|

|

市場調査レポート

商品コード

1497430

プラスチックコンパウンドの世界市場:製品別、由来別、最終用途産業別、地域別 - 2029年までの予測Plastic Compounds Market by Product (PVC, PP, PE, PS, PA, PC, PET, PU, ABS), Source, End-use Industry (Automotive, Packaging, Electrical & Electronics, Building & Construction, Consumer Goods, Medical), and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| プラスチックコンパウンドの世界市場:製品別、由来別、最終用途産業別、地域別 - 2029年までの予測 |

|

出版日: 2024年06月17日

発行: MarketsandMarkets

ページ情報: 英文 266 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

プラスチックコンパウンドの市場規模は、2024年の708億米ドルから2029年には973億米ドルに成長し、予測期間中のCAGRは6.6%になると予測されています。

プラスチックコンパウンドの適応性と多様な特性は、パッケージング、建築・建設業界の進化するニーズを満たすために不可欠なものとなり、世界のプラスチックコンパウンド市場の成長を牽引しています。また、リサイクル可能なプラスチックコンパウンドの採用が増加していることも市場を牽引しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 対象ユニット | 金額(100万米ドル)、数量(キロトン) |

| セグメント | 製品別、由来別、最終用途産業別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

PCコンパウンドは世界のプラスチックコンパウンド市場の重要なセグメントであり、その卓越した強度、透明性、耐衝撃性で有名です。これらのコンパウンドは、自動車、エレクトロニクス、建築、医療機器などの産業で広く利用されています。PCコンパウンドの需要を牽引しているのは、過酷な条件や機械的ストレスに耐える高性能材料へのニーズの高まりです。コンパウンド技術の進歩により、耐紫外線性、耐薬品性、熱安定性が向上した特殊なPCブレンドが開発され、応用範囲が広がっています。持続可能性への関心の高まりは、リサイクル可能で環境に優しいPCコンパウンドの生産も促進しています。

再生プラスチックコンパウンドは、消費者または産業廃棄物由来のプラスチックであり、環境問題、技術の進歩、市場の需要に後押しされ、いくつかの重要な動向を経験しています。消費者や企業がプラスチック汚染が環境に与える影響をより強く認識するようになるにつれ、リサイクル材料から作られた製品やパッケージングに対する需要が高まっています。この動向は、メーカー各社が自社製品にリサイクル材をより高い割合で組み込もうとする原動力となり、再生プラスチックコンパウンドの需要増につながっています。

プラスチックコンパウンドは、様々な建築・建設用途で広く使用されています。新築住宅から商業ビルの改修・改装、病院から学校まで、プラスチックはコスト効率を最大化し、耐久性を高めるのに役立っています。プラスチックコンパウンドは、耐久性、汎用性、費用対効果に貢献し、様々な用途のための住宅で広く使用されています。PVCは、一般的なプラスチックコンパウンドで、床材、壁材、その他の用途に使用されています。金属、木材、石積みのような伝統的な建築材料に代わる、費用対効果の高い選択肢を提供しています。プラスチックコンパウンドは、耐久性、耐候性、長寿命を提供し、メンテナンスコストを削減します。また、設計の自由度が高く、電気配線、床材、壁材、防水材、ファスナー、パイプ、バルブ、継手、ヒンジ、装飾など、さまざまな部材を作ることができます。プラスチックは、特定の要求を満たすために、さまざまな形や大きさに成形することができます。

当レポートでは、世界のプラスチックコンパウンド市場について調査し、製品別、由来別、最終用途産業別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- ポーターのファイブフォース分析

- マクロ経済指標

- 主な利害関係者と購入基準

- バリューチェーン分析

- エコシステム分析

- ケーススタディ分析

- 規制状況

- 技術分析

- 顧客ビジネスに影響を与える動向/混乱

- 貿易分析

- 2024年~2025年の主な会議とイベント

- 価格動向分析

- 投資と資金調達のシナリオ

- 特許分析

第6章 プラスチックコンパウンド市場(製品別)

- イントロダクション

- ポリ塩化ビニル(PVC)

- ポリエチレン(PE)

- ポリスチレン(PS)

- ポリアミド(PA)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- ポリカーボネート(PC)

- ポリウレタン(PU)

- アクリロニトリルブタジエンスチレン(ABS)

- その他

第7章 プラスチックコンパウンド市場(由来別)

- イントロダクション

- 化石燃料ベース

- バイオベース

- リサイクル

第8章 プラスチックコンパウンド市場(最終用途産業別)

- イントロダクション

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 消費財

- 医療

- その他

第9章 プラスチックコンパウンド市場(地域別)

- イントロダクション

- 北米

- アジア太平洋

- 欧州

- 中東・アフリカ

- 南米

第10章 競合情勢

- イントロダクション

- 主要参入企業の戦略/強み

- 市場シェア分析

- 収益分析

- 市場ランキング分析

- 企業価値評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオと動向

第11章 企業プロファイル

- 主要参入企業

- BASF SE

- THE DOW CHEMICAL COMPANY

- LYONDELLBASELL INDUSTRIES HOLDINGS

- SABIC

- ASAHI KASEI CORPORATION

- COVESTRO AG

- CELANESE CORPORATION

- ARKEMA

- RTP COMPANY

- WESTLAKE CORPORATION

- その他の企業

- AVIENT CORPORATION

- GEON PERFORMANCE SOLUTIONS

- RAVAGO

- AURORA MATERIAL SOLUTIONS

- ORBIA

- AMERICHEM

- POLYKEMI

- RIKEN AMERICAS CORPORATION

- TEKNI-PLEX, INC.

- SHINTECH INC.

- MANNER POLYMERS

- EIQSA

- POLYMER ASIA

- DENKA CHEMICALS HOLDINGS

- RADICI PARTECIPAZIONI SPA

第12章 付録

The plastic compounds market size is projected to grow from USD 70.8 billion in 2024 to USD 97.3 billion by 2029, registering a CAGR of 6.6% during the forecast period. The adaptability and diverse properties of plastic compounds have made them indispensable in meeting the evolving needs of the packaging, and building, & construction industries, driving the growth of the global plastic compounds market. In addition, rising adoption of recyclable plastic compounds also drives the market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Million), and Volume (Kiloton) |

| Segments | Product, Source, End-use Industry, and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

"Polycarbonate (PC) is projected to be the second fastest growing segment by product in terms of value."

PC compounds are a vital segment of the global plastic compounds market, renowned for their exceptional strength, transparency, and impact resistance. These compounds are widely utilized in industries such as automotive, electronics, construction, and medical devices. The demand for PC compounds is driven by the increasing need for high-performance materials that can withstand harsh conditions and mechanical stress. Advancements in compounding technology are leading to the development of specialized PC blends that offer improved UV resistance, chemical resistance, and thermal stability, broadening their application scope. The growing focus on sustainability is also fostering the production of recyclable and eco-friendly PC compounds.

"Recycled segment to be the second fastest growing segment by source in terms of value."

Recycled plastic compounds, derived from post-consumer or post-industrial plastic waste, are experiencing several key trends driven by environmental concerns, technological advancements, and market demand. As consumers and businesses become more aware of the environmental impact of plastic pollution, there's a growing demand for products and packaging made from recycled materials. This trend is driving manufacturers to incorporate higher percentages of recycled content into their products, leading to increased demand for recycled plastic compounds.

"Building & construction accounted for the second largest share in the end-use industry segment of plastic compounds market in terms of value."

Plastic compounds are widely used in various building & construction applications. From the construction of new houses to retrofit and renovation of commercial buildings, and from hospitals to schools, plastics help to maximize cost efficiency, and provide enhanced durability. Plastic compounds are extensively used in residential buildings for various applications, contributing to their durability, versatility, and cost-effectiveness. PVC is a common plastic compound used for flooring, wall materials, and other applications in residential buildings. They offer a cost-effective alternative to traditional building materials like metal, wood, and masonry. Plastic compounds offer durability weather resistance, and longevity, thus reducing maintenance costs. They provide enhanced design flexibility, allowing for the creation of various components like electric wiring, flooring, wall covering, waterproofing, fasteners, pipes, valves, fittings, hinges, and decorative touches. Plastics can be molded into different shapes and sizes to meet specific requirements.

"Europe is the third-largest market for plastic compounds."

Europe holds the third-largest market share globally in the plastic compounds market due to several key factors. Firstly, the region benefits from a well-established infrastructure, advanced research and development capabilities, and stringent regulatory standards, fostering innovation and quality in plastic compounds products. The increasing demand for plastic compounds from the transportation and medical industries is the major driver of the market in the region. The stringent environmental regulations implemented in the European region require vehicles to lower emissions. Plastic compounds provide a lightweight alternative for various conventional materials used in the construction of automotive components. This has led to the increased usage of plastic compounds in the automotive industry to manufacture various interior, exterior, and under-the-hood components in the region.

In-depth interviews were conducted with Chief Executive Officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the plastic compounds market, and information was gathered from secondary research to determine and verify the market size of several segments.

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: C Level Executives- 20%, Directors - 10%, and Others - 70%

- By Region: North America - 20%, Europe - 20%, APAC - 40%, South America- 10% , and

the Middle East & Africa -10%

The plastic compounds market comprises major players such as BASF SE (Germany), The Dow Chemical Company (US), LyondellBasell Industries Holdings B.V. (Netherlands), SABIC (Saudi Arabia), Asahi Kasei Corporation (Japan), Covestro AG (Germany), Arkema (France), RTP Company (US), and Westlake Corporation (US). The study includes in-depth competitive analysis of these key players in the plastic compounds market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the market for plastic compounds market on the basis of product, source, end-use industry, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and mergers & acquisition associated with the market for plastic compounds market.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view on the competitive landscape; emerging and high-growth segments of the plastic compounds market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Market Penetration: Comprehensive information on the plastic compounds market offered by top players in the global plastic compounds market.

- Analysis of drivers: (increasing demand in packaging and building & construction industries, rising adoption of recyclable plastic compounds), restraints (volatility in raw material prices, availability of substitutes), opportunities (growth in automotive & transportation industry, advancements in additive manufacturing), and challenges (plastic waste management crisis) influencing the growth of plastic compounds market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the plastic compounds market.

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for plastic compounds market across regions.

- Market Capacity: Production capacities of companies producing plastic compounds are provided wherever available with upcoming capacities for the plastic compounds market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the plastic compounds market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- TABLE 1 PLASTIC COMPOUNDS MARKET: INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- FIGURE 1 PLASTIC COMPOUNDS MARKET SEGMENTATION

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 IMPACT OF RECESSION

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 PLASTIC COMPOUNDS MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary data sources: demand and supply sides

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of interviews with experts

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 3 MARKET SIZE ESTIMATION APPROACH: DEMAND SIDE

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- FIGURE 6 PLASTIC COMPOUNDS MARKET: DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 GROWTH RATE ASSUMPTIONS/GROWTH FORECAST

- 2.5.1 SUPPLY SIDE

- 2.5.2 DEMAND SIDE

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 7 PP SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 8 FOSSIL-BASED SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 9 AUTOMOTIVE SEGMENT TO RECORD FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 10 ASIA PACIFIC MARKET TO REGISTER FASTEST GROWTH DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PLASTIC COMPOUNDS MARKET

- FIGURE 11 RAPID INDUSTRIALIZATION IN EMERGING ECONOMIES TO DRIVE MARKET DURING FORECAST PERIOD

- 4.2 PLASTIC COMPOUNDS MARKET, BY PRODUCT

- FIGURE 12 PP SEGMENT TO LEAD PLASTIC COMPOUNDS MARKET DURING FORECAST PERIOD

- 4.3 PLASTIC COMPOUNDS MARKET, BY SOURCE

- FIGURE 13 BIO-BASED SEGMENT TO WITNESS HIGHEST GROWTH DURING FORECAST PERIOD

- 4.4 PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY

- FIGURE 14 PACKAGING SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.5 PLASTIC COMPOUNDS MARKET, BY COUNTRY

- FIGURE 15 CHINA AND INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 16 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN PLASTIC COMPOUNDS MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing demand in packaging and building & construction industries

- 5.2.1.2 Rising adoption of recyclable plastic compounds

- 5.2.2 RESTRAINTS

- 5.2.2.1 Volatility in raw material prices

- 5.2.2.2 Availability of substitutes

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growth in automotive & transportation industry

- FIGURE 17 YOY PERCENTAGE INCREASE IN AUTOMOTIVE & TRANSPORT INDUSTRY, 2022-2023

- 5.2.3.2 Advancements in additive manufacturing

- 5.2.4 CHALLENGES

- 5.2.4.1 Plastic waste management crisis

- FIGURE 18 GLOBAL PLASTIC MATERIAL PRODUCTION SHARE IN 2022, BY REGION

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 19 PORTER'S FIVE FORCES ANALYSIS OF PLASTIC COMPOUNDS MARKET

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- TABLE 2 PLASTIC COMPOUNDS MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.4 MACROECONOMIC INDICATORS

- 5.4.1 GLOBAL GDP TRENDS

- TABLE 3 PROJECTED REAL GDP GROWTH (ANNUAL PERCENTAGE CHANGE) OF KEY COUNTRIES, 2021-2029

- 5.4.2 AUTOMOBILE PRODUCTION TRENDS

- TABLE 4 AUTOMOBILE PRODUCTION IN KEY COUNTRIES, 2021-2023

- 5.5 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.5.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 20 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR THREE KEY END-USE INDUSTRIES

- TABLE 5 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR THREE KEY END-USE INDUSTRIES (%)

- 5.5.2 BUYING CRITERIA

- FIGURE 21 BUYING CRITERIA FOR THREE KEY END-USE INDUSTRIES

- TABLE 6 BUYING CRITERIA FOR THREE KEY END-USE INDUSTRIES

- 5.6 VALUE CHAIN ANALYSIS

- FIGURE 22 PLASTIC COMPOUNDS MARKET: VALUE CHAIN ANALYSIS

- 5.6.1 RAW MATERIAL SUPPLIERS

- 5.6.2 RESIN MANUFACTURERS

- 5.6.3 COMPOUNDERS

- 5.6.4 MOLDERS

- 5.6.5 END USERS

- 5.7 ECOSYSTEM ANALYSIS

- FIGURE 23 PLASTIC COMPOUNDS MARKET: ECOSYSTEM ANALYSIS

- TABLE 7 PLASTIC COMPOUNDS MARKET: ROLE IN ECOSYSTEM

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 OEM USES COVESTRO'S LIGHTWEIGHT MAKROLON TC POLYCARBONATE FOR FOG LAMP HOUSING

- 5.8.2 RTP COMPANY DEVELOPS INNOVATIVE SOLUTIONS TO REDUCE ABRASION AND NOISE IN CABLE CONVEYOR SYSTEM

- 5.9 REGULATORY LANDSCAPE

- 5.9.1 REGULATIONS

- 5.9.1.1 North America

- 5.9.1.2 Europe

- 5.9.1.3 Asia Pacific

- 5.9.1 REGULATIONS

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 High-shear and continuous mixers for consistent polymer compounding

- 5.10.2 COMPLEMENTARY TECHNOLOGIES

- 5.10.2.1 Advanced twin-screw extruders for efficient polymer compounding

- 5.10.3 ADJACENT TECHNOLOGIES

- 5.10.3.1 Technologies for compounding biodegradable and bio-based polymers

- 5.10.1 KEY TECHNOLOGIES

- 5.11 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.11.1 REVENUE SHIFTS AND NEW REVENUE POCKETS FOR PLASTIC COMPOUNDS MARKET

- FIGURE 24 REVENUE SHIFT FOR PLASTIC COMPOUNDS MARKET

- 5.12 TRADE ANALYSIS

- TABLE 8 IMPORT TRADE DATA FOR PVC, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 9 EXPORT TRADE DATA FOR PVC, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 10 IMPORT TRADE DATA FOR PLASTICS, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 11 EXPORT TRADE DATA FOR PLASTICS, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 12 IMPORT TRADE DATA FOR PP, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 13 EXPORT TRADE DATA FOR PP, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 14 IMPORT TRADE DATA FOR PA, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 15 EXPORT TRADE DATA FOR PA, BY COUNTRY, 2019-2023 (USD THOUSAND)

- 5.13 KEY CONFERENCES AND EVENTS, 2024-2025

- TABLE 16 PLASTIC COMPOUNDS MARKET: KEY CONFERENCES & EVENTS, 2024-2025

- 5.14 PRICING TREND ANALYSIS

- 5.14.1 AVERAGE SELLING PRICE, BY REGION

- TABLE 17 AVERAGE SELLING PRICE, BY REGION (USD/KG)

- 5.14.2 AVERAGE SELLING PRICES OF KEY PLAYERS, BY PRODUCT

- TABLE 18 AVERAGE SELLING PRICES OF KEY PLAYERS, BY PRODUCT (USD/KG)

- 5.14.3 AVERAGE SELLING PRICES OF KEY PLAYERS, BY SOURCE

- TABLE 19 AVERAGE SELLING PRICES OF KEY PLAYERS, BY SOURCE (USD/KG)

- 5.14.4 AVERAGE SELLING PRICES OF KEY PLAYERS, BY END-USE INDUSTRY

- TABLE 20 AVERAGE SELLING PRICES OF KEY PLAYERS, BY END-USE INDUSTRY (USD/KG)

- 5.15 INVESTMENT AND FUNDING SCENARIO

- FIGURE 25 INVESTMENT AND FUNDING SCENARIO, 2023

- 5.16 PATENT ANALYSIS

- 5.16.1 METHODOLOGY

- 5.16.2 DOCUMENT TYPE

- FIGURE 26 GRANTED PATENTS

- 5.16.3 PUBLICATION TRENDS - LAST 10 YEARS

- FIGURE 27 TOTAL NUMBER OF PATENTS PUBLISHED FROM 2013 TO 2023

- 5.16.4 INSIGHTS

- 5.16.5 LEGAL STATUS OF PATENTS

- FIGURE 28 PATENT ANALYSIS, BY LEGAL STATUS

- 5.16.6 JURISDICTION-WISE PATENT ANALYSIS

- FIGURE 29 TOP JURISDICTIONS FOR PATENTS RELATED TO PLASTIC COMPOUNDS

- 5.16.7 TOP 10 COMPANIES/APPLICANTS

- FIGURE 30 COMPANIES/APPLICANTS WITH HIGHEST NUMBER OF PATENTS

- TABLE 21 PATENTS: SEMICONDUCTOR ENERGY LABORATORY CO., LTD.

- TABLE 22 PATENTS: SAMSUNG DISPLAY

- TABLE 23 PATENTS: BASF SE

- 5.16.8 TOP 10 PATENT OWNERS IN LAST 10 YEARS

- TABLE 24 TOP TEN PATENT OWNERS

6 PLASTIC COMPOUNDS MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- FIGURE 31 POLYPROPYLENE (PP) SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 25 PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (USD MILLION)

- TABLE 26 PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 27 PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (KILOTON)

- TABLE 28 PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (KILOTON)

- 6.2 POLYVINYL CHLORIDE (PVC)

- 6.2.1 IDEAL CHOICE FOR OUTDOOR APPLICATIONS

- 6.3 POLYETHYLENE (PE)

- 6.3.1 WIDE APPLICATIONS IN FOOD PACKAGING

- 6.4 POLYSTYRENE (PS)

- 6.4.1 VERSATILE MATERIAL USED ACROSS INDUSTRIES

- 6.5 POLYAMIDE (PA)

- 6.5.1 HIGH-PERFORMANCE THERMOPLASTIC WITH MULTIPLE APPLICATIONS

- 6.6 POLYETHYLENE TEREPHTHALATE (PET)

- 6.6.1 HIGH DEMAND DUE TO WIDE-RANGING PROPERTIES

- 6.7 POLYPROPYLENE (PP)

- 6.7.1 WIDE ADOPTION IN AUTOMOTIVE AND PACKING INDUSTRIES

- 6.8 POLYCARBONATE (PC)

- 6.8.1 HIGH-PERFORMANCE MATERIAL SUITED TO HARSH CONDITIONS

- 6.9 POLYURETHANE (PU)

- 6.9.1 VERSATILITY TO DRIVE DEMAND ACROSS INDUSTRIES

- 6.10 ACRYLONITRILE BUTADIENE STYRENE (ABS)

- 6.10.1 DRIVES EFFICIENCY AND PERFORMANCE IN KEY INDUSTRIES

- 6.11 OTHER PRODUCTS

7 PLASTIC COMPOUNDS MARKET, BY SOURCE

- 7.1 INTRODUCTION

- FIGURE 32 FOSSIL-BASED SEGMENT TO LEAD PLASTIC COMPOUNDS MARKET DURING FORECAST PERIOD

- TABLE 29 PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (USD MILLION)

- TABLE 30 PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- TABLE 31 PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (KILOTON)

- TABLE 32 PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (KILOTON)

- 7.2 FOSSIL-BASED

- 7.2.1 GROWING USE IN PACKAGING AND INDUSTRIAL APPLICATIONS

- 7.3 BIO-BASED

- 7.3.1 SUSTAINABLE ALTERNATIVES WITH WIDE-RANGING APPLICATIONS

- 7.4 RECYCLED

- 7.4.1 FACILITATE PLASTIC WASTE REDUCTION ACROSS INDUSTRIES

8 PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY

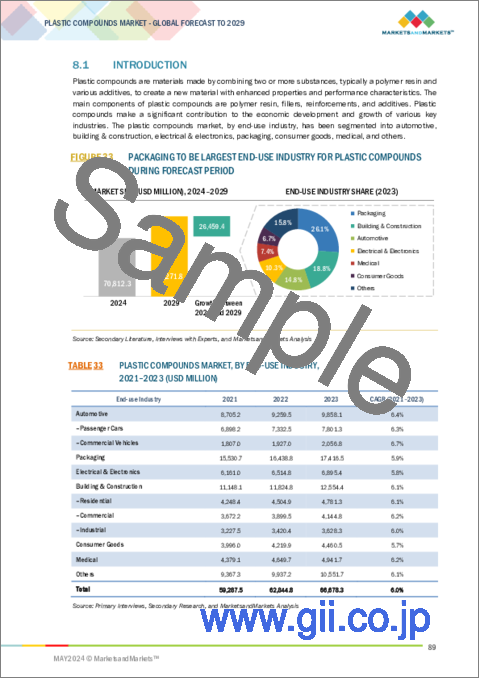

- 8.1 INTRODUCTION

- FIGURE 33 PACKAGING TO BE LARGEST END-USE INDUSTRY FOR PLASTIC COMPOUNDS DURING FORECAST PERIOD

- TABLE 33 PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 34 PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 35 PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 36 PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 8.2 AUTOMOTIVE

- 8.2.1 GROWING DEMAND TO REDUCE VEHICLE WEIGHT AND ENHANCE FUEL CONSUMPTION

- 8.2.2 PASSENGER CARS

- 8.2.3 COMMERCIAL VEHICLES

- 8.3 BUILDING & CONSTRUCTION

- 8.3.1 WIDE-RANGING APPLICATIONS DUE TO DURABILITY AND COST-EFFECTIVENESS

- 8.3.2 RESIDENTIAL

- 8.3.3 COMMERCIAL

- 8.3.4 INDUSTRIAL

- 8.4 ELECTRICAL & ELECTRONICS

- 8.4.1 INCREASING USE DUE TO IMPROVED SAFETY AND HIGH HEAT RESISTANCE

- 8.5 PACKAGING

- 8.5.1 HIGH DEMAND FOR LIGHTWEIGHT PLASTIC MATERIALS

- 8.6 CONSUMER GOODS

- 8.6.1 GROWING PREFERENCE FOR DURABLE AND COST-EFFECTIVE MATERIALS

- 8.7 MEDICAL

- 8.7.1 RISING DEMAND FOR PLASTICS WITH HIGH CHEMICAL RESISTANCE

- 8.8 OTHER INDUSTRIES

9 PLASTIC COMPOUNDS MARKET, BY REGION

- 9.1 INTRODUCTION

- FIGURE 34 PLASTIC COMPOUNDS MARKET: GEOGRAPHIC SNAPSHOT

- TABLE 37 PLASTIC COMPOUNDS MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 38 PLASTIC COMPOUNDS MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 39 PLASTIC COMPOUNDS MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 40 PLASTIC COMPOUNDS MARKET, BY REGION, 2024-2029 (KILOTON)

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: IMPACT OF RECESSION

- FIGURE 35 NORTH AMERICA: PLASTIC COMPOUNDS MARKET SNAPSHOT

- TABLE 41 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 42 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 43 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 44 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 45 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (USD MILLION)

- TABLE 46 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 47 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (KILOTON)

- TABLE 48 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (KILOTON)

- TABLE 49 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (USD MILLION)

- TABLE 50 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- TABLE 51 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (KILOTON)

- TABLE 52 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (KILOTON)

- TABLE 53 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 54 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 55 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 56 NORTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.2.2 US

- 9.2.2.1 Strict environment-related regulations to drive demand

- TABLE 57 US: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 58 US: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 59 US: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 60 US: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.2.3 CANADA

- 9.2.3.1 Thriving automotive industry to drive demand

- TABLE 61 CANADA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 62 CANADA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 63 CANADA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 64 CANADA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.2.4 MEXICO

- 9.2.4.1 Presence of leading automobile companies to drive market

- TABLE 65 MEXICO: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 66 MEXICO: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 67 MEXICO: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 68 MEXICO: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3 ASIA PACIFIC

- 9.3.1 ASIA PACIFIC: IMPACT OF RECESSION

- FIGURE 36 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET SNAPSHOT

- TABLE 69 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 70 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 71 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 72 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 73 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (USD MILLION)

- TABLE 74 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 75 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (KILOTON)

- TABLE 76 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (KILOTON)

- TABLE 77 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (USD MILLION)

- TABLE 78 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- TABLE 79 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (KILOTON)

- TABLE 80 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (KILOTON)

- TABLE 81 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 82 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 83 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 84 ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.2 CHINA

- 9.3.2.1 Strong demand in manufacturing sector to propel market

- TABLE 85 CHINA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 86 CHINA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 87 CHINA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 88 CHINA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.3 INDIA

- 9.3.3.1 Easy availability of raw materials to boost market

- TABLE 89 INDIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 90 INDIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 91 INDIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 92 INDIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.4 JAPAN

- 9.3.4.1 Rising demand in healthcare sector to drive market

- TABLE 93 JAPAN: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 94 JAPAN: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 95 JAPAN: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 96 JAPAN: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.5 SOUTH KOREA

- 9.3.5.1 High-performing manufacturing sector to boost market

- TABLE 97 SOUTH KOREA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 98 SOUTH KOREA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 99 SOUTH KOREA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 100 SOUTH KOREA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.6 MALAYSIA

- 9.3.6.1 Rising demand across industries to fuel market

- TABLE 101 MALAYSIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 102 MALAYSIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 103 MALAYSIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 104 MALAYSIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.7 PHILIPPINES

- 9.3.7.1 Government initiatives to drive market

- TABLE 105 PHILIPPINES: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 106 PHILIPPINES: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 107 PHILIPPINES: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 108 PHILIPPINES: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.8 THAILAND

- 9.3.8.1 Industrial growth and focus on innovation to fuel market

- TABLE 109 THAILAND: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 110 THAILAND: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 111 THAILAND: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 112 THAILAND: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.9 INDONESIA

- 9.3.9.1 Industrial expansion to drive demand

- TABLE 113 INDONESIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 114 INDONESIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 115 INDONESIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 116 INDONESIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.10 AUSTRALIA

- 9.3.10.1 Rising demand in key sectors to boost market

- TABLE 117 AUSTRALIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 118 AUSTRALIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 119 AUSTRALIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 120 AUSTRALIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.3.11 REST OF ASIA PACIFIC

- TABLE 121 REST OF ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 122 REST OF ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 123 REST OF ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 124 REST OF ASIA PACIFIC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.4 EUROPE

- 9.4.1 EUROPE: IMPACT OF RECESSION

- TABLE 125 EUROPE: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 126 EUROPE: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 127 EUROPE: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 128 EUROPE: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 129 EUROPE: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (USD MILLION)

- TABLE 130 EUROPE: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 131 EUROPE: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (KILOTON)

- TABLE 132 EUROPE: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (KILOTON)

- TABLE 133 EUROPE: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (USD MILLION)

- TABLE 134 EUROPE: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- TABLE 135 EUROPE: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (KILOTON)

- TABLE 136 EUROPE: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (KILOTON)

- TABLE 137 EUROPE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 138 EUROPE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 139 EUROPE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 140 EUROPE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.4.2 GERMANY

- 9.4.2.1 Strong demand in packaging industry to drive market

- TABLE 141 GERMANY: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 142 GERMANY: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 143 GERMANY: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 144 GERMANY: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.4.3 FRANCE

- 9.4.3.1 Growing pharmaceutical industry to drive demand

- TABLE 145 FRANCE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 146 FRANCE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 147 FRANCE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 148 FRANCE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.4.4 UK

- 9.4.4.1 Increasing investments in manufacturing sector to boost market

- TABLE 149 UK: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 150 UK: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 151 UK: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 152 UK: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.4.5 ITALY

- 9.4.5.1 Presence of global players to propel market growth

- TABLE 153 ITALY: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 154 ITALY: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 155 ITALY: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 156 ITALY: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.4.6 SPAIN

- 9.4.6.1 Rising demand for packaging across industries to boost market

- TABLE 157 SPAIN: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 158 SPAIN: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 159 SPAIN: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 160 SPAIN: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.4.7 REST OF EUROPE

- TABLE 161 REST OF EUROPE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 162 REST OF EUROPE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 163 REST OF EUROPE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 164 REST OF EUROPE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 MIDDLE EAST & AFRICA: IMPACT OF RECESSION

- TABLE 165 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 166 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 167 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 168 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 169 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (USD MILLION)

- TABLE 170 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 171 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (KILOTON)

- TABLE 172 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (KILOTON)

- TABLE 173 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (USD MILLION)

- TABLE 174 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- TABLE 175 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (KILOTON)

- TABLE 176 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (KILOTON)

- TABLE 177 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 178 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 179 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 180 MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.5.1.1 GCC Countries

- 9.5.1.2 Saudi Arabia

- 9.5.1.2.1 Growth in healthcare sector to drive demand

- TABLE 181 SAUDI ARABIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 182 SAUDI ARABIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 183 SAUDI ARABIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 184 SAUDI ARABIA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.5.1.3 UAE

- 9.5.1.3.1 Recovering construction industry to fuel market

- 9.5.1.3 UAE

- TABLE 185 UAE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 186 UAE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 187 UAE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 188 UAE: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.5.2 REST OF GCC

- TABLE 189 REST OF GCC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 190 REST OF GCC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 191 EST OF GCC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 192 REST OF GCC: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.5.3 SOUTH AFRICA

- 9.5.3.1 Growing government initiatives to drive demand

- TABLE 193 SOUTH AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 194 SOUTH AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 195 SOUTH AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 196 SOUTH AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.5.4 REST OF MIDDLE EAST & AFRICA

- TABLE 197 REST OF MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 198 REST OF MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 199 REST OF MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 200 REST OF MIDDLE EAST & AFRICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.6 SOUTH AMERICA

- 9.6.1 SOUTH AMERICA: IMPACT OF RECESSION

- TABLE 201 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 202 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 203 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 204 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 205 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (USD MILLION)

- TABLE 206 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 207 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2021-2023 (KILOTON)

- TABLE 208 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY PRODUCT, 2024-2029 (KILOTON)

- TABLE 209 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (USD MILLION)

- TABLE 210 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- TABLE 211 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2021-2023 (KILOTON)

- TABLE 212 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY SOURCE, 2024-2029 (KILOTON)

- TABLE 213 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 214 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 215 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 216 SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.6.2 BRAZIL

- 9.6.2.1 Growing automotive industry to fuel market

- TABLE 217 BRAZIL: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 218 BRAZIL: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 219 BRAZIL: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 220 BRAZIL: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.6.3 ARGENTINA

- 9.6.3.1 Rising demand across industries to propel market

- TABLE 221 ARGENTINA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 222 ARGENTINA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 223 ARGENTINA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 224 ARGENTINA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.6.4 REST OF SOUTH AMERICA

- TABLE 225 REST OF SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 226 REST OF SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 227 REST OF SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 228 REST OF SOUTH AMERICA: PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2019-APRIL 2024

- FIGURE 37 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN PLASTIC COMPOUNDS MARKET, JANUARY 2019-APRIL 2024

- 10.3 MARKET SHARE ANALYSIS

- FIGURE 38 SHARE OF LEADING COMPANIES IN PLASTIC COMPOUNDS MARKET, 2023

- TABLE 229 PLASTIC COMPOUNDS MARKET: DEGREE OF COMPETITION

- 10.4 REVENUE ANALYSIS

- FIGURE 39 REVENUE ANALYSIS OF KEY COMPANIES IN PLASTIC COMPOUNDS MARKET, 2023

- 10.5 MARKET RANKING ANALYSIS

- FIGURE 40 RANKING OF KEY PLAYERS IN PLASTIC COMPOUNDS MARKET, 2023

- 10.6 COMPANY VALUATION AND FINANCIAL METRICS

- FIGURE 41 COMPANY VALUATION OF LEADING COMPANIES IN PLASTIC COMPOUNDS MARKET, 2023

- FIGURE 42 FINANCIAL METRICS OF LEADING COMPANIES IN PLASTIC COMPOUNDS MARKET, 2023

- 10.7 BRAND/PRODUCT COMPARISON

- FIGURE 43 PLASTIC COMPOUNDS MARKET: BRAND/PRODUCT COMPARISON

- 10.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 10.8.1 STARS

- 10.8.2 EMERGING LEADERS

- 10.8.3 PERVASIVE PLAYERS

- 10.8.4 PARTICIPANTS

- FIGURE 44 PLASTIC COMPOUNDS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- 10.8.5 COMPANY FOOTPRINT, KEY PLAYERS, 2023

- 10.8.5.1 Company footprint

- 10.8.5.2 Region footprint

- 10.8.5.3 Product footprint

- 10.8.5.4 Source footprint

- 10.8.5.5 End-use industry footprint

- 10.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 10.9.1 PROGRESSIVE COMPANIES

- 10.9.2 RESPONSIVE COMPANIES

- 10.9.3 DYNAMIC COMPANIES

- 10.9.4 STARTING BLOCKS

- FIGURE 45 PLASTIC COMPOUNDS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- 10.9.5 COMPETITIVE BENCHMARKING

- TABLE 230 PLASTIC COMPOUNDS MARKET: KEY STARTUPS/SMES

- TABLE 231 PLASTIC COMPOUNDS MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- 10.10 COMPETITIVE SCENARIO AND TRENDS

- 10.10.1 PRODUCT LAUNCHES

- TABLE 232 PLASTIC COMPOUNDS MARKET: PRODUCT LAUNCHES, JANUARY 2019-APRIL 2024

- 10.10.2 DEALS

- TABLE 233 PLASTIC COMPOUNDS MARKET: DEALS, JANUARY 2019-APRIL 2024

- 10.10.3 EXPANSIONS

- TABLE 234 PLASTIC COMPOUNDS MARKET: EXPANSIONS, JANUARY 2019-APRIL 2024

11 COMPANY PROFILES

- (Business overview, Products/Solutions/Services offered, Recent developments & MnM View)**

- 11.1 MAJOR PLAYERS

- 11.1.1 BASF SE

- TABLE 235 BASF SE: COMPANY OVERVIEW

- FIGURE 46 BASF SE: COMPANY SNAPSHOT

- 11.1.2 THE DOW CHEMICAL COMPANY

- TABLE 236 THE DOW CHEMICAL COMPANY: COMPANY OVERVIEW

- FIGURE 47 THE DOW CHEMICAL COMPANY: COMPANY SNAPSHOT

- 11.1.3 LYONDELLBASELL INDUSTRIES HOLDINGS

- TABLE 237 LYONDELLBASELL INDUSTRIES HOLDINGS: COMPANY OVERVIEW

- FIGURE 48 LYONDELLBASELL INDUSTRIES HOLDINGS: COMPANY SNAPSHOT

- 11.1.4 SABIC

- TABLE 238 SABIC: COMPANY OVERVIEW

- FIGURE 49 SABIC: COMPANY SNAPSHOT

- 11.1.5 ASAHI KASEI CORPORATION

- TABLE 239 ASAHI KASEI CORPORATION: COMPANY OVERVIEW

- FIGURE 50 ASAHI KASEI CORPORATION: COMPANY SNAPSHOT

- 11.1.6 COVESTRO AG

- TABLE 240 COVESTRO AG: COMPANY OVERVIEW

- FIGURE 51 COVESTRO AG: COMPANY SNAPSHOT

- 11.1.7 CELANESE CORPORATION

- TABLE 241 CELANESE CORPORATION: COMPANY OVERVIEW

- FIGURE 52 CELANESE CORPORATION: COMPANY SNAPSHOT

- 11.1.8 ARKEMA

- TABLE 242 ARKEMA: COMPANY OVERVIEW

- FIGURE 53 ARKEMA: COMPANY SNAPSHOT

- 11.1.9 RTP COMPANY

- TABLE 243 RTP COMPANY: COMPANY OVERVIEW

- 11.1.10 WESTLAKE CORPORATION

- TABLE 244 WESTLAKE CORPORATION: COMPANY OVERVIEW

- FIGURE 54 WESTLAKE CORPORATION: COMPANY SNAPSHOT

- *Details on Business overview, Products/Solutions/Services offered, Recent developments & MnM View might not be captured in case of unlisted companies.

- 11.2 OTHER PLAYERS

- 11.2.1 AVIENT CORPORATION

- TABLE 245 AVIENT CORPORATION: BUSINESS OVERVIEW

- 11.2.2 GEON PERFORMANCE SOLUTIONS

- TABLE 246 GEON PERFORMANCE SOLUTIONS: BUSINESS OVERVIEW

- 11.2.3 RAVAGO

- TABLE 247 RAVAGO: BUSINESS OVERVIEW

- 11.2.4 AURORA MATERIAL SOLUTIONS

- TABLE 248 AURORA MATERIAL SOLUTIONS: BUSINESS OVERVIEW

- 11.2.5 ORBIA

- TABLE 249 ORBIA: BUSINESS OVERVIEW

- 11.2.6 AMERICHEM

- TABLE 250 AMERICHEM: BUSINESS OVERVIEW

- 11.2.7 POLYKEMI

- TABLE 251 POLYKEMI: BUSINESS OVERVIEW

- 11.2.8 RIKEN AMERICAS CORPORATION

- TABLE 252 RIKEN AMERICAS CORPORATION: BUSINESS OVERVIEW

- 11.2.9 TEKNI-PLEX, INC.

- TABLE 253 TEKNI-PLEX, INC.: BUSINESS OVERVIEW

- 11.2.10 SHINTECH INC.

- TABLE 254 SHINTECH INC.: BUSINESS OVERVIEW

- 11.2.11 MANNER POLYMERS

- TABLE 255 MANNER POLYMERS: BUSINESS OVERVIEW

- 11.2.12 EIQSA

- TABLE 256 EIQSA: BUSINESS OVERVIEW

- 11.2.13 POLYMER ASIA

- TABLE 257 POLYMER ASIA: BUSINESS OVERVIEW

- 11.2.14 DENKA CHEMICALS HOLDINGS

- TABLE 258 DENKA CHEMICALS HOLDINGS: BUSINESS OVERVIEW

- 11.2.15 RADICI PARTECIPAZIONI SPA

- TABLE 259 RADICI PARTECIPAZIONI SPA: BUSINESS OVERVIEW

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS