|

|

市場調査レポート

商品コード

1476281

人工木材接着剤の世界市場:樹脂別、技術別、製品別、用途別、地域別 - 2029年までの予測Engineered Wood Adhesives Market by Resin (Melamine Formaldehyde, Phenol Resorcinol Formaldehyde), Product (CLT, OSB, MDF, LVL), Technology (Solvent-Based, Water-Based), Application (Structural, Non-Structural), and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 人工木材接着剤の世界市場:樹脂別、技術別、製品別、用途別、地域別 - 2029年までの予測 |

|

出版日: 2024年05月02日

発行: MarketsandMarkets

ページ情報: 英文 300 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界の人工木材接着剤の市場規模は、CAGR 3.7%で拡大し、2024年の87億米ドルから105億米ドルに成長すると予測されています。

人工木材接着剤は、木材資源の利用を最適化するために不可欠であり、特に大きくて質の良い木の利用可能性が低下しています。木材業界は、より小さな丸太、あまり好ましくない樹種、以前は使えなかった廃材を活用する革新的な人工木材製品を開発することで対応してきました。i-ジョイスト、集成材(グルラム)、LVL、PSL、LSL、OSLなどの様々な形態の構造用複合材を含むこれらの製品は、無垢の製材の構造特性を模倣するように設計されているが、製造中に自然の欠点が取り除かれるため、構造特性はより均一になっています。これらの近代的な人工木材製品は、建築用ドア、窓、フレームから、合板、パーティクルボード、中密度繊維板(MDF)、配向性ストランドボード(OSB)など、より一般的な部材まで、幅広い建築用途に不可欠です。これらの製品に接着剤を使用することで、木材の効率的な利用が促進されるだけでなく、耐火性など最終製品の性能特性も向上します。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 検討単位 | 金額(100万米ドル/10億米ドル) |

| セグメント別 | 樹脂別、技術別、製品別、用途別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋地域、その他の地域 |

水性接着剤は、特に環境規制が強化される中で、望ましい代替品として台頭してきています。これらの接着剤は水を溶剤として使用するため、VOC排出量が大幅に削減されます。主な利点としては、より安全な作業環境と環境への影響の低減が挙げられます。しかし、水系接着剤の性能は、一般に、耐水性や温度変化下での接着強度の点で溶剤系に劣る。この性能差を埋めるため、化学配合の改良が進められています。

建設業界では、合板、クロスラミネート・ティンバー(CLT)、ラミネート・ベニア・ランバー(LVL)、オリエンテッド・ストランド・ボード(OSB)などの人工木材製品の戦略的利用が、その強化された機械的特性、環境持続可能性、費用対効果により極めて重要です。これらの製品はそれぞれ、構造上の明確な役割を果たし、特定の性能基準を満たすように設計されているため、現代の建築には欠かせないものとなっています。

合板は、木材単板を積層し、断面を接着することで製造されます。この構成により、合板は卓越した強度と反りに対する抵抗力を持ち、床材、屋根材、壁下地など幅広い用途に適しています。木目全体に荷重を均等に分散させることができるため、厳しい環境でも信頼できる選択肢となります。

アジア太平洋の人工木材接着剤市場は、予測期間中に数量ベースで最も高いシェアを獲得すると予測されます。

当レポートでは、世界の人工木材接着剤市場について調査し、樹脂別、技術別、製品別、用途別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 現代の木製品に使用される接着剤の種類

- エンジニアリング人工木材接着剤プロジェクト

- 主要新興国対EU27か国および米国

- 市場力学

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- マクロ経済指標

- サプライチェーン分析

- 価格分析

- 貿易分析

- 規制状況と基準

- エコシステム/市場マップ

- 顧客ビジネスに影響を与える動向と混乱

- 投資と資金調達のシナリオ

- 特許分析

- 技術分析

- 市場の成長に影響を与える世界経済のシナリオ

- ケーススタディ分析

- 主な会議とイベント

第6章 人工木材接着剤市場、樹脂別

- イントロダクション

- メラミンホルムアルデヒド

- フェノールレゾルシノールホルムアルデヒド

- ポリウレタン

- その他

第7章 人工木材接着剤市場、製品別

- イントロダクション

第8章 人工木材接着剤市場、技術別

- イントロダクション

- 溶剤型

- 水性

- 非溶剤型

- 反応型

第9章 人工木材接着剤市場、用途別

- イントロダクション

- 構造

- 非構造

第10章 人工木材接着剤市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- その他の地域

第11章 競合情勢

- 主要参入企業の戦略

- 市場シェア分析

- 参入企業主要5社の収益分析

- 企業評価と財務指標、2023年

- ブランド/製品比較分析

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオと動向

第12章 企業プロファイル

- 主要参入企業

- H.B. FULLER COMPANY

- HENKEL AG & CO. KGAA

- AKZO NOBEL N.V.

- ARKEMA SA

- BASF SE(JANUARY 2018-DECEMBER 2023)

- DOW

- HUNTSMAN CORPORATION

- AICA KOGYO CO., LTD.

- ASTRAL LIMITED

- HEXION

- CHEMIQUE ADHESIVES & SEALANTS LTD.

- BOLTON GROUP

- WINLONG GW INTERNATIONAL TECHNOLOGY(QINGDAO)CO., LTD.

- SUPER BOND ADHESIVE PVT. LTD.

- JOWAT SE

- MAPEI CORPORATION

- SURFACTANT INDUSTRIES

- ARCLIN, INC.

- AKKIM SEALANTS & ADHESIVES

- IFS INDUSTRIES INC.

- KIILTO

- TREMCO

- NAPCO

- DYNEA

- ROBATECH AG

第13章 隣接市場と関連市場

第14章 付録

The global engineered wood adhesives market size is projected to grow from USD 8.7 billion in 2024 to USD 10.5 billion, at a CAGR of 3.7%. Wood adhesives are essential for optimizing the use of timber resources, especially as the availability of large, quality trees decline. The wood industry has responded by developing innovative engineered wood products that leverage smaller logs, less desirable wood species, and previously unusable wood waste. These products, which include I-joists, glued laminated timber (glulam), and various forms of structural composite lumber such as LVL, PSL, LSL, and OSL, are designed to emulate the structural characteristics of solid-sawn lumber but with greater uniformity in their structural properties due to the removal of natural defects during manufacturing. These modern engineered wood products are integral to a wide range of construction applications, from architectural doors, windows, and frames to more ubiquitous elements like plywood, particleboard, medium-density fiberboard (MDF), and oriented strand board (OSB). The use of adhesives in these products not only facilitates the efficient use of wood but also enhances the performance characteristics of the final products, including their fire resistance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By Resin, By Technology, By Product, By Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, and Rest of the World |

The water-based segment is expected to register one of the highest market share during the forecast period

Water-based adhesives are emerging as a preferable alternative, especially under tighter environmental regulations. These adhesives use water as a solvent, which significantly reduces VOC emissions. The primary advantages include safer working conditions and lower environmental impact. However, the performance of water-based adhesives generally lags behind solvent-based types in terms of water resistance and bonding strength under variable temperature conditions. Enhancements in chemical formulations are being developed to close this performance gap.

The structural segment is expected to register one of the highest market share during the forecast period

In the construction industry, the strategic utilization of engineered wood products such as plywood, cross-laminated timber (CLT), laminated veneer lumber (LVL), and oriented strand board (OSB) is pivotal due to their enhanced mechanical properties, environmental sustainability, and cost-effectiveness. Each of these products serves distinct structural roles and is engineered to meet specific performance criteria, making them indispensable in modern building practices.

Plywood is crafted through the layering and cross-sectional bonding of wood veneers, utilizing adhesives that enhance its structural integrity. This configuration grants plywood exceptional strength and resistance to warping, making it suitable for a wide range of applications including flooring, roofing, and wall sheathing. Its ability to distribute loads evenly across the grain makes it a reliable choice for demanding environments.

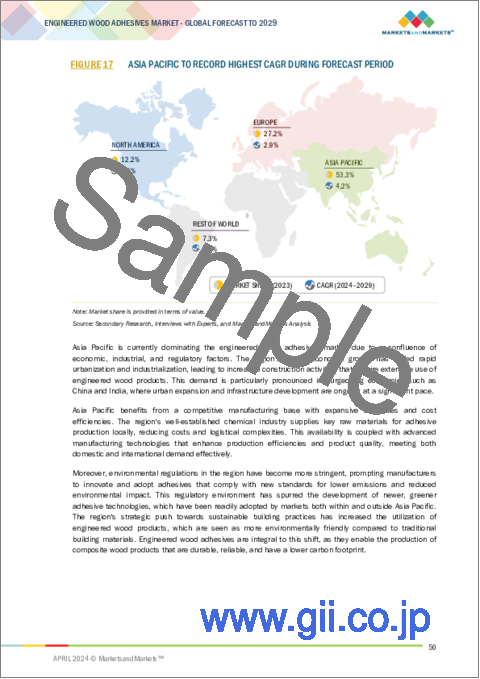

Asia Pacific engineered wood adhesives market is estimated to capture one of the highest share in terms of volume during the forecast period

The Asia Pacific region stands out as both the largest and fastest-growing market, driven by robust economic growth and significant investments in various end-use industries. The area's prominence is further reinforced by the strategic initiatives of global industry leaders who are establishing production facilities, opening sales offices, and expanding distribution networks within the region. These strategic decisions reflect the sustained demand in the region and aim to capitalize on its cost-effective production capabilities and dynamic market conditions to enhance profit margins.

Despite this positive outlook, the market faces several challenges that could impact its growth trajectory. Economic fluctuations, the instability of raw material costs, and intense competition among local players are significant obstacles that could hinder progress. Nevertheless, the rigorous enforcement of regulatory standards across the region highlights the industry's commitment to quality and compliance with biocompatibility standards, ensuring that products meet the highest safety and performance criteria. This rigorous approach to regulation not only maintains product integrity but also supports sustainable market growth amidst these challenges.

The break-up of the profile of primary participants in the engineered wood adhesives market:

- By Company Type: Tier 1 - 46%, Tier 2 - 36%, and Tier 3 - 18%

- By Designation: C Level - 21%, D Level - 23%, and Others - 56%

- By Region: North America - 37%, Europe - 23%, Asia Pacific- 26%, and Rest of the World- 14%

The key companies profiled in this report are H.B. Fuller Company (US), Henkel AG & Co., KGaA. (Germany), AkzoNobel N.V. (Netherlands), Arkema SA (France), BASF SE (Germany), Dow (US), Huntsman Corporation (US), AICA Kogyo Co., Ltd (Japan), Astral Limited (India), Hexion (US), and others.

Research Coverage:

The engineered wood adhesives market is segmented by Resin (Melamine Formaldehyde, Phenol Resorcinol Formaldehyde, Polyurethane, and Others), Product (Cross-Laminated Timber, Laminated Veneer Lumber, Oriented Strand Board, Glulam, Plywood, Medium Density Fiberboard, and Others), Technology (Solvent-Based, Water-Based, Solvent-Less, and Reactive), Application (Structural, and Non-Residential), and Region (North America, Europe, Asia Pacific, and Rest of the World). The study's coverage covers detailed information on the key factors influencing the growth of the engineered wood adhesives market, such as drivers, constraints, challenges, and opportunities. A thorough examination of the top industry players was carried out in order to provide insights into their company overview, solutions, and services; essential strategies; contracts, partnerships, and agreements. This includes coverage of new product and service launches, mergers and acquisitions, and ongoing developments in the engineered wood adhesives market. A competitive analysis of emerging companies in the engineered wood adhesives business ecosystem is included in this study. Reasons to buy this report: The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall engineered wood adhesives market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing demand for engineered wood adhesives in sustainable infrastructure where engineered wood is required), restraints (volatility in raw material prices), opportunities (collaboration of distributors in untapped markets), and challenges (stringent regulatory policies).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the engineered wood adhesives market

- Market Development: Comprehensive information about lucrative markets - the report analyses the engineered wood adhesives market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the engineered wood adhesives market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like H.B. Fuller Company (US), Henkel AG & Co., KGaA. (Germany), AkzoNobel N.V. (Netherlands), Arkema SA (France), BASF SE (Germany), Dow (US), Huntsman Corporation (US), AICA Kogyo Co., Ltd (Japan), Astral Limited (India), and Hexion (US). The report also helps stakeholders understand the pulse of the engineered wood adhesives market and provides them information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.2.2 DEFINITION AND INCLUSIONS, BY RESIN TYPE

- 1.2.3 DEFINITION AND INCLUSIONS, BY PRODUCT

- 1.2.4 DEFINITION AND INCLUSIONS, BY TECHNOLOGY

- 1.2.5 DEFINITION AND INCLUSIONS, BY APPLICATION

- 1.3 MARKET SCOPE

- FIGURE 1 ENGINEERED WOOD ADHESIVES MARKET SEGMENTATION

- 1.3.1 REGIONS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATE, 2019-2022

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 ENGINEERED WOOD ADHESIVES MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of interviews with experts

- FIGURE 3 BREAKDOWN OF INTERVIEWS WITH EXPERTS

- 2.1.2.3 Primary data sources

- 2.1.2.4 Key industry insights

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 6 ENGINEERED WOOD ADHESIVES MARKET ESTIMATION, BY RESIN TYPE

- FIGURE 7 ENGINEERED WOOD ADHESIVES MARKET SIZE ESTIMATION, BY REGION

- 2.3 MARKET FORECAST APPROACH

- 2.3.1 SUPPLY-SIDE FORECAST

- FIGURE 8 ENGINEERED WOOD ADHESIVES MARKET: SUPPLY-SIDE FORECAST

- 2.3.2 DEMAND-SIDE FORECAST

- FIGURE 9 ENGINEERED WOOD ADHESIVES MARKET: DEMAND-SIDE FORECAST

- FIGURE 10 METHODOLOGY FOR SUPPLY-SIDE SIZING OF ENGINEERED WOOD ADHESIVES MARKET

- 2.4 FACTOR ANALYSIS

- FIGURE 11 MAJOR FACTORS RESPONSIBLE FOR GLOBAL RECESSION AND THEIR IMPACT ON MARKET

- 2.5 DATA TRIANGULATION

- FIGURE 12 ENGINEERED WOOD ADHESIVES MARKET: DATA TRIANGULATION

- 2.6 ASSUMPTIONS

- 2.7 LIMITATIONS

- 2.8 GROWTH FORECAST

- 2.9 RISK ASSESSMENT

- TABLE 2 ENGINEERED WOOD ADHESIVES MARKET: RISK ASSESSMENT

- 2.10 RECESSION IMPACT ANALYSIS

3 EXECUTIVE SUMMARY

- TABLE 3 ENGINEERED WOOD ADHESIVES MARKET SNAPSHOT (2024 VS. 2029)

- FIGURE 13 MELAMINE FORMALDEHYDE TO BE LARGEST RESIN SEGMENT IN ENGINEERED WOOD ADHESIVES MARKET

- FIGURE 14 PLYWOOD TO DOMINATE OVERALL MARKET DURING FORECAST PERIOD

- FIGURE 15 MEDIUM DENSITY FIBERBOARD TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 16 NON-STRUCTURAL APPLICATION TO ACCOUNT FOR LARGER SHARE OF ENGINEERED WOOD ADHESIVES MARKET

- FIGURE 17 ASIA PACIFIC TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ENGINEERED WOOD ADHESIVES MARKET

- FIGURE 18 EMERGING ECONOMIES TO OFFER LUCRATIVE GROWTH OPPORTUNITIES FOR MARKET PLAYERS

- 4.2 ENGINEERED WOOD ADHESIVES MARKET, BY RESIN

- FIGURE 19 MELAMINE FORMALDEHYDE SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.3 ENGINEERED WOOD ADHESIVES MARKET IN ASIA PACIFIC, BY RESIN TYPE AND COUNTRY

- FIGURE 20 CHINA ACCOUNTED FOR LARGEST SHARE OF ENGINEERED WOOD ADHESIVES MARKET IN ASIA PACIFIC

- 4.4 ENGINEERED WOOD ADHESIVES MARKET, DEVELOPED VS. EMERGING ECONOMIES

- FIGURE 21 EMERGING COUNTRIES TO REGISTER HIGHER GROWTH DURING FORECAST PERIOD

- 4.5 ENGINEERED WOOD ADHESIVES MARKET, BY KEY COUNTRIES

- FIGURE 22 INDIA TO RECORD HIGHEST GROWTH DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 TYPES OF ADHESIVES USED IN MODERN WOOD PRODUCTS

- 5.3 ENGINEERED WOOD ADHESIVE PROJECTS

- 5.4 KEY EMERGING ECONOMIES VS. EU27 AND US

- FIGURE 23 AVERAGE CHEMICAL PRODUCTION GROWTH PER ANNUM (2011-2021)

- 5.5 MARKET DYNAMICS

- FIGURE 24 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN ENGINEERED WOOD ADHESIVES MARKET

- 5.5.1 DRIVERS

- 5.5.1.1 Growth of building & construction industry in emerging economies

- 5.5.1.2 Increasing urban population

- 5.5.1.3 Rising demand in North America

- 5.5.1.4 Capacity expansion to cater to increasing demand

- 5.5.2 RESTRAINTS

- 5.5.2.1 Volatility in raw material prices

- 5.5.3 OPPORTUNITIES

- 5.5.3.1 Establishing authenticity through various certifications

- 5.5.3.2 Rising demand for sustainable infrastructure

- 5.5.4 CHALLENGES

- 5.5.4.1 Shifting rules and changing standards

- 5.6 PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 ENGINEERED WOOD ADHESIVES MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 25 PORTER'S FIVE FORCES ANALYSIS: ENGINEERED WOOD ADHESIVES MARKET

- 5.6.1 THREAT FROM NEW ENTRANTS

- 5.6.2 THREAT OF SUBSTITUTES

- 5.6.3 BARGAINING POWER OF BUYERS

- 5.6.4 BARGAINING POWER OF SUPPLIERS

- 5.6.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.7 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.7.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- TABLE 5 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP APPLICATIONS (%)

- 5.7.2 BUYING CRITERIA

- FIGURE 27 KEY BUYING CRITERIA FOR ENGINEERED WOOD ADHESIVES

- TABLE 6 KEY BUYING CRITERIA FOR ENGINEERED WOOD ADHESIVES

- 5.8 MACROECONOMIC INDICATORS

- 5.8.1 INTRODUCTION

- 5.8.2 GDP TRENDS AND FORECAST

- TABLE 7 GDP TRENDS AND FORECAST, PERCENTAGE CHANGE (2020-2027)

- 5.8.3 TRENDS IN GLOBAL CONSTRUCTION INDUSTRY

- 5.9 SUPPLY CHAIN ANALYSIS

- FIGURE 28 ENGINEERED WOOD ADHESIVES MARKET: SUPPLY CHAIN ANALYSIS

- 5.10 PRICING ANALYSIS

- 5.10.1 AVERAGE SELLING PRICE TREND, BY REGION

- FIGURE 29 AVERAGE SELLING PRICE TREND OF ENGINEERED WOOD ADHESIVES, BY REGION, 2021-2024

- TABLE 8 AVERAGE SELLING PRICE OF ENGINEERED WOOD ADHESIVES, BY REGION, 2022-2023 (USD/KG)

- 5.10.2 AVERAGE SELLING PRICE TREND, BY RESIN TYPE

- FIGURE 30 AVERAGE SELLING PRICE TREND OF ENGINEERED WOOD ADHESIVES, BY RESIN TYPE (2023)

- 5.10.3 AVERAGE SELLING PRICE TREND, BY STRUCTURAL PRODUCT

- FIGURE 31 AVERAGE SELLING PRICE TREND OF ENGINEERED WOOD ADHESIVES, BY STRUCTURAL PRODUCT (2023)

- 5.10.4 AVERAGE SELLING PRICE TREND, BY NON-STRUCTURAL PRODUCT

- FIGURE 32 AVERAGE SELLING PRICE TREND OF ENGINEERED WOOD ADHESIVES, BY NON-STRUCTURAL PRODUCT (2023)

- 5.10.5 AVERAGE SELLING PRICE TREND, BY APPLICATION

- FIGURE 33 AVERAGE SELLING PRICE TREND OF ENGINEERED WOOD ADHESIVES, BY APPLICATION (2023)

- 5.10.6 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- FIGURE 34 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- TABLE 9 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TOP APPLICATIONS, 2023 (USD/KG)

- 5.11 TRADE ANALYSIS

- 5.11.1 EXPORT SCENARIO

- FIGURE 35 REGION-WISE EXPORT DATA, 2019-2023 (USD THOUSAND)

- TABLE 10 COUNTRY-WISE EXPORT DATA, 2021-2023 (USD THOUSAND)

- 5.11.2 IMPORT SCENARIO

- FIGURE 36 REGION-WISE IMPORT DATA, 2019-2023 (USD THOUSAND)

- TABLE 11 COUNTRY-WISE IMPORT DATA, 2021-2023 (USD THOUSAND)

- 5.12 REGULATORY LANDSCAPE AND STANDARDS

- 5.12.1 REGULATIONS IMPACTING ENGINEERED WOOD ADHESIVES BUSINESS

- TABLE 12 EMISSION LIMITS FOR ENGINEERED WOOD PRODUCTS

- 5.12.1.1 Frequent questions asked

- 5.12.2 WOOD MANUFACTURING REGULATIONS

- 5.12.3 ENVIRONMENTAL REGULATIONS FOR WOOD MANUFACTURING

- 5.12.3.1 Clean Air Act

- 5.12.3.2 Clean Water Act

- 5.12.3.3 Toxic Substances Control Act (TSCA)

- 5.12.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13 ECOSYSTEM/MARKET MAP

- TABLE 16 ENGINEERED WOOD ADHESIVES MARKET: ROLE IN ECOSYSTEM

- FIGURE 37 ENGINEERED WOOD ADHESIVES MARKET: ECOSYSTEM MAPPING

- FIGURE 38 ENGINEERED WOOD ADHESIVES: ECOSYSTEM ANALYSIS

- 5.14 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 39 TRENDS IN END-USE INDUSTRIES IMPACTING BUSINESS OF ENGINEERED WOOD ADHESIVE MANUFACTURERS

- 5.15 INVESTMENT AND FUNDING SCENARIO

- TABLE 17 INVESTMENT AND FUNDING SCENARIO

- 5.16 PATENT ANALYSIS

- 5.16.1 METHODOLOGY

- 5.16.2 PUBLICATION TRENDS

- FIGURE 40 PUBLISHED PATENTS, 2019-2023

- 5.16.3 JURISDICTION ANALYSIS

- FIGURE 41 PATENTS PUBLISHED BY JURISDICTION, 2019-2023

- 5.16.4 TOP APPLICANTS

- FIGURE 42 PATENTS PUBLISHED BY MAJOR APPLICANTS, 2019-2023

- TABLE 18 TOP PATENT OWNERS

- FIGURE 43 TOP PATENT APPLICANTS

- 5.17 TECHNOLOGY ANALYSIS

- 5.17.1 KEY TECHNOLOGIES

- 5.17.1.1 Melamine formaldehyde

- 5.17.1.2 Phenol resorcinol formaldehyde

- 5.17.2 COMPLIMENTARY TECHNOLOGIES

- 5.17.2.1 Polyurethane

- 5.17.3 ADJACENT TECHNOLOGIES

- 5.17.3.1 Dowel-laminated timber

- 5.17.3.2 Mechanical fasteners

- 5.17.1 KEY TECHNOLOGIES

- 5.18 GLOBAL ECONOMIC SCENARIO AFFECTING MARKET GROWTH

- 5.18.1 RUSSIA-UKRAINE WAR

- 5.18.2 CHINA

- 5.18.2.1 Decreasing FDI cooling China's growth trajectory

- 5.18.2.2 Environmental commitments

- 5.18.3 EUROPE

- 5.18.3.1 Energy crisis in Europe

- 5.18.4 CHOKEPOINTS THREATENING GLOBAL TRADE

- 5.18.5 OUTLOOK FOR CHEMICAL INDUSTRY

- 5.19 CASE STUDY ANALYSIS

- 5.19.1 CASE STUDY 1

- 5.19.2 CASE STUDY 2

- 5.19.3 CASE STUDY 3

- 5.20 KEY CONFERENCES AND EVENTS

- TABLE 19 ENGINEERED WOOD ADHESIVES MARKET: KEY CONFERENCES AND EVENTS, 2024-2025

6 ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE

- 6.1 INTRODUCTION

- FIGURE 44 MELAMINE FORMALDEHYDE TO ACCOUNT FOR LARGEST SHARE OF ENGINEERED WOOD ADHESIVES MARKET

- TABLE 20 ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (USD MILLION)

- TABLE 21 ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (KILOTON)

- 6.2 MELAMINE FORMALDEHYDE

- 6.2.1 UREA

- 6.2.1.1 Superior bond and cost-effectiveness boosting demand

- 6.2.2 MELAMINE UREA FORMALDEHYDE

- 6.2.2.1 High performance and cost-efficiency to boost demand

- TABLE 22 MELAMINE FORMALDEHYDE: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 23 MELAMINE FORMALDEHYDE: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- 6.2.1 UREA

- 6.3 PHENOL RESORCINOL FORMALDEHYDE

- 6.3.1 ENHANCED DURABILITY AND STABILITY TO DRIVE DEMAND

- TABLE 24 PHENOL RESORCINOL FORMALDEHYDE: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 25 PHENOL RESORCINOL FORMALDEHYDE: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- 6.4 POLYURETHANE

- 6.4.1 ROBUST FLEXIBILITY AND EXCELLENT MOISTURE RESISTANCE TO FUEL DEMAND

- TABLE 26 POLYURETHANE: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 27 POLYURETHANE: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- 6.5 OTHER RESIN TYPES

- TABLE 28 OTHER RESIN TYPES: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 29 OTHER RESIN TYPES: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

7 ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT

- 7.1 INTRODUCTION

- FIGURE 45 PLYWOOD TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 46 MEDIUM DENSITY FIBERBOARD TO LEAD MARKET IN NON-STRUCTURAL PRODUCT SEGMENT

- TABLE 30 ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 31 ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 32 ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 33 ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (KILOTON)

- 7.1.1 STRUCTURAL

- 7.1.1.1 Plywood

- 7.1.1.1.1 Prominent usage in multiple construction activities to fuel demand

- 7.1.1.2 Oriented strand board

- 7.1.1.2.1 Versatile properties suitable for structural applications to drive market

- 7.1.1.3 Other structural products

- 7.1.1.3.1 Cross-laminated timber

- 7.1.1.3.2 Glulam

- 7.1.1.3.3 Laminated veneer lumber

- 7.1.1.1 Plywood

- TABLE 34 PLYWOOD: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 35 PLYWOOD: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- TABLE 36 ORIENTED STRAND BOARD: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 37 ORIENTED STRAND BOARD: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- TABLE 38 OTHER STRUCTURAL PRODUCTS: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 39 OTHER STRUCTURAL PRODUCTS: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- 7.1.2 NON-STRUCTURAL

- 7.1.2.1 Medium density fiberboard

- 7.1.2.1.1 Structural stability and strength to drive demand

- 7.1.2.2 Particle board

- 7.1.2.2.1 Furniture and construction industries to drive market

- 7.1.2.1 Medium density fiberboard

- 7.1.3 OTHERS

- TABLE 40 MEDIUM DENSITY FIBERBOARD: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 41 MEDIUM DENSITY FIBERBOARD: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- TABLE 42 PARTICLE BOARD: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 43 PARTICLE BOARD: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- TABLE 44 OTHER NON-STRUCTURAL PRODUCTS: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 45 OTHER NON-STRUCTURAL PRODUCTS: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

8 ENGINEERED WOOD ADHESIVES MARKET, BY TECHNOLOGY

- 8.1 INTRODUCTION

- 8.2 SOLVENT-BASED

- 8.2.1 ROBUST PERFORMANCE AND HIGH STRENGTH TO DRIVE DEMAND

- 8.3 WATER-BASED

- 8.3.1 EMERGING ECONOMIES TO FUEL DEMAND FOR WATER-BASED ADHESIVES

- 8.4 SOLVENT-LESS

- 8.4.1 GROWING DEMAND FROM CONSTRUCTION SECTOR TO DRIVE MARKET

- 8.5 REACTIVE TECHNOLOGY

- 8.5.1 EPOXY

- 8.5.1.1 Resistant to moisture and UV light to fuel demand

- 8.5.2 POLYURETHANE

- 8.5.2.1 High durability and structural integrity to support market growth

- 8.5.3 CYANOACRYLATE

- 8.5.3.1 Minimal clamp time and durable adhesive to drive demand

- 8.5.4 POLYISOCYANATE

- 8.5.4.1 Structural integrity and longevity to drive market

- 8.5.1 EPOXY

9 ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- FIGURE 47 NON-STRUCTURAL SEGMENT TO DOMINATE OVERALL ENGINEERED WOOD ADHESIVES MARKET

- TABLE 46 ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 47 ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 9.2 STRUCTURAL

- 9.2.1 STRUCTURAL APPLICATION TO REGISTER HIGH GROWTH RATE DURING FORECAST PERIOD

- TABLE 48 STRUCTURAL: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 49 STRUCTURAL: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- 9.3 NON-STRUCTURAL

- 9.3.1 AESTHETIC ADAPTABILITY AND COST-EFFECTIVENESS DRIVING DEMAND IN NON-STRUCTURAL APPLICATIONS

- TABLE 50 NON-NSTRUCTURAL: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 51 NON-STRUCTURAL: ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

10 ENGINEERED WOOD ADHESIVES MARKET, BY REGION

- 10.1 INTRODUCTION

- TABLE 52 GLOBAL CONSTRUCTION OUTLOOK

- FIGURE 48 SHARE OF BUILDINGS IN TOTAL FINAL ENERGY CONSUMPTION IN 2022

- FIGURE 49 SHARE OF BUILDINGS IN TOTAL FINAL ENERGY CONSUMPTION IN 2022

- FIGURE 50 ASIA PACIFIC TO REGISTER HIGHEST CAGR FOR ENGINEERED WOOD ADHESIVES BETWEEN 2024 AND 2029

- TABLE 53 ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (USD MILLION)

- TABLE 54 ENGINEERED WOOD ADHESIVES MARKET, BY REGION, 2021-2029 (KILOTON)

- 10.2 NORTH AMERICA

- TABLE 55 NORTH AMERICA: SUMMARY TABLE OF MARKET FORECASTS FOR 2023 AND 2024

- 10.2.1 RECESSION IMPACT

- FIGURE 51 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET SNAPSHOT

- TABLE 56 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- TABLE 57 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY COUNTRY, 2021-2029 (KILOTON)

- TABLE 58 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (USD MILLION)

- TABLE 59 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (KILOTON)

- TABLE 60 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 61 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 62 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 63 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 64 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 65 NORTH AMERICA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.2.2 US

- 10.2.2.1 Presence of major manufacturers to drive market

- TABLE 66 US: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 67 US: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.2.3 CANADA

- 10.2.3.1 Residential construction to drive market

- TABLE 68 CANADA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 69 CANADA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.2.4 MEXICO

- 10.2.4.1 Investments in infrastructure, energy, and commercial construction projects to drive market

- TABLE 70 MEXICO: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 71 MEXICO: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3 EUROPE

- 10.3.1 RECESSION IMPACT

- FIGURE 52 EUROPE: ENGINEERED WOOD ADHESIVES MARKET SNAPSHOT

- TABLE 72 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- TABLE 73 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY COUNTRY 2021-2029 (KILOTON)

- TABLE 74 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (USD MILLION)

- TABLE 75 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (KILOTON)

- TABLE 76 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 77 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 78 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 79 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 80 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 81 EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.2 GERMANY

- 10.3.2.1 Infrastructure enhancement and high for commercial projects upthrust the demand

- TABLE 82 GERMANY: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 83 GERMANY: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.3 AUSTRIA

- 10.3.3.1 Resurgence of wooden commercial projects to drive demand

- TABLE 84 AUSTRIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 85 AUSTRIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.4 SWITZERLAND

- 10.3.4.1 High R&D investments and economic growth propelling demand

- TABLE 86 CONSTRUCTION AND HOUSING KEY FIGURES

- TABLE 87 SWITZERLAND: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 88 SWITZERLAND: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.5 ITALY

- 10.3.5.1 High disposable income and rising FII investments

- TABLE 89 ITALY: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 90 ITALY: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.6 UK

- 10.3.6.1 Growing construction sector to boost demand

- TABLE 91 UK: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 92 UK: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.7 FRANCE

- 10.3.7.1 Population growth to generate demand for residential construction to increase demand

- TABLE 93 FRANCE: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 94 FRANCE: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.8 TURKEY

- 10.3.8.1 Recovery of construction industry to increase demand

- TABLE 95 TURKEY: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 96 TURKEY: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.9 DENMARK

- 10.3.9.1 Strong infrastructure growth to support demand

- TABLE 97 DENMARK: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 98 DENMARK: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.10 NORWAY

- 10.3.10.1 Green building projects and stricter building codes to increase demand

- TABLE 99 NORWAY: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 100 NORWAY: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.11 SWEDEN

- 10.3.11.1 Strategic public-private partnership projects across country to drive market

- TABLE 101 SWEDEN: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 102 SWEDEN: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.12 FINLAND

- 10.3.12.1 Rising residential construction to increase demand

- TABLE 103 FINLAND: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 104 FINLAND: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.13 SLOVAKIA

- 10.3.13.1 Economic recovery and rising investment to stabilize demand

- TABLE 105 SLOVAKIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 106 SLOVAKIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.14 CZECH REPUBLIC

- 10.3.14.1 Moderate growth and residential housing sector recovery hold demand

- TABLE 107 CZECH REPUBLIC: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 108 CZECH REPUBLIC: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.3.15 REST OF EUROPE

- TABLE 109 REST OF EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 110 REST OF EUROPE: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4 ASIA PACIFIC

- 10.4.1 RECESSION IMPACT

- FIGURE 53 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET SNAPSHOT

- TABLE 111 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- TABLE 112 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY COUNTRY 2021-2029 (KILOTON)

- TABLE 113 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (USD MILLION)

- TABLE 114 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (KILOTON)

- TABLE 115 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 116 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 117 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 118 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 119 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 120 ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.2 CHINA

- 10.4.2.1 Significant increase in investments in real estate and non-residential construction to boost market

- TABLE 121 CHINA: TIMBER PRODUCTION BY PROVINCE, 2020-2021

- TABLE 122 CHINA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 123 CHINA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.3 INDIA

- 10.4.3.1 Emerging economy and rising FDI investment to drive market

- TABLE 124 INDIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 125 INDIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.4 JAPAN

- 10.4.4.1 Investments by government in commercial and reconstruction to boost demand

- FIGURE 54 WOOD SUPPLY IN JAPAN (BY COUNTRY)

- TABLE 126 JAPAN: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 127 JAPAN: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.5 SOUTH KOREA

- 10.4.5.1 Significant expenditure on construction projects to increase demand

- TABLE 128 SOUTH KOREA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 129 SOUTH KOREA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.6 INDONESIA

- 10.4.6.1 Rising consumer spending and growing construction industry to boost market

- TABLE 130 INDONESIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 131 INDONESIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.7 THAILAND

- 10.4.7.1 Enhancing tourism, stabilizing private consumption, and boosting public investment to boost market

- TABLE 132 THAILAND: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 133 THAILAND: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.8 MALAYSIA

- 10.4.8.1 Sustaining domestic demand and rising exports to boost market

- TABLE 134 MALAYSIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 135 MALAYSIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.9 AUSTRALIA AND NEW ZEALAND

- 10.4.9.1 Sustainable construction to uphold demand

- TABLE 136 AUSTRALIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 137 AUSTRALIA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.4.10 REST OF ASIA PACIFIC

- TABLE 138 REST OF ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 139 REST OF ASIA PACIFIC: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.5 REST OF THE WORLD

- 10.5.1 RECESSION IMPACT

- FIGURE 55 BRAZIL TO REGISTER HIGHEST CAGR BETWEEN 2024 AND 2029

- TABLE 140 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- TABLE 141 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY COUNTRY, 2021-2029 (KILOTON)

- TABLE 142 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (USD MILLION)

- TABLE 143 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY RESIN TYPE, 2021-2029 (KILOTON)

- TABLE 144 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 145 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 146 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (USD MILLION)

- TABLE 147 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY PRODUCT (NON-STRUCTURAL), 2021-2029 (KILOTON)

- TABLE 148 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 149 REST OF THE WORLD: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.5.2 BRAZIL

- 10.5.2.1 Easy availability of raw materials to propel market growth

- TABLE 150 BRAZIL: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 151 BRAZIL: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.5.3 ARGENTINA

- 10.5.3.1 Increase in population and improved economic conditions to drive demand

- TABLE 152 ARGENTINA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 153 ARGENTINA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.5.4 SOUTH AFRICA

- 10.5.4.1 Growing building projects to increase demand

- TABLE 154 SOUTH AFRICA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 155 SOUTH AFRICA: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

- 10.5.5 OTHER COUNTRIES

- TABLE 156 OTHER COUNTRIES: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 157 OTHER COUNTRIES: ENGINEERED WOOD ADHESIVES MARKET, BY APPLICATION, 2021-2029 (KILOTON)

11 COMPETITIVE LANDSCAPE

- 11.1 KEY PLAYER STRATEGIES

- 11.1.1 BY KEY PLAYERS STRATEGIES/RIGHT TO WIN, (JANUARY 2018 TO DECEMBER 2023)

- TABLE 158 OVERVIEW OF STRATEGIES ADOPTED BY KEY MARKET PLAYERS (JANUARY 2018 TO DECEMBER 2023)

- 11.2 MARKET SHARE ANALYSIS

- FIGURE 56 MARKET SHARE ANALYSIS, 2023

- TABLE 159 ENGINEERED WOOD ADHESIVES MARKET: DEGREE OF COMPETITION

- 11.2.1 MARKET RANKING ANALYSIS

- FIGURE 57 MARKET RANKING ANALYSIS, 2023

- 11.3 TOP 5 PLAYERS' REVENUE ANALYSIS

- FIGURE 58 MARKET REVENUE ANALYSIS OF TOP FIVE PLAYERS

- 11.4 COMPANY VALUATION AND FINANCIAL METRICS, 2023

- 11.4.1 COMPANY VALUATION

- FIGURE 59 COMPANY VALUATION

- 11.4.2 FINANCIAL METRICS

- FIGURE 60 FINANCIAL METRICS

- 11.5 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 11.5.1 BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 61 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 11.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 11.6.1 STARS

- 11.6.2 EMERGING LEADERS

- 11.6.3 PERVASIVE PLAYERS

- 11.6.4 PARTICIPANTS

- FIGURE 62 ENGINEERED WOOD ADHESIVES MARKET: COMPANY EVALUATION MATRIX, KEY PLAYERS, 2023

- FIGURE 63 PRODUCT FOOTPRINT (25 COMPANIES)

- 11.6.5 COMPANY FOOTPRINT: KEY PLAYERS

- TABLE 160 COMPANY FOOTPRINT (25 COMPANIES)

- TABLE 161 REGION FOOTPRINT (25 COMPANIES)

- TABLE 162 APPLICATION FOOTPRINT (25 COMPANIES)

- TABLE 163 RESIN TYPE FOOTPRINT (25 COMPANIES)

- TABLE 164 PRODUCT FOOTPRINT (25 COMPANIES)

- 11.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 RESPONSIVE COMPANIES

- 11.7.3 DYNAMIC COMPANIES

- 11.7.4 STARTING BLOCKS

- FIGURE 64 ENGINEERED WOOD ADHESIVES MARKET: COMPANY EVALUATION MATRIX, STARTUPS/SMES, 2023

- 11.7.5 COMPETITIVE BENCHMARKING

- 11.7.5.1 Detailed list of key startups/SMEs

- TABLE 165 ENGINEERED WOOD ADHESIVES MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- 11.7.5.2 Competitive benchmarking of key startups/SMEs

- TABLE 166 ENGINEERED WOOD ADHESIVES MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS (STARTUPS/SMES)

- 11.8 COMPETITIVE SCENARIO AND TRENDS

- 11.8.1 ENGINEERED WOOD ADHESIVES MARKET: PRODUCT LAUNCHES, JANUARY 2018-DECEMBER 2023

- TABLE 167 ENGINEERED WOOD ADHESIVES MARKET: PRODUCT LAUNCHES, JANUARY 2018-DECEMBER 2023

- 11.8.2 ENGINEERED WOOD ADHESIVES MARKET: DEALS, JANUARY 2018-DECEMBER 2023

- TABLE 168 ENGINEERED WOOD ADHESIVES MARKET: DEALS, JANUARY 2018-DECEMBER 2023

- 11.8.3 ENGINEERED WOOD ADHESIVES MARKET: EXPANSIONS, JANUARY 2018-DECEMBER 2023

- TABLE 169 ENGINEERED WOOD ADHESIVES MARKET: EXPANSIONS, JANUARY 2018-DECEMBER 2023

12 COMPANY PROFILES

(Business overview, Products/Solutions/Services offered, Recent Developments, MnM view, Key strengths, Strategic choices, Weaknesses and competitive threats) **

- 12.1 MAJOR PLAYERS

- 12.1.1 H.B. FULLER COMPANY

- TABLE 170 H.B. FULLER COMPANY: BUSINESS OVERVIEW

- FIGURE 65 H.B. FULLER COMPANY: COMPANY SNAPSHOT

- TABLE 171 H.B. FULLER COMPANY: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 172 H.B. FULLER COMPANY: DEALS, JANUARY 2018-DECEMBER 2023

- TABLE 173 H.B. FULLER COMPANY: EXPANSIONS, JANUARY 2018- DECEMBER 2023

- 12.1.2 HENKEL AG & CO. KGAA

- TABLE 174 HENKEL AG & CO. KGAA: COMPANY OVERVIEW

- FIGURE 66 HENKEL AG & CO. KGAA: COMPANY SNAPSHOT

- TABLE 175 HENKEL AG & CO. KGAA: DEALS, JANUARY 2018-DECEMBER 2023

- TABLE 176 HENKEL AG & CO. KGAA: EXPANSIONS, JANUARY 2018-DECEMBER 2023

- 12.1.3 AKZO NOBEL N.V.

- TABLE 177 AKZO NOBEL N.V.: COMPANY OVERVIEW

- FIGURE 67 AKZO NOBEL N.V.: COMPANY SNAPSHOT

- 12.1.4 ARKEMA SA

- TABLE 178 ARKEMA SA: COMPANY OVERVIEW

- FIGURE 68 ARKEMA SA: COMPANY SNAPSHOT

- TABLE 179 ARKEMA SA: DEALS, JANUARY 2018-DECEMBER 2023

- 12.1.5 BASF SE (JANUARY 2018 - DECEMBER 2023)

- TABLE 180 BASF SE: COMPANY OVERVIEW

- FIGURE 69 BASF SE: COMPANY SNAPSHOT

- TABLE 181 BASF SE: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- TABLE 182 BASF SE: DEALS, JANUARY 2018-DECEMBER 2023

- 12.1.6 DOW

- TABLE 183 DOW: COMPANY OVERVIEW

- FIGURE 70 DOW: COMPANY SNAPSHOT

- 12.1.7 HUNTSMAN CORPORATION

- TABLE 184 HUNTSMAN CORPORATION: COMPANY OVERVIEW

- FIGURE 71 HUNTSMAN CORPORATION: COMPANY SNAPSHOT

- TABLE 185 HUNTSMAN CORPORATION: DEALS, JANUARY 2018-DECEMBER 2023

- 12.1.8 AICA KOGYO CO., LTD.

- TABLE 186 AICA KOGYO CO., LTD.: COMPANY OVERVIEW

- FIGURE 72 AICA KOGYO CO., LTD.: COMPANY SNAPSHOT

- TABLE 187 AICA KOGYO CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.9 ASTRAL LIMITED

- TABLE 188 ASTRAL LIMITED: COMPANY OVERVIEW

- FIGURE 73 ASTRAL LIMITED: COMPANY SNAPSHOT

- TABLE 189 ASTRAL LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.10 HEXION

- TABLE 190 HEXION: COMPANY OVERVIEW

- TABLE 191 HEXION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- 12.1.11 CHEMIQUE ADHESIVES & SEALANTS LTD.

- TABLE 192 CHEMIQUE ADHESIVES & SEALANTS LTD.: COMPANY OVERVIEW

- TABLE 193 CHEMIQUE ADHESIVES & SEALANTS LTD.: PRODUCTS/SOLUTIONS/ SERVICES OFFERINGS

- 12.1.12 BOLTON GROUP

- TABLE 194 BOLTON GROUP: COMPANY OVERVIEW

- TABLE 195 BOLTON GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.13 WINLONG GW INTERNATIONAL TECHNOLOGY (QINGDAO) CO., LTD.

- TABLE 196 WINLONG GW INTERNATIONAL TECHNOLOGY (QINGDAO) CO., LTD.: COMPANY OVERVIEW

- TABLE 197 WINLONG GW INTERNATIONAL TECHNOLOGY (QINGDAO) CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.14 SUPER BOND ADHESIVE PVT. LTD.

- TABLE 198 SUPER BOND ADHESIVE PVT. LTD.: COMPANY OVERVIEW

- TABLE 199 SUPER BOND ADHESIVE PVT. LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.15 JOWAT SE

- TABLE 200 JOWAT SE: COMPANY OVERVIEW

- TABLE 201 JOWAT SE: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.16 MAPEI CORPORATION

- TABLE 202 MAPEI CORPORATION: COMPANY OVERVIEW

- TABLE 203 MAPEI CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.17 SURFACTANT INDUSTRIES

- TABLE 204 SURFACTANT INDUSTRIES: COMPANY OVERVIEW

- TABLE 205 SURFACTANT INDUSTRIES: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.18 ARCLIN, INC.

- TABLE 206 ARCLIN, INC.: COMPANY OVERVIEW

- TABLE 207 ARCLIN, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- TABLE 208 ARCLIN, INC.: DEALS, JANUARY 2018-DECEMBER 2023

- 12.1.19 AKKIM SEALANTS & ADHESIVES

- TABLE 209 AKKIM SEALANTS & ADHESIVES: COMPANY OVERVIEW

- TABLE 210 AKKIM SEALANTS & ADHESIVES: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.20 IFS INDUSTRIES INC.

- TABLE 211 IFS INDUSTRIES INC.: COMPANY OVERVIEW

- TABLE 212 IFS INDUSTRIES INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.21 KIILTO

- TABLE 213 KIILTO: COMPANY OVERVIEW

- TABLE 214 KIILTO: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- TABLE 215 KIILTO: DEALS, JANUARY 2018-DECEMBER 2023

- 12.1.22 TREMCO

- TABLE 216 TREMCO: COMPANY OVERVIEW

- TABLE 217 TREMCO: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.23 NAPCO

- TABLE 218 NAPCO: COMPANY OVERVIEW

- TABLE 219 NAPCO: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.24 DYNEA

- TABLE 220 DYNEA: COMPANY OVERVIEW

- TABLE 221 DYNEA: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- 12.1.25 ROBATECH AG

- TABLE 222 ROBATECH AG: COMPANY OVERVIEW

- TABLE 223 ROBATECH AG: PRODUCTS/SOLUTIONS/SERVICES OFFERINGS

- *Details on Business overview, Products/Solutions/Services offered, Recent Developments, MnM view, Key strengths, Strategic choices, Weaknesses and competitive threats might not be captured in case of unlisted companies.

13 ADJACENT AND RELATED MARKETS

- 13.1 INTRODUCTION

- 13.2 CROSS-LAMINATED TIMBER

- 13.2.1 MARKET DEFINITION

- 13.2.2 CROSS-LAMINATED TIMBER: MARKET OVERVIEW

- 13.2.3 CROSS-LAMINATED TIMBER MARKET, BY TYPE

- TABLE 224 CROSS-LAMINATED TIMBER MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 225 CROSS-LAMINATED TIMBER MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 226 CROSS-LAMINATED TIMBER MARKET, BY TYPE, 2020-2022 (THOUSAND CUBIC METERS)

- TABLE 227 CROSS-LAMINATED TIMBER MARKET, BY TYPE, 2023-2028 (THOUSAND CUBIC METERS)

- 13.2.4 CROSS-LAMINATED TIMBER MARKET, BY END-USE INDUSTRY

- TABLE 228 CROSS-LAMINATED TIMBER MARKET, BY END-USE INDUSTRY, 2020-2022 (USD MILLION)

- TABLE 229 CROSS-LAMINATED TIMBER MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 230 CROSS-LAMINATED TIMBER MARKET, BY END-USE INDUSTRY, 2020-2022 (THOUSAND CUBIC METERS)

- TABLE 231 CROSS-LAMINATED TIMBER MARKET, BY END-USE INDUSTRY, 2023-2028 (THOUSAND CUBIC METERS)

- 13.2.5 CROSS-LAMINATED TIMBER MARKET, BY INDUSTRY

- TABLE 232 CROSS-LAMINATED TIMBER MARKET, BY INDUSTRY, 2020-2022 (USD MILLION)

- TABLE 233 CROSS-LAMINATED TIMBER MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 234 CROSS-LAMINATED TIMBER MARKET, BY INDUSTRY, 2020-2022 (THOUSAND CUBIC METER)

- TABLE 235 CROSS-LAMINATED TIMBER MARKET, BY INDUSTRY, 2023-2028 (THOUSAND CUBIC METER)

- 13.2.6 CROSS-LAMINATED TIMBER MARKET, BY REGION

- TABLE 236 CROSS-LAMINATED TIMBER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 237 CROSS-LAMINATED TIMBER MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 238 CROSS-LAMINATED TIMBER MARKET, BY REGION, 2020-2022 (THOUSAND CUBIC METERS)

- TABLE 239 CROSS-LAMINATED TIMBER MARKET, BY REGION, 2023-2028 (THOUSAND CUBIC METERS)

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS