SNAPSHOT

- FIGURE 58 AVNET, INC.: COMPANY SNAPSHOT

The global AI vision market is expected to reach USD 43.02 billion in 2029 from USD 14.85 billion in 2024, at a CAGR of 23.7% during the forecast period. The AI vision market is experiencing accelerated growth due to the high adoption of cloud computing, machine learning (ML), and deep learning (DL). Advancements in edge computing boost the demand for real-time analytics in the automotive and manufacturing sectors. However, the market faces challenges from legal as well as reputational risks and the quality of data that is required to produce a guaranteed level of accuracy. As such, the integration of AI into the next-generation vision solution is driving the market forward with some new opportunities that have emerged across various industries, such as retail, manufacturing, and healthcare.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, By Service Type, By Technology, By mode of Operation, By Vertical, and Region |

| Regions covered | North America, Europe, APAC, RoW |

"Healthcare vertical segment is expected to dominate during the forecast period."

The healthcare vertical is expected to dominate the AI vision market. This segment has the highest impact on medical diagnostics and patient care. AI vision influences the healthcare vertical by providing all-around diagnosis accuracy, individualized treatment plans, support for continuous patient monitoring, and faster decision-making. It improves efficiency and reduces hospital costs. As medical professionals increasingly rely on AI vision for critical tasks like cancer detection and surgery assistance, the demand for these technologies will continue to grow.

"Vision software segment is expected to grow at second highest CAGR in AI vision market."

The vision software segment has the second-highest growth rate in the AI vision market. Vision software is expected to experience substantial growth as it addresses the rising demand for scalable and efficient AI solutions across various verticals, such as healthcare, manufacturing, retail, and others. With continuous advancements in artificial intelligence and machine learning, these tools are becoming indispensable for tasks such as customer tracking in retail and enhancing operational efficiency in manufacturing. As organizations increasingly aim to utilize visual data for strategic decision-making, the adoption of vision software will continue to expand, solidifying its role as a vital component of the AI vision market.

"North America is projected to hold the second largest market share in the AI vision market."

North American region will hold the second largest share in the AI vision market during the forecast period. With increased technological advancements and substantial adoption in the healthcare, manufacturing, and retail industries, North America ranks as the second-largest AI vision market. Major technology companies such as Microsoft Corporation (US), NVIDIA Corporation (US), and Alphabet, Inc (US) are driving the market. At the same time, government funding for research and development in AI takes on the added support provided to this industry. Canada's focus on improving its computing infrastructure and responsible AI research capability also adds to the region's strength. Mexico is continually trying to upgrade its infrastructure and support businesses involved in AI. All these combined factors strengthen a dynamic environment that promotes innovation and ensures the integration of AI vision solutions across North America.

- By Company Type: Tier 1 - 25%, Tier 2 - 40%, and Tier 3 - 35%

- By Designation: C-level Executives - 28%, Directors - 30%, and Others - 42%

- By Region: North America- 37%, Europe - 15%, Asia Pacific- 43% and RoW- 5%

NVIDIA Corporation (US), Microsoft Corporation (US), Intel Corporation (US), Alphabet Inc. (US), Amazon.com, Inc. (US), IBM (US), Oracle (US), Cognex Corporation (US), Qualcomm Technologies, Inc. (US), STMicroelectronics (Switzerland) are some of the key players in the AI vision market.

The study includes an in-depth competitive analysis of these key players in the AI vision market, as well as their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the AI vision market by offering (Vision Software, Vision Platforms, and Custom Solutions), by service type (Behavioral Analysis, Optical Character Recognition, Spatial Analysis, Image Recognition, and Heatmap Analysis), by technology (Machine Learning (Deep Learning, and Convolutional Neural Networks), and Generative AI), by mode of operation (Edge Inferencing and Cloud-based Learning), by vertical (Transportation & Logistics, Retail, Healthcare, Manufacturing, Agriculture, Oil & Gas, Construction, and Other Verticals (Telecommunications, Automotive, Energy & Power, and Robotics)), and by region (North America, Europe, Asia Pacific, and RoW). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the AI vision market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; new product & service launches, mergers and acquisitions; and recent developments associated with the AI vision market. This report covers the competitive analysis of upcoming startups in the AI vision market ecosystem.

Reasons to buy this report

The report will help market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall AI vision market and its subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (growing inclination toward cloud computing, integration of ML and DL technologies into next-generation vision solutions, increasing adoption of edge computing, surging need for real-time analytics across automotive and manufacturing sectors), restraints (legal and reputational risks, dependence on high-quality data for accurate results), opportunities (rapid innovations in healthcare, growing demand for optical character recognition technology from AI vision system providers, increasing number of smart city projects), and challenges (complexities associated with maintenance and upgrades, high data storage and management costs, training AI vision models effectively for optimal performance) influencing the growth of the AI vision market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the AI vision market

- Market Development: The report provides comprehensive information about lucrative markets and analyses the AI vision market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the AI vision market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the AI vision market, such as NVIDIA Corporation (US), Microsoft Corporation (US), Intel Corporation (US), Alphabet Inc. (US), Amazon.com, Inc. (US), IBM (US), Oracle (US), Cognex Corporation (US), Qualcomm Technologies, Inc. (US), and STMicroelectronics (Switzerland), among others in the AI vision market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS AND EXCLUSIONS

- 1.3.2 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 MARKET STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primaries

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.3.1 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RISK ASSESSMENT

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AI VISION MARKET

- 4.2 AI VISION MARKET IN NORTH AMERICA, BY COUNTRY AND VERTICAL

- 4.3 AI VISION MARKET IN ASIA PACIFIC, BY VERTICAL

- 4.4 AI VISION MARKET, BY GEOGRAPHY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing inclination toward cloud computing

- 5.2.1.2 Integration of ML and DL technologies into next-generation vision solutions

- 5.2.1.3 Increasing adoption of edge computing

- 5.2.1.4 Surging need for real-time analytics across automotive and manufacturing sectors

- 5.2.2 RESTRAINTS

- 5.2.2.1 Legal and reputational risks

- 5.2.2.2 Dependence on high-quality data for accurate results

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rapid innovations in healthcare

- 5.2.3.2 Growing demand for optical character recognition technology from AI vision system providers

- 5.2.3.3 Increasing number of smart city projects

- 5.2.3.4 Enhancing proactive monitoring with AI vision in security and surveillance

- 5.2.4 CHALLENGES

- 5.2.4.1 Complexities associated with system maintenance and upgrades

- 5.2.4.2 High data storage and management costs

- 5.2.4.3 Training AI vision models effectively for optimal performance

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY OFFERING

- 5.6.2 AVERAGE SELLING PRICE TREND OF VISION PLATFORMS OFFERED BY KEY PLAYERS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Edge computing

- 5.7.1.2 Machine learning

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Internet of Things (IoT)

- 5.7.2.2 5G connectivity

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Deep learning

- 5.7.3.2 Augmented natural language processing (NLP)

- 5.7.1 KEY TECHNOLOGIES

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.8.2 BARGAINING POWER OF SUPPLIERS

- 5.8.3 BARGAINING POWER OF BUYERS

- 5.8.4 THREAT OF SUBSTITUTES

- 5.8.5 THREAT OF NEW ENTRANTS

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.9.2 BUYING CRITERIA

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 WATER UTILITY COMPANY IMPLEMENTED IRONYUN'S VAIDIO AI VISION PLATFORM TO AVOID FALSE ALERTS

- 5.10.2 MIDWEST POLICE DEPARTMENT DEPLOYED IRONYUN'S VAIDIO LPR AND VIDEO SEARCH SOLUTIONS FOR FASTER CRIME DETECTION AND INVESTIGATION

- 5.10.3 BENGALURU AIRPORT EMPLOYED INDUSTRY.AI'S VISION AI PLATFORM AND NVIDIA'S AI TOOLS TO ENSURE REAL-TIME MONITORING AND EFFECTIVE TERMINAL MANAGEMENT

- 5.10.4 PEPSICO IMPLEMENTED KOIREADER TECHNOLOGIES' AI-POWERED MACHINE VISION TECHNOLOGY TO ENHANCE LABEL AND BARCODE SCANNING ACCURACY

- 5.10.5 MULTINATION PHARMA COMPANY DEPLOYED SOLOMON'S SOLVISION AI TO DETECT DEFECTIVE TABLETS IN REAL TIME

- 5.11 INVESTMENT AND FUNDING SCENARIO

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT DATA (HS CODE 852580)

- 5.12.2 EXPORT DATA (HS CODE 852580)

- 5.13 PATENT ANALYSIS

- 5.14 KEY CONFERENCES AND EVENTS, 2024-2026

- 5.15 REGULATORY LANDSCAPE

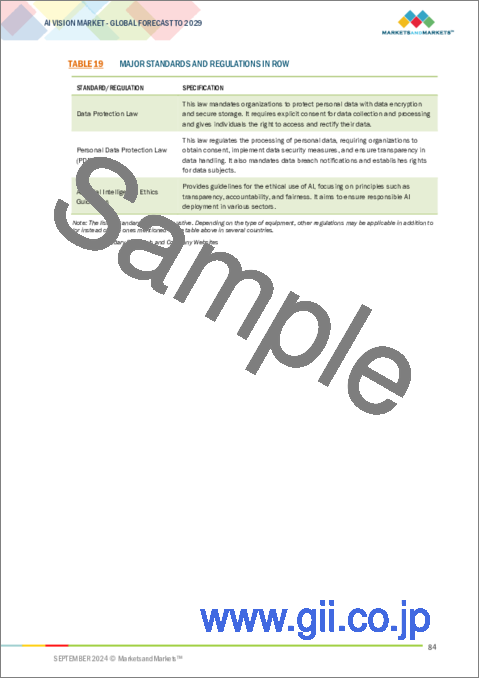

- 5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15.2 STANDARDS AND REGULATIONS

6 USE CASES FOR AI VISION

- 6.1 INTRODUCTION

- 6.2 AUTONOMOUS VEHICLES

- 6.3 AUGMENTED REALITY DEVICES

- 6.4 ROBOTIC VISION SYSTEMS

- 6.5 3D PRINTERS

- 6.6 MEDICAL IMAGING SOLUTIONS

- 6.7 TRAFFIC MONITORING SYSTEMS

- 6.8 AUTOMATED LICENSE PLATE RECOGNITION SYSTEMS

- 6.9 SECURITY AND SURVEILLANCE SYSTEMS

- 6.10 DIGITAL ASSET MANAGEMENT SOLUTIONS

7 AI VISION MARKET, BY OFFERING

- 7.1 INTRODUCTION

- 7.2 VISION PLATFORMS

- 7.2.1 PRESSING NEED FOR REAL-TIME DATA ANALYSIS TO DRIVE SEGMENTAL GROWTH

- 7.3 VISION SOFTWARE

- 7.3.1 APPLICATION PROGRAMMING INTERFACES

- 7.3.1.1 Growing demand for cloud services to accelerate segmental growth

- 7.3.2 SOFTWARE DEVELOPMENT KITS

- 7.3.2.1 Increasing investments in AI and ML technologies to fuel segmental growth

- 7.3.1 APPLICATION PROGRAMMING INTERFACES

- 7.4 CUSTOM SOLUTIONS

- 7.4.1 ADVANCEMENTS IN EDGE COMPUTING TO SUPPORT MARKET GROWTH

8 AI VISION MARKET, BY SERVICE TYPE

- 8.1 INTRODUCTION

- 8.2 BEHAVIORAL ANALYSIS

- 8.2.1 GROWING NEED TO MONITOR CROWD BEHAVIOR IN PUBLIC PLACES TO ACCELERATE MARKET GROWTH

- 8.2.2 FACIAL RECOGNITION

- 8.3 OPTICAL CHARACTER RECOGNITION

- 8.3.1 INCREASING AUTOMATION IN DATA PROCESSING AND DOCUMENT MANAGEMENT TO BOOST MARKET GROWTH

- 8.4 SPATIAL ANALYSIS

- 8.4.1 MOTION DETECTION

- 8.4.1.1 Elevating deployment of smart home and home automation devices to boost segmental growth

- 8.4.2 INTRUSION DETECTION

- 8.4.2.1 Increasing cyberattacks and rising security threats to drive market

- 8.4.3 MONITORING SURROUNDINGS

- 8.4.3.1 Increasing smart city projects to foster market growth

- 8.4.1 MOTION DETECTION

- 8.5 IMAGE RECOGNITION

- 8.5.1 GOVERNMENT INVESTMENTS TO MINIMIZE RETAIL CRIMES TO SUPPORT MARKET GROWTH

- 8.6 HEATMAP ANALYSIS

- 8.6.1 INCREASING DEMAND FOR ADVANCED CROWD MANAGEMENT SOLUTIONS TO DRIVE MARKET

- 8.6.2 CROWD DENSITY ANALYSIS

9 AI VISION MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 MACHINE LEARNING

- 9.2.1 DEEP LEARNING

- 9.2.1.1 Government and private sector funding for R&D in AI and DL to foster market growth

- 9.2.2 CONVOLUTIONAL NEURAL NETWORKS

- 9.2.2.1 Increasing use of automation across several industries to boost segmental growth

- 9.2.1 DEEP LEARNING

- 9.3 GENERATIVE AI

- 9.3.1 RISING NEED FOR SOPHISTICATED CONTENT CREATION TO SUPPORT MARKET GROWTH

10 AI VISION MARKET, BY MODE OF OPERATION

- 10.1 INTRODUCTION

- 10.2 EDGE INFERENCING

- 10.2.1 EASY SETUP AND TRAINING PROCESS TO BOOST ADOPTION

- 10.3 CLOUD-BASED LEARNING

- 10.3.1 RISING DEMAND FOR SCALABLE, EFFICIENT, AND ACCESSIBLE AI SOLUTIONS TO DRIVE MARKET

11 AI VISION MARKET, BY VERTICAL

- 11.1 INTRODUCTION

- 11.2 TRANSPORTATION & LOGISTICS

- 11.2.1 INVESTMENT IN ADVANCED LOGISTICS HUBS AND WAREHOUSES TO BOOST SEGMENTAL GROWTH

- 11.3 RETAIL

- 11.3.1 GROWING FOCUS OF RETAIL SECTOR ON INVENTORY MANAGEMENT AND CUSTOMER BEHAVIOR ANALYSIS TO DRIVE MARKET

- 11.4 HEALTHCARE

- 11.4.1 PRESSING NEED FOR ACCURATE AND EFFICIENT MEDICAL DIAGNOSTICS AND IMPROVED PATIENT CARE TO ACCELERATE DEMAND

- 11.5 MANUFACTURING

- 11.5.1 ABILITY OF AI VISION TO DETECT MINUTE DEFECTS AND ENSURE COMPLIANCE WITH QUALITY STANDARDS TO STIMULATE DEMAND

- 11.6 AGRICULTURE

- 11.6.1 INVESTMENTS IN ADVANCED AGRICULTURAL TECHNOLOGIES TO BOOST SEGMENT GROWTH

- 11.7 OIL & GAS

- 11.7.1 RISING FOCUS OF OIL AND GAS COMPANIES ON AUTOMATING COMPLEX PROCESSES TO FUEL MARKET GROWTH

- 11.8 CONSTRUCTION

- 11.8.1 ESCALATING REQUIREMENT TO TRACK PROGRESS AGAINST PROJECT TIMELINES TO CREATE OPPORTUNITIES

- 11.9 OTHER VERTICALS

12 AI VISION MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC FACTORS FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 Increasing investments by government and technology giants in cutting-edge technologies to drive market

- 12.2.3 CANADA

- 12.2.3.1 Strategic government investments in AI infrastructure development to fuel market growth

- 12.2.4 MEXICO

- 12.2.4.1 Surging adoption of AI-powered solutions in manufacturing sector to boost market growth

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC FACTORS FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Increasing number of AI startups to contribute to market growth

- 12.3.3 UK

- 12.3.3.1 Commitment to becoming global leader in artificial intelligence to accelerate market growth

- 12.3.4 FRANCE

- 12.3.4.1 Robust research and strategic investments in establishing AI startups to fuel market growth

- 12.3.5 ITALY

- 12.3.5.1 Significant focus on developing and scaling AI vision technologies to create growth opportunities

- 12.3.6 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC FACTORS FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 Ventures between research institutions and entrepreneurs to drive market

- 12.4.3 JAPAN

- 12.4.3.1 Investment in digital skilling programs to accelerate market growth

- 12.4.4 SOUTH KOREA

- 12.4.4.1 Startup Koria policy and government investment in AI development to support market growth

- 12.4.5 REST OF ASIA PACIFIC

- 12.5 ROW

- 12.5.1 MACROECONOMIC FACTORS FOR ROW

- 12.5.2 MIDDLE EAST

- 12.5.2.1 Strategic investments in digital transformation and innovation to spike demand

- 12.5.2.2 GCC countries

- 12.5.2.3 Rest of Middle East & Africa

- 12.5.3 AFRICA

- 12.5.3.1 International collaborations funding AI projects to boost market growth

- 12.5.4 SOUTH AMERICA

- 12.5.4.1 Increasing public-private sector investments in AI technology to fuel market growth

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2024

- 13.3 REVENUE ANALYSIS, 2019-2023

- 13.4 MARKET SHARE ANALYSIS, 2023

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- 13.7.5.1 Company footprint

- 13.7.5.2 Mode of operation footprint

- 13.7.5.3 Technology footprint

- 13.7.5.4 Offering footprint

- 13.7.5.5 Vertical footprint

- 13.7.5.6 Region footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2023

- 13.8.5.1 Detailed list of startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 13.9.2 DEALS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 NVIDIA CORPORATION

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches/Developments

- 14.1.1.3.2 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses

- 14.1.2 MICROSOFT CORPORATION

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches/Developments

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses

- 14.1.3 INTEL CORPORATION

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services Offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches/Developments

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses

- 14.1.4 ALPHABET INC.

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Key strengths

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses

- 14.1.5 AMAZON.COM, INC.

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches/Developments

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses

- 14.1.6 IBM

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches/Developments

- 14.1.7 ORACLE

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Deals

- 14.1.8 COGNEX CORPORATION

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches/Developments

- 14.1.9 QUALCOMM TECHNOLOGIES, INC.

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.10 STMICROELECTRONICS

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.11 AVNET, INC.

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches/Developments

- 14.1.12 AVEVA GROUP LIMITED

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Product launches/Developments

- 14.1.1 NVIDIA CORPORATION

- 14.2 OTHER PLAYERS

- 14.2.1 SYMPHONYAI

- 14.2.2 APERA AI

- 14.2.3 CHOOCH

- 14.2.4 IRONYUN INC.

- 14.2.5 KYUNGWOO SYSTECH, INC.

- 14.2.6 LANDINGAI

- 14.2.7 ML6

- 14.2.8 OPENSISTEMAS

- 14.2.9 ROBOVISION BV

- 14.2.10 SENSETIME

- 14.2.11 SEVENLAB

- 14.2.12 SOLOMON TECHNOLOGY CORPORATION

- 14.2.13 VISO.AI

- 14.2.14 ZEBRA TECHNOLOGIES

- 14.2.15 AI VISION TECHNOLOGIES LLC

- 14.2.16 HELLBENDER

- 14.2.17 MVISION AI

15 APPENDIX

- 15.1 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.2 CUSTOMIZATION OPTIONS

- 15.3 RELATED REPORTS

- 15.4 AUTHOR DETAILS