|

|

市場調査レポート

商品コード

1473660

スチールファイバーの世界市場:タイプ別、製造プロセス別、用途別、地域別 - 予測(~2029年)Steel Fiber Market by Type (Hooked, Straight, Deformed, Crimped), Manufacturing Process (Cold Drawn, Cut Wire, Melt Extract, Slit Sheet), Application (Concrete Reinforcements, Composite Reinforcements, Refractories), & Region- Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| スチールファイバーの世界市場:タイプ別、製造プロセス別、用途別、地域別 - 予測(~2029年) |

|

出版日: 2024年04月25日

発行: MarketsandMarkets

ページ情報: 英文 233 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界のスチールファイバーの市場規模は、2024年の19億6,000万米ドルから、予測期間中は4.5%のCAGRで推移し、2029年には24億4,000万米ドルの規模に成長すると予測されています。

スチールファイバーは適応性が高く、価格も手頃で、コンクリート、複合材料、耐火物など補強が必要なさまざまな用途に適しています。フック付きスチールファイバーは、多くの補強用途でもっとも好まれる選択肢です。フック付きスチールファイバーは、鉄筋コンクリートのひび割れ抵抗性を高め、耐久性を向上させる機械的特性を持っています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020-2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024-2029年 |

| 単位 | 金額 (米ドル)・数量 (キロトン) |

| セグメント | タイプ・製造プロセス・用途別 |

| 対象地域 | 北米・アジア太平洋・ラテンアメリカ・中東・アフリカ |

タイプ別では、ストレートタイプが金額ベースで2番目に高いCAGRを記録:

ストレートスチールファイバーは、工業用床材、舗装、吹付けコンクリート、トンネル覆工、プレキャストコンクリート部材など、幅広い補強用途で一般的に使用されています。世界中で建築やインフラプロジェクトが増加しているため、建設業界ではスチールファイバーの需要が徐々に高まっています。

用途別では、複合材料の部門が金額ベースでもっとも高いCAGRを記録する:

同部門は、自動車や航空宇宙など、さまざまなエンドユーザー産業における複合材料の需要増加に牽引され、成長が見込まれています。スチールファイバーは、さまざまな産業や用途における複合材料の機械的特性を高める上で重要な役割を果たします。スチールファイバーをセラミック、ポリマーなどの異なるマトリックス材料と組み合わせることで、エンジニアは特定の性能要件を満たすために複合材料を調整することができます。

地域別では、アジア太平洋地域が予測期間中に最大のCAGRを記録する:

アジア太平洋地域は、スチールファイバーの市場としてもっとも急成長しています。同地域のスチールファイバー市場は、急速な都市化と、同地域の多くの国々におけるインフラ開発への政府投資の増加によって牽引されています。欧米市場の経済の縮小と飽和に伴い、市場はアジア太平洋にシフトしています。世界銀行によると、この地域は建設産業が急速に発展しており、建設支出の約40%を占めているため、スチールファイバーメーカーはこの地域をターゲットとしています。

当レポートでは、世界のスチールファイバーの市場を調査し、市場概要、市場影響因子および市場機会の分析、技術・特許の動向、法規制環境、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ポーターのファイブフォース分析

- エコシステム分析

- 価格分析

- 貿易分析

- サプライチェーン分析

- バリューチェーン分析

- 流通経路

- 技術分析

- 主なステークホルダーと購入基準

- 特許分析

- 規制状況

- 主な会議とイベント

- ケーススタディ分析

- 顧客ビジネスに影響を与える動向とディスラプション

- 投資と資金調達のシナリオ

第6章 スチールファイバー市場:タイプ別

- フック付き

- ストレート

- 変形

- クリンプ

- その他

第7章 スチールファイバー市場:製造プロセス別

- 冷間引抜

- カットワイヤー

- スリットシート

- 溶融抽出

- その他

第8章 スチールファイバー市場:用途別

- コンクリート補強

- 複合材料補強

- 耐火物

- その他

第9章 スチールファイバー市場:地域別

- 北米

- アジア太平洋

- 欧州

- ラテンアメリカ

- 中東・アフリカ

第10章 競合情勢

- 主要企業の戦略/有力企業

- 収益分析

- 市場シェア分析

- ブランド/製品比較分析

- 企業評価マトリックス:主要企業

- 企業評価マトリックス:スタートアップ/中小企業

- スチールファイバー製造業者の評価と財務指標

- 競合シナリオと動向

第11章 企業プロファイル

- 主要企業

- BEKAERT

- ARCELORMITTAL

- NIPPON SEISEN CO., LTD.

- FIBROMETALS

- SIKA AG

- JIANGSU SHAGANG GROUP CO., LTD.

- ZHEJIANG BOEN METAL PRODUCTS CO., LTD

- GREEN STEEL GROUP

- SPAJIC DOO

- KOSTEEL CO., LTD.

- SEVERSTAL

- ENVIROMESH PTY LTD.

- HUNAN SHUANGXING STEEL FIBER CO., LTD.

- KERAKOLL SPA

- その他の企業

- INTRAMICRON, INC.

- PRECISION DRAWELL

- STEWOLS INDIA PVT. LTD.

- KASTURI METAL COMPOSITES LTD.

- HEBEI SWIIT METALLIC FIBER CO., LTD.

- NIKKO TECHNO, LTD.

- ISW CORPORATION

- DELTA STUD WELD

- NYCON

- THE EUCLID CHEMICAL COMPANY

第12章 付録

The Steel Fiber Market is estimated at USD 1.96 billion in 2024 and is projected to reach USD 2.44 billion by 2029, at a CAGR of 4.5% from 2024 to 2029. Steel fibers are more adaptable, affordable, and suitable for a range of applications where reinforcing is required like concrete, composites, and refractories. Hooked steel fibers are the most favored option for many reinforcement applications. It has mechanical properties that increase the crack resistance of the reinforced concrete and make it more durable.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Million), Volume (Kiloton) |

| Segments | Equipment Type, Agriculture Tractors Tires, By Power Output, Agriculture Tractors Tracks, By Power Output, Industrial Equipment, By Type, Tire Type, OTR Tires for Construction Equipment, By Tire Type, Rim Size, Retreading, By Process, Retreading, By Application, By Application, Aftermarket, and By Equipment Type |

| Regions covered | Europe, North America, Asia Pacific, Latin America, Middle East, and Africa |

''In terms of value, Straight steel fiber type to register the second highest CAGR in the overall Steel Fiber Market.''

Straight steel fibers are well-known for their consistent and uniform shape along their entire length that helps the steel fibers to align randomly within the concrete mix, depending on the mixing process and the flow characteristics of the concrete. Straight steel fibers are commonly used in a wide range of reinforcement applications including industrial flooring, pavements, shotcrete, tunnel linings, and precast concrete elements. There is gradually increasing demand of steel fibers in the construction industry as the building and infrastructure projects are increasing all around the world.

''In terms of value, composite application to register the highest CAGR in the overall Steel Fiber Market.''

The market for steel fiber in the composite application is expected to grow, driven by the increasing demand for composites in various end use industries like automotive and aerospace. Steel fibers play an important role in enhancing the mechanical properties of composite materials across various industries and applications. By combining steel fibers with different matrix materials like ceramics, polymer, and others, engineers can tailor composite materials to meet specific performance requirements.

"During the forecast period, the Steel Fiber Market in Asia Pacific region is to register the highest CAGR."

Asia Pacific is the fastest-growing market for steel fibers. The market for steel fibers in the region is driven by the rapid urbanization and increasing investments from government in infrastructure development in many countries in this region. With economic contraction and saturation in the European and North American markets, the market is shifting to Asia Pacific. Manufacturers of steel fibers are targeting this region as it has a rapidly advancing construction industry, accounting for approximately 40% of the construction spending, according to the World Bank.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 40%, Tier 2- 33%, and Tier 3- 27%

- By Designation- C Level- 50%, Director Level- 30%, and Executives- 20%

- By Region- North America- 15%, Europe- 50%, Asia Pacific (APAC) - 20%, South America -10%, Middle East & Africa -5%.

The report provides a comprehensive analysis of company profiles:

Prominent companies include Bekaert (Belgium), ArcelorMittal (Luxembourg), Nippon Seisen (Japan), Fibrometals (Romania), Sika AG (Switzerland), Jiangsu Shagang Group (China), Zhejiang Boen Metal Products Co., Ltd. (China), Green Steel Group (Italy), Spajic Doo (Serbia), Kosteel Co., Ltd. (South Korea), Severstal (Russia), Enviromesh Pty ltd. (Australia), Hunan Shuanxing Steel Fiber Co., Ltd. (China), and Kerakoll SPA (Italy).

Research Coverage

This research report categorizes the Steel Fiber Market, By Type (Hooked, Straight, Deformed, Crimped, and Others), By Manufacturing Process (Cut Wires, Cold Drawn, Slit Sheet, Melt Extract and Others), By Application (Concrete, Composites, and Refractories), and Region (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The scope of the report includes detailed information about the major factors influencing the growth of the Steel Fiber Market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions, and services, key strategies, contracts, partnerships, and agreements. New product and service launches, mergers and acquisitions, and recent developments in the Steel Fiber Market are all covered. This report includes a competitive analysis of upcoming startups in the Steel Fiber Market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall Steel Fiber Market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing demand for steel fibers in construction and building industry, high tensile and shear strength compared to synthetic fibers, and rising demand for steel fibers in automotive composites), restraints (surge in use of glass and synthetic fibers, and high cost of steel fibers over traditional reinforcement materials), opportunities (the research and advancements in manufacturing technologies present opportunities to develop new and improved steel fibers, and growing emphasis on sustainable construction and building materials), and challenges (susceptibility of steel fibers to corrosion, and need for uniform mixing and handling of steel fibers) influencing the growth of the Steel Fiber Market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the Steel Fiber Market

- Market Development: Comprehensive information about lucrative markets - the report analyses the Steel Fiber Market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the Steel Fiber Market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like include Bekaert (Belgium), ArcelorMittal (Luxembourg), Nippon Seisen (Japan), Fibrometals (Romania), Sika AG (Switzerland), Jiangsu Shagang Group (China), Zhejiang Boen Metal Products Co., Ltd. (China), Green Steel Group (Italy), Spajic Doo (Serbia), Kosteel Co., Ltd. (South Korea), Severstal (Russia), Enviromesh Pty ltd. (Australia), Hunan Shuanxing Steel Fiber Co., Ltd. (China), and Kerakoll SPA (Italy) among others in the steel fiber market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- FIGURE 1 STEEL FIBER MARKET SEGMENTATION

- 1.3.1 INCLUSIONS & EXCLUSIONS

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.9 IMPACT OF RECESSION

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 STEEL FIBER MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key primary participants

- 2.1.2.3 Breakdown of primary interviews

- 2.1.2.4 Key industry insights

- 2.2 RECESSION IMPACT

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.4 BASE NUMBER CALCULATION

- 2.4.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- FIGURE 5 METHODOLOGY FOR SUPPLY-SIDE SIZING OF STEEL FIBER MARKET

- 2.4.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- FIGURE 6 METHODOLOGY FOR DEMAND-SIDE SIZING OF STEEL FIBER MARKET

- 2.5 GROWTH FORECAST

- 2.5.1 SUPPLY SIDE

- 2.5.2 DEMAND SIDE

- 2.6 DATA TRIANGULATION

- FIGURE 7 STEEL FIBER MARKET: DATA TRIANGULATION

- 2.7 FACTOR ANALYSIS

- 2.8 RESEARCH ASSUMPTIONS

- 2.9 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

- FIGURE 8 HOOKED TYPE RECORDED HIGHEST GROWTH IN 2023

- FIGURE 9 COLD-DRAWN PROCESS ACCOUNTED FOR LARGEST SHARE IN 2023

- FIGURE 10 CONCRETE REINFORCEMENT APPLICATION DOMINATED STEEL FIBER MARKET IN 2023

- FIGURE 11 CHINA LED MARKET DURING FORECAST PERIOD

- FIGURE 12 ASIA PACIFIC DOMINATED MARKET IN 2023

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN STEEL FIBER MARKET

- FIGURE 13 HIGH DEMAND FROM END-USE INDUSTRIES TO DRIVE MARKET

- 4.2 STEEL FIBER MARKET, BY TYPE

- FIGURE 14 HOOKED TYPE DOMINATED OVERALL MARKET IN 2023

- 4.3 STEEL FIBER MARKET, BY MANUFACTURING PROCESS

- FIGURE 15 COLD-DRAWN PROCESS DOMINATED OVERALL MARKET IN 2023

- 4.4 STEEL FIBER MARKET, BY APPLICATION

- FIGURE 16 CONCRETE REINFORCEMENT SEGMENT RECORDED HIGHEST GROWTH IN 2023

- 4.5 STEEL FIBER MARKET, BY KEY COUNTRY

- FIGURE 17 MARKET IN CHINA TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 18 DYNAMICS OF STEEL FIBER MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing demand for steel fibers in construction & building industry

- 5.2.1.2 High tensile and shear strengths compared to synthetic fibers

- 5.2.1.3 Rising demand for steel fibers in automotive composites

- 5.2.2 RESTRAINTS

- 5.2.2.1 Surge in use of glass and synthetic fibers

- 5.2.2.2 High cost of steel fibers over traditional reinforcement materials

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Advancements in manufacturing technologies

- 5.2.3.2 Growing emphasis on sustainable construction and building materials

- 5.2.4 CHALLENGES

- 5.2.4.1 Susceptibility of steel fibers to corrosion

- 5.2.4.2 Need for uniform mixing and handling of steel fibers

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 19 STEEL FIBER MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- TABLE 1 STEEL FIBER MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- FIGURE 20 STEEL FIBER MARKET: ECOSYSTEM

- FIGURE 21 STEEL FIBER MARKET: MARKET MAP

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- FIGURE 22 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR TOP THREE APPLICATIONS (USD/KG)

- 5.5.2 AVERAGE SELLING PRICE TREND, BY TYPE

- FIGURE 23 AVERAGE SELLING PRICE TREND, BY TYPE

- TABLE 2 AVERAGE SELLING PRICE, BY TYPE

- 5.5.3 AVERAGE SELLING PRICE TREND, BY REGION

- TABLE 3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO FOR HS CODE 732599

- FIGURE 24 IMPORT FOR HS CODE 732599, BY KEY COUNTRY, 2019-2022 (USD MILLION)

- FIGURE 25 IMPORT FOR HS CODE 732599, BY KEY COUNTRY, 2019-2022 (TON)

- TABLE 4 LEADING IMPORTING COUNTRIES FOR HS CODE 732599 IN 2022

- 5.6.2 EXPORT SCENARIO FOR HS CODE 732599

- FIGURE 26 EXPORT FOR HS CODE 732599, BY KEY COUNTRY, 2019-2022 (USD MILLION)

- FIGURE 27 EXPORT FOR HS CODE 732599, BY KEY COUNTRY, 2019-2022 (TON)

- TABLE 5 LEADING EXPORTING COUNTRIES FOR HS CODE 732599 IN 2022

- 5.7 SUPPLY CHAIN ANALYSIS

- TABLE 6 STEEL FIBER MARKET: SUPPLY CHAIN ANALYSIS

- 5.7.1 RAW MATERIALS

- FIGURE 28 LEADING STEEL FIBER RAW MATERIAL MANUFACTURERS AND SUPPLIERS

- 5.7.2 PRODUCT MANUFACTURERS

- FIGURE 29 LEADING PRODUCT MANUFACTURERS

- 5.7.3 END USERS

- FIGURE 30 MAJOR END USERS OF STEEL FIBERS

- 5.8 VALUE CHAIN ANALYSIS

- FIGURE 31 STEEL FIBER MARKET: VALUE CHAIN ANALYSIS

- 5.9 DISTRIBUTION CHANNEL

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGY

- 5.10.1.1 Steel fiber manufacturing process

- 5.10.1 KEY TECHNOLOGY

- 5.11 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 32 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- TABLE 7 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- 5.11.2 BUYING CRITERIA

- FIGURE 33 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- TABLE 8 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- 5.12 PATENT ANALYSIS

- 5.12.1 INTRODUCTION

- 5.12.2 METHODOLOGY

- 5.12.3 DOCUMENT TYPES

- TABLE 9 STEEL FIBER MARKET: GLOBAL PATENT COUNT

- FIGURE 34 GLOBAL PATENT ANALYSIS, BY DOCUMENT TYPE

- FIGURE 35 GLOBAL PATENT PUBLICATION TREND ANALYSIS IN LAST 10 YEARS

- 5.12.4 INSIGHTS

- 5.12.5 LEGAL STATUS OF PATENTS

- FIGURE 36 STEEL FIBER MARKET: LEGAL STATUS OF PATENTS

- 5.12.6 JURISDICTION ANALYSIS

- FIGURE 37 GLOBAL JURISDICTION ANALYSIS

- 5.12.7 TOP APPLICANTS

- FIGURE 38 STATE GRID CORP CHINA ACCOUNTED FOR HIGHEST PATENT COUNT, 2014-2024

- 5.12.8 PATENTS BY STATE GRID CORP CHINA

- 5.12.9 PATENTS BY UNIV SHENYANG JIANZHU

- 5.12.10 PATENTS BY UNIV SOUTHEAST

- 5.12.11 TOP 10 PATENT OWNERS (US) IN LAST 10 YEARS

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATIONS IN STEEL FIBER MARKET

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 REST OF WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14 KEY CONFERENCES & EVENTS IN 2024-2025

- TABLE 14 STEEL FIBER MARKET: KEY CONFERENCES & EVENTS, 2024-2025

- 5.15 CASE STUDY ANALYSIS

- 5.15.1 CASE STUDY 1: ARCELORMITTAL LAUNCHED CARBON NEUTRAL STEEL FIBER PRODUCT RANGE.

- 5.15.2 CASE STUDY 2: BEKAERT PARTNERED WITH ALMASA FOR STEEL WIRE ACTIVITIES IN US

- 5.15.3 CASE STUDY 3: SIKA AG EXPANDED ITS OPERATIONS IN ASIA PACIFIC AND NORTH AMERICA

- 5.16 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 39 REVENUE SHIFT OF STEEL FIBERS

- 5.17 INVESTMENT AND FUNDING SCENARIO

- FIGURE 40 INVESTOR DEALS AND FUNDING IN STEEL FIBERS

- FIGURE 41 PROMINENT STEEL FIBER MANUFACTURERS IN 2024 (USD BILLION)

6 STEEL FIBER MARKET, BY TYPE

- 6.1 INTRODUCTION

- FIGURE 42 HOOKED STEEL FIBER TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 15 STEEL FIBER MARKET, BY TYPE, 2020-2029 (USD MILLION)

- TABLE 16 STEEL FIBER MARKET, BY TYPE, 2020-2029 (KILOTON)

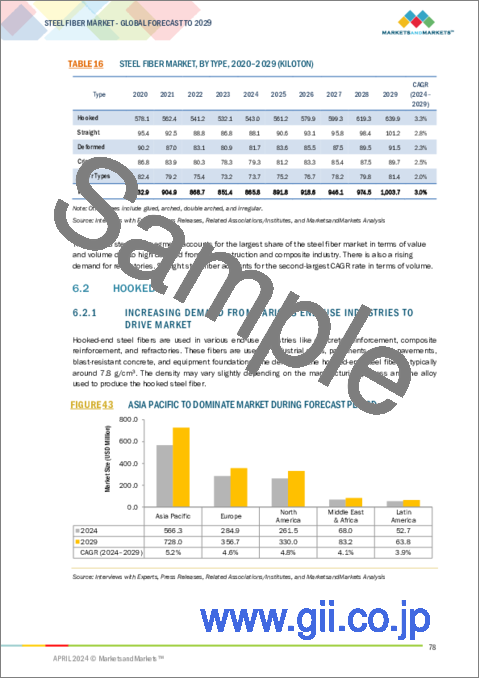

- 6.2 HOOKED

- 6.2.1 INCREASING DEMAND FROM VARIOUS END-USE INDUSTRIES TO DRIVE MARKET

- FIGURE 43 ASIA PACIFIC TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 17 HOOKED: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 18 HOOKED: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 6.3 STRAIGHT

- 6.3.1 RISING DEMAND FROM CONSTRUCTION SECTOR TO DRIVE MARKET

- FIGURE 44 ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- TABLE 19 STRAIGHT: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 20 STRAIGHT: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 6.4 DEFORMED

- 6.4.1 WIDE USE IN CONCRETE APPLICATIONS TO FUEL MARKET

- FIGURE 45 ASIA PACIFIC TO BE FASTEST-GROWING DEFORMED STEEL FIBER MARKET DURING FORECAST PERIOD

- TABLE 21 DEFORMED: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 22 DEFORMED: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 6.5 CRIMPED

- 6.5.1 RISE IN CONSTRUCTION ACTIVITIES IN EMERGING ECONOMIES TO DRIVE MARKET

- FIGURE 46 ASIA PACIFIC TO BE FASTEST-GROWING CRIMPED STEEL FIBER MARKET DURING FORECAST PERIOD

- TABLE 23 CRIMPED: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 24 CRIMPED: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 6.6 OTHER TYPES

- FIGURE 47 ASIA PACIFIC TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 25 OTHER TYPES: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 26 OTHER TYPES: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

7 STEEL FIBER MARKET, BY MANUFACTURING PROCESS

- 7.1 INTRODUCTION

- FIGURE 48 COLD DRAWN PROCESS TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 27 STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (USD MILLION)

- TABLE 28 STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (KILOTON)

- 7.2 COLD DRAWN

- 7.2.1 INCREASING DEMAND IN PRODUCTION OF HOOKED STEEL FIBERS TO DRIVE MARKET

- TABLE 29 COLD DRAWN: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 30 COLD DRAWN: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 7.3 CUT WIRE

- 7.3.1 INFRASTRUCTURE DEVELOPMENT TO DRIVE MARKET

- TABLE 31 CUT WIRE: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 32 CUT WIRE: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 7.4 SLIT SHEET

- 7.4.1 WIDE DEPLOYMENT IN CONCRETE REINFORCEMENT APPLICATIONS TO DRIVE MARKET

- TABLE 33 SLIT SHEET: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 34 SLIT SHEET: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 7.5 MELT EXTRACT

- 7.5.1 INCREASING DEMAND FOR REFRACTORY CASTABLE REINFORCEMENT FIBERS TO DRIVE MARKET

- TABLE 35 MELT EXTRACT: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 36 MELT EXTRACT: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 7.6 OTHER MANUFACTURING PROCESSES

- TABLE 37 OTHER MANUFACTURING PROCESSES: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 38 OTHER MANUFACTURING PROCESSES: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

8 STEEL FIBER MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- FIGURE 49 COMPOSITE REINFORCEMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 39 STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 40 STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 8.2 CONCRETE REINFORCEMENT

- 8.2.1 INCREASING DEMAND FOR TUNNEL LINING AND FLOORING TO DRIVE MARKET

- TABLE 41 CONCRETE REINFORCEMENT: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 42 CONCRETE REINFORCEMENT: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 8.3 COMPOSITE REINFORCEMENT

- 8.3.1 WIDE APPLICATION IN TEXTILE AND SPORTS INDUSTRIES TO BOOST MARKET

- TABLE 43 COMPOSITE REINFORCEMENT: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 44 COMPOSITE REINFORCEMENT: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 8.4 REFRACTORIES

- 8.4.1 INCREASING DEMAND IN MINING AND AEROSPACE INDUSTRIES TO DRIVE MARKET

- TABLE 45 REFRACTORIES: STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 46 REFRACTORIES: STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 8.5 OTHER APPLICATIONS

- TABLE 47 STEEL FIBER MARKET BY OTHER APPLICATION, BY REGION 2020-2029 (USD MILLION)

- TABLE 48 STEEL FIBER MARKET BY OTHER APPLICATION, BY REGION 2020-2029 (KILOTON)

9 STEEL FIBER MARKET, BY REGION

- 9.1 INTRODUCTION

- FIGURE 50 CHINA TO RECORD FASTEST GROWTH DURING FORECAST PERIOD

- TABLE 49 STEEL FIBER MARKET, BY REGION, 2020-2029 (USD MILLION)

- TABLE 50 STEEL FIBER MARKET, BY REGION, 2020-2029 (KILOTON)

- 9.2 NORTH AMERICA

- 9.2.1 RECESSION IMPACT

- FIGURE 51 NORTH AMERICA: STEEL FIBER MARKET SNAPSHOT

- 9.2.2 NORTH AMERICA: STEEL FIBER MARKET, BY TYPE

- TABLE 51 NORTH AMERICA: STEEL FIBER MARKET, BY TYPE, 2020-2029 (USD MILLION)

- TABLE 52 NORTH AMERICA: STEEL FIBER MARKET, BY TYPE, 2020-2029 (KILOTON)

- 9.2.3 NORTH AMERICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS

- TABLE 53 NORTH AMERICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (USD MILLION)

- TABLE 54 NORTH AMERICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (KILOTON)

- 9.2.4 NORTH AMERICA: STEEL FIBER MARKET, BY APPLICATION

- TABLE 55 NORTH AMERICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 56 NORTH AMERICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.2.5 NORTH AMERICA: STEEL FIBER MARKET, BY COUNTRY

- TABLE 57 NORTH AMERICA: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

- TABLE 58 NORTH AMERICA: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (KILOTON)

- 9.2.5.1 US

- 9.2.5.1.1 Increasing demand for electric vehicles to drive market

- 9.2.5.1 US

- TABLE 59 US: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 60 US: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.2.5.2 CANADA

- 9.2.5.2.1 Growth of construction sector to boost market

- 9.2.5.2 CANADA

- TABLE 61 CANADA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 62 CANADA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.3 ASIA PACIFIC

- 9.3.1 RECESSION IMPACT

- FIGURE 52 ASIA PACIFIC: STEEL FIBER MARKET SNAPSHOT

- 9.3.2 ASIA PACIFIC: STEEL FIBER MARKET, BY TYPE

- TABLE 63 ASIA PACIFIC: STEEL FIBER MARKET, BY TYPE, 2020-2029 (USD MILLION)

- TABLE 64 ASIA PACIFIC: STEEL FIBER MARKET, BY TYPE, 2020-2029 (KILOTON)

- 9.3.3 ASIA PACIFIC: STEEL FIBER MARKET, BY MANUFACTURING PROCESS

- TABLE 65 ASIA PACIFIC: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (USD MILLION)

- TABLE 66 ASIA PACIFIC: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (KILOTON)

- 9.3.4 ASIA PACIFIC: STEEL FIBER MARKET, BY APPLICATION

- TABLE 67 ASIA PACIFIC: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 68 ASIA PACIFIC: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.3.5 ASIA PACIFIC: STEEL FIBER MARKET, BY COUNTRY

- TABLE 69 ASIA PACIFIC: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

- TABLE 70 ASIA PACIFIC: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (KILOTON)

- 9.3.5.1 China

- 9.3.5.1.1 Presence of prominent steel fiber manufacturers to drive market

- 9.3.5.1 China

- TABLE 71 CHINA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 72 CHINA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.3.5.2 Japan

- 9.3.5.2.1 Increasing demand for steel fibers in concrete reinforcement to drive market

- 9.3.5.2 Japan

- TABLE 73 JAPAN: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 74 JAPAN: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.3.5.3 India

- 9.3.5.3.1 High demand for hooked and deformed fibers to boost market

- 9.3.5.3 India

- TABLE 75 INDIA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 76 INDIA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.3.5.4 Australia & New Zealand

- 9.3.5.4.1 Increasing demand from building and construction sector to drive market

- 9.3.5.4 Australia & New Zealand

- TABLE 77 AUSTRALIA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 78 AUSTRALIA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.3.5.5 South Korea

- 9.3.5.5.1 Rise in infrastructure development to fuel market

- 9.3.5.5 South Korea

- TABLE 79 SOUTH KOREA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 80 SOUTH KOREA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.3.5.6 Rest of Asia Pacific

- TABLE 81 REST OF ASIA PACIFIC: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 82 REST OF ASIA PACIFIC: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4 EUROPE

- 9.4.1 RECESSION IMPACT

- FIGURE 53 EUROPE: STEEL FIBER MARKET SNAPSHOT

- 9.4.2 EUROPEAN STEEL FIBER MARKET, BY TYPE

- TABLE 83 EUROPE: STEEL FIBER MARKET, BY TYPE, 2020-2029 (USD MILLION)

- TABLE 84 EUROPE: STEEL FIBER MARKET, BY TYPE, 2020-2029 (KILOTON)

- 9.4.3 EUROPEAN STEEL FIBER MARKET, BY MANUFACTURING PROCESS

- TABLE 85 EUROPE: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (USD MILLION)

- TABLE 86 EUROPE: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (KILOTON)

- 9.4.4 EUROPEAN STEEL FIBER MARKET, BY APPLICATION

- TABLE 87 EUROPE: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 88 EUROPE: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5 EUROPEAN STEEL FIBER MARKET, BY COUNTRY

- TABLE 89 EUROPE: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

- TABLE 90 EUROPE: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (KILOTON)

- 9.4.5.1 GERMANY

- 9.4.5.1.1 Technological advancements in infrastructure development to fuel market

- 9.4.5.1 GERMANY

- TABLE 91 GERMANY: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 92 GERMANY: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.2 Italy

- 9.4.5.2.1 Increase in construction & infrastructure activities to boost market

- 9.4.5.2 Italy

- TABLE 93 ITALY: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 94 ITALY: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.3 France

- 9.4.5.3.1 High demand for steel fibers in various applications to drive market

- 9.4.5.3 France

- TABLE 95 FRANCE: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 96 FRANCE: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.4 UK

- 9.4.5.4.1 Pressing need for hooked and straight steel fibers to drive market

- 9.4.5.4 UK

- TABLE 97 UK: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 98 UK: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.5 Spain

- 9.4.5.5.1 Increase in composites consumption to drive market

- 9.4.5.5 Spain

- TABLE 99 SPAIN: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 100 SPAIN: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.6 Turkey

- 9.4.5.6.1 Rise in infrastructure development and urbanization projects to boost market

- 9.4.5.6 Turkey

- TABLE 101 TURKEY: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 102 TURKEY: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.7 Norway

- 9.4.5.7.1 Need for sustainable construction materials to drive market

- 9.4.5.7 Norway

- TABLE 103 NORWAY: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 104 NORWAY: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.8 Denmark

- 9.4.5.8.1 Sustainable construction practices to drive market

- 9.4.5.8 Denmark

- TABLE 105 DENMARK: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 106 DENMARK: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.9 Sweden

- 9.4.5.9.1 Rise in construction activities to drive market

- 9.4.5.9 Sweden

- TABLE 107 SWEDEN: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 108 SWEDEN: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.10 Poland

- 9.4.5.10.1 Presence of prominent steel industries to drive market

- 9.4.5.10 Poland

- TABLE 109 POLAND: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 110 POLAND: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.11 Baltic states

- 9.4.5.11.1 Increasing construction activities to drive market

- 9.4.5.11 Baltic states

- TABLE 111 BALTIC STATES: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 112 BALTIC STATES: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.5.12 Rest of Europe

- TABLE 113 REST OF EUROPE: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 114 REST OF EUROPE: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.4.6 STEEL FIBER MARKET IN POLAND, NORDIC COUNTRIES, AND BALTIC STATES

- 9.4.6.1 Recession impact on steel fiber market

- 9.4.6.2 Impact of Covid-19 on steel fiber market

- 9.4.6.3 Impact of Russia-Ukraine conflict on steel fiber market

- 9.4.6.4 Major suppliers/distributors

- 9.4.6.5 Construction industry outlook for each country

- 9.4.6.5.1 Denmark

- 9.4.6.5.2 Poland

- 9.4.6.5.3 Sweden

- 9.4.6.5.4 Latvia

- 9.4.6.5.5 Estonia

- 9.4.6.5.6 Lithuania

- 9.4.6.6 Government policies/regulations impacting market

- TABLE 115 GOVERNMENT POLICIES/REGULATIONS IMPACTING MARKET

- 9.5 LATIN AMERICA

- 9.5.1 RECESSION IMPACT

- 9.5.2 LATIN AMERICA: STEEL FIBER MARKET, BY TYPE

- TABLE 116 LATIN AMERICA: STEEL FIBER MARKET, BY TYPE, 2020-2029 (USD MILLION)

- TABLE 117 LATIN AMERICA: STEEL FIBER MARKET, BY TYPE, 2020-2029 (KILOTON)

- 9.5.3 LATIN AMERICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS

- TABLE 118 LATIN AMERICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (USD MILLION)

- TABLE 119 LATIN AMERICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (KILOTON)

- 9.5.4 LATIN AMERICA: STEEL FIBER MARKET, BY APPLICATION

- TABLE 120 LATIN AMERICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 121 LATIN AMERICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.5.5 LATIN AMERICA: STEEL FIBER MARKET, BY COUNTRY

- TABLE 122 LATIN AMERICA: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

- TABLE 123 LATIN AMERICA: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (KILOTON)

- 9.5.5.1 Brazil

- 9.5.5.1.1 Rise in large-scale construction projects to boost market

- 9.5.5.1 Brazil

- TABLE 124 BRAZIL: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 125 BRAZIL: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.5.5.2 Mexico

- 9.5.5.2.1 Presence of prominent steel fiber companies to drive market

- 9.5.5.2 Mexico

- TABLE 126 MEXICO: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 127 MEXICO: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.5.5.3 Argentina

- 9.5.5.3.1 Wide demand from transportation sector to drive market

- 9.5.5.3 Argentina

- TABLE 128 ARGENTINA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 129 ARGENTINA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.5.5.4 Rest of Latin America

- TABLE 130 REST OF LATIN AMERICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 131 REST OF LATIN AMERICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 RECESSION IMPACT

- 9.6.2 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY TYPE

- TABLE 132 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY TYPE, 2020-2029 (USD MILLION)

- TABLE 133 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY TYPE, 2020-2029 (KILOTON)

- 9.6.3 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS

- TABLE 134 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (USD MILLION)

- TABLE 135 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY MANUFACTURING PROCESS, 2020-2029 (KILOTON)

- 9.6.4 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY APPLICATION

- TABLE 136 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 137 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.6.5 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY COUNTRY

- TABLE 138 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

- TABLE 139 MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY COUNTRY, 2020-2029 (KILOTON)

- 9.6.5.1 GCC countries

- TABLE 140 GCC COUNTRIES: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 141 GCC COUNTRIES: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.6.5.1.1 Saudi Arabia

- 9.6.5.1.1.1 Increasing focus on developmental projects like NEOM to drive market

- 9.6.5.1.1 Saudi Arabia

- TABLE 142 SAUDI ARABIA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 143 SAUDI ARABIA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.6.5.1.2 UAE

- 9.6.5.1.2.1 Green infrastructure deployment to boost market

- 9.6.5.1.2 UAE

- TABLE 144 UAE: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 145 UAE: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.6.5.1.3 Rest of GCC Countries

- TABLE 146 REST OF GCC COUNTRIES: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 147 REST OF GCC COUNTRIES: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.6.5.2 South Africa

- 9.6.5.2.1 Increased infrastructural spending to drive market

- 9.6.5.2 South Africa

- TABLE 148 SOUTH AFRICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 149 SOUTH AFRICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

- 9.6.5.3 Rest of Middle East & Africa

- TABLE 150 REST OF MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

- TABLE 151 REST OF MIDDLE EAST & AFRICA: STEEL FIBER MARKET, BY APPLICATION, 2020-2029 (KILOTON)

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 10.2.1 STRATEGIES ADOPTED BY STEEL FIBER MANUFACTURERS

- 10.3 REVENUE ANALYSIS

- FIGURE 54 STEEL FIBER MARKET: REVENUE ANALYSIS OF TOP 5 MARKET PLAYERS

- 10.4 MARKET SHARE ANALYSIS

- FIGURE 55 SHARES OF TOP COMPANIES IN STEEL FIBER MARKET

- TABLE 152 DEGREE OF COMPETITION: STEEL FIBER MARKET

- 10.4.1 MARKET RANKING ANALYSIS

- FIGURE 56 RANKING OF TOP 5 PLAYERS IN STEEL FIBER MARKET

- 10.5 BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 57 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 10.5.1 DRAMIX

- 10.5.2 TABIX

- 10.5.3 NASLON

- 10.5.4 NOVOCON

- 10.5.5 BUNDREX

- 10.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 10.6.1 STARS

- 10.6.2 PERVASIVE PLAYERS

- 10.6.3 EMERGING LEADERS

- 10.6.4 PARTICIPANTS

- FIGURE 58 STEEL FIBER MARKET: COMPANY EVALUATION MATRIX, 2023

- 10.6.5 COMPANY FOOTPRINT

- 10.6.5.1 Company footprint

- FIGURE 59 STEEL FIBER MARKET: COMPANY FOOTPRINT (14 COMPANIES)

- 10.6.5.2 Region footprint

- TABLE 153 STEEL FIBER MARKET: REGION FOOTPRINT (14 COMPANIES)

- 10.6.5.3 Type footprint

- TABLE 154 STEEL FIBER MARKET: TYPE FOOTPRINT (14 COMPANIES)

- 10.6.5.4 Manufacturing process footprint

- TABLE 155 STEEL FIBER MARKET: MANUFACTURING PROCESS FOOTPRINT (14 COMPANIES)

- 10.6.5.5 Application footprint

- TABLE 156 STEEL FIBER MARKET: APPLICATION FOOTPRINT (14 COMPANIES)

- 10.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 10.7.1 PROGRESSIVE COMPANIES

- 10.7.2 RESPONSIVE COMPANIES

- 10.7.3 DYNAMIC COMPANIES

- 10.7.4 STARTING BLOCKS

- FIGURE 60 STEEL FIBER MARKET: STARTUP/SME EVALUATION MATRIX, 2023

- 10.7.5 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 157 STEEL FIBER MARKET: KEY STARTUPS/SMES (10 COMPANIES)

- TABLE 158 STEEL FIBER MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 10.8 VALUATION AND FINANCIAL METRICS OF STEEL FIBER MANUFACTURERS

- FIGURE 61 EV/EBITDA OF KEY MANUFACTURERS

- FIGURE 62 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY MANUFACTURERS

- 10.9 COMPETITIVE SCENARIO AND TRENDS

- 10.9.1 PRODUCT LAUNCHES

- TABLE 159 STEEL FIBER MARKET: PRODUCT LAUNCHES, JANUARY 2018-JANUARY 2024

- 10.9.2 DEALS

- TABLE 160 STEEL FIBER MARKET: DEALS, JANUARY 2018-JANUARY 2024

- 10.9.3 EXPANSIONS

- TABLE 161 STEEL FIBER MARKET: EXPANSIONS, JANUARY 2020-JANUARY 2024

11 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, MnM View Right to win, Strategic choices made, Weaknesses and competitive threats) **

- 11.1 KEY COMPANIES

- 11.1.1 BEKAERT

- TABLE 162 BEKAERT: COMPANY OVERVIEW

- FIGURE 63 BEKAERT: COMPANY SNAPSHOT

- TABLE 163 BEKAERT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 164 BEKAERT: DEALS

- TABLE 165 BEKAERT: EXPANSIONS

- TABLE 166 BEKAERT: OTHERS

- 11.1.2 ARCELORMITTAL

- TABLE 167 ARCELORMITTAL: COMPANY OVERVIEW

- FIGURE 64 ARCELORMITTAL: COMPANY SNAPSHOT

- TABLE 168 ARCELORMITTAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 169 ARCELORMITTAL: PRODUCT LAUNCHES

- TABLE 170 ARCELORMITTAL: DEALS

- TABLE 171 ARCELORMITTAL: EXPANSIONS

- TABLE 172 ARCELORMITTAL: OTHERS

- 11.1.3 NIPPON SEISEN CO., LTD.

- TABLE 173 NIPPON SEISEN CO., LTD.: COMPANY OVERVIEW

- FIGURE 65 NIPPON SEISEN CO., LTD.: COMPANY SNAPSHOT

- TABLE 174 NIPPON SEISEN CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.4 FIBROMETALS

- TABLE 175 FIBROMETALS: COMPANY OVERVIEW

- TABLE 176 FIBROMETALS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.5 SIKA AG

- TABLE 177 SIKA AG: COMPANY OVERVIEW

- FIGURE 66 SIKA AG: COMPANY SNAPSHOT

- TABLE 178 SIKA AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 179 SIKA AG: DEALS

- TABLE 180 SIKA AG: EXPANSIONS

- 11.1.6 JIANGSU SHAGANG GROUP CO., LTD.

- TABLE 181 JIANGSU SHAGANG GROUP CO., LTD.: COMPANY OVERVIEW

- TABLE 182 JIANGSU SHAGANG GROUP CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.7 ZHEJIANG BOEN METAL PRODUCTS CO., LTD

- TABLE 183 ZHEJIANG BOEN METAL PRODUCTS CO., LTD: COMPANY OVERVIEW

- TABLE 184 ZHEJIANG BOEN METAL PRODUCTS CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.8 GREEN STEEL GROUP

- TABLE 185 GREEN STEEL GROUP: COMPANY OVERVIEW

- TABLE 186 GREEN STEEL GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.9 SPAJIC DOO

- TABLE 187 SPAJIC DOO: COMPANY OVERVIEW

- TABLE 188 SPAJIC DOO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.10 KOSTEEL CO., LTD.

- TABLE 189 KOSTEEL CO., LTD.: COMPANY OVERVIEW

- TABLE 190 KOSTEEL CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 191 KOSTEEL CO., LTD.: EXPANSIONS

- 11.1.11 SEVERSTAL

- TABLE 192 SEVERSTAL: COMPANY OVERVIEW

- FIGURE 67 SEVERSTAL: COMPANY SNAPSHOT

- TABLE 193 SEVERSTAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.12 ENVIROMESH PTY LTD.

- TABLE 194 ENVIROMESH PTY LTD.: COMPANY OVERVIEW

- TABLE 195 ENVIROMESH PTY LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.13 HUNAN SHUANGXING STEEL FIBER CO., LTD.

- TABLE 196 HUNAN SHUANGXING STEEL FIBER CO., LTD.: COMPANY OVERVIEW

- TABLE 197 HUNAN SHUANGXING STEEL FIBER CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 11.1.14 KERAKOLL SPA

- TABLE 198 KERAKOLL SPA: COMPANY OVERVIEW

- TABLE 199 KERAKOLL SPA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 200 KERAKOLL SPA: EXPANSIONS

- 11.2 OTHER PLAYERS

- 11.2.1 INTRAMICRON, INC.

- TABLE 201 INTRAMICRON, INC.: COMPANY OVERVIEW

- 11.2.2 PRECISION DRAWELL

- TABLE 202 PRECISION DRAWELL: COMPANY OVERVIEW

- 11.2.3 STEWOLS INDIA PVT. LTD.

- TABLE 203 STEWOLS INDIA PVT. LTD.: COMPANY OVERVIEW

- 11.2.4 KASTURI METAL COMPOSITES LTD.

- TABLE 204 KASTURI METAL COMPOSITES LTD.: COMPANY OVERVIEW

- 11.2.5 HEBEI SWIIT METALLIC FIBER CO., LTD.

- TABLE 205 HEBEI SWIIT METALLIC FIBER CO., LTD.: COMPANY OVERVIEW

- 11.2.6 NIKKO TECHNO, LTD.

- TABLE 206 NIKKO TECHNO, LTD.: COMPANY OVERVIEW

- 11.2.7 ISW CORPORATION

- TABLE 207 ISW CORPORATION: COMPANY OVERVIEW

- 11.2.8 DELTA STUD WELD

- TABLE 208 DELTA STUD WELD: COMPANY OVERVIEW

- 11.2.9 NYCON

- TABLE 209 NYCON: COMPANY OVERVIEW

- 11.2.10 THE EUCLID CHEMICAL COMPANY

- TABLE 210 THE EUCLID CHEMICAL COMPANY: COMPANY OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, MnM View, Right to win, Strategic choices made, Weaknesses and competitive threats might not be captured in case of unlisted companies.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS