|

|

市場調査レポート

商品コード

1493070

ロボット放射線治療の世界市場の規模:製品別、技術別、用途別、エンドユーザー別、地域別 - 予測(~2028年)Robotic Radiotherapy Market Size by Product (System, Software, 3D Camera), Technology (LINAC, Stereotactic, Particle Therapy), Application (Lung, Breast, Colorectal), End-User (Hospitals, Radiotherapy Centres), & Region - Global Forecast to 2028 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ロボット放射線治療の世界市場の規模:製品別、技術別、用途別、エンドユーザー別、地域別 - 予測(~2028年) |

|

出版日: 2024年04月15日

発行: MarketsandMarkets

ページ情報: 英文 195 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界のロボット放射線治療の市場規模は、2023年の11億米ドルから2028年までに19億米ドルに達し、予測期間にCAGRで11.9%の成長が見込まれます。

がんの有病率の上昇とロボット放射線治療の利用の拡大は、予測年間における市場成長の主な促進要因です。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2028年 |

| 基準年 | 2023年 |

| 予測期間 | 2023年~2028年 |

| 単位 | 金額(10億米ドル) |

| セグメント | 製品、技術、用途、エンドユーザー、地域 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

「市場の3Dカメラ(SGRT)セグメントが予測期間にもっとも高いCAGRで成長します。」

3Dカメラセグメントが予測期間にもっとも高いCAGRを記録する見込みです。このセグメントの成長は主に、非侵襲かつリアルタイムの、6次の患者の位置決めとモニタリングを放射線治療プロセス前と治療中に提供する能力によるものであり、それが正確な治療の提供につながり、がん施設に広く受け入れられています。しかし、SGRT製品に関連する多額のメンテナンスコストや、新興国全体でのロボット放射線治療に関する規制ガイドラインの導入の遅れなどの要因が、市場成長を抑制すると予測されます。

「用途別では、肺がんセグメントが2020年に市場で最大のシェアを占めました」

肺がんセグメントが2022年に市場の最大のシェアを占めました。このセグメントの主な促進要因は、喫煙率の増加、特に空気質の悪い都市部での大気汚染物質への暴露、鉱業、建設、製造での発がん性物質への暴露です。現代のライフスタイルや食習慣は、肺がんのリスクをさらに高める可能性があります。世界の人々が高齢化するにつれて、肺がんの罹患率は上昇する傾向にあり、患者数の増加につながる可能性があります。

「病院エンドユーザーセグメントの成長を促進する政府の取り組みと設置の増加」

病院はロボット放射線治療製品の主要エンドユーザーです。このエンドユーザーが大きなシェアを占めている主な理由は、自動放射線治療システムの需要、自動放射線治療システムの進歩、ARTステーションの設置の増加、効果的なARTと治療に向けた政府投資の増加です。

「地域別では、アジア太平洋市場が予測期間にもっとも高い成長率を記録します。」

アジア太平洋市場は、可処分所得の増加とがん患者の増加により、大きく成長する可能性が高いです。各国政府によるロボット放射線治療システムへの投資や、産業インフラと公共インフラの近代化、病院における最先端放射線治療の浸透が注目されます。しかし、先進の器具の操作に熟練した専門家の不足、予算の制約による治療の実施の遅れ、著名な製品メーカーが直面する価格圧力などが、アジア太平洋に大きな機会があるにもかかわらず、ロボット放射線治療市場の主な成長抑制要因となっています。

当レポートでは、世界のロボット放射線治療市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- ロボット放射線治療市場の概要

- ロボット放射線治療市場:製品別(2023年・2028年)

- 北米のロボット放射線治療市場:国別、エンドユーザー別(2022年)

- ロボット放射線治療市場:各国の成長率の比較

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 技術分析

- ポーターのファイブフォース分析

- 主なステークホルダーと購入基準

- 規制分析

- 米国

- 欧州

- 日本

- 償還シナリオ

- エコシステム分析

- バリューチェーン分析

- 研究開発

- 調達、製品開発

- マーケティング、販売・流通、アフターサービス

- サプライチェーン分析

- 著名企業

- 中小企業

- エンドユーザー

- 価格分析

- 特許分析

- 貿易分析

- 主な会議とイベント(2022年~2023年)

- 顧客のビジネスに影響を与える動向/混乱

第6章 ロボット放射線治療市場:製品別

- イントロダクション

- 放射線治療システム

- ソフトウェア

- 3Dカメラ

- その他の製品

第7章 ロボット放射線治療市場:技術別

- イントロダクション

- リニアアクセラレーター

- 定位放射線治療

- 粒子線治療システム

第8章 ロボット放射線治療市場:用途別

- イントロダクション

- 肺がん

- 乳がん

- 前立腺がん

- 頭頸部がん

- 大腸がん

- その他のがん

第9章 ロボット放射線治療市場:エンドユーザー別

- イントロダクション

- 病院

- 独立放射線治療センター

第10章 ロボット放射線治療市場:地域別

- イントロダクション

- 北米

- 北米に対する不況の影響

- 米国

- カナダ

- 欧州

- 欧州に対する不況の影響

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- アジア太平洋に対する不況の影響

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- その他の地域

第11章 競合情勢

- 概要

- 主要企業戦略

- 収益分析

- 市場シェア分析:ロボット放射線治療市場、主要企業別(2022年)

- 企業評価マトリクス(2022年)

- スタートアップ/中小企業の評価マトリクス(2022年)

- 競合ベンチマーキング

- 競合シナリオ(2019年~2023年)

第12章 企業プロファイル

- 主要企業

- SIEMENS HEALTHINEERS AG (VARIAN MEDICAL SYSTEMS, INC.)

- ELEKTA

- ACCURAY INCORPORATED

- VIEWRAY TECHNOLOGIES, INC.

- C-RAD

- IBA

- HITACHI LTD.

- MEVION MEDICAL SYSTEMS

- PANACEA MEDICAL TECHNOLOGIES PVT. LTD.

- P-CURE

- PROVISION HEALTHCARE

- SUMITOMO HEAVY INDUSTRY LTD.

- PHILIPS HEALTHCARE

- RAYSEARCH LABORATORIES

- PROTOM INTERNATIONAL, INC.

- OPTIVUS PROTON THERAPY, INC.

- TOSHIBA CORPORATION

- VISION RT LTD.

- ADVANCED ONCOTHERAPY PLC

- MIM SOFTWARE INC.

- その他の企業

- STANDARD IMAGING, INC.

- BRAINLAB AG

- MAGNETTX ONCOLOGY SOLUTIONS LTD.

- PTW FREIBURG GMBH

- DOSISOFT SA

第13章 付録

The global robotic radiotherapy market is projected to reach USD 1.9 billion by 2028 from USD 1.1 billion in 2023, growing at a CAGR of 11.9% during the forecast period. The rising prevalence of cancer and the growing use of robotic radiotherapy is one of the major factors anticipated to boost market growth in the forecasting years.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2028 |

| Base Year | 2023 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD) Billion |

| Segments | Product, Technology, Application, End Users, and Region |

| Regions covered | North America, Europe, Asia Pacific, and the Rest of the world |

"3D cameras (SGRT) segment of global robotic radiotherapy market to grow with the highest CAGR in the forecast period."

On the basis of product, the robotic radiotherapy market is segmented into radiotherapy systems, software, 3D cameras, and others. The 3D cameras segment is expected to register the highest CAGR in the forecast period. Growth in this segment is majorly driven by the ability to offer non-invasive, real-time, 6-degree dimensional patient positioning and monitoring before and during the radiation therapy treatment process, resulting in accurate treatment delivery and wide acceptance by cancer facilities. However, factors such as significant maintenance costs associated with SGRT products, as well as the slow implementation of regulatory guidelines for robotic radiotherapy across emerging countries, are expected to restrain market growth.

"Lung cancer segment, by application, accounted for the largest market share of global robotic radiotherapy market in 2020."

Based on application, the global robotic radiotherapy market is segmented into prostate cancer, breast cancer, lung cancer, head & neck cancer, colorectal cancer, and other cancers. The lung cancer segment accounted for the largest share of the global robotic radiotherapy market in 2022. The major drivers of this segment are increasing smoking rates, exposure to air pollutants, especially in urban areas with poor air quality, and exposure to carcinogens in mining, construction, and manufacturing. Modern lifestyles and dietary habits may further elevate the risk of lung cancer. As the global population ages, lung cancer incidence tends to rise, potentially leading to a higher number of cases.

"Increased installations and government initiatives to drive the segment growth of hospitals end-user segment."

Based on the end user, the robotic radiotherapy market is segmented into hospitals and independent radiotherapy centers. Hospitals are the major end users of robotic radiotherapy products. The large share of this end-user segment is primarily attributed to the demand for automated radiation therapy systems, advancement in automated radiation therapy systems and the increasing installations of ART stations, and the rising government investments for effective ART and treatment.

"The APAC market, by region, to register highest growth rate in the forecast period."

On the basis of region, the robotic radiotherapy market is segmented into North America, Europe, Asia Pacific, and the Rest of the World. The Asia-Pacific market is likely witness significant growth owing to increase in disposable income and increase in cancer patient pool. Focus on governments on investment on robotic radiotherapy systems, modernization of industrial and public infrastructures, and rising penetration of cutting-edge radiation therapy in hospitals. However, a dearth of skilled professionals for the operation of advanced instruments, slow implementation of therapy due to budgetary constraints, and pricing pressures faced by prominent product manufacturers are the key factors restraining the growth of the robotic radiotherapy market despite the great opportunities available in the APAC region.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-48%, Tier 2-36%, and Tier 3- 16%

- By Designation: C-level-10%, Director-level-14%, and Others-76%

- By Region: North America-40%, Europe-32%, Asia Pacific-20%, Latin America-5%, MEA- 3%

The prominent players in the robotic radiotherapy market are Siemens Healthcare GmbH (Germany), Elekta (Sweden), Accuray Incorporated (US), IBA (Belgium), ViewRay Technologies, Inc. (US), C-RAD (Sweden), IBA Worldwide (Belgium), Hitachi Ltd. (Japan (US), Mevion Medical Systems (US), Optivus Proton Therapy, Inc. (US) and Panacea Medical Technologies Pvt. Ltd. (India), among others.

Research Coverage

This report studies the robotic radiotherapy market based on product, technology, application, end-user, and region. It also covers the factors affecting market growth, analyzes the various opportunities and challenges in the market, and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets with respect to their individual growth trends and forecasts the revenue of the market segments with respect to four main regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them to garner a larger market share. Firms purchasing the report could use one or a combination of the below-mentioned strategies to strengthen their market presence.

This report provides insights on the following pointers:

- Analysis of key drivers (growing demand for non-invasive treatments, technological advancements, rising prevalence of cancer, growing use of automated radiation therapy for cancer treatment), restraints (lack of adequate healthcare, high cost of automated radiation therapy systems, complex nature of technology, dearth of skilled radiologist), opportunities (rising healthcare expenditure across developing countries, growing government and private investments, adoption of radiation therapy), and challenges (risk of radiation exposure, competition from alternative treatment modalities) influencing the growth of robotic radiotherapy market

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the robotic radiotherapy market

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the robotic radiotherapy market

- Market Development: Comprehensive information on lucrative emerging regions

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the market

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 GEOGRAPHIES COVERED

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 LIMITATIONS

- 1.5 MARKET STAKEHOLDERS

- 1.5.1 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.2 RESEARCH DESIGN

- 2.2.1 SECONDARY RESEARCH

- 2.2.2 PRIMARY RESEARCH

- 2.2.2.1 Primary sources

- 2.2.2.2 Key data from secondary sources

- 2.2.2.3 Breakdown of primaries

- FIGURE 1 BREAKDOWN OF PRIMARY INTERVIEWS: SUPPLY-SIDE AND DEMAND-SIDE PARTICIPANTS

- FIGURE 2 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.3 MARKET SIZE ESTIMATION

- FIGURE 3 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Approach 1: Company revenue estimation approach

- FIGURE 4 MARKET SIZE ESTIMATION FOR ROBOTIC RADIOTHERAPY: APPROACH 1 (COMPANY REVENUE ESTIMATION)

- 2.3.1.2 Approach 2: Customer-based market estimation

- FIGURE 5 ROBOTIC RADIOTHERAPY MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 2.3.1.3 Approach 3: Top-down approach

- 2.3.1.4 Approach 4: Primary interviews

- 2.3.2 TOP-DOWN APPROACH

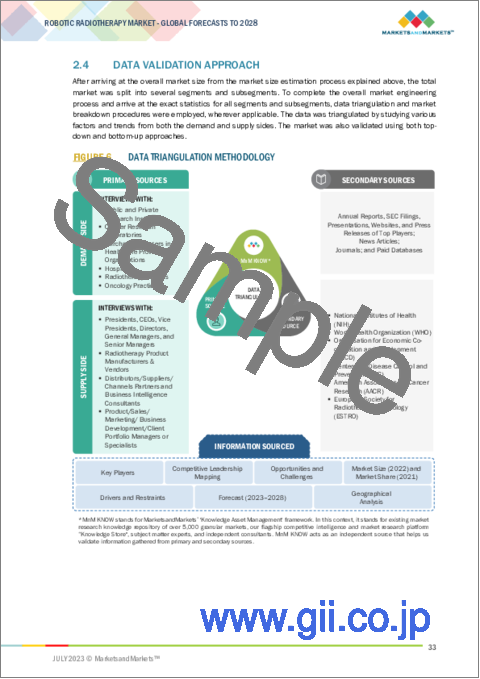

- 2.4 DATA VALIDATION APPROACH

- FIGURE 6 DATA TRIANGULATION METHODOLOGY

- 2.5 MARKET SHARE ASSESSMENT

- 2.6 STUDY ASSUMPTIONS

- 2.7 RISK ASSESSMENT

- TABLE 1 LIMITATIONS AND ASSOCIATED RISKS

- 2.8 GROWTH RATE ASSUMPTIONS

- 2.9 RECESSION IMPACT ANALYSIS

3 EXECUTIVE SUMMARY

- FIGURE 7 ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2023 VS. 2028 (USD MILLION)

- FIGURE 8 ROBOTIC RADIOTHERAPY MARKET, BY APPLICATION, 2023 VS. 2028 (USD MILLION)

- FIGURE 9 ROBOTIC RADIOTHERAPY MARKET, BY TECHNOLOGY, 2023 VS. 2028 (USD MILLION)

- FIGURE 10 ROBOTIC RADIOTHERAPY MARKET, BY END USER, 2023 VS. 2028 (USD MILLION)

- FIGURE 11 GEOGRAPHICAL SNAPSHOT: ROBOTIC RADIOTHERAPY MARKET

4 PREMIUM INSIGHTS

- 4.1 ROBOTIC RADIOTHERAPY MARKET OVERVIEW

- FIGURE 12 INCREASING GERIATRIC POPULATION AND GROWING R&D INVESTMENTS TO DRIVE MARKET

- 4.2 ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2023 VS. 2028 (USD MILLION)

- FIGURE 13 RADIOTHERAPY SYSTEMS TO DOMINATE MARKET IN 2028

- 4.3 NORTH AMERICA: ROBOTIC RADIOTHERAPY MARKET, BY COUNTRY AND END USER, 2022 (USD MILLION)

- FIGURE 14 HOSPITALS DOMINATED END-USER MARKET IN 2022

- 4.4 ROBOTIC RADIOTHERAPY MARKET: COMPARISON OF COUNTRY-WISE GROWTH RATES

- FIGURE 15 INDIA AND CHINA TO SHOW HIGHEST GROWTH DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 16 ROBOTIC RADIOTHERAPY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Rising prevalence of cancer

- TABLE 2 PROJECTED INCREASE IN CANCER CASES, 2020-2040

- 5.2.1.2 Growing demand for noninvasive treatment

- 5.2.2 RESTRAINTS

- 5.2.2.1 Premium Product Pricing

- 5.2.2.2 Complexities associated with automated/robotic radiotherapy

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising healthcare expenditure across emerging economies

- 5.2.3.2 Government and private investments to boost cancer treatment availability

- 5.2.4 CHALLENGES

- 5.2.4.1 Risk of radiation exposure

- 5.2.4.2 Dearth of skilled personnel

- 5.3 TECHNOLOGY ANALYSIS

- 5.4 PORTER'S FIVE FORCES ANALYSIS

- TABLE 3 ROBOTIC RADIOTHERAPY MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.4.1 THREAT OF NEW ENTRANTS

- 5.4.2 THREAT OF SUBSTITUTES

- 5.4.3 BARGAINING POWER OF SUPPLIERS

- 5.4.4 BARGAINING POWER OF BUYERS

- 5.4.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.5 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.5.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 17 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF RADIOTHERAPY SYSTEMS

- TABLE 4 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY PRODUCT SEGMENTS (%)

- 5.6 REGULATORY ANALYSIS

- 5.6.1 US

- TABLE 5 US: MEDICAL DEVICE REGULATORY APPROVAL PROCESS

- 5.6.2 EUROPE

- 5.6.3 JAPAN

- TABLE 6 JAPAN: MEDICAL DEVICE CLASSIFICATION UNDER PMDA

- 5.7 REIMBURSEMENT SCENARIO

- TABLE 7 CPT CODES FOR IMRT

- TABLE 8 CPT CODES FOR SBRT

- TABLE 9 CPT CODES FOR PROTON BEAM THERAPY

- TABLE 10 FREESTANDING PER COURSE NATIONAL AVERAGE MEDICARE REIMBURSEMENT, 2021 VS 2022

- TABLE 11 PROPOSED AMBULATORY PAYMENT CLASSIFICATION 2023 RATES

- TABLE 12 IMPACT OF CLINICAL LABOR PRICE CHANGES ON RADIATION ONCOLOGY SERVICES

- 5.8 ECOSYSTEM ANALYSIS

- 5.9 VALUE CHAIN ANALYSIS

- 5.9.1 RESEARCH & DEVELOPMENT

- 5.9.2 PROCUREMENT AND PRODUCT DEVELOPMENT

- 5.9.3 MARKETING, SALES & DISTRIBUTION, AND POST-SALES SERVICES

- FIGURE 18 VALUE CHAIN ANALYSIS IN ROBOTIC RADIOTHERAPY MARKET

- 5.10 SUPPLY CHAIN ANALYSIS

- 5.10.1 PROMINENT COMPANIES

- 5.10.2 SMALL & MEDIUM-SIZED COMPANIES

- 5.10.3 END USERS

- FIGURE 19 SUPPLY CHAIN ANALYSIS OF ROBOTIC RADIOTHERAPY MARKET

- 5.11 PRICING ANALYSIS

- TABLE 13 PRICING ANALYSIS OF RADIOTHERAPY SYSTEMS (USD)

- 5.12 PATENT ANALYSIS

- FIGURE 20 TOP TEN PATENT APPLICANTS FOR RADIOTHERAPY (JANUARY 2012 TO JUNE 2022)

- FIGURE 21 TOP TEN PATENT INVENTORS FOR RADIOTHERAPY (JANUARY 2012 TO JUNE 2023)

- FIGURE 22 TOP TEN PATENT OWNERS FOR RADIOTHERAPY (JANUARY 2012 TO JUNE 2023)

- 5.13 TRADE ANALYSIS

- TABLE 14 IMPORT DATA FOR RADIOTHERAPY SYSTEMS (HS CODE 9022), BY COUNTRY, 2018-2022 (USD THOUSAND)

- TABLE 15 EXPORT DATA FOR RADIOTHERAPY SYSTEMS (HS CODE 9022), BY COUNTRY, 2018-2022 (USD THOUSAND)

- 5.14 KEY CONFERENCES AND EVENTS IN 2022-2023

- TABLE 16 ROBOTIC RADIOTHERAPY MARKET: DETAILED LIST OF KEY CONFERENCES AND EVENTS IN 2022-2023

- 5.15 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 23 EMERGING TRENDS AND OPPORTUNITIES AFFECTING FUTURE REVENUE MIX

6 ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- TABLE 17 ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 6.2 RADIOTHERAPY SYSTEMS

- 6.2.1 RISING USE OF AI AND AUTOMATION TO DRIVE MARKET

- TABLE 18 RADIOTHERAPY SYSTEMS MARKET, BY REGION, 2020-2028 (USD MILLION)

- 6.3 SOFTWARE

- 6.3.1 NEED TO ENSURE TREATMENT EFFECTIVENESS AND ACCURACY TO BOOST GROWTH

- TABLE 19 SOFTWARE MARKET, BY REGION, 2020-2028 (USD MILLION)

- 6.4 3D CAMERAS

- 6.4.1 GROWING USE OF SGRT TO DRIVE DEMAND

- TABLE 20 3D CAMERAS MARKET, BY REGION, 2020-2028 (USD MILLION)

- 6.5 OTHER PRODUCTS

- TABLE 21 OTHER ROBOTIC RADIOTHERAPY MARKET, BY REGION, 2020-2028 (USD MILLION)

7 ROBOTIC RADIOTHERAPY MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- TABLE 22 ROBOTIC RADIOTHERAPY MARKET, BY TECHNOLOGY, 2020-2028 (USD MILLION)

- 7.2 LINEAR ACCELERATORS

- TABLE 23 LINEAR ACCELERATORS MARKET, BY TYPE, 2020-2028 (USD MILLION)

- 7.2.1 CONVENTIONAL LINEAR ACCELERATORS

- 7.2.1.1 Longer treatment duration to limit adoption

- 7.2.2 MRI LINEAR ACCELERATORS

- 7.2.2.1 Rising awareness about benefits to enhance demand

- 7.3 STEREOTACTIC RADIATION THERAPY

- TABLE 24 STEREOTACTIC RADIATION THERAPY MARKET, BY TYPE, 2020-2028 (USD MILLION)

- 7.3.1 CYBERKNIFE

- 7.3.1.1 Precision and correction capabilities to boost adoption

- 7.3.2 GAMMA KNIFE

- 7.3.2.1 Ongoing product development to drive market

- 7.4 PARTICLE THERAPY SYSTEMS

- TABLE 25 PARTICLE THERAPY SYSTEMS MARKET, BY TYPE, 2020-2028 (USD MILLION)

- 7.4.1 PROTON BEAM THERAPY

- 7.4.1.1 Rising establishment of proton therapy cancer centers to drive market

- 7.4.2 HEAVY ION THERAPY

- 7.4.2.1 Limited number of facilities to slow growth

8 ROBOTIC RADIOTHERAPY MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- TABLE 26 ROBOTIC RADIOTHERAPY MARKET, BY APPLICATION, 2020-2028 (USD MILLION)

- 8.2 LUNG CANCER

- 8.2.1 LUNG CANCER TO DOMINATE APPLICATIONS MARKET

- TABLE 27 ROBOTIC RADIOTHERAPY MARKET FOR LUNG CANCER, BY REGION, 2020-2028 (USD MILLION)

- 8.3 BREAST CANCER

- 8.3.1 INCREASING INCIDENCE OF BREAST CANCER TO DRIVE MARKET

- TABLE 28 ROBOTIC RADIOTHERAPY MARKET FOR BREAST CANCER, BY REGION, 2020-2028 (USD MILLION)

- 8.4 PROSTATE CANCER

- 8.4.1 PREFERENCE FOR NONINVASIVE TREATMENT TO BOOST GROWTH

- TABLE 29 ROBOTIC RADIOTHERAPY MARKET FOR PROSTATE CANCER, BY REGION, 2020-2028 (USD MILLION)

- 8.5 HEAD & NECK CANCER

- 8.5.1 GROWING UTILIZATION OF CYBERKNIFE FOR TREATMENT TO DRIVE MARKET

- TABLE 30 ROBOTIC RADIOTHERAPY MARKET FOR HEAD & NECK CANCER, BY REGION, 2020-2028 (USD MILLION)

- 8.6 COLORECTAL CANCER

- 8.6.1 RISING INCIDENCE OF COLORECTAL CANCER TO SUPPORT GROWTH

- TABLE 31 ROBOTIC RADIOTHERAPY MARKET FOR COLORECTAL CANCER, BY REGION, 2020-2028 (USD MILLION)

- 8.7 OTHER CANCERS

- TABLE 32 ROBOTIC RADIOTHERAPY MARKET FOR OTHER CANCERS, BY REGION, 2020-2028 (USD MILLION)

9 ROBOTIC RADIOTHERAPY MARKET, BY END USER

- 9.1 INTRODUCTION

- TABLE 33 ROBOTIC RADIOTHERAPY MARKET, BY END USER, 2020-2028 (USD MILLION)

- 9.2 HOSPITALS

- 9.2.1 LARGE NUMBER OF SURGICAL AND DIAGNOSTIC PROCEDURES TO PROPEL MARKET

- TABLE 34 ROBOTIC RADIOTHERAPY MARKET FOR HOSPITALS, BY REGION, 2020-2028 (USD MILLION)

- 9.3 INDEPENDENT RADIOTHERAPY CENTERS

- 9.3.1 LIMITED SURGICAL CAPABILITIES OF AVAILABLE PRODUCTS TO RESTRAIN ADOPTION

- TABLE 35 ROBOTIC RADIOTHERAPY MARKET FOR INDEPENDENT RADIOTHERAPY CENTERS, BY REGION, 2020-2028 (USD MILLION)

10 ROBOTIC RADIOTHERAPY MARKET, BY REGION

- 10.1 INTRODUCTION

- TABLE 36 ROBOTIC RADIOTHERAPY MARKET, BY REGION, 2020-2028 (USD MILLION)

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 24 NORTH AMERICA: ROBOTIC RADIOTHERAPY MARKET SNAPSHOT

- TABLE 37 NORTH AMERICA: ROBOTIC RADIOTHERAPY MARKET, BY COUNTRY, 2020-2028 (USD MILLION)

- TABLE 38 NORTH AMERICA: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- TABLE 39 NORTH AMERICA: ROBOTIC RADIOTHERAPY MARKET, BY TECHNOLOGY, 2020-2028 (USD MILLION)

- TABLE 40 NORTH AMERICA: ROBOTIC RADIOTHERAPY MARKET, BY APPLICATION, 2020-2028 (USD MILLION)

- TABLE 41 NORTH AMERICA: ROBOTIC RADIOTHERAPY MARKET, BY END USER, 2020-2028 (USD MILLION)

- 10.2.2 US

- 10.2.2.1 US to dominate North American market over forecast period

- TABLE 42 US: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.2.3 CANADA

- 10.2.3.1 Increasing government initiatives and favorable reimbursement to drive market

- TABLE 43 CANADA: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.3 EUROPE

- 10.3.1 EUROPE: RECESSION IMPACT

- TABLE 44 EUROPE: ROBOTIC RADIOTHERAPY MARKET, BY COUNTRY, 2020-2028 (USD MILLION)

- TABLE 45 EUROPE: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- TABLE 46 EUROPE: ROBOTIC RADIOTHERAPY MARKET, BY TECHNOLOGY, 2020-2028 (USD MILLION)

- TABLE 47 EUROPE: ROBOTIC RADIOTHERAPY MARKET, BY APPLICATION, 2020-2028 (USD MILLION)

- TABLE 48 EUROPE: ROBOTIC RADIOTHERAPY MARKET, BY END USER, 2020-2028 (USD MILLION)

- 10.3.2 GERMANY

- 10.3.2.1 Increasing aging population and rising life expectancy to drive market

- TABLE 49 GERMANY: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.3.3 FRANCE

- 10.3.3.1 Well-developed healthcare sector and rising geriatric population to drive market

- TABLE 50 FRANCE: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.3.4 UK

- 10.3.4.1 High burden of chronic diseases to support adoption

- TABLE 51 UK: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.3.5 ITALY

- 10.3.5.1 Increasing geriatric population to drive market

- TABLE 52 ITALY: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.3.6 SPAIN

- 10.3.6.1 Technological developments in healthcare to drive market

- TABLE 53 SPAIN: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.3.7 REST OF EUROPE

- TABLE 54 REST OF EUROPE: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 25 ASIA PACIFIC: ROBOTIC RADIOTHERAPY MARKET SNAPSHOT

- TABLE 55 ASIA PACIFIC: ROBOTIC RADIOTHERAPY MARKET, BY COUNTRY, 2020-2028 (USD MILLION)

- TABLE 56 ASIA PACIFIC: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- TABLE 57 ASIA PACIFIC: ROBOTIC RADIOTHERAPY MARKET, BY TECHNOLOGY, 2020-2028 (USD MILLION)

- TABLE 58 ASIA PACIFIC: ROBOTIC RADIOTHERAPY MARKET, BY APPLICATION, 2020-2028 (USD MILLION)

- TABLE 59 ASIA PACIFIC: ROBOTIC RADIOTHERAPY MARKET, BY END USER, 2020-2028 (USD MILLION)

- 10.4.2 JAPAN

- 10.4.2.1 Rising geriatric population and surgical procedures to drive market

- TABLE 60 JAPAN: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.4.3 CHINA

- 10.4.3.1 Developing healthcare infrastructure to drive market

- TABLE 61 CHINA: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.4.4 INDIA

- 10.4.4.1 Rising awareness and government support to boost growth

- TABLE 62 INDIA: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.4.5 AUSTRALIA

- 10.4.5.1 Well-established healthcare system to favor adoption

- TABLE 63 AUSTRALIA: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.4.6 SOUTH KOREA

- 10.4.6.1 Growing target patient population to drive market

- TABLE 64 SOUTH KOREA: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.4.7 REST OF ASIA PACIFIC

- TABLE 65 REST OF ASIA PACIFIC: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- 10.5 REST OF THE WORLD

- 10.5.1 REST OF THE WORLD: RECESSION IMPACT

- TABLE 66 REST OF THE WORLD: ROBOTIC RADIOTHERAPY MARKET, BY PRODUCT, 2020-2028 (USD MILLION)

- TABLE 67 REST OF THE WORLD: ROBOTIC RADIOTHERAPY MARKET, BY TECHNOLOGY, 2020-2028 (USD MILLION)

- TABLE 68 REST OF THE WORLD: ROBOTIC RADIOTHERAPY MARKET, BY APPLICATION, 2020-2028 (USD MILLION)

- TABLE 69 REST OF THE WORLD: ROBOTIC RADIOTHERAPY MARKET, BY END USER, 2020-2028 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES

- FIGURE 26 KEY DEVELOPMENTS IN ROBOTIC RADIOTHERAPY MARKET (2019 TO 2023)

- 11.3 REVENUE ANALYSIS

- FIGURE 27 REVENUE ANALYSIS OF TOP FIVE PLAYERS (2019-2022)

- 11.4 MARKET SHARE ANALYSIS: ROBOTIC RADIOTHERAPY MARKET, BY KEY PLAYER (2022)

- FIGURE 28 ROBOTIC RADIOTHERAPY MARKET SHARE, BY KEY PLAYER, 2022

- TABLE 70 ROBOTIC RADIOTHERAPY MARKET: DEGREE OF COMPETITION

- 11.5 COMPANY EVALUATION MATRIX (2022)

- 11.5.1 STARS

- 11.5.2 PERVASIVE PLAYERS

- 11.5.3 EMERGING LEADERS

- 11.5.4 PARTICIPANTS

- FIGURE 29 ROBOTIC RADIOTHERAPY MARKET: COMPANY EVALUATION MATRIX, 2022

- 11.6 COMPANY EVALUATION MATRIX FOR START-UPS/SMES (2022)

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 DYNAMIC COMPANIES

- 11.6.3 RESPONSIVE COMPANIES

- 11.6.4 STARTING BLOCKS

- FIGURE 30 COMPANY EVALUATION MATRIX FOR START-UPS/SMES, 2022

- 11.7 COMPETITIVE BENCHMARKING

- 11.7.1 OVERALL COMPANY FOOTPRINT

- TABLE 71 OVERALL FOOTPRINT ANALYSIS: ROBOTIC RADIOTHERAPY MARKET

- 11.7.2 COMPANY PRODUCT FOOTPRINT

- TABLE 72 PRODUCT FOOTPRINT ANALYSIS: ROBOTIC RADIOTHERAPY MARKET

- 11.7.3 COMPANY REGIONAL FOOTPRINT

- TABLE 73 REGIONAL FOOTPRINT ANALYSIS: ROBOTIC RADIOTHERAPY MARKET

- 11.8 COMPETITIVE SCENARIO (2019-2023)

- 11.8.1 PRODUCT LAUNCHES & APPROVALS

- 11.8.2 DEALS

- 11.8.3 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- (Business Overview, Products/Services/Solutions Offered, Recent Developments, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats)**

- 12.1.1 SIEMENS HEALTHINEERS AG (VARIAN MEDICAL SYSTEMS, INC.)

- TABLE 74 SIEMENS HEALTHINEERS AG: COMPANY OVERVIEW

- FIGURE 31 SIEMENS HEALTHINEERS AG: COMPANY SNAPSHOT (2022)

- 12.1.2 ELEKTA

- TABLE 75 ELEKTA: COMPANY OVERVIEW

- FIGURE 32 ELEKTA: COMPANY SNAPSHOT (2022)

- 12.1.3 ACCURAY INCORPORATED

- TABLE 76 ACCURAY INCORPORATED: COMPANY OVERVIEW

- FIGURE 33 ACCURAY INCORPORATED: COMPANY SNAPSHOT (2022)

- 12.1.4 VIEWRAY TECHNOLOGIES, INC.

- TABLE 77 VIEWRAY TECHNOLOGIES, INC.: COMPANY OVERVIEW

- FIGURE 34 VIEWRAY TECHNOLOGIES, INC.: COMPANY SNAPSHOT (2022)

- 12.1.5 C-RAD

- TABLE 78 C-RAD: COMPANY OVERVIEW

- FIGURE 35 C-RAD: COMPANY SNAPSHOT (2022)

- 12.1.6 IBA

- TABLE 79 IBA: COMPANY OVERVIEW

- FIGURE 36 IBA: COMPANY SNAPSHOT (2022)

- 12.1.7 HITACHI LTD.

- TABLE 80 HITACHI LTD.: COMPANY OVERVIEW

- FIGURE 37 HITACHI LTD.: COMPANY SNAPSHOT (2021)

- 12.1.8 MEVION MEDICAL SYSTEMS

- TABLE 81 MEVION MEDICAL SYSTEMS: COMPANY OVERVIEW

- 12.1.9 PANACEA MEDICAL TECHNOLOGIES PVT. LTD.

- TABLE 82 PANACEA MEDICAL TECHNOLOGIES PVT. LTD.: COMPANY OVERVIEW

- 12.1.10 P-CURE

- TABLE 83 P-CURE: COMPANY OVERVIEW

- 12.1.11 PROVISION HEALTHCARE

- TABLE 84 PROVISION HEALTHCARE: COMPANY OVERVIEW

- 12.1.12 SUMITOMO HEAVY INDUSTRY LTD.

- TABLE 85 SUMITOMO HEAVY INDUSTRY LTD.: COMPANY OVERVIEW

- FIGURE 38 SUMITOMO HEAVY INDUSTRIES: COMPANY SNAPSHOT (2021)

- 12.1.13 PHILIPS HEALTHCARE

- TABLE 86 PHILIPS HEALTHCARE: COMPANY OVERVIEW

- FIGURE 39 PHILIPS HEALTHCARE: COMPANY SNAPSHOT (2022)

- 12.1.14 RAYSEARCH LABORATORIES

- TABLE 87 RAYSEARCH LABORATORIES: COMPANY OVERVIEW

- FIGURE 40 RAYSEARCH LABORATORIES: COMPANY SNAPSHOT (2022)

- 12.1.15 PROTOM INTERNATIONAL, INC.

- TABLE 88 PROTOM INTERNATIONAL, INC.: COMPANY OVERVIEW

- 12.1.16 OPTIVUS PROTON THERAPY, INC.

- TABLE 89 OPTIVUS PROTON THERAPY, INC.: COMPANY OVERVIEW

- 12.1.17 TOSHIBA CORPORATION

- TABLE 90 TOSHIBA CORPORATION: COMPANY OVERVIEW

- FIGURE 41 TOSHIBA CORPORATION: COMPANY SNAPSHOT (2022)

- 12.1.18 VISION RT LTD.

- TABLE 91 VISION RT LTD.: COMPANY OVERVIEW

- 12.1.19 ADVANCED ONCOTHERAPY PLC

- TABLE 92 ADVANCED ONCOTHERAPY PLC: COMPANY OVERVIEW

- 12.1.20 MIM SOFTWARE INC.

- TABLE 93 MIM SOFTWARE INC.: COMPANY OVERVIEW

- *Business Overview, Products/Services/Solutions Offered, Recent Developments, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats might not be captured in case of unlisted companies.

- 12.2 OTHER PLAYERS

- 12.2.1 STANDARD IMAGING, INC.

- 12.2.2 BRAINLAB AG

- 12.2.3 MAGNETTX ONCOLOGY SOLUTIONS LTD.

- 12.2.4 PTW FREIBURG GMBH

- 12.2.5 DOSISOFT SA

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS