|

|

市場調査レポート

商品コード

1462807

上下水道処理装置の世界市場:タイプ別、プロセス別、エンドユーザー別、地域別 - 2029年までの予測Water and Wastewater Treatment Equipment Market by Product Type (Filtration, Disinfection, Desalination, Sludge Treatment, Biological), Process (Primary, Secondary And Tertiary), End-User (Municipal, Industrial), And Region -Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 上下水道処理装置の世界市場:タイプ別、プロセス別、エンドユーザー別、地域別 - 2029年までの予測 |

|

出版日: 2024年04月09日

発行: MarketsandMarkets

ページ情報: 英文 257 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

上下水道処理装置の市場規模は、2024年の687億米ドルからCAGR 5.0%で拡大し、2029年には877億米ドルに達すると予測されています。

上下水道処理装置産業のエンドユーザーとしては、自治体が最大の市場シェアを占めています。まず、世界の都市化と人口増加により、都市部では清潔な水の供給と効果的な廃水処理に対する需要が高まっています。自治体は、住民に安全な飲料水を提供し、公衆衛生と環境を守るために廃水を処理する責任を負っています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2023年~2028年 |

| 基準年 | 2022年 |

| 予測期間 | 2023年~2028年 |

| 検討単位 | 金額(100万米ドル) |

| セグメント別 | タイプ別、プロセス別、エンドユーザー別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

さらに、政府機関が課す厳しい規制や基準により、自治体は品質基準や排出基準を遵守するため、高度な上下水道処理インフラに投資する必要があります。こうした規制により、自治体は人口増加のニーズや環境問題に対応するため、既存の処理施設のアップグレードや新設を義務付けられることが多くなります。

多くの都市部ではインフラが老朽化しているため、上下水処理システムの改修や近代化のために多額の投資が必要となっています。自治体は、老朽化した設備を交換し、革新的な技術を導入して処理効率を高め、運営コストを削減し、システム全体の性能を向上させなければなりません。

さらに、水系感染症や汚染事故の増加により、自治体における堅牢な水処理システムの重要性が強調されています。公衆衛生を守り、水系病原菌や汚染物質に関連するリスクを軽減するため、自治体は信頼性が高く効率的な上下水道処理設備への投資を優先しています。

当レポートでは、世界の上下水道処理装置市場について調査し、タイプ別、プロセス別、エンドユーザー別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

第6章 業界の動向

- イントロダクション

- 顧客ビジネスに影響を与える動向/混乱

- 価格分析

- バリューチェーン分析

- エコシステム/市場マップ

- 技術分析

- 特許分析

- 貿易分析

- 2024年~2025年の主な会議とイベント

- ケーススタディ

- 関税と規制状況

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- 投資と資金調達のシナリオ

第7章 上下水道処理装置市場、タイプ別

- イントロダクション

- 濾過

- 消毒

- 淡水化

- 汚泥処理

- 生物学的処理

- テスト

第8章 上下水道処理装置市場、プロセス別

- イントロダクション

- 一次

- 二次

- 三次

第9章 上下水道処理装置市場、エンドユーザー別

- イントロダクション

- 自治体

- 工業

第10章 上下水道処理装置市場、地域別

- イントロダクション

- アジア太平洋

- 欧州

- 北米

- 南米

- 中東・アフリカ

第11章 競合情勢

- イントロダクション

- 主要参入企業の戦略

- 市場シェア分析

- 収益分析

- ブランド/製品比較分析

- 企業評価マトリックス:2023年の主要参入企業

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオと動向

第12章 企業プロファイル

- 主要参入企業

- VEOLIA

- XYLEM

- ECOLAB

- DUPONT

- PENTAIR

- 3M

- AQUATECH INTERNATIONAL

- THERMAX LIMITED

- CULLIGAN WATER

- CALGON CARBON CORPORATION

- その他の企業

- TORAY INDUSTRIES, INC.

- HITACHI, LTD.

- IEI(ION EXCHNAGE)

- BWT

- DANAHER

- CHEMBOND CHEMICALS LIMITED

- KURITA WATER INDUSTRIES LTD

- INPHLOX WATER SYSTEMS PVT LTD.

- MITA WATER TECHNOLOGIES S.R.L.

- GRACE GREEN INFRA

- FLUENCE CORPORATION LIMITED

- KOVALUS SEPARATION SOLUTIONS

- TOSHIBA WATER SOLUTIONS PRIVATE LIMITED

- A.O. SMITH WATER TECHNOLOGIES

- ECOLOGIX ENVIRONMENTAL SYSTEMS

第13章 付録

The Water & wastewater treatment equipment Market is projected to reach USD 87.7 billion by 2029, at a CAGR of 5.0% from USD 68.7 billion in 2024. Municipalities hold the largest market share as end-users in the water and wastewater treatment equipment industry. Firstly, the increasing urbanization and population growth worldwide have led to higher demand for clean water supply and effective wastewater treatment in urban areas. Municipalities are responsible for providing safe drinking water to residents and treating wastewater to protect public health and the environment.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD Million) |

| Segments | By Platform, Capability, End-Use, Product and Region |

| Regions covered | North America, Europe, APAC, RoW |

Additionally, stringent regulations and standards imposed by governmental bodies require municipalities to invest in advanced water and wastewater treatment infrastructure to comply with quality and discharge standards. These regulations often mandate municipalities to upgrade existing treatment facilities or build new ones to meet growing population needs and environmental concerns.

Moreover, the aging infrastructure in many urban areas necessitates significant investments in water and wastewater treatment systems for rehabilitation and modernization. Municipalities must replace outdated equipment and adopt innovative technologies to improve treatment efficiency, reduce operational costs, and enhance overall system performance.

Furthermore, the increasing prevalence of waterborne diseases and contamination incidents emphasizes the importance of robust water treatment systems in municipal settings. To safeguard public health and mitigate the risks associated with waterborne pathogens and pollutants, municipalities prioritize investments in reliable and efficient water and wastewater treatment equipment.

Lastly, the growing awareness among policymakers and the public about the importance of sustainable water management practices drives municipalities to invest in eco-friendly treatment solutions that minimize environmental impact and promote resource conservation. As a result, the municipal sector remains the largest market segment for water and wastewater treatment equipment, driving continuous innovation and growth in the industry.

"Disinfection, by product type, accounts for the second-largest market share in 2023."

Disinfection by product type holds the second-largest share in the water and wastewater treatment equipment market. Firstly, disinfection is a critical step in water treatment processes to eliminate harmful pathogens, bacteria, and viruses, ensuring that water is safe for consumption and meets regulatory standards. As a result, there is a constant demand for disinfection equipment and technologies across various end-user sectors, including municipal water treatment plants, industrial facilities, and commercial establishments.

Moreover, the increasing emphasis on water quality and public health safety drives the adoption of advanced disinfection methods and technologies. Concerns about waterborne diseases and microbial contaminants in drinking water sources necessitate the implementation of effective disinfection solutions to prevent outbreaks and ensure the delivery of clean, potable water to consumers.

Furthermore, the emergence of new disinfection technologies, such as ultraviolet (UV) disinfection, ozone treatment, and advanced oxidation processes, offers more efficient and environmentally friendly alternatives to traditional disinfection methods like chlorination. These innovative disinfection technologies provide superior disinfection efficacy, reduced chemical usage, and fewer disinfection by-products (DBPs), addressing concerns about the potential health and environmental impacts associated with conventional disinfection practices.

"Tertiary is expected to be the fastest growing process segment at CAGR 5.3% for water & wastewater treatment equipment market during the forecast period, in terms of value."

Tertiary treatment processes are experiencing rapid growth in the water and wastewater treatment equipment market due to several key factors. Firstly, tertiary treatment plays a crucial role in achieving stringent water quality standards and regulatory compliance by addressing specific contaminants that may remain after primary and secondary treatment processes. As environmental regulations become more stringent worldwide, there is a growing emphasis on the removal of nutrients, pathogens, and emerging contaminants from wastewater effluents before discharge into receiving water bodies.

Moreover, increasing urbanization, industrialization, and population growth are leading to higher volumes of wastewater generation, placing greater pressure on existing treatment infrastructure. Tertiary treatment processes, such as filtration, disinfection, and advanced oxidation, offer effective solutions for treating complex wastewater streams and meeting the rising demand for clean water resources.

Furthermore, growing awareness of water scarcity and the need for water reuse and recycling initiatives drive the adoption of tertiary treatment processes in water-stressed regions. Tertiary treated wastewater can be reclaimed for various non-potable applications such as irrigation, industrial processes, and groundwater recharge, reducing the strain on freshwater resources and enhancing sustainability.

Additionally, the increasing investment in wastewater infrastructure upgrades and modernization projects, particularly in developing economies, fuels the demand for tertiary treatment equipment and systems. Governments, municipalities, and industrial facilities are investing in advanced tertiary treatment technologies to improve water quality, protect ecosystems, and support sustainable development goals.

"Based on region, North America was the second largest market for water & wastewater treatment equipment market in 2023."

North America occupies a significant position as the second-largest region in the water and wastewater treatment equipment market due to several key factors. Firstly, stringent regulatory standards enforced by agencies such as the Environmental Protection Agency (EPA) drive the demand for advanced treatment solutions to ensure compliance with water quality regulations. The Clean Water Act and Safe Drinking Water Act mandate the treatment of wastewater and drinking water to safeguard public health and the environment, leading to substantial investments in water infrastructure and treatment technologies.

Moreover, North America's aging water and wastewater infrastructure presents challenges related to water quality, supply, and reliability. As existing treatment plants reach the end of their service life and population growth strains existing resources, there is a pressing need for infrastructure upgrades and modernization projects. This creates opportunities for the adoption of advanced treatment equipment and systems to enhance the efficiency and resilience of water treatment processes.

Additionally, increasing industrialization and urbanization in North America result in higher volumes of wastewater generation from various sectors, including manufacturing, energy production, and municipal sources. This drives the demand for wastewater treatment equipment capable of addressing diverse contaminants and pollutants present in industrial effluents.

Furthermore, growing concerns about emerging contaminants, such as pharmaceuticals, microplastics, and industrial chemicals, amplify the need for advanced treatment technologies capable of removing these substances from water and wastewater streams. Innovative solutions such as membrane filtration, advanced oxidation processes, and UV disinfection systems are increasingly deployed to address these emerging challenges.

In the process of determining and verifying the market size for several segments and subsegments identified through secondary research, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees is as follows:

- By Company Type: Tier 1 - 40%, Tier 2 -30%, and Tier 3 - 30%

- By Designation: C-Level - 20%, Director Level - 10%, and Others - 70%

- By Region: North America - 20%, Europe -30%, Asia Pacific - 30%, Middle East & Africa - 10%, and South America- 10%

The key players in this market are Veolia (France), Xylem (US), Ecolab (US), DuPont (US), Pentair (UK), 3M (US), Aquatech International (US), Thermax Limited (India), Culligan Water (US), Calgon Carbon Corporation (US) etc.

Research Coverage

This report segments the market for the water and wastewater treatment equipment market on the basis of product type, process, end-user and region. It provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and mergers & acquisitions associated with the market for the water & wastewater treatment equipment market.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the water and wastewater treatment equipment market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers: The market growth is driven by increasing water scarcity concerns which in turn drives the adoption of sustainable water management practices. The increase in industrial water consumption and discharge and growing global population along with rising industrialization and urbanization.

- Market Penetration: Comprehensive information on the water and wastewater treatment equipment market offered by top players in the global water and wastewater treatment equipment market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the water and wastewater treatment equipment market.

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for the water and wastewater treatment equipment market across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global water and wastewater treatment equipment market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the water and wastewater treatment equipment market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS & EXCLUSIONS

- 1.4 MARKET SCOPE

- FIGURE 1 WATER & WASTEWATER TREATMENT EQUIPMENT MARKET SEGMENTATION

- 1.4.1 REGIONS COVERED

- 1.4.2 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.7 LIMITATIONS

- 1.8 STAKEHOLDERS

- 1.9 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary data sources

- 2.1.2.2 Key water and wastewater treatment equipment manufacturers

- 2.1.2.3 Breakdown of interviews with experts

- 2.1.2.4 Key industry insights

- 2.2 BASE NUMBER CALCULATION

- 2.2.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 2.2.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 2.3 FORECAST NUMBER CALCULATION

- 2.3.1 SUPPLY SIDE

- 2.3.2 DEMAND SIDE

- 2.4 MARKET SIZE ESTIMATION

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: REVENUE OF MARKET PLAYERS

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- FIGURE 4 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: DATA TRIANGULATION

- 2.6 ASSUMPTIONS

- 2.7 RECESSION IMPACT

- 2.8 GROWTH FORECAST

- 2.9 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 5 FILTRATION SEGMENT TO DOMINATE MARKET BETWEEN 2024 AND 2029

- FIGURE 6 TERTIARY SEGMENT TO LEAD MARKET BETWEEN 2024 AND 2029

- FIGURE 7 MUNICIPAL END USER TO LEAD MARKET BETWEEN 2024 AND 2030

- FIGURE 8 ASIA PACIFIC TO DOMINATE MARKET DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

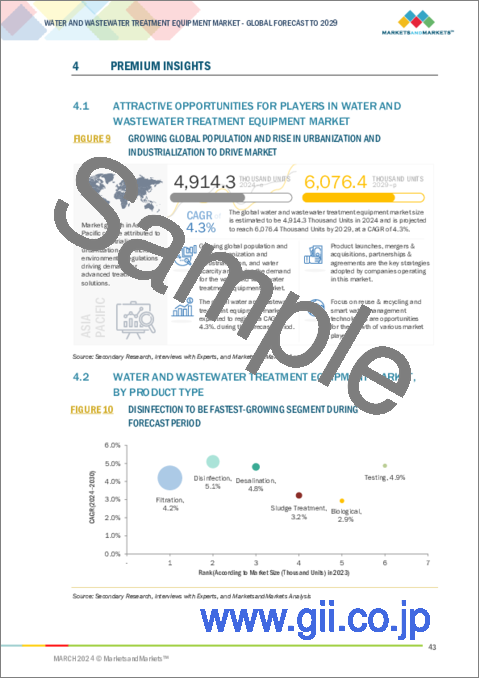

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- FIGURE 9 GROWING GLOBAL POPULATION AND RISE IN URBANIZATION AND INDUSTRIALIZATION TO DRIVE MARKET

- 4.2 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE

- FIGURE 10 DISINFECTION TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- 4.3 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS

- FIGURE 11 TERTIARY TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- 4.4 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER

- FIGURE 12 INDUSTRIAL TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- 4.5 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY

- FIGURE 13 INDIA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 14 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Water scarcity and lack of freshwater driving adoption of sustainable water management practices

- 5.2.1.2 Increase in industrial water consumption and discharge

- 5.2.1.3 Growing global population and rise in urbanization and industrialization

- 5.2.2 RESTRAINTS

- 5.2.2.1 Stringent regulation in wastewater industry

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Smart water management & data analytics

- 5.2.3.2 Focus on water reuse & recycling

- 5.2.3.3 Growing demand for energy-efficient water treatment technologies

- 5.2.4 CHALLENGES

- 5.2.4.1 High installation, equipment, and operation costs

- 5.2.4.2 Aging infrastructure and lack of financing

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESSES

- 6.2.1 REVENUE SHIFT AND NEW REVENUE POCKETS FOR WATER & WASTEWATER TREATMENT EQUIPMENT MANUFACTURERS

- FIGURE 15 REVENUE SHIFT OF WATER & WASTEWATER TREATMENT EQUIPMENT MARKET

- 6.3 PRICING ANALYSIS

- 6.3.1 AVERAGE SELLING PRICE TREND, BY REGION

- FIGURE 16 WATER & WASTEWATER TREATMENT EQUIPMENT MARKET: AVERAGE SELLING PRICE TREND, BY REGION, 2020-2029

- 6.3.2 INDICATIVE PRICING ANALYSIS, BY PRODUCT TYPE

- 6.4 VALUE CHAIN ANALYSIS

- FIGURE 17 VALUE CHAIN ANALYSIS

- 6.4.1 EQUIPMENT MANUFACTURERS

- 6.4.2 DISTRIBUTORS

- 6.4.3 INSTALLATION & OPERATIONAL SERVICES

- 6.4.4 END USERS

- 6.5 ECOSYSTEM/MARKET MAP

- TABLE 1 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: ECOSYSTEM

- 6.6 TECHNOLOGY ANALYSIS

- TABLE 2 KEY TECHNOLOGIES OFFERED IN WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- TABLE 3 COMPLEMENTARY TECHNOLOGIES OFFERED IN WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- TABLE 4 ADJACENT TECHNOLOGIES OFFERED FOR WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- 6.7 PATENT ANALYSIS

- 6.7.1 INTRODUCTION

- 6.7.2 METHODOLOGY

- 6.7.3 DOCUMENT TYPE

- TABLE 5 GRANTED PATENTS ACCOUNT FOR 20.8% OF TOTAL COUNT IN LAST 10 YEARS

- 6.7.3.1 Publication trends over last ten years

- FIGURE 18 NUMBER OF PATENTS GRANTED YEARLY OVER LAST 10 YEARS

- 6.7.4 INSIGHTS

- 6.7.5 LEGAL STATUS OF PATENTS

- 6.7.6 JURISDICTION ANALYSIS

- FIGURE 19 REGIONAL ANALYSIS OF PATENT GRANTED FOR WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, 2023

- 6.7.7 TOP COMPANIES/APPLICANTS

- FIGURE 20 TOP TEN COMPANIES WITH HIGHEST NUMBER OF PATENTS IN LAST TEN YEARS

- TABLE 6 MAJOR PATENTS FOR WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- 6.7.8 MAJOR PATENTS

- TABLE 7 MAJOR PATENTS FOR WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- 6.8 TRADE ANALYSIS

- 6.8.1 IMPORT SCENARIO

- FIGURE 21 IMPORT OF WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2019-2022

- 6.8.2 EXPORT SCENARIO

- FIGURE 22 EXPORT OF WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET BY COUNTRY, 2019-2022

- 6.9 KEY CONFERENCES & EVENTS IN 2024-2025

- TABLE 8 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

- 6.10 CASE STUDY

- 6.10.1 CASE STUDY FROM VEOLIA ABOUT BIOLOGICAL PACKAGED WASTEWATER TREATMENT UNITS ENSURES SAFE AND RELIABLE SEWAGE TREATMENT THROUGHOUT KUWAIT

- 6.10.2 CASE STUDY ABOUT XYLEM'S JABSCO BRAND PARTNERS WITH SWISS FRESH WATER ON INNOVATIVE REVERSE OSMOSIS WATER TREATMENT SOLUTION

- 6.10.3 CASE STUDY ABOUT KOREAN AUTOMAKER REDUCING WASTEWATER SLUDGE WITH EXPERT SUPPORT FROM NALCO WATER

- 6.11 TARIFF AND REGULATORY LANDSCAPE

- 6.11.1 TARIFF AND REGULATIONS RELATED TO WATER AND WASTEWATER TREATMENT EQUIPMENT

- TABLE 9 TARIFFS RELATED TO WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- 6.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.12 PORTER'S FIVE FORCES ANALYSIS

- TABLE 15 PORTERS 5 FORCES IMPACT ON WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- FIGURE 23 PORTER'S FIVE FORCES ANALYSIS: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET

- 6.12.1 THREAT OF NEW ENTRANTS

- 6.12.2 THREATS OF SUBSTITUTES

- 6.12.3 BARGAINING POWER OF SUPPLIERS

- 6.12.4 BARGAINING POWER OF BUYERS

- 6.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.12.6 VOLUME DATA

- 6.12.7 GDP TRENDS AND FORECASTS OF MAJOR ECONOMIES

- TABLE 16 PROJECTED REAL GDP GROWTH (ANNUAL PERCENTAGE CHANGE) OF KEY COUNTRIES, 2018-2025

- 6.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 24 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP 2 APPLICATIONS

- TABLE 17 INFLUENCE OF INSTITUTIONAL BUYERS ON BUYING PROCESS FOR TOP 2 APPLICATIONS

- 6.13.2 BUYING CRITERIA

- FIGURE 25 KEY BUYING CRITERIA FOR APPLICATION

- TABLE 18 KEY BUYING CRITERIA FOR APPLICATIONS

- 6.14 INVESTMENT AND FUNDING SCENARIO

- FIGURE 26 INVESTOR DEALS AND FUNDING IN WATER AND WASTEWATER TREATMENT EQUIPMENT SOARED IN 2023

7 WATER AND WASTEWATER TREATMENT MARKET, BY TYPE

- 7.1 INTRODUCTION

- FIGURE 27 FILTRATION SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 19 WATER AND WASTEWATER TREATMENT MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 20 WATER AND WASTEWATER TREATMENT MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 21 WATER AND WASTEWATER TREATMENT MARKET, BY TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 22 WATER AND WASTEWATER TREATMENT MARKET, BY TYPE, 2024-2029 (THOUSAND UNITS)

- 7.2 FILTRATION

- 7.2.1 MULTI-LAYERED DEFENSE SYSTEMS TO DRIVE DEMAND

- 7.2.2 GRANULAR/SAND FILTRATION

- 7.2.3 REVERSE OSMOSIS (RO)

- 7.2.4 MICROFILTRATION (MF)

- 7.2.5 OTHER TYPES

- 7.3 DISINFECTION

- 7.3.1 DISINFECTION SECURING WATER QUALITY THROUGH PATHOGEN ELIMINATION TO DRIVE MARKET

- 7.3.2 CHLORINE

- 7.3.3 ULTRAVIOLET

- 7.3.4 OZONE

- 7.3.5 OTHER DISINFECTIONS

- 7.4 DESALINATION

- 7.4.1 HIGH DEMAND FOR FRESHWATER IN WATER-SCARCE REGIONS TO DRIVE MARKET

- 7.5 SLUDGE TREATMENT

- 7.5.1 GROWING IMPORTANCE OF ENVIRONMENTAL PROTECTION AND RESOURCE RECOVERY TO DRIVE MARKET

- 7.6 BIOLOGICAL

- 7.6.1 MICROORGANISMS BREAKING DOWN POLLUTANTS TO IMPROVE WATER QUALITY SUSTAINABLY TO DRIVE MARKET

- 7.7 TESTING

- 7.7.1 BETTER WATER QUALITY, TREATMENT EFFICIENCY, AND REGULATORY COMPLIANCE TO DRIVE MARKET

8 WATER & WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS

- 8.1 INTRODUCTION

- FIGURE 28 TERTIARY BY PROCESS TO LEAD MARKET DURING FORECAST PERIOD (2024-2029)

- TABLE 23 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS, 2020-2023 (USD MILLION)

- TABLE 24 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS, 2024-2029 (USD MILLION)

- 8.2 PRIMARY

- 8.2.1 REDUCING ORGANIC LOAD IN WASTEWATER, MAKING SUBSEQUENT TREATMENT STAGES MORE EFFICIENT, TO DRIVE MARKET

- 8.3 SECONDARY

- 8.3.1 BIOLOGICAL ACTIVITY ENHANCES WATER QUALITY AND SUPPORTS ECOLOGICAL BALANCE IN AQUATIC ENVIRONMENTS

- 8.4 TERTIARY

- 8.4.1 PRECISE CONTROL, HIGH EFFICIENCY, AND VERSATILITY IN REMOVING SPECIFIC CONTAMINANTS AND IMPROVING WATER CLARITY AND SAFETY TO DRIVE MARKET

9 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER

- 9.1 INTRODUCTION

- FIGURE 29 MUNICIPAL SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD (USD MILLION)

- TABLE 25 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 26 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2030 (USD MILLION)

- 9.2 MUNICIPAL

- 9.2.1 ENSURING CLEAN WATER SUPPLY AND EFFECTIVE WASTEWATER MANAGEMENT FOR RESIDENTIAL AREAS AND COMMERCIAL BUSINESSES TO DRIVE MARKET

- 9.2.2 RESIDENTIAL

- 9.2.3 COMMERCIAL

- 9.3 INDUSTRIAL

- 9.3.1 PROMOTING SUSTAINABILITY AND ENVIRONMENT CONSCIOUSNESS THROUGH EFFECTIVE WATER MANAGEMENT AND WASTEWATER TREATMENT AND DISPOSAL

- 9.3.2 OIL & GAS

- 9.3.3 PULP &PAPER

- 9.3.4 CHEMICALS

- 9.3.5 FOOD & BEVERGAE

- 9.3.6 OTHER END USERS

10 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 30 ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- TABLE 27 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 28 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 29 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY REGION, 2020-2023 (THOUSAND UNITS)

- TABLE 30 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY REGION, 2024-2029 (THOUSAND UNITS)

- 10.2 ASIA PACIFIC

- FIGURE 31 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET SNAPSHOT

- 10.2.1 RECESSION IMPACT

- TABLE 31 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 32 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 33 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (THOUSAND UNITS)

- TABLE 34 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (THOUSAND UNITS)

- TABLE 35 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 36 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 37 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 38 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (THOUSAND UNITS)

- TABLE 39 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS, 2020-2023 (USD MILLION)

- TABLE 40 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS, 2024-2029 (USD MILLION)

- TABLE 41 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER 2020-2023 (USD MILLION)

- TABLE 42 ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER 2024-2029 (USD MILLION)

- 10.2.2 CHINA

- 10.2.2.1 Rapid urbanization and population growth to drive market

- TABLE 43 CHINA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 44 CHINA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 45 CHINA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER 2020-2023 (USD MILLION)

- TABLE 46 CHINA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER 2024-2029 (USD MILLION)

- 10.2.3 JAPAN

- 10.2.3.1 Focus on advanced technologies, stringent regulations, and commitment to sustainable water management to drive market

- TABLE 47 JAPAN: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 48 JAPAN: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 49 JAPAN: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 50 JAPAN: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.2.4 INDIA

- 10.2.4.1 Need for advanced water and wastewater treatment to drive market

- TABLE 51 INDIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 52 INDIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 53 INDIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER 2020-2023 (USD MILLION)

- TABLE 54 INDIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER 2024-2029 (USD MILLION)

- 10.2.5 SOUTH KOREA

- 10.2.5.1 Limited freshwater resources and growing emphasis on water reuse in high-tech industries

- TABLE 55 SOUTH KOREA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 56 SOUTH KOREA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 57 SOUTH KOREA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 58 SOUTH KOREA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.2.6 AUSTRALIA

- 10.2.6.1 Robust government investment in water infrastructure and evolving trends in wastewater treatment technology adoption to drive market

- TABLE 59 AUSTRALIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 60 AUSTRALIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 61 AUSTRALIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 62 AUSTRALIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.2.7 REST OF ASIA PACIFIC

- TABLE 63 REST OF ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 64 REST OF ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 65 REST OF ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 66 REST OF ASIA PACIFIC: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3 EUROPE

- FIGURE 32 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET SNAPSHOT

- 10.3.1 RECESSION IMPACT

- TABLE 67 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 68 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 69 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (THOUSAND UNITS)

- TABLE 70 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (THOUSAND UNITS)

- TABLE 71 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 72 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 73 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 74 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (THOUSAND UNITS)

- TABLE 75 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS, 2020-2023 (USD MILLION)

- TABLE 76 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS, 2024-2029 (USD MILLION)

- TABLE 77 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 78 EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.2 GERMANY

- 10.3.2.1 Increased public awareness and stringent government regulations to drive market

- TABLE 79 GERMANY: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 80 GERMANY: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 81 GERMANY: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 82 GERMANY: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.3 UK

- 10.3.3.1 Strict regulations and high compliance rates in wastewater treatment to drive demand

- TABLE 83 UK: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 84 UK: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 85 UK: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 86 UK: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.4 FRANCE

- 10.3.4.1 Continuous maintenance and replacement of aging infrastructure to fuel demand for equipment and services

- TABLE 87 FRANCE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 88 FRANCE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 89 FRANCE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 90 FRANCE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.5 ITALY

- 10.3.5.1 Aging infrastructure and investments in wastewater treatment sectors to drive market

- TABLE 91 ITALY: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 92 ITALY: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 93 ITALY: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 94 ITALY: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.6 RUSSIA

- 10.3.6.1 Need for infrastructure modernization and tackling water bodies pollution to drive market

- TABLE 95 RUSSIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 96 RUSSIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 97 RUSSIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 98 RUSSIA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.7 REST OF EUROPE

- TABLE 99 REST OF EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 100 REST OF EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 101 REST OF EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 102 REST OF EUROPE: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4 NORTH AMERICA

- FIGURE 33 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET SNAPSHOT

- 10.4.1 RECESSION IMPACT

- TABLE 103 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 104 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 105 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (THOUSAND UNITS)

- TABLE 106 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (THOUSAND UNITS)

- TABLE 107 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 108 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 109 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 110 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (THOUSAND UNITS)

- TABLE 111 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS, 2020-2023 (USD MILLION)

- TABLE 112 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PROCESS, 2024-2029 (USD MILLION)

- TABLE 113 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 114 NORTH AMERICA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.2 US

- 10.4.2.1 Increased emphasis on water reuse initiatives to drive demand for advanced water and wastewater treatment equipment

- TABLE 115 US: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 116 US: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 117 US: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 118 US: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.3 CANADA

- 10.4.3.1 Drive for comprehensive wastewater treatment to safeguard environmental and human health through advanced treatment technologies and infrastructure investments to drive market

- TABLE 119 CANADA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 120 CANADA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 121 CANADA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 122 CANADA: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.4 MEXICO

- 10.4.4.1 Government investments to aging water infrastructure upgrade to drive market

- TABLE 123 MEXICO: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 124 MEXICO: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 125 MEXICO: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 126 MEXICO: WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5 SOUTH AMERICA

- 10.5.1 RECESSION IMPACT

- TABLE 127 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 128 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 129 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (THOUSAND UNITS)

- TABLE 130 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (THOUSAND UNITS)

- TABLE 131 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 132 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 133 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 134 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (THOUSAND UNITS)

- TABLE 135 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PROCESS, 2020-2023 (USD MILLION)

- TABLE 136 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PROCESS, 2024-2029 (USD MILLION)

- TABLE 137 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 138 SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5.2 BRAZIL

- 10.5.2.1 Well-established government plans to conserve water and reuse wastewater in industrial sectors to propel demand

- TABLE 139 BRAZIL: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 140 BRAZIL: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 141 BRAZIL: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 142 BRAZIL: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5.3 ARGENTINA

- 10.5.3.1 Substantial foreign investments in industrial sector to drive demand

- TABLE 143 ARGENTINA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 144 ARGENTINA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 145 ARGENTINA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 146 ARGENTINA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5.4 REST OF SOUTH AMERICA

- TABLE 147 REST OF SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 148 REST OF SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 149 REST OF SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 150 REST OF SOUTH AMERICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.6 MIDDLE EAST AND AFRICA

- 10.6.1 RECESSION IMPACT

- TABLE 151 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 152 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 153 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY COUNTRY, 2020-2023 (THOUSAND UNITS)

- TABLE 154 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY COUNTRY, 2024-2029 (THOUSAND UNITS)

- TABLE 155 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 156 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 157 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 158 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (THOUSAND UNITS)

- TABLE 159 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PROCESS, 2020-2023 (USD MILLION)

- TABLE 160 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PROCESS, 2024-2029 (USD MILLION)

- TABLE 161 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 162 MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.6.2 SAUDI ARABIA

- 10.6.2.1 Well-established oil & gas industry coupled with ambitious infrastructure development projects to drive market

- TABLE 163 SAUDI ARABIA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 164 SAUDI ARABIA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 165 SAUDI ARABIA: WATER & WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 166 SAUDI ARABIA: WATER & WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.6.3 UAE

- 10.6.3.1 Strategic investments in wastewater treatment plants to drive market

- TABLE 167 UAE: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 168 UAE: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 169 UAE: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 170 UAE: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.6.4 SOUTH AFRICA

- 10.6.4.1 Strategic approach to water security and water treatment to drive market

- TABLE 171 SOUTH AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 172 SOUTH AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 173 SOUTH AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 174 SOUTH AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.6.5 REST OF GCC COUNTRIES

- 10.6.5.1 Rest of GCC countries combating water pollution, safeguarding natural water sources, and promoting sustainable water management to drive market

- TABLE 175 REST OF GCC COUNTRIES: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 176 REST OF GCC COUNTRIES: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 177 REST OF GCC COUNTRIES: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 178 REST OF GCC COUNTRIES: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.6.6 REST OF MIDDLE EAST & AFRICA

- TABLE 179 REST OF MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2020-2023 (USD MILLION)

- TABLE 180 REST OF MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY PRODUCT TYPE, 2024-2029 (USD MILLION)

- TABLE 181 REST OF MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 182 REST OF MIDDLE EAST & AFRICA: WATER AND WASTEWATER EQUIPMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY WATER AND WASTEWATER TREATMENT EQUIPMENT MANUFACTURERS

- 11.3 MARKET SHARE ANALYSIS

- 11.3.1 RANKING OF KEY MARKET PLAYERS, 2023

- FIGURE 34 RANKING OF TOP FIVE PLAYERS IN WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, 2023

- 11.3.2 MARKET SHARE OF KEY PLAYERS

- TABLE 183 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: DEGREE OF COMPETITION

- FIGURE 35 SHARE OF KEY PLAYERS IN WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET, 2023

- 11.3.2.1 VEOLIA (FRANCE)

- 11.3.2.2 XYLEM (US)

- 11.3.2.3 ECOLAB (US)

- 11.3.2.4 DUPONT (US)

- 11.3.2.5 PENTAIR (UK)

- 11.4 REVENUE ANALYSIS

- FIGURE 36 REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024

- 11.5 BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 37 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY SEGMENTS

- 11.6 COMPANY EVALUATION MATRIX: KEY PLAYERS 2023

- 11.6.1 STARS

- 11.6.2 EMERGING LEADERS

- 11.6.3 PERVASIVE PLAYERS

- 11.6.4 PARTICIPANTS

- FIGURE 38 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: COMPANY EVALUATION MATRIX, 2023

- 11.6.5 COMPANY FOOTPRINT

- FIGURE 39 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: COMPANY FOOTPRINT

- TABLE 184 COMPANY END-USER FOOTPRINT (10 COMPANIES)

- TABLE 185 COMPANY BY PROCESS FOOTPRINT (10 COMPANIES)

- TABLE 186 COMPANY PRODUCT TYPE FOOTPRINT (10 COMPANIES)

- TABLE 187 COMPANY REGION FOOTPRINT (10 COMPANIES)

- 11.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023.

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 RESPONSIVE COMPANIES

- 11.7.3 DYNAMIC COMPANIES

- 11.7.4 STARTING BLOCKS

- FIGURE 40 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: STARTUPS/SMES EVALUATION MATRIX, 2022

- 11.7.5 COMPETITIVE BENCHMARKING

- TABLE 188 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- 11.7.5.1 Competitive benchmarking of key startups/SMEs

- TABLE 189 STARTUPS/SMES END-USER FOOTPRINT (14 COMPANIES)

- TABLE 190 STARTUPS/SMES PROCESS FOOTPRINT (14 COMPANIES)

- TABLE 191 STARTUPS/SMES PRODUCT TYPE FOOTPRINT (14 COMPANIES)

- TABLE 192 STARTUPS/SMES REGION FOOTPRINT (14 COMPANIES)

- 11.7.6 VALUATION AND FINANCIAL METRICS OF WATER WASTEWATER TREATMENT EQUIPMENT VENDORS

- FIGURE 41 EV/EBITDA OF KEY VENDORS

- FIGURE 42 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- 11.8 COMPETITIVE SCENARIO AND TRENDS

- 11.8.1 PRODUCT LAUNCHES

- TABLE 193 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: PRODUCT LAUNCHES, JANUARY 2020-2024 DECEMBER

- 11.8.2 DEALS

- TABLE 194 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: DEALS, JANUARY 2020-DECEMBER 2024

- 11.8.3 EXPANSIONS

- TABLE 195 WATER AND WASTEWATER TREATMENT EQUIPMENT MARKET: EXPANSIONS, JANUARY 2021-DECEMBER 2023

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- (Business overview, Products/Solutions/Services offered, Recent developments, MnM view, Key strategies, Strategic choices made, and Weaknesses and Competitive threats)**

- 12.1.1 VEOLIA

- TABLE 196 VEOLIA: COMPANY OVERVIEW

- FIGURE 43 VEOLIA: COMPANY SNAPSHOT

- TABLE 197 VEOLIA: PRODUCT OFFERINGS

- TABLE 198 VEOLIA: DEALS, 2021-2023

- 12.1.2 XYLEM

- TABLE 199 XYLEM: COMPANY OVERVIEW

- FIGURE 44 XYLEM: COMPANY SNAPSHOT

- TABLE 200 XYLEM: PRODUCT OFFERINGS

- TABLE 201 XYLEM: DEALS, 2021-2024

- TABLE 202 XYLEM: OTHER DEVELOPMENTS, 2022-2023

- 12.1.3 ECOLAB

- TABLE 203 ECOLAB: COMPANY OVERVIEW

- FIGURE 45 ECOLAB: COMPANY SNAPSHOT

- TABLE 204 ECOLAB: PRODUCT OFFERINGS

- TABLE 205 ECOLAB: PRODUCT LAUNCHES, 2021-2024

- TABLE 206 ECOLAB: DEALS, 2021-2024

- 12.1.4 DUPONT

- TABLE 207 DUPONT: COMPANY OVERVIEW

- FIGURE 46 DUPONT: COMPANY SNAPSHOT

- TABLE 208 DUPONT: PRODUCT OFFERINGS

- TABLE 209 DUPONT: PRODUCT LAUNCHES, 2021-2023

- TABLE 210 DUPONT: DEALS, 2021-2023

- 12.1.5 PENTAIR

- TABLE 211 PENTAIR: COMPANY OVERVIEW

- FIGURE 47 PENTAIR: COMPANY SNAPSHOT

- TABLE 212 PENTAIR: PRODUCT OFFERINGS

- TABLE 213 PENTAIR: PRODUCT LAUNCHES, 2021-2022

- TABLE 214 PENTAIR: DEALS, 2021-2023

- 12.1.6 3M

- TABLE 215 3M: COMPANY OVERVIEW

- FIGURE 48 3M: COMPANY SNAPSHOT

- TABLE 216 3M: PRODUCT OFFERINGS

- TABLE 217 3M: DEALS, 2021-2023

- TABLE 218 3M: OTHER DEVELOPMENTS, 2021-2023

- 12.1.7 AQUATECH INTERNATIONAL

- TABLE 219 AQUATECH INTERNATIONAL: COMPANY OVERVIEW

- TABLE 220 AQUATECH INTERNATIONAL: PRODUCT OFFERINGS

- TABLE 221 AQUATECH INTERNATIONAL: PRODUCT LAUNCHES (2021-2023)

- TABLE 222 AQUATECH INTERNATIONAL: DEALS, 2021-2023

- 12.1.8 THERMAX LIMITED

- TABLE 223 THERMAX LIMITED: COMPANY OVERVIEW

- FIGURE 49 THERMAX LIMITED: COMPANY SNAPSHOT

- TABLE 224 THERMAX LIMITED: PRODUCT OFFERINGS

- TABLE 225 THERMAX LIMITED: PRODUCT LAUNCHES, 2020-2023

- TABLE 226 THERMAX LIMITED: DEALS, 2021-2024

- 12.1.9 CULLIGAN WATER

- TABLE 227 CULLIGAN WATER: COMPANY OVERVIEW

- TABLE 228 CULLIGAN WATER: PRODUCT OFFERINGS

- TABLE 229 CULLIGAN WATER: PRODUCT LAUNCHES, 2020-2023

- TABLE 230 CULLIGAN WATER: DEALS, 2020-2024

- TABLE 231 CULLIAGN WATER: EXPANSIONS, 2022-2023

- 12.1.10 CALGON CARBON CORPORATION

- TABLE 232 CALGON CARBON CORPORATION: COMPANY OVERVIEW

- TABLE 233 CALGON CARBON CORPORATION: PRODUCT OFFERINGS

- TABLE 234 CALGON CARBON CORPORATION: DEALS, 2020-2024

- TABLE 235 CALGON CARBON CORPORATION: EXPANSIONS, 2022-2023

- 12.2 OTHER PLAYERS

- 12.2.1 TORAY INDUSTRIES, INC.

- TABLE 236 TORAY INDUSTRIES, INC.: COMPANY OVERVIEW

- 12.2.2 HITACHI, LTD.

- TABLE 237 HITACHI, LTD.: COMPANY OVERVIEW

- 12.2.3 IEI (ION EXCHNAGE)

- TABLE 238 IEI (ION EXCHNAGE): COMPANY OVERVIEW

- 12.2.4 BWT

- TABLE 239 BWT: COMPANY OVERVIEW

- 12.2.5 DANAHER

- TABLE 240 DANAHER: COMPANY OVERVIEW

- 12.2.6 CHEMBOND CHEMICALS LIMITED

- TABLE 241 CHEMBOND CHEMICALS LIMITED: COMPANY OVERVIEW

- 12.2.7 KURITA WATER INDUSTRIES LTD

- TABLE 242 KURITA WATER INDUSTRIES LTD: COMPANY OVERVIEW

- 12.2.8 INPHLOX WATER SYSTEMS PVT LTD.

- TABLE 243 INPHLOX WATER SYSTEMS PVT LTD.: COMPANY OVERVIEW

- 12.2.9 MITA WATER TECHNOLOGIES S.R.L.

- TABLE 244 MITA WATER TECHNOLOGIES S.R.L.: COMPANY OVERVIEW

- 12.2.10 GRACE GREEN INFRA

- TABLE 245 GRACE GREEN INFRA: COMPANY OVERVIEW

- 12.2.11 FLUENCE CORPORATION LIMITED

- TABLE 246 FLUENCE CORPORATION LIMITED: COMPANY OVERVIEW

- 12.2.12 KOVALUS SEPARATION SOLUTIONS

- TABLE 247 KOVALUS SEPARATION SOLUTIONS: COMPANY OVERVIEW

- 12.2.13 TOSHIBA WATER SOLUTIONS PRIVATE LIMITED

- TABLE 248 TOSHIBA WATER SOLUTIONS PRIVATE LIMITED: COMPANY OVERVIEW

- 12.2.14 A.O. SMITH WATER TECHNOLOGIES

- TABLE 249 A.O. SMITH WATER TECHNOLOGIES: COMPANY OVERVIEW

- 12.2.15 ECOLOGIX ENVIRONMENTAL SYSTEMS

- TABLE 250 ECOLOGIX ENVIRONMENTAL SYSTEMS: COMPANY OVERVIEW

- *Details on Business overview, Products/Solutions/Services offered, Recent developments, MnM view, Key strategies, Strategic choices made, and Weaknesses and Competitive threats might not be captured in case of unlisted companies.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS