|

|

市場調査レポート

商品コード

1554600

SDDC (ソフトウェア定義データセンター) の世界市場:SDコンピューティング・SDストレージ・SDネットワーキング・オートメーション別 (~2029年)Software-Defined Data Center Market by Software-Defined Computing, Software-Defined Storage, Software-Defined Networking, Automation - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| SDDC (ソフトウェア定義データセンター) の世界市場:SDコンピューティング・SDストレージ・SDネットワーキング・オートメーション別 (~2029年) |

|

出版日: 2024年08月28日

発行: MarketsandMarkets

ページ情報: 英文 240 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界のSDDC (ソフトウェア定義データセンター) の市場規模は、2024年の759億米ドルから、予測期間中はCAGR 19.4%で推移し、2029年には1,845億米ドルの規模に成長すると予測されています。

SDDC市場は、完全なインフラ管理、高度な自動化、リアルタイムのリソースの最適化を組み合わせることから、企業、通信サービスプロバイダー、クラウドサービスプロバイダー、マネージドサービスプロバイダーなど、さまざまなセグメントで人気を集めています。SDDCは、仮想化の完全な管理、自動供給、リソース割り当て、セキュリティの向上を提供します。生産性を向上し、成長要件に適合し、IT投資からのリターンを最適化するために、SDDCを利用する組織がますます増えています。これらのソリューションは、AI、自動化、現在のITシステムとのシームレスな相互作用によるコンピューティング、ストレージ、ネットワークの仮想化に焦点を当てています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2019-2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024-2029年 |

| 検討単位 | 米ドル |

| セグメント | 提供区分・ソリューション・組織規模・エンドユーザー |

| 対象地域 | 北米・欧州・アジア太平洋・中東&アフリカ、ラテンアメリカ |

エンドユーザー別では、マネージドサービスプロバイダー (MSP) の部門が予測期間中にCAGRがもっとも高い見通しです。MSPは、SDDCを活用してソフトウェアですべてのデータセンター資産を管理し、より優れた自動化、迅速な対応、よりインテリジェントなリソースの活用を実現しています。このアプローチは、MSPがカスタマイズされたオンデマンドサービスを提供するのに役立ち、これは今日の変化するIT情勢に不可欠です。さらにSDDCは、MSPが顧客の要求をより迅速かつ効率的に満たすことをサポートします。また、SDDCにSDNとSDSを含めることで、MSPは複雑なネットワークと大規模なストレージシステムを管理するための新しい機能を得ることができます。

SDDCに影響を与える主な動向には、ハイブリッドクラウドソリューションに対する需要の高まりがあり、SDDCはオンプレミスとクラウドシステムを制御し組み合わせる上で重要な役割を果たします。もう1つの動向は、運用における自動化とAIの台頭であり、SDDC内に予測保守と自動化プロセスを統合することで、サービスデリバリーを改善し、ダウンタイムを最小化します。

組織規模では、大企業の部門が予測期間中に最大のシェアを示す見通しです。SDDCは、大企業の複雑なITシステムを処理するための堅牢で適応性の高いソリューションを提供します。大企業におけるSDDCの導入は、リソースの迅速なセットアップと拡張を支援し、広範なワークロードとグローバルな運用の変化する要求に対応します。また、自動化されたセットアップとルールによりリソースを有効活用し、ランニングコストを削減し、企業の目標に適合させられます。SDDCシステム内の監視と分析のための組み込みツールは、物事が正しく実行されているか、セキュリティがどのように維持されているか、ルールがどのように守られているかを明確に表示し、積極的な管理と微調整を可能にします。

SDDCは現在のITセットアップとスムーズに連携し、ハイブリッドクラウドやマルチクラウド環境をサポートし、レガシーシステムとの相互運用性を確保します。この柔軟性により、大企業は広範なITエコシステムをコントロールしながら、市場環境の変化に対応し、イノベーションを起こすことができます。

当レポートでは、世界のSDDC (ソフトウェア定義データセンター) の市場を調査し、市場概要、市場成長への各種影響因子の分析、技術・特許の動向、法規制環境、ケーススタディ、市場規模の推移・予測、各種区分・地域別の詳細分析、競合環境、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要と業界動向

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 顧客の事業に影響を与える動向/ディスラプション

- 価格分析

- サプライチェーン分析

- エコシステム

- 技術分析

- 主要技術

- 補完的技術

- 隣接技術

- 特許分析

- 主な会議とイベント

- 規制状況

- ポーターのファイブフォース分析

- 購入プロセスにおける主要なステークホルダー

- 購入基準

- ビジネスモデル分析

- 投資と資金調達のシナリオ

- SDデータセンター市場の将来

- AI/生成AIがSDデータセンター市場に与える影響

- ケーススタディ分析

第6章 SDDC (ソフトウェア定義データセンター) 市場:提供内容別

- ソリューション

- サービス

- トレーニング・コンサルティング

- 統合・展開

- サポート・メンテナンス

第7章 SDDC (ソフトウェア定義データセンター) 市場:ソリューション別

- SDコンピューティング

- 仮想化プラットフォーム

- ハイパーバイザー

- 管理ツール

- SDストレージ

- ストレージ仮想化ソフトウェア

- ストレージ管理ソフトウェア

- ハイパーコンバージドインフラストラクチャ (HCI)

- SDネットワーク

- SDネットワークコントローラ

- SDネットワークインフラ (スイッチ、ルーター)

- ネットワーク仮想化ソフトウェア

- 管理・運営

- 自動化・オーケストレーション

- 管理・監視

第8章 SDDC (ソフトウェア定義データセンター) 市場:組織規模別

- 中小企業

- 大企業

第9章 SDDC (ソフトウェア定義データセンター) 市場:エンドユーザー別

- 企業

- 通信サービスプロバイダー

- クラウドサービスプロバイダー

- マネージドサービスプロバイダー

第10章 SDDC (ソフトウェア定義データセンター) 市場:地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第11章 競合情勢

- 概要

- 主要企業の戦略/有力企業

- 収益分析

- 市場シェア分析

- 企業評価マトリックス:主要企業

- 企業評価マトリックス:スタートアップ/中小企業

- 企業価値評価と財務指標

- ブランド/製品比較

- 競合シナリオと動向

第12章 企業プロファイル

- 主要企業

- VMWARE

- MICROSOFT

- CISCO

- HPE

- IBM

- DELL TECHNOLOGIES

- ORACLE

- NUTANIX

- HUAWEI

- FUJITSU

- その他の企業

- JUNIPER NETWORKS

- COMMVAULT

- ARISTA NETWORKS

- DATACORE SOFTWARE

- SCALITY

- SUSE

- NETAPP

- CITRIX

- NUAGE NETWORKS

- LENOVO

- RACKSPACE TECHNOLOGY

- スタートアップ/SME

- LIGHTBITS

- HIVEIO

- WHIZWORKS

- PI SYSTEMS AND NETWORKS

第13章 隣接/関連市場

第14章 付録

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2019-2023

- TABLE 2 FACTOR ANALYSIS

- TABLE 3 SOFTWARE-DEFINED DATA CENTER MARKET SIZE AND GROWTH, 2019-2023 (USD MILLION, Y-O-Y)

- TABLE 4 SOFTWARE-DEFINED DATA CENTER MARKET SIZE AND GROWTH, 2024-2029 (USD MILLION, Y-O-Y)

- TABLE 5 INDICATIVE PRICING LEVELS OF SOFTWARE-DEFINED DATA CENTER SOLUTIONS

- TABLE 6 INDICATIVE PRICING ANALYSIS, BY REGION

- TABLE 7 TOP TEN PATENT OWNERS IN LAST 10 YEARS

- TABLE 8 SOFTWARE-DEFINED DATA CENTER MARKET: KEY CONFERENCES AND EVENTS IN 2024-2025

- TABLE 9 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 PORTER'S FIVE FORCES' IMPACT ON SOFTWARE-DEFINED DATA CENTER MARKET

- TABLE 14 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- TABLE 15 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 16 SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 17 SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 18 SOLUTIONS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 19 SOLUTIONS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 20 SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2019-2023 (USD MILLION)

- TABLE 21 SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2024-2029 (USD MILLION)

- TABLE 22 SERVICES: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 23 SERVICES: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 24 TRAINING & CONSULTING: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 25 TRAINING & CONSULTING: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 26 INTEGRATION & DEPLOYMENT: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 27 INTEGRATION & DEPLOYMENT: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 28 SUPPORT & MAINTENANCE: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 29 SUPPORT & MAINTENANCE: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 30 SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2019-2023 (USD MILLION)

- TABLE 31 SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2024-2029 (USD MILLION)

- TABLE 32 SOFTWARE-DEFINED COMPUTING: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 33 SOFTWARE-DEFINED COMPUTING: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 34 SOFTWARE-DEFINED COMPUTING: SOFTWARE-DEFINED DATA CENTER MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 35 SOFTWARE-DEFINED COMPUTING: SOFTWARE-DEFINED DATA CENTER MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 36 SOFTWARE-DEFINED STORAGE: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 37 SOFTWARE-DEFINED STORAGE: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 38 SOFTWARE-DEFINED STORAGE: SOFTWARE-DEFINED DATA CENTER MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 39 SOFTWARE-DEFINED STORAGE: SOFTWARE-DEFINED DATA CENTER MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 40 SOFTWARE-DEFINED NETWORKING: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 41 SOFTWARE-DEFINED NETWORKING: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 42 SOFTWARE-DEFINED NETWORKING: SOFTWARE-DEFINED DATA CENTER MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 43 SOFTWARE-DEFINED NETWORKING: SOFTWARE-DEFINED DATA CENTER MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 44 MANAGEMENT & OPERATIONS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 45 MANAGEMENT & OPERATIONS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 46 SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 47 SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 48 SMALL AND MEDIUM-SIZED ENTERPRISES: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 49 SMALL AND MEDIUM-SIZED ENTERPRISES: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 50 LARGE ENTERPRISES: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 51 LARGE ENTERPRISES: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 52 SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 53 SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 54 ENTERPRISES: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 55 ENTERPRISES: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 56 TELECOM SERVICE PROVIDERS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 57 TELECOM SERVICE PROVIDERS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 58 CLOUD SERVICE PROVIDERS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 59 CLOUD SERVICE PROVIDERS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 60 MANAGED SERVICE PROVIDERS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 61 MANAGED SERVICE PROVIDERS: SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 62 SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 63 SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 64 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 65 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 66 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2019-2023 (USD MILLION)

- TABLE 67 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2024-2029 (USD MILLION)

- TABLE 68 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2019-2023 (USD MILLION)

- TABLE 69 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2024-2029 (USD MILLION)

- TABLE 70 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 71 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 72 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 73 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 74 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 75 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 76 US: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 77 US: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 78 US: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 79 US: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 80 CANADA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 81 CANADA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 82 CANADA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 83 CANADA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 84 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 85 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 86 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2019-2023 (USD MILLION)

- TABLE 87 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2024-2029 (USD MILLION)

- TABLE 88 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2019-2023 (USD MILLION)

- TABLE 89 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2024-2029 (USD MILLION)

- TABLE 90 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 91 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 92 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 93 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 94 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 95 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 96 UK: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 97 UK: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 98 UK: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 99 UK: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 100 GERMANY: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 101 GERMANY: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 102 GERMANY: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 103 GERMANY: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 104 FRANCE: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 105 FRANCE: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 106 FRANCE: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 107 FRANCE: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 108 ITALY: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 109 ITALY: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 110 ITALY: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 111 ITALY: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 112 REST OF EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 113 REST OF EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 114 REST OF EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 115 REST OF EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 116 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 117 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 118 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2019-2023 (USD MILLION)

- TABLE 119 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2024-2029 (USD MILLION)

- TABLE 120 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2019-2023 (USD MILLION)

- TABLE 121 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2024-2029 (USD MILLION)

- TABLE 122 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 123 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 124 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 125 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 126 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 127 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 128 CHINA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 129 CHINA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 130 CHINA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 131 CHINA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 132 JAPAN: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 133 JAPAN: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 134 JAPAN: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 135 JAPAN: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 136 AUSTRALIA & NEW ZEALAND: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 137 AUSTRALIA & NEW ZEALAND: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 138 AUSTRALIA & NEW ZEALAND: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 139 AUSTRALIA & NEW ZEALAND: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 140 REST OF ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 141 REST OF ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 142 REST OF ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 143 REST OF ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 144 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 145 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 146 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2019-2023 (USD MILLION)

- TABLE 147 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2024-2029 (USD MILLION)

- TABLE 148 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2019-2023 (USD MILLION)

- TABLE 149 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2024-2029 (USD MILLION)

- TABLE 150 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 151 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 152 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 153 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 154 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 155 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 156 GULF COOPERATION COUNCIL COUNTRIES: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 157 GULF COOPERATION COUNCIL COUNTRIES: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 158 GULF COOPERATION COUNCIL COUNTRIES: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 159 GULF COOPERATION COUNCIL COUNTRIES: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 160 SOUTH AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 161 SOUTH AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 162 SOUTH AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 163 SOUTH AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 164 REST OF MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 165 REST OF MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 166 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 167 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 168 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2019-2023 (USD MILLION)

- TABLE 169 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SERVICE, 2024-2029 (USD MILLION)

- TABLE 170 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2019-2023 (USD MILLION)

- TABLE 171 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION, 2024-2029 (USD MILLION)

- TABLE 172 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 173 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 174 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 175 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 176 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 177 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 178 BRAZIL: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 179 BRAZIL: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 180 BRAZIL: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 181 BRAZIL: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 182 MEXICO: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 183 MEXICO: SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 184 MEXICO: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 185 MEXICO: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 186 REST OF LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2019-2023 (USD MILLION)

- TABLE 187 REST OF LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 188 OVERVIEW OF STRATEGIES ADOPTED BY KEY SOFTWARE-DEFINED DATA CENTER MARKET VENDORS

- TABLE 189 SOFTWARE-DEFINED DATA CENTER MARKET: DEGREE OF COMPETITION

- TABLE 190 SOFTWARE-DEFINED DATA CENTER MARKET: OFFERING FOOTPRINT

- TABLE 191 SOFTWARE-DEFINED DATA CENTER MARKET: SOLUTION FOOTPRINT

- TABLE 192 SOFTWARE-DEFINED DATA CENTER MARKET: END-USER FOOTPRINT

- TABLE 193 SOFTWARE-DEFINED DATA CENTER MARKET: REGIONAL FOOTPRINT

- TABLE 194 SOFTWARE-DEFINED DATA CENTER MARKET: KEY START-UPS/SMES

- TABLE 195 SOFTWARE-DEFINED DATA CENTER MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- TABLE 196 SOFTWARE-DEFINED DATA CENTER MARKET: PRODUCT LAUNCHES AND ENHANCEMENTS, MARCH 2021-JULY 2024

- TABLE 197 SOFTWARE-DEFINED DATA CENTER MARKET: DEALS, MARCH 2021-JULY 2024

- TABLE 198 VMWARE: COMPANY OVERVIEW

- TABLE 199 VMWARE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 200 VMWARE: PRODUCT LAUNCHES

- TABLE 201 VMWARE: DEALS

- TABLE 202 MICROSOFT: COMPANY OVERVIEW

- TABLE 203 MICROSOFT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 204 MICROSOFT: PRODUCT LAUNCHES

- TABLE 205 CISCO: COMPANY OVERVIEW

- TABLE 206 CISCO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 207 CISCO: PRODUCT LAUNCHES

- TABLE 208 CISCO: DEALS

- TABLE 209 HPE: COMPANY OVERVIEW

- TABLE 210 HPE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 211 HPE: PRODUCT ENHANCEMENTS

- TABLE 212 HPE: DEALS

- TABLE 213 IBM: COMPANY OVERVIEW

- TABLE 214 IBM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 215 IBM: PRODUCT LAUNCHES

- TABLE 216 IBM: DEALS

- TABLE 217 DELL TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 218 DELL TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 219 DELL TECHNOLOGIES: PRODUCT LAUNCHES

- TABLE 220 ORACLE: COMPANY OVERVIEW

- TABLE 221 ORACLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 222 ORACLE: DEALS

- TABLE 223 NUTANIX: COMPANY OVERVIEW

- TABLE 224 NUTANIX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 225 NUTANIX: PRODUCT ENHANCEMENTS

- TABLE 226 NUTANIX: DEALS

- TABLE 227 HUAWEI: COMPANY OVERVIEW

- TABLE 228 HUAWEI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 229 HUAWEI: PRODUCT LAUNCHES

- TABLE 230 HUAWEI: DEALS

- TABLE 231 FUJITSU: COMPANY OVERVIEW

- TABLE 232 FUJITSU: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 233 FUJITSU: PRODUCT LAUNCHES

- TABLE 234 HYPER-CONVERGED INFRASTRUCTURE MARKET, BY COMPONENT, 2016-2019 (USD MILLION)

- TABLE 235 HYPER-CONVERGED INFRASTRUCTURE MARKET, BY COMPONENT, 2020-2025 (USD MILLION)

- TABLE 236 HYPER-CONVERGED INFRASTRUCTURE MARKET, BY APPLICATION, 2016-2019 (USD MILLION)

- TABLE 237 HYPER-CONVERGED INFRASTRUCTURE MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 238 HYPER-CONVERGED INFRASTRUCTURE MARKET, BY ENTERPRISE, 2016-2019 (USD MILLION)

- TABLE 239 HYPER-CONVERGED INFRASTRUCTURE MARKET, BY ENTERPRISE, 2020-2025 (USD MILLION)

List of Figures

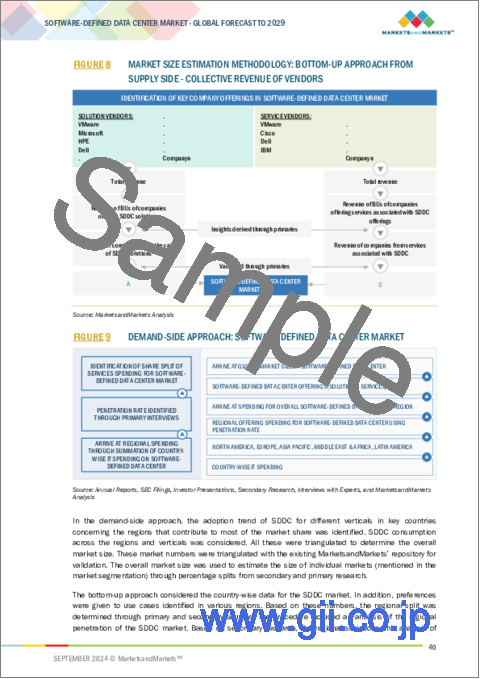

- FIGURE 1 SOFTWARE-DEFINED DATA CENTER MARKET: RESEARCH DESIGN

- FIGURE 2 DATA TRIANGULATION

- FIGURE 3 SOFTWARE-DEFINED DATA CENTER MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 6 SOFTWARE-DEFINED DATA CENTER MARKET: RESEARCH FLOW

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

- FIGURE 8 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH FROM SUPPLY SIDE - COLLECTIVE REVENUE OF VENDORS

- FIGURE 9 DEMAND-SIDE APPROACH: SOFTWARE-DEFINED DATA CENTER MARKET

- FIGURE 10 GLOBAL SOFTWARE-DEFINED DATA CENTER MARKET TO WITNESS SIGNIFICANT GROWTH, 2019-2029 (USD MILLION, Y-O-Y)

- FIGURE 11 FASTEST-GROWING SEGMENTS IN SOFTWARE-DEFINED DATA CENTER MARKET, 2024-2029

- FIGURE 12 SOFTWARE-DEFINED DATA CENTER MARKET: REGIONAL SNAPSHOT

- FIGURE 13 INCREASING DEMAND FOR RESILIENT INFRASTRUCTURE TO ELIMINATE SYSTEM OUTAGES AND AUGMENT SERVICE UPTIME TO DRIVE MARKET

- FIGURE 14 SOLUTIONS SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 15 SOFTWARE-DEFINED COMPUTING SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 16 LARGE ENTERPRISES SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 17 ENTERPRISES SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 18 ASIA PACIFIC TO EMERGE AS BEST MARKET FOR INVESTMENT IN NEXT FIVE YEARS

- FIGURE 19 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: SOFTWARE-DEFINED DATA CENTER MARKET

- FIGURE 20 SOFTWARE-DEFINED DATA CENTER MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 21 SOFTWARE-DEFINED DATA CENTER MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 22 KEY PLAYERS IN SOFTWARE-DEFINED DATA CENTER MARKET ECOSYSTEM

- FIGURE 23 NUMBER OF PATENTS PUBLISHED, 2013-2023

- FIGURE 24 TOP 10 PATENT APPLICANTS (GLOBAL) IN 2023

- FIGURE 25 PORTER'S FIVE FORCES ANALYSIS: SOFTWARE-DEFINED DATA CENTER MARKET

- FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- FIGURE 27 KEY BUYING CRITERIA FOR TOP THREE END USERS

- FIGURE 28 LEADING GLOBAL SOFTWARE-DEFINED DATA CENTER MARKET VENDORS, BY NUMBER OF INVESTORS AND FUNDING ROUNDS, 2023

- FIGURE 29 IMPACT OF GENERATIVE AI ON SOFTWARE-DEFINED DATA CENTER, 2023

- FIGURE 30 SERVICES SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 31 SUPPORT & MAINTENANCE SERVICES SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 32 SOFTWARE-DEFINED NETWORKING SOLUTIONS SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 33 SMALL AND MEDIUM-SIZED ENTERPRISES SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 34 ENTERPRISES SEGMENT TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- FIGURE 35 NORTH AMERICA TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- FIGURE 36 NORTH AMERICA: MARKET SNAPSHOT

- FIGURE 37 ASIA PACIFIC: MARKET SNAPSHOT

- FIGURE 38 REVENUE ANALYSIS FOR KEY COMPANIES IN LAST THREE YEARS

- FIGURE 39 MARKET SHARE ANALYSIS, 2023

- FIGURE 40 SOFTWARE-DEFINED DATA CENTER MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 41 SOFTWARE-DEFINED DATA CENTER MARKET: COMPANY FOOTPRINT

- FIGURE 42 SOFTWARE-DEFINED DATA CENTER MARKET: COMPANY EVALUATION MATRIX (START-UPS/SMES), 2023

- FIGURE 43 COMPANY VALUATION

- FIGURE 44 FINANCIAL METRICS AS PER KEY SOFTWARE-DEFINED DATA CENTER VENDORS

- FIGURE 45 BRAND/PRODUCT COMPARISON

- FIGURE 46 VMWARE: COMPANY SNAPSHOT

- FIGURE 47 MICROSOFT: COMPANY SNAPSHOT

- FIGURE 48 CISCO: COMPANY SNAPSHOT

- FIGURE 49 HPE: COMPANY SNAPSHOT

- FIGURE 50 IBM: COMPANY SNAPSHOT

- FIGURE 51 DELL TECHNOLOGIES: COMPANY SNAPSHOT

- FIGURE 52 ORACLE: COMPANY SNAPSHOT

- FIGURE 53 NUTANIX: COMPANY SNAPSHOT

- FIGURE 54 FUJITSU: COMPANY SNAPSHOT

The global SDDC market will grow from USD 75.9 billion in 2024 to USD 184.5 billion by 2029 at a compounded annual growth rate (CAGR) of 19.4% during the forecast period. The SDDC market is gaining popularity in various segments, including enterprises, telecom service providers, cloud service providers, and managed service providers, by combining complete infrastructure management, advanced automation, and real-time resource optimization. This SDDC provides complete administration of virtualization, automatic supplies, resource allocation, and improved security. More and more organizations are now turning to SDDC to increase productivity, conform to growth requirements, and optimize the return from IT investments. The solutions focus on computing, storage, and network virtualization powered by AI, automation, and seamless interaction with current IT systems.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | USD (Billion) |

| Segments | Offering, Solutions, Organization Size, End Users |

| Regions covered | North America, Europe, Asia Pacific, Middle East Africa, and Latin America |

By end user, the managed service providers hold the highest CAGR during the forecast period.

Managed service providers utilize SDDC to manage all data center assets using software, leading to better automation, quicker responses, and more intelligent use of resources. This approach helps MSPs offer customized and on-demand services, which is essential in today's changing IT landscape. In addition, SDDC supports MSPs to satisfy customer demands more quickly and efficiently. Also, including SDN and SDS in SDDC gives MSPs new functionality for managing complicated networks and large-scale storage systems.

Major trends affecting SDDC include increased demand for hybrid cloud solutions, in which SDDC plays a vital role in controlling and combining on-premises and cloud systems. Another trend is the rise of automation and artificial intelligence in operations, integrating predictive maintenance and automated processes within the SDDC to improve service delivery and minimize downtime.

The large enterprises segment holds the largest market share during the forecast period based on organization size.

The SDDC market is divided by organization size into large enterprises and SMEs. The large enterprise segment holds the largest market share. Organizations with an employee strength of more than 1,000 can be considered large enterprises. SDDC provides robust and adaptable solutions for handling complicated IT systems in large enterprises. The deployment of SDDC in large enterprises helps quickly set up and expand resources, meeting the changing demands of extensive workloads and global operations. It also makes better use of resources with automated setups and rules, reduces running costs, and matches company goals. Built-in tools for monitoring and analyzing within SDDC systems give clear views on how things are running correctly, how security is maintained, and how rules are followed, enabling active management and fine-tuning.

SDDC works smoothly with current IT setups, supporting hybrid and multi-cloud environments and ensuring interoperability with legacy systems. This flexibility allows large enterprises to innovate and adapt to changing market conditions while controlling their extensive IT ecosystems.

Based on the solutions, the software-defined networking segment holds the highest CAGR during the forecast period.

Software-defined data center networking solutions transform network management within data centers by virtualizing and automating network functions. It abstracts network resources and creates a software-based control layer that manages data flow across the network. This virtualized layer enables dynamic configuration and optimization of network resources based on real-time demands. Software-defined networking solutions use software controllers to automate network tasks, such as routing, switching, and load balancing, ensuring efficient and reliable data flow within the data center. The centralized control and automation capabilities of Software-defined networking enable quick and efficient network adjustments, reducing downtime and enhancing operational efficiency. SDDCN also supports advanced security measures, such as micro-segmentation and automated threat detection, providing robust protection for data center networks. Programmatically managing network resources enables seamless integration with cloud services and other digital infrastructure.

Prominent companies like Cisco and Juniper Networks are pioneers in the software-defined networking market, providing advanced solutions that enhance network management within data centers. The software-defined networking solution is projected to grow as organizations seek to modernize their network infrastructure to support digital transformation initiatives. The increasing adoption of cloud services, IoT, and edge computing drives the need for agile and secure network management solutions.

Software-defined networking offers a cost-effective alternative with greater control than traditional networking; this enables centralized control of the network traffic without configuring the settings of individual switches. Software-defined networking provides dynamic, cost-effective, manageable, and adaptable solutions, making it ideal for dynamic applications utilizing high bandwidth. Software-defined networking aids end users in managing the high degree of change necessary on the network to support virtual workloads, reducing the complexity of the network in data centers, and allowing for automation and orchestration of network configurations. Software-defined networking provides advantages, such as on-demand and simplified implementation of rules, prioritization, and restrictions. Software-defined networking has a variety of applications for CSPs that require complex networking with heavy data traffic management capabilities. Software-defined networking enables network automation, programmability, and architectural flexibility for policy-driven control and self-service innovation by unbundling the traditional device-bound vertically integrated device stack. During the forecasted period, the software-defined networking solution is expected to have the highest market share owing to several factors, such as the proliferation of emerging technologies, such as 5G, IoT, and cloud computing, which need robust and flexible network infrastructures and digital transformation across industries.

Breakdown of primaries

We interviewed Chief Executive Officers (CEOs), directors of innovation and technology, system integrators, and executives from several significant SDDC market companies.

- By Company: Tier I: 30%, Tier II: 45%, and Tier III: 25%

- By Designation: C-Level Executives: 35%, Director Level: 25%, and Others: 40%

- By Region: North America: 45%, Europe: 20%, Asia Pacific: 30%, Rest of World: 5%

Some of the significant SDDC market vendors are VMware (US), Microsoft (US), Cisco (US), HPE (US), IBM (US), Dell Technologies (US), Oracle (US), Nutanix (UK), Huawei (China), and Fujitsu (Japan).

Research coverage:

In the market report, we covered the SDDC market across segments. We estimated the market size and growth potential for many segments based on offerings, solutions, organization size, end users, and region. It contains a thorough competition analysis of the major market participants, information about their businesses, essential observations about their product and service offerings, current trends, and critical market strategies.

Reasons to buy this report:

With information on the most accurate revenue estimates for the whole SDDC industry and its subsegments, the research will benefit market leaders and recent newcomers. Stakeholders will benefit from this report's increased understanding of the competitive environment, which will help them better position their companies and develop go-to-market strategies. The research offers information on the main market drivers, constraints, opportunities, and challenges, as well as aids players in understanding the pulse of the industry.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing demand for data security, Customization and control over IT infrastructure, enhanced performance, and reliability), restraints (complexity of implementation and management), opportunities (integration with emerging technologies like AI, ML, and automation into SDDC), and challenges (inadequate maturity in storage virtualization lead to inefficient data management and slower performance) influencing the growth of the SDDC market.

- Product Development/Innovation: Comprehensive analysis of emerging technologies, R&D initiatives, and new service and product introductions in the SDDC industry.

- Market Development: In-depth details regarding profitable markets: the paper examines the global SDDC industry.

- Market Diversification: Comprehensive details regarding recent advancements, investments, unexplored regions, new goods and services, and the SDDC industry.

- Competitive Assessment: Thorough analysis of the market shares, expansion plans, and service portfolios of the top competitors in the SDDC industry, such as VMware (US), Microsoft (US), Cisco (US), HPE (US), and IBM (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary interviews

- 2.1.2.2 Key insights from industry experts

- 2.2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.3.3 MARKET ESTIMATION APPROACHES

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 MAJOR OPPORTUNITIES FOR KEY PLAYERS IN SOFTWARE-DEFINED DATA CENTER MARKET

- 4.2 SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING

- 4.3 SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION

- 4.4 SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE

- 4.5 SOFTWARE-DEFINED DATA CENTER P MARKET, BY END USER

- 4.6 SOFTWARE-DEFINED DATA CENTER MARKET: REGIONAL SCENARIO

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Reduced dependency on legacy hardware

- 5.2.1.2 Focus on enhancing security measures and meeting regulatory standards

- 5.2.1.3 Rising adoption of multi-cloud solutions

- 5.2.1.4 Growing demand for upgraded and advanced data centers

- 5.2.2 RESTRAINTS

- 5.2.2.1 Complexity in implementation of SDDCs and reconfiguration of traditional infrastructure

- 5.2.2.2 Complexities in integrating hardware and software components from different vendors and lack of standardization

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Focus on integrating SDDC with emerging technologies

- 5.2.3.2 Emphasis on automation and orchestration

- 5.2.3.3 Enhancing resilience and uptime

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of skilled workforce and inadequate management practices

- 5.2.4.2 Rising pressure on achieving storage, networking, and server virtualization maturity

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 INDICATIVE PRICING LEVELS OF SOFTWARE-DEFINED DATA CENTER SOLUTIONS

- 5.4.2 INDICATIVE PRICING ANALYSIS, BY REGION

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 ECOSYSTEM

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Cloud computing

- 5.7.1.2 Edge computing

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 IoT

- 5.7.2.2 Cybersecurity

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 AI/ML

- 5.7.3.2 Big data

- 5.7.1 KEY TECHNOLOGIES

- 5.8 PATENT ANALYSIS

- 5.9 KEY CONFERENCES AND EVENTS, 2024-2025

- 5.10 REGULATORY LANDSCAPE

- 5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.10.2 REGULATIONS, BY REGION

- 5.10.2.1 North America

- 5.10.2.2 Europe

- 5.10.2.3 Asia Pacific

- 5.10.2.4 Middle East & South Africa

- 5.10.2.5 Latin America

- 5.10.3 REGULATORY IMPLICATIONS AND INDUSTRY STANDARDS

- 5.10.3.1 General Data Protection Regulation (GDPR)

- 5.10.3.2 SEC Rule 17a-4

- 5.10.3.3 ISO/IEC 27001

- 5.10.3.4 System and Organization Controls 2 type II compliance

- 5.10.3.5 Financial Industry Regulatory Authority (FINRA)

- 5.10.3.6 Freedom Of Information Act (FOIA)

- 5.10.3.7 Health Insurance Portability and Accountability Act (HIPAA)

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 THREAT OF NEW ENTRANTS

- 5.11.2 THREAT OF SUBSTITUTES

- 5.11.3 BARGAINING POWER OF SUPPLIERS

- 5.11.4 BARGAINING POWER OF BUYERS

- 5.11.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.12 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.13 BUYING CRITERIA

- 5.14 BUSINESS MODEL ANALYSIS

- 5.14.1 SUBSCRIPTION-BASED MODELS

- 5.14.2 PAY-AS-YOU-GO

- 5.14.3 MANAGED SERVICES PROVIDERS

- 5.14.4 LICENSING MODELS

- 5.14.5 CONSULTING & PROFESSIONAL SERVICES

- 5.15 INVESTMENT AND FUNDING SCENARIO

- 5.16 FUTURE OF SOFTWARE-DEFINED DATA CENTER MARKET

- 5.17 IMPACT OF AI/GEN AI ON SOFTWARE-DEFINED DATA CENTER MARKET

- 5.17.1 INDUSTRY TRENDS: USE CASES

- 5.17.1.1 Use Case 1: Blue Diamond Growers implemented HPE Aruba Networking to process almonds, simplify network management, and reduce trouble call resolution times by 50%

- 5.17.2 TOP CLIENTS ADAPTING TO GEN AI

- 5.17.2.1 Microsoft

- 5.17.2.2 VMware

- 5.17.1 INDUSTRY TRENDS: USE CASES

- 5.18 CASE STUDY ANALYSIS

- 5.18.1 CASE STUDY 1: BBVA USED CISCO DNA CENTER AND SD-ACCESS TO VERIFY TRUST AND PREVENT FINANCIAL FRAUD

- 5.18.2 CASE STUDY 2: BLOOMBERG MEDIA SOLVED CLOUD MEDIA WORKFLOWS ACROSS HYBRID AND MULTI-CLOUD ENVIRONMENTS

- 5.18.3 CASE STUDY 3: NANTES CHU LEVERAGED VMWARE FOR ITS TRANSFORMATION AS "DIGITAL HOSPITAL"

- 5.18.4 CASE STUDY 4: DATACORE'S SYNCHRONOUS MIRRORING ENSURED AVAILABILITY OF IT SYSTEMS AND AUGMENTED PERFORMANCE FOR ROCKET TESTING

6 SOFTWARE-DEFINED DATA CENTER MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERINGS: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 6.2 SOLUTIONS

- 6.2.1 NEED FOR FLEXIBLE, SCALABLE, AND EFFICIENT NETWORK MANAGEMENT SOLUTIONS TO PROPEL MARKET

- 6.3 SERVICES

- 6.3.1 SERVICES TO ENABLE SEAMLESS AND EFFICIENT IMPLEMENTATION OF ADVANCED SOLUTIONS TO FUEL MARKET GROWTH

- 6.3.2 TRAINING & CONSULTING

- 6.3.3 INTEGRATION & DEPLOYMENT

- 6.3.4 SUPPORT & MAINTENANCE

7 SOFTWARE-DEFINED DATA CENTER MARKET, BY SOLUTION

- 7.1 INTRODUCTION

- 7.1.1 SOLUTIONS: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 7.2 SOFTWARE-DEFINED COMPUTING

- 7.2.1 EFFICIENT ALLOCATION OF WORKLOADS AMONG SERVERS TO BOOST DEMAND FOR SOFTWARE-DEFINED COMPUTING SOLUTIONS

- 7.2.2 VIRTUALIZATION PLATFORMS

- 7.2.3 HYPERVISORS

- 7.2.4 MANAGEMENT TOOLS

- 7.3 SOFTWARE-DEFINED STORAGE

- 7.3.1 NEED FOR AUTOMATED MANAGEMENT, COST EFFICIENCY, INCREASED FLEXIBILITY, GREATER OPERATIONAL EFFICIENCY, AND REDUCED COSTS TO BOOST DEMAND FOR SOFTWARE-DEFINED STORAGE SOLUTIONS

- 7.3.2 STORAGE VIRTUALIZATION SOFTWARE

- 7.3.3 STORAGE MANAGEMENT SOFTWARE

- 7.3.4 HYPERCONVERGED INFRASTRUCTURE (HCI)

- 7.4 SOFTWARE-DEFINED NETWORKING

- 7.4.1 SHIFT TOWARD MODERN NETWORK INFRASTRUCTURE FOR DIGITAL TRANSFORMATION INITIATIVES TO FOSTER MARKET GROWTH

- 7.4.2 SOFTWARE-DEFINED NETWORKING CONTROLLERS

- 7.4.3 SOFTWARE-DEFINED NETWORKING INFRASTRUCTURE (SWITCHES, ROUTERS)

- 7.4.4 NETWORK VIRTUALIZATION SOFTWARE

- 7.5 MANAGEMENT & OPERATIONS

- 7.5.1 NEED FOR UNIFIED MANAGEMENT PLATFORM FOR STREAMLINING OPERATIONS ACROSS VIRTUALIZED ENVIRONMENTS TO BOLSTER MARKET GROWTH

- 7.5.2 AUTOMATION & ORCHESTRATION

- 7.5.3 MANAGEMENT & MONITORING

8 SOFTWARE-DEFINED DATA CENTER MARKET, BY ORGANIZATION SIZE

- 8.1 INTRODUCTION

- 8.1.1 ORGANIZATION SIZES: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 8.2 SMALL AND MEDIUM-SIZED ENTERPRISES (SMES)

- 8.2.1 HIGH FOCUS ON COST OPTIMIZATION AND SCALABLE SOLUTIONS TO DRIVE DEMAND FOR SOFTWARE-DEFINED SOLUTIONS IN SMALL AND MEDIUM-SIZED ENTERPRISES

- 8.3 LARGE ENTERPRISES

- 8.3.1 GROWING DEMAND FOR SCALABLE SOLUTIONS FOR MANAGING COMPLEX AND EXTENSIVE IT INFRASTRUCTURE TO PROPEL MARKET

9 SOFTWARE-DEFINED DATA CENTER MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.1.1 END USERS: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 9.2 ENTERPRISES

- 9.2.1 NEED FOR REDUCED HARDWARE DEPENDENCY, STREAMLINED OPERATIONS, AND ENHANCED COST CONTROL THROUGH RESOURCE POOLING AND DYNAMIC PROVISIONING TO BOOST MARKET GROWTH

- 9.2.2 ENTERPRISES: APPLICATION AREAS

- 9.2.2.1 Hybrid cloud management

- 9.2.2.2 Business continuity & disaster recovery

- 9.2.2.3 Data center consolidation

- 9.2.2.4 Other enterprise application areas

- 9.3 TELECOM SERVICE PROVIDERS

- 9.3.1 EMPHASIS ON DELIVERING HIGH-PERFORMANCE AND LOW LATENCY APPLICATIONS WITH 5G, EDGE COMPUTING, AND NFV TO ACCELERATE MARKET GROWTH

- 9.3.2 TELECOM SERVICE PROVIDERS: APPLICATION AREAS

- 9.3.2.1 Network Functions Virtualization (NFV)

- 9.3.2.2 5G infrastructure

- 9.3.2.3 Edge computing

- 9.3.2.4 Other telecom service provider application areas

- 9.4 CLOUD SERVICE PROVIDERS

- 9.4.1 HYBRID AND MULTI-CLOUD ENVIRONMENT TO FACILITATE SEAMLESS INTEGRATION AND MANAGEMENT ACROSS DIVERSE CLOUD PLATFORMS

- 9.4.2 CLOUD SERVICE PROVIDERS: APPLICATION AREAS

- 9.4.2.1 Integration as a service

- 9.4.2.2 Platform as a service

- 9.4.2.3 Security & compliance

- 9.4.2.4 Other cloud service provider application areas

- 9.5 MANAGED SERVICE PROVIDERS

- 9.5.1 GROWING FOCUS ON FASTER DEPLOYMENT OF CUSTOMIZED AND ON-DEMAND SERVICES TO DRIVE MARKET

- 9.5.2 MANAGED SERVICE PROVIDERS: APPLICATION AREAS

- 9.5.2.1 Remote management & monitoring

- 9.5.2.2 Backup & disaster recovery

- 9.5.2.3 Security services

- 9.5.2.4 Other managed service provider application areas

10 SOFTWARE-DEFINED DATA CENTER MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 10.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 10.2.3 US

- 10.2.3.1 Extensive investments in cloud infrastructure and advancements in IT automation and security investment to drive market

- 10.2.4 CANADA

- 10.2.4.1 Increased government initiatives for cloud adoption to fuel demand for SDDC solutions

- 10.3 EUROPE

- 10.3.1 EUROPE: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 10.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 10.3.3 UK

- 10.3.3.1 Need for cloud computing due to its scalability and flexibility to boost demand for SDDC solutions

- 10.3.4 GERMANY

- 10.3.4.1 Presence of several SMEs and rapid adoption of cloud computing to propel market

- 10.3.5 FRANCE

- 10.3.5.1 Enhanced data management capabilities, innovation in cloud services, and adoption of integrated, flexible IT solutions to bolster market growth

- 10.3.6 ITALY

- 10.3.6.1 Strategic investments and regulatory developments aimed at enhancing digital infrastructure to fuel market growth

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 10.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 10.4.3 CHINA

- 10.4.3.1 Rapid development of 5G, IoT, AI, and VR technologies spurring adoption of cloud-based services to drive market

- 10.4.4 JAPAN

- 10.4.4.1 Advanced communications technology and increasing need for Data Center Interconnect (DCI) bandwidth to boost market growth

- 10.4.5 AUSTRALIA & NEW ZEALAND

- 10.4.5.1 Growing need for edge computing and cloud-based solutions to foster demand for SDDC solutions

- 10.4.6 REST OF ASIA PACIFIC

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 MIDDLE EAST & AFRICA: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 10.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 10.5.3 GULF COOPERATION COUNCIL COUNTRIES

- 10.5.3.1 Focus on enhancing eGovernment services and rapid adoption of cloud technologies to fuel market growth

- 10.5.3.2 Kingdom of Saudi Arabia (KSA)

- 10.5.3.3 United Arab Emirates (UAE)

- 10.5.3.4 Rest of GCC countries

- 10.5.4 SOUTH AFRICA

- 10.5.4.1 Need to enhance scalability, improve operational efficiency, and enable more agile IT infrastructure management to boost demand for SDDC solutions

- 10.5.5 REST OF MIDDLE EAST & AFRICA

- 10.6 LATIN AMERICA

- 10.6.1 LATIN AMERICA: SOFTWARE-DEFINED DATA CENTER MARKET DRIVERS

- 10.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 10.6.3 BRAZIL

- 10.6.3.1 Expanding IT industry and strong focus on renewable energy to foster demand for SDDC solutions

- 10.6.4 MEXICO

- 10.6.4.1 Growing investment in technological infrastructure and smart city projects to accelerate market growth

- 10.6.5 REST OF LATIN AMERICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.3 REVENUE ANALYSIS

- 11.4 MARKET SHARE ANALYSIS

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- 11.5.5.1 Company footprint

- 11.5.5.2 Offering footprint

- 11.5.5.3 Solution footprint

- 11.5.5.4 End-user footprint

- 11.5.5.5 Regional footprint

- 11.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2023

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2023

- 11.6.5.1 Key start-ups/SMEs

- 11.6.5.2 Competitive benchmarking of key start-ups/SMEs

- 11.7 COMPANY VALUATION AND FINANCIAL METRICS

- 11.8 BRAND/PRODUCT COMPARISON

- 11.8.1 VMWARE: VSPHERE

- 11.8.2 MICROSOFT: AZURE STACK HCI

- 11.8.3 DELL: DELL VXRAIL

- 11.8.4 CISCO: CISCO ACI

- 11.8.5 HPE: HPE SYNERGY

- 11.9 COMPETITIVE SCENARIO AND TRENDS

- 11.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 11.9.2 DEALS

12 COMPANY PROFILES

- 12.1 INTRODUCTION

- 12.2 MAJOR PLAYERS

- 12.2.1 VMWARE

- 12.2.1.1 Business overview

- 12.2.1.2 Products/Solutions/Services offered

- 12.2.1.3 Recent developments

- 12.2.1.3.1 Product launches

- 12.2.1.3.2 Deals

- 12.2.1.4 MnM view

- 12.2.1.4.1 Right to win

- 12.2.1.4.2 Strategic choices

- 12.2.1.4.3 Weaknesses and competitive threats

- 12.2.2 MICROSOFT

- 12.2.2.1 Business overview

- 12.2.2.2 Products/Solutions/Services offered

- 12.2.2.3 Recent developments

- 12.2.2.3.1 Product launches

- 12.2.2.4 MnM view

- 12.2.2.4.1 Right to win

- 12.2.2.4.2 Strategic choices

- 12.2.2.4.3 Weaknesses and competitive threats

- 12.2.3 CISCO

- 12.2.3.1 Business overview

- 12.2.3.2 Products/Solutions/Services offered

- 12.2.3.3 Recent developments

- 12.2.3.3.1 Product launches

- 12.2.3.3.2 Deals

- 12.2.3.4 MnM view

- 12.2.3.4.1 Right to win

- 12.2.3.4.2 Strategic choices

- 12.2.3.4.3 Weaknesses and competitive threats

- 12.2.4 HPE

- 12.2.4.1 Business overview

- 12.2.4.2 Products/Solutions/Services offered

- 12.2.4.3 Recent developments

- 12.2.4.3.1 Product enhancements

- 12.2.4.3.2 Deals

- 12.2.4.4 MnM view

- 12.2.4.4.1 Right to win

- 12.2.4.4.2 Strategic choices

- 12.2.4.4.3 Weaknesses and competitive threats

- 12.2.5 IBM

- 12.2.5.1 Business overview

- 12.2.5.2 Products/Solutions/Services offered

- 12.2.5.3 Recent developments

- 12.2.5.3.1 Product launches

- 12.2.5.3.2 Deals

- 12.2.5.4 MnM view

- 12.2.5.4.1 Right to win

- 12.2.5.4.2 Strategic choices

- 12.2.5.4.3 Weaknesses and competitive threats

- 12.2.6 DELL TECHNOLOGIES

- 12.2.6.1 Business overview

- 12.2.6.2 Products/Solutions/Services offered

- 12.2.6.3 Recent developments

- 12.2.6.3.1 Product launches

- 12.2.7 ORACLE

- 12.2.7.1 Business overview

- 12.2.7.2 Products/Solutions/Services offered

- 12.2.7.3 Recent developments

- 12.2.7.3.1 Deals

- 12.2.8 NUTANIX

- 12.2.8.1 Business overview

- 12.2.8.2 Products/Solutions/Services offered

- 12.2.8.3 Recent developments

- 12.2.8.3.1 Product enhancements

- 12.2.8.3.2 Deals

- 12.2.9 HUAWEI

- 12.2.9.1 Business overview

- 12.2.9.2 Products/Solutions/Services offered

- 12.2.9.3 Recent developments

- 12.2.9.3.1 Product launches

- 12.2.9.3.2 Deals

- 12.2.10 FUJITSU

- 12.2.10.1 Business overview

- 12.2.10.2 Products/Solutions/Services offered

- 12.2.10.3 Recent developments

- 12.2.10.3.1 Product launches

- 12.2.1 VMWARE

- 12.3 OTHER PLAYERS

- 12.3.1 JUNIPER NETWORKS

- 12.3.2 COMMVAULT

- 12.3.3 ARISTA NETWORKS

- 12.3.4 DATACORE SOFTWARE

- 12.3.5 SCALITY

- 12.3.6 SUSE

- 12.3.7 NETAPP

- 12.3.8 CITRIX

- 12.3.9 NUAGE NETWORKS

- 12.3.10 LENOVO

- 12.3.11 RACKSPACE TECHNOLOGY

- 12.4 START-UPS/SMES

- 12.4.1 LIGHTBITS

- 12.4.2 HIVEIO

- 12.4.3 WHIZWORKS

- 12.4.4 PI SYSTEMS AND NETWORKS

13 ADJACENT/RELATED MARKETS

- 13.1 INTRODUCTION

- 13.1.1 RELATED MARKETS

- 13.1.2 LIMITATIONS

- 13.2 HYPER-CONVERGED INFRASTRUCTURE MARKET

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS