|

|

市場調査レポート

商品コード

1418779

ヘルスケアシミュレーションの世界市場:製品・サービス別(シミュレーション、トレーニングサービス)、技術別、エンドユーザー別、地域別-2028年までの予測Healthcare Simulation Market by Offering (Simulation, Training Services), Technology, End User & Region - Global Forecast to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ヘルスケアシミュレーションの世界市場:製品・サービス別(シミュレーション、トレーニングサービス)、技術別、エンドユーザー別、地域別-2028年までの予測 |

|

出版日: 2024年01月18日

発行: MarketsandMarkets

ページ情報: 英文 359 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2028年 |

| 基準年 | 2022年 |

| 予測期間 | 2023年~2028年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント | 製品・サービス別、技術別、エンドユーザー別 |

| 対象地域 | 北米、欧州、アジア太平洋、ラテンアメリカ、中東アフリカ |

世界のヘルスケアシミュレーションの市場規模は、2023年の23億米ドルから2028年には52億米ドルに達すると予測され、予測期間中のCAGRは16.7%になるとみられています。

市場拡大の原動力となっているのは、患者の安全性を重視する傾向の高まりと、バーチャルな相互作用に対する嗜好の高まりです。とはいえ、熟練したヘルスケア専門家の不足やシミュレータの高コストといった課題は、市場の成長をやや阻害すると予想されます。

製品・サービス別では、予測期間を通じてウェブベースのシミュレーション分野がヘルスケアシミュレーション市場で最も大きな成長を遂げました。同分野の拡大は、インターネットサービスの普及と、ヘルスケア情報技術(HCIT)ソリューションの導入に向けた政府の取り組みが活発化していることに起因しています。

2022年のヘルスケアシミュレーション市場では、学術機関セグメントが最も高い成長率を示すと予測されています。医療手術におけるシミュレーションモデルの使用の増加、エラー削減の重視の高まり、医療医師向けの手技トレーニングの費用対効果などが、今後数年間におけるヘルスケアシミュレーションサービスの需要を促進すると予測されます。

アジア太平洋がヘルスケアシミュレーション市場において最も高い成長率を示している背景には、同地域全体で医療における高度な医療トレーニングと患者の安全性の重要性に対する認識が高まっていること、医療インフラや教育への投資の増加がシミュレーション技術の導入に寄与していること、技術の進歩と相まって熟練した医療従事者に対する需要の高まりが革新的なトレーニング方法の必要性を煽っていること、などの要因があります。これらの要因が組み合わさることで、同地域はヘルスケアシミュレーションソリューションの市場としてダイナミックかつ急速に拡大しています。

当レポートでは、世界のヘルスケアシミュレーション市場について調査し、製品・サービス別業界別、技術別、エンドユーザー別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 市場力学:影響分析

- 業界の動向

- 技術分析

- エコシステム分析

- バリューチェーン分析

- ポーターのファイブフォース分析

- 特許分析

- 関税と規制状況

- 価格分析

- ヘルスケアシミュレーション市場の投資情勢

- 主要な会議とイベント(2023年第4四半期~2024年第3四半期)

- 顧客のビジネスに影響を与える動向/混乱

- 主要な利害関係者と購入基準

- ケーススタディ分析

- アンメットニーズ

第6章 ヘルスケアシミュレーション市場、製品・サービス別

- イントロダクション

- ヘルスケアシミュレーションの解剖学的モデル

- ウェブベースのシミュレーション

- ヘルスケアシミュレーションソフトウェア

- ヘルスケアシミュレーショントレーニングサービス

第7章 ヘルスケアシミュレーション市場、技術別

- イントロダクション

- 仮想患者シミュレーション

- 3Dプリント

- 手技リハーサル技術

第8章 ヘルスケアシミュレーション市場、エンドユーザー別

- イントロダクション

- 学術機関

- 病院

- 軍事組織

- その他

第9章 ヘルスケアシミュレーション市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第10章 競合情勢

- イントロダクション

- 主要参入企業の戦略/秘策

- 市場の主要企業の収益シェア分析、2022年

- 市場シェア分析

- 市場ランキング分析

- ブランド/製品の比較分析

- 企業評価マトリックス

- スタートアップ/中小企業の評価マトリックス

- 競合シナリオ

第11章 企業プロファイル

- 主要参入企業

- CAE INC.

- LAERDAL MEDICAL

- GAUMARD SCIENTIFIC CO.

- KYOTO KAGAKU

- LIMBS & THINGS

- MENTICE AB

- SIMULAB CORPORATION

- SIMULAIDS

- INTELLIGENT ULTRASOUND GROUP PLC

- OPERATIVE EXPERIENCE INC.

- SURGICAL SCIENCE SWEDEN AB

- CARDIONICS INC.(SUBSIDIARY OF 3B SCIENTIFIC)

- VIRTAMED AG

- SYNBONE AG

- INGMAR MEDICAL

- MEDICAL-X

- KAVO DENTAL GMBH

- ALTAY SCIENTIFIC

- TRUCORP LTD.

- SIMENDO B.V.

- その他の企業

- HAAG-STREIT SIMULATION GMBH

- SYMGERY

- HRV SIMULATION

- SYNAPTIVE MEDICAL

- INOVUS MEDICAL

第12章 付録

Report Description

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD) Billion |

| Segments | Product & Service, Technology, End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America and Middle East and Africa |

The global healthcare simulation market is projected to reach USD 5.2 billion by 2028 from USD 2.3 billion in 2023, at a high CAGR of 16.7% during the forecast period. The market's expansion is fueled by an increasing emphasis on patient safety and a preference for virtual interaction. Nevertheless, challenges such as a shortage of skilled healthcare professionals and the high cost of simulators are anticipated to somewhat impede the market's growth.

"The segment of web-based simulation demonstrated the most substantial growth in the healthcare simulation market, by product & service."

In terms of product & service, the web-based simulation segment experienced the most significant growth in the healthcare simulation market throughout the forecast period. The expansion of this segment can be attributed to the widespread availability of internet services and the increasing government initiatives to adopt Healthcare Information Technology (HCIT) solutions.

"The largest segment in the healthcare simulation market by the end user was academic institutes in the year 2022."

The academic institutes segment is anticipated to experience the highest growth rate in the healthcare simulation market in 2022. The rising use of simulation models in medical surgeries, a heightened emphasis on error reduction, and the cost-effectiveness of procedural training for medical physicians are expected to fuel the demand for healthcare simulation services in the upcoming years.

"APAC region is expected to experience the most substantial growth rate throughout the forecast period."

The Asia-Pacific region is experiencing the highest growth rate in the healthcare simulation market due to several factors such as there is a rising awareness of the importance of advanced medical training and patient safety in healthcare across the region, increasing investments in healthcare infrastructure and education contribute to the adoption of simulation technologies and the growing demand for skilled healthcare professionals, coupled with advancements in technology, fuels the need for innovative training methods. The combination of these factors positions the region as a dynamic and rapidly expanding market for healthcare simulation solutions.

The break-down of primary participants is as mentioned below:

- By Company Type - Tier 1: 45%, Tier 2: 30%, and Tier 3: 25%

- By Designation - C-level: 42%, Director-level: 31%, and Others: 27%

- By Region - North America: 32%, Europe: 32%, Asia Pacific: 26%, Middle East & Africa: 5%, Latin America: 5%

Key Players in the Healthcare Simulation Market

The key players functioning in the healthcare simulation market include CAE (Canada), Laerdal Medical (Norway), Simulab Corporation (US), Simulaids (US), Limbs & Things (UK), Kyoto Kagaku (Japan), Mentice AB (Sweden), Gaumard Scientific Co. (US), Operative Experience Inc. (US), Cardionics Inc. (US) (a subsidiary of 3B Scientific), VirtaMed AG (Switzerland), SYNBONE AG (Switzerland), IngMar Medical (US), Medical-X (Netherlands), KaVo Dental GmbH (Germany), Altay Scientific (Italy), Simendo B.V. (Netherlands) VRMagic Holding AG (Germany), Symgery (Canada), HRV Simulation (France), Synaptive Medical (Canada), Inovus Medical (UK), TruCorp Ltd. (Ireland), and Surgical Science Sweden AG (Sweden).

Research Coverage:

The report analyses the healthcare simulation market. It aims to estimate the market size and future growth potential of various market segments based on product & service, end-user, and region. The report also provides a competitive analysis of the key players in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will enrich established firms and new entrants/smaller firms to gauge the market's pulse, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the below-mentioned strategies to strengthen their positions in the market.

This report provides insights on:

- Analysis of key drivers: (Limited access to patients during medical training, Rising technological advancements in medical education), restraints (Increasing focus on patient safety, Growing preference for virtual interaction), opportunities (Growing awareness about simulation training in emerging economies), and challenges (High cost of simulators, Operational challenges) influencing the growth of the healthcare simulation market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the healthcare simulation market.

- Market Development: Comprehensive information on the lucrative emerging markets, products & services, end-users, and regions.

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the healthcare simulation market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players in the healthcare simulation market like CAE (Canada), Laerdal Medical (Norway), Simulab Corporation (US), Simulaids (US), Limbs & Things (UK).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION AND SCOPE

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.2.2 MARKET SCOPE

- FIGURE 1 HEALTHCARE SIMULATION MARKET SEGMENTATION

- 1.2.3 REGIONAL SCOPE

- 1.2.4 YEARS CONSIDERED

- 1.3 CURRENCY CONSIDERED

- 1.4 UNITS CONSIDERED

- TABLE 1 EXCHANGE RATES CONSIDERED FOR CONVERSION TO USD

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

- 1.7 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.2 HEALTHCARE SIMULATION MARKET: RESEARCH DESIGN

- 2.2.1 SECONDARY RESEARCH

- 2.2.1.1 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- FIGURE 2 PRIMARY SOURCES

- 2.2.2.1 Key data from primary sources

- 2.2.2.2 Insights from primary experts

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY, DESIGNATION, AND REGION

- 2.2.1 SECONDARY RESEARCH

- 2.3 MARKET SIZE ESTIMATION: HEALTHCARE SIMULATION MARKET

- FIGURE 4 ESTIMATION OF MARKET SIZE FOR HEALTHCARE SIMULATION ACADEMIC INSTITUTES AND HOSPITALS THROUGH DEMAND-SIDE APPROACH

- FIGURE 5 ESTIMATION OF GLOBAL HEALTHCARE SIMULATION MARKET SIZE THROUGH DEMAND-SIDE APPROACH

- FIGURE 6 SUPPLY-SIDE MARKET SIZE ESTIMATION: REVENUE SHARE ANALYSIS

- FIGURE 7 BOTTOM-UP APPROACH: SEGMENTAL EXTRAPOLATION

- FIGURE 8 CAGR PROJECTIONS FROM ANALYSIS OF DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 9 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 10 DATA TRIANGULATION

- 2.5 MARKET SHARE ESTIMATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS

- 2.7.1 METHODOLOGY-RELATED LIMITATIONS

- 2.7.2 SCOPE-RELATED LIMITATIONS

- 2.8 RISK ASSESSMENT

- TABLE 2 RISK ASSESSMENT: HEALTHCARE SIMULATION MARKET

- 2.9 RECESSION IMPACT ANALYSIS

3 EXECUTIVE SUMMARY

- FIGURE 11 HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2023 VS. 2028 (USD MILLION)

- FIGURE 12 HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2023 VS. 2028 (USD MILLION)

- FIGURE 13 HEALTHCARE SIMULATION MARKET, BY END USER, 2023 VS. 2028 (USD MILLION)

- FIGURE 14 HEALTHCARE SIMULATION MARKET: REGIONAL SNAPSHOT

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HEALTHCARE SIMULATION MARKET

- FIGURE 15 ADVANCEMENTS IN MEDICAL TECHNOLOGIES TO DRIVE NORTH AMERICAN MARKET GROWTH

- 4.2 ASIA PACIFIC: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE AND COUNTRY

- FIGURE 16 HEALTHCARE SIMULATION ANATOMICAL MODELS SEGMENT ACCOUNTED FOR LARGEST SHARE OF ASIA PACIFIC

- 4.3 HEALTHCARE SIMULATION MARKET: REGIONAL GROWTH OPPORTUNITIES

- FIGURE 17 CHINA TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- 4.4 REGIONAL MIX: HEALTHCARE SIMULATION MARKET

- FIGURE 18 NORTH AMERICA TO LEAD HEALTHCARE SIMULATION MARKET DURING FORECAST PERIOD

- 4.5 HEALTHCARE SIMULATION MARKET: EMERGING VS. DEVELOPED ECONOMIES

- FIGURE 19 EMERGING COUNTRIES TO REGISTER HIGHER GROWTH RATE DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 20 HEALTHCARE SIMULATION MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.3 MARKET DYNAMICS: IMPACT ANALYSIS

- 5.3.1 DRIVERS

- 5.3.1.1 Limited access to patients during medical training

- 5.3.1.2 Rising technological advancements in medical education

- 5.3.1.3 Growing demand for minimally invasive treatments

- FIGURE 21 TOP MINIMALLY INVASIVE COSMETIC PROCEDURES PERFORMED IN 2022

- 5.3.1.4 Increasing focus on patient safety

- 5.3.1.5 Growing preference for virtual interaction

- 5.3.2 RESTRAINTS

- 5.3.2.1 Limited availability of funds

- 5.3.2.2 Poorly designed medical simulators

- 5.3.3 OPPORTUNITIES

- 5.3.3.1 Shortage of healthcare personnel

- 5.3.3.2 Growing awareness about simulation training in emerging economies

- 5.3.4 CHALLENGES

- 5.3.4.1 High cost of simulators

- 5.3.4.2 Operational challenges

- 5.3.1 DRIVERS

- 5.4 INDUSTRY TRENDS

- 5.4.1 USE OF VIRTUAL REALITY AND AUGMENTED REALITY IN HEALTHCARE SIMULATION

- 5.4.2 HIGH-FIDELITY TECHNOLOGICAL ADVANCEMENTS

- 5.4.3 MULTIMODAL APPROACH IN DEVELOPMENT OF SIMULATORS

- 5.4.4 UTILIZATION OF ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING SOFTWARE IN SURGICAL PROCEDURES

- 5.4.5 GROWING USE OF HCIT/EMR

- 5.5 TECHNOLOGY ANALYSIS

- 5.5.1 INTEGRATION OF ARTIFICIAL INTELLIGENCE AND VIRTUAL REALITY

- 5.6 ECOSYSTEM ANALYSIS

- FIGURE 22 HEALTHCARE SIMULATION MARKET: ECOSYSTEM

- 5.7 VALUE CHAIN ANALYSIS

- FIGURE 23 HEALTHCARE SIMULATION MARKET: VALUE CHAIN ANALYSIS

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- TABLE 3 HEALTHCARE SIMULATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 THREAT OF NEW ENTRANTS

- 5.8.2 THREAT OF SUBSTITUTES

- 5.8.3 BARGAINING POWER OF SUPPLIERS

- 5.8.4 BARGAINING POWER OF BUYERS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 PATENT ANALYSIS

- 5.9.1 PATENT PUBLICATION TRENDS FOR HEALTHCARE SIMULATION MARKET

- FIGURE 24 PATENT PUBLICATION TRENDS (2013-2023)

- 5.9.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- FIGURE 25 TOP APPLICANTS & OWNERS (COMPANIES/INSTITUTIONS) OF HEALTHCARE SIMULATION PATENTS (JANUARY 2013-DECEMBER 2023)

- FIGURE 26 TOP APPLICANT COUNTRIES/REGIONS FOR HEALTHCARE SIMULATION PATENTS (JANUARY 2013-DECEMBER 2023)

- 5.9.3 LIST OF MAJOR PATENTS

- TABLE 4 KEY PATENTS IN HEALTHCARE SIMULATION MARKET

- 5.10 TARIFF AND REGULATORY LANDSCAPE

- 5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 5 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 6 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 HEALTHCARE SIMULATION MARKET: REGULATORY STANDARDS

- 5.10.2 HEALTHCARE SIMULATION PRODUCTS

- 5.10.2.1 North America

- 5.10.2.1.1 US

- 5.10.2.1 North America

- TABLE 9 CLASSIFICATION OF MEDICAL DEVICES BY US FDA

- 5.10.2.1.2 Canada

- 5.10.2.2 Europe

- 5.10.2.3 Asia Pacific

- 5.10.2.3.1 Japan

- TABLE 10 CLASSIFICATION OF MEDICAL DEVICES AND REVIEWING BODY IN JAPAN

- 5.10.2.3.2 China

- TABLE 11 NMPA MEDICAL DEVICE CLASSIFICATION

- 5.10.2.3.3 India

- 5.10.3 INTEROPERABILITY STANDARDS

- TABLE 12 KEY STANDARDS FOR INTEROPERABILITY IN DIGITAL HEALTH SPECTRUM

- TABLE 13 QUALITATIVE ANALYSIS OF WIDELY USED DATA TRANSMISSION STANDARDS IN DIGITAL HEALTH SPECTRUM

- 5.11 PRICING ANALYSIS

- 5.11.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT

- FIGURE 27 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT

- TABLE 14 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT

- 5.11.2 REGIONAL PRICING ANALYSIS OF MEDICAL SIMULATORS

- 5.12 HEALTHCARE SIMULATION MARKET INVESTMENT LANDSCAPE

- FIGURE 28 HEALTHCARE SIMULATION FUNDING IN 2022

- FIGURE 29 MOST VALUED HEALTHCARE SIMULATION FIRMS IN 2022 (USD BILLION)

- 5.13 KEY CONFERENCES AND EVENTS (Q4 2023-Q3 2024)

- 5.14 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 30 REVENUE SHIFT IN HEALTHCARE SIMULATION MARKET

- 5.15 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- TABLE 15 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- 5.15.2 BUYING CRITERIA

- FIGURE 32 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 16 KEY BUYING CRITERIA FOR TOP THREE END USERS

- 5.16 CASE STUDY ANALYSIS

- 5.16.1 CASE STUDY 1

- 5.16.2 CASE STUDY 2

- 5.17 UNMET NEEDS

- TABLE 17 UNMET NEEDS IN HEALTHCARE SIMULATION MARKET

- 5.17.1 END USER EXPECTATIONS

- TABLE 18 END USER EXPECTATIONS IN HEALTHCARE SIMULATION MARKET

6 HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE

- 6.1 INTRODUCTION

- TABLE 19 HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- 6.2 HEALTHCARE SIMULATION ANATOMICAL MODELS

- TABLE 20 HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 21 HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1 PATIENT SIMULATORS

- TABLE 22 KEY PLAYERS OFFERING PATIENT SIMULATORS

- TABLE 23 PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 24 PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 25 PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.1 By type

- 6.2.1.1.1 High-fidelity simulators

- 6.2.1.1.1.1 Growing adoption of high-fidelity simulators in educational training to drive growth

- 6.2.1.1.1 High-fidelity simulators

- 6.2.1.1 By type

- TABLE 26 KEY MARKET PLAYERS OFFERING HIGH-FIDELITY SIMULATORS

- TABLE 27 HIGH-FIDELITY PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.1.2 Medium-fidelity simulators

- 6.2.1.1.2.1 Cost benefits of medium-fidelity simulation to drive demand

- 6.2.1.1.2 Medium-fidelity simulators

- TABLE 28 KEY MARKET PLAYERS OFFERING MEDIUM-FIDELITY SIMULATORS

- TABLE 29 MEDIUM-FIDELITY PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.1.3 Low-fidelity simulators

- 6.2.1.1.3.1 Budgetary constraints and ease of use to drive demand

- 6.2.1.1.3 Low-fidelity simulators

- TABLE 30 KEY MARKET PLAYERS OFFERING LOW-FIDELITY SIMULATORS

- TABLE 31 LOW-FIDELITY PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.2 By application

- 6.2.1.2.1 Laparoscopic surgical simulators

- 6.2.1.2.1.1 Increasing prevalence of minimally invasive surgeries to drive growth

- 6.2.1.2.1 Laparoscopic surgical simulators

- 6.2.1.2 By application

- TABLE 32 LAPAROSCOPIC SURGICAL PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.2.2 Gynecology simulators

- 6.2.1.2.2.1 Increasing incidence of fibroids and polyps in women to drive demand

- 6.2.1.2.2 Gynecology simulators

- TABLE 33 GYNECOLOGY PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.2.3 Cardiovascular simulators

- 6.2.1.2.3.1 Increasing prevalence of diabetes to boost demand

- 6.2.1.2.3 Cardiovascular simulators

- TABLE 34 CARDIOVASCULAR PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.2.4 Orthopedic surgical simulators

- 6.2.1.2.4.1 Enhancement in surgeon skills by orthopedic simulation training to drive demand

- 6.2.1.2.4 Orthopedic surgical simulators

- TABLE 35 ORTHOPEDIC SURGICAL PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.2.5 Spine surgical simulators

- 6.2.1.2.5.1 Mastering spine surgeries through advanced simulation techniques to boost demand

- 6.2.1.2.5 Spine surgical simulators

- TABLE 36 SPINE SURGICAL PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.2.6 Endovascular simulators

- 6.2.1.2.6.1 Reduced mortality rates associated with endovascular simulators to boost demand

- 6.2.1.2.6 Endovascular simulators

- TABLE 37 ENDOVASCULAR PATIENT SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.1.2.7 Other applications in patient simulators

- TABLE 38 PATIENT SIMULATORS MARKET FOR OTHER APPLICATIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.2 TASK TRAINERS

- 6.2.2.1 Inability to imitate emotional attributes of patients to restrain growth

- TABLE 39 KEY MARKET PLAYERS OFFERING TASK TRAINERS

- TABLE 40 TASK TRAINERS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.3 INTERVENTIONAL/SURGICAL SIMULATORS

- TABLE 41 INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 42 INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 6.2.3.1 Laparoscopic surgical simulators

- 6.2.3.1.1 Increasing preference for minimally invasive surgeries to drive growth

- 6.2.3.1 Laparoscopic surgical simulators

- TABLE 43 KEY MARKET PLAYERS OFFERING LAPAROSCOPIC SURGICAL SIMULATORS

- TABLE 44 LAPAROSCOPIC SURGICAL SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.3.2 Gynecology simulators

- 6.2.3.2.1 Increasing incidence of fibroids and polyps in women to drive demand for gynecology simulators

- 6.2.3.2 Gynecology simulators

- TABLE 45 KEY MARKET PLAYERS OFFERING GYNECOLOGY SIMULATORS

- TABLE 46 GYNECOLOGY SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.3.3 Cardiovascular simulators

- 6.2.3.3.1 Increasing prevalence of obesity and diabetes to boost demand

- 6.2.3.3 Cardiovascular simulators

- TABLE 47 KEY MARKET PLAYERS OFFERING CARDIOVASCULAR SIMULATORS

- TABLE 48 CARDIOVASCULAR SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

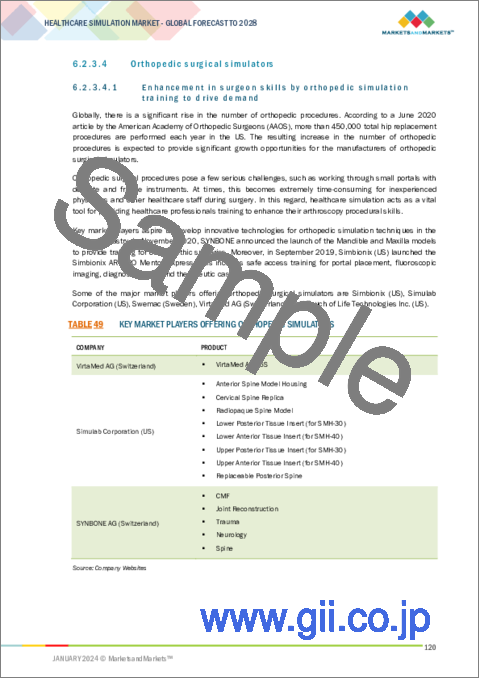

- 6.2.3.4 Orthopedic surgical simulators

- 6.2.3.4.1 Enhancement in surgeon skills by orthopedic simulation training to drive demand

- 6.2.3.4 Orthopedic surgical simulators

- TABLE 49 KEY MARKET PLAYERS OFFERING ORTHOPEDIC SIMULATORS

- TABLE 50 ORTHOPEDIC SURGICAL SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.3.5 Spine surgical simulators

- 6.2.3.5.1 Mastering spine surgeries through advanced simulation techniques to boost demand

- 6.2.3.5 Spine surgical simulators

- TABLE 51 KEY MARKET PLAYERS OFFERING SPINE SURGICAL SIMULATORS

- TABLE 52 SPINE SURGICAL SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.3.6 Endovascular simulators

- 6.2.3.6.1 Ability to reduce mortality rates to drive demand for endovascular simulators

- 6.2.3.6 Endovascular simulators

- TABLE 53 KEY MARKET PLAYERS OFFERING ENDOVASCULAR SIMULATORS

- TABLE 54 ENDOVASCULAR SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.3.7 Other surgical simulators

- TABLE 55 KEY MARKET PLAYERS OFFERING OTHER SURGICAL SIMULATORS

- TABLE 56 OTHER SURGICAL SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.4 ULTRASOUND SIMULATORS

- 6.2.4.1 Inferior quality images due to low dynamics and spatial resolution to restrain growth

- TABLE 57 KEY MARKET PLAYERS OFFERING ULTRASOUND SIMULATORS

- TABLE 58 ULTRASOUND SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.5 DENTAL SIMULATORS

- 6.2.5.1 Expanding dental tourism industry to drive growth

- TABLE 59 KEY PLAYERS OFFERING DENTAL SIMULATORS

- TABLE 60 DENTAL SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.6 EYE SIMULATORS

- 6.2.6.1 Increasing incidence of eye disorders to drive growth

- TABLE 61 KEY PLAYERS OFFERING EYE SIMULATORS

- TABLE 62 EYE SIMULATORS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.3 WEB-BASED SIMULATION

- 6.3.1 RISING TECHNOLOGICAL ADVANCEMENTS TO DRIVE ADOPTION OF WEB-BASED SIMULATION

- TABLE 63 KEY PLAYERS OFFERING WEB-BASED SIMULATORS

- TABLE 64 WEB-BASED SIMULATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.4 HEALTHCARE SIMULATION SOFTWARE

- 6.4.1 KEY ADVANTAGES OFFERED BY HEALTHCARE SIMULATION SOFTWARE TO DRIVE ADOPTION

- TABLE 65 KEY MARKET PLAYERS OFFERING HEALTHCARE SIMULATION SOFTWARE

- TABLE 66 HEALTHCARE SIMULATION SOFTWARE MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.5 HEALTHCARE SIMULATION TRAINING SERVICES

- TABLE 67 HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 68 HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.5.1 VENDOR-BASED TRAINING

- 6.5.1.1 High focus on patient safety to drive demand

- TABLE 69 KEY MARKET PLAYERS OFFERING VENDOR-BASED TRAINING SERVICES

- TABLE 70 VENDOR-BASED TRAINING SERVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.5.2 EDUCATIONAL SOCIETIES

- 6.5.2.1 Growing need for proper training and authenticity of knowledge to drive growth

- TABLE 71 KEY PLAYERS OFFERING EDUCATIONAL SOCIETIES SIMULATORS

- TABLE 72 EDUCATIONAL SOCIETIES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.5.3 CUSTOM CONSULTING SERVICES

- 6.5.3.1 Growing need to limit errors associated with traditional medical training systems to drive growth

- TABLE 73 KEY MARKET PLAYERS OFFERING CUSTOM CONSULTING SERVICES

- TABLE 74 CUSTOM CONSULTING SERVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

7 HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- TABLE 75 HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- 7.2 VIRTUAL PATIENT SIMULATION

- 7.2.1 INCREASING FOCUS ON AUGMENTED REALITY/VIRTUAL REALITY TO DRIVE MARKET

- TABLE 76 VIRTUAL PATIENT SIMULATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 7.3 3D PRINTING

- 7.3.1 INCREASING ADOPTION IN MEDICAL TRAINING TO DRIVE MARKET

- TABLE 77 3D PRINTING MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 7.4 PROCEDURAL REHEARSAL TECHNOLOGY

- 7.4.1 IMPROVING SURGICAL SKILLS WITH PROCEDURAL REHEARSAL TECHNOLOGY TO DRIVE MARKET

- TABLE 78 PROCEDURAL REHEARSAL TECHNOLOGY MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

8 HEALTHCARE SIMULATION MARKET, BY END USER

- 8.1 INTRODUCTION

- TABLE 79 HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 8.2 ACADEMIC INSTITUTES

- 8.2.1 GROWING NEED FOR SKILLED MEDICAL PROFESSIONALS TO DRIVE DEMAND

- TABLE 80 HEALTHCARE SIMULATION MARKET FOR ACADEMIC INSTITUTES, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.3 HOSPITALS

- 8.3.1 RISING FOCUS ON MINIMIZING MEDICAL ERRORS TO DRIVE DEMAND

- TABLE 81 HEALTHCARE SIMULATION MARKET FOR HOSPITALS, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.4 MILITARY ORGANIZATIONS

- 8.4.1 EXPLORATION OF NEW METHODS OF MEDICAL CARE DURING WARFARE TO DRIVE DEMAND

- TABLE 82 HEALTHCARE SIMULATION MARKET FOR MILITARY ORGANIZATIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.5 OTHER END USERS

- TABLE 83 HEALTHCARE SIMULATION MARKET FOR OTHER END USERS, BY COUNTRY, 2021-2028 (USD MILLION)

9 HEALTHCARE SIMULATION MARKET, BY REGION

- 9.1 INTRODUCTION

- TABLE 84 HEALTHCARE SIMULATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 9.2 NORTH AMERICA

- FIGURE 33 NORTH AMERICA: HEALTHCARE SIMULATION MARKET SNAPSHOT (2022)

- TABLE 85 NORTH AMERICA: HEALTHCARE SIMULATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 86 NORTH AMERICA: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 87 NORTH AMERICA: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 88 NORTH AMERICA: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 89 NORTH AMERICA: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 90 NORTH AMERICA: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 91 NORTH AMERICA: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 92 NORTH AMERICA: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 93 NORTH AMERICA: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.2.1 NORTH AMERICA: RECESSION IMPACT ANALYSIS

- 9.2.2 US

- 9.2.2.1 Increasing demand for virtual tutors and high healthcare spending to boost growth

- TABLE 94 US: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 95 US: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 96 US: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 97 US: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 98 US: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 99 US: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 100 US: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 101 US: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.2.3 CANADA

- 9.2.3.1 Increasing funding and surgical capabilities to drive growth

- TABLE 102 CANADA: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 103 CANADA: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 104 CANADA: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 105 CANADA: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 106 CANADA: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 107 CANADA: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 108 CANADA: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 109 CANADA: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3 EUROPE

- TABLE 110 EUROPE: HEALTHCARE SIMULATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 111 EUROPE: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 112 EUROPE: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 113 EUROPE: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 114 EUROPE: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 115 EUROPE: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 116 EUROPE: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 117 EUROPE: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 118 EUROPE: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.1 EUROPE: RECESSION IMPACT ANALYSIS

- 9.3.2 UK

- 9.3.2.1 Rising number of healthcare simulation centers and hospitals to drive growth

- TABLE 119 UK: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 120 UK: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 121 UK: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 122 UK: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 123 UK: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 124 UK: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 125 UK: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 126 UK: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.3 FRANCE

- 9.3.3.1 Growing focus on use of innovative methods in medical training to drive growth

- TABLE 127 FRANCE: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 128 FRANCE: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 129 FRANCE: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 130 FRANCE: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 131 FRANCE: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 132 FRANCE: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 133 FRANCE: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 134 FRANCE: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.4 GERMANY

- 9.3.4.1 High healthcare spending to drive growth

- TABLE 135 GERMANY: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 136 GERMANY: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 137 GERMANY: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 138 GERMANY: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 139 GERMANY: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 140 GERMANY: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 141 GERMANY: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 142 GERMANY: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.5 ITALY

- 9.3.5.1 Shortage of trained healthcare personnel to drive growth

- TABLE 143 ITALY: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 144 ITALY: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 145 ITALY: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 146 ITALY: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 147 ITALY: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 148 ITALY: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 149 ITALY: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 150 ITALY: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.6 SPAIN

- 9.3.6.1 Increasing number of surgical procedures to boost growth

- TABLE 151 SPAIN: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 152 SPAIN: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 153 SPAIN: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 154 SPAIN: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 155 SPAIN: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 156 SPAIN: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 157 SPAIN: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 158 SPAIN: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.7 REST OF EUROPE

- TABLE 159 REST OF EUROPE: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 160 REST OF EUROPE: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 161 REST OF EUROPE: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 162 REST OF EUROPE: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 163 REST OF EUROPE: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 164 REST OF EUROPE: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 165 REST OF EUROPE: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 166 REST OF EUROPE: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4 ASIA PACIFIC

- FIGURE 34 ASIA PACIFIC: HEALTHCARE SIMULATION MARKET SNAPSHOT (2022)

- TABLE 167 ASIA PACIFIC: HEALTHCARE SIMULATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 168 ASIA PACIFIC: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 169 ASIA PACIFIC: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 170 ASIA PACIFIC: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 171 ASIA PACIFIC: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 172 ASIA PACIFIC: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 173 ASIA PACIFIC: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 174 ASIA PACIFIC: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 175 ASIA PACIFIC: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.1 ASIA PACIFIC: RECESSION IMPACT ANALYSIS

- 9.4.2 JAPAN

- 9.4.2.1 Increasing demand for virtual tutors and technologically advanced simulators to drive growth

- TABLE 176 JAPAN: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 177 JAPAN: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 178 JAPAN: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 179 JAPAN: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 180 JAPAN: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 181 JAPAN: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 182 JAPAN: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 183 JAPAN: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.3 CHINA

- 9.4.3.1 Increasing demand for trained medical professionals to drive growth

- TABLE 184 CHINA: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 185 CHINA: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 186 CHINA: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 187 CHINA: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 188 CHINA: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 189 CHINA: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 190 CHINA: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 191 CHINA: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.4 INDIA

- 9.4.4.1 Growing awareness regarding patient safety due to healthcare negligence to drive growth

- TABLE 192 INDIA: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 193 INDIA: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 194 INDIA: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 195 INDIA: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 196 INDIA: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 197 INDIA: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 198 INDIA: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 199 INDIA: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.5 REST OF ASIA PACIFIC

- TABLE 200 REST OF ASIA PACIFIC: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 201 REST OF ASIA PACIFIC: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 202 REST OF ASIA PACIFIC: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 203 REST OF ASIA PACIFIC: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 204 REST OF ASIA PACIFIC: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 205 REST OF ASIA PACIFIC: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 206 REST OF ASIA PACIFIC: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 207 REST OF ASIA PACIFIC: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.5 LATIN AMERICA

- TABLE 208 LATIN AMERICA: HEALTHCARE SIMULATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 209 LATIN AMERICA: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 210 LATIN AMERICA: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 211 LATIN AMERICA: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 212 LATIN AMERICA: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 213 LATIN AMERICA: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 214 LATIN AMERICA: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 215 LATIN AMERICA: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 216 LATIN AMERICA: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.5.1 LATIN AMERICA: RECESSION IMPACT ANALYSIS

- 9.5.2 BRAZIL

- 9.5.2.1 High incidence of chronic diseases to drive market

- TABLE 217 BRAZIL: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 218 BRAZIL: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 219 BRAZIL: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 220 BRAZIL: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 221 BRAZIL: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 222 BRAZIL: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 223 BRAZIL: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 224 BRAZIL: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.5.3 MEXICO

- 9.5.3.1 Disruptive technologies and public-private partnerships to boost growth

- TABLE 225 MEXICO: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 226 MEXICO: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 227 MEXICO: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 228 MEXICO: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 229 MEXICO: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 230 MEXICO: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 231 MEXICO: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 232 MEXICO: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.5.4 REST OF LATIN AMERICA

- TABLE 233 REST OF LATIN AMERICA: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 234 REST OF LATIN AMERICA: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 235 REST OF LATIN AMERICA: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 236 REST OF LATIN AMERICA: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 237 REST OF LATIN AMERICA: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 238 REST OF LATIN AMERICA: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 239 REST OF LATIN AMERICA: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 240 REST OF LATIN AMERICA: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.6 MIDDLE EAST & AFRICA

- TABLE 241 MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 242 MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 243 MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 244 MIDDLE EAST & AFRICA: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 245 MIDDLE EAST & AFRICA: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 246 MIDDLE EAST & AFRICA: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 247 MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 248 MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 249 MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.6.1 MIDDLE EAST & AFRICA: RECESSION IMPACT ANALYSIS

- 9.6.2 GCC

- 9.6.2.1 Focus on enhancing patient care to drive market

- TABLE 250 GCC: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 251 GCC: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 252 GCC: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 253 GCC: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 254 GCC: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 255 GCC: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 256 GCC: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 257 GCC: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.6.3 REST OF MIDDLE EAST & AFRICA

- TABLE 258 REST OF MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 259 REST OF MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION ANATOMICAL MODELS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 260 REST OF MIDDLE EAST & AFRICA: PATIENT SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 261 REST OF MIDDLE EAST & AFRICA: PATIENT SIMULATORS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 262 REST OF MIDDLE EAST & AFRICA: INTERVENTIONAL/SURGICAL SIMULATORS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 263 REST OF MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION TRAINING SERVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 264 REST OF MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 265 REST OF MIDDLE EAST & AFRICA: HEALTHCARE SIMULATION MARKET, BY END USER, 2021-2028 (USD MILLION)

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- TABLE 266 KEY DEVELOPMENTS BY MAJOR PLAYERS BETWEEN JANUARY 2020 AND DECEMBER 2023

- 10.3 REVENUE SHARE ANALYSIS OF TOP MARKET PLAYERS, 2022

- FIGURE 35 HEALTHCARE SIMULATION MARKET: REVENUE SHARE ANALYSIS OF MARKET PLAYERS

- 10.4 MARKET SHARE ANALYSIS

- FIGURE 36 HEALTHCARE SIMULATION: MARKET SHARE ANALYSIS

- 10.5 MARKET RANKING ANALYSIS

- FIGURE 37 HEALTHCARE SIMULATION MARKET RANKING, 2022

- 10.6 BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 38 HEALTHCARE SIMULATION: TOP TRENDING BRAND/PRODUCTS

- 10.6.1 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY PRODUCT & SERVICE

- FIGURE 39 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY PRODUCT & SERVICE

- 10.6.1.1 Laerdal Medical

- 10.6.1.2 CAE Inc.

- 10.6.1.3 Simulab

- 10.6.2 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY TECHNOLOGY PROVIDER COMPANY

- FIGURE 40 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY TECHNOLOGY PROVIDER COMPANY

- 10.6.2.1 Siemens Healthineers AG

- 10.6.2.2 Veradigm

- 10.6.2.3 Koninklijke Philips N.V.

- 10.7 COMPANY EVALUATION MATRIX

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- FIGURE 41 HEALTHCARE SIMULATION MARKET: COMPANY EVALUATION MATRIX, 2022

- 10.7.5 COMPANY FOOTPRINT ANALYSIS

- TABLE 267 OVERALL COMPANY FOOTPRINT (20 COMPANIES)

- TABLE 268 COMPANY PRODUCT & SERVICE FOOTPRINT ANALYSIS (20 COMPANIES)

- TABLE 269 COMPANY REGIONAL FOOTPRINT ANALYSIS (20 COMPANIES)

- 10.8 STARTUP/SME EVALUATION MATRIX

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- FIGURE 42 HEALTHCARE SIMULATION MARKET: STARTUP/SME EVALUATION MATRIX, 2022

- 10.8.5 COMPETITIVE BENCHMARKING

- TABLE 270 HEALTHCARE SIMULATION MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 271 HEALTHCARE SIMULATION MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS (STARTUPS/SMES)

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- TABLE 272 HEALTHCARE SIMULATION MARKET: PRODUCT LAUNCHES, JANUARY 2020- DECEMBER 2023

- 10.9.2 DEALS

- TABLE 273 HEALTHCARE SIMULATION MARKET: DEALS, JANUARY 2020-DECEMBER 2023

- 10.9.3 OTHER DEVELOPMENTS

- TABLE 274 HEALTHCARE SIMULATION MARKET: OTHER DEVELOPMENTS, JANUARY 2020- DECEMBER 2023

11 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, MnM View Right to win, Strategic choices made, Weaknesses and competitive threats) **

- 11.1 KEY PLAYERS

- 11.1.1 CAE INC.

- TABLE 275 CAE INC.: BUSINESS OVERVIEW

- FIGURE 43 CAE INC.: COMPANY SNAPSHOT (2022)

- 11.1.2 LAERDAL MEDICAL

- TABLE 276 LAERDAL MEDICAL: BUSINESS OVERVIEW

- 11.1.3 GAUMARD SCIENTIFIC CO.

- TABLE 277 GAUMARD SCIENTIFIC CO.: BUSINESS OVERVIEW

- 11.1.4 KYOTO KAGAKU

- TABLE 278 KYOTO KAGAKU: BUSINESS OVERVIEW

- 11.1.5 LIMBS & THINGS

- TABLE 279 LIMBS & THINGS: BUSINESS OVERVIEW

- 11.1.6 MENTICE AB

- TABLE 280 MENTICE AB: BUSINESS OVERVIEW

- FIGURE 44 MENTICE AB: COMPANY SNAPSHOT (2022)

- 11.1.7 SIMULAB CORPORATION

- TABLE 281 SIMULAB CORPORATION: BUSINESS OVERVIEW

- 11.1.8 SIMULAIDS

- TABLE 282 SIMULAIDS: BUSINESS OVERVIEW

- 11.1.9 INTELLIGENT ULTRASOUND GROUP PLC

- TABLE 283 INTELLIGENT ULTRASOUND GROUP PLC.: BUSINESS OVERVIEW

- FIGURE 45 INTELLIGENT ULTRASOUND GROUP PLC: COMPANY SNAPSHOT (2022)

- 11.1.10 OPERATIVE EXPERIENCE INC.

- TABLE 284 OPERATIVE EXPERIENCE INC.: BUSINESS OVERVIEW

- 11.1.11 SURGICAL SCIENCE SWEDEN AB

- TABLE 285 SURGICAL SCIENCE SWEDEN AB: BUSINESS OVERVIEW

- FIGURE 46 SURGICAL SCIENCE SWEDEN AB: COMPANY SNAPSHOT (2022)

- 11.1.12 CARDIONICS INC. (SUBSIDIARY OF 3B SCIENTIFIC)

- TABLE 286 CARDIONICS INC.: BUSINESS OVERVIEW

- 11.1.13 VIRTAMED AG

- TABLE 287 VIRTAMED AG: BUSINESS OVERVIEW

- 11.1.14 SYNBONE AG

- TABLE 288 SYNBONE AG: BUSINESS OVERVIEW

- 11.1.15 INGMAR MEDICAL

- TABLE 289 INGMAR MEDICAL: BUSINESS OVERVIEW

- 11.1.16 MEDICAL-X

- TABLE 290 MEDICAL-X: BUSINESS OVERVIEW

- 11.1.17 KAVO DENTAL GMBH

- TABLE 291 KAVO DENTAL GMBH: BUSINESS OVERVIEW

- 11.1.18 ALTAY SCIENTIFIC

- TABLE 292 ALTAY SCIENTIFIC: BUSINESS OVERVIEW

- 11.1.19 TRUCORP LTD.

- TABLE 293 TRUCORP LTD.: BUSINESS OVERVIEW

- 11.1.20 SIMENDO B.V.

- TABLE 294 SIMENDO B.V.: BUSINESS OVERVIEW

- 11.2 OTHER PLAYERS

- 11.2.1 HAAG-STREIT SIMULATION GMBH

- 11.2.2 SYMGERY

- 11.2.3 HRV SIMULATION

- 11.2.4 SYNAPTIVE MEDICAL

- 11.2.5 INOVUS MEDICAL

- *Details on Business Overview, Products Offered, Recent Developments, MnM View, Right to win, Strategic choices made, Weaknesses and competitive threats might not be captured in case of unlisted companies.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 CUSTOMIZATION OPTIONS

- 12.3 RELATED REPORTS

- 12.4 AUTHOR DETAILS