|

|

市場調査レポート

商品コード

1671384

スマート照明の世界市場:通信技術別、最終用途別、流通チャネル別、オファリング別、設置タイプ別、地域別 - 2030年までの予測Smart Lighting Market by Lights and Luminaire, Lighting Controls, LED Drivers and Ballasts, Sensors, Switches, Gateways, Dimmers, Relay Units, DALI, Power over Ethernet (PoE), Power Line Communications (PLC) and Zigbee - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| スマート照明の世界市場:通信技術別、最終用途別、流通チャネル別、オファリング別、設置タイプ別、地域別 - 2030年までの予測 |

|

出版日: 2025年03月04日

発行: MarketsandMarkets

ページ情報: 英文 305 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

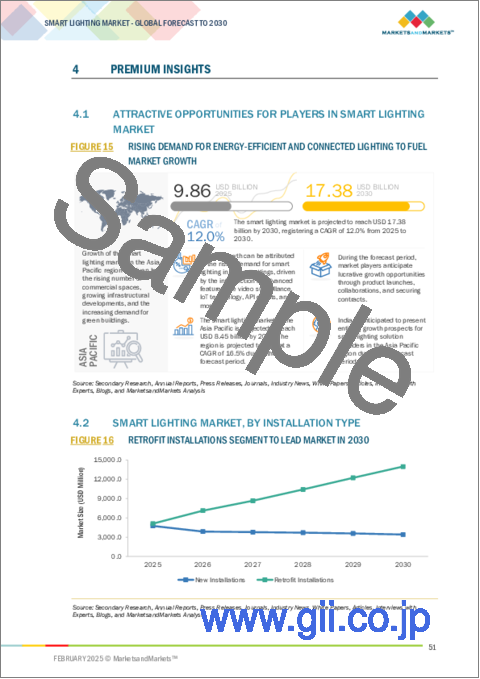

世界のスマート照明の市場規模は、2025年に98億6,000万米ドル、2030年には173億8,000万米ドルに達すると予測されており、予測期間中のCAGRは12.0%と予測されています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント別 | 通信技術別、最終用途別、流通チャネル別、オファリング別、設置タイプ別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

屋外用途におけるLED照明と照明器具の採用拡大、スマート照明におけるデータ分析の浸透拡大、スマートオフィスとスマート小売の新興市場動向、人間中心照明の採用拡大、太陽光発電とハイブリッド型スマート照明ソリューションの開発が市場成長の主な促進要因です。

屋外用途は、都市安全イニシアチブ、スマートシティインフラ、エネルギー効率の高い大量レベルの公共照明配備への投資の増加により、スマート照明市場で最も高いCAGRを示す見込みです。世界中の政府や地方都市当局は、従来の街灯を適応型スマート照明に改修しており、遠隔監視、調光制御、モーション・センシングなどの機能を提供して電力利用を最適化しています。さらに、住宅や商業分野での屋外の安全性向上に対する関心の高まりが、監視システムやIoTベースの監視システムを伴うスマート照明システムの需要を促進しています。

予測期間中、オフライン流通チャネルが市場をリードすると予想されます。スマート照明の消費者は、物理的なチャネルを購入の優先的な選択肢として利用し続けています。大半の消費者は、小売店や販売店を通じてスマート照明製品を購入することを好みますが、これは、品質や選択に関する専門家のアドバイスが付属する製品の直接デモンストレーションを望んでいるからです。複雑なスマート照明ソリューションには専門的な設置サポートが必要なため、オフラインの流通チャネルが顧客満足の基本となります。さらに、請負業者や建築家のような専門的な顧客は、大量注文やオーダーメイドのソリューション、アフターサービスを行う際、オフラインの卸売業者や販売業者に依存する傾向があります。

インドは、急速な都市化、エネルギー効率を支援する政府政策、大規模なスマートシティプロジェクトにより、アジア太平洋のスマート照明市場で最も高いCAGRが見込まれています。インド政府は、エネルギー効率の高い照明を促進するために、いくつかの計画やイニシアチブを立ち上げています。例えば、インド政府の街路照明国家計画(SLNP)では、すでに数百万台のLED街灯が設置されており、スマート照明の採用拡大に向けた強固な基盤となっています。産業・商業分野でのIoTと自動化の普及が進むにつれ、センサーと人工知能ベースの制御メカニズムを組み込んだインテリジェントなコネクテッド照明システムの必要性が高まっています。さらに、LEDの価格が低下し、住民がエネルギー効率の高い照明の利点を認識するにつれて、住宅におけるスマート照明の急速な採用が続いています。

当レポートでは、世界のスマート照明市場について調査し、通信技術別、最終用途別、流通チャネル別、オファリング別、設置タイプ別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 顧客ビジネスに影響を与える動向/混乱

- 価格分析

- バリューチェーン分析

- エコシステム分析

- 投資と資金調達のシナリオ

- 技術分析

- 特許分析

- 貿易分析

- 2025年~2026年の主な会議とイベント

- ケーススタディ分析

- 関税と規制状況

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- AI/生成AIがスマート照明市場に与える影響

第6章 スマート照明市場、通信技術別

- イントロダクション

- 有線

- 無線

第7章 スマート照明市場、最終用途別

- イントロダクション

- 屋内

- 屋外

第8章 スマート照明市場、流通チャネル別

- イントロダクション

- オフライン販売

- オンライン販売

第9章 スマート照明市場、オファリング別

- イントロダクション

- ハードウェア

- ソフトウェア

- サービス

第10章 スマート照明市場、設置タイプ別

- イントロダクション

- 新規設置

- 改造設備

第11章 スマート照明市場、地域別

- イントロダクション

- 南北アメリカ

- 南北アメリカ:マクロ経済見通し

- 北米

- 南米

- 欧州

- 欧州:マクロ経済見通し

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- オランダ

- その他

- アジア太平洋

- アジア太平洋:マクロ経済見通し

- 中国

- 日本

- インド

- オーストラリアとニュージーランド

- 韓国

- その他

- その他の地域

- その他の地域:マクロ経済見通し

- 中東

- アフリカ

第12章 競合情勢

- 概要

- 主要参入企業の戦略/強み、2021年1月~2025年1月

- 収益分析、2020年~2024年

- 市場シェア分析、2024年

- 企業価値評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業、2024年

- 競合シナリオ

第13章 企業プロファイル

- イントロダクション

- 主要参入企業

- SIGNIFY HOLDING

- LEGRAND

- ACUITY BRANDS, INC.

- ZUMTOBEL GROUP

- PANASONIC HOLDINGS CORPORATION

- AMS-OSRAM AG

- HONEYWELL INTERNATIONAL INC.

- WIPRO LIGHTING

- LUTRON ELECTRONICS CO., INC

- CREE LIGHTING USA LLC

- LEDVANCE GMBH

- その他の企業

- HLI SOLUTIONS, INC.

- SAVANT SYSTEMS, INC.

- DIALIGHT

- SCHNEIDER ELECTRIC

- ABB

- LIGHTWAVE

- RAB LIGHTING INC.

- SYNAPSE WIRELESS INC.

- LEVITON MANUFACTURING CO., INC.

- SYSKA

- BUILDING ROBOTICS INC.(SIEMENS COMPANY)

- HELVAR

- LIFX

- SENGLED GMBH

- TVILIGHT PROJECTS B.V.

- NANOLEAF

- UBICQUIA, INC.

- JAQUAR INDIA

- INTER IKEA SYSTEMS B.V.

第14章 付録

List of Tables

- TABLE 1 RISK FACTOR ANALYSIS

- TABLE 2 AVERAGE SELLING PRICE OF HARDWARE TYPE OFFERED KEY PLAYERS, BY OFFERING

- TABLE 3 AVERAGE SELLING PRICE TREND OF SMART LIGHTS AND LUMINAIRES, BY REGION, 2020-2024 (USD)

- TABLE 4 ROLES OF COMPANIES IN SMART LIGHTING ECOSYSTEM

- TABLE 5 SMART LIGHTING MARKET: LIST OF MAJOR PATENTS, 2022-2024

- TABLE 6 IMPORT DATA RELATED TO HS CODE 9405-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 7 EXPORT DATA FOR HS CODE 9405-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 8 SMART LIGHTING MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 9 MFN TARIFF FOR HS CODE 9405-COMPLIANT PRODUCTS, 2023

- TABLE 10 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 SMART LIGHTING MARKET: IMPACT ANALYSIS OF PORTER'S FIVE FORCES

- TABLE 15 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE APPLICATION (%)

- TABLE 16 KEY BUYING CRITERIA, BY END-USE APPLICATION

- TABLE 17 SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 18 SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 19 SMART LIGHTING MARKET FOR WIRED COMMUNICATION TECHNOLOGY, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 20 SMART LIGHTING MARKET FOR WIRED COMMUNICATION TECHNOLOGY, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 21 WIRED: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 22 WIRED: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 23 WIRELESS: SMART LIGHTING MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 24 WIRELESS: SMART LIGHTING MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 25 WIRELESS: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 26 WIRELESS: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 27 SMART LIGHTING MARKET, BY END-USE APPLICATION, 2021-2024 (USD MILLION)

- TABLE 28 SMART LIGHTING MARKET, BY END-USE APPLICATION, 2025-2030 (USD MILLION)

- TABLE 29 INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 30 INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 31 INDOOR SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 32 INDOOR SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33 OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 34 OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 35 OUTDOOR SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 36 OUTDOOR SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37 SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2021-2024 (USD MILLION)

- TABLE 38 SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 39 OFFLINE SALES: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 40 OFFLINE SALES: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 41 ONLINE SALES: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 42 ONLINE SALES: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 43 SMART LIGHTING MARKET, BY OFFERING, 2021-2024 (USD MILLION)

- TABLE 44 SMART LIGHTING MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 45 HARDWARE: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 46 HARDWARE: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 47 SMART LIGHTING MARKET, BY HARDWARE, 2021-2024 (USD MILLION)

- TABLE 48 SMART LIGHTING MARKET, BY HARDWARE, 2025-2030 (USD MILLION)

- TABLE 49 LIGHTING CONTROLS: SMART LIGHTING MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 50 LIGHTING CONTROLS: SMART LIGHTING MARKET, BY COMPONENT, 2025-2030 (USD MILLION)

- TABLE 51 LIGHTING CONTROLS: SMART LIGHTING MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 52 LIGHTING CONTROLS: SMART LIGHTING MARKET, BY COMPONENT, 2025-2030 (THOUSAND UNITS)

- TABLE 53 SOFTWARE: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 54 SOFTWARE: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 55 SERVICES: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 56 SERVICES: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 57 SMART LIGHTING MARKET FOR SERVICES, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 58 SMART LIGHTING MARKET FOR SERVICES, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 59 SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 60 SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 61 SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 62 SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 63 AMERICAS: SMART LIGHTING MARKET, BY SUB-REGION, 2021-2024 (USD MILLION)

- TABLE 64 AMERICAS: SMART LIGHTING MARKET, BY SUB-REGION, 2025-2030 (USD MILLION)

- TABLE 65 AMERICAS: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 66 AMERICAS: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 67 AMERICAS: SMART LIGHTING MARKET, BY OFFERING, 2021-2024 (USD MILLION)

- TABLE 68 AMERICAS: SMART LIGHTING MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 69 AMERICAS: SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 70 AMERICAS: SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 71 AMERICAS: SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2021-2024 (USD MILLION)

- TABLE 72 AMERICAS: SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 73 AMERICAS: SMART LIGHTING MARKET, BY END-USE APPLICATION, 2021-2024 (USD MILLION)

- TABLE 74 AMERICAS: SMART LIGHTING MARKET, BY END-USE APPLICATION, 2025-2030 (USD MILLION)

- TABLE 75 AMERICAS: INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 76 AMERICAS: INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 77 AMERICAS: OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 78 AMERICAS: OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 79 NORTH AMERICA: SMART LIGHTING MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 80 NORTH AMERICA: SMART LIGHTING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 81 NORTH AMERICA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 82 NORTH AMERICA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 83 US: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 84 US: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 85 CANADA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 86 CANADA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 87 MEXICO: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 88 MEXICO: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 89 SOUTH AMERICA: SMART LIGHTING MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 90 SOUTH AMERICA: SMART LIGHTING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 91 SOUTH AMERICA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 92 SOUTH AMERICA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 93 BRAZIL: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 94 BRAZIL: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 95 ARGENTINA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 96 ARGENTINA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 97 REST OF SOUTH AMERICA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 98 REST OF SOUTH AMERICA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 99 EUROPE: SMART LIGHTING MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 100 EUROPE: SMART LIGHTING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 101 EUROPE: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 102 EUROPE: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 103 EUROPE: SMART LIGHTING MARKET, BY OFFERING, 2021-2024 (USD MILLION)

- TABLE 104 EUROPE: SMART LIGHTING MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 105 EUROPE: SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 106 EUROPE: SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 107 EUROPE: SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2021-2024 (USD MILLION)

- TABLE 108 EUROPE: SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 109 EUROPE: SMART LIGHTING MARKET, BY END-USE APPLICATION, 2021-2024 (USD MILLION)

- TABLE 110 EUROPE: SMART LIGHTING MARKET, BY END-USE APPLICATION, 2025-2030 (USD MILLION)

- TABLE 111 EUROPE: INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 112 EUROPE: INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 113 EUROPE: OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 114 EUROPE: OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 115 GERMANY: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 116 GERMANY: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 117 FRANCE: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 118 FRANCE: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 119 UK: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 120 UK: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 121 ITALY: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 122 ITALY: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 123 SPAIN: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 124 SPAIN: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 125 NETHERLANDS: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 126 NETHERLANDS: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 127 REST OF EUROPE: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 128 REST OF EUROPE: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 129 ASIA PACIFIC: SMART LIGHTING MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 130 ASIA PACIFIC: SMART LIGHTING MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 131 ASIA PACIFIC: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 132 ASIA PACIFIC: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 133 ASIA PACIFIC: SMART LIGHTING MARKET, BY OFFERING, 2021-2024 (USD MILLION)

- TABLE 134 ASIA PACIFIC: SMART LIGHTING MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 135 ASIA PACIFIC: SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 136 ASIA PACIFIC: SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 137 ASIA PACIFIC: SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2021-2024 (USD MILLION)

- TABLE 138 ASIA PACIFIC: SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 139 ASIA PACIFIC: SMART LIGHTING MARKET, BY END-USE APPLICATION, 2021-2024 (USD MILLION)

- TABLE 140 ASIA PACIFIC: SMART LIGHTING MARKET, BY END-USE APPLICATION, 2025-2030 (USD MILLION)

- TABLE 141 ASIA PACIFIC: INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 142 ASIA PACIFIC: INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 143 ASIA PACIFIC: OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 144 ASIA PACIFIC: OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 145 CHINA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 146 CHINA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 147 JAPAN: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 148 JAPAN: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 149 INDIA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 150 INDIA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 151 AUSTRALIA & NEW ZEALAND: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 152 AUSTRALIA & NEW ZEALAND: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 153 SOUTH KOREA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 154 SOUTH KOREA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 155 REST OF ASIA PACIFIC: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 156 REST OF ASIA PACIFIC: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 157 ROW: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 158 ROW: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 159 ROW: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 160 ROW: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 161 ROW: SMART LIGHTING MARKET, BY OFFERING, 2021-2024 (USD MILLION)

- TABLE 162 ROW: SMART LIGHTING MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 163 ROW: SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2021-2024 (USD MILLION)

- TABLE 164 ROW: SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 165 ROW: SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2021-2024 (USD MILLION)

- TABLE 166 ROW: SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 167 ROW: SMART LIGHTING MARKET, BY END-USE APPLICATION, 2021-2024 (USD MILLION)

- TABLE 168 ROW: SMART LIGHTING MARKET, BY END-USE APPLICATION, 2025-2030 (USD MILLION)

- TABLE 169 ROW: INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 170 ROW: INDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 171 ROW: OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 172 ROW: OUTDOOR SMART LIGHTING MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 173 MIDDLE EAST: SMART LIGHTING MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 174 MIDDLE EAST: SMART LIGHTING MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 175 MIDDLE EAST: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 176 MIDDLE EAST: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 177 GCC COUNTRIES: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 178 GCC COUNTRIES: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 179 REST OF MIDDLE EAST: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 180 REST OF MIDDLE EAST: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 181 AFRICA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2021-2024 (USD MILLION)

- TABLE 182 AFRICA: SMART LIGHTING MARKET, BY INSTALLATION TYPE, 2025-2030 (USD MILLION)

- TABLE 183 SMART LIGHTING MARKET: KEY STRATEGIES ADOPTED BY LEADING PLAYERS, JANUARY 2021-JANUARY 2025

- TABLE 184 SMART LIGHTING MARKET: DEGREE OF COMPETITION

- TABLE 185 SMART LIGHTING MARKET: REGION FOOTPRINT

- TABLE 186 SMART LIGHTING MARKET: INSTALLATION TYPE FOOTPRINT

- TABLE 187 SMART LIGHTING MARKET: OFFERING FOOTPRINT

- TABLE 188 SMART LIGHTING MARKET: END-USE APPLICATION FOOTPRINT

- TABLE 189 SMART LIGHTING MARKET: COMMUNICATION TECHNOLOGY FOOTPRINT

- TABLE 190 SMART LIGHTING MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 191 SMART LIGHTING MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 192 SMART LIGHTING MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, APRIL 2020-JANUARY 2025

- TABLE 193 SMART LIGHTING MARKET: DEALS, APRIL 2020-JANUARY 2025

- TABLE 194 SMART LIGHTING MARKET: EXPANSIONS, APRIL 2020-JANUARY 2025

- TABLE 195 SIGNIFY HOLDING: COMPANY OVERVIEW

- TABLE 196 SIGNIFY HOLDING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 197 SIGNIFY HOLDING: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 198 SIGNIFY HOLDING: DEALS

- TABLE 199 LEGRAND: COMPANY OVERVIEW

- TABLE 200 LEGRAND: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 201 LEGRAND: PRODUCT LAUNCHES /DEVELOPMENTS

- TABLE 202 LEGRAND: DEALS

- TABLE 203 ACUITY BRANDS, INC.: COMPANY OVERVIEW

- TABLE 204 ACUITY BRANDS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 205 ACUITY BRANDS, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 206 ACUITY BRANDS, INC.: DEALS

- TABLE 207 ZUMTOBEL GROUP: COMPANY OVERVIEW

- TABLE 208 ZUMTOBEL GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 209 ZUMTOBEL GROUP: DEALS

- TABLE 210 PANASONIC HOLDINGS CORPORATION: COMPANY OVERVIEW

- TABLE 211 PANASONIC HOLDINGS CORPORATION: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 212 PANASONIC HOLDINGS CORPORATION: EXPANSIONS

- TABLE 213 AMS-OSRAM AG: COMPANY OVERVIEW

- TABLE 214 AMS-OSRAM AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 215 AMS-OSRAM AG: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 216 AMS-OSRAM AG: DEALS

- TABLE 217 HONEYWELL INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 218 HONEYWELL INTERNATIONAL INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 219 HONEYWELL INTERNATIONAL INC.: DEALS

- TABLE 220 WIPRO LIGHTING: COMPANY OVERVIEW

- TABLE 221 WIPRO LIGHTING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 222 WIPRO LIGHTING: DEALS

- TABLE 223 WIPRO LIGHTING: EXPANSIONS

- TABLE 224 LUTRON ELECTRONICS CO., INC: COMPANY OVERVIEW

- TABLE 225 LUTRON ELECTRONICS CO., INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 226 LUTRON ELECTRONICS CO., INC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 227 CREE LIGHTING USA LLC: COMPANY OVERVIEW

- TABLE 228 CREE LIGHTING USA LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 229 CREE LIGHTING USA LLC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 230 LEDVANCE GMBH: COMPANY OVERVIEW

- TABLE 231 LEDVANCE GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 232 LEDVANCE GMBH: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 233 LEDVANCE GMBH: DEALS

List of Figures

- FIGURE 1 SMART LIGHTING MARKET SEGMENTATION

- FIGURE 2 SMART LIGHTING MARKET: RESEARCH DESIGN

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE) - REVENUE GENERATED BY KEY PLAYERS

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2 (DEMAND SIDE) -BOTTOM-UP ESTIMATION BASED ON REGION

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 7 DATA TRIANGULATION

- FIGURE 8 GLOBAL SMART LIGHTING MARKET, 2021-2030 (USD MILLION)

- FIGURE 9 HARDWARE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 10 WIRELESS COMMUNICATION TECHNOLOGY TO RECORD HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 11 RETROFIT INSTALLATIONS TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 12 INDOOR APPLICATION TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 13 ONLINE SALES TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 14 ASIA PACIFIC HELD LARGEST SHARE OF SMART LIGHTING MARKET IN 2024

- FIGURE 15 RISING DEMAND FOR ENERGY-EFFICIENT AND CONNECTED LIGHTING TO FUEL MARKET GROWTH

- FIGURE 16 RETROFIT INSTALLATIONS SEGMENT TO LEAD MARKET IN 2030

- FIGURE 17 INDOOR SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 18 HARDWARE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 19 WIRED COMMUNICATION TECHNOLOGY SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 20 OFFLINE SALES SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 21 ASIA PACIFIC TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 22 SMART LIGHTING MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 23 SMART LIGHTING MARKET DRIVERS: IMPACT ANALYSIS

- FIGURE 24 SMART LIGHTING MARKET RESTRAINTS: IMPACT ANALYSIS

- FIGURE 25 SMART LIGHTING MARKET OPPORTUNITIES: IMPACT ANALYSIS

- FIGURE 26 SMART LIGHTING MARKET CHALLENGES: IMPACT ANALYSIS

- FIGURE 27 TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

- FIGURE 28 AVERAGE SELLING PRICE OF HARDWARE TYPE OFFERED KEY PLAYERS, BY OFFERING

- FIGURE 29 AVERAGE SELLING PRICE TREND OF LIGHTS AND LUMINAIRES, BY REGION, 2020-2024 (USD)

- FIGURE 30 SMART LIGHTING MARKET: VALUE CHAIN ANALYSIS

- FIGURE 31 SMART LIGHTING ECOSYSTEM ANALYSIS

- FIGURE 32 SMART LIGHTING MARKET: INVESTMENT AND FUNDING SCENARIO FOR STARTUPS, 2020-2024 (USD MILLION)

- FIGURE 33 SMART LIGHTING MARKET: PATENT ANALYSIS, 2015-2024

- FIGURE 34 IMPORT DATA FOR HS CODE 9405-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2019-2023 (USD MILLION)

- FIGURE 35 EXPORT DATA RELATED TO HS CODE 9405-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2019-2023 (USD MILLION)

- FIGURE 36 SMART LIGHTING MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 37 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE APPLICATION

- FIGURE 38 KEY BUYING CRITERIA, BY END-USE APPLICATION

- FIGURE 39 SMART LIGHTING MARKET: IMPACT OF AI/GEN AI

- FIGURE 40 WIRELESS COMMUNICATION TECHNOLOGY TO REGISTER HIGH GROWTH DURING FORECAST PERIOD

- FIGURE 41 INDOOR APPLICATION TO DOMINATE MARKET IN 2030

- FIGURE 42 OFFLINE SALES SEGMENT TO HOLD LARGER MARKET SHARE IN 2025

- FIGURE 43 HARDWARE SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 44 LIGHTS AND LUMINAIRES SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 45 RETROFIT INSTALLATIONS TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 46 ASIA PACIFIC TO LEAD SMART LIGHTING MARKET FROM 2025 TO 2030

- FIGURE 47 SMART LIGHTING MARKET IN INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 48 AMERICAS: SMART LIGHTING MARKET SNAPSHOT

- FIGURE 49 EUROPE: SMART LIGHTING MARKET SNAPSHOT

- FIGURE 50 ASIA PACIFIC: SMART LIGHTING MARKET SNAPSHOT

- FIGURE 51 ROW: SMART LIGHTING MARKET SNAPSHOT

- FIGURE 52 SMART LIGHTING MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024 (USD BILLION)

- FIGURE 53 SMART LIGHTING MARKET SHARE ANALYSIS, 2024

- FIGURE 54 SMART LIGHTING MARKET: COMPANY VALUATION, 2024

- FIGURE 55 SMART LIGHTING MARKET: FINANCIAL METRICS, 2024

- FIGURE 56 SMART LIGHTING MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 57 SMART LIGHTING MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 58 SMART LIGHTING MARKET: COMPANY FOOTPRINT

- FIGURE 59 SMART LIGHTING MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 60 SIGNIFY HOLDING: COMPANY SNAPSHOT

- FIGURE 61 LEGRAND: COMPANY SNAPSHOT

- FIGURE 62 ACUITY BRANDS, INC.: COMPANY SNAPSHOT

- FIGURE 63 ZUMTOBEL GROUP: COMPANY SNAPSHOT

- FIGURE 64 PANASONIC HOLDINGS CORPORATION: COMPANY SNAPSHOT

- FIGURE 65 AMS-OSRAM AG: COMPANY SNAPSHOT

- FIGURE 66 HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

The global smart lighting market was valued at USD 9.86 billion in 2025 and is projected to reach USD 17.38 billion by 2030; it is expected to register a CAGR of 12.0% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, By Installation Type, By Communication Technology, By End-use Application, By Distribution Channel, By Region |

| Regions covered | North America, Europe, APAC, RoW |

The increasing adoption of LED lighting and luminaires in outdoor applications, growing penetration of data analytics in smart lighting, emerging smart offices and smart retail trends, rising adoption of human-centric lighting, and development of solar-powered and hybrid smart lighting solutions are the major drivers contributing to the market growth.

"The outdoor application segment is expected to grow at the highest CAGR during the forecast period"

Outdoor application is expected to witness the highest CAGR in the smart lighting market due to increased investments in urban safety initiatives, smart city infrastructure, and mass-level public lighting deployments that are energy-efficient. Governments and local city authorities across the world are retrofitting conventional streetlights with adaptive smart lighting, offering features like remote monitoring, dimmable control, and motion sensing to optimize power utilization. Further, growing concern about enhancing outdoor safety in residential and commercial sectors is driving the demand for smart lighting systems accompanied by surveillance and IoT-based monitoring systems.

"Offline distribution channel segment likely to lead the smart lighting market during the forecast period"

The offline distribution channel is expected to lead the market during the forecast period. Smart lighting consumers continue to use physical channels as their preferred choice for purchase as these channels enable personal interactions while providing firsthand product examinations. The majority of customers prefer to buy smart lighting products through retail outlets or dealerships because they want a firsthand demonstration of products that come with expert advice on quality and selection. Complex smart lighting solutions need specialized installation support which makes offline distribution channels fundamental for customer satisfaction. Moreover, professional customers, like contractors and architects, tend to depend on offline wholesalers and distributors when making bulk orders, tailor-made solutions, and after-sales service.

"India is likely to grow at the highest CAGR during the forecast period"

India is expected to have the highest CAGR in the Asia Pacific smart lighting market owing to fast urbanization, government policies supporting energy efficiency, and smart city projects on a large scale. The government of India has launched several schemes and initiatives to promote energy-efficient lighting; for instance, the Indian government's Street Lighting National Programme (SLNP) has already seen millions of LED streetlights installed, providing a solid base for increased adoption of smart lighting. The increasing IoT and automation penetration in industrial and commercial sectors drive the need for intelligent connected lighting systems that incorporate sensors and artificial intelligence-based control mechanisms. Moreover, the rapid adoption of smart lighting in residential properties continues as LED prices decrease and residents realize the benefits of energy-efficient lighting.

Breakdown of primaries

The study contains insights from various industry experts, ranging from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type - Tier 1 - 55%, Tier 2 - 25%, Tier 3 - 20%

- By Designation- Directors - 50%, Managers - 30%, Others - 20%

- By Region-North America - 40%, Europe - 35%, Asia Pacific - 20%, RoW - 05%

The smart lighting market is dominated by a few globally established players: Signify Holding (Netherlands), Acuity Brands, Inc. (US), Panasonic Holdings Corporation (Japan), Legrand (France), Zumtobel Group (Austria), and ams-OSRAM AG (Austria), among others. The study includes an in-depth competitive analysis of these key players in the smart lighting market, with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the smart lighting market and forecasts its size by offering, installation type, end-use application, distribution channel, communication technology, and region. The report also discusses the drivers, restraints, opportunities, and challenges pertaining to the market. It gives a detailed view of the market across four main regions-Americas, Europe, Asia Pacific, and RoW. Value chain analysis has been included in the report, along with the key players and their competitive analysis in the smart lighting ecosystem.

Key Benefits to Buy the Report:

- Analysis of key drivers (rising adoption of LED lighting and luminaire in outdoor applications, increasing penetration of data analytics in smart lighting, rising smart city initiatives across the globe, advances in AI and Edge computing, establishment of standard and digital protocols by authorized bodies, growing demand for IoT-integrated smart lighting), Restraint (cybersecurity concerns associated with internet-connected lighting systems, difficulties associated with retrofitting traditional lighting systems), Opportunity (development of solar-powered and hybrid smart lighting solutions, emerging smart office and smart retail trends, growing adoption of human-centric lighting, growing adoption of PoE-based lighting solutions in commercial and healthcare applications, increasing demand for personalized lighting control solutions), Challenges (high upfront cost of equipment and accessories, interoperability and compatibility issues)

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the smart lighting market

- Market Development: Comprehensive information about lucrative markets - the report analyses the smart lighting market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the smart lighting market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and offerings of leading players like Signify Holding (Netherlands), Acuity Brands, Inc. (US), Panasonic Holdings Corporation (Japan), Legrand (France), Zumtobel Group (Austria), ams-OSRAM AG (Austria), LEDVANCE GmbH (Germany, and Honeywell International (US) among others in the smart lighting market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.1.2 Key secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key participants in primary interviews

- 2.1.2.3 Breakdown of primary interviews

- 2.1.2.4 Insights of industry experts

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to derive market size using bottom-up analysis

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to derive market size using top-down analysis

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET SHARE ESTIMATION

- 2.4 DATA TRIANGULATION

- 2.5 RISK ASSESSMENT

- 2.6 RESEARCH ASSUMPTIONS AND LIMITATIONS

- 2.6.1 RESEARCH ASSUMPTIONS

- 2.6.2 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SMART LIGHTING MARKET

- 4.2 SMART LIGHTING MARKET, BY INSTALLATION TYPE

- 4.3 SMART LIGHTING MARKET, BY END-USE APPLICATION

- 4.4 SMART LIGHTING MARKET, BY OFFERING

- 4.5 SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY

- 4.6 SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL

- 4.7 SMART LIGHTING MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising smart city initiatives globally

- 5.2.1.2 Advancements in Artificial Intelligence (AI) and edge computing technologies

- 5.2.1.3 Establishment of standard and digital protocols by authorized bodies

- 5.2.1.4 Growing demand for Internet of Things (IoT)-integrated smart lighting solutions

- 5.2.1.5 Rising adoption of LED lights and luminaires in outdoor applications

- 5.2.1.6 Increasing incorporation of data analytics into smart lighting

- 5.2.2 RESTRAINTS

- 5.2.2.1 Cybersecurity concerns associated with internet-connected lighting systems

- 5.2.2.2 Difficulties associated with retrofitting of traditional lighting infrastructure

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Development of solar-powered and hybrid smart lighting solutions

- 5.2.3.2 Emerging smart office and smart retail trends

- 5.2.3.3 Rising adoption of human-centric lighting solutions

- 5.2.3.4 Growing adoption of Power over Ethernet (PoE)-based lighting solutions in commercial and healthcare applications

- 5.2.3.5 Increasing demand for personalized lighting control solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 High upfront costs of equipment and accessories

- 5.2.4.2 Interoperability and compatibility issues

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY OFFERING, 2024

- 5.4.2 AVERAGE SELLING PRICE TREND, BY REGION, 2020-2024

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- 5.7 INVESTMENT AND FUNDING SCENARIO

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Internet of Things (IoT)

- 5.8.1.2 Communication protocols

- 5.8.1.3 Smart sensors

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.8.2.2 Light fidelity (Li-Fi)

- 5.8.2.3 Geofencing technology

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Building management system (BMS)

- 5.8.3.2 5G infrastructure

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PATENT ANALYSIS

- 5.10 TRADE ANALYSIS

- 5.10.1 IMPORT SCENARIO (HS CODE 9405)

- 5.10.2 EXPORT SCENARIO (HS CODE 9405)

- 5.11 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 ULINE USES CREE LIGHTING LUMINAIRES INTEGRATED WITH SYNAPSE SIMPLYSNAP CONTROLS TO HELP ACHIEVE OPERATIONAL EXCELLENCE AND RELIABILITY

- 5.12.2 GERMAN MUNICIPALITY IMPLEMENTS SIGNIFY HOLDING'S BRIGHTSITES SOLUTION TO ADVANCE SMART CITY GOALS

- 5.12.3 HONEYWELL INTERNATIONAL INC. ESTABLISHES NEW AIRFIELD GROUND LIGHT MANUFACTURING FACILITY IN INDIA

- 5.13 TARIFF AND REGULATORY LANDSCAPE

- 5.13.1 TARIFF ANALYSIS

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.3 REGULATIONS

- 5.13.3.1 Restriction of Hazardous Substances (ROHS) and Waste Electrical and Electronic Equipment (WEEE)

- 5.13.3.2 Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH)

- 5.13.3.3 United Nations Framework Convention on Climate Change (UNFCCC)

- 5.13.3.4 General Data Protection Regulation (GDPR)

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.14.2 THREAT OF NEW ENTRANTS

- 5.14.3 THREAT OF SUBSTITUTES

- 5.14.4 BARGAINING POWER OF BUYERS

- 5.14.5 BARGAINING POWER OF SUPPLIERS

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 IMPACT OF AI/GEN AI ON SMART LIGHTING MARKET

6 SMART LIGHTING MARKET, BY COMMUNICATION TECHNOLOGY

- 6.1 INTRODUCTION

- 6.2 WIRED

- 6.2.1 DALI

- 6.2.1.1 Offers versatility and greater energy savings

- 6.2.2 POWER OVER ETHERNET (POE)

- 6.2.2.1 Used to power devices through Ethernet cables

- 6.2.3 POWER LINE COMMUNICATIONS (PLCS)

- 6.2.3.1 Help improve connectivity between lighting solutions

- 6.2.4 WIRED HYBRID PROTOCOLS

- 6.2.4.1 Ensure security and isolation of control systems

- 6.2.1 DALI

- 6.3 WIRELESS

- 6.3.1 ZIGBEE

- 6.3.1.1 Serves low-power wireless IoT networks

- 6.3.2 WI-FI

- 6.3.2.1 Facilitates direct device-to-device connections

- 6.3.3 BLE

- 6.3.3.1 Enhances user mobility by eliminating cables

- 6.3.4 ENOCEAN

- 6.3.4.1 Enables prolonged communication without need for recharging

- 6.3.5 6LOWPAN

- 6.3.5.1 Facilitates communication for devices with limited processing capabilities

- 6.3.6 WIRELESS HYBRID PROTOCOLS

- 6.3.6.1 Improve data transmission through proactive and reactive routing

- 6.3.1 ZIGBEE

7 SMART LIGHTING MARKET, BY END-USE APPLICATION

- 7.1 INTRODUCTION

- 7.2 INDOOR

- 7.2.1 COMMERCIAL

- 7.2.1.1 Increasing demand from corporate offices to drive growth

- 7.2.2 INDUSTRIAL

- 7.2.2.1 Rising demand for enhanced safety and productivity to drive market

- 7.2.3 RESIDENTIAL

- 7.2.3.1 Growing demand for smart home solutions to boost market

- 7.2.4 OTHERS

- 7.2.1 COMMERCIAL

- 7.3 OUTDOOR

- 7.3.1 HIGHWAYS AND ROADWAYS LIGHTING

- 7.3.1.1 Growing need for connected street lighting systems to fuel growth

- 7.3.2 ARCHITECTURAL LIGHTING

- 7.3.2.1 Increasing proliferation of human-centric lighting to drive demand

- 7.3.3 LIGHTING FOR PUBLIC PLACES

- 7.3.3.1 Growing need to enhance safety and security to drive growth

- 7.3.1 HIGHWAYS AND ROADWAYS LIGHTING

8 SMART LIGHTING MARKET, BY DISTRIBUTION CHANNEL

- 8.1 INTRODUCTION

- 8.2 OFFLINE SALES

- 8.2.1 EXPANSION OF SMART CITY PROJECTS AND COMMERCIAL RETROFITTING TO FUEL DEMAND

- 8.3 ONLINE SALES

- 8.3.1 WIDER PRODUCT AVAILABILITY, COMPETITIVE PRICING, CONVENIENCE, AND DETAILED PRODUCT COMPARISONS TO DRIVE MARKET

9 SMART LIGHTING MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.2 HARDWARE

- 9.2.1 LIGHTS AND LUMINAIRES

- 9.2.1.1 Increasing adoption of energy-efficient LED luminaires, rising smart home penetration, and large-scale infrastructure projects to boost demand

- 9.2.2 LIGHTING CONTROLS

- 9.2.2.1 LED drivers and ballasts

- 9.2.2.1.1 Ability of programmable and adaptive LED to enhance energy efficiency and extend the lifespan of LED luminaires to drive growth

- 9.2.2.2 Sensors

- 9.2.2.2.1 Increasing adoption in residential applications to drive growth

- 9.2.2.3 Switches

- 9.2.2.3.1 Easy lighting control to increase demand

- 9.2.2.4 Dimmers

- 9.2.2.4.1 Enhanced flexibility to drive market

- 9.2.2.5 Relay units

- 9.2.2.5.1 Improved lighting control to drive market

- 9.2.2.6 Gateways

- 9.2.2.6.1 High demand for facilitating communication between controllers to drive market

- 9.2.2.1 LED drivers and ballasts

- 9.2.1 LIGHTS AND LUMINAIRES

- 9.3 SOFTWARE

- 9.3.1 ABILITY TO OPTIMIZE ENERGY CONSUMPTION WHILE ENHANCING USER CONVENIENCE TO DRIVE MARKET

- 9.4 SERVICES

- 9.4.1 PRE-INSTALLATION SERVICES

- 9.4.1.1 Help tailor lighting solutions to suit customer requirements

- 9.4.2 POST-INSTALLATION SERVICES

- 9.4.2.1 Prolonged lifespan of luminaires and lamps while optimizing energy consumption and efficiency to drive demand

- 9.4.1 PRE-INSTALLATION SERVICES

10 SMART LIGHTING MARKET, BY INSTALLATION TYPE

- 10.1 INTRODUCTION

- 10.2 NEW INSTALLATIONS

- 10.2.1 INCREASING ADOPTION OF SMART CITY INITIATIVES AND STRINGENT ENERGY EFFICIENCY REGULATIONS TO DRIVE GROWTH

- 10.3 RETROFIT INSTALLATIONS

- 10.3.1 REDUCED DOWNTIME AND INSTALLATION COSTS DUE TO COMPATIBILITY WITH EXISTING LIGHTING TO DRIVE ADOPTION

11 SMART LIGHTING MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 AMERICAS

- 11.2.1 AMERICAS: MACROECONOMIC OUTLOOK

- 11.2.2 NORTH AMERICA

- 11.2.2.1 US

- 11.2.2.1.1 Burgeoning demand for energy-efficient lighting technologies to drive market

- 11.2.2.2 Canada

- 11.2.2.2.1 Rising demand in commercial and industrial sectors to drive growth

- 11.2.2.3 Mexico

- 11.2.2.3.1 Development of smart cities and growing utilization of wireless technologies to boost demand

- 11.2.2.1 US

- 11.2.3 SOUTH AMERICA

- 11.2.3.1 Brazil

- 11.2.3.1.1 Government policies and large-scale urban modernization projects to drive growth

- 11.2.3.2 Argentina

- 11.2.3.2.1 Rising need to replace traditional lamps with energy-efficient alternatives to fuel demand

- 11.2.3.3 Rest of South America

- 11.2.3.1 Brazil

- 11.3 EUROPE

- 11.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 11.3.2 GERMANY

- 11.3.2.1 Increasing demand from commercial sector to drive market

- 11.3.3 FRANCE

- 11.3.3.1 Need for sustainable lighting in public spaces to fuel market

- 11.3.4 UK

- 11.3.4.1 Growing demand from public and private spaces to propel market

- 11.3.5 ITALY

- 11.3.5.1 Resurgence of construction industry to boost demand

- 11.3.6 SPAIN

- 11.3.6.1 Emission reduction goals to drive market

- 11.3.7 NETHERLANDS

- 11.3.7.1 Government initiatives promoting energy-efficient lighting to drive growth

- 11.3.8 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 11.4.2 CHINA

- 11.4.2.1 Rising construction activities to accelerate demand

- 11.4.3 JAPAN

- 11.4.3.1 Growing focus on smart city development to propel market

- 11.4.4 INDIA

- 11.4.4.1 Increasing demand from construction sector to drive growth

- 11.4.5 AUSTRALIA & NEW ZEALAND

- 11.4.5.1 Growing focus on sustainability initiatives to boost market

- 11.4.6 SOUTH KOREA

- 11.4.6.1 Growing demand from commercial buildings and residential developments to fuel growth

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 ROW

- 11.5.1 ROW: MACROECONOMIC OUTLOOK

- 11.5.2 MIDDLE EAST

- 11.5.2.1 Demand for connected urban environments to drive market

- 11.5.2.2 GCC Countries

- 11.5.2.3 Rest of the Middle East

- 11.5.3 AFRICA

- 11.5.3.1 Increasing investments in infrastructure and renewable energy to drive market

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2021- JANUARY 2025

- 12.3 REVENUE ANALYSIS, 2020-2024

- 12.4 MARKET SHARE ANALYSIS, 2024

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.5.1 COMPANY VALUATION

- 12.5.2 FINANCIAL METRICS

- 12.6 BRAND/PRODUCT COMPARISON

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Installation type footprint

- 12.7.5.4 Offering footprint

- 12.7.5.5 End-use application footprint

- 12.7.5.6 Communication technology footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS

- 13.2.1 SIGNIFY HOLDING

- 13.2.1.1 Business overview

- 13.2.1.2 Products/Solutions/Services offered

- 13.2.1.3 Recent developments

- 13.2.1.3.1 Product launches/developments

- 13.2.1.3.2 Deals

- 13.2.1.4 MnM view

- 13.2.1.4.1 Key strengths

- 13.2.1.4.2 Strategic choices

- 13.2.1.4.3 Weaknesses and competitive threats

- 13.2.2 LEGRAND

- 13.2.2.1 Business overview

- 13.2.2.2 Products/Solutions/Services offered

- 13.2.2.3 Recent developments

- 13.2.2.3.1 Product launches/Developments

- 13.2.2.3.2 Deals

- 13.2.2.4 MnM view

- 13.2.2.4.1 Key strengths

- 13.2.2.4.2 Strategic choices

- 13.2.2.4.3 Weaknesses and competitive threats

- 13.2.3 ACUITY BRANDS, INC.

- 13.2.3.1 Business overview

- 13.2.3.2 Products/Solutions/Services offered

- 13.2.3.3 Recent developments

- 13.2.3.3.1 Product launches/developments

- 13.2.3.3.2 Deals

- 13.2.3.4 MnM view

- 13.2.3.4.1 Key strengths

- 13.2.3.4.2 Strategic choices

- 13.2.3.4.3 Weaknesses and competitive threats

- 13.2.4 ZUMTOBEL GROUP

- 13.2.4.1 Business overview

- 13.2.4.2 Products/Solutions/Services offered

- 13.2.4.3 Recent developments

- 13.2.4.3.1 Deals

- 13.2.4.4 MnM view

- 13.2.4.4.1 Key strengths

- 13.2.4.4.2 Strategic choices

- 13.2.4.4.3 Weaknesses and competitive threats

- 13.2.5 PANASONIC HOLDINGS CORPORATION

- 13.2.5.1 Business overview

- 13.2.5.2 Products/Solutions/Services offered

- 13.2.5.3 Recent developments

- 13.2.5.3.1 Expansions

- 13.2.5.4 MnM view

- 13.2.5.4.1 Key strengths

- 13.2.5.4.2 Strategic choices

- 13.2.5.4.3 Weaknesses and competitive threats

- 13.2.6 AMS-OSRAM AG

- 13.2.6.1 Business overview

- 13.2.6.2 Products/Solutions/Services offered

- 13.2.6.3 Recent developments

- 13.2.6.3.1 Product launches/developments

- 13.2.6.3.2 Deals

- 13.2.7 HONEYWELL INTERNATIONAL INC.

- 13.2.7.1 Business overview

- 13.2.7.2 Products/Solutions/Services offered

- 13.2.7.3 Recent developments

- 13.2.7.3.1 Deals

- 13.2.8 WIPRO LIGHTING

- 13.2.8.1 Business overview

- 13.2.8.2 Products/Solutions/Services offered

- 13.2.8.3 Recent developments

- 13.2.8.3.1 Deals

- 13.2.8.3.2 Expansions

- 13.2.9 LUTRON ELECTRONICS CO., INC

- 13.2.9.1 Business overview

- 13.2.9.2 Products/Solutions/Services offered

- 13.2.9.3 Recent developments

- 13.2.9.3.1 Product launches/developments

- 13.2.10 CREE LIGHTING USA LLC

- 13.2.10.1 Business overview

- 13.2.10.2 Products/Solutions/Services offered

- 13.2.10.3 Recent developments

- 13.2.10.3.1 Product launches/developments

- 13.2.11 LEDVANCE GMBH

- 13.2.11.1 Business overview

- 13.2.11.2 Products/Solutions/Services offered

- 13.2.11.3 Recent developments

- 13.2.11.3.1 Product launches/developments

- 13.2.11.3.2 Deals

- 13.2.1 SIGNIFY HOLDING

- 13.3 OTHER PLAYERS

- 13.3.1 HLI SOLUTIONS, INC.

- 13.3.2 SAVANT SYSTEMS, INC.

- 13.3.3 DIALIGHT

- 13.3.4 SCHNEIDER ELECTRIC

- 13.3.5 ABB

- 13.3.6 LIGHTWAVE

- 13.3.7 RAB LIGHTING INC.

- 13.3.8 SYNAPSE WIRELESS INC.

- 13.3.9 LEVITON MANUFACTURING CO., INC.

- 13.3.10 SYSKA

- 13.3.11 BUILDING ROBOTICS INC. (SIEMENS COMPANY)

- 13.3.12 HELVAR

- 13.3.13 LIFX

- 13.3.14 SENGLED GMBH

- 13.3.15 TVILIGHT PROJECTS B.V.

- 13.3.16 NANOLEAF

- 13.3.17 UBICQUIA, INC.

- 13.3.18 JAQUAR INDIA

- 13.3.19 INTER IKEA SYSTEMS B.V.

14 APPENDIX

- 14.1 INSIGHTS FROM INDUSTRY EXPERTS

- 14.2 DISCUSSION GUIDE

- 14.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.4 CUSTOMIZATION OPTIONS

- 14.5 RELATED REPORTS

- 14.6 AUTHOR DETAILS