|

|

市場調査レポート

商品コード

1681527

ワイヤー・ケーブルの世界市場:製品タイプ別、材料タイプ別、電圧別、敷設別、最終用途産業別、地域別 - 予測(~2029年)Wire & Cable Market by Product Type (Electronic Wire, Power Cable, Control & Instrumentation Cable, Communication Cable, Flexible & Specialty Cable), Material Type, Voltage, Installation, End-Use Industry, and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ワイヤー・ケーブルの世界市場:製品タイプ別、材料タイプ別、電圧別、敷設別、最終用途産業別、地域別 - 予測(~2029年) |

|

出版日: 2025年03月01日

発行: MarketsandMarkets

ページ情報: 英文 259 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界のワイヤー・ケーブルの市場規模は、2024年の2,010億米ドルから2029年までに2,662億米ドルに達すると予測され、2024年~2029年にCAGRで5.8%の成長が見込まれます。

この成長は、送電にケーブルを使用する太陽光発電や風力発電による再生可能エネルギー発電の増加によるものです。また、電気自動車(EV)需要の増加により、このような効率運転ソリューションに向けた先進の配線システムの必要性が拡大しています。技術の進歩、スマートグリッド、IoTの受容は、先進の効果的なケーブルシステムを増加させ、市場を継続的に後押ししています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2022年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 単位 | 10億米ドル |

| セグメント | 製品タイプ、材料、敷設、電圧、最終用途産業、地域 |

| 対象地域 | 北米、アジア太平洋、中東・アフリカ、ラテンアメリカ |

「地下敷設セグメントが世界のワイヤー・ケーブル市場で金額ベースでもっとも急成長するセグメントとなります。」

地下敷設は、従来の敷設システムよりも地下敷設が好まれるようになったことを反映し、予測期間にもっとも高いCAGRを記録する見込みです。この成長は、都市部における信頼性、安全性、美観の向上への要望など、複数の要因によるものです。地下ケーブルは、厳しい気象条件や偶発的な損傷などの環境上の危険からの高い保護を提供し、メンテナンスコストを削減し、システムの寿命を向上させます。

「電子ワイヤーが金額ベースで世界のワイヤー・ケーブル市場を独占すると予測されます。」

電子ワイヤーは製品タイプセグメントを支配し、また予測期間にもっとも急成長するセグメントとなる見込みです。電子ワイヤーは電子機器に欠かせないコンポーネントです。電化の進行と日常生活における電子機器の使用の増加が、電子ワイヤの需要を押し上げています。

「金属製ワイヤー・ケーブルが金額ベースで世界のワイヤー・ケーブル市場を独占すると予測されます。」

ワイヤー・ケーブルは主に金属とポリマーで構成されています。金属には、優れた導電性を持つ銅やアルミニウムが含まれます。これらはワイヤー・ケーブルに不可欠なコンポーネントであるため、予測期間に市場を独占すると予測されます。銅は高い導電性が要求されるワイヤー・ケーブルに使われ、アルミニウムは費用対効果が高く軽量なワイヤー・ケーブルに使われます。今日まで、ワイヤー・ケーブルに使用できる、金属の代替となる原材料は開発されていません。したがって、ワイヤー・ケーブル市場の成長に伴い、金属製のワイヤー・ケーブルの増加が予測されます。

「低電圧セグメントが市場を独占する見込みです。」

適応性の高さから、低電圧ワイヤー・ケーブルがワイヤー・ケーブル市場でもっとも大きな割合を占めています。家庭、商業、工業において、これらのコンポーネントは信号や電力の伝達に役立っています。これは、照明システム、家電、ネットワーク回路時代に広く使用され、安価であるため、社会における官民いずれの領域でも普及しているからです。より精巧な建物や構造物が建築され、建物に省エネ機能が追加されているため、高品質な低電圧ケーブルの供給とサポートが常に必要とされています。

「自動車最終用途産業が予測期間にもっとも急成長するセグメントになると推定されます。」

自動車産業は、車両の製造における技術革新と自動車の電化への関心の高まりにより、ワイヤー・ケーブル市場でもっとも急成長している最終用途産業です。電気自動車やハイブリッド車などの新型車の開発に伴い、高電圧やADAS、インフォテインメントシステムをサポートする効率的な配線要件を満たすソリューションに対する需要が大きく変化しています。ハイエンドの組み込み電子機器、センサー、接続性モジュールを内蔵した近年の自動車もこの需要を支えており、自動車用途に対応した高性能で耐久性のある特定産業向けのケーブルが必要とされています。さらに、自動車の安全性と乗客の快適性を追求する動きは、自動車の効率を高める軽量で柔軟な設計を持つケーブルを採用するようメーカーに圧力をかけています。

当レポートでは、世界のワイヤー・ケーブル市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- ワイヤー・ケーブル市場の企業にとって魅力的な機会

- ワイヤー・ケーブル市場:最終用途産業別、地域別

- ワイヤー・ケーブル市場:製品タイプ別

- ワイヤー・ケーブル市場:材料別

- ワイヤー・ケーブル市場:電圧別

- ワイヤー・ケーブル市場:敷設別

- ワイヤー・ケーブル市場:主要国別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ポーターのファイブフォース分析

- 主なステークホルダーと購入基準

- マクロ経済の見通し

- イントロダクション

- GDPの動向と予測

- 世界の建設産業の動向

- 世界の自動車産業の動向

- 世界の家電産業の動向

- サプライチェーン分析

- 原材料の分析

- 製品タイプの分析

- 電圧の分析

- 敷設の分析

- 最終製品の分析

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 主要企業の平均販売価格の動向:最終用途産業別

- 平均販売価格の動向:地域別

- 貿易分析

- HSコード761410の輸入シナリオ

- HSコード761410の輸出シナリオ

- 技術分析

- 主要技術

- 補完技術

- 特許分析

- イントロダクション

- 調査手法

- 文献の種類

- 考察

- 法的地位

- 管轄分析

- 主な出願者

- 過去5年間の上位10の特許保有者(米国)

- 規制情勢

- 主な会議とイベント(2024年~2025年)

- ケーススタディ分析

- 顧客ビジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ

- AI/生成AIの影響

- 主なユースケースと市場の将来性

- ワイヤー・ケーブル市場におけるAI導入のケーススタディ

第6章 ワイヤー・ケーブル市場:製品タイプ別

- イントロダクション

- 電子ワイヤー

- 電力ケーブル

- 制御・計装ケーブル

- 通信ケーブル

- フレキシブルケーブル・特殊ケーブル

第7章 ワイヤー・ケーブル市場:材料別

- イントロダクション

- 金属

- ポリマー

第8章 配線・ケーブル市場:敷設別

- イントロダクション

- 架空

- 地下

- 水中

第9章 ワイヤー・ケーブル市場:電圧別

- イントロダクション

- 低電圧

- 中電圧

- 高電圧

- 超高電圧

第10章 ワイヤー・ケーブル市場:最終用途産業別

- イントロダクション

- 航空宇宙・防衛

- 建築・建設

- 石油・ガス

- エネルギー・電力

- IT・通信

- 自動車

- 医療機器

- その他の最終用途産業

第11章 ワイヤー・ケーブル市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

第12章 競合情勢

- イントロダクション

- 主要参入企業の戦略

- 収益分析(2019年~2023年)

- 市場シェア分析

- ブランド/製品の比較

- ワイヤー・ケーブルブランド/製品の比較:製品別

- ALPHA WIRE

- DRAKA

- AMER CABLE

- GLEASON REEL CORPORATION

- 企業の評価マトリクス:主要企業(2023年)

- 企業の評価マトリクス:スタートアップ/中小企業(2023年)

- 企業の評価と財務指標

- 競合シナリオと動向

第13章 企業プロファイル

- 主要企業

- BELDEN INC.

- FUJIKURA LTD.

- FURUKAWA ELECTRIC CO., LTD.

- LEONI AG

- EMERSON ELECTRIC CO.

- PRYSMIAN

- HELLENIC CABLES

- KEI INDUSTRIES

- AMPHENOL

- FINOLEX CABLES LTD.

- NKT A/S

- SUMITOMO ELECTRIC INDUSTRIES, LTD.

- HELUKABEL

- LS CABLE & SYSTEM

- NEXANS

- その他の企業

- SAREL

- REMEE WIRE & CABLE

- HUBBELL

- TRATOS GROUP

- DONCASTER CABLES

- TT CABLES

- BRUGG CABLES

- STUDER CABLES AG

- HENAN CENTRAL PLAIN CABLES AND WIRES CO., LTD.

- CORDS CABLE

第14章 付録

List of Tables

- TABLE 1 WIRE & CABLE MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 2 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

- TABLE 3 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

- TABLE 4 GDP PERCENTAGE (%) CHANGE, KEY COUNTRY, 2020-2029

- TABLE 5 TRENDS OF GLOBAL AUTOMOTIVE INDUSTRY

- TABLE 6 WIRE & CABLE MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 7 AVERAGE SELLING PRICE TREND, BY REGION

- TABLE 8 LEADING IMPORTING COUNTRIES FOR HS CODE 761410 IN 2023

- TABLE 9 LEADING EXPORTING COUNTRIES FOR HS CODE 761410 IN 2023

- TABLE 10 WIRE & CABLE MARKET: TOTAL NUMBER OF PATENTS

- TABLE 11 LIST OF PATENTS BY HITACHI METALS LTD.

- TABLE 12 LIST OF PATENTS BY SUMITOMO ELECTRIC INDUSTRY

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 REST OF WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 WIRE & CABLE MARKET: DETAILED LIST OF CONFERENCES & EVENTS, 2024-2025

- TABLE 18 TOP USE CASES AND MARKET POTENTIAL

- TABLE 19 CASE STUDIES OF GEN AI IMPLEMENTATION IN WIRE & CABLE MARKET

- TABLE 20 WIRE & CABLE MARKET, BY PRODUCT TYPE, 2022-2029 (USD BILLION)

- TABLE 21 WIRE & CABLE MARKET, BY MATERIAL TYPE, 2022-2029 (USD BILLION)

- TABLE 22 METAL: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 23 POLYMER: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 24 WIRE & CABLE MARKET, BY INSTALLATION, 2022-2029 (USD BILLION)

- TABLE 25 OVERHEAD: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 26 UNDERGROUND: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 27 SUBMARINE: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 28 WIRE & CABLE MARKET, BY VOLTAGE, 2022-2029 (USD BILLION)

- TABLE 29 LOW VOLTAGE: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 30 MEDIUM VOLTAGE: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 31 HIGH VOLTAGE: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 32 EXTRA-HIGH VOLTAGE: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 33 WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 34 AEROSPACE & DEFENSE: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 35 BUILDING & CONSTRUCTION: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 36 OIL & GAS: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 37 ENERGY & POWER: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 38 IT & TELECOM: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 39 AUTOMOTIVE: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 40 MEDICAL EQUIPMENT: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 41 OTHER END-USE INDUSTRIES: WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 42 WIRE & CABLE MARKET, BY REGION, 2022-2029 (USD BILLION)

- TABLE 43 NORTH AMERICA: WIRE & CABLE MARKET, BY MATERIAL TYPE, 2022-2029 (USD BILLION)

- TABLE 44 NORTH AMERICA: WIRE & CABLE MARKET, BY VOLTAGE, 2022-2029 (USD BILLION)

- TABLE 45 NORTH AMERICA: WIRE & CABLE MARKET, BY INSTALLATION, 2022-2029 (USD BILLION)

- TABLE 46 NORTH AMERICA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 47 NORTH AMERICA: WIRE & CABLE MARKET, BY COUNTRY, 2022-2029 (USD BILLION)

- TABLE 48 US: WIRE & CABLE MARKET, BY END-USE INDUSTRY 2022-2029 (USD BILLION)

- TABLE 49 CANADA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 50 EUROPE: WIRE & CABLE MARKET, BY MATERIAL TYPE, 2022-2029 (USD BILLION)

- TABLE 51 EUROPE: WIRE & CABLE MARKET, BY VOLTAGE, 2022-2029 (USD BILLION)

- TABLE 52 EUROPE: WIRE & CABLE MARKET, BY INSTALLATION, 2022-2029 (USD BILLION)

- TABLE 53 EUROPE: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 54 EUROPE: WIRE & CABLE MARKET, BY COUNTRY, 2022-2029 (USD BILLION)

- TABLE 55 GERMANY: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 56 FRANCE: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 57 UK: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 58 ITALY: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 59 SPAIN: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 60 RUSSIA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 61 REST OF EUROPE: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 62 ASIA PACIFIC: WIRE & CABLE MARKET, BY MATERIAL TYPE, 2022-2029 (USD BILLION)

- TABLE 63 ASIA PACIFIC: WIRE & CABLE MARKET, BY VOLTAGE, 2022-2029 (USD BILLION)

- TABLE 64 ASIA PACIFIC: WIRE & CABLE MARKET, BY INSTALLATION, 2022-2029 (USD BILLION)

- TABLE 65 ASIA PACIFIC: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 66 ASIA PACIFIC: WIRE & CABLE MARKET, BY COUNTRY, 2022-2029 (USD BILLION)

- TABLE 67 CHINA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 68 JAPAN: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 69 INDIA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 70 SOUTH KOREA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 71 AUSTRALIA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 72 REST OF ASIA PACIFIC: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 73 LATIN AMERICA: WIRE & CABLE MARKET, BY MATERIAL TYPE, 2022-2029 (USD BILLION)

- TABLE 74 LATIN AMERICA: WIRE & CABLE MARKET, BY VOLTAGE, 2022-2029 (USD BILLION)

- TABLE 75 LATIN AMERICA: WIRE & CABLE MARKET, BY INSTALLATION, 2022-2029 (USD BILLION)

- TABLE 76 LATIN AMERICA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 77 LATIN AMERICA: WIRE & CABLE MARKET, BY COUNTRY, 2022-2029 (USD BILLION)

- TABLE 78 BRAZIL: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 79 MEXICO: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 80 REST OF LATIN AMERICA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 81 MIDDLE EAST & AFRICA: WIRE & CABLE MARKET, BY MATERIAL TYPE, 2022-2029 (USD BILLION)

- TABLE 82 MIDDLE EAST & AFRICA: WIRE & CABLE MARKET, BY VOLTAGE, 2022-2029 (USD BILLION)

- TABLE 83 MIDDLE EAST & AFRICA: WIRE & CABLE MARKET, BY INSTALLATION, 2022-2029 (USD BILLION)

- TABLE 84 MIDDLE EAST & AFRICA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 85 MIDDLE EAST & AFRICA: WIRE & CABLE MARKET, BY COUNTRY, 2022-2029 (USD BILLION)

- TABLE 86 UAE: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 87 SAUDI ARABIA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 88 REST OF GCC COUNTRIES: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 89 SOUTH AFRICA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 90 REST OF MIDDLE EAST & AFRICA: WIRE & CABLE MARKET, BY END-USE INDUSTRY, 2022-2029 (USD BILLION)

- TABLE 91 STRATEGIES ADOPTED BY WIRE AND CABLE MANUFACTURERS

- TABLE 92 DEGREE OF COMPETITION: WIRE & CABLE MARKET

- TABLE 93 WIRE & CABLE MARKET: PRODUCT TYPE FOOTPRINT

- TABLE 94 WIRE & CABLE MARKET: INSTALLATION FOOTPRINT

- TABLE 95 WIRE & CABLE MARKET: VOLTAGE FOOTPRINT

- TABLE 96 WIRE & CABLE MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 97 WIRE & CABLE MARKET: REGION FOOTPRINT

- TABLE 98 WIRE & CABLE MARKET: KEY STARTUPS/SMES

- TABLE 99 WIRE & CABLE MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 100 WIRE & CABLE MARKET: PRODUCT LAUNCHES, JANUARY 2019-JULY 2024

- TABLE 101 WIRE & CABLE MARKET: DEALS, JANUARY 2019-JULY 2024

- TABLE 102 WIRE & CABLE MARKET: EXPANSIONS, JANUARY 2019-JULY 2024

- TABLE 103 WIRE & CABLE MARKET: OTHER DEVELOPMENTS, JANUARY 2019-JULY 2024

- TABLE 104 BELDEN INC.: COMPANY OVERVIEW

- TABLE 105 BELDEN INC.: PRODUCTS OFFERED

- TABLE 106 BELDEN INC.: PRODUCT LAUNCHES

- TABLE 107 FUJIKURA LTD.: COMPANY OVERVIEW

- TABLE 108 FUJIKURA LTD.: PRODUCTS OFFERED

- TABLE 109 FUJIKURA LTD.: PRODUCT LAUNCHES

- TABLE 110 FUJIKURA LTD.: DEALS

- TABLE 111 FUJIKURA LTD.: EXPANSIONS

- TABLE 112 FURUKAWA ELECTRIC CO., LTD.: COMPANY OVERVIEW

- TABLE 113 FURUKAWA ELECTRIC CO., LTD.: PRODUCTS OFFERED

- TABLE 114 FURUKAWA ELECTRIC CO., LTD.: DEALS

- TABLE 115 FURUKAWA ELECTRIC CO., LTD.: OTHER DEVELOPMENTS

- TABLE 116 LEONI AG: COMPANY OVERVIEW

- TABLE 117 LEONI AG: PRODUCTS OFFERED

- TABLE 118 LEONI AG: PRODUCT LAUNCHES

- TABLE 119 LEONI AG: EXPANSIONS

- TABLE 120 LEONI AG: OTHER DEVELOPMENTS

- TABLE 121 EMERSON ELECTRIC CO.: COMPANY OVERVIEW

- TABLE 122 EMERSON ELECTRIC CO.: PRODUCTS OFFERED

- TABLE 123 PRYSMIAN: COMPANY OVERVIEW

- TABLE 124 PRYSMIAN: PRODUCTS OFFERED

- TABLE 125 PRYSMIAN: PRODUCT LAUNCHES

- TABLE 126 PRYSMIAN: DEALS

- TABLE 127 PRYSMIAN: EXPANSIONS

- TABLE 128 HELLENIC CABLES: COMPANY OVERVIEW

- TABLE 129 HELLENIC CABLES: PRODUCTS OFFERED

- TABLE 130 HELLENIC CABLES: PRODUCT LAUNCHES

- TABLE 131 HELLENIC CABLES: DEALS

- TABLE 132 HELLENIC CABLES: OTHER DEVELOPMENTS

- TABLE 133 KEI INDUSTRIES: COMPANY OVERVIEW

- TABLE 134 KEI INDUSTRIES: PRODUCTS OFFERED

- TABLE 135 KEI INDUSTRIES: DEALS

- TABLE 136 AMPHENOL: COMPANY OVERVIEW

- TABLE 137 AMPHENOL: PRODUCTS OFFERED

- TABLE 138 AMPHENOL: PRODUCT LAUNCHES

- TABLE 139 AMPHENOL: EXPANSIONS

- TABLE 140 AMPHENOL: DEALS

- TABLE 141 FINOLEX CABLES LTD.: COMPANY OVERVIEW

- TABLE 142 FINOLEX CABLES LTD.: PRODUCTS OFFERED

- TABLE 143 FINOLEX CABLES LTD.: DEALS

- TABLE 144 NKT A/S: COMPANY OVERVIEW

- TABLE 145 NKT A/S: PRODUCTS OFFERED

- TABLE 146 NKT A/S: DEALS

- TABLE 147 NKT A/S: OTHER DEVELOPMENTS

- TABLE 148 SUMITOMO ELECTRIC INDUSTRIES, LTD.: COMPANY OVERVIEW

- TABLE 149 SUMITOMO ELECTRIC INDUSTRIES, LTD.: PRODUCTS OFFERED

- TABLE 150 SUMITOMO ELECTRIC INDUSTRIES, LTD.: DEALS

- TABLE 151 SUMITOMO ELECTRIC INDUSTRIES, LTD.: EXPANSION

- TABLE 152 SUMITOMO ELECTRIC INDUSTRIES, LTD.: OTHER DEVELOPMENTS

- TABLE 153 HELUKABEL: COMPANY OVERVIEW

- TABLE 154 HELUKABEL: PRODUCTS OFFERED

- TABLE 155 LS CABLE & SYSTEM: COMPANY OVERVIEW

- TABLE 156 LS CABLE & SYSTEM: PRODUCTS OFFERED

- TABLE 157 LS CABLE & SYSTEM: PRODUCT LAUNCHES

- TABLE 158 LS CABLE & SYSTEM: DEALS

- TABLE 159 LS CABLE & SYSTEM: EXPANSIONS

- TABLE 160 LS CABLE & SYSTEM: OTHER DEVELOPMENTS

- TABLE 161 NEXANS: COMPANY OVERVIEW

- TABLE 162 NEXANS: PRODUCTS OFFERED

- TABLE 163 NEXANS: PRODUCT LAUNCHES

- TABLE 164 NEXANS: DEALS

- TABLE 165 NEXANS: OTHER DEVELOPMENTS

- TABLE 166 SAREL: COMPANY OVERVIEW

- TABLE 167 REMEE WIRE & CABLE: COMPANY OVERVIEW

- TABLE 168 HUBBELL: COMPANY OVERVIEW

- TABLE 169 TRATOS GROUP: COMPANY OVERVIEW

- TABLE 170 DONCASTER CABLES: COMPANY OVERVIEW

- TABLE 171 TT CABLES: COMPANY OVERVIEW

- TABLE 172 BRUGG CABLES: COMPANY OVERVIEW

- TABLE 173 STUDER CABLES AG: COMPANY OVERVIEW

- TABLE 174 HENAN CENTRAL PLAIN CABLES AND WIRES CO., LTD.: COMPANY OVERVIEW

- TABLE 175 CORDS CABLE: COMPANY OVERVIEW

List of Figures

- FIGURE 1 WIRE & CABLE MARKET SEGMENTATION

- FIGURE 2 WIRE & CABLE MARKET: RESEARCH DESIGN

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 5 WIRE & CABLE MARKET: DATA TRIANGULATION

- FIGURE 6 ELECTRONIC WIRES ACCOUNTED FOR HIGHEST MARKET SHARE IN 2023

- FIGURE 7 METAL SEGMENT REGISTERED HIGHEST MARKET SHARE IN 2023

- FIGURE 8 LOW VOLTAGE WIRE & CABLE ACCOUNTED FOR LARGEST SHARE IN 2023

- FIGURE 9 OVERHEAD INSTALLATION LED MARKET IN 2023

- FIGURE 10 ENERGY & POWER SEGMENT DOMINATED MARKET IN 2023

- FIGURE 11 ASIA PACIFIC TO BE FASTEST-GROWING REGION DURING FORECAST PERIOD

- FIGURE 12 RISING INVESTMENTS IN OFFSHORE WIND ENERGY PROJECTS TO BOOST DEMAND FOR WIRES & CABLES

- FIGURE 13 ENERGY & POWER END-USE INDUSTRY & ASIA PACIFIC DOMINATED MARKET IN 2023

- FIGURE 14 ELECTRONIC WIRES TO HOLD LARGEST SHARE IN 2029

- FIGURE 15 METAL SEGMENT EXPECTED TO DOMINATE MARKET IN 2029

- FIGURE 16 LOW VOLTAGE WIRE & CABLE SEGMENT TO DOMINATE MARKET IN 2029

- FIGURE 17 OVERHEAD WIRE & CABLE SEGMENT TO HOLD LARGEST SHARE IN 2029

- FIGURE 18 CHINA TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 19 WIRE & CABLE MARKET: DRIVES, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 20 RENEWABLE ENERGY PRODUCTION CONTRIBUTION IN TOTAL ELECTRICITY PRODUCTION IN US, BY SOURCE TYPE, 2023

- FIGURE 21 TOTAL OFFSHORE WIND INSTALLATIONS, 2023

- FIGURE 22 WIRE & CABLE MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 23 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

- FIGURE 24 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

- FIGURE 25 WIRE & CABLE MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 26 WIRE & CABLE MARKET: VALUE CHAIN ANALYSIS

- FIGURE 27 WIRE & CABLE MARKET: KEY STAKEHOLDERS IN ECOSYSTEM

- FIGURE 28 WIRE & CABLE MARKET: ECOSYSTEM

- FIGURE 29 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY

- FIGURE 30 IMPORT FOR HS CODE 761410, BY KEY COUNTRY, 2019-2023 (USD MILLION)

- FIGURE 31 EXPORT FOR HS CODE 761410, BY KEY COUNTRY, 2019-2023 (USD MILLION)

- FIGURE 32 PATENT ANALYSIS, BY DOCUMENT TYPE

- FIGURE 33 PATENT PUBLICATION TREND, 2018-2023

- FIGURE 34 WIRE & CABLE MARKET: LEGAL STATUS OF PATENTS

- FIGURE 35 CHINESE JURISDICTION REGISTERED HIGHEST NUMBER OF PATENTS BETWEEN 2018 AND 2023

- FIGURE 36 HITACHI METALS LTD. REGISTERED HIGHEST NUMBER OF PATENTS

- FIGURE 37 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS IN WIRE & CABLE MARKET

- FIGURE 38 DEALS AND FUNDING IN WIRE & CABLE MARKET SOARED IN 2024

- FIGURE 39 PROMINENT WIRE & CABLE MANUFACTURING FIRMS IN 2024 (USD BILLION)

- FIGURE 40 ELECTRONIC WIRES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 41 METAL SEGMENT TO LEAD WIRE & CABLE MARKET DURING FORECAST PERIOD

- FIGURE 42 UNDERGROUND INSTALLATION SEGMENT TO LEAD WIRE & CABLE MARKET DURING FORECAST PERIOD

- FIGURE 43 LOW-VOLTAGE SEGMENT TO CONTINUE TO DOMINATE MARKET IN 2029

- FIGURE 44 ENERGY & POWER INDUSTRY TO DOMINATE WIRE & CABLE MARKET DURING FORECAST PERIOD

- FIGURE 45 CHINA TO BE FASTEST-GROWING WIRE & CABLE MARKET DURING FORECAST PERIOD

- FIGURE 46 NORTH AMERICA: WIRE & CABLE MARKET SNAPSHOT

- FIGURE 47 EUROPE: WIRE & CABLE MARKET SNAPSHOT

- FIGURE 48 ASIA PACIFIC: WIRE & CABLE MARKET SNAPSHOT

- FIGURE 49 WIRE & CABLE MARKET: REVENUE ANALYSIS OF TOP 5 MARKET PLAYERS

- FIGURE 50 SHARES OF TOP COMPANIES IN WIRE & CABLE MARKET

- FIGURE 51 WIRE & CABLE MARKET: TOP TRENDING BRAND/PRODUCTS

- FIGURE 52 BRAND/PRODUCT COMPARISON, BY WIRE & CABLE PRODUCTS

- FIGURE 53 WIRE & CABLE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 54 WIRE & CABLE MARKET: COMPANY FOOTPRINT

- FIGURE 55 WIRE & CABLE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- FIGURE 56 WIRE & CABLE MARKET: EV/EBITDA OF KEY MANUFACTURERS

- FIGURE 57 WIRE & CABLE MARKET: YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY MANUFACTURERS

- FIGURE 58 BELDEN INC.: COMPANY SNAPSHOT

- FIGURE 59 FUJIKURA LTD.: COMPANY SNAPSHOT

- FIGURE 60 FURUKAWA ELECTRIC CO., LTD.: COMPANY SNAPSHOT

- FIGURE 61 LEONI AG: COMPANY SNAPSHOT

- FIGURE 62 EMERSON ELECTRIC CO.: COMPANY SNAPSHOT

- FIGURE 63 PRYSMIAN: COMPANY SNAPSHOT

- FIGURE 64 HELLENIC CABLES: COMPANY SNAPSHOT

- FIGURE 65 KEI INDUSTRIES: COMPANY SNAPSHOT

- FIGURE 66 AMPHENOL: COMPANY SNAPSHOT

- FIGURE 67 FINOLEX CABLES LTD.: COMPANY SNAPSHOT

- FIGURE 68 NKT A/S.: COMPANY SNAPSHOT

- FIGURE 69 SUMITOMO ELECTRIC INDUSTRIES, LTD.: COMPANY SNAPSHOT

- FIGURE 70 LS CABLE & SYSTEM: COMPANY SNAPSHOT

- FIGURE 71 NEXANS: COMPANY SNAPSHOT

The global Wire & Cable market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% from 2024 to 2029, with a projected value of USD 266.2 billion by 2029, up from USD 201.0 billion in 2024. This growth is observed due to the addition of renewable power in to the energy generation through harnessing of energy from solar and wind that entails the use of cables in the transmission process. Also, an increase in electric vehicle (EV) demand is extending the need for sophisticated wiring systems for such efficiency driving solutions. The advances in technology, smart grid, and inclusion of IoT (Internet of Things) provides a continuous boost to the market to increase the more advanced and effective cable systems.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | Product Type, Material, Installation, Voltage, End-Use Industry, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and Latin America |

"The underground installation segment to be the fastest growing segment in terms of value in the global wire & cable market."

Underground installation is expected to register the highest CAGR (Compound Annual Growth Rate) during the forecasted period, reflecting the increase in preference for underground installation over traditional installation systems. This growth is observed due to several factors, including the desire for enhanced reliability, safety, and aesthetic appeal in urban areas. Underground cables offer high protection from environmental hazards, such as severe weather conditions and accidental damage which reduce maintenance costs and improve system longevity.

"The electronic wires are expected to dominate the global wire & cable market in terms of value."

The product type segment includes electronic wires, power cables, control & instrumentation cables, communication cables, and flexible & specialty cables. Among these, the electronic wire is expected to dominate this segment and also be the fastest-growing segment in the forecasted period. Electronic wires are an irrepressible component of electronic equipment. The growing electrification and increasing use of electronic devices in daily life are boosting the demand for electronic wires.

"The wire & cables made from metals are expected to dominate the global wire & cable market in terms of value."

The wire and cables are primarily made up of metals and polymers. Metals include copper and aluminium which have excellent electrical conductivity. These are essential components of a wire and cable and thus are expected to dominate the market in the forecasted period. Copper is used in wires and cables where the requirement is for high electricity conductivity and aluminum is used in cost-effective and lightweight wire and cables. Up to date, there is no substitute raw material developed for metals that can be used in wire and cable. Thus, as we see growth in the wire & cable market there is an expected increase in wire & cable made from metals.

"Low voltage segment is expected to dominate the market."

The wire and cable market is divided into four categories: extra-high, high, medium, and low voltage. Due to their adaptability, low voltage wires and cables make up the highest portion of the wire and cable market. In-home, commercial, and industrial settings, these components are helpful for conveying signals and electric power. This is because they are widely used in lighting systems, appliances, and network circuit age and are inexpensive, making them popular in both public and private domains in society. There is always a need for high-quality low voltage cables to be supplied and supported since more sophisticated buildings and structures are being built, and energy-saving features are being added to buildings.

"Automotive end-use industry is estimated to be the fastest-growing segment during forecast period."

The automotive industry is the fastest growing end-use industry in the wire and cable market, backed by technological innovations in vehicle manufacturing and growing concern for automotive electrification. With the development of new models of cars like electric and hybrid ones, there is a massive shift in demand for solutions to meet these efficient wiring requirements to support the high voltage and ADAS as well as infotainment systems. The nowadays' vehicles with high-end built-in electronics, sensors, and connectivity modules also support this demand, as well as requiring industry-specific cables of high performance and durability meeting automotive applications. Further, the drive for safety in vehicles and comfort to passengers is putting pressure on manufactures to adopt cables that include light and flex designs to enhance the efficiency of the vehicles.

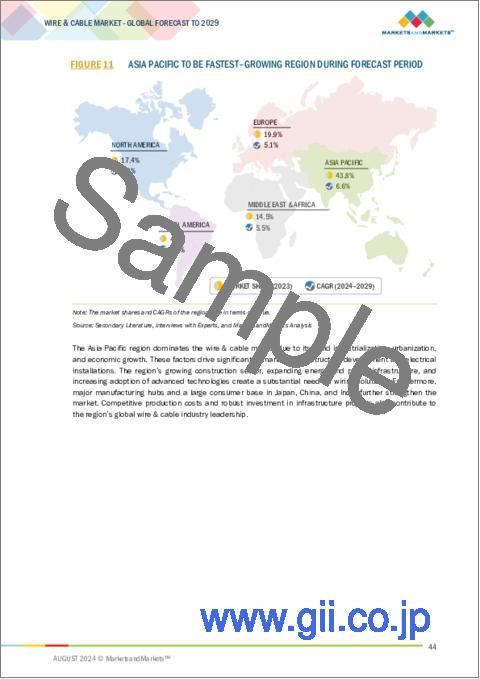

"Asia Pacific is the largest regional level market in the global wire & cable market."

Asia Pacific is to be the largest and fastest growing region for wire & cable attributed to rapid urbanization coupled with extensive infrastructure projects, and robust economic growth. Countries like China and India are developing and expanding the infrastructure for electrical grids, telecommunication and transportation need wire and cables which required these products. An emerging construction industry and growth in the use of IT applications in electrical systems and distribution networks, including smart grids and renewable systems, are other factors to this increase..

This study has been validated through primaries conducted with various industry experts, globally. These primary sources have been divided into the following three categories:

- By Company Type - Tier 1- 40%, Tier 2- 33%, and Tier 3- 27%

- By Designation - C Level- 50%, Director Level- 30%, and Executives- 20%

- By Region - North America- 15%, Europe- 50%, Asia Pacific- 20%, Middle East & Africa (MEA)-5%, Latin America-10%

The report provides a comprehensive analysis of company profiles listed below:

- Prysmian (Italy)

- Belden Inc. (US)

- Fujikura Ltd. (Japan)

- Furukawa Electric Co., Ltd (Japan)

- Leoni Ag (Germany)

- Nexans (France)

- Emerson Electric Co. (US)

- Hellenic Cables (Greece)

- KEI Industries (India)

- Sumitomo Electric Industries, Ltd. (Japan)

- NKT A/S (Denmark)

- Finolex Cables Ltd (India)

- Helukabel (Germany)

- LS Cable and System (South Korea)

Research Coverage

This report covers the global wire & cable market and forecasts the market size until 2029. The report includes the market segmentation - installation (overhead, underground, and submarine), voltage (extra-high voltage, high voltage, medium voltage, and low voltage), material (Metal, Polymer), product type (Electronic wires, power cables, control & instrumentation cables, communication cables, flexible & specialty cables), End-use industry(Aerospace & defense, building & construction, oil & gas, energy & power, it & telecom, automotive, medical equipment and other end-use industries), and Region (Europe, North America, APAC, Latin America, and MEA). Porter's Five Forces analysis, along with the drivers, restraints, opportunities, and challenges, are discussed in the report. It also provides company profiles and competitive strategies adopted by the major players in the global wire & cable market.

Key benefits of buying the report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall wire & cable market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing demand for cables from renewable energy sector to drive the demand), Restraints (Fluctuating raw material prices), Opportunities (Growing demand for cables for in EV infrastructure), Challenges (Challenges in enhancing insulation durability)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the transportation composite market

- Market Development: Comprehensive information about lucrative markets - the report analyses the wire & cable market across various regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the transportation composite market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Prysmian (Italy), Belden Inc. (US), Fujikura Ltd. (Japan), Furukawa Electric Co., Ltd (Japan), Leoni Ag (Germany), Nexans (France), Emerson Electric Co. (US), Hellenic Cables (Greece), KEI Industries (India), Sumitomo Electric Industries, Ltd. (Japan), NKT A/S (Denmark), Finolex Cables Ltd (India), Helukabel (Germany), and LS Cable and System (South Korea) among others in the Wire & Cable market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS & EXCLUSIONS

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key primary participants

- 2.1.2.3 Breakdown of interviews with experts

- 2.1.2.4 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 BASE NUMBER CALCULATION

- 2.2.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 2.2.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 2.3 FORECAST NUMBER CALCULATION

- 2.3.1 SUPPLY SIDE

- 2.3.2 DEMAND SIDE

- 2.4 MARKET SIZE ESTIMATION

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- 2.6 FACTOR ANALYSIS

- 2.7 RESEARCH ASSUMPTIONS

- 2.8 GROWTH FORECAST

- 2.9 RESEARCH LIMITATIONS

- 2.10 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WIRE & CABLE MARKET

- 4.2 WIRE & CABLE MARKET, BY END-USE INDUSTRY AND REGION

- 4.3 WIRE & CABLE MARKET, BY PRODUCT TYPE

- 4.4 WIRE & CABLE MARKET, BY MATERIAL TYPE

- 4.5 WIRE & CABLE MARKET, BY VOLTAGE

- 4.6 WIRE & CABLE MARKET, BY INSTALLATION

- 4.7 WIRE & CABLE MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising demand for cables from renewable energy sector

- 5.2.1.2 Increased focus on safety and compliance

- 5.2.1.3 Surging government investments in grid technology and infrastructure projects

- 5.2.2 RESTRAINTS

- 5.2.2.1 Fluctuating raw material prices

- 5.2.2.2 Global trade war escalation

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing demand for cables in EV infrastructure

- 5.2.3.2 Expansion of offshore wind energy projects

- 5.2.3.3 Rising need to modernize electrical grids

- 5.2.4 CHALLENGES

- 5.2.4.1 Enhancing insulation durability under harsh conditions

- 5.2.4.2 Requirement for technical expertise to develop and install advanced cables

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.4.2 BUYING CRITERIA

- 5.5 MACROECONOMIC OUTLOOK

- 5.5.1 INTRODUCTION

- 5.5.2 GDP TRENDS AND FORECAST

- 5.5.3 TRENDS IN GLOBAL CONSTRUCTION INDUSTRY

- 5.5.4 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.5.5 TRENDS IN GLOBAL APPLIANCES INDUSTRY

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.6.1 RAW MATERIAL ANALYSIS

- 5.6.2 PRODUCT TYPE ANALYSIS

- 5.6.2.1 Electronic wires/coaxial cables

- 5.6.2.2 Power cables

- 5.6.2.3 Control & instrumentation cables

- 5.6.2.4 Communication cables

- 5.6.2.5 Flexible & specialty cables

- 5.6.3 VOLTAGE ANALYSIS

- 5.6.4 INSTALLATION ANALYSIS

- 5.6.5 FINAL PRODUCT ANALYSIS

- 5.7 VALUE CHAIN ANALYSIS

- 5.8 ECOSYSTEM ANALYSIS

- 5.9 PRICING ANALYSIS

- 5.9.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY

- 5.9.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.10 TRADE ANALYSIS

- 5.10.1 IMPORT SCENARIO FOR HS CODE 761410

- 5.10.2 EXPORT SCENARIO FOR HS CODE 761410

- 5.11 TECHNOLOGY ANALYSIS

- 5.11.1 KEY TECHNOLOGIES

- 5.11.1.1 Wire drawing

- 5.11.1.2 Annealing

- 5.11.1.3 Twisting and stranding

- 5.11.1.4 Extrusion

- 5.11.1.5 Cabling

- 5.11.2 COMPLEMENTARY TECHNOLOGIES

- 5.11.2.1 3D printed wires

- 5.11.2.2 Smart wires & cables

- 5.11.2.3 Nanotechnology

- 5.11.1 KEY TECHNOLOGIES

- 5.12 PATENT ANALYSIS

- 5.12.1 INTRODUCTION

- 5.12.2 METHODOLOGY

- 5.12.3 DOCUMENT TYPES

- 5.12.4 INSIGHTS

- 5.12.5 LEGAL STATUS

- 5.12.6 JURISDICTION ANALYSIS

- 5.12.7 TOP APPLICANTS

- 5.12.8 TOP 10 PATENT OWNERS (US) IN LAST 5 YEARS

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14 KEY CONFERENCES & EVENTS, 2024-2025

- 5.15 CASE STUDY ANALYSIS

- 5.15.1 CASE STUDY 1: SOUTHWIRE TO DESIGN AND INSTALL ONSHORE HIGH-VOLTAGE CABLES

- 5.15.2 CASE STUDY 2: NEXANS AND EQUINOR PARTNERSHIP

- 5.15.3 CASE STUDY 3: SUMITOMO ELECTRIC ACQUIRES MAJORITY STAKE IN SUDKABEL

- 5.16 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.17 INVESTMENT AND FUNDING SCENARIO

- 5.18 IMPACT OF AI/GEN AI

- 5.18.1 TOP USE CASES AND MARKET POTENTIAL

- 5.18.2 CASE STUDIES OF AI IMPLEMENTATION IN WIRE & CABLE MARKET

6 WIRE & CABLE MARKET, BY PRODUCT TYPE

- 6.1 INTRODUCTION

- 6.2 ELECTRONIC WIRES

- 6.3 POWER CABLES

- 6.4 CONTROL & INSTRUMENTATION CABLES

- 6.5 COMMUNICATION CABLES

- 6.6 FLEXIBLE & SPECIALTY CABLES

7 WIRE & CABLE MARKET, BY MATERIAL TYPE

- 7.1 INTRODUCTION

- 7.2 METAL

- 7.2.1 SUPERIOR ELECTRICAL CONDUCTIVITY AND DURABILITY TO DRIVE MARKET

- 7.3 POLYMER

- 7.3.1 CAPACITY TO PROVIDE LONG-LASTING PROTECTION AND ADAPT TO VARIOUS ENVIRONMENTAL SITUATIONS TO DRIVE MARKET

8 WIRE & CABLE MARKET, BY INSTALLATION

- 8.1 INTRODUCTION

- 8.2 OVERHEAD

- 8.2.1 GOVERNMENT INVESTMENTS IN INFRASTRUCTURE DEVELOPMENT TO DRIVE MARKET

- 8.3 UNDERGROUND

- 8.3.1 RAPID URBANIZATION TO BOOST MARKET GROWTH

- 8.4 SUBMARINE

- 8.4.1 INCREASING GLOBAL CONNECTIVITY TO PROPEL MARKET

9 WIRE & CABLE MARKET, BY VOLTAGE

- 9.1 INTRODUCTION

- 9.2 LOW VOLTAGE

- 9.2.1 RISE OF SMART HOME TECHNOLOGIES TO DRIVE MARKET

- 9.3 MEDIUM VOLTAGE

- 9.3.1 ADVANCEMENTS IN ELECTRICAL GRID TECHNOLOGY TO PROPEL MARKET

- 9.4 HIGH VOLTAGE

- 9.4.1 RISING DEMAND FOR ROBUST AND RELIABLE POWER TRANSMISSION SYSTEMS TO PROPEL MARKET

- 9.5 EXTRA-HIGH VOLTAGE

- 9.5.1 RISING NUMBER OF SUBMARINE PROJECTS TO DRIVE DEMAND

10 WIRE & CABLE MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 AEROSPACE & DEFENSE

- 10.2.1 SURGE IN GOVERNMENT SPENDING IN DEFENSE SECTOR TO DRIVE MARKET

- 10.3 BUILDING & CONSTRUCTION

- 10.3.1 GROWING INVESTMENTS IN INFRASTRUCTURE DEVELOPMENT IN DEVELOPING COUNTRIES TO PROPEL MARKET

- 10.4 OIL & GAS

- 10.4.1 RISING INVESTMENTS IN OIL & GAS INDUSTRY TO DRIVE MARKET

- 10.5 ENERGY & POWER

- 10.5.1 GROWING RENEWABLE ENERGY PROJECTS TO BOOST MARKET

- 10.6 IT & TELECOM

- 10.6.1 ADVANCEMENTS IN DATA CENTERS TO DRIVE MARKET

- 10.7 AUTOMOTIVE

- 10.7.1 RISING DEMAND FOR EV VEHICLES TO DRIVE MARKET

- 10.8 MEDICAL EQUIPMENT

- 10.8.1 GROWTH IN REMOTE AND WEARABLE HEALTH TECHNOLOGIES TO DRIVE MARKET

- 10.9 OTHER END-USE INDUSTRIES

11 WIRE & CABLE MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Booming aerospace & defense industry to drive demand for wires & cables

- 11.2.2 CANADA

- 11.2.2.1 Advancements in IT & telecom industry to drive market

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Rapid electrification of transportation to boost demand for wires & cables

- 11.3.2 FRANCE

- 11.3.2.1 Rising demand for grid installation to drive market

- 11.3.3 UK

- 11.3.3.1 Rising focus on offshore wind generation to boost market

- 11.3.4 ITALY

- 11.3.4.1 Surge in Italian data centers to drive market

- 11.3.5 SPAIN

- 11.3.5.1 Advancements in IT & Telecom industry to drive market

- 11.3.6 RUSSIA

- 11.3.6.1 Rising investments in defense to boost demand for wire & cable products

- 11.3.7 REST OF EUROPE

- 11.3.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 CHINA

- 11.4.1.1 Rising demand for EVs in China to drive market

- 11.4.2 JAPAN

- 11.4.2.1 Pressing need for clean energy to drive market

- 11.4.3 INDIA

- 11.4.3.1 Growth of automotive industry to drive market

- 11.4.4 SOUTH KOREA

- 11.4.4.1 Government incentives to promote EV demand to drive market

- 11.4.5 AUSTRALIA

- 11.4.5.1 Growing renewable energy demand to drive market

- 11.4.6 REST OF ASIA PACIFIC

- 11.4.1 CHINA

- 11.5 LATIN AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Increasing investments in infrastructure projects to drive demand

- 11.5.2 MEXICO

- 11.5.2.1 Growing focus on energy and power sector to drive market

- 11.5.3 REST OF LATIN AMERICA

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

- 11.6.1.1 UAE

- 11.6.1.1.1 Government investments in infrastructure projects to drive market

- 11.6.1.2 Saudi Arabia

- 11.6.1.2.1 Rising focus on oil field industry to drive market

- 11.6.1.3 Rest of GCC countries

- 11.6.1.1 UAE

- 11.6.2 SOUTH AFRICA

- 11.6.2.1 Government initiatives in the energy & power sector to boost demand

- 11.6.3 REST OF MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES

- 12.3 REVENUE ANALYSIS, 2019-2023

- 12.4 MARKET SHARE ANALYSIS

- 12.5 BRAND/PRODUCT COMPARISON

- 12.5.1 BRAND/PRODUCT COMPARISON, BY WIRE & CABLE PRODUCTS

- 12.5.2 ALPHA WIRE

- 12.5.3 DRAKA

- 12.5.4 AMER CABLE

- 12.5.5 GLEASON REEL CORPORATION

- 12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- 12.6.5 COMPANY FOOTPRINT

- 12.6.5.1 Company footprint

- 12.6.5.2 Product type footprint

- 12.6.5.3 Installation footprint

- 12.6.5.4 Voltage footprint

- 12.6.5.5 End-use industry footprint

- 12.6.5.6 Region footprint

- 12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 RESPONSIVE COMPANIES

- 12.7.3 DYNAMIC COMPANIES

- 12.7.4 STARTING BLOCKS

- 12.7.5 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2023

- 12.7.5.1 Detailed list of key startups/SMEs

- 12.7.5.2 Competitive benchmarking of key startups/SMES

- 12.8 COMPANY VALUATION AND FINANCIAL METRICS

- 12.9 COMPETITIVE SCENARIO AND TRENDS

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

- 12.9.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY COMPANIES

- 13.1.1 BELDEN INC.

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 FUJIKURA LTD.

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 FURUKAWA ELECTRIC CO., LTD.

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Deals

- 13.1.3.3.2 Other developments

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 LEONI AG

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Expansions

- 13.1.4.3.3 Other developments

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 EMERSON ELECTRIC CO.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Right to win

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses and competitive threats

- 13.1.6 PRYSMIAN

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Deals

- 13.1.6.3.2 Expansions

- 13.1.6.4 MnM view

- 13.1.6.4.1 Right to win

- 13.1.6.4.2 Strategic choices

- 13.1.6.4.3 Weaknesses and competitive threats

- 13.1.7 HELLENIC CABLES

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Deals

- 13.1.7.3.3 Other developments

- 13.1.7.4 MnM view

- 13.1.7.4.1 Right to win

- 13.1.7.4.2 Strategic choices

- 13.1.7.4.3 Weaknesses and competitive threats

- 13.1.8 KEI INDUSTRIES

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Deals

- 13.1.8.4 MnM view

- 13.1.8.4.1 Right to win

- 13.1.8.4.2 Strategic choices

- 13.1.8.4.3 Weaknesses and competitive threats

- 13.1.9 AMPHENOL

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches

- 13.1.9.3.2 Expansions

- 13.1.9.3.3 Deals

- 13.1.9.4 MnM view

- 13.1.9.4.1 Right to win

- 13.1.9.4.2 Strategic choices

- 13.1.9.4.3 Weaknesses and competitive threats

- 13.1.10 FINOLEX CABLES LTD.

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Deals

- 13.1.10.4 MnM view

- 13.1.10.4.1 Right to win

- 13.1.10.4.2 Strategic choices

- 13.1.10.4.3 Weaknesses and competitive threats

- 13.1.11 NKT A/S

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Deals

- 13.1.11.3.2 Other developments

- 13.1.11.4 MnM view

- 13.1.11.4.1 Right to win

- 13.1.11.4.2 Strategic choices

- 13.1.11.4.3 Weaknesses and competitive threats

- 13.1.12 SUMITOMO ELECTRIC INDUSTRIES, LTD.

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Deals

- 13.1.12.3.2 Expansions

- 13.1.12.3.3 Other developments

- 13.1.12.4 MnM view

- 13.1.12.4.1 Right to win

- 13.1.12.4.2 Strategic choices

- 13.1.12.4.3 Weaknesses and competitive threats

- 13.1.13 HELUKABEL

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.13.3 MnM view

- 13.1.13.3.1 Right to win

- 13.1.13.3.2 Strategic choices

- 13.1.13.3.3 Weaknesses and competitive threats

- 13.1.14 LS CABLE & SYSTEM

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Product launches

- 13.1.14.3.2 Deals

- 13.1.14.3.3 Expansions

- 13.1.14.3.4 Other developments

- 13.1.14.4 MnM view

- 13.1.14.4.1 Right to win

- 13.1.14.4.2 Strategic choices

- 13.1.14.4.3 Weaknesses and competitive threats

- 13.1.15 NEXANS

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.15.3 Recent developments

- 13.1.15.3.1 Product launches

- 13.1.15.3.2 Deals

- 13.1.15.3.3 Other developments

- 13.1.15.4 MnM view

- 13.1.15.4.1 Right to win

- 13.1.15.4.2 Strategic choices

- 13.1.15.4.3 Weaknesses and competitive threats

- 13.1.1 BELDEN INC.

- 13.2 OTHER PLAYERS

- 13.2.1 SAREL

- 13.2.2 REMEE WIRE & CABLE

- 13.2.3 HUBBELL

- 13.2.4 TRATOS GROUP

- 13.2.5 DONCASTER CABLES

- 13.2.6 TT CABLES

- 13.2.7 BRUGG CABLES

- 13.2.8 STUDER CABLES AG

- 13.2.9 HENAN CENTRAL PLAIN CABLES AND WIRES CO., LTD.

- 13.2.10 CORDS CABLE

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS