|

|

市場調査レポート

商品コード

1956050

グラフトポリオレフィンの世界市場:タイプ別、加工技術別、用途別、最終用途産業別、地域別 - 2030年までの予測Grafted Polyolefins Market by Type (Maleic Anhydride Grafted PE, PP, EVA), Application (Adhesion Promotion, Compatibilization), End-use Industry (Automotive, Packaging, Construction), Processing Technology, Region - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| グラフトポリオレフィンの世界市場:タイプ別、加工技術別、用途別、最終用途産業別、地域別 - 2030年までの予測 |

|

出版日: 2026年02月18日

発行: MarketsandMarkets

ページ情報: 英文 297 Pages

納期: 即納可能

|

概要

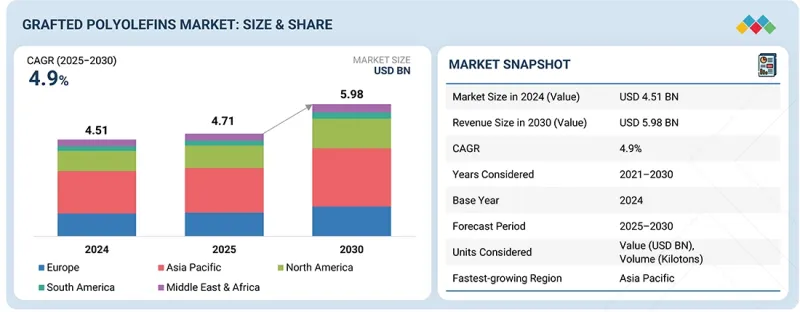

グラフトポリオレフィンの市場規模は、2025年の47億1,000万米ドルから2030年までに59億8,000万米ドルへ成長し、予測期間中にCAGR4.9%を記録すると見込まれています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2021年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 対象単位 | 価値(100万/10億米ドル)、数量(キロトン) |

| セグメント | タイプ別、加工技術別、用途別、最終用途産業別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

自動車、包装、建設分野における多材料適合性と接着性能への需要が、グラフトポリオレフィン市場の成長を牽引しています。ポリマーブレンド、複合材料、再生プラスチックを採用する企業が増える中、効果的な相溶化剤としてグラフトポリオレフィンが注目されています。自動車分野における軽量化の取り組みや多層包装システムの開発は、引き続きこの市場の成長を支えています。新規制が持続可能性とリサイクル性を重視する中、金属や溶剤代替手法を用いずに性能向上を図るため、機能化ポリオレフィンの採用が増加しています。反応性押出やコンパウンディングプロセスといった新技術は、コスト効率と用途の多様性を高めています。

グラフトポリオレフィン市場において最大のタイプを占めるセグメントは、無水マレイン酸グラフトポリエチレンです。低コスト、高い汎用性、加工の容易さなど様々な特長から、最も広く使用されているグラフトポリオレフィンです。無水マレイン酸グラフトポリエチレンは、極性基材に対する優れた接着性と相溶性を有しながらも、ポリエチレンと比較して広い柔軟性範囲と耐薬品性を維持しています。このため、無水マレイン酸グラフトポリエチレンは、多層包装フィルム、パイプ、ケーブル、再生ポリマーのブレンドなど、大量生産用途におけるタイ剤または相溶化剤として頻繁に利用されています。グラフトポリエチレンは、包装業界や建設業界からの高い需要、ポリエチレン原料の豊富さ、スケーラブルな押出ベースのグラフト化技術による製造可能性から、グラフトポリオレフィンの中で依然として主流のタイプです。

グラフトポリオレフィン市場の最大の最終用途産業の一つは自動車産業です。同産業では、複合材料を用いた軽量化や、様々な用途における多様な材料の使用が重視されているためです。したがって、グラフトポリオレフィンは、互換化剤(様々な種類のポリマー材料との)としてのポリマー加工や、機械構造体内の混合材料構成における接着強化・密着性向上に幅広く活用されています。異種材料の混合物に対して、優れた接着特性・密着性を提供するからです。これにより、自動車内の金属部品を代替する複合材料構成の機械的強度、耐衝撃性、熱安定性が劇的に向上します。内装、外装、エンジンルーム内用途に大量に使用されるプラスチック部品に加え、政府の燃費基準・排出ガス規制、車両/エンジン性能全般に関する要求事項により、自動車製造向けグラフトポリオレフィンは大量かつ頻繁な需要が高まっています。

アジア太平洋は、その膨大な製造能力、発展途上の産業構造、自動車、包装、建設、消費財など多岐にわたる産業におけるプラスチックの多用により、グラフトポリオレフィンにとって最大かつ最も急速に成長している地域市場です。さらに、ポリオレフィンの大規模生産に加え、コスト効率の高い押出成形およびコンパウンディング設備、ならびに原材料の入手可能性が、この地域の成長を継続的に牽引しています。自動車生産の増加、フレキシブル包装への需要拡大、ポリマーブレンドや再生プラスチックの使用増加も、この市場の成長を支えています。先進的なポリマー加工技術への投資増加、発展途上国からの輸出拡大、輸出志向型環境を後押しする政府の製造支援政策の結果、グラフトポリオレフィンの市場成長は大幅に増加しています。

グラフトポリオレフィン市場には、Mitsubishi Chemical Group Corporation(日本)、Guangzhou Lushan New Materials(中国)、LyondellBasell Industries Holdings B.V.(米国)、Mitsui Chemicals Asia Pacific, Ltd.(日本)、Arkema(フランス)、Clariant (スイス)、Borealis AG(オーストリア)、SI Group, Inc.(米国)、Dow(米国)、COACE Chemical Company Limited(中国)などの主要企業が参入しています。本調査では、グラフトポリオレフィン市場におけるこれらの主要企業について、企業プロファイル、最近の動向、主要な市場戦略を含む詳細な競合分析を行っています。

調査範囲

当レポートでは、グラフトポリオレフィン市場をタイプ、加工技術、最終用途産業、用途、地域に基づいてセグメント化し、各地域における市場全体の価値予測を提供します。主要業界参入企業の詳細な分析を実施し、グラフトポリオレフィン市場に関連する事業概要、製品・サービス、主要戦略、事業拡大に関する洞察を提供します。

当レポート購入の主な利点

本調査レポートは、業界分析(業界動向)、主要企業の市場ランキング分析、企業プロファイルなど、様々なレベルの分析に焦点を当てており、これらを総合することで、競合情勢の全体像、グラフトポリオレフィン市場の新興・高成長セグメント、高成長地域、市場促進要因、抑制要因、機会、課題について包括的な見解を提供します。

当レポートは以下のポイントに関する洞察を提供します:

- 成長要因の分析:(ポリマーブレンド・複合材料の性能向上、包装接着性・自動車軽量化の支援、リサイクル互換性・循環材料性能の改善)、抑制要因(材料コストプレミアム・配合複雑性の管理)、機会(混合廃棄物リサイクル用互換化剤の成長捕捉)、課題(グラフトレベルと溶融加工性のバランス)がグラフトポリオレフィン市場の成長に与える影響。

- 市場浸透状況:世界のグラフトポリオレフィン市場における主要企業が提供するグラフトポリオレフィンに関する包括的な情報。

- 製品開発/イノベーション:グラフトポリオレフィン市場における今後の技術動向、製品発売、事業拡大、買収に関する詳細な分析。

- 市場開発:収益性の高い新興市場に関する包括的な情報。当レポートでは、地域別にグラフトポリオレフィン市場の動向を分析しています。

- 市場容量:入手可能な範囲で各社の生産能力を提示し、グラフトポリオレフィン市場における今後の生産能力拡大計画についても言及します。

- 競合評価:グラフトポリオレフィン市場における主要企業の市場シェア、戦略、製品、製造能力に関する詳細な評価。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズと空白

- 相互接続された市場と分野横断的な機会

- ティア1/2/3参入企業の戦略的動き

第5章 業界動向

- ポーターのファイブフォース分析

- マクロ経済指標

- サプライチェーン分析

- 価格分析

- エコシステム分析

- 貿易分析

- 2026年の主な会議とイベント

- 顧客ビジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ

- ケーススタディ分析

- 2025年の米国関税の影響- グラフトポリオレフィン市場

第6章 技術の進歩、AIによる影響、特許、イノベーション、将来の応用

- 主要な新興技術

- 補完的技術

- 隣接技術

- 技術/製品ロードマップ

- 特許分析

- 将来の応用

- AI/生成AIがグラフトポリオレフィン市場に与える影響

- 成功事例と実世界への応用

第7章 持続可能性と規制状況

- 地域の規制とコンプライアンス

- 持続可能性への取り組み

- 持続可能性への影響と規制政策の取り組み

- 認証、ラベル、環境基準

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 購入者の利害関係者と購入評価基準

- 採用障壁と内部課題

- さまざまな最終用途産業におけるアンメットニーズ

- 市場収益性

第9章 グラフトポリオレフィン市場(タイプ別)

- 無水マレイン酸グラフトPE

- 無水マレイン酸グラフトPP

- 無水マレイン酸グラフトEVA

- その他

第10章 グラフトポリオレフィン市場(加工技術別)

- 押出

- メルトグラフト

- その他

第11章 グラフトポリオレフィン市場(用途別)

- イントロダクション

- 接着促進

- 衝撃の修正

- 互換性

- ボンディング

- その他

第12章 グラフトポリオレフィン市場(最終用途産業別)

- 自動車

- 包装

- 建設

- 繊維

- 接着剤とシーラント

- その他

第13章 グラフトポリオレフィン市場(地域別)

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- イタリア

- フランス

- 英国

- スペイン

- ロシア

- その他

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他

- 南米

- アルゼンチン

- ブラジル

- その他

第14章 競合情勢

- 主要参入企業の戦略/強み

- 市場シェア分析、2024年

- 収益分析

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業、2024年

- ブランド/製品比較

- 企業評価と財務指標

- 競合シナリオ

第15章 企業プロファイル

- 主要参入企業

- MITSUBISHI CHEMICAL GROUP CORPORATION

- GUANGZHOU LUSHAN NEW MATERIALS CO., LTD.

- LYONDELLBASELL INDUSTRIES HOLDINGS B.V.

- MITSUI CHEMICALS ASIA PACIFIC, LTD.

- ARKEMA

- CLARIANT

- BOREALIS GMBH

- SI GROUP, INC.

- DOW

- COACE CHEMICAL COMPANY LIMITED

- その他の企業

- SWASTIK INTERCHEM PRIVATE LIMITED

- THE COMPOUND COMPANY

- WILL & CO B.V.

- FAER WAX

- NAGASE AMERICA LLC

- PAYESH C-ONE POLYMER

- WESTLAKE CORPORATION

- FINE-BLEND POLYMER(SHANGHAI)CO., LTD.

- SYNTHOMER PLC

- SACO AEI POLYMERS

- SHENYANG KETONG PLASTIC CO., LTD.