|

|

市場調査レポート

商品コード

1472068

未来のバッテリーの世界市場:タイプ別、車両タイプ別、バッテリー形態別、パッケージ別、地域別 - 予測(~2035年)Future of Batteries Market by Type, Vehicle Type, Battery Form, Packaging & Region - Global Forecast 2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 未来のバッテリーの世界市場:タイプ別、車両タイプ別、バッテリー形態別、パッケージ別、地域別 - 予測(~2035年) |

|

出版日: 2024年04月22日

発行: MarketsandMarkets

ページ情報: 英文 210 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界の未来のバッテリーの市場規模は、2024年の1,600万個から2035年には6,200万個へと、CAGR12.7%で成長すると予測されています。

気候変動や大気汚染への懸念が高まる中、より環境に優しく持続可能な選択肢として、ガソリン車よりも電気自動車を選ぶ人が増えています。現在のEV販売ブームの結果、EV用バッテリーの需要が高まっています。さらに、研究者たちはバッテリー技術の改善に取り組んでおり、航続距離、寿命、充電時間において顕著な進歩を遂げています。EV電池市場は、こうした市場開発によってさらに刺激され、顧客にとってEVがより望ましく、実用的になっています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2024年~2035年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2035年 |

| 検討単位 | 金額(個) |

| セグメント | タイプ別、車両タイプ別、バッテリー形態別、パッケージ別(CTM、CTP、CTC、MTC)、地域別 |

| 対象地域 | 中国、米国、欧州、アジア太平洋、その他の地域 |

プリズム型セルは、アノード、カソード、セパレーターの内部層を扁平なスパイラル状または立方体状に折りたたむことを特徴とする、円筒型セルのよりコンパクトなバリエーションです。その結果、構造はよりコンパクトになります。ポリマーまたは金属のハウジングが電池の内容物を固定します。プリズム型バッテリーは、エネルギー密度が低くても(円筒型電池より20~50%低い)、スペースの有効利用が可能です。角形セルはゼリー圧延されているにもかかわらず、表面積が大きく、内層圧延の手順が難しいため、円筒形セルよりも製造コストが高くなる可能性があります。

当レポートでは、世界の未来のバッテリー市場について調査し、タイプ別、車両タイプ別、バッテリー形態別、パッケージ別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 電動化自動車市場

- イントロダクション

- 自動車の電動化の主要市場

- EVバッテリー市場、2019年~2035年年

- 自動車用途のバッテリー需要

- 現在のバッテリー製造能力と将来のバッテリー製造能力

第3章 バッテリー技術への洞察

- イントロダクション

- 既存のEVバッテリー技術

- EVバッテリー技術の未来

- さまざまなEVバッテリーの比較

- EVバッテリーの使用事例に関するMNMの見解

- EVバッテリーのOEMマッピングに関するMNMの見解

第4章 バッテリー価格、技術別

- イントロダクション

- バッテリー材料

- バッテリー価格分析、OEM別

- リチウムイオン電池パックとセルの価格分析

- リチウムイオン電池の価格(タイプ別)

- EVバッテリーの平均販売価格、地域別

第5章 バッテリーパッケージ形態に関する考察

- イントロダクション

- 既存のバッテリーパッケージ形式

- バッテリーパッケージングフォーマットの将来

- バッテリーパッケージ形式の長所と短所

- バッテリーメーカーの前方統合と後方統合

- バッテリーパッケージ形式のOEMマッピングに関するMNMの洞察

第6章 バッテリー形態に関する考察

- イントロダクション

- 既存のバッテリー形態

- バッテリー形態の長所と短所

- バッテリーフォームのOEMマッピングに関するMNMの見解

第7章 競合情勢

- イントロダクション

- 主要参入企業の戦略/強み、2020年~2024年

- 市場シェア分析、2023年

- 収益分析、2019年~2023年

- 企業価値評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオ

第8章 企業プロファイル

- 主要参入企業

- CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED

- BYD COMPANY LTD.

- LG ENERGY SOLUTION

- PANASONIC HOLDINGS CORPORATION

- SK INNOVATION CO., LTD.

- CALB

- SAMSUNG SDI CO., LTD.

- GOTION, INC.

- EVE ENERGY CO., LTD.

- SUNWODA ELECTRONIC CO., LTD.

- FARASIS ENERGY(GANZHOU)CO., LTD.

第9章 付録

The global future of batteries market is projected to grow from 16 million units in 2024 to 62 million units by 2035, at a CAGR of 12.7%. People increasingly choose electric vehicles over gasoline-powered cars as a greener and more sustainable option as worries about climate change and air pollution grow. EV batteries are in high demand as a result of the current boom in EV sales. Additionally, researchers are working to improve battery technology, with notable advancements in range, lifespan, and charging times. The EV batteries market is further stimulated by these developments, which are making EVs more desirable and practicable for customers.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2035 |

| Base Year | 2023 |

| Forecast Period | 2024-2035 |

| Units Considered | Value (Units) |

| Segments | Type, Vehicle Type, Battery Form, Packaging (CTM, CTP, CTC, MTC) & Region |

| Regions covered | China, US, Europe, Asia Pacific, and Rest of the World |

"Prismatic form to hold largest market share during the forecast period."

Prismatic cells are a more compact variation of cylindrical cells, characterized by folding the anode, cathode, and separator internal layers into a flattened spiral or cubic shape. As a result, its structure is more compact. A polymer or metal housing holds the battery's contents in place. Prismatic cells enable better space utilization even if they have a lower energy density (20-50% less than cylindrical cells). Despite being jelly-rolled, prismatic cells can be more expensive to produce than cylindrical cells because of their larger surface areas and more difficult internal layer rolling procedure. CATL, BYD, and Samsung SDI are major manufacturers of prismatic cells. For instance, in October 2023, Samsung SDI announced the company had clinched a supply deal for electric vehicle batteries with Hyundai Motor Company for the first time. Samsung SDI will supply prismatic batteries for Hyundai Motor's EVs, targeting the European market for seven years from 2026 through 2032. This development will increase the demand for urban transit trains during the forecast period.

"By Battery Packaging form Cell to Pack hold the largest market share."

Major EV and battery manufacturers have shown interest in developing cell to pack battery packs. Contemporary Amperex Technology Co., Limited. (CATL) (China), C4V (US), LG Energy Solution. (South Korea), Sunwoda Electronic Co., Ltd. (China), Tesla (US), BYD Company Ltd. (China), Ford Motor Company (US), and others have already started launching products that include cell to pack batteries. The growth of this ssegment is mainly driven by the increasing demand for high-voltage batteries to achieve a longer driving range. With new electric vehicles to be launched in the market, battery manufacturers and global EV OEMs continuously work on extensive research and developments and invest in advancing technology. CTP batteries are one of the results of such advancements, eliminating the use of modules and directly integrating cells into battery packs. This allows the use of larger and more cells within battery packs with reduced interconnections and a simplified assembly process resulting in an increased volumetric density of batteries and reduced cost. CTP technology is yet to be commercially launched in most EV-dominating countries. It is expected to gain traction by 2024-2025 in the US, South Korea, Japan, and European countries.

"Europe to be the fastest growing market for EV battery during the forecast period."

European OMEs are making significant investments in domestic battery manufacturing. The intention is to become self-sufficient and less dependent on the massive Asian battery companies. Across the continent, several gigafactories are being planned and built, strengthening the European economy and generating thousands of employment. Recognizing the market's enormous potential, major automakers, IT firms, and private investors are investing billions of euros in European EV batteries. This capital inflow is speeding up manufacturing and innovation, which is boosting the market's expansion even more. Furthermore, Europe is seeing a steady rise in the demand for electric vehicles. Customers are searching for environmentally friendly transportation options as their concern for the environment grows. In response, automakers expanded their electric vehicles' range, raising the need for EV batteries.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 57%, Tier I - 29%, Tier II- 14%,

- By Designation: CXOs - 54%, Directors- 32%, Others- 14%

- By Region: China - 22%, US- 19%, Asia Pacific (excl. China) - 24%, Europe - 25%, Rest of the World - 10%

The future of batteries market is dominated by established players such as CATL (China), LG Energy Solution Ltd. (South Korea), BYD Company Ltd. (China), Panasonic Holdings Corporation (Japan), and SK Innovation Co., Ltd. (South Korea). These companies manufacture battery and develop new technologies. These companies have set up R&D facilities and offer best-in-class products to their customers.

Research Coverage:

The Market Study Covers the future of batteries By Battery Type (Lithium-Ion, Solid-State, Sodium-Ion, and Lithium-Air), By Vehicle Type (Passenger Cars, Commercial Vehicles And Off-Road Vehicles), By Battery Form (Prismatic, Pouch, and Cylindrical), By Packaging Form (Cell to Module, Cell to Pack, Cell to Chassis, Module to chassia) and Region (China, US, Europe, Asia Pacific (excl. China), and Rest of the World). It also covers the competitive landscape and company profiles of the major players in the future of batteries market ecosystem.

Key Benefits of the Report

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall future of batteries market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing sales of EVs, Improvements in battery technology, Targets to reduce vehicle emissions, Launch of new plug-in models by major EV manufacturers, Reducing prices of EV batteries), restraints (Procurement concerns related to raw materials, Low number of charging stations in emerging economies, Development in hydrogen and ethanol vehicles), opportunities (Introduction of battery-as-a-service (BaaS) models, Development in solid-state batteries, Increase in R&D efforts toward creating more advanced battery chemistries), and challenges (High initial investments and high cost of electricity, Low availability of lithium for use in EV batteries, Concerns over battery safety, High cost of EVs compared to ICE vehicles) influencing the growth of the future of batteries market .

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the future of batteries market

- Market Development: Comprehensive information about lucrative markets - the report analyses the future of batteries market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the future of batteries market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like CATL (China), LG Energy Solution Ltd. (South Korea), BYD Company Ltd. (China), Panasonic Holdings Corporation (Japan), and SK Innovation Co., Ltd. (South Korea) and among others in the future of batteries market Page 25 of 34 strategies. The report also helps stakeholders understand the pulse of the EV market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- TABLE 1 MARKET DEFINITION, BY BATTERY TYPE

- TABLE 2 MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 3 MARKET DEFINITION, BY BATTERY FORM

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- TABLE 4 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 FUTURE OF BATTERIES MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 5 CURRENCY EXCHANGE RATES (PER USD)

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 RESEARCH ASSUMPTIONS

- 1.8 RESEARCH LIMITATIONS

2 ELECTRIFIED AUTOMOTIVE MARKET

- 2.1 INTRODUCTION

- 2.2 KEY MARKETS FOR AUTOMOTIVE ELECTRIFICATION

- FIGURE 2 AUTOMAKER ELECTRIFICATION TARGET FOR ELECTRIC VEHICLES, 2023

- FIGURE 3 ELECTRIFIED AUTOMOTIVE MARKET, BY REGION, 2024-2035 (THOUSAND UNITS)

- TABLE 6 ELECTRIFIED AUTOMOTIVE MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 7 ELECTRIFIED AUTOMOTIVE MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 8 ELECTRIFIED AUTOMOTIVE MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- 2.2.1 PASSENGER CARS

- 2.2.1.1 Availability of subsidies and tax rebates to drive growth

- FIGURE 4 BEST-SELLING PLUG-IN ELECTRIC VEHICLE MODELS GLOBALLY, 2023 (THOUSAND UNITS)

- TABLE 9 ELECTRIC PASSENGER CARS MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 10 ELECTRIC PASSENGER CARS MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 11 ELECTRIC PASSENGER CARS MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- 2.2.2 COMMERCIAL VEHICLES

- 2.2.2.1 Increasing collaborations between automotive manufacturers to drive growth

- TABLE 12 ELECTRIC COMMERCIAL VEHICLES MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 13 ELECTRIC COMMERCIAL VEHICLES MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 14 ELECTRIC COMMERCIAL VEHICLES MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- 2.2.3 OFF-ROAD VEHICLES

- 2.2.3.1 Stringent emission standards and noise regulations to drive growth

- TABLE 15 ELECTRIC OFF-ROAD VEHICLES MARKET, BY REGION, 2019-2023 (THOUSAND UNITS)

- TABLE 16 ELECTRIC OFF-ROAD VEHICLES MARKET, BY REGION, 2024-2030 (THOUSAND UNITS)

- TABLE 17 ELECTRIC OFF-ROAD VEHICLES MARKET, BY REGION, 2031-2035 (THOUSAND UNITS)

- 2.3 EV BATTERY MARKET, 2019-2035

- FIGURE 5 EV BATTERY MARKET, BY REGION, 2024-2035 (USD BILLION)

- 2.4 BATTERY DEMAND FROM AUTOMOTIVE APPLICATIONS

- TABLE 18 BATTERY DEMAND, BY VEHICLE TYPE, 2023-2035 (GWH)

- 2.5 CURRENT VS. FUTURE BATTERY MANUFACTURING CAPACITY

- FIGURE 6 BATTERY MANUFACTURING CAPACITY, BY COUNTRY

- TABLE 19 BATTERY MANUFACTURING CAPACITY, BY COUNTRY, 2022

- TABLE 20 BATTERY MANUFACTURING CAPACITY, BY COUNTRY, 2027

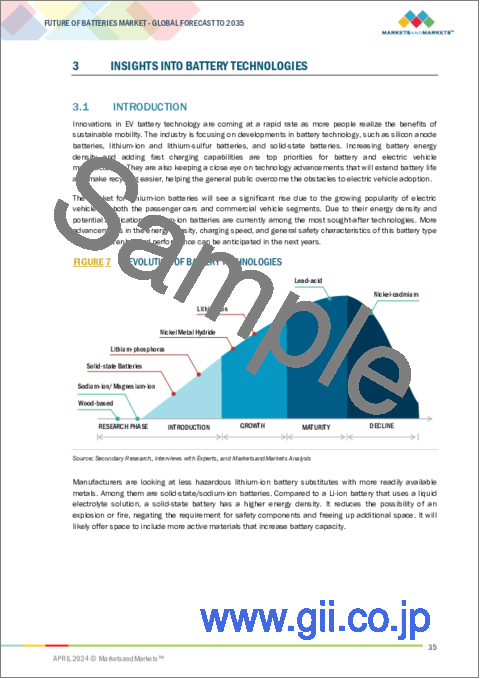

3 INSIGHTS INTO BATTERY TECHNOLOGIES

- 3.1 INTRODUCTION

- FIGURE 7 EVOLUTION OF BATTERY TECHNOLOGIES

- FIGURE 8 ROADMAP FOR BATTERY TECHNOLOGIES

- TABLE 21 NEXT-GENERATION BATTERY TECHNOLOGIES

- 3.2 EXISTING EV BATTERY TECHNOLOGIES

- 3.2.1 LITHIUM-ION

- FIGURE 9 GLOBAL LITHIUM-ION BATTERY DEMAND, 2022-2030 (GWH)

- 3.2.1.1 Lithium iron phosphate

- TABLE 22 ELECTROCHEMICAL REACTIONS OF LITHIUM IRON PHOSPHATE BATTERIES

- FIGURE 10 BENEFITS OF LITHIUM IRON PHOSPHATE BATTERIES FOR ELECTRIC PASSENGER CARS

- TABLE 23 RECENT DEVELOPMENTS IN LITHIUM IRON PHOSPHATE BATTERIES

- 3.2.1.2 Nickel manganese cobalt

- TABLE 24 ELECTROCHEMICAL REACTIONS OF NICKEL MANGANESE COBALT BATTERIES

- TABLE 25 RECENT DEVELOPMENTS IN NICKEL MANGANESE COBALT BATTERIES

- 3.2.1.3 Lithium manganese iron phosphate

- TABLE 26 RECENT DEVELOPMENTS IN LITHIUM MANGANESE IRON PHOSPHATE BATTERIES

- FIGURE 11 ANTICIPATED APPLICATIONS OF LITHIUM MANGANESE IRON PHOSPHATE BATTERIES AND PROJECTED SHIPMENT VOLUME IN CHINA

- TABLE 27 COMPARISON BETWEEN LFP, LMFP, AND NMC BATTERIES

- 3.2.1.4 Others

- FIGURE 12 VISUAL COMPARISON OF LITHIUM-ION BATTERIES

- 3.2.2 SODIUM-ION

- TABLE 28 ELECTROCHEMICAL REACTIONS OF SODIUM-ION BATTERIES

- TABLE 29 RECENT DEVELOPMENTS IN SODIUM-ION BATTERIES

- 3.3 FUTURE OF EV BATTERY TECHNOLOGIES

- 3.3.1 SOLID-STATE

- TABLE 30 DIFFERENCE BETWEEN LITHIUM-ION AND SOLID-STATE BATTERIES

- TABLE 31 RECENT DEVELOPMENTS IN SOLID-STATE BATTERIES

- 3.3.2 LITHIUM-AIR

- FIGURE 13 SCHEMATIC OF LITHIUM-AIR BATTERY CHARGE AND DISCHARGE CYCLES

- 3.4 COMPARISON BETWEEN DIFFERENT EV BATTERIES

- TABLE 32 COMPARISON BETWEEN DIFFERENT EV BATTERIES

- 3.5 MNM INSIGHTS ON EV BATTERY USE CASES

- 3.5.1 PASSENGER CARS

- 3.5.2 COMMERCIAL VEHICLES

- 3.5.3 OFF-ROAD VEHICLES

- 3.6 MNM INSIGHTS ON OEM MAPPING OF EV BATTERIES

- 3.6.1 PASSENGER CARS

- TABLE 33 UPCOMING OEM PASSENGER CAR LAUNCHES, BY BATTERY TYPE

- 3.6.2 COMMERCIAL VEHICLES

- TABLE 34 UPCOMING OEM COMMERCIAL VEHICLE LAUNCHES, BY BATTERY TYPE

- 3.6.3 OFF-ROAD VEHICLES

- TABLE 35 UPCOMING OEM OFF-ROAD VEHICLE LAUNCHES, BY BATTERY TYPE

- 3.6.4 REIGN OF LITHIUM-ION AND RISE OF CHALLENGERS

- 3.6.5 EV BATTERY TRENDS PERTAINING TO VEHICLE CLASS

4 BATTERY PRICING, BY TECHNOLOGY

- 4.1 INTRODUCTION

- 4.2 SELECTED BATTERY MATERIALS

- FIGURE 14 PRICE OF SELECTED BATTERY MATERIALS, 2015-2023

- FIGURE 15 COST BREAKDOWN OF CELLS, BY MATERIAL, 2023

- 4.3 BATTERY PRICING ANALYSIS, BY OEM

- TABLE 36 BATTERY PRICING ANALYSIS, BY OEM (USD/KWH), 2022-2030

- TABLE 37 VEHICLE BATTERY COSTS, BY MODEL

- 4.4 LITHIUM-ION BATTERY PACK AND CELL PRICING ANALYSIS

- FIGURE 16 VOLUME-WEIGHTED AVERAGE LITHIUM-ION BATTERY PACK AND CELL PRICE, 2019-2023

- 4.5 LITHIUM-ION BATTERY PRICING, BY TYPE

- TABLE 38 LITHIUM-ION BATTERY PRICING, BY TYPE

- 4.6 AVERAGE SELLING PRICE OF EV BATTERIES, BY REGION

- FIGURE 17 AVERAGE SELLING PRICE OF EV BATTERIES, BY REGION, 2019-2023

5 INSIGHTS INTO BATTERY PACKAGING FORMATS

- 5.1 INTRODUCTION

- FIGURE 18 MULTISCALE HIERARCHICAL FRAMEWORK FOR THERMO-ELECTRIC-CHEMICAL CO-DESIGN OF BATTERIES AND ELECTRIC VEHICLES

- 5.2 EXISTING BATTERY PACKAGING FORMATS

- 5.2.1 CELL-TO-MODULE

- 5.2.2 CELL-TO-PACK

- FIGURE 19 CELL-TO-PACK BATTERY MANUFACTURING PROCESS

- FIGURE 20 CELL-TO-PACK BATTERY MARKET, BY REGION, 2024-2030

- 5.3 FUTURE OF BATTERY PACKAGING FORMATS

- 5.3.1 CELL-TO-CHASSIS

- 5.3.2 MODULE-TO-CHASSIS

- 5.4 PROS AND CONS OF BATTERY PACKAGING FORMATS

- TABLE 39 PROS AND CONS OF BATTERY PACKAGING FORMATS

- FIGURE 21 EV POWER BATTERY STRUCTURE DEVELOPMENT

- 5.5 FORWARD AND BACKWARD INTEGRATION OF BATTERY MANUFACTURERS

- 5.5.1 FORWARD INTEGRATION OF BATTERY MANUFACTURERS

- 5.5.2 BACKWARD INTEGRATION OF BATTERY MANUFACTURERS

- 5.6 MNM INSIGHTS ON OEM MAPPING OF BATTERY PACKAGING FORMATS

- 5.6.1 PASSENGER CARS

- TABLE 40 PASSENGER CAR BATTERY PACKAGING FORMATS, BY OEM

- 5.6.2 COMMERCIAL VEHICLES

- TABLE 41 COMMERCIAL VEHICLE BATTERY PACKAGING FORMATS, BY OEM

- 5.6.3 OFF-ROAD VEHICLES

- TABLE 42 OFF-ROAD VEHICLE BATTERY PACKAGING FORMATS, BY OEM

6 INSIGHTS INTO BATTERY FORMS

- 6.1 INTRODUCTION

- FIGURE 22 CELL FORMATS PRODUCED BY EV BATTERY MANUFACTURERS

- FIGURE 23 CELL FORMATS USED BY MAJOR OEMS

- 6.2 EXISTING BATTERY FORMS

- 6.2.1 PRISMATIC

- 6.2.2 POUCH

- 6.2.3 CYLINDRICAL

- FIGURE 24 TESLA CYLINDRICAL BATTERY SIZES

- 6.3 PROS AND CONS OF BATTERY FORMS

- TABLE 43 PROS AND CONS OF BATTERY FORMS

- 6.4 MNM INSIGHTS ON OEM MAPPING OF BATTERY FORMS

- 6.4.1 PASSENGER CARS

- TABLE 44 PASSENGER CAR BATTERY FORMS, BY OEM

- 6.4.2 COMMERCIAL VEHICLES

- TABLE 45 COMMERCIAL VEHICLE BATTERY FORMS, BY OEM

7 COMPETITIVE LANDSCAPE

- 7.1 INTRODUCTION

- 7.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2024

- TABLE 46 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2024

- 7.3 MARKET SHARE ANALYSIS, 2023

- TABLE 47 DEGREE OF COMPETITION, 2023

- FIGURE 25 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2023

- 7.4 REVENUE ANALYSIS, 2019-2023

- FIGURE 26 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2019-2023

- 7.5 COMPANY VALUATION AND FINANCIAL METRICS

- 7.5.1 COMPANY VALUATION

- FIGURE 27 COMPANY VALUATION OF KEY PLAYERS, 2024

- 7.5.2 FINANCIAL METRICS

- FIGURE 28 FINANCIAL METRICS OF KEY PLAYERS, 2024

- 7.6 BRAND/PRODUCT COMPARISON

- FIGURE 29 BRAND/PRODUCT COMPARISON OF TOP FIVE PLAYERS

- 7.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 7.7.1 STARS

- 7.7.2 EMERGING LEADERS

- 7.7.3 PERVASIVE PLAYERS

- 7.7.4 PARTICIPANTS

- FIGURE 30 COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- 7.7.5 COMPANY FOOTPRINT

- FIGURE 31 COMPANY FOOTPRINT, 2023

- TABLE 48 PRODUCT FOOTPRINT, 2023

- TABLE 49 REGION FOOTPRINT, 2023

- 7.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2023

- 7.8.1 PROGRESSIVE COMPANIES

- 7.8.2 RESPONSIVE COMPANIES

- 7.8.3 DYNAMIC COMPANIES

- 7.8.4 STARTING BLOCKS

- FIGURE 32 COMPANY EVALUATION MATRIX (START-UPS/SMES), 2023

- 7.8.5 COMPETITIVE BENCHMARKING

- TABLE 50 KEY START-UPS/SMES

- TABLE 51 COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- 7.9 COMPETITIVE SCENARIO

- 7.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 52 PRODUCT LAUNCHES/DEVELOPMENTS, 2020-2024

- 7.9.2 DEALS

- TABLE 53 DEALS, 2020-2024

- 7.9.3 EXPANSION

- TABLE 54 EXPANSIONS, 2020-2024

- 7.9.4 OTHERS

- TABLE 55 OTHERS, 2020-2024

8 COMPANY PROFILES

- (Business overview, Products offered, Recent developments & MnM View)**

- 8.1 KEY PLAYERS

- 8.1.1 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED

- TABLE 56 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: COMPANY OVERVIEW

- FIGURE 33 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: COMPANY SNAPSHOT

- FIGURE 34 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: TECHNOLOGY ROADMAP

- TABLE 57 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: SUPPLY AGREEMENTS

- TABLE 58 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: PRODUCTS OFFERED

- TABLE 59 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 60 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: DEALS

- TABLE 61 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: EXPANSIONS

- TABLE 62 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: OTHERS

- 8.1.2 BYD COMPANY LTD.

- TABLE 63 BYD COMPANY LTD.: COMPANY OVERVIEW

- FIGURE 35 BYD COMPANY LTD.: COMPANY SNAPSHOT

- TABLE 64 BYD COMPANY LTD.: PRODUCTS OFFERED

- TABLE 65 BYD COMPANY LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 66 BYD COMPANY LTD.: DEALS

- TABLE 67 BYD COMPANY LTD.: EXPANSIONS

- 8.1.3 LG ENERGY SOLUTION

- TABLE 68 LG ENERGY SOLUTION: COMPANY OVERVIEW

- FIGURE 36 LG ENERGY SOLUTION: COMPANY SNAPSHOT

- TABLE 69 LG ENERGY SOLUTION: R&D OVERVIEW

- TABLE 70 LG ENERGY SOLUTION: SUPPLY AGREEMENTS

- FIGURE 37 BENEFITS OF LG ENERGY SOLUTION BATTERIES

- FIGURE 38 LG ENERGY SOLUTION: FUTURE TECHNOLOGY DEVELOPMENT

- FIGURE 39 LG ENERGY SOLUTION: NEXT-GENERATION BATTERIES

- TABLE 71 LG ENERGY SOLUTION: PRODUCTS OFFERED

- TABLE 72 LG ENERGY SOLUTION: DEALS

- TABLE 73 LG ENERGY SOLUTION: OTHERS

- 8.1.4 PANASONIC HOLDINGS CORPORATION

- TABLE 74 PANASONIC HOLDINGS CORPORATION: COMPANY OVERVIEW

- FIGURE 40 PANASONIC HOLDINGS CORPORATION: COMPANY SNAPSHOT

- TABLE 75 PANASONIC HOLDINGS CORPORATION: SUPPLY AGREEMENTS

- TABLE 76 PANASONIC HOLDINGS CORPORATION: PRODUCTS OFFERED

- TABLE 77 PANASONIC HOLDINGS CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 78 PANASONIC HOLDINGS CORPORATION: DEALS

- TABLE 79 PANASONIC HOLDINGS CORPORATION: EXPANSIONS

- TABLE 80 PANASONIC HOLDINGS CORPORATION: OTHERS

- 8.1.5 SK INNOVATION CO., LTD.

- TABLE 81 SK INNOVATION CO., LTD.: COMPANY OVERVIEW

- FIGURE 41 SK INNOVATION CO., LTD.: COMPANY SNAPSHOT

- TABLE 82 SK INNOVATION CO., LTD.: SUPPLY AGREEMENTS

- FIGURE 42 SK INNOVATION CO., LTD.: GLOBAL BATTERY PRODUCTION

- TABLE 83 SK INNOVATION CO., LTD.: PRODUCTS OFFERED

- TABLE 84 SK INNOVATION CO., LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 85 SK INNOVATION CO., LTD.: DEALS

- TABLE 86 SK INNOVATION CO., LTD.: EXPANSIONS

- TABLE 87 SK INNOVATION CO., LTD.: OTHERS

- 8.1.6 CALB

- TABLE 88 CALB: COMPANY OVERVIEW

- FIGURE 43 CALB: COMPANY SNAPSHOT

- TABLE 89 CALB: SUPPLY AGREEMENTS

- TABLE 90 CALB: PRODUCTS OFFERED

- TABLE 91 CALB: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 92 CALB: DEALS

- 8.1.7 SAMSUNG SDI CO., LTD.

- TABLE 93 SAMSUNG SDI CO., LTD.: COMPANY OVERVIEW

- FIGURE 44 SAMSUNG SDI CO., LTD.: COMPANY SNAPSHOT

- TABLE 94 SAMSUNG SDI CO., LTD.: SUPPLY AGREEMENTS

- FIGURE 45 SAMSUNG SDI CO., LTD.: GLOBAL FOOTPRINT

- TABLE 95 SAMSUNG SDI CO., LTD.: PRODUCTS OFFERED

- TABLE 96 SAMSUNG SDI CO., LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 97 SAMSUNG SDI CO., LTD.: DEALS

- TABLE 98 SAMSUNG SDI CO., LTD.: EXPANSIONS

- TABLE 99 SAMSUNG SDI CO., LTD.: OTHERS

- 8.1.8 GOTION, INC.

- TABLE 100 GOTION, INC.: COMPANY OVERVIEW

- FIGURE 46 GOTION, INC.: COMPANY SNAPSHOT

- TABLE 101 GOTION, INC.: PRODUCTS OFFERED

- TABLE 102 GOTION, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 103 GOTION, INC.: DEALS

- TABLE 104 GOTION, INC.: EXPANSIONS

- 8.1.9 EVE ENERGY CO., LTD.

- TABLE 105 EVE ENERGY CO., LTD.: COMPANY OVERVIEW

- FIGURE 47 EVE ENERGY CO., LTD.: COMPANY SNAPSHOT

- TABLE 106 EVE ENERGY CO., LTD.: SUPPLY AGREEMENTS

- TABLE 107 EVE ENERGY CO., LTD.: PRODUCTS OFFERED

- TABLE 108 EVE ENERGY CO., LTD.: DEALS

- TABLE 109 EVE ENERGY CO., LTD.: OTHERS

- 8.1.10 SUNWODA ELECTRONIC CO., LTD.

- TABLE 110 SUNWODA ELECTRONIC CO., LTD.: COMPANY OVERVIEW

- FIGURE 48 SUNWODA ELECTRONIC CO., LTD.: COMPANY SNAPSHOT

- TABLE 111 SUNWODA ELECTRONIC CO., LTD.: SUPPLY AGREEMENTS

- TABLE 112 SUNWODA ELECTRONIC CO., LTD.: PRODUCTS OFFERED

- TABLE 113 SUNWODA ELECTRONIC CO., LTD.: DEALS

- TABLE 114 SUNWODA ELECTRONIC CO., LTD.: OTHERS

- 8.1.11 FARASIS ENERGY (GANZHOU) CO., LTD.

- TABLE 115 FARASIS ENERGY (GANZHOU) CO., LTD.: COMPANY OVERVIEW

- FIGURE 49 FARASIS ENERGY (GANZHOU) CO., LTD.: COMPANY SNAPSHOT

- TABLE 116 FARASIS ENERGY (GANZHOU) CO., LTD.: PRODUCTS OFFERED

- TABLE 117 FARASIS ENERGY (GANZHOU) CO., LTD.: DEALS

- TABLE 118 FARASIS ENERGY (GANZHOU) CO., LTD.: EXPANSIONS

- *Details on Business overview, Products offered, Recent developments & MnM View might not be captured in case of unlisted companies.

9 APPENDIX

- 9.1 KEY INDUSTRY INSIGHTS

- 9.2 DISCUSSION GUIDE

- 9.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 9.4 CUSTOMIZATION OPTIONS

- 9.4.1 ADDITIONAL COMPANY PROFILES

- 9.4.2 FUTURE OF BATTERIES MARKET, BY PROPULSION TYPE, AT COUNTRY LEVEL

- 9.4.3 FUTURE OF BATTERIES MARKET, BY PROPULSION TYPE, AT VEHICLE TYPE LEVEL

- 9.5 RELATED REPORTS

- 9.6 AUTHOR DETAILS