|

|

市場調査レポート

商品コード

1473822

生成AIの世界市場:提供別、モダリティ別、用途別、業界別、地域別 - 予測(~2030年)Generative AI Market by Offering (Transformer Models (GPT-1, GPT-2, GPT-3, GPT-4, LaMDA), Services), Modality (Text, Image, Video, Audio & Speech, Code), Application (Content Management, Search & Discovery), Vertical and Region - Global Forecast to 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 生成AIの世界市場:提供別、モダリティ別、用途別、業界別、地域別 - 予測(~2030年) |

|

出版日: 2024年04月29日

発行: MarketsandMarkets

ページ情報: 英文 738 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の生成AIの市場規模は、2024年の209億米ドルから2030年までに1,367億米ドルに達し、予測期間にCAGRで36.7%の成長が見込まれます。

データへのアクセスを容易にするクラウドストレージソリューションの登場や、AIとディープラーニングの進化、コンテンツ生成と革新的用途の急速な台頭により、市場は成長すると予測されます。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2019年~2030年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2030年 |

| 単位 | 10億米ドル |

| セグメント | 提供、データモダリティ、用途、業界、地域 |

| 対象地域 | 北米、欧州、アジア太平洋、中東・アフリカ、ラテンアメリカ |

「ソフトウェアタイプ別では、トランスフォーマーモデルセグメントが予測期間にもっとも高い市場成長率を記録する見込みです。」

生成AI市場のトランスフォーマーモデルソフトウェアタイプは、自然言語処理(NLP)とテキスト生成タスクにおける比類のない能力により、予測期間にもっとも高い成長率を記録する見込みです。GPT-3のようなトランスフォーマーモデルは、人間らしいテキストの理解と生成において大きな成功を示しており、チャットボット、言語翻訳、コンテンツ作成などの用途で非常に価値の高い存在となっています。企業が顧客エンゲージメントやデータアナリティクスにおいてAIを活用した言語ソリューションへの依存度を高める中、トランスフォーマーベースの生成AIソフトウェアの需要は急増し、このセグメントの急成長を促進することになります。

「データモダリティ別では、テキストモダリティセグメントが予測期間に最大の市場シェアを占める見込みです。」

生成AI市場のテキストデータモダリティセグメントは、複数の魅力的な要因により、予測期間に最大の市場シェアを獲得する見込みです。自然言語処理(NLP)や言語生成モデルなどのテキストベースの生成AI用途は、コンテンツ生成、チャットボット、センチメント分析、言語翻訳などのタスクにさまざまな業界で広く採用されています。小売、医療、金融などの部門で、AIを活用したカスタマーサービスソリューションや、パーソナライズされたコンテンツ作成、効率的なデータアナリティクスに対する需要が高まっていることが、このセグメントの大幅な成長を後押ししています。さらに、精巧なテキストベースの生成AIモデルの成熟度と利用可能性が採用をさらに加速させており、生成AI市場における支配的なモダリティとなっています。

「地域別では、アジア太平洋がもっとも速いペースで成長し、北米が予測期間に最大の市場シェアを占める見込みです。」

アジア太平洋の生成AI市場は、同地域における急速なデジタルトランスフォーメーションや、さまざまな業界におけるAI技術の急速な採用、AI開発を促進する政府の取り組みにより、予測期間にもっとも高い成長率を示すことが予測されます。中国、日本、インドなどの国々はAIの研究開発に多額の投資を行っており、生成AIソリューションの需要を促進しています。一方、北米は最大の市場シェアを占めると見られており、その主な理由は、主要市場企業の強力なプレゼンス、強固な技術インフラ、医療、小売、自動車などの業界におけるAIの早期採用にあります。この地域の研究機関や大手テック企業を含む先進のAIエコシステムが、北米の生成AI市場のフロントランナーとしての地位をさらに強固なものにしています。

当レポートでは、世界の生成AI市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 生成AI市場の企業にとって魅力的な機会

- 生成AI市場:上位3つの用途

- 北米の生成AI市場:提供別、業界別

- 生成AI市場:地域別

第5章 市場の概要、産業動向

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 生成AIの倫理と影響

- 生成AIの進化

- 生成AIの投資の収益率

- 生成AIの成熟曲線

- 生成AI:開発・展開コスト

- エコシステム分析

- サプライチェーン分析

- 生成AIのツールとフレームワーク

- 生成AIの技術・手法

- 投資情勢と資金調達シナリオ

- ケーススタディ分析

- 技術分析

- 規制情勢

- 特許分析

- 価格設定の分析

- 主な会議とイベント

- ポーターのファイブフォース分析

- 技術ロードマップ

- 生成AIのビジネスモデル

- 顧客のビジネスに影響を与える動向/混乱

- 主なステークホルダーと購入基準

第6章 生成AI市場:提供別

- イントロダクション

- ソフトウェア

- サービス

第7章 生成AI市場:データモダリティ別

- イントロダクション

- テキスト

- 画像

- 動画

- 音声・スピーチ

- コード

第8章 生成AI市場:用途別

- イントロダクション

- ビジネスインテリジェンス・視覚化

- コンテンツ管理

- 合成データ管理

- 検索・発見

- 自動化・統合

- デザイン生成AI

- その他の用途

第9章 生成AI市場:業界別

- イントロダクション

- メディア・エンターテインメント

- BFSI

- 医療・ライフサイエンス

- 製造

- 小売・eコマース

- 輸送・ロジスティクス

- 建設・不動産

- エネルギー・ユーティリティ

- 政府・防衛

第10章 生成AI市場:地域別

- 概要

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第11章 競合情勢

- 概要

- 主な企業の戦略

- 収益分析

- 市場シェア分析

- 製品の比較分析

- 主要ベンダーの企業評価と財務指標

- 企業評価マトリクス:主要企業

- 企業評価マトリクス:スタートアップ/中小企業

- 競合シナリオと動向

第12章 企業プロファイル

- イントロダクション

- 主要企業

- MICROSOFT

- AWS

- ADOBE

- OPENAI

- IBM

- META

- ANTHROPIC

- NVIDIA

- ACCENTURE

- CAPGEMINI

- INSILICO MEDICINE

- SIMPLIFIED

- LUMEN5

- AI21 LABS

- HUGGING FACE

- DIALPAD

- PERSADO

- LIGHTRICKS

- PAIGE.AI

- PLAY.HT

- SPEECHIFY

- MIDJOURNEY

- FIREFLIES

- SYNTHESIA

- MOSTLY AI

- CHARACTER.AI

- HYPOTENUSE AI

- VIABLE

- DEFOG.AI

- DEEPSEARCH LABS

- WRITESONIC

- AMBERSEARCH

- COPY.AI

- SYNTHESIS AI

- COLOSSYAN

- INFLECTION AI

- GLEAN

- JASPER

- RUNWAY

- INWORLD AI

- TYPEFACE

- INSTADEEP

- FORETHOUGHT

- TOGETHER AI

- UPSTAGE

- MISTRAL AI

- ADEPT

- MOSAIC ML

- STABILITY AI

- COHERE

- OPEN-SOURCE COMPANIES

- GFP-GAN

- FONTJOY

- ELEUTHERAI

- STARRYAI

- MAGIC STUDIO

- BAICHUAN AI

- SALESFORCE

- TECHNOLOGY INNOVATION INSTITUTE

- ABACUS.AI

- OPENLM

第13章 隣接市場と関連市場

- イントロダクション

- 対話型AI市場 - 世界の予測(~2028年)

- チャットボット市場 - 世界の予測(~2028年)

第14章 付録

The generative AI market is projected to grow from USD 20.9 billion in 2024 to USD 136.7 billion by 2030, at a compound annual growth rate (CAGR) of 36.7% during the forecast period. Market is anticipated to grow due to the emergence of cloud storage solutions that make data easily accessible, evolution of AI and deep learning and rapid rise in content generation and innovative applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2030 |

| Base Year | 2023 |

| Forecast Period | 2024-2030 |

| Units Considered | USD (Billion) |

| Segments | Offering, Data Modality, Application, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

"By software type, transformer models segment is expected to register the fastest market growth rate during the forecast period."

The transformer models software type of the generative AI market is expected to experience the fastest growth rate during the forecast period due to its unmatched capabilities in natural language processing (NLP) and text generation tasks. Transformer models, such as GPT-3, have demonstrated remarkable success in understanding and generating human-like text, making them invaluable for applications like chatbots, language translation, content creation, and more. As businesses increasingly rely on AI-powered language solutions for customer engagement and data analysis, the demand for transformer-based generative AI software is set to soar, driving the rapid growth of this segment.

"by data modality, text modality segment is expected to account for the largest market share during the forecast period."

The text data modality segment of the generative AI market is poised to capture the largest market share during the forecast period due to several compelling factors. Text-based generative AI applications, such as natural language processing (NLP) and language generation models, are widely adopted across various industries for tasks like content generation, chatbots, sentiment analysis, and language translation. The growing demand for AI-powered customer service solutions, personalized content creation, and efficient data analysis in sectors like retail, healthcare, and finance is driving the significant growth of this segment. Additionally, the maturity and availability of sophisticated text-based generative AI models have further accelerated adoption, making it the dominant modality in the generative AI market.

"By Region, Asia Pacific is slated to grow at the fastest rate and North America to have the largest market share during the forecast period."

The Asia Pacific generative AI market is expected to witness the fastest growth rate during the forecast period due to the region's rapid digital transformation, burgeoning adoption of AI technologies across various industries, and government initiatives promoting AI development. Countries like China, Japan, and India are investing heavily in AI research and development, driving the demand for generative AI solutions. On the other hand, North America is poised to hold the largest market share, primarily attributed to the strong presence of key market players, robust technological infrastructure, and early adoption of AI across industries such as healthcare, retail, and automotive. The region's advanced AI ecosystem, including research institutions and tech giants, further solidifies North America's position as a frontrunner in the generative AI market.

Breakdown of primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the generative AI market.

- By Company: Tier I - 30%, Tier II - 45%, and Tier III - 25%

- By Designation: C-Level Executives - 40%, D-Level Executives - 32%, and others - 28%

- By Region: North America - 38%, Europe - 26%, Asia Pacific - 23%, Middle East & Africa - 8%, and Latin America - 5%

The report includes the study of key players offering generative AI solutions. It profiles major vendors in the generative AI market. The major players in the generative AI market include Microsoft (US), IBM (US), Google (US), AWS (US), META (US), Adobe (US), OpenAI (US), NVIDIA (US), Accenture (Ireland), Capgemini (France), Insilico Medicine (Hong Kong), Simplified (US), Anthropic (US), AI21 Labs (Israel), Lumen5 (Canada), Hugging Face (US), Dialpad (US), Persado (US), Copy.ai (US), Synthesis AI (US), Together AI (US), PlayHT (US), Speechify (US), Mistral AI (France), Midjourney (US), Fireflies (US), Adept (US), Stability AI (UK), Lightricks (Israel), Synthesia (UK), Mostly AI (Austria), Cohere (Canada), Colossyan (UK), Mosaic ML (US), Inflection AI (US), Glean (US), Charater.ai (US), Hypotenuse AI (US), Viable (US), Defog.ai (US), Jasper (US), DeepSearch Labs (UK), Writesonic (US), amberSearch (Germany), Runway (US), Inworld AI (US), Typeface (US), Paige (US), Upstage (South Korea), InstaDeep (UK), Forethought (US), GFP-GAN (US), Fontjoy (Italy), EleutherAI (US), StarryAI (US), Magic Studio (US), Baichuan Intelligence (China), Salesforce (US), Technology Innovation Institute (UAE), Abacus.AI (US), and OpenLM (US).

Research coverage

This research report categorizes the generative AI market by Offering (Software and Services), Software By Type (Rule Based Models, Statistical Models, Deep Learning, Generative Adversarial Networks (GANs), Autoencoders, Convolutional Neural Networks (CNNs), and Transformer Models), Software By Deployment Mode (Cloud and On-premises), By Services (Professional Services (Training & Consulting, System Integration & Implementation, and Support & Maintenance) and Managed Services), By Data Modality (Text, Image, Video, Audio & Speech, and Code), By Application (Business Intelligence & Visualization, Content Management, Synthetic Data Management, Search & Discovery, Automation & Integration, Generative Design AI, Other Applications (Predictive Maintenance, File Conversion, and Mathematical Problem Solving)), By Vertical (Media & Entertainment, Transportation & Logistics, Manufacturing, Healthcare & Life Sciences, IT & ITeS, BFSI, Energy & Utilities, Retail & Ecommerce, Government & Defense, Construction & Real Estate, Telecommunications, Others (Travel & Hospitality And Education), and By Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the generative AI market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, mergers and acquisitions, and recent developments associated with the generative AI market. Competitive analysis of upcoming startups in the generative AI market ecosystem is covered in this report.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall generative AI market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights better to position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (innovation of cloud storage enabling easy access to data, Evolution of AI and deep learning, Rise in content creation and creative applications), restraints (high cost associated with training data preparation, issues related to bias and inaccurately generated output, risks associated with data breaches and sensitive information leakage), opportunities (increasing deployment of large language models, growing interest of enterprises in commercializing synthetic images, robust improvement in generative ML leading to human baseline performance), and challenges (concerns regarding misuse of generative AI for illegal activities, quality of the output generated by generative AI models, computational complexity and technical challenges of generative AI ).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the generative AI market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the generative AI market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the generative AI market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Microsoft (US), IBM (US), Google (US), AWS (US), META (US), Adobe (US), OpenAI (US), NVIDIA (US), Accenture (Ireland), Capgemini (France), Insilico Medicine (Hong Kong), Simplified (US), Anthropic (US), AI21 Labs (Israel), Lumen5 (Canada), Hugging Face (US), Dialpad (US), and Persado (US), among others in the generative AI market. The report also helps stakeholders understand the pulse of the generative AI market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- FIGURE 1 GENERATIVE AI MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- FIGURE 2 GENERATIVE AI MARKET SEGMENTATION, BY REGION

- 1.3.3 YEARS CONSIDERED

- FIGURE 3 STUDY YEARS/PERIODS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATES, 2019-2023

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

- 1.6.1 IMPACT OF RECESSION

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 4 GENERATIVE AI MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- TABLE 2 PRIMARY INTERVIEWS

- 2.1.2.1 Breakup of primary profiles

- FIGURE 5 PRIMARY PROFILES, BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.1.2.2 Key industry insights

- FIGURE 6 INSIGHTS FROM INDUSTRY EXPERTS

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 7 GENERATIVE AI MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- 2.2.1 TOP-DOWN APPROACH

- 2.2.2 BOTTOM-UP APPROACH

- FIGURE 8 APPROACH 1 (BOTTOM-UP; SUPPLY-SIDE): REVENUE FROM KEY PLAYERS OFFERING SOLUTIONS/SERVICES OF GENERATIVE AI

- FIGURE 9 APPROACH 2 (BOTTOM-UP; SUPPLY-SIDE): COLLECTIVE REVENUE FROM ALL SOLUTIONS/SERVICES OF GENERATIVE AI

- FIGURE 10 APPROACH 3 (BOTTOM-UP; SUPPLY-SIDE): MARKET ESTIMATION STEPS AND CORRESPONDING SOURCES

- FIGURE 11 APPROACH 4 (BOTTOM-UP; DEMAND-SIDE): SHARE OF GENERATIVE AI THROUGH OVERALL ARTIFICIAL INTELLIGENCE SPENDING

- 2.3 DATA TRIANGULATION

- FIGURE 12 DATA TRIANGULATION

- 2.4 MARKET FORECAST

- TABLE 3 FACTOR ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 STUDY LIMITATIONS

- 2.7 IMPACT OF RECESSION ON GENERATIVE AI MARKET

- TABLE 4 IMPACT OF RECESSION ON GLOBAL GENERATIVE AI MARKET

3 EXECUTIVE SUMMARY

- TABLE 5 GENERATIVE AI MARKET SIZE AND GROWTH RATE, 2020-2023 (USD MILLION, Y-O-Y)

- TABLE 6 GENERATIVE AI MARKET SIZE AND GROWTH RATE, 2024-2030 (USD MILLION, Y-O-Y)

- FIGURE 13 GENERATIVE AI SOFTWARE TO BE LARGER MARKET THAN SERVICES IN 2024

- FIGURE 14 DEEP LEARNING TO BE LEADING SEGMENT AMONG SOFTWARE TYPES IN 2024

- FIGURE 15 CLOUD DEPLOYMENT OF GENERATIVE AI SOFTWARE TO BE FASTER-GROWING MODE DURING FORECAST PERIOD

- FIGURE 16 PROFESSIONAL SERVICES TO BE DOMINANT SERVICE SEGMENT IN 2024

- FIGURE 17 TRAINING & CONSULTING SERVICES SET TO REGISTER HIGHEST SHARE AMONG PROFESSIONAL SERVICES IN 2024

- FIGURE 18 TEXT DATA MODALITY TO ACCOUNT FOR LARGEST MARKET SHARE IN 2024

- FIGURE 19 CONTENT MANAGEMENT TO BE LEADING APPLICATION IN 2024

- FIGURE 20 RETAIL & ECOMMERCE TO WITNESS HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 21 ASIA PACIFIC TO REGISTER FASTEST GROWTH RATE BETWEEN 2024 AND 2030

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR GENERATIVE AI MARKET PLAYERS

- FIGURE 22 INCREASE IN DEMAND FOR MULTIMODAL GENERATIVE AI AND IMPROVED PERFORMANCE OF LARGE LANGUAGE MODELS TO DRIVE MARKET GROWTH

- 4.2 GENERATIVE AI MARKET: TOP THREE APPLICATIONS

- FIGURE 23 SYNTHETIC DATA MANAGEMENT SEGMENT TO ACCOUNT FOR HIGHEST GROWTH RATE DURING FORECAST PERIOD

- 4.3 NORTH AMERICA: GENERATIVE AI MARKET, BY OFFERING AND VERTICAL

- FIGURE 24 SOFTWARE AND MEDIA & ENTERTAINMENT TO BE LARGEST SEGMENTAL SHAREHOLDERS IN NORTH AMERICAN MARKET IN 2024

- 4.4 GENERATIVE AI MARKET, BY REGION

- FIGURE 25 NORTH AMERICA TO ACCOUNT FOR LARGEST REGIONAL SHARE IN 2024

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 26 GENERATIVE AI MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Innovation of cloud storage to enable easy access to data

- 5.2.1.2 Evolution of AI and deep learning

- FIGURE 27 ADVANCEMENTS IN DEEP LEARNING LED TO DEVELOPMENT OF EXTREMELY LARGE LANGUAGE MODELS, 2018-2023 (BILLION PARAMETERS)

- 5.2.1.3 Rise in content creation and creative applications

- FIGURE 28 GENERATIVE AI TOP USE CASES ACROSS ENTERPRISE SIZE, 2022

- 5.2.2 RESTRAINTS

- 5.2.2.1 High costs associated with training data preparation

- FIGURE 29 TRAINING COSTS PER MILLION PARAMETERS FOR VARIOUS GPT-3 BASED LLMS

- 5.2.2.2 Issues related to bias and inaccurately generated output

- FIGURE 30 ISSUES RELATED TO TRAINING DATA HIGHLIGHTED IN CHATGPT'S RESPONSES

- 5.2.2.3 Risks associated with data breaches and sensitive information leakage

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increase in deployment of large language models

- FIGURE 31 LARGE LANGUAGE MODEL SPENDING, BY END USER, 2024 VS. 2030 (USD MILLION)

- 5.2.3.2 Growth in interest of enterprises in commercializing synthetic images

- 5.2.3.3 Robust improvement in generative ML leading to human baseline performance

- FIGURE 32 SCORES OF SOME PROMINENT GENERATIVE AI MODELS IN HUMAN COGNITIVE SKILLS, 2022

- 5.2.4 CHALLENGES

- 5.2.4.1 Concerns regarding misuse of generative AI for illegal activities

- 5.2.4.2 Quality of output generated by generative AI models

- FIGURE 33 MODEL DRIFT IN GPT-4 WITHIN 3 MONTHS IN 2023

- 5.2.4.3 Computational complexity and technical challenges of generative AI

- FIGURE 34 COMPUTE REQUIREMENTS OF SOME PROMINENT GENERATIVE AI MODELS (TERAFLOPS)

- 5.3 ETHICS AND IMPLICATIONS OF GENERATIVE AI

- FIGURE 35 GENERATIVE AI ETHICAL SCENARIO TIMELINE, 2023-2025

- 5.3.1 BIAS AND FAIRNESS

- 5.3.2 PRIVACY AND SECURITY

- 5.3.3 INTELLECTUAL PROPERTY

- 5.3.4 ACCOUNTABILITY AND RESPONSIBILITY

- 5.3.5 SOCIETAL AND ECONOMIC IMPACT

- 5.3.6 ENVIRONMENTAL IMPACT

- FIGURE 36 CO2 EQUIVALENT EMISSIONS (TONNES) OF GENERATIVE AI MODELS COMPARED WITH REAL-LIFE EXAMPLES, 2022

- 5.4 EVOLUTION OF GENERATIVE AI

- FIGURE 37 EVOLUTION OF GENERATIVE AI

- 5.5 GENERATIVE AI RETURN ON INVESTMENT

- FIGURE 38 GENERATIVE AI PRODUCTIVITY IMPACT, BY INDUSTRY (USD BILLION)

- FIGURE 39 NET ROI IMPACT OF GENERATIVE AI CLOUD PROGRAMS ACROSS ENTERPRISES (PERCENTAGE POINTS)

- 5.6 GENERATIVE AI MATURITY CURVE

- FIGURE 40 GENERATIVE AI MATURITY CURVE

- 5.7 GENERATIVE AI: DEVELOPMENT & DEPLOYMENT COSTS

- FIGURE 41 COST TO TRAIN GENERATIVE AI MODEL WITH GPT-3 LEVEL PERFORMANCE, 2020-2030 (USD)

- 5.7.1 HARDWARE COSTS

- FIGURE 42 HARDWARE COSTS FOR GENERATIVE AI MODEL TRAINING

- 5.7.2 SOFTWARE COSTS

- FIGURE 43 SOFTWARE COSTS FOR TRAINING GENERATIVE AI MODELS USING NEURAL NETWORKS

- 5.7.3 SKILLED LABOR COSTS

- FIGURE 44 MEDIAN HOURLY RATES OF AI SOFTWARE WORKFORCE, 2023 (USD/HR)

- 5.8 ECOSYSTEM ANALYSIS

- TABLE 7 GENERATIVE AI MARKET: ECOSYSTEM

- FIGURE 45 KEY PLAYERS IN GENERATIVE AI MARKET ECOSYSTEM

- 5.8.1 TEXT GENERATOR PROVIDERS

- 5.8.2 VIDEO GENERATOR PROVIDERS

- 5.8.3 IMAGE GENERATOR PROVIDERS

- 5.8.4 AUDIO & SPEECH GENERATOR PROVIDERS

- 5.8.5 CODE GENERATOR PROVIDERS

- 5.8.6 CLOUD PLATFORM PROVIDERS

- 5.8.7 API-AS-A-SERVICE PROVIDERS

- 5.8.8 END USERS

- 5.8.9 GOVERNMENT AND REGULATORY BODIES

- 5.9 SUPPLY CHAIN ANALYSIS

- FIGURE 46 GENERATIVE AI MARKET: SUPPLY CHAIN ANALYSIS

- TABLE 8 GENERATIVE AI MARKET: SUPPLY CHAIN ANALYSIS

- 5.10 GENERATIVE AI TOOLS AND FRAMEWORK

- 5.10.1 TENSORFLOW

- 5.10.2 PYTORCH

- 5.10.3 KERAS

- 5.10.4 CAFFE

- 5.10.5 THEANO

- 5.10.6 MXNET

- 5.10.7 TORCH

- 5.10.8 HUGGING FACE

- 5.11 GENERATIVE AI TECHNIQUES & METHODS

- 5.11.1 TEXT GENERATION & LANGUAGE MODELING

- 5.11.1.1 Recurrent neural networks for text generation

- 5.11.1.2 Language modeling with transformers

- 5.11.1.3 Seq2Seq models for translation

- 5.11.2 IMAGE & VIDEO GENERATION

- 5.11.2.1 Generative adversarial networks for image generation

- 5.11.2.2 Style transfer and image-to-image translation

- 5.11.2.3 Video generation with GANs

- 5.11.3 MUSIC & AUDIO GENERATION

- 5.11.3.1 WaveNet and SampleRNN for audio generation

- 5.11.3.2 Music generation with LSTM networks

- 5.11.4 REINFORCEMENT LEARNING

- 5.11.4.1 Policy gradient methods

- 5.11.4.2 Actor-critic methods

- 5.11.1 TEXT GENERATION & LANGUAGE MODELING

- 5.12 INVESTMENT LANDSCAPE AND FUNDING SCENARIO

- FIGURE 47 GENERATIVE AI EQUITY FUNDING AND DEALS, 2019-2023

- FIGURE 48 LEADING GENERATIVE AI VENDORS BY FUNDING VALUE AND FUNDING ROUNDS, 2017-2024

- FIGURE 49 MOST VALUED GENERATIVE AI COMPANIES, 2023 (USD BILLION)

- FIGURE 50 GENERATIVE AI STARTUPS, BY FUNDING STAGE, 2023

- FIGURE 51 DISTRIBUTION OF GENERATIVE AI FUNDING, 2021-2022 (USD MILLION)

- FIGURE 52 INVESTMENTS IN GENERATIVE AI, BY CATEGORY, 2023 (USD MILLION)

- FIGURE 53 INVESTMENTS IN LARGE LANGUAGE MODEL OPERATIONS (LLMOPS), BY CATEGORY, 2023 (USD MILLION)

- FIGURE 54 LARGE LANGUAGE MODELS DEAL COUNT AND DEAL VALUE, Q1 2021-Q3 2023 (USD MILLION)

- 5.13 CASE STUDY ANALYSIS

- 5.13.1 MARKS & SPENCER ENHANCED EMAIL CONVERSION BY 20-34% WITH PERSADO'S MOTIVATION AI

- 5.13.2 VODAFONE GROUP PLC UNCOVERED KEY TRENDS AND RICH INSIGHTS THROUGH PERSADO'S MOTIVATION AI

- 5.13.3 WPP TRAINED 50,000 EMPLOYEES WITH AI VIDEOS

- 5.13.4 TELEPERFORMANCE TRAINED GLOBAL WORKFORCE WITH SYNTHESIA STUDIO

- 5.13.5 CISCO SCALED VIDEO CONTENT LOCALIZATION USING LUMEN5

- 5.13.6 SIEMENS DIGITALIZED ITS COMMUNICATIONS WITH LUMEN5

- 5.13.7 INTEL AND ACCENTURE COLLABORATED TO CREATE SET OF 34 OPEN-SOURCE AI REFERENCE KITS

- 5.14 TECHNOLOGY ANALYSIS

- 5.14.1 KEY TECHNOLOGIES

- 5.14.1.1 Generative Adversarial Networks (GANs)

- 5.14.1.2 Variational Autoencoders (VAEs)

- 5.14.1.3 Transformer Architecture

- 5.14.1.4 Attention Mechanisms

- 5.14.1.5 Transfer Learning

- 5.14.2 ADJACENT TECHNOLOGIES

- 5.14.2.1 Natural Language Processing (NLP)

- 5.14.2.2 Computer Vision

- 5.14.2.3 Reinforcement Learning

- 5.14.2.4 Knowledge Graphs

- 5.14.3 COMPLEMENTARY TECHNOLOGIES

- 5.14.3.1 High-Performance Computing (HPC)

- 5.14.3.2 Explainable AI

- 5.14.3.3 Privacy-Preserving AI

- 5.14.3.4 Blockchain

- 5.14.1 KEY TECHNOLOGIES

- 5.15 REGULATORY LANDSCAPE

- 5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15.2 REGULATIONS

- 5.15.2.1 North America

- 5.15.2.1.1 SCR 17: Artificial Intelligence Bill (California)

- 5.15.2.1.2 S1103: Artificial Intelligence Automated Decision Bill (Connecticut)

- 5.15.2.1.3 National Artificial Intelligence Initiative Act (NAIIA) (US)

- 5.15.2.1.4 Artificial Intelligence and Data Act (AIDA) (Canada)

- 5.15.2.2 Europe

- 5.15.2.2.1 The European Union (EU) - Artificial Intelligence Act (AIA)

- 5.15.2.2.2 General Data Protection Regulation (Europe)

- 5.15.2.3 Asia Pacific

- 5.15.2.3.1 Interim Administrative Measures for Generative Artificial Intelligence Services (China)

- 5.15.2.3.2 The National AI Strategy (Singapore)

- 5.15.2.3.3 Hiroshima AI Process Comprehensive Policy Framework (Japan)

- 5.15.2.4 Middle East & Africa

- 5.15.2.4.1 National Strategy for Artificial Intelligence (UAE)

- 5.15.2.4.2 The National Artificial Intelligence Strategy (Qatar)

- 5.15.2.4.3 AI Ethics Principles and Guidelines (Dubai)

- 5.15.2.5 Latin America

- 5.15.2.5.1 Santiago Declaration (Chile)

- 5.15.2.5.2 Brazilian Artificial Intelligence Strategy (EBIA)

- 5.15.2.1 North America

- 5.16 PATENT ANALYSIS

- 5.16.1 METHODOLOGY

- 5.16.2 PATENTS FILED, BY DOCUMENT TYPE

- TABLE 14 PATENTS FILED, 2013-2023

- 5.16.3 INNOVATION AND PATENT APPLICATIONS

- FIGURE 55 NUMBER OF PATENTS GRANTED IN LAST 10 YEARS, 2013-2023

- 5.16.3.1 Top 10 applicants in generative AI market

- FIGURE 56 TOP 10 APPLICANTS IN GENERATIVE AI MARKET, 2013-2023

- TABLE 15 TOP 20 PATENT OWNERS IN GENERATIVE AI MARKET, 2013-2023

- TABLE 16 LIST OF FEW PATENTS IN GENERATIVE AI MARKET, 2022-2023

- FIGURE 57 REGIONAL ANALYSIS OF PATENTS GRANTED, 2013-2023

- 5.17 PRICING ANALYSIS

- 5.17.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY DATA MODALITY

- FIGURE 58 AVERAGE SELLING PRICES OF KEY PLAYERS FOR TOP THREE DATA MODALITIES (USD/MONTH)

- TABLE 17 AVERAGE SELLING PRICES OF KEY PLAYERS FOR TOP THREE DATA MODALITIES (USD/MONTH)

- 5.17.2 INDICATIVE PRICING ANALYSIS, BY OFFERING

- TABLE 18 INDICATIVE PRICING LEVELS OF GENERATIVE AI SOLUTIONS, BY OFFERING

- 5.18 KEY CONFERENCES AND EVENTS

- TABLE 19 GENERATIVE AI MARKET: DETAILED LIST OF CONFERENCES & EVENTS, 2024-2025

- 5.19 PORTER'S FIVE FORCES ANALYSIS

- TABLE 20 PORTER'S FIVE FORCES' IMPACT ON GENERATIVE AI MARKET

- FIGURE 59 GENERATIVE AI MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.19.1 THREAT OF NEW ENTRANTS

- 5.19.2 THREAT OF SUBSTITUTES

- 5.19.3 BARGAINING POWER OF SUPPLIERS

- 5.19.4 BARGAINING POWER OF BUYERS

- 5.19.5 INTENSITY OF COMPETITION RIVALRY

- 5.20 TECHNOLOGY ROADMAP

- FIGURE 60 TECHNOLOGY ROADMAP FOR GENERATIVE AI MARKET

- 5.21 GENERATIVE AI BUSINESS MODELS

- FIGURE 61 GENERATIVE AI BUSINESS MODELS

- 5.21.1 GENERATIVE AI MODEL-AS-A-SERVICE

- 5.21.2 BUILT-IN-APPS BUSINESS MODEL

- 5.21.3 VERTICAL INTEGRATION BUSINESS MODEL

- 5.21.4 MARKETPLACES/EXCHANGES MODEL

- 5.22 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.22.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 62 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.23 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.23.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 63 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- TABLE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- 5.23.2 BUYING CRITERIA

- FIGURE 64 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- TABLE 22 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

6 GENERATIVE AI MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: GENERATIVE AI MARKET DRIVERS

- FIGURE 65 GENERATIVE AI SERVICES TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- TABLE 23 GENERATIVE AI MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 24 GENERATIVE AI MARKET, BY OFFERING, 2024-2030 (USD MILLION)

- 6.2 SOFTWARE

- TABLE 25 GENERATIVE AI SOFTWARE MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 26 GENERATIVE AI SOFTWARE MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.1 GENERATIVE AI SOFTWARE MARKET, BY TYPE

- FIGURE 66 DEEP LEARNING SUBSEGMENT TO BE LARGEST AMONG GENERATIVE AI SOFTWARE IN 2024

- TABLE 27 GENERATIVE AI SOFTWARE MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 28 GENERATIVE AI SOFTWARE MARKET, BY TYPE, 2024-2030 (USD MILLION)

- 6.2.1.1 Rule-based models

- 6.2.1.1.1 Rule-based models offer clear and interpretable approach to generative AI with explicit rules for data generation

- 6.2.1.1 Rule-based models

- TABLE 29 RULE-BASED GENERATIVE AI MODELS MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 30 RULE-BASED GENERATIVE AI MODELS MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.1.1.1.1 Knowledge-based models

- 6.2.1.1.1.2 Script-based models

- 6.2.1.1.1.3 Expert systems

- 6.2.1.2 Statistical models

- 6.2.1.2.1 Statistical models provide powerful means to capture complex patterns in data and generate precise outputs

- TABLE 31 STATISTICAL GENERATIVE AI MODELS MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 32 STATISTICAL GENERATIVE AI MODELS MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.1.2.1.1 Markov models

- 6.2.1.2.1.2 Hidden Markov models

- 6.2.1.2.1.3 Gaussian mixture models

- 6.2.1.2.1.4 Conditional random fields

- 6.2.1.3 Deep learning models

- 6.2.1.3.1 Deep learning models excel at generative tasks requiring fine-grained details

- TABLE 33 DEEP LEARNING GENERATIVE AI MODELS MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 34 DEEP LEARNING GENERATIVE AI MODELS MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.1.3.1.1 Feedforward neural networks

- 6.2.1.3.1.2 Recurrent neural networks

- 6.2.1.3.1.3 Long short-term memory (LSTM) networks

- 6.2.1.3.1.4 Gated recurrent units (GRUs)

- 6.2.1.4 Generative adversarial networks (GANs)

- 6.2.1.4.1 GANs provide unique approach to generative AI by training two competing neural networks to generate diverse data

- TABLE 35 GENERATIVE ADVERSARIAL NETWORKS MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 36 GENERATIVE ADVERSARIAL NETWORKS MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.1.4.1.1 Conditional generative adversarial networks (CGANs)

- 6.2.1.4.1.2 Style GANs

- 6.2.1.4.1.3 Cycle GANs

- 6.2.1.5 Autoencoders

- 6.2.1.5.1 Autoencoders used for generative tasks requiring new data points similar to original input

- TABLE 37 AUTOENCODERS: GENERATIVE AI MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 38 AUTOENCODERS: GENERATIVE AI MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.1.5.1.1 Denoising autoencoders

- 6.2.1.5.1.2 Variational autoencoders

- 6.2.1.6 Convolutional neural networks (CNNs)

- 6.2.1.6.1 Convolutional neural networks (CNNs) learn hierarchical features of image data to generate realistic images

- TABLE 39 CONVOLUTIONAL NEURAL NETWORKS MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 40 CONVOLUTIONAL NEURAL NETWORKS MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.1.6.1.1 Image-generating CNNs

- 6.2.1.6.1.2 Video-generating CNNs

- 6.2.1.7 Transformer-based Large Language Models (LLMs)

- 6.2.1.7.1 Transformer-based LLMs offer art performance and can generate coherent and contextually relevant text

- TABLE 41 TRANSFORMER-BASED LLMS MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 42 TRANSFORMER-BASED LLMS MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.1.7.1.1 Bidirectional encoder representations from transformers (BERTs)

- 6.2.1.7.1.2 Generative pre-trained transformer-1 (GPT-1)

- 6.2.1.7.1.3 Generative pre-trained transformer-2 (GPT-2)

- 6.2.1.7.1.4 Generative pre-trained transformer-3 (GPT-3)

- 6.2.1.7.1.5 Generative pre-trained transformer-4 (GPT-4)

- 6.2.1.7.1.6 Language model for dialogue applications (LaMDA)

- 6.2.1.7.1.7 Other transformer models

- 6.2.2 SOFTWARE MARKET, BY DEPLOYMENT MODE

- FIGURE 67 CLOUD SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- TABLE 43 GENERATIVE AI SOFTWARE MARKET, BY DEPLOYMENT MODE, 2019-2023 (USD MILLION)

- TABLE 44 GENERATIVE AI SOFTWARE MARKET, BY DEPLOYMENT MODE, 2024-2030 (USD MILLION)

- 6.2.2.1 On-premises

- 6.2.2.1.1 On-premise solutions to help organizations tailor generative AI to integrate seamlessly with existing systems

- 6.2.2.1 On-premises

- TABLE 45 ON-PREMISE GENERATIVE AI SOFTWARE MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 46 ON-PREMISE GENERATIVE AI SOFTWARE MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.2.2.2 Cloud

- 6.2.2.2.1 Cloud deployment to enable faster deployment of AI solutions and accessibility of AI technologies

- 6.2.2.2 Cloud

- TABLE 47 CLOUD-BASED GENERATIVE AI SOFTWARE MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 48 CLOUD-BASED GENERATIVE AI SOFTWARE MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.3 SERVICES

- FIGURE 68 MANAGED SERVICES TO REGISTER HIGHER CAGR IN GENERATIVE AI MARKET FOR SERVICES DURING FORECAST PERIOD

- TABLE 49 GENERATIVE AI MARKET, BY SERVICE, 2019-2023 (USD MILLION)

- TABLE 50 GENERATIVE AI MARKET, BY SERVICE, 2024-2030 (USD MILLION)

- TABLE 51 GENERATIVE AI SERVICES MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 52 GENERATIVE AI SERVICES MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.3.1 PROFESSIONAL SERVICES

- 6.3.1.1 Requirement assessment and customized implementation and assistance with deployment of generative AI solutions

- FIGURE 69 SYSTEM INTEGRATION & IMPLEMENTATION SUBSEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 53 GENERATIVE AI SERVICES MARKET, BY PROFESSIONAL SERVICE, 2019-2023 (USD MILLION)

- TABLE 54 GENERATIVE AI SERVICES MARKET, BY PROFESSIONAL SERVICE, 2024-2030 (USD MILLION)

- TABLE 55 GENERATIVE AI PROFESSIONAL SERVICES MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 56 GENERATIVE AI PROFESSIONAL SERVICES MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.3.1.2 Training & consulting services

- TABLE 57 GENERATIVE AI TRAINING & CONSULTING SERVICES MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 58 GENERATIVE AI TRAINING & CONSULTING SERVICES MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.3.1.2.1 Model design & training

- 6.3.1.2.2 Model fine-tuning

- 6.3.1.2.3 Prompt engineering

- 6.3.1.2.4 Consulting & system architecting

- 6.3.1.3 System integration & implementation services

- TABLE 59 GENERATIVE AI SYSTEM INTEGRATION & IMPLEMENTATION SERVICES MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 60 GENERATIVE AI SYSTEM INTEGRATION & IMPLEMENTATION SERVICES MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.3.1.3.1 Model Integration & Deployment

- 6.3.1.3.2 Custom App Development

- 6.3.1.3.3 API-based Model Integration

- 6.3.1.4 Support & maintenance services

- TABLE 61 GENERATIVE AI SUPPORT & MAINTENANCE SERVICES MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 62 GENERATIVE AI SUPPORT & MAINTENANCE SERVICES MARKET, BY REGION, 2024-2030 (USD MILLION)

- 6.3.1.4.1 Model Performance Metrics

- 6.3.1.4.2 Security & Compliance Audits

- 6.3.1.4.3 Model Optimization

- 6.3.2 MANAGED SERVICES

- 6.3.2.1 Managed services provide end-to-end management for generative AI, helping businesses focus on core competencies

- TABLE 63 GENERATIVE AI MANAGED SERVICES MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 64 GENERATIVE AI MANAGED SERVICES MARKET, BY REGION, 2024-2030 (USD MILLION)

7 GENERATIVE AI MARKET, BY DATA MODALITY

- 7.1 INTRODUCTION

- 7.1.1 DATA MODALITY: GENERATIVE AI MARKET DRIVERS

- FIGURE 70 VIDEO DATA MODALITY TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 65 GENERATIVE AI MARKET, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 66 GENERATIVE AI MARKET, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 7.2 TEXT

- 7.2.1 ADVANCED TECHNIQUES SUCH AS RNNS AND TRANSFORMER ARCHITECTURES TO PROCESS AND GENERATE TEXT

- TABLE 67 GENERATIVE AI MARKET, BY TEXT MODALITY, 2019-2023 (USD MILLION)

- TABLE 68 GENERATIVE AI MARKET, BY TEXT MODALITY, 2024-2030 (USD MILLION)

- 7.2.2 TEXT GENERATION

- TABLE 69 GENERATIVE AI MARKET IN TEXT GENERATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 70 GENERATIVE AI MARKET IN TEXT GENERATION, BY REGION, 2024-2030 (USD MILLION)

- 7.2.3 TEXT-BASED CHATBOTS

- TABLE 71 GENERATIVE AI MARKET IN TEXT-BASED CHATBOTS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 72 GENERATIVE AI MARKET IN TEXT-BASED CHATBOTS, BY REGION, 2024-2030 (USD MILLION)

- 7.2.4 TEXT SUMMARIZATION

- TABLE 73 GENERATIVE AI MARKET IN TEXT SUMMARIZATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 74 GENERATIVE AI MARKET IN TEXT SUMMARIZATION, BY REGION, 2024-2030 (USD MILLION)

- 7.2.5 TEXT TRANSLATION

- TABLE 75 GENERATIVE AI MARKET IN TEXT TRANSLATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 76 GENERATIVE AI MARKET IN TEXT TRANSLATION, BY REGION, 2024-2030 (USD MILLION)

- 7.2.6 OTHER TEXT MODALITIES

- TABLE 77 GENERATIVE AI MARKET IN OTHER TEXT MODALITIES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 78 GENERATIVE AI MARKET IN OTHER TEXT MODALITIES, BY REGION, 2024-2030 (USD MILLION)

- 7.3 IMAGE

- 7.3.1 CREATING VISUAL CONTENT, RANGING FROM PHOTOREALISTIC IMAGES TO ABSTRACT ART, USING ARTIFICIAL INTELLIGENCE IMAGE TECHNIQUES

- TABLE 79 GENERATIVE AI MARKET, BY IMAGE MODALITY, 2019-2023 (USD MILLION)

- TABLE 80 GENERATIVE AI MARKET, BY IMAGE MODALITY, 2024-2030 (USD MILLION)

- 7.3.2 IMAGE GENERATION

- TABLE 81 GENERATIVE AI MARKET IN IMAGE GENERATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 82 GENERATIVE AI MARKET IN IMAGE GENERATION, BY REGION, 2024-2030 (USD MILLION)

- 7.3.3 IMAGE CAPTIONING

- TABLE 83 GENERATIVE AI MARKET IN IMAGE CAPTIONING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 84 GENERATIVE AI MARKET IN IMAGE CAPTIONING, BY REGION, 2024-2030 (USD MILLION)

- 7.3.4 IMAGE EDITING & ENHANCEMENT

- TABLE 85 GENERATIVE AI MARKET IN IMAGE EDITING & ENHANCEMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 86 GENERATIVE AI MARKET IN IMAGE EDITING & ENHANCEMENT, BY REGION, 2024-2030 (USD MILLION)

- 7.3.5 OTHER IMAGE MODALITIES

- TABLE 87 GENERATIVE AI MARKET IN OTHER IMAGE MODALITIES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 88 GENERATIVE AI MARKET IN OTHER IMAGE MODALITIES, BY REGION, 2024-2030 (USD MILLION)

- 7.4 VIDEO

- 7.4.1 DEEP LEARNING MODELS UNDERSTAND AND RECREATE VISUAL DATA, ENABLING LIFELIKE VIDEOS

- TABLE 89 GENERATIVE AI MARKET, BY VIDEO MODALITY, 2019-2023 (USD MILLION)

- TABLE 90 GENERATIVE AI MARKET, BY VIDEO MODALITY, 2024-2030 (USD MILLION)

- 7.4.2 VIDEO GENERATION

- TABLE 91 GENERATIVE AI MARKET IN VIDEO GENERATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 92 GENERATIVE AI MARKET IN VIDEO GENERATION, BY REGION, 2024-2030 (USD MILLION)

- 7.4.3 VIDEO EDITING & ENHANCEMENT

- TABLE 93 GENERATIVE AI MARKET IN VIDEO EDITING & ENHANCEMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 94 GENERATIVE AI MARKET IN VIDEO EDITING & ENHANCEMENT, BY REGION, 2024-2030 (USD MILLION)

- 7.4.4 VIDEO ANNOTATION

- TABLE 95 GENERATIVE AI MARKET IN VIDEO ANNOTATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 96 GENERATIVE AI MARKET IN VIDEO ANNOTATION, BY REGION, 2024-2030 (USD MILLION)

- 7.4.5 OTHER VIDEO MODALITIES

- TABLE 97 GENERATIVE AI MARKET IN OTHER VIDEO MODALITIES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 98 GENERATIVE AI MARKET IN OTHER VIDEO MODALITIES, BY REGION, 2024-2030 (USD MILLION)

- 7.5 AUDIO & SPEECH

- 7.5.1 THROUGH ADVANCED ALGORITHMS AND DEEP LEARNING TECHNIQUES, GENERATIVE MODELS CAN ANALYZE AND SYNTHESIZE AUDIO DATA WITH REMARKABLE ACCURACY

- TABLE 99 GENERATIVE AI MARKET, BY AUDIO & SPEECH MODALITY, 2019-2023 (USD MILLION)

- TABLE 100 GENERATIVE AI MARKET, BY AUDIO & SPEECH MODALITY, 2024-2030 (USD MILLION)

- 7.5.2 TEXT-TO-SPEECH

- TABLE 101 GENERATIVE AI MARKET IN TEXT-TO-SPEECH, BY REGION, 2019-2023 (USD MILLION)

- TABLE 102 GENERATIVE AI MARKET IN TEXT-TO-SPEECH, BY REGION, 2024-2030 (USD MILLION)

- 7.5.3 SPEECH RECOGNITION & TRANSCRIPTION

- TABLE 103 GENERATIVE AI MARKET IN SPEECH RECOGNITION & TRANSCRIPTION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 104 GENERATIVE AI MARKET IN SPEECH RECOGNITION & TRANSCRIPTION, BY REGION, 2024-2030 (USD MILLION)

- 7.5.4 MUSIC GENERATION

- TABLE 105 GENERATIVE AI MARKET IN MUSIC GENERATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 106 GENERATIVE AI MARKET IN MUSIC GENERATION, BY REGION, 2024-2030 (USD MILLION)

- 7.5.5 OTHER AUDIO & SPEECH MODALITIES

- TABLE 107 GENERATIVE AI MARKET IN OTHER AUDIO & SPEECH MODALITIES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 108 GENERATIVE AI MARKET IN OTHER AUDIO & SPEECH MODALITIES, BY REGION, 2024-2030 (USD MILLION)

- 7.6 CODE

- 7.6.1 GENERATIVE AI WITH CODE UNDERSTANDING CAPABILITIES CAN ASSIST IN TASKS SUCH AS SOFTWARE MAINTENANCE, REFACTORING, AND OPTIMIZATION

- TABLE 109 GENERATIVE AI MARKET, BY CODE MODALITY, 2019-2023 (USD MILLION)

- TABLE 110 GENERATIVE AI MARKET, BY CODE MODALITY, 2024-2030 (USD MILLION)

- 7.6.2 CODE GENERATION

- TABLE 111 GENERATIVE AI MARKET IN CODE GENERATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 112 GENERATIVE AI MARKET IN CODE GENERATION, BY REGION, 2024-2030 (USD MILLION)

- 7.6.3 CODE DOCUMENTATION

- TABLE 113 GENERATIVE AI MARKET IN CODE DOCUMENTATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 114 GENERATIVE AI MARKET IN CODE DOCUMENTATION: GENERATIVE AI MARKET, BY REGION, 2024-2030 (USD MILLION)

- 7.6.4 CODE TRANSLATION & TRANSPILATION

- TABLE 115 GENERATIVE AI MARKET IN CODE TRANSLATION & TRANSLATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 116 GENERATIVE AI MARKET IN CODE TRANSLATION & TRANSPILATION, BY REGION, 2024-2030 (USD MILLION)

- 7.6.5 OTHER CODE MODALITIES

- TABLE 117 GENERATIVE AI MARKET IN OTHER CODE MODALITIES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 118 GENERATIVE AI MARKET IN OTHER CODE MODALITIES, BY REGION, 2024-2030 (USD MILLION)

8 GENERATIVE AI MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.1.1 APPLICATION: GENERATIVE AI MARKET DRIVERS

- FIGURE 71 SYNTHETIC DATA MANAGEMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

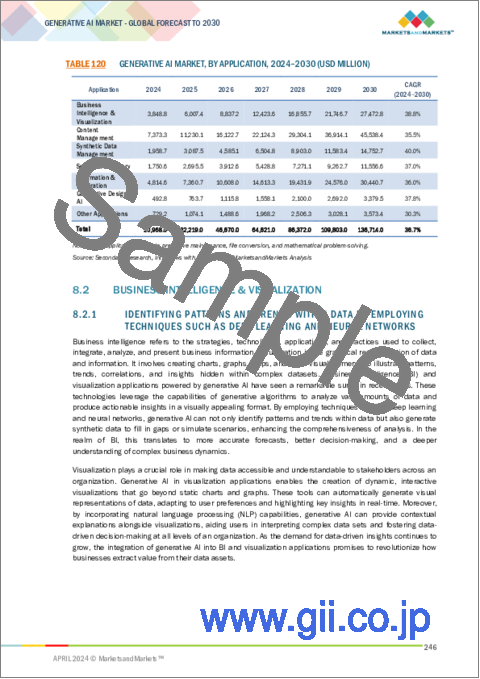

- TABLE 119 GENERATIVE AI MARKET, BY APPLICATION, 2019-2023 (USD MILLION)

- TABLE 120 GENERATIVE AI MARKET, BY APPLICATION, 2024-2030 (USD MILLION)

- 8.2 BUSINESS INTELLIGENCE & VISUALIZATION

- 8.2.1 IDENTIFYING PATTERNS AND TRENDS WITHIN DATA BY EMPLOYING TECHNIQUES SUCH AS DEEP LEARNING AND NEURAL NETWORKS

- TABLE 121 GENERATIVE AI MARKET IN BUSINESS INTELLIGENCE & VISUALIZATION, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 122 GENERATIVE AI MARKET IN BUSINESS INTELLIGENCE & VISUALIZATION, BY VERTICAL, 2024-2030 (USD MILLION)

- TABLE 123 GENERATIVE AI MARKET IN BUSINESS INTELLIGENCE & VISUALIZATION, BY SUBAPPLICATION, 2019-2023 (USD MILLION)

- TABLE 124 GENERATIVE AI MARKET IN BUSINESS INTELLIGENCE & VISUALIZATION, BY SUBAPPLICATION, 2024-2030 (USD MILLION)

- 8.2.2 SALES INTELLIGENCE

- TABLE 125 GENERATIVE AI MARKET IN SALES INTELLIGENCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 126 GENERATIVE AI MARKET IN SALES INTELLIGENCE, BY REGION, 2024-2030 (USD MILLION)

- 8.2.3 MARKETING INTELLIGENCE

- TABLE 127 GENERATIVE AI MARKET IN MARKETING INTELLIGENCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 128 GENERATIVE AI MARKET IN MARKETING INTELLIGENCE, BY REGION, 2024-2030 (USD MILLION)

- 8.2.4 HUMAN RESOURCE INTELLIGENCE

- TABLE 129 GENERATIVE AI MARKET IN HUMAN RESOURCE INTELLIGENCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 130 GENERATIVE AI MARKET IN HUMAN RESOURCE INTELLIGENCE, BY REGION, 2024-2030 (USD MILLION)

- 8.2.5 FINANCE INTELLIGENCE

- TABLE 131 GENERATIVE AI MARKET IN FINANCE INTELLIGENCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 132 GENERATIVE AI MARKET IN FINANCE INTELLIGENCE, BY REGION, 2024-2030 (USD MILLION)

- 8.2.6 OPERATIONS INTELLIGENCE

- TABLE 133 GENERATIVE AI MARKET IN OPERATIONS INTELLIGENCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 134 GENERATIVE AI MARKET IN OPERATIONS INTELLIGENCE, BY REGION, 2024-2030 (USD MILLION)

- 8.3 CONTENT MANAGEMENT

- 8.3.1 IMPROVING CONTENT MANAGEMENT BY OPTIMIZING WORKFLOWS AND ENHANCING SCALABILITY USING GENERATIVE AI

- TABLE 135 GENERATIVE AI MARKET IN CONTENT MANAGEMENT, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 136 GENERATIVE AI MARKET IN CONTENT MANAGEMENT, BY VERTICAL, 2024-2030 (USD MILLION)

- TABLE 137 GENERATIVE AI MARKET IN CONTENT MANAGEMENT, BY SUBAPPLICATION, 2019-2023 (USD MILLION)

- TABLE 138 GENERATIVE AI MARKET IN CONTENT MANAGEMENT, BY SUBAPPLICATION, 2024-2030 (USD MILLION)

- 8.3.2 CONTENT GENERATION

- TABLE 139 GENERATIVE AI MARKET IN CONTENT GENERATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 140 GENERATIVE AI MARKET IN CONTENT GENERATION, BY REGION, 2024-2030 (USD MILLION)

- 8.3.3 CONTENT CURATION, TAGGING, AND CATEGORIZATION

- TABLE 141 GENERATIVE AI MARKET IN CONTENT CURATION, TAGGING, AND CATEGORIZATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 142 GENERATIVE AI MARKET IN CONTENT CURATION, TAGGING, AND CATEGORIZATION, BY REGION, 2024-2030 (USD MILLION)

- 8.3.4 DIGITAL MARKETING

- TABLE 143 GENERATIVE AI MARKET IN DIGITAL MARKETING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 144 GENERATIVE AI MARKET IN DIGITAL MARKETING, BY REGION, 2024-2030 (USD MILLION)

- 8.3.5 MEDIA EDITING

- TABLE 145 GENERATIVE AI MARKET IN MEDIA EDITING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 146 GENERATIVE AI MARKET IN MEDIA EDITING, BY REGION, 2024-2030 (USD MILLION)

- 8.4 SYNTHETIC DATA MANAGEMENT

- 8.4.1 MIMICKING REAL-WORLD DATA DISTRIBUTIONS WITHOUT COMPROMISING INDIVIDUAL PRIVACY BY UTILIZING GANS AND VAES

- TABLE 147 GENERATIVE AI MARKET IN SYNTHETIC DATA MANAGEMENT, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 148 GENERATIVE AI MARKET IN SYNTHETIC DATA MANAGEMENT, BY VERTICAL, 2024-2030 (USD MILLION)

- TABLE 149 GENERATIVE AI MARKET IN SYNTHETIC DATA MANAGEMENT, BY SUBAPPLICATION, 2019-2023 (USD MILLION)

- TABLE 150 GENERATIVE AI MARKET IN SYNTHETIC DATA MANAGEMENT, BY SUBAPPLICATION, 2024-2030 (USD MILLION)

- 8.4.2 SYNTHETIC DATA AUGMENTATION

- TABLE 151 GENERATIVE AI MARKET IN SYNTHETIC DATA AUGMENTATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 152 GENERATIVE AI MARKET IN SYNTHETIC DATA AUGMENTATION, BY REGION, 2024-2030 (USD MILLION)

- 8.4.3 SYNTHETIC DATA TRAINING

- TABLE 153 GENERATIVE AI MARKET IN SYNTHETIC DATA TRAINING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 154 GENERATIVE AI MARKET IN SYNTHETIC DATA TRAINING, BY REGION, 2024-2030 (USD MILLION)

- 8.5 SEARCH & DISCOVERY

- 8.5.1 NEED TO UNCOVER HIDDEN PATTERNS, EXTRACT INSIGHTS, AND GENERATE PERSONALIZED RECOMMENDATIONS

- TABLE 155 GENERATIVE AI MARKET IN SEARCH & DISCOVERY, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 156 GENERATIVE AI MARKET IN SEARCH & DISCOVERY, BY VERTICAL, 2024-2030 (USD MILLION)

- TABLE 157 GENERATIVE AI MARKET IN SEARCH & DISCOVERY, BY SUBAPPLICATION, 2019-2023 (USD MILLION)

- TABLE 158 GENERATIVE AI MARKET IN SEARCH & DISCOVERY, BY SUBAPPLICATION, 2024-2030 (USD MILLION)

- 8.5.2 GENERAL SEARCH

- TABLE 159 GENERATIVE AI MARKET IN GENERAL SEARCH, BY REGION, 2019-2023 (USD MILLION)

- TABLE 160 GENERATIVE AI MARKET IN GENERAL SEARCH, BY REGION, 2024-2030 (USD MILLION)

- 8.5.3 INSIGHT GENERATION

- TABLE 161 GENERATIVE AI MARKET IN INSIGHT GENERATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 162 GENERATIVE AI MARKET IN INSIGHT GENERATION, BY REGION, 2024-2030 (USD MILLION)

- 8.6 AUTOMATION & INTEGRATION

- 8.6.1 STREAMLINING AND ENHANCING VARIOUS PROCESSES WITHIN BUSINESSES BY UTILIZING AUTOMATION & INTEGRATION POWER OF GENERATIVE AI

- TABLE 163 GENERATIVE AI MARKET IN AUTOMATION & INTEGRATION, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 164 GENERATIVE AI MARKET IN AUTOMATION & INTEGRATION, BY VERTICAL, 2024-2030 (USD MILLION)

- TABLE 165 GENERATIVE AI MARKET IN AUTOMATION & INTEGRATION, BY SUBAPPLICATION, 2019-2023 (USD MILLION)

- TABLE 166 GENERATIVE AI MARKET IN AUTOMATION & INTEGRATION, BY SUBAPPLICATION, 2024-2030 (USD MILLION)

- 8.6.2 PERSONALIZATION & RECOMMENDATION SYSTEMS

- TABLE 167 GENERATIVE AI MARKET IN PERSONALIZATION & RECOMMENDATION SYSTEMS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 168 GENERATIVE AI MARKET IN PERSONALIZATION & RECOMMENDATION SYSTEMS, BY REGION, 2024-2030 (USD MILLION)

- 8.6.3 CUSTOMER EXPERIENCE MANAGEMENT

- TABLE 169 GENERATIVE AI MARKET IN CUSTOMER EXPERIENCE MANAGEMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 170 GENERATIVE AI MARKET IN CUSTOMER EXPERIENCE MANAGEMENT, BY REGION, 2024-2030 (USD MILLION)

- 8.6.4 APPLICATION DEVELOPMENT & API INTEGRATION

- TABLE 171 GENERATIVE AI MARKET IN APPLICATION DEVELOPMENT & API INTEGRATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 172 GENERATIVE AI MARKET IN APPLICATION DEVELOPMENT & API INTEGRATION, BY REGION, 2024-2030 (USD MILLION)

- 8.6.5 CYBERSECURITY INTELLIGENCE

- TABLE 173 GENERATIVE AI MARKET IN CYBERSECURITY INTELLIGENCE, BY SUBAPPLICATION, 2019-2023 (USD MILLION)

- TABLE 174 GENERATIVE AI MARKET IN CYBERSECURITY INTELLIGENCE, BY SUBAPPLICATION, 2024-2030 (USD MILLION)

- 8.6.5.1 Fraud Detection & Prevention

- TABLE 175 GENERATIVE AI MARKET IN FRAUD DETECTION & PREVENTION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 176 GENERATIVE AI MARKET IN FRAUD DETECTION & PREVENTION, BY REGION, 2024-2030 (USD MILLION)

- 8.6.5.2 Risk & Compliance Management

- TABLE 177 GENERATIVE AI MARKET IN RISK & COMPLIANCE MANAGEMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 178 GENERATIVE AI MARKET IN RISK & COMPLIANCE MANAGEMENT, BY REGION, 2024-2030 (USD MILLION)

- 8.6.5.3 Automated Patch Management

- TABLE 179 GENERATIVE AI MARKET IN AUTOMATED PATCH MANAGEMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 180 GENERATIVE AI MARKET IN AUTOMATED PATCH MANAGEMENT, BY REGION, 2024-2030 (USD MILLION)

- 8.6.5.4 Digital Forensics & Incident Analysis

- TABLE 181 GENERATIVE AI MARKET IN DIGITAL FORENSICS & INCIDENT ANALYSIS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 182 GENERATIVE AI MARKET IN DIGITAL FORENSICS & INCIDENT ANALYSIS, BY REGION, 2024-2030 (USD MILLION)

- 8.6.5.5 Threat Simulation & Training

- TABLE 183 GENERATIVE AI MARKET IN THREAT SIMULATION & TRAINING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 184 GENERATIVE AI MARKET IN THREAT SIMULATION & TRAINING, BY REGION, 2024-2030 (USD MILLION)

- 8.7 GENERATIVE DESIGN AI

- 8.7.1 ANALYZING VAST AMOUNTS OF DATA AND HARNESSING MACHINE LEARNING ALGORITHMS FOR NUMEROUS DESIGN ITERATIONS

- TABLE 185 GENERATIVE AI MARKET IN GENERATIVE DESIGN AI, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 186 GENERATIVE AI MARKET IN GENERATIVE DESIGN AI, BY VERTICAL, 2024-2030 (USD MILLION)

- TABLE 187 GENERATIVE AI MARKET IN GENERATIVE DESIGN AI, BY SUBAPPLICATION, 2019-2023 (USD MILLION)

- TABLE 188 GENERATIVE AI MARKET IN GENERATIVE DESIGN AI, BY SUBAPPLICATION, 2024-2030 (USD MILLION)

- 8.7.2 DESIGN EXPLORATION & VARIATION

- TABLE 189 GENERATIVE AI MARKET IN DESIGN EXPLORATION & VARIATION, BY REGION, 2019-2023 (USD MILLION)

- TABLE 190 GENERATIVE AI MARKET IN DESIGN EXPLORATION & VARIATION, BY REGION, 2024-2030 (USD MILLION)

- 8.7.3 MODELING & PROTOTYPING

- TABLE 191 GENERATIVE AI MARKET IN MODELING & PROTOTYPING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 192 GENERATIVE AI MARKET IN MODELING & PROTOTYPING, BY REGION, 2024-2030 (USD MILLION)

- 8.7.4 PRODUCT RENDERINGS & VISUAL COLLATERALS

- TABLE 193 GENERATIVE AI MARKET IN PRODUCT RENDERINGS & VISUAL COLLATERALS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 194 GENERATIVE AI MARKET IN PRODUCT RENDERINGS & VISUAL COLLATERALS, BY REGION, 2024-2030 (USD MILLION)

- 8.8 OTHER APPLICATIONS

- TABLE 195 GENERATIVE AI MARKET IN OTHER APPLICATIONS, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 196 GENERATIVE AI MARKET IN OTHER APPLICATIONS, BY VERTICAL, 2024-2030 (USD MILLION)

- TABLE 197 GENERATIVE AI MARKET IN OTHER APPLICATIONS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 198 GENERATIVE AI MARKET IN OTHER APPLICATIONS, BY REGION, 2024-2030 (USD MILLION)

9 GENERATIVE AI MARKET, BY VERTICAL

- 9.1 INTRODUCTION

- 9.1.1 VERTICAL: GENERATIVE AI MARKET DRIVERS

- FIGURE 72 ADOPTION OF GENERATIVE AI IN RETAIL & ECOMMERCE TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 199 GENERATIVE AI MARKET, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 200 GENERATIVE AI MARKET, BY VERTICAL, 2024-2030 (USD MILLION)

- 9.2 MEDIA & ENTERTAINMENT

- 9.2.1 DEMAND FOR HYPER-PERSONALIZED CONTENT EXPERIENCES AND HYPER-REALISTIC VIRTUAL ENVIRONMENTS

- 9.2.2 MEDIA & ENTERTAINMENT: GENERATIVE AI SUCCESS STORIES

- FIGURE 73 MEDIA & ENTERTAINMENT: GENERATIVE AI SUCCESS STORIES

- TABLE 201 GENERATIVE AI MARKET IN MEDIA & ENTERTAINMENT, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 202 GENERATIVE AI MARKET IN MEDIA & ENTERTAINMENT, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 9.2.3 GENERATIVE AI MARKET IN MEDIA & ENTERTAINMENT VERTICAL, BY TEXT MODALITY

- TABLE 203 GENERATIVE AI TEXT MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 204 GENERATIVE AI TEXT MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2024-2030 (USD MILLION)

- 9.2.3.1 Script & Dialogue Generation

- 9.2.3.2 Content Summarization

- 9.2.3.3 Language Translation & Localization

- 9.2.3.4 Interactive Storytelling

- 9.2.3.5 Automated News Generation

- 9.2.4 GENERATIVE AI MARKET IN MEDIA & ENTERTAINMENT VERTICAL, BY VIDEO MODALITY

- TABLE 205 GENERATIVE AI VIDEO MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 206 GENERATIVE AI VIDEO MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2024-2030 (USD MILLION)

- 9.2.4.1 Video Synthesis

- 9.2.4.2 Video Inpainting

- 9.2.4.3 Video Summarization

- 9.2.4.4 Visual Effects Enhancement

- 9.2.4.5 Virtual Set Design

- 9.2.5 GENERATIVE AI MARKET IN MEDIA & ENTERTAINMENT VERTICAL, BY IMAGE MODALITY

- TABLE 207 GENERATIVE AI IMAGE MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 208 GENERATIVE AI IMAGE MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2024-2030 (USD MILLION)

- 9.2.5.1 Content Creation

- 9.2.5.2 Style Transfer

- 9.2.5.3 Face & Character Generation

- 9.2.5.4 Image Super-Resolution

- 9.2.5.5 Automated Thumbnail Generation

- 9.2.6 GENERATIVE AI MARKET IN MEDIA & ENTERTAINMENT VERTICAL, BY CODE MODALITY

- TABLE 209 GENERATIVE AI CODE MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 210 GENERATIVE AI CODE MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2024-2030 (USD MILLION)

- 9.2.6.1 Procedural Content Generation

- 9.2.6.2 Automated Animation Scripting

- 9.2.6.3 Code Comment Generation

- 9.2.6.4 Code Translation

- 9.2.6.5 Code Refactoring Suggestions

- 9.2.7 GENERATIVE AI MARKET IN MEDIA & ENTERTAINMENT VERTICAL, BY AUDIO & SPEECH MODALITY

- TABLE 211 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2019-2023 (USD MILLION)

- TABLE 212 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2024-2030 (USD MILLION)

- 9.2.7.1 Music Composition

- 9.2.7.2 Voice Synthesis

- 9.2.7.3 Sound Effects Generation

- 9.2.7.4 Podcast Automation

- 9.2.7.5 Audio Restoration

- 9.3 BFSI

- 9.3.1 IDENTIFYING PATTERNS OF FRAUDULENT ACTIVITY AND ENHANCING CUSTOMER SERVICE AND SUPPORT USING GENERATIVE AI

- 9.3.2 BFSI: GENERATIVE AI SUCCESS STORIES

- FIGURE 74 BFSI: GENERATIVE AI SUCCESS STORIES

- TABLE 213 GENERATIVE AI MARKET IN BFSI, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 214 GENERATIVE AI MARKET IN BFSI, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 9.3.3 GENERATIVE AI MARKET IN BFSI VERTICAL, BY TEXT MODALITY

- TABLE 215 GENERATIVE AI TEXT MODALITY MARKET IN BFSI, BY REGION, 2019-2023 (USD MILLION)

- TABLE 216 GENERATIVE AI TEXT MODALITY MARKET IN BFSI, BY REGION, 2024-2030 (USD MILLION)

- 9.3.3.1 Automated Customer Support

- 9.3.3.2 Financial Document Summarization

- 9.3.3.3 Sentiment Analysis

- 9.3.3.4 Financial News Generation

- 9.3.3.5 Fraudulent Mail Detection

- 9.3.4 GENERATIVE AI MARKET IN BFSI VERTICAL, BY VIDEO MODALITY

- TABLE 217 GENERATIVE AI VIDEO MODALITY MARKET IN BFSI, BY REGION, 2019-2023 (USD MILLION)

- TABLE 218 GENERATIVE AI VIDEO MODALITY MARKET IN BFSI, BY REGION, 2024-2030 (USD MILLION)

- 9.3.4.1 Automated Video Surveillance

- 9.3.4.2 Virtual Financial Consultation

- 9.3.4.3 Visual-cognitive Credit Assessment

- 9.3.4.4 Interactive Banking Tutorials

- 9.3.5 GENERATIVE AI MARKET IN BFSI VERTICAL, BY IMAGE MODALITY

- TABLE 219 GENERATIVE AI IMAGE MODALITY MARKET IN BFSI, BY REGION, 2019-2023 (USD MILLION)

- TABLE 220 GENERATIVE AI IMAGE MODALITY MARKET IN BFSI, BY REGION, 2024-2030 (USD MILLION)

- 9.3.5.1 Signature Verification

- 9.3.5.2 Transaction Anomaly Detection

- 9.3.5.3 Document Digitization

- 9.3.5.4 Card Fraud Detection

- 9.3.5.5 Customer Identity Verification

- 9.3.6 GENERATIVE AI MARKET IN BFSI VERTICAL, BY CODE MODALITY

- TABLE 221 GENERATIVE AI CODE MODALITY MARKET IN BFSI, BY REGION, 2019-2023 (USD MILLION)

- TABLE 222 GENERATIVE AI CODE MODALITY MARKET IN BFSI, BY REGION, 2024-2030 (USD MILLION)

- 9.3.6.1 Algorithmic Trading Strategies

- 9.3.6.2 Automated Report Generation

- 9.3.6.3 Code Review & Optimization

- 9.3.6.4 Fraud Detection Algorithm Development

- 9.3.6.5 Automated Compliance Checks

- 9.3.7 GENERATIVE AI MARKET IN BFSI VERTICAL, BY AUDIO & SPEECH MODALITY

- TABLE 223 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN BFSI, BY REGION, 2019-2023 (USD MILLION)

- TABLE 224 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN BFSI, BY REGION, 2024-2030 (USD MILLION)

- 9.3.7.1 Financial Data Audio Transcription

- 9.3.7.2 Customer Support & Service

- 9.3.7.3 Automated Meeting Summaries

- 9.3.7.4 Financial Podcast Generation

- 9.3.7.5 Voice-enabled Financial Apps

- 9.4 HEALTHCARE & LIFE SCIENCES

- 9.4.1 REVOLUTIONIZING DRUG DISCOVERY, MEDICAL IMAGING ANALYSIS, AND PERSONALIZED TREATMENT PLANS

- 9.4.2 HEALTHCARE & LIFE SCIENCES: GENERATIVE AI SUCCESS STORIES

- FIGURE 75 HEALTHCARE & LIFE SCIENCES: GENERATIVE AI SUCCESS STORIES

- TABLE 225 GENERATIVE AI MARKET IN HEALTHCARE & LIFE SCIENCES, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 226 GENERATIVE AI MARKET IN HEALTHCARE & LIFE SCIENCES, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 9.4.3 GENERATIVE AI MARKET IN HEALTHCARE & LIFE SCIENCES VERTICAL, BY TEXT MODALITY

- TABLE 227 GENERATIVE AI TEXT MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 228 GENERATIVE AI TEXT MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2024-2030 (USD MILLION)

- 9.4.3.1 Electronic Health Records (EHR)

- 9.4.3.2 Clinical Documentation Generation

- 9.4.3.3 Drug Interaction Prediction

- 9.4.3.4 Medical Literature Summarization

- 9.4.3.5 Patient Communication & Education

- 9.4.4 GENERATIVE AI MARKET IN HEALTHCARE & LIFE SCIENCES VERTICAL, BY VIDEO MODALITY

- TABLE 229 GENERATIVE AI VIDEO MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 230 GENERATIVE AI VIDEO MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2024-2030 (USD MILLION)

- 9.4.4.1 Surgical Procedure Simulation

- 9.4.4.2 Rehabilitation Exercise Generation

- 9.4.4.3 Gait Analysis & Recovery

- 9.4.4.4 Remote Patient Monitoring

- 9.4.4.5 Medical Training Videos

- 9.4.5 GENERATIVE AI MARKET IN HEALTHCARE & LIFE SCIENCES VERTICAL, BY IMAGE MODALITY

- TABLE 231 GENERATIVE AI IMAGE MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 232 GENERATIVE AI IMAGE MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2024-2030 (USD MILLION)

- 9.4.5.1 Synthetic Medical Imaging

- 9.4.5.2 Tumor Detection & Segmentation

- 9.4.5.3 Radiation Therapy Planning

- 9.4.5.4 AR/VR Visualization for Anatomy

- 9.4.5.5 Synthetic Molecular Structure Generation

- 9.4.6 GENERATIVE AI MARKET IN HEALTHCARE & LIFE SCIENCES VERTICAL, BY CODE MODALITY

- TABLE 233 GENERATIVE AI CODE MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 234 GENERATIVE AI CODE MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2024-2030 (USD MILLION)

- 9.4.6.1 Automated Medical Report Generation

- 9.4.6.2 Algorithmic Medical Diagnosis

- 9.4.6.3 Drug Dosage Calculation

- 9.4.6.4 Healthcare Workflow Automation

- 9.4.6.5 Clinical Decision Support Systems

- 9.4.7 GENERATIVE AI MARKET IN HEALTHCARE & LIFE SCIENCES VERTICAL, BY AUDIO & SPEECH MODALITY

- TABLE 235 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 236 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2024-2030 (USD MILLION)

- 9.4.7.1 Voice Assistants for Patients

- 9.4.7.2 Speech Synthesis for Assistive Devices

- 9.4.7.3 Medical Dictation and Transcription

- 9.4.7.4 Speech-to-Text Medical Transcription

- 9.4.7.5 Customized Audiograms

- 9.5 MANUFACTURING

- 9.5.1 TRANSFORMING QUALITY CONTROL IN MANUFACTURING BY ENABLING AUTOMATED INSPECTION AND DEFECT DETECTION

- 9.5.2 MANUFACTURING: GENERATIVE AI SUCCESS STORIES

- FIGURE 76 MANUFACTURING: GENERATIVE AI SUCCESS STORIES

- TABLE 237 GENERATIVE AI MARKET IN MANUFACTURING, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 238 GENERATIVE AI MARKET IN MANUFACTURING, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 9.5.3 GENERATIVE AI MARKET IN MANUFACTURING VERTICAL, BY TEXT MODALITY

- TABLE 239 GENERATIVE AI TEXT MODALITY MARKET IN MANUFACTURING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 240 GENERATIVE AI TEXT MODALITY MARKET IN MANUFACTURING, BY REGION, 2024-2030 (USD MILLION)

- 9.5.3.1 Technical Documentation

- 9.5.3.2 RFQ/RFP Generation

- 9.5.3.3 Automated Email Communication

- 9.5.3.4 Maintenance & Repair Manuals

- 9.5.3.5 Demand Forecasting & Inventory Management

- 9.5.4 GENERATIVE AI MARKET IN MANUFACTURING VERTICAL, BY VIDEO MODALITY

- TABLE 241 GENERATIVE AI VIDEO MODALITY MARKET IN MANUFACTURING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 242 GENERATIVE AI VIDEO MODALITY MARKET IN MANUFACTURING, BY REGION, 2024-2030 (USD MILLION)

- 9.5.4.1 Process Optimization

- 9.5.4.2 Predictive Maintenance

- 9.5.4.3 Robotic Process Control

- 9.5.4.4 Worker Training and Safety

- 9.5.4.5 Supply Chain Visualization

- 9.5.5 GENERATIVE AI MARKET IN MANUFACTURING VERTICAL, BY IMAGE MODALITY

- TABLE 243 GENERATIVE AI IMAGE MODALITY MARKET IN MANUFACTURING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 244 GENERATIVE AI IMAGE MODALITY MARKET IN MANUFACTURING, BY REGION, 2024-2030 (USD MILLION)

- 9.5.5.1 Product Design/3D Prototyping

- 9.5.5.2 Defect Detection

- 9.5.5.3 Customized Manufacturing

- 9.5.5.4 Generative Design

- 9.5.5.5 Visual Inspection and Quality Control

- 9.5.6 GENERATIVE AI MARKET IN MANUFACTURING VERTICAL, BY CODE MODALITY

- TABLE 245 GENERATIVE AI CODE MODALITY MARKET IN MANUFACTURING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 246 GENERATIVE AI CODE MODALITY MARKET IN MANUFACTURING, BY REGION, 2024-2030 (USD MILLION)

- 9.5.6.1 Automated Script Generation

- 9.5.6.2 Digital Twin Simulation

- 9.5.6.3 Data Analysis & Visualization

- 9.5.6.4 IoT Devices Integration

- 9.5.6.5 CNC Machine G-Codes

- 9.5.7 GENERATIVE AI MARKET IN MANUFACTURING VERTICAL, BY AUDIO & SPEECH MODALITY

- TABLE 247 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN MANUFACTURING, BY REGION, 2019-2023 (USD MILLION)

- TABLE 248 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN MANUFACTURING, BY REGION, 2024-2030 (USD MILLION)

- 9.5.7.1 Acoustic Quality Control

- 9.5.7.2 Worker Assistance & Communication

- 9.5.7.3 Real-time Monitoring & Alerts

- 9.5.7.4 Virtual Training & Simulations

- 9.5.7.5 Voice-controlled Interfaces

- 9.6 RETAIL & ECOMMERCE

- 9.6.1 UTILIZING GENERATIVE AI TO CREATE VIRTUAL SHOPPING ASSISTANTS AND CHATBOTS TO INTERACT WITH CUSTOMERS

- 9.6.2 RETAIL & ECOMMERCE: GENERATIVE AI SUCCESS STORIES

- FIGURE 77 RETAIL & ECOMMERCE: GENERATIVE AI SUCCESS STORIES

- TABLE 249 GENERATIVE AI MARKET IN RETAIL & ECOMMERCE, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 250 GENERATIVE AI MARKET IN RETAIL & ECOMMERCE, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 9.6.3 GENERATIVE AI MARKET IN RETAIL & ECOMMERCE VERTICAL, BY TEXT MODALITY

- TABLE 251 GENERATIVE AI TEXT MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 252 GENERATIVE AI TEXT MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2024-2030 (USD MILLION)

- 9.6.3.1 Product Descriptions

- 9.6.3.2 Chatbots and Customer Service

- 9.6.3.3 Social Media Content Creation

- 9.6.3.4 Email Marketing

- 9.6.3.5 Personalized Shopping Recommendations

- 9.6.4 GENERATIVE AI MARKET IN RETAIL & ECOMMERCE VERTICAL, BY VIDEO MODALITY

- TABLE 253 GENERATIVE AI VIDEO MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 254 GENERATIVE AI VIDEO MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2024-2030 (USD MILLION)

- 9.6.4.1 Product Showcase Videos

- 9.6.4.2 Video Advertisements

- 9.6.4.3 Virtual Store Tours

- 9.6.4.4 Instructional Videos

- 9.6.4.5 User-Generated Content Compilation

- 9.6.5 GENERATIVE AI MARKET IN RETAIL & ECOMMERCE VERTICAL, BY IMAGE MODALITY

- TABLE 255 GENERATIVE AI IMAGE MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 256 GENERATIVE AI IMAGE MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2024-2030 (USD MILLION)

- 9.6.5.1 Product Image Generation

- 9.6.5.2 Virtual Try-on

- 9.6.5.3 Interior Design Simulation

- 9.6.5.4 Customized Packaging Design

- 9.6.5.5 Visual Search Enhancement

- 9.6.6 GENERATIVE AI MARKET IN RETAIL & ECOMMERCE VERTICAL, BY CODE MODALITY

- TABLE 257 GENERATIVE AI CODE MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 258 GENERATIVE AI CODE MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2024-2030 (USD MILLION)

- 9.6.6.1 Automated Inventory Management

- 9.6.6.2 Dynamic Pricing Optimization

- 9.6.6.3 Fraud Detection and Prevention

- 9.6.6.4 Supply Chain Optimization

- 9.6.6.5 eCommerce Platform Customization

- 9.6.7 GENERATIVE AI MARKET IN RETAIL & ECOMMERCE VERTICAL, BY AUDIO & SPEECH MODALITY

- TABLE 259 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 260 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN RETAIL & ECOMMERCE, BY REGION, 2024-2030 (USD MILLION)

- 9.6.7.1 Voice Assistants

- 9.6.7.2 Personalized Audio Ads

- 9.6.7.3 Audio Product Guides

- 9.6.7.4 Voice Search Optimization

- 9.6.7.5 Customer Escalation management

- 9.7 TRANSPORTATION & LOGISTICS

- 9.7.1 RISE IN NEED FOR EFFICIENCY, OPTIMIZATION, AND SUSTAINABILITY

- 9.7.2 TRANSPORTATION & LOGISTICS: GENERATIVE AI SUCCESS STORIES

- FIGURE 78 TRANSPORTATION & LOGISTICS: GENERATIVE AI SUCCESS STORIES

- TABLE 261 GENERATIVE AI MARKET IN TRANSPORTATION & LOGISTICS, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 262 GENERATIVE AI MARKET IN TRANSPORTATION & LOGISTICS, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 9.7.3 GENERATIVE AI MARKET IN TRANSPORTATION & LOGISTICS VERTICAL, BY TEXT MODALITY

- TABLE 263 GENERATIVE AI TEXT MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 264 GENERATIVE AI TEXT MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2024-2030 (USD MILLION)

- 9.7.3.1 Supply Chain Risk Assessment

- 9.7.3.2 Spare Parts Documentation

- 9.7.3.3 Incident Reports

- 9.7.3.4 Freight Documentation

- 9.7.3.5 Vehicle Maintenance Logs

- 9.7.4 GENERATIVE AI MARKET IN TRANSPORTATION & LOGISTICS VERTICAL, BY VIDEO MODALITY

- TABLE 265 GENERATIVE AI VIDEO MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 266 GENERATIVE AI VIDEO MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2024-2030 (USD MILLION)

- 9.7.4.1 Surveillance & Security

- 9.7.4.2 Driver Behavior Analysis

- 9.7.4.3 Loading & Unloading Optimization

- 9.7.4.4 Accident Reconstruction

- 9.7.4.5 Parking Management

- 9.7.5 GENERATIVE AI MARKET IN TRANSPORTATION & LOGISTICS VERTICAL, BY IMAGE MODALITY

- TABLE 267 GENERATIVE AI IMAGE MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 268 GENERATIVE AI IMAGE MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2024-2030 (USD MILLION)

- 9.7.5.1 Virtual Test Environments

- 9.7.5.2 Customized Vehicle Personalization

- 9.7.5.3 Damage Inspection

- 9.7.5.4 Route Optimization Visualization

- 9.7.5.5 Traffic Flow Simulation

- 9.7.6 GENERATIVE AI MARKET IN TRANSPORTATION & LOGISTICS VERTICAL, BY CODE MODALITY

- TABLE 269 GENERATIVE AI CODE MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 270 GENERATIVE AI CODE MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2024-2030 (USD MILLION)

- 9.7.6.1 Algorithm Development for Autonomous Vehicles

- 9.7.6.2 Automated Data Processing for Logistics

- 9.7.6.3 Vehicle Control Systems

- 9.7.6.4 Predictive Analytics for Maintenance

- 9.7.6.5 Intelligent Scheduling and Resource Allocation

- 9.7.7 GENERATIVE AI MARKET IN TRANSPORTATION & LOGISTICS VERTICAL, BY AUDIO & SPEECH MODALITY

- TABLE 271 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2019-2023 (USD MILLION)

- TABLE 272 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2024-2030 (USD MILLION)

- 9.7.7.1 Emergency Response and Assistance

- 9.7.7.2 Voice-Enabled Navigation

- 9.7.7.3 Fleet Management & Coordination

- 9.7.7.4 Speech Recognition for Driver Commands

- 9.7.7.5 Hands-Free Data Entry

- 9.8 CONSTRUCTION & REAL ESTATE

- 9.8.1 INTEGRATION OF GENERATIVE AI TO HELP REAL ESTATE FIRMS ATTRACT AND RETAIN TENANTS

- 9.8.2 CONSTRUCTION & REAL ESTATE: GENERATIVE AI SUCCESS STORIES

- FIGURE 79 CONSTRUCTION & REAL ESTATE: GENERATIVE AI SUCCESS STORIES

- TABLE 273 GENERATIVE AI MARKET IN CONSTRUCTION & REAL ESTATE, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 274 GENERATIVE AI MARKET IN CONSTRUCTION & REAL ESTATE, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 9.8.3 GENERATIVE AI MARKET IN CONSTRUCTION & REAL ESTATE VERTICAL, BY TEXT MODALITY

- TABLE 275 GENERATIVE AI TEXT MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 276 GENERATIVE AI TEXT MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2024-2030 (USD MILLION)

- 9.8.3.1 Automated Property Descriptions

- 9.8.3.2 Legal Document Generation

- 9.8.3.3 Project Planning Reports

- 9.8.3.4 Client Communication

- 9.8.3.5 Environmental Impact Assessments

- 9.8.4 GENERATIVE AI MARKET IN CONSTRUCTION & REAL ESTATE VERTICAL, BY VIDEO MODALITY

- TABLE 277 GENERATIVE AI VIDEO MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 278 GENERATIVE AI VIDEO MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2024-2030 (USD MILLION)

- 9.8.4.1 Construction Progress Videos

- 9.8.4.2 Virtual Reality Property Walkthroughs

- 9.8.4.3 Safety Training Videos

- 9.8.4.4 Quality Assurance Inspections

- 9.8.4.5 Property Valuation Videos

- 9.8.5 GENERATIVE AI MARKET IN CONSTRUCTION & REAL ESTATE VERTICAL, BY IMAGE MODALITY

- TABLE 279 GENERATIVE AI IMAGE MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 280 GENERATIVE AI IMAGE MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2024-2030 (USD MILLION)

- 9.8.5.1 Architectural Design Generation

- 9.8.5.2 Facade Visualization

- 9.8.5.3 Interior Layout Suggestions

- 9.8.5.4 Site Progress Monitoring

- 9.8.5.5 Virtual Staging

- 9.8.6 GENERATIVE AI MARKET IN CONSTRUCTION & REAL ESTATE VERTICAL, BY CODE MODALITY

- TABLE 281 GENERATIVE AI CODE MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 282 GENERATIVE AI CODE MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2024-2030 (USD MILLION)

- 9.8.6.1 Automated Building Information Modeling (BIM)

- 9.8.6.2 Construction Workflow Automation

- 9.8.6.3 Generative Design for Structures

- 9.8.6.4 Energy Efficiency Simulations

- 9.8.6.5 Maintenance and Repairs

- 9.8.7 GENERATIVE AI MARKET IN CONSTRUCTION & REAL ESTATE VERTICAL, BY AUDIO & SPEECH MODALITY

- TABLE 283 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2019-2023 (USD MILLION)

- TABLE 284 GENERATIVE AI AUDIO & SPEECH MODALITY MARKET IN CONSTRUCTION & REAL ESTATE, BY REGION, 2024-2030 (USD MILLION)

- 9.8.7.1 Construction Site Monitoring

- 9.8.7.2 Voice-activated Property Tours

- 9.8.7.3 Automated Customer Support Calls

- 9.8.7.4 Occupancy Monitoring

- 9.8.7.5 Equipment Maintenance Alerts

- 9.9 ENERGY & UTILITIES

- 9.9.1 GENERATIVE AI TOOLS TO DETECT OUTAGES AND OFFER QUALITY SERVICES TO RETAIN EXISTING CUSTOMERS

- 9.9.2 ENERGY & UTILITIES: GENERATIVE AI SUCCESS STORIES

- FIGURE 80 ENERGY & UTILITIES: GENERATIVE AI SUCCESS STORIES

- TABLE 285 GENERATIVE AI MARKET IN ENERGY & UTILITIES, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 286 GENERATIVE AI MARKET IN ENERGY & UTILITIES, BY DATA MODALITY, 2024-2030 (USD MILLION)

- 9.9.3 GENERATIVE AI MARKET IN ENERGY & UTILITIES VERTICAL, BY TEXT MODALITY

- TABLE 287 GENERATIVE AI TEXT MODALITY MARKET IN ENERGY & UTILITIES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 288 GENERATIVE AI TEXT MODALITY MARKET IN ENERGY & UTILITIES, BY REGION, 2024-2030 (USD MILLION)

- 9.9.3.1 Energy Consumption Forecasting

- 9.9.3.2 Automated Reporting

- 9.9.3.3 Customer Support & Resolution

- 9.9.3.4 Regulatory Compliance

- 9.9.3.5 Energy Trading Insights

- 9.9.4 GENERATIVE AI MARKET IN ENERGY & UTILITIES VERTICAL, BY VIDEO MODALITY

- TABLE 289 GENERATIVE AI VIDEO MODALITY MARKET IN ENERGY & UTILITIES, BY REGION, 2019-2023 (USD MILLION)

- TABLE 290 GENERATIVE AI VIDEO MODALITY MARKET IN ENERGY & UTILITIES, BY REGION, 2024-2030 (USD MILLION)

- 9.9.4.1 Safety Compliance Monitoring

- 9.9.4.2 Renewable Energy Site Selection

- 9.9.4.3 Real-time Equipment Monitoring

- 9.9.4.4 Energy Theft Detection

- 9.9.4.5 Workforce Training

- 9.9.5 GENERATIVE AI MARKET IN ENERGY & UTILITIES VERTICAL, BY IMAGE MODALITY

- TABLE 291 GENERATIVE AI IMAGE MODALITY MARKET IN ENERGY & UTILITIES, BY REGION, 2019-2023 (USD MILLION)