|

|

市場調査レポート

商品コード

1458542

南北アメリカのケーブル市場:ポリマー/絶縁タイプ別、半導電層別、用途別、電圧別、エンドユーザー別、地域別 - 予測(~2029年)Americas Cables Market by Polymer and Insulation Type (Semiconducting polymer, XLPE, EPR, HEPR, low Voltage Cables), Semiconducting Layer (Inner & Outer Semiconducting layer), Application, Voltage, End User & Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 南北アメリカのケーブル市場:ポリマー/絶縁タイプ別、半導電層別、用途別、電圧別、エンドユーザー別、地域別 - 予測(~2029年) |

|

出版日: 2024年03月28日

発行: MarketsandMarkets

ページ情報: 英文 272 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

南北アメリカのケーブルの市場規模は、2024年の87億米ドルから2029年までに109億米ドルに達すると推定され、予測期間にCAGRで4.5%の成長が見込まれます。

市場は、産業の成長、都市化、インフラ開発によって拡大しています。また、電気、通信、再生可能エネルギーに対する需要の高まりも、最先端のケーブルソリューションに対するニーズに拍車をかけています。さらに、スマートケーブルシステムや高性能絶縁材料の開発など、ケーブル製造産業の技術開発が市場拡大を促進しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2022年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 単位 | 米ドル |

| セグメント | ポリマー/絶縁タイプ、半導電層、定格電圧、用途、エンドユーザー、地域 |

| 対象地域 | 北米、南米、中米 |

「エンドユーザー別では、再生可能エネルギーセグメントが南北アメリカケーブル市場の最速のセグメントです。」

再生可能エネルギーセグメントの成長は、太陽光発電所や風力発電所のような再生可能エネルギープロジェクトの急速な拡大によるものです。グリッド接続や送電に、これらのプロジェクトは多くのケーブルを必要とします。再生可能エネルギーセグメントの成長は、グリーンエネルギーに対する政府の支援の高まり、技術開発、持続可能なエネルギーソリューションに対する需要の高まりによっても促進されます。太陽光発電や風力発電施設などの再生可能エネルギー用途に適した高品質ケーブルは、信頼性が高く効果的な送配電システムに向けたこの拡張の要件により、需要が高まっています。

「半導電層別では、内部半導電層がもっとも急成長するセグメントとなることが予測されます。」

内部半導電層はケーブルの性能と信頼性を向上させる重要な役割を担っているため、市場の内部半導電層セグメントはもっとも急成長すると予測されます。この層は、電界を均一に分布させ電気的ストレスの集中を低下させることでケーブルの寿命を延ばし、絶縁不良の可能性を低下させます。

「用途別では、地下が最大のセグメントとなる見込みです。

市場では、都市化とインフラ開発が進むにつれて地下ケーブルの需要が高まっています。これらは架空電線と比較して、信頼性の向上、環境への影響の低減、視覚的な魅力などの多くの利点があります。地下ケーブルは、都市化の進行や人口密集地における信頼性の高い配電の必要性から、ますます需要が高まっています。その結果、地下ケーブルは市場拡大の大きな促進要因となっています。

「北米が市場で最大の地域となる見込みです。」

同地域の強固な工業インフラによって南北アメリカのケーブル市場は拡大しており、このことが製造、石油・ガス産業、自動車産業などからの需要を促進しています。また、特に米国とカナダで再生可能エネルギーへの取り組みが活発化していることも、需要を増加させています。また、データセンターや通信といった強力な商業も市場を牽引しています。業界における北米の優位性は、都市化プロジェクトにおける地中ケーブルの広範な利用や、オフショアエネルギー施設向けの海底ケーブルの展開によってさらに強化されています。

当レポートでは、南北アメリカのケーブル市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 南北アメリカのケーブル市場における企業にとって魅力的な機会

- 南北アメリカのケーブル市場:地域別

- 北米のケーブル市場:エンドユーザー別、国別

- 南北アメリカのケーブル市場:ポリマー/絶縁タイプ別

- 南北アメリカのケーブル市場:半導電層別

- 南北アメリカのケーブル市場:エンドユーザー別

- 南北アメリカのケーブル市場:電圧定格別

- 南北アメリカのケーブル市場:用途別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 顧客ビジネスに影響を与える動向/混乱

- エコシステム分析

- 南北アメリカのケーブル市場における投資と資金調達の情勢

- バリューチェーン分析

- 技術分析

- コア技術

- 補完技術

- 隣接技術

- 特許分析

- 貿易分析

- HSコード8544に準拠した製品の貿易分析

- 輸出データ

- 輸入データ

- 価格分析

- 規制情勢

- 規制機関、政府機関、その他の組織

- 南北アメリカのケーブルに関する規制

- 関税分析

- ポーターのファイブフォース分析

- ケーススタディ分析

- 主なステークホルダーと購入基準

- 主な会議とイベント(2024年)

第6章 南北アメリカのケーブル市場:ポリマー/絶縁タイプ別

- イントロダクション

- 半導電ポリマーケーブル

- XLPEケーブル

- EPR/EPDMケーブル

- HEPRケーブル

- 低電圧ケーブル

第7章 南北アメリカのケーブル市場:半導電層別

- イントロダクション

- 内部

- 外部

第8章 南北アメリカのケーブル市場:電圧定格別

- イントロダクション

- 5KV以下

- 5~8KV

- 8~15KV

- 15~35KV

- 35~46KV

- 69KV

- 115KV

- 138KV

第9章 南北アメリカのケーブル市場:用途別

- イントロダクション

- 地下

- 海底

第10章 南北アメリカのケーブル市場:エンドユーザー別

- イントロダクション

- 工業部門

- ユーティリティ

- 石油・ガス

- 化学・石油化学

- 金属・鉱業

- 製造

- セメント

- その他の工業エンドユーザー

- 再生可能エネルギー部門

- 太陽光発電所

- 風力発電所

- 商業部門

第11章 南北アメリカのケーブル市場:地域別

- イントロダクション

- 北米

- 景気後退の影響:北米

- 米国

- カナダ

- メキシコ

- 中米

- 景気後退の影響:中米

- グアテマラ

- パナマ

- コスタリカ

- 南米

- 景気後退の影響:南米

- ブラジル

- アルゼンチン

- ベネズエラ

- その他の南米

第12章 競合情勢

- 主要企業が採用した戦略

- 上位5社の市場シェア分析(2023年)

- 南北アメリカのケーブル市場における上位5社の収益分析(2018年~2022年)

- 企業の評価マトリクス、主要企業(2023年)

- 企業の評価マトリクス:スタートアップ/中小企業(2023年)

- 南北アメリカの大手ケーブルベンダーの企業評価と財務指標

- ブランド/製品の比較分析

- 競合シナリオと動向

第13章 企業プロファイル

- 主要企業

- PRYSMIAN GROUP

- SOUTHWIRE COMPANY, LLC

- NEXANS

- LS CABLE & SYSTEM LTD.

- NKT A/S

- AMPHENOL TPC

- BELDEN INC.

- LEONI

- BIZLINK GROUP

- SUMITOMO ELECTRIC INDUSTRIES, LTD.

- THE OKONITE COMPANY

- TFKABLE

- TRATOS

- ZTT

- HELUKABEL GROUP

- その他の企業(絶縁製品、サービスプロバイダー)

- DOW

- FURUKAWA ELECTRIC CO., LTD.

- ZHEJIANG WANMA CO., LTO.

- HANWHA GROUP

- TRELLEBORG GROUP

- BOREALIS AG

- AVIENT CORPORATION

- SACO AEI POLYMERS

- HJ POLYMER CHINA CO., LTD.

- WTEC ENERGY INNOVATION

- PRAMKOR

- ELECTRIC CABLE COMPOUNDS, INC.

- MIXER S.P.A.

第14章 付録

The Americas Cables market is estimated to grow from USD 10.9 billion by 2029 from an estimated USD 8.7 billion in 2024, at a CAGR of 4.5% during the forecast period. The market for cables in the Americas is expanding due to rising industry, urbanization, and infrastructure development. The need for cutting-edge cable solutions is also fueled by the growing demand for electricity, telecommunications, and renewable energy initiatives. Additionally, technological developments in the cable manufacturing industry, like the creation of smart cable systems and high-performance insulation materials, are driving market expansion.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD) |

| Segments | Polymer and Insulation type, Semiconducting Layer, Voltage rating, Application, End User and Region |

| Regions covered | North America, South America, and Central America |

"Renewable Energy Sector segment is the fastest segment of the Americas Cables market, by end user."

Based on end user, the Americas Cables market has been split into three types: industrial, renewables, and commercial. The renewables segment growth is due to the rapid expansion of renewable energy projects like as solar and wind farms. For grid connectivity and power transfer, these projects need a lot of cabling. Growth in the renewable energy sector is also driven by rising government support for green energy, technological developments, and growing demand for sustainable energy solutions. High-quality cables appropriate for renewable energy applications, such as solar and wind power installations, are in high demand due to this expansion's requirement for reliable, effective power transmission and distribution systems.

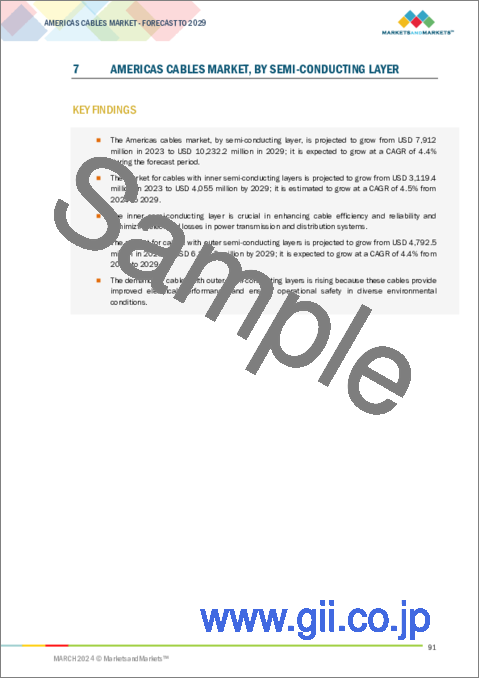

"Inner Semiconducting Layer is expected to emerge as the fastest-growing segment based on semiconducting layer."

Based on semiconducting layer, the Americas Cables market has been segmented into inner semiconducting layer and outer semiconducting layer. The inner semiconducting layer segment of the Americas Cables Market is expected to be the fastest-growing due to its importance in increasing cable performance and dependability. By distributing the electric field uniformly and lowering electrical stress concentrations, this layer prolongs the life of cables and lowers the possibility of insulation failure.

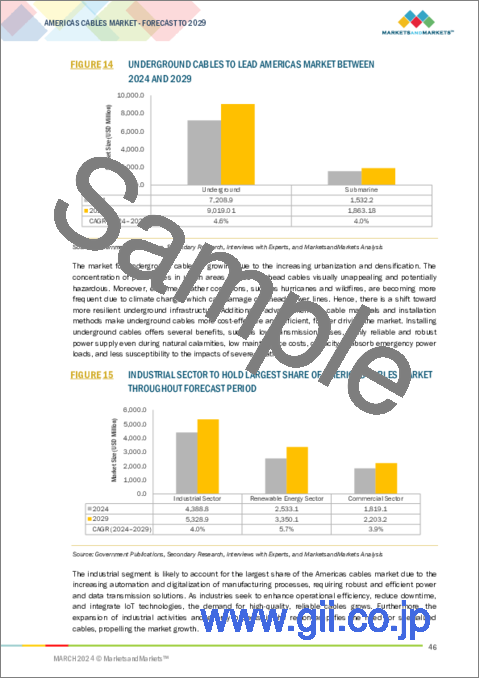

"Underground is expected to be the largest segment based on application."

Demand for underground cables is increasing in the Americas Cables Market as urbanization and infrastructure development continue. When compared to overhead wires, they have many advantages, including improved dependability, decreased environmental effect, and visual attractiveness. Subterranean cables are becoming more and more in demand due to growing urbanization initiatives and the necessity for dependable power distribution in densely populated areas. As a result, they are becoming a major factor driving market expansion.

"North America is expected to emerge as the largest region based on Americas Cables market."

By region, the Americas Cables market has been segmented into Asia Pacific, North America, South America, and Central America. In the region, the Americas Cables market is expanding in North America because of the region's robust industrial infrastructure, which fuels demand from sectors including manufacturing, oil and gas, and the automotive industry; industrial end-users play a major role. Demand is also increased by the increased focus on renewable energy initiatives, especially in the US and Canada. The market is also driven by strong commercial industries like data centers and telecommunications. North America's dominance in the industry is further strengthened by the extensive usage of subterranean cables for urbanization projects and the deployment of submarine cables for offshore energy facilities.

Breakdown of Primaries:

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information, as well as to assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1- 45%, Tier 2- 30%, and Tier 3- 25%

By Designation: C-Level- 35%, Director Levels- 25%, and Others- 40%

By Region: North America- 50%, South America- 30% and Central America- 20%

Note: Others include product engineers, product specialists, and engineering leads.

Note: The tiers of the companies are defined on the basis of their total revenues as of 2021. Tier 1: > USD 1 billion, Tier 2: From USD 500 million to USD 1 billion, and Tier 3: < USD 500 million

The Americas Cables market is dominated by a few major players that have a wide regional presence. The leading players in the Americas Cables market are Prysmian Group (Italy), Southwire Company, LLC (US), Nexans (France), LS Cable & System Ltd (South Korea) and NKT a/s (Denmark).

Research Coverage:

The report defines, describes, and forecasts the Americas Cables market, polymer and insulation type, semiconducting layer, voltage, application, end user, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report provides a comprehensive review of the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates, in terms of value, and future trends in the Americas Cables market.

Key Benefits of Buying the Report

- Increase in renewable energy generation in major countries is fueling the demand for cables, especially in the US. Rapid pace of industrialization and urbanization across America.

- Product Development/ Innovation: The trends such as self-healing cables and smart grid solutions.

- Market Development: The global scenario of Americas Cables has developed due to a global shift towards sustainable energy solutions, increased adoption of renewable sources like solar and wind power, technological advancements enhancing efficiency, and the growing investments done by government and companies. These factors collectively propel innovation, creating a dynamic landscape for Americas Cables technologies to meet evolving energy demands.

- Market Diversification: Market diversification in the Americas Cables market is a response to varied energy needs across industries and regions. As renewable energy adoption expands, diverse applications emerge, from residential solar installations to utility-scale projects. Americas Cables manufacturers diversify their product offerings to cater to the specific requirements of different sectors, fostering market growth and resilience.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Prysmian Group (Italy), Southwire Company, LLC (US), Nexans (France), LS Cable & System Ltd. (South Korea) and NKT A/S (Denmark) among others in the Americas Cables market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS.

- 1.3.1 AMERICAS CABLES MARKET, BY POLYMER AND INSULATION TYPE

- 1.3.2 AMERICAS CABLES MARKET, BY SEMI-CONDUCTING LAYER

- 1.3.3 AMERICAS CABLES MARKET, BY VOLTAGE RATING

- 1.3.4 AMERICAS CABLES MARKET, BY END USER

- 1.3.5 AMERICAS CABLES MARKET, BY APPLICATION

- 1.4 MARKET SCOPE

- 1.4.1 MARKET SEGMENTATION

- 1.4.2 REGIONAL SCOPE

- 1.4.3 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.7 LIMITATIONS

- 1.8 STAKEHOLDERS

- 1.9 SUMMARY OF CHANGES

- 1.10 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 AMERICAS CABLES MARKET: RESEARCH DESIGN

- 2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 2 DATA TRIANGULATION

- 2.2.1 SECONDARY DATA

- 2.2.1.1 Key data from secondary sources

- 2.2.1.2 List of major secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 List of key participants in primary interviews

- 2.2.2.2 Breakdown of primaries

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 4 MAIN METRICS CONSIDERED TO ANALYZE AND ASSESS DEMAND FOR CABLES IN AMERICAS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.3.3 DEMAND-SIDE ANALYSIS

- 2.3.3.1 Regional analysis

- 2.3.3.2 Country-level analysis

- 2.3.3.3 Assumptions for demand-side analysis

- 2.3.3.4 Calculations for demand-side analysis

- 2.3.4 SUPPLY-SIDE ANALYSIS

- FIGURE 7 KEY STEPS CONSIDERED TO ASSESS SUPPLY OF CABLES IN AMERICAS

- FIGURE 8 AMERICAS CABLES MARKET: SUPPLY-SIDE ANALYSIS

- 2.3.4.1 Assumptions for supply-side analysis

- 2.3.4.2 Calculations for supply-side analysis

- FIGURE 9 COMPANY REVENUE ANALYSIS, 2023

- 2.3.5 GROWTH FORECAST

- 2.4 RISK ASSESSMENT

- 2.5 IMPACT OF RECESSION ON AMERICAS CABLES MARKET

3 EXECUTIVE SUMMARY

- TABLE 1 AMERICAS CABLES MARKET SNAPSHOT

- FIGURE 10 NORTH AMERICA DOMINATED AMERICAS CABLES MARKET IN 2023

- FIGURE 11 SEMI-CONDUCTING POLYMER CABLES TO ACCOUNT FOR LARGER MARKET SHARE THROUGHOUT FORECAST PERIOD

- FIGURE 12 OUTER SEMI-CONDUCTING LAYER TO HOLD LARGER SHARE OF AMERICAS CABLES MARKET THROUGHOUT FORECAST PERIOD

- FIGURE 13 35-46 KV CABLES TO CAPTURE LARGEST SHARE OF AMERICAS MARKET FROM 2024 TO 2029

- FIGURE 14 UNDERGROUND CABLES TO LEAD AMERICAS MARKET BETWEEN 2024 AND 2029

- FIGURE 15 INDUSTRIAL SECTOR TO HOLD LARGEST SHARE OF AMERICAS CABLES MARKET THROUGHOUT FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AMERICAS CABLES MARKET

- FIGURE 16 INVESTMENTS IN RENEWABLE ENERGY PROJECTS TO CREATE OPPORTUNITIES FOR PLAYERS IN AMERICAS CABLES MARKET

- 4.2 AMERICAS CABLES MARKET, BY REGION

- FIGURE 17 NORTH AMERICA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- 4.3 NORTH AMERICAN CABLES MARKET, BY END USER AND COUNTRY

- FIGURE 18 INDUSTRIAL SECTOR AND US HELD LARGEST SHARES OF NORTH AMERICAN MARKET IN 2024

- 4.4 AMERICAS CABLES MARKET, BY POLYMER AND INSULATION TYPE

- FIGURE 19 SEMI-CONDUCTING POLYMER CABLES TO DOMINATE MARKET IN AMERICAS IN 2029

- 4.5 AMERICAS CABLES MARKET, BY SEMI-CONDUCTING LAYER

- FIGURE 20 OUTER SEMI-CONDUCTING LAYER TO ACCOUNT FOR LARGER SHARE OF AMERICAS CABLES MARKET IN 2029

- 4.6 AMERICAS CABLES MARKET, BY END USER

- FIGURE 21 INDUSTRIAL SECTOR TO ACCOUNT FOR LARGEST SHARE OF AMERICAS CABLES MARKET IN 2029

- 4.7 AMERICAS CABLES MARKET, BY VOLTAGE RATING

- FIGURE 22 35-46 SEGMENT TO ACCOUNT FOR LARGEST SHARE OF AMERICAS CABLES MARKET IN 2029

- 4.8 AMERICAS CABLES MARKET, BY APPLICATION

- FIGURE 23 UNDERGROUND SEGMENT TO ACCOUNT FOR LARGER SHARE OF AMERICAS CABLES MARKET IN 2029

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 24 AMERICAS CABLES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Integration of renewable energy sources into industrial facilities to reduce carbon footprint

- FIGURE 25 PERCENTAGE OF RENEWABLE ENERGY IN TOTAL ELECTRICITY PRODUCTION IN US, BY SOURCE TYPE, 2022

- FIGURE 26 US ANNUAL ELECTRICITY GENERATING CAPACITY USING RENEWABLES (GW), 2018-2024

- 5.2.1.2 Rapid industrialization and urbanization across Americas

- FIGURE 27 URBAN POPULATION GROWTH IN US, 2012 VS. 2022

- 5.2.1.3 Supportive government policies and investments in underground cables, grid technologies, and infrastructure projects

- 5.2.1.4 Pressing need to modernize electrical grids to enhance resilience and reliability

- 5.2.2 RESTRAINTS

- 5.2.2.1 Volatility in raw material prices

- 5.2.2.2 Delay in project authorization process due to complex regulatory and environmental policies

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Strong focus on increasing power generation capacity

- FIGURE 28 ANNUAL ELECTRICITY GENERATION WORLDWIDE, BY SOURCE (GW), 2019-2025

- 5.2.3.2 Adoption of smart grid technologies and development of innovative cable solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 Requirement for technical know-how to develop and install advanced cable products

- 5.2.4.2 Availability of low-cost cable solutions

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 29 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 ECOSYSTEM ANALYSIS

- TABLE 2 ROLE OF PARTICIPANTS IN ECOSYSTEM

- FIGURE 30 KEY PLAYERS IN ECOSYSTEM

- 5.5 INVESTMENTS AND FUNDING LANDSCAPE IN AMERICAS CABLES MARKET

- FIGURE 31 FUNDING RAISED BY PLAYERS IN AMERICAS CABLES MARKET, 2021-2022

- TABLE 3 PRYSMIAN GROUP: FUNDING DETAILS

- TABLE 4 LEONI: FUNDING DETAILS

- TABLE 5 DOW: FUNDING DETAILS

- 5.6 VALUE CHAIN ANALYSIS

- FIGURE 32 AMERICAS CABLES MARKET: VALUE CHAIN ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 CORE TECHNOLOGY

- 5.7.1.1 High-temperature superconducting (HTS) cables

- 5.7.1.2 Self-healing cables

- 5.7.2 COMPLIMENTARY TECHNOLOGY

- 5.7.2.1 Smart grid solutions

- 5.7.2.2 Advanced insulation materials

- 5.7.3 ADJACENT TECHNOLOGY

- 5.7.3.1 Monitoring and control systems

- 5.7.1 CORE TECHNOLOGY

- 5.8 PATENT ANALYSIS

- FIGURE 33 AMERICAS CABLES MARKET: INNOVATIONS AND PATENT REGISTRATIONS, 2013-2023

- TABLE 6 AMERICAS CABLES MARKET: INNOVATIONS AND PATENT REGISTRATIONS, JANUARY 2019-DECEMBER 2023

- 5.9 TRADE ANALYSIS

- 5.9.1 TRADE ANALYSIS FOR PRODUCTS COMPLY WITH HS CODE 8544

- 5.9.2 EXPORT DATA

- TABLE 7 EXPORT VALUES FOR HS CODE 8544-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2022 (USD THOUSAND)

- FIGURE 34 EXPORT DATA FOR HS CODE 8544-COMPLIANT PRODUCTS FOR TOP 5 COUNTRIES, 2020-2022 (USD THOUSAND)

- 5.9.3 IMPORT DATA

- TABLE 8 IMPORT VALUES FOR HS CODE 8544-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2022 (USD THOUSAND)

- FIGURE 35 IMPORT DATA FOR HS CODE 8544-COMPLIANT PRODUCTS FOR TOP 5 COUNTRIES, 2020-2022 (USD THOUSAND)

- 5.10 PRICING ANALYSIS

- FIGURE 36 AVERAGE SELLING PRICE OF CABLES, BY POLYMER AND INSULATION TYPE, 2022-2024 (USD/TONNES)

- TABLE 9 AVERAGE SELLING PRICE OF CABLES, BY POLYMER AND INSULATION TYPE, 2022-2024 (USD/TONNES)

- FIGURE 37 AVERAGE SELLING PRICE OF CABLES, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2024 (USD/TONNES)

- TABLE 10 AVERAGE SELLING PRICE OF CABLES, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2024 (USD/TONNES)

- FIGURE 38 AVERAGE SELLING PRICE OF CABLES, BY REGION, 2022-2024 (USD/TONNES)

- TABLE 11 AVERAGE SELLING PRICE OF CABLES, BY REGION, 2022-2024 (USD/TONNES)

- 5.11 REGULATORY LANDSCAPE

- 5.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.2 CODES AND REGULATIONS RELATED TO AMERICAS CABLES

- TABLE 14 AMERICAS CABLES MARKET: CODES AND REGULATIONS

- 5.12 TARIFF ANALYSIS

- 5.12.1 COUNTRY-WISE IMPORT TARIFFS FOR HS CODE 8544-COMPLIANT PRODUCTS

- TABLE 15 IMPORT TARIFFS FOR HS 8544-COMPLIANT PRODUCTS, 2023

- 5.13 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 39 AMERICAS CABLES MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 16 AMERICAS CABLES MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.13.1 THREAT OF NEW ENTRANTS

- 5.13.2 BARGAINING POWER OF SUPPLIERS

- 5.13.3 BARGAINING POWER OF BUYERS

- 5.13.4 THREAT OF SUBSTITUTES

- 5.13.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.14 CASE STUDY ANALYSIS

- 5.14.1 BRUGG CABLES PROVIDED CABLES AND ACCESSORIES FOR POWER SUPPLY PROJECTS DURING BEIJING OLYMPIC GAMES IN CHINA

- 5.14.2 US DEPARTMENT OF ENERGY INVESTED IN GRID MODERNIZATION TECHNOLOGIES TO SAFEGUARD ENERGY INFRASTRUCTURE

- 5.14.3 NORTH SEA LINK CONNECTED ELECTRICITY GRIDS OF NORWAY AND UNITED KINGDOM VIA SUBSEA POWER CABLE

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 40 INFLUENCE OF KEY STAKEHOLDERS ON BUYING PROCESS FOR END USERS

- TABLE 17 INFLUENCE OF KEY STAKEHOLDERS ON BUYING PROCESS FOR END USERS

- 5.15.2 BUYING CRITERIA

- FIGURE 41 KEY BUYING CRITERIA FOR END USERS

- TABLE 18 KEY BUYING CRITERIA FOR TOP END USERS

- 5.16 KEY CONFERENCES AND EVENTS, 2024

- TABLE 19 AMERICAS CABLES MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2024

6 AMERICAS CABLES MARKET, BY POLYMER AND INSULATION TYPE

- 6.1 INTRODUCTION

- FIGURE 42 AMERICAS CABLES MARKET, BY POLYMER AND INSULATION TYPE, 2023

- TABLE 20 AMERICAS CABLES MARKET, BY POLYMER AND INSULATION TYPE, 2022-2029 (USD MILLION)

- TABLE 21 POLYMER AND INSULATION TYPE: AMERICAS CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (USD MILLION)

- TABLE 22 AMERICAS CABLES MARKET, BY POLYMER AND INSULATION TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 23 POLYMER AND INSULATION TYPE: AMERICAS CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (THOUSAND TONNES)

- 6.2 SEMI-CONDUCTING POLYMER CABLES

- 6.2.1 PRESSING NEED FOR RELIABLE AND STABLE OPERATION OF SMART GRID INFRASTRUCTURE TO FOSTER MARKET GROWTH

- TABLE 24 SEMI-CONDUCTING POLYMER CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- TABLE 25 SEMI-CONDUCTING POLYMER CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (THOUSAND TONNES)

- 6.3 XLPE CABLES

- 6.3.1 EXCEPTIONAL ELECTRICAL PERFORMANCE AND HIGH THERMAL STABILITY FEATURES TO BOOST SEGMENTAL GROWTH

- TABLE 26 XLPE CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- TABLE 27 XLPE CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (THOUSAND TONNES)

- 6.4 EPR/EPDM CABLES

- 6.4.1 HIGH THERMAL ELECTRICITY AND ABILITY TO WITHSTAND CHEMICAL ATTACKS WITHOUT DEGRADATION TO DRIVE MARKET

- TABLE 28 EPR/EPDM CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- TABLE 29 EPR/EPDM CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (THOUSAND TONNES)

- 6.5 HEPR CABLES

- 6.5.1 OIL & GAS AND PETROCHEMICALS INDUSTRIES TO CONTRIBUTE TO SEGMENTAL GROWTH

- TABLE 30 HEPR CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- TABLE 31 HEPR CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (THOUSAND TONNES)

- 6.6 LOW-VOLTAGE CABLES

- 6.6.1 GROWING ADOPTION OF AUTOMATION SOLUTIONS IN INDUSTRIAL FACILITIES TO BOOST DEMAND

- TABLE 32 LOW-VOLTAGE CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- TABLE 33 LOW-VOLTAGE CABLES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (THOUSAND TONNES)

7 AMERICAS CABLES MARKET, BY SEMI-CONDUCTING LAYER

- 7.1 INTRODUCTION

- FIGURE 43 AMERICAS CABLES MARKET, BY SEMI-CONDUCTING LAYER, 2023

- TABLE 34 AMERICAS CABLES MARKET, BY SEMI-CONDUCTING LAYER, 2022-2029 (USD MILLION)

- 7.2 INNER

- 7.2.1 RAPID INDUSTRIALIZATION AND URBANIZATION TO CREATE GROWTH OPPORTUNITIES

- TABLE 35 INNER: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 7.3 OUTER

- 7.3.1 SIGNIFICANT INVESTMENT IN EXPANSION AND MODERNIZATION OF TRANSMISSION INFRASTRUCTURE TO DRIVE MARKET

- TABLE 36 OUTER: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

8 AMERICAS CABLES MARKET, BY VOLTAGE RATING

- 8.1 INTRODUCTION

- FIGURE 44 AMERICAS CABLES MARKET, BY VOLTAGE RATING, 2023

- TABLE 37 AMERICAS CABLES MARKET, BY VOLTAGE RATING, 2022-2029 (USD MILLION)

- 8.2 UP TO 5 KV

- 8.2.1 RISING USE IN INDUSTRIAL AND COMMERCIAL POWER DISTRIBUTION INFRASTRUCTURE TO DRIVE MARKET

- TABLE 38 UP TO 5 KV: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 8.3 5-8 KV

- 8.3.1 INCREASING INVESTMENT IN RENEWABLE ENERGY PROJECTS AND MODERNIZATION OF ELECTRICAL INFRASTRUCTURE TO SUPPORT MARKET GROWTH

- TABLE 39 5-8 KV: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 8.4 8-15 KV

- 8.4.1 GROWING INCLINATION TOWARD CLEAN ENERGY TO CONTRIBUTE TO MARKET GROWTH

- TABLE 40 8-15 KV: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 8.5 15-35 KV

- 8.5.1 PRESSING NEED FOR RELIABLE AND EFFICIENT POWER TRANSMISSION TO FUEL SEGMENTAL GROWTH

- TABLE 41 15-35 KV: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 8.6 35-46 KV

- 8.6.1 STRONG FOCUS OF CABLE MANUFACTURERS ON MEETING STRINGENT PERFORMANCE AND DURABILITY REQUIREMENTS TO BOOST DEMAND

- TABLE 42 35-46 KV: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 8.7 69 KV

- 8.7.1 INDUSTRIAL DIGITALIZATION TO FOSTER DEMAND FOR MEDIUM-VOLTAGE CABLES

- TABLE 43 69 KV: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 8.8 115 KV

- 8.8.1 GROWING DEMAND FOR CLEANER ENERGY AND IMPERATIVE TO MODERNIZE AGING INFRASTRUCTURE TO DRIVE MARKET

- TABLE 44 115 KV: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 8.9 138 KV

- 8.9.1 SURGING NEED FOR ROBUST AND RELIABLE POWER TRANSMISSION SYSTEM TO ACCELERATE ADOPTION OF HIGH-VOLTAGE CABLES

- TABLE 45 138 KV: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

9 AMERICAS CABLES MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- FIGURE 45 AMERICAS CABLES MARKET, BY APPLICATION, 2023

- TABLE 46 AMERICAS CABLES MARKET, BY APPLICATION, 2022-2029 (USD MILLION)

- 9.2 UNDERGROUND

- 9.2.1 LOW TRANSMISSION LOSSES AND MAINTENANCE COST TO BOOST DEMAND

- TABLE 47 UNDERGROUND: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 9.3 SUBMARINE

- 9.3.1 BOOMING OFFSHORE WIND INDUSTRY IN US TO FUEL SEGMENTAL GROWTH

- TABLE 48 SUBMARINE: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

10 AMERICAS CABLES MARKET, BY END USER

- 10.1 INTRODUCTION

- FIGURE 46 AMERICAS CABLES MARKET, BY END USER, 2023

- TABLE 49 AMERICAS CABLES MARKET, BY END USER, 2022-2029 (USD MILLION)

- 10.2 INDUSTRIAL SECTOR

- FIGURE 47 UTILITIES SEGMENT HELD LARGEST SHARE OF AMERICAS CABLES MARKET FOR INDUSTRIAL SECTOR IN 2023

- TABLE 50 AMERICAS CABLES MARKET, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 51 INDUSTRIAL SECTOR: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.2.1 UTILITIES

- 10.2.1.1 Increasing investment in grid modernization to drive market

- TABLE 52 UTILITIES: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.2.2 OIL & GAS

- 10.2.2.1 Rising focus on refinery capacity expansion to fuel market growth

- TABLE 53 OILS & GAS: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.2.3 CHEMICALS & PETROCHEMICALS

- 10.2.3.1 Exposure to corrosive chemicals, high temperatures, moisture, abrasion, and mechanical stress to boost requirement for specialized cables

- TABLE 54 CHEMICALS & PETROCHEMICALS: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.2.4 METALS & MINING

- 10.2.4.1 Research and innovations related to development of high-strength and high-conductivity alloys to foster market growth

- TABLE 55 METALS & MINING: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.2.5 MANUFACTURING

- 10.2.5.1 Growing focus on building smart factories to accelerate need for XLPE and PVC cables

- TABLE 56 MANUFACTURING: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.2.6 CEMENT

- 10.2.6.1 Rapid urbanization and industrialization to accelerate market growth

- TABLE 57 CEMENT: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.2.7 OTHER INDUSTRIAL END USERS

- TABLE 58 OTHER INDUSTRIAL END USERS: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.3 RENEWABLE ENERGY SECTOR

- FIGURE 48 AMERICAS CABLES MARKET, BY RENEWABLE ENERGY SECTOR END USER, 2023

- TABLE 59 AMERICAS CABLES MARKET, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 60 RENEWABLE ENERGY SECTOR: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.3.1 SOLAR PLANTS

- 10.3.1.1 Transition toward robust and sustainable energy future to drive market

- TABLE 61 SOLAR PLANTS: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.3.2 WIND FARMS

- 10.3.2.1 Ongoing large-scale offshore wind projects to boost demand

- TABLE 62 WIND FARMS: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- 10.4 COMMERCIAL SECTOR

- 10.4.1 ELECTRIFICATION AND INFRASTRUCTURE MODIFICATION IN RAILWAY INDUSTRY TO PROPEL MARKET

- TABLE 63 COMMERCIAL SECTOR: AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

11 AMERICAS CABLES MARKET, BY REGION

- 11.1 INTRODUCTION

- FIGURE 49 AMERICAS CABLES MARKET, BY REGION, 2023 (%)

- FIGURE 50 NORTH AMERICA TO BE FASTEST-GROWING REGION IN AMERICAS CABLES MARKET DURING FORECAST PERIOD

- TABLE 64 AMERICAS CABLES MARKET, BY REGION, 2022-2029 (USD MILLION)

- TABLE 65 AMERICAS CABLES MARKET, BY POLYMER AND INSULATION TYPE, 2022-2029 (USD MILLION)

- TABLE 66 AMERICAS CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (USD MILLION)

- TABLE 67 AMERICAS CABLES MARKET, BY SEMI-CONDUCTING LAYER, 2022-2029 (USD MILLION)

- TABLE 68 AMERICAS CABLES MARKET, BY CABLE TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 69 AMERICAS CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 70 AMERICAS CABLES MARKET, BY APPLICATION, 2022-2029 (USD MILLION)

- TABLE 71 AMERICAS CABLES MARKET, BY VOLTAGE RATING, 2022-2029 (USD MILLION)

- TABLE 72 AMERICAS CABLES MARKET, BY END USER, 2022-2029 (USD MILLION)

- TABLE 73 AMERICAS CABLES MARKET, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 74 AMERICAS CABLES MARKET, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.2 NORTH AMERICA

- FIGURE 51 NORTH AMERICA: MARKET SNAPSHOT

- 11.3 RECESSION IMPACT: NORTH AMERICA

- TABLE 75 NORTH AMERICAN CABLES MARKET, BY POLYMER AND INSULATION TYPE, 2022-2029 (USD MILLION)

- TABLE 76 POLYMER AND INSULATION TYPE: NORTH AMERICAN CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (USD MILLION)

- TABLE 77 NORTH AMERICAN CABLES MARKET, BY POLYMER AND INSULATION TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 78 POLYMER AND INSULATION TYPE: NORTH AMERICAN CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 79 NORTH AMERICAN CABLES MARKET, BY SEMI-CONDUCTING LAYER, 2022-2029 (USD MILLION)

- TABLE 80 NORTH AMERICAN CABLES MARKET, BY APPLICATION, 2022-2029 (USD MILLION)

- TABLE 81 NORTH AMERICAN CABLES MARKET, BY VOLTAGE RATING, 2022-2029 (USD MILLION)

- TABLE 82 NORTH AMERICAN CABLES MARKET, BY END USER 2022-2029 (USD MILLION)

- TABLE 83 NORTH AMERICAN CABLES MARKET, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 84 NORTH AMERICAN CABLES MARKET, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 85 NORTH AMERICAN CABLES MARKET, BY COUNTRY, 2022-2029 (USD MILLION)

- 11.4 US

- 11.4.1 EXPANSION OF OFFSHORE WIND FARMS TO DRIVE MARKET

- TABLE 86 NORTH AMERICAN CABLES MARKET IN US, BY END USER, 2022-2029 (USD MILLION)

- TABLE 87 NORTH AMERICAN CABLES MARKET IN US, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 88 NORTH AMERICAN CABLES MARKET IN US, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.5 CANADA

- 11.5.1 GROWING EMPHASIS ON GRID MODERNIZATION AND RENEWABLE ENERGY INTEGRATION TO FOSTER MARKET GROWTH

- TABLE 89 NORTH AMERICAN CABLES MARKET IN CANADA, BY END USER, 2022-2029 (USD MILLION)

- TABLE 90 NORTH AMERICAN CABLES MARKET IN CANADA, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 91 NORTH AMERICAN CABLES MARKET IN CANADA, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.6 MEXICO

- 11.6.1 EXPANSION OF DATA CENTER FACILITIES TO FUEL MARKET GROWTH

- TABLE 92 NORTH AMERICAN CABLES MARKET IN MEXICO, BY END USER, 2022-2029 (USD MILLION)

- TABLE 93 NORTH AMERICAN CABLES MARKET IN MEXICO, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 94 NORTH AMERICAN CABLES MARKET IN MEXICO, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.7 CENTRAL AMERICA

- 11.8 RECESSION IMPACT: CENTRAL AMERICA

- TABLE 95 CENTRAL AMERICAN CABLES MARKET, BY SEMI-CONDUCTING LAYER, 2022-2029 (USD MILLION)

- TABLE 96 CENTRAL AMERICAN CABLES MARKET, BY APPLICATION, 2022-2029 (USD MILLION)

- TABLE 97 CENTRAL AMERICAN CABLES MARKET, BY VOLTAGE RATING, 2022-2029 (USD MILLION)

- TABLE 98 CENTRAL AMERICAN CABLES MARKET, BY END USER, 2022-2029 (USD MILLION)

- TABLE 99 CENTRAL AMERICAN CABLES MARKET, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 100 CENTRAL AMERICAN CABLES MARKET, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 101 CENTRAL AMERICAN CABLES MARKET, BY POLYMER AND INSULATING TYPE, 2022-2029 (USD MILLION)

- TABLE 102 CENTRAL AMERICAN CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (USD MILLION)

- TABLE 103 CENTRAL AMERICAN CABLES MARKET, BY POLYMER AND INSULATING TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 104 CENTRAL AMERICAN CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 105 CENTRAL AMERICAN CABLES MARKET, BY COUNTRY, 2022-2029 (USD MILLION)

- 11.9 GUATEMALA

- 11.9.1 INVESTMENTS IN RENEWABLE ENERGY PROJECTS TO FUEL MARKET GROWTH

- TABLE 106 CENTRAL AMERICAN CABLES MARKET IN GUATEMALA, BY END USER, 2022-2029 (USD MILLION)

- TABLE 107 CENTRAL AMERICAN CABLES MARKET IN GUATEMALA, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 108 CENTRAL AMERICAN CABLES MARKET IN GUATEMALA, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.10 PANAMA

- 11.10.1 STRONG FOCUS ON ENHANCING POWER INFRASTRUCTURE TO BOOST DEMAND

- TABLE 109 CENTRAL AMERICAN CABLES MARKET IN PANAMA, BY END USER, 2022-2029 (USD MILLION)

- TABLE 110 CENTRAL AMERICAN CABLES MARKET IN PANAMA, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 111 CENTRAL AMERICAN CABLES MARKET IN PANAMA, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.11 COSTA RICA

- 11.11.1 AMBITIOUS RENEWABLE ENERGY TARGETS AND COMMITMENT TO REDUCE CARBON EMISSIONS TO SUPPORT MARKET GROWTH

- TABLE 112 CENTRAL AMERICAN CABLES MARKET IN COSTA RICA, BY END USER, 2022-2029 (USD MILLION)

- TABLE 113 CENTRAL AMERICAN CABLES MARKET IN COSTA RICA, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 114 CENTRAL AMERICAN CABLES MARKET IN COSTA RICA, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.12 SOUTH AMERICA

- 11.13 RECESSION IMPACT: SOUTH AMERICA

- TABLE 115 SOUTH AMERICAN CABLES MARKET, BY POLYMER AND INSULATION TYPE, 2022-2029 (USD MILLION)

- TABLE 116 SOUTH AMERICAN CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (USD MILLION)

- TABLE 117 SOUTH AMERICAN CABLES MARKET, BY POLYMER AND INSULATION TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 118 SOUTH AMERICAN CABLES MARKET, BY SEMI-CONDUCTING POLYMER CABLE TYPE, 2022-2029 (THOUSAND TONNES)

- TABLE 119 SOUTH AMERICAN CABLES MARKET, BY SEMI-CONDUCTING LAYER, 2022-2029 (USD MILLION)

- TABLE 120 SOUTH AMERICAN CABLES MARKET, BY APPLICATION, 2022-2029 (USD MILLION)

- TABLE 121 SOUTH AMERICAN CABLES MARKET, BY VOLTAGE RATING, 2022-2029 (USD MILLION)

- TABLE 122 SOUTH AMERICAN CABLES MARKET, BY END USER, 2022-2029 (USD MILLION)

- TABLE 123 SOUTH AMERICAN CABLES MARKET, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 124 SOUTH AMERICAN CABLES MARKET, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 125 SOUTH AMERICAN CABLES MARKET, BY COUNTRY, 2022-2029 (USD MILLION)

- 11.14 BRAZIL

- 11.14.1 RENEWABLE ENERGY INTEGRATION AND OFFSHORE WIND PROJECTS TO FUEL MARKET GROWTH

- TABLE 126 SOUTH AMERICAN CABLES MARKET IN BRAZIL, BY END USER, 2022-2029 (USD MILLION)

- TABLE 127 SOUTH AMERICAN CABLES MARKET IN BRAZIL, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 128 SOUTH AMERICAN CABLES MARKET IN BRAZIL, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.15 ARGENTINA

- 11.15.1 POTENTIAL FOR OFFSHORE WIND ENERGY DEVELOPMENT TO STIMULATE MARKET GROWTH

- TABLE 129 SOUTH AMERICAN CABLES MARKET IN ARGENTINA, BY END USER, 2022-2029 (USD MILLION)

- TABLE 130 SOUTH AMERICAN CABLES MARKET IN ARGENTINA, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 131 SOUTH AMERICAN CABLES MARKET IN ARGENTINA, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.16 VENEZUELA

- 11.16.1 INITIATION OF OIL AND GAS PROJECTS TO SUPPORT MARKET GROWTH

- TABLE 132 SOUTH AMERICAN CABLES MARKET IN VENEZUELA, BY END USER, 2022-2029 (USD MILLION)

- TABLE 133 SOUTH AMERICAN CABLES MARKET IN VENEZUELA, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 134 SOUTH AMERICAN CABLES MARKET IN VENEZUELA, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

- 11.17 REST OF SOUTH AMERICA

- TABLE 135 SOUTH AMERICAN CABLES MARKET IN REST OF SOUTH AMERICA, BY END USER, 2022-2029 (USD MILLION)

- TABLE 136 SOUTH AMERICAN CABLES MARKET IN REST OF SOUTH AMERICA, BY INDUSTRIAL SECTOR END USER, 2022-2029 (USD MILLION)

- TABLE 137 SOUTH AMERICAN CABLES MARKET IN REST OF SOUTH AMERICA, BY RENEWABLE ENERGY SECTOR END USER, 2022-2029 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 138 OVERVIEW OF KEY STRATEGIES ADOPTED BY TOP PLAYERS, 2018-2023

- 12.2 MARKET SHARE ANALYSIS OF TOP 5 PLAYERS, 2023

- TABLE 139 AMERICAS CABLES MARKET: DEGREE OF COMPETITION, 2023

- FIGURE 52 AMERICAS CABLES MARKET SHARE ANALYSIS, 2023

- 12.3 REVENUE ANALYSIS OF TOP 5 PLAYERS IN AMERICAS CABLES MARKET, 2018 TO 2022

- FIGURE 53 FIVE-YEAR REVENUE ANALYSIS OF TOP 4 PLAYERS IN AMERICAS CABLES MARKET, 2018-2022

- 12.4 COMPANY EVALUATION MATRIX, KEY PLAYERS, 2023

- 12.4.1 STARS

- 12.4.2 PERVASIVE PLAYERS

- 12.4.3 EMERGING LEADERS

- 12.4.4 PARTICIPANTS

- 12.4.5 COMPANY FOOTPRINT: KEY PLAYERS

- 12.4.5.1 Polymer and insulation type footprint

- TABLE 140 COMPANY FOOTPRINT: BY POLYMER AND INSULATION TYPE

- 12.4.5.2 End user footprint

- TABLE 141 COMPANY FOOTPRINT: BY END USER

- 12.4.5.3 Voltage rating footprint

- TABLE 142 COMPANY FOOTPRINT: BY VOLTAGE RATING

- 12.4.5.4 Region footprint

- TABLE 143 COMPANY FOOTPRINT: BY REGION

- 12.4.5.5 Competitive benchmarking of key startups/smes, 2023

- TABLE 144 AMERICAS CABLES MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- FIGURE 54 AMERICAS CABLES MARKET: COMPANY FOOTPRINT

- FIGURE 55 AMERICAS CABLES MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- 12.5 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 12.5.1 PROGRESSIVE COMPANIES

- 12.5.2 RESPONSIVE COMPANIES

- 12.5.3 DYNAMIC COMPANIES

- 12.5.4 STARTING BLOCKS

- FIGURE 56 AMERICAS CABLES MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- 12.5.5 COMPETITIVE BENCHMARKING, STARTUPS/SMES, 2023

- 12.5.5.1 List of startups/SMES

- TABLE 145 AMERICAS CABLES MARKET: KEY STARTUP/SMES

- 12.6 COMPANY VALUATION AND FINANCIAL METRICS FOR MAJOR CABLES VENDORS IN AMERICAS

- FIGURE 57 EV/EBITDA OF KEY VENDORS

- FIGURE 58 COMPANY VALUATION OF KEY VENDORS

- 12.7 BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 59 AMERICAS CABLES MARKET: TOP TRENDING BRANDS/PRODUCTS

- 12.8 COMPETITIVE SCENARIO AND TRENDS

- 12.8.1 DEALS

- TABLE 146 AMERICAS CABLES MARKET: DEALS, JANUARY 2018-DECEMBER 2023

- 12.8.1.1.1 Expansions

- TABLE 147 AMERICAS CABLES: EXPANSIONS, JANUARY 2018-DECEMBER 2023

- 12.8.1.1.2 Others

- TABLE 148 AMERICAS CABLES MARKET: OTHERS, JANUARY 2018-DECEMBER 2023

13 COMPANY PROFILES

(Business overview, Products offered, Recent Developments, MNM view)**

- 13.1 KEY PLAYERS

- 13.1.1 PRYSMIAN GROUP

- TABLE 149 PRYSMIAN GROUP: COMPANY OVERVIEW

- FIGURE 60 PRYSMIAN GROUP: COMPANY SNAPSHOT

- TABLE 150 PRYSMIAN GROUP: PRODUCTS OFFERED

- TABLE 151 PRYSMIAN GROUP: DEALS

- TABLE 152 PRYSMIAN GROUP: OTHERS

- 13.1.2 SOUTHWIRE COMPANY, LLC

- TABLE 153 SOUTHWIRE COMPANY, LLC: COMPANY OVERVIEW

- TABLE 154 SOUTHWIRE COMPANY, LLC: PRODUCTS OFFERED

- TABLE 155 SOUTHWIRE COMPANY, LLC: DEALS

- TABLE 156 SOUTHWIRE COMPANY: EXPANSIONS

- TABLE 157 SOUTHWIRE COMPANY: OTHERS

- 13.1.3 NEXANS

- TABLE 158 NEXANS: COMPANY OVERVIEW

- FIGURE 61 NEXANS: COMPANY SNAPSHOT

- TABLE 159 NEXANS: PRODUCTS OFFERED

- TABLE 160 NEXANS: DEALS

- TABLE 161 NEXANS: EXPANSIONS

- TABLE 162 NEXANS: OTHERS

- 13.1.4 LS CABLE & SYSTEM LTD.

- TABLE 163 LS CABLE & SYSTEM LTD.: COMPANY OVERVIEW

- FIGURE 62 LS CABLE & SYSTEM LTD.: COMPANY SNAPSHOT

- TABLE 164 LS CABLE & SYSTEM LTD.: PRODUCTS OFFERED

- TABLE 165 LS CABLE & SYSTEM LTD.: PRODUCT LAUNCHES

- TABLE 166 LS CABLE & SYSTEM LTD.: DEALS

- TABLE 167 LS CABLE & SYSTEM LTD.: EXPANSIONS

- 13.1.5 NKT A/S

- TABLE 168 NKT A/S: COMPANY OVERVIEW

- FIGURE 63 NKT A/S: COMPANY SNAPSHOT

- TABLE 169 NKT A/S: PRODUCTS OFFERED

- TABLE 170 NKT A/S: DEALS

- TABLE 171 NKT A/S: EXPANSIONS

- TABLE 172 NKT A/S: OTHERS

- 13.1.6 AMPHENOL TPC

- TABLE 173 AMPHENOL TPC: COMPANY OVERVIEW

- TABLE 174 AMPHENOL TPC: PRODUCTS OFFERED

- TABLE 175 AMPHENOL TPC: PRODUCT LAUNCHES

- TABLE 176 AMPHENOL TPC: DEALS

- 13.1.7 BELDEN INC.

- TABLE 177 BELDEN INC.: COMPANY OVERVIEW

- FIGURE 64 BELDEN INC.: COMPANY SNAPSHOT

- TABLE 178 BELDEN INC.: PRODUCTS OFFERED

- TABLE 179 BELDEN INC.: PRODUCT LAUNCHES

- TABLE 180 BELDEN INC.: DEALS

- 13.1.8 LEONI

- TABLE 181 LEONI: COMPANY OVERVIEW

- FIGURE 65 LEONI: COMPANY SNAPSHOT

- TABLE 182 LEONI: PRODUCTS OFFERED

- TABLE 183 LEONI: OTHERS

- 13.1.9 BIZLINK GROUP

- TABLE 184 BIZLINK GROUP: COMPANY OVERVIEW

- FIGURE 66 BIZLINK GROUP: COMPANY SNAPSHOT

- TABLE 185 BIZLINK GROUP: PRODUCTS OFFERED

- TABLE 186 BIZLINK GROUP: DEALS

- 13.1.10 SUMITOMO ELECTRIC INDUSTRIES, LTD.

- TABLE 187 SUMITOMO ELECTRIC INDUSTRIES, LTD.: COMPANY OVERVIEW

- FIGURE 67 SUMITOMO ELECTRIC INDUSTRIES, LTD.: COMPANY SNAPSHOT

- TABLE 188 SUMITOMO ELECTRIC INDUSTRIES, LTD.: PRODUCTS OFFERED

- TABLE 189 SUMITOMO ELECTRIC INDUSTRIES, LTD.: OTHERS

- 13.1.11 THE OKONITE COMPANY

- TABLE 190 THE OKONITE COMPANY: COMPANY OVERVIEW

- TABLE 191 THE OKONITE COMPANY: PRODUCTS OFFERED

- 13.1.12 TFKABLE

- TABLE 192 TFKABLE: COMPANY OVERVIEW

- TABLE 193 TFKABLE: PRODUCTS OFFERED

- 13.1.13 TRATOS

- TABLE 194 TRATOS: COMPANY OVERVIEW

- TABLE 195 TRATOS: PRODUCTS OFFERED

- 13.1.14 ZTT

- TABLE 196 ZTT: COMPANY OVERVIEW

- FIGURE 68 ZTT: COMPANY SNAPSHOT

- TABLE 197 ZTT: PRODUCTS OFFERED

- 13.1.15 HELUKABEL GROUP

- TABLE 198 HELUKABEL GROUP: COMPANY OVERVIEW

- TABLE 199 HELUKABEL GROUP: PRODUCTS OFFERED

- 13.2 OTHER PLAYERS (INSULATION PRODUCT AND SERVICE PROVIDERS)

- 13.2.1 DOW

- TABLE 200 DOW: COMPANY OVERVIEW

- FIGURE 69 DOW: COMPANY SNAPSHOT

- TABLE 201 DOW: PRODUCTS OFFERED

- 13.2.2 FURUKAWA ELECTRIC CO., LTD.

- TABLE 202 FURUKAWA ELECTRIC CO., LTD.: COMPANY OVERVIEW

- FIGURE 70 FURUKAWA ELECTRIC CO., LTD.: COMPANY SNAPSHOT

- TABLE 203 FURUKAWA ELECTRIC CO., LTD.: PRODUCTS OFFERED

- TABLE 204 FURUKAWA ELECTRIC CO., LTD.: OTHERS

- 13.2.3 ZHEJIANG WANMA CO., LTO.

- TABLE 205 ZHEJIANG WANMA CO., LTO.: COMPANY OVERVIEW

- TABLE 206 ZHEJIANG WANMA CO., LTO.: PRODUCTS OFFERED

- 13.2.4 HANWHA GROUP

- TABLE 207 HANWHA GROUP: COMPANY OVERVIEW

- TABLE 208 HANWHA GROUP: PRODUCTS OFFERED

- 13.2.5 TRELLEBORG GROUP

- TABLE 209 TRELLEBORG GROUP: COMPANY OVERVIEW

- FIGURE 71 TRELLEBORG GROUP: COMPANY SNAPSHOT

- TABLE 210 TRELLEBORG GROUP: PRODUCTS OFFERED

- 13.2.6 BOREALIS AG

- TABLE 211 BOREALIS AG: COMPANY OVERVIEW

- FIGURE 72 BOREALIS AG: COMPANY SNAPSHOT

- TABLE 212 BOREALIS AG: PRODUCTS OFFERED

- 13.2.7 AVIENT CORPORATION

- TABLE 213 AVIENT CORPORATION: COMPANY OVERVIEW

- FIGURE 73 AVIENT CORPORATION: COMPANY SNAPSHOT

- TABLE 214 AVIENT CORPORATION: PRODUCTS OFFERED

- 13.2.8 SACO AEI POLYMERS

- 13.2.9 HJ POLYMER CHINA CO., LTD.

- 13.2.10 WTEC ENERGY INNOVATION

- 13.2.11 PRAMKOR

- 13.2.12 ELECTRIC CABLE COMPOUNDS, INC.

- 13.2.13 MIXER S.P.A.

- *Details on Business overview, Products offered, Recent Developments, MNM view might not be captured in case of unlisted companies.

14 APPENDIX

- 14.1 INSIGHTS FROM INDUSTRY EXPERTS

- 14.2 DISCUSSION GUIDE

- 14.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.4 CUSTOMIZATION OPTIONS

- 14.5 RELATED REPORTS

- 14.6 AUTHOR DETAILS