|

|

市場調査レポート

商品コード

1409031

3Dイメージングの世界市場 (~2028年):コンポーネント (ハードウェア・ソフトウェア・サービス・技術)・産業・地域別3D Imaging Market by Component (Hardware, Software, Services, Technology ), Vertical and Region - Global Forecast to 2028 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 3Dイメージングの世界市場 (~2028年):コンポーネント (ハードウェア・ソフトウェア・サービス・技術)・産業・地域別 |

|

出版日: 2024年01月09日

発行: MarketsandMarkets

ページ情報: 英文 323 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

レポート概要

| 調査範囲 | |

|---|---|

| 調査対象年 | 2018-2028年 |

| 基準年 | 2022年 |

| 予測期間 | 2023-2028年 |

| 単位 | 米ドル |

| セグメント | コンポーネント・技術・産業・地域別 |

| 対象地域 | 北米・欧州・アジア太平洋・中東&アフリカ・ラテンアメリカ |

世界の3Dイメージングの市場規模は、予測期間中にCAGR 20.8%で推移し、2023年の343億米ドルから、2028年には884億米ドルの規模に成長すると予測されています。

ヘルスケアおよびライフサイエンス分野における3Dイメージングは、診断、治療、患者ケアに革新をもたらします。内部の構造の全体的なビューを示すことで、病態の理解と特定精度が向上します。この精密な画像は、診断能力を向上させ、侵襲的な処置に取って代わる可能性があるだけでなく、治療計画を最適化し、手術時間を短縮し、健康な組織へのダメージを軽減します。さらに、医療従事者と患者とのコミュニケーションをより明確にし、貴重な教育ツールとしての役割も果たします。AR (拡張現実) や新たなAIとの統合は、手術ナビゲーションと診断精度をさらに向上させます。つまり、3Dイメージングの変革的影響は、詳細な洞察を提供し、処置を合理化し、強化された視覚化と正確な位置特定によって臨床医と患者の双方に力を与え、医療行為の環境を根本的に変える能力にあります。

コンポーネント別では、ハードウェアの部門が予測期間中に最大の規模を示す見通しです。3Dイメージングでは、多様なハードウェアが3Dデータの取得、処理、活用において重要な役割を果たしています。構造化光カメラや飛行時間カメラなどの3Dセンサーは、光の反射を発光・検出することで奥行き情報を取得し、詳細な空間マップの作成を可能にします。これらのセンサーは、顔認識、ジェスチャートラッキング、自動運転車など、さまざまな用途に不可欠です。さらに、3Dスキャナーは、レーザーやカメラを利用して物体や環境の複雑な詳細をキャプチャし、建築、製造、ヘルスケアなどの業界で使用される高精度のデジタルモデルの作成を容易にします。

技術別では、構造化光イメージングの部門が予測期間中に最大のCAGRを維持する見通しです。構造化光イメージングは、3Dイメージングに不可欠な技術であり、既知のパターンを面や物体に投影します。構造化光イメージングは、その精度と複雑な詳細をキャプチャする能力により、製造、ヘルスケア、コンピュータビジョンなどのさまざまな産業で広く採用されており、品質管理、顔認識、医療画像における正確な測定などの用途を可能にし、3次元データの認識・操作の方法に革新をもたらしています。

当レポートでは、世界の3Dイメージングの市場を調査し、市場概要、市場影響因子の分析、技術・特許の動向、法規制環境、ケーススタディ、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要と業界動向

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ケーススタディ分析

- 関税と規制状況

- 規制機関、政府機関、その他の組織

- 貿易分析/HSコード

- 3Dイメージング市場の進化

- エコシステム/市場マップ

- サプライチェーン分析

- 価格分析

- 顧客のビジネスに影響を与える動向/ディスラプション

- 特許分析

- ポーターのファイブフォース分析

- 主要な会議とイベント

- 主要なステークホルダーと購入基準

- 技術分析

- 3Dイメージング市場のロードマップ

- 3Dイメージング市場のベストプラクティス

- 3Dイメージング技術

第6章 3Dイメージング市場:コンポーネント別

- ハードウェア

- 3Dカメラ

- 3Dスキャナー

- 3Dセンサー

- 3Dディスプレイ

- ソフトウェア

- サービス

- プロフェッショナルサービス

- マネージドサービス

第7章 3Dイメージング市場:技術別

- 立体イメージング

- アナグリフィック3D

- 偏光3D

- シャッターガラス

- オートステレオスコピー

- 構造化光イメージング

- 三角測量法

- パターン投影

- デスマッピング・再構築

- オブジェクトスキャニング・測定

- レーザーベースイメージング

- ライダー

- レーザースキャン

- レーザープロファイリング

- レーザーホログラフィー

- ホログラフィックイメージング

- ホログラフィックディスプレイ

- ホログラフィックプロジェクション

- ホログラフィックのキャプチャ&レコーディング

- ホログラフィック干渉計

- 飛行時間型 (TOF) イメージング

- 深度センシング&マッピング

- ジェスチャー認識

- 3Dスキャン

- 顔認識

第8章 3Dイメージング市場:産業別

- 航空宇宙・防衛

- 自動車

- 製造

- ヘルスケア&ライフサイエンス

- 建築・建設

- メディア&エンターテイメント

- 小売・電子商取引

- 政府

- エネルギー・ユーティリティ

- その他

第9章 3Dイメージング市場:地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第10章 競合情勢

- 概要

- 主要企業の戦略

- 収益分析

- 市場シェア分析

- ブランド/製品の比較分析

- 企業評価マトリックス

- スタートアップ/中小企業の評価マトリックス

- 競合シナリオと動向

- 主要ベンダーの評価と財務指標

第11章 企業プロファイル

- 主要企業

- GE HEALTHCARE

- AUTODESK

- STMICROELECTRONICS

- PANASONIC

- SONY

- TRIMBLE

- FARO

- PHILIPS

- ADOBE

- HP

- DASSAULT SYSTEMES

- BENTLEY SYSTEMS

- その他の企業

- LOCKHEED MARTIN

- ESRI

- TOPCON

- ABLE SOFTWARE

- スタートアップ/SME

- MAXON

- ESRI

- ARCHILOGIC

- PIX4D

- BRAINKEY

- PRECISMO

- KAARTA

- LIGTHCODE PHOTONICS

- VZENSE TECHNOLOGY

- CAPOOM

- ATOMONTAGE

- HIVEMAPPER

- SHAPR3D

- INNERSIGHT

第12章 隣接市場および関連市場

第13章 付録

Report Description

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2018-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | USD Billion |

| Segments | By Component, Technology, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America |

The global market for 3D Imaging market is projected to grow from USD 34.3 billion in 2023 to USD 88.4 billion by 2028, at a CAGR of 20.8% during the forecast period. 3D imaging in healthcare and life sciences sector revolutionizes diagnostics, treatment, and patient care. Offering comprehensive views of internal structures, enhances understanding and accuracy in identifying pathologies. This precise imaging not only improves diagnostic capabilities, potentially replacing invasive procedures, but also optimizes treatment planning, reducing operating time and damage to healthy tissue. Moreover, it fosters clearer communication between healthcare professionals and patients, serving as a valuable educational tool. Integration with augmented reality and emerging AI further refines surgical navigation and diagnostic accuracy. Ultimately, 3D imaging's transformative impact lies in its ability to provide detailed insights, streamline procedures, and empower both clinicians and patients with enhanced visualization and precise localization, fundamentally altering the landscape of medical practice.

"The hardware segment is projected to be the largest market during the forecast period."

In 3D imaging, diverse hardware plays significant roles in capturing, processing, and utilizing three-dimensional data. 3D sensors, such as structured light or time-of-flight cameras, acquire depth information by emitting and detecting light reflections, enabling the creation of detailed spatial maps. These sensors are integral in various applications, including facial recognition, gesture tracking, and autonomous vehicles. Additionally, 3D scanners utilize lasers or cameras to capture intricate details of objects or environments, facilitating the creation of highly accurate digital models used in industries such as architecture, manufacturing, and healthcare. Complementing this, 3D printers interpret digital designs to produce physical objects layer by layer, revolutionizing prototyping, product development, and even biomedical applications by generating custom prosthetics or tissue scaffolds. The convergence of these hardware components empowers industries with transformative capabilities, ranging from precise data acquisition to the tangible manifestation of digitally conceived creations.

"Among Technology, Structured Light Imaging is anticipated to hold the highest CAGR during the forecast period."

Structured light imaging is a technique vital in 3D imaging that involves projecting a known pattern onto a surface or object. This pattern, often grids or stripes, distorts upon hitting the object and is captured by a camera, allowing precise depth and shape calculations based on the distortion. The deformation of the pattern provides information used to reconstruct a detailed three-dimensional model of the object or surface. This method is widely employed in various industries such as manufacturing, healthcare, and computer vision due to its accuracy and ability to capture intricate details, enabling applications such as quality control, facial recognition, and precise measurements in medical imaging, thereby revolutionizing how we perceive and interact with three-dimensional data.

"Among services, the professional services is anticipated to hold the largest market during the forecast period."

Professional services in 3D imaging encompass consulting services, support and maintenance, and deployment and integration to optimize technology integration. These services offer tailored solutions, training programs, and ongoing support for seamless incorporation into workflows. These services ensure efficient utilization, addressing specific industry needs, and providing continuous maintenance for sustained performance, enhancing the overall effectiveness of 3D imaging solutions across diverse sectors.

"North America to account for the largest market size during the forecast period."

North America emerged as the primary revenue hub in the global 3D imaging market. The region's dominance is fueled by substantial investments in cutting-edge technologies such as AI and IoT, specifically aimed at producing high-resolution 3D images. These robust investments significantly bolster market expansion, enabling organizations, particularly in the US, to embrace 3D imaging sensor hardware and animation solutions. This adoption aims to elevate customer experiences, highlighting a strategic shift towards leveraging advanced imaging technologies for enhanced engagement and service delivery. The concerted efforts and investments made by companies in these technological avenues underscore North America's pivotal role in spearheading the evolution and application of 3D imaging within diverse industries.

Breakdown of primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the 3D Imaging market.

- By Company: Tier I: 15%, Tier II: 40%, and Tier III: 45%

- By Designation: C-Level Executives: 50%, Directors: 30%, and Others: 20%

- By Region: North America: 25%, Europe: 30%, APAC: 30%, MEA: 10%, Latin America: 5%

Major vendors offering 3D Imaging solutions and services across the globe GE Healthcare (US), Autodesk (US), STMicroelectronics (Switzerland), Panasonic (Japan), Sony Corporation (Japan), Trimble (US), FARO Technologies (US), Philips (Netherlands), Google (US), Adobe (US), HP (US), Dassault Systemes (France), Bentley Systems (US), Lockheed Martin (US), Topcon (Japan), Able Software (US), Maxon (Germany), ESRI (US), Archilogic (Switzerland), Pix4D (Switzerland), Brainkey (US), Precismo (US), Kaarta (US), LightCode Photonics (Estonia), Vzense Technology (US), Capoom (Istanbul), Atomontage (US), Hivemapper (US), Shapr3D (Hungary), Innersight (UK).

Research Coverage

The market study covers 3D Imaging Market across segments. It aims to estimate the market size and the growth potential across different segments, such as component, technology, vertical, and region. It includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market for 3D Imaging market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights better to position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (rising demand for personalized medicine, growth in entertainment and media entertainment, rising demand for 3D-enabled devices across verticals, increasing urbanization, push for productivity, and environment concerns in the architecture and construction vertical), restraints (limited field of view and depth perception, high maintenance costs of 3D imaging hardware, interoperability issues with 3D imaging solutions and hardware), opportunities (adoption of 3D printing in healthcare, increasing investments in AI by 3D medical imaging device manufacturers, high demand for 3D imaging solutions in the retail and eCommerce vertical), and challenges (the need for education and training, data processing and storage demands, high power consumption requirements for 3D image processing) influencing the growth of the 3D Imaging market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the 3D Imaging market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the 3D Imaging market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in 3D Imaging market strategies; the report also helps stakeholders understand the pulse of the 3D Imaging market and provides them with information on key market drivers, restraints, challenges, and opportunities.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as GE Healthcare (US), Adobe (US), Autodesk (US), Trimble (US), Dassault Systemes (France), and others in the 3D Imaging market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATES, 2020-2022

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 3D IMAGING MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- FIGURE 2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- FIGURE 3 3D IMAGING MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 1 (SUPPLY SIDE): REVENUE OF HARDWARE/SOFTWARE/SERVICES OF 3D IMAGING MARKET

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 2, BOTTOM-UP (SUPPLY SIDE): COLLECTIVE REVENUE OF ALL HARDWARE/SOFTWARE/SERVICES OF 3D IMAGING MARKET

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 3, TOP-DOWN (DEMAND SIDE): SHARE OF 3D IMAGING SOFTWARE THROUGH OVERALL 3D IMAGING SPENDING

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 4, BOTTOM-UP (DEMAND SIDE)

- 2.4 MARKET FORECAST

- TABLE 2 FACTOR ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 LIMITATIONS AND RISK ASSESSMENT

- 2.7 IMPLICATIONS OF RECESSION ON 3D IMAGING MARKET

3 EXECUTIVE SUMMARY

- TABLE 3 GLOBAL 3D IMAGING MARKET AND GROWTH RATE, 2018-2022 (USD MILLION, Y-O-Y GROWTH)

- TABLE 4 GLOBAL 3D IMAGING MARKET AND GROWTH RATE, 2023-2028 (USD MILLION, Y-O-Y GROWTH)

- FIGURE 8 HARDWARE SEGMENT TO BE DOMINANT MARKET IN 2023

- FIGURE 9 3D DISPLAY SEGMENT TO LEAD MARKET IN 2023

- FIGURE 10 3D MODELING SOFTWARE SEGMENT TO LEAD MARKET IN 2023

- FIGURE 11 STRUCTURED LIGHT IMAGING SEGMENT TO ACCOUNT FOR LARGEST SHARE IN 2023

- FIGURE 12 PROFESSIONAL SERVICES SEGMENT TO LEAD MARKET IN 2023

- FIGURE 13 DEPLOYMENT & INTEGRATION SEGMENT TO ACCOUNT FOR LARGEST SHARE IN 2023

- FIGURE 14 AUTOMOTIVE SEGMENT TO LEAD MARKET IN 2023

- FIGURE 15 3D IMAGING MARKET SNAPSHOT: REGIONAL ANALYSIS

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN 3D IMAGING MARKET

- FIGURE 16 RISING DEMAND FOR 3D-ENABLED DEVICES ACROSS VERTICALS AND INCREASING URBANIZATION TO DRIVE 3D IMAGING MARKET GROWTH

- 4.2 3D IMAGING MARKET: RECESSION OVERVIEW

- FIGURE 17 3D IMAGING MARKET TO WITNESS MINOR DECLINE IN Y-O-Y GROWTH RATE IN 2023

- 4.3 3D IMAGING MARKET: TOP 3 VERTICALS

- FIGURE 18 MANUFACTURING VERTICAL TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- 4.4 3D IMAGING MARKET, BY REGION

- FIGURE 19 NORTH AMERICA TO ACCOUNT FOR LARGEST SHARE IN 2023

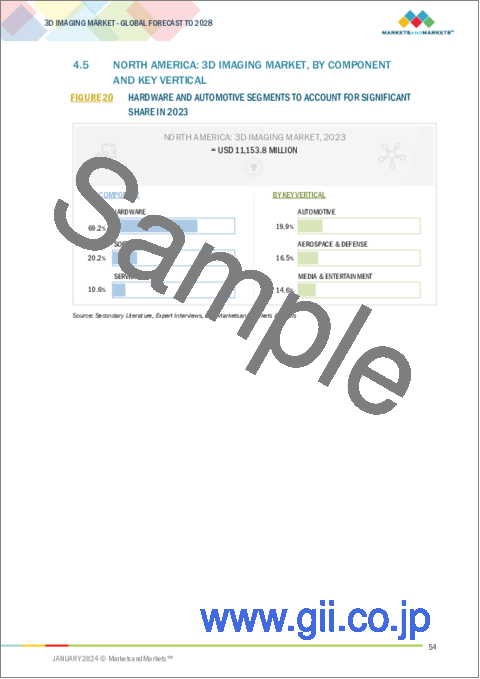

- 4.5 NORTH AMERICA: 3D IMAGING MARKET, BY COMPONENT AND KEY VERTICAL

- FIGURE 20 HARDWARE AND AUTOMOTIVE SEGMENTS TO ACCOUNT FOR SIGNIFICANT SHARE IN 2023

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 21 3D IMAGING MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Rising demand for personalized medicines

- 5.2.1.2 Growth in entertainment & media industry

- 5.2.1.3 Rising demand for 3D-enabled devices across verticals

- 5.2.1.4 Increasing urbanization, push for productivity, and environment concerns in architecture and construction vertical

- 5.2.2 RESTRAINTS

- 5.2.2.1 Limited field of view and depth perception

- 5.2.2.2 High maintenance cost of 3D imaging hardware

- 5.2.2.3 Interoperability issues with 3D imaging solutions and hardware

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Adoption of 3D printing in healthcare

- 5.2.3.2 Increasing investments in AI by 3D medical imaging device manufacturers

- 5.2.3.3 High demand for 3D imaging solutions in retail & eCommerce vertical

- 5.2.4 CHALLENGES

- 5.2.4.1 Need for education and training

- 5.2.4.2 Demand for data processing and storage

- 5.2.4.3 High power consumption requirements

- 5.3 CASE STUDY ANALYSIS

- 5.3.1 TATA INTERACTIVE SYSTEMS (TIS) COLLABORATED WITH AUTODESK TO INNOVATE ELEARNING WITH 3D ANIMATION

- 5.3.2 JP CULLEN ADOPTED TRIMBLE'S SOLUTIONS TO BUILD HIGH-QUALITY PRODUCTS WITH 3D MODELING

- 5.3.3 KOBELCO CONSTRUCTION MACHINERY COLLABORATED WITH DASSAULT SYSTEMES TO MANAGE GLOBAL MANUFACTURING OPERATIONS

- 5.3.4 FEOPS COLLABORATED WITH DASSAULT SYSTEMES TO IMPROVE OUTCOMES IN HEART VALVE REPLACEMENT

- 5.3.5 TRUEPOINT PROVIDED 3D LASER SCANNING AND MODELING SERVICES FOR POWER PLANT IN MICHIGAN

- 5.3.6 CHINA RAILWAY DESIGN CORPORATION ADOPTED DASSAULT SYSTEMES' 3DEXPERIENCE PLATFORM TO DESIGN RAILWAY PROJECTS

- 5.3.7 BIOLITE ADOPTED AUTODESK SOFTWARE TO CREATE ELECTRICITY-GENERATING BIOMASS STOVES FOR IMPROVING PUBLIC HEALTH

- 5.4 TARIFF AND REGULATORY LANDSCAPE

- 5.4.1 TARIFF RELATED TO 3D IMAGING MARKET

- TABLE 5 TARIFF RELATED TO 3D IMAGING MARKET, 2022

- 5.5 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.5.1 NORTH AMERICA

- TABLE 6 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.5.2 EUROPE

- TABLE 7 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.5.3 ASIA PACIFIC

- TABLE 8 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.5.4 MIDDLE EAST & AFRICA

- TABLE 9 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.5.5 LATIN AMERICA

- TABLE 10 LATIN AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.6 TRADE ANALYSIS/HS CODE

- 5.6.1 IMPORT SCENARIO OF TELEVISION CAMERAS, DIGITAL CAMERAS, AND VIDEO CAMERA RECORDERS

- FIGURE 22 IMPORT DATA FOR TELEVISION CAMERAS, DIGITAL CAMERAS, AND VIDEO CAMERA RECORDERS, BY KEY COUNTRY, 2015-2022 (USD MILLION)

- 5.6.2 EXPORT SCENARIO OF TELEVISION CAMERAS, DIGITAL CAMERAS, AND VIDEO CAMERA RECORDERS

- FIGURE 23 EXPORT DATA FOR TELEVISION CAMERAS, DIGITAL CAMERAS, AND VIDEO CAMERA RECORDERS, BY KEY COUNTRY, 2015-2022 (USD MILLION)

- 5.7 3D IMAGING MARKET EVOLUTION

- FIGURE 24 EVOLUTION OF 3D IMAGING TECHNOLOGIES

- 5.8 ECOSYSTEM/MARKET MAP

- FIGURE 25 KEY PLAYERS IN 3D IMAGING MARKET ECOSYSTEM

- TABLE 11 ROLE OF PLAYERS IN 3D IMAGING MARKET ECOSYSTEM

- 5.9 SUPPLY CHAIN ANALYSIS

- FIGURE 26 SUPPLY CHAIN ANALYSIS

- 5.10 PRICING ANALYSIS

- 5.10.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY HARDWARE

- FIGURE 27 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY HARDWARE

- 5.10.2 INDICATIVE PRICING ANALYSIS OF 3D IMAGING SOFTWARE

- TABLE 12 INDICATIVE PRICING LEVELS OF 3D IMAGING SOFTWARE

- 5.11 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 28 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.12 PATENT ANALYSIS

- 5.12.1 METHODOLOGY

- 5.12.2 PATENTS FILED, BY DOCUMENT TYPE

- TABLE 13 PATENTS FILED, 2013-2023

- 5.12.3 INNOVATION AND PATENT APPLICATIONS

- FIGURE 29 NUMBER OF PATENTS GRANTED, 2013-2023

- 5.12.4 TOP 10 PATENT APPLICANTS IN 3D IMAGING MARKET

- FIGURE 30 TOP 10 PATENT APPLICANTS IN 3D IMAGING MARKET, 2013-2023

- FIGURE 31 REGIONAL ANALYSIS OF PATENTS GRANTED, 2013-2023

- TABLE 14 TOP 20 PATENT OWNERS IN 3D IMAGING MARKET, 2013-2023

- TABLE 15 LIST OF PATENTS ISSUED IN 3D IMAGING MARKET, 2021-2022

- 5.13 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 32 PORTER'S FIVE FORCES ANALYSIS

- 5.13.1 THREAT OF NEW ENTRANTS

- 5.13.2 THREAT OF SUBSTITUTES

- 5.13.3 BARGAINING POWER OF SUPPLIERS

- 5.13.4 BARGAINING POWER OF BUYERS

- 5.13.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.14 KEY CONFERENCES & EVENTS

- TABLE 16 DETAILED LIST OF KEY CONFERENCES & EVENTS, 2023-2024

- 5.15 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 33 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 VERTICALS

- TABLE 17 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 VERTICALS

- 5.15.2 BUYING CRITERIA

- FIGURE 34 KEY BUYING CRITERIA FOR TOP 3 VERTICALS

- TABLE 18 KEY BUYING CRITERIA FOR TOP 3 VERTICALS

- 5.16 TECHNOLOGY ANALYSIS

- 5.16.1 KEY TECHNOLOGIES

- 5.16.1.1 Photogrammetry

- 5.16.1.2 3D printing

- 5.16.1.3 Real-time simulation

- 5.16.2 COMPLIMENTARY TECHNOLOGIES

- 5.16.2.1 Geographic information system

- 5.16.2.2 Digital twin

- 5.16.3 ADJACENT TECHNOLOGIES

- 5.16.3.1 Artificial intelligence & machine learning

- 5.16.3.2 Cloud computing

- 5.16.3.3 Blockchain

- 5.16.1 KEY TECHNOLOGIES

- 5.17 ROADMAP FOR 3D IMAGING MARKET

- TABLE 19 3D IMAGING MARKET ROADMAP, 2023-2030

- 5.18 BEST PRACTICES IN 3D IMAGING MARKET

- TABLE 20 BEST PRACTICES IN 3D IMAGING MARKET

- 5.19 3D IMAGING TECHNIQUES

- FIGURE 35 3D IMAGING TECHNIQUES

6 3D IMAGING MARKET, BY COMPONENT

- 6.1 INTRODUCTION

- 6.1.1 COMPONENTS: 3D IMAGING MARKET DRIVERS

- FIGURE 36 SERVICES SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 21 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 22 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 6.2 HARDWARE

- 6.2.1 INCREASING DEMAND FOR ADVANCED 3D IMAGING HARDWARE AND DEVICES TO DRIVE GROWTH

- TABLE 23 HARDWARE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 24 HARDWARE MARKET, BY REGION, 2023-2028 (USD MILLION)

- FIGURE 37 3D SENSORS SEGMENT TO GROW AT HIGHEST CAGR BY 2028

- TABLE 25 3D IMAGING MARKET, BY HARDWARE, 2018-2022 (USD MILLION)

- TABLE 26 3D IMAGING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- 6.2.2 3D CAMERAS

- 6.2.2.1 3D cameras to revolutionize industries with advanced 3D mapping techniques

- 6.2.2.2 Stereo vision

- 6.2.2.3 Time-of-flight (TOF)

- 6.2.2.4 Structured light

- 6.2.2.5 Laser triangulation

- TABLE 27 3D CAMERAS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 28 3D CAMERAS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.2.3 3D SCANNERS

- 6.2.3.1 Need for improving efficiency and accuracy in manufacturing processes to drive use of 3D scanners

- 6.2.3.2 Laser scanners

- 6.2.3.3 Optimal scanners

- 6.2.3.4 Portable scanners

- 6.2.3.5 Handheld scanners

- 6.2.3.6 Others

- TABLE 29 3D SCANNERS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 30 3D SCANNERS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.2.4 3D SENSORS

- 6.2.4.1 Rise in demand for 3D imaging sensors and their rapidly evolving applications in IoT and AI technologies to drive growth

- 6.2.4.2 Depth sensors

- 6.2.4.3 Image sensors

- 6.2.4.4 Position sensors

- 6.2.4.5 Accelerometers

- 6.2.4.6 Others

- TABLE 31 3D SENSORS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 32 3D SENSORS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.2.5 3D DISPLAY

- 6.2.5.1 Need for evolution and expansion of 3D display technology and innovations to fuel market growth

- 6.2.5.2 Volumetric displays

- 6.2.5.3 Stereoscopic displays

- 6.2.5.4 Head-mounted displays

- TABLE 33 3D DISPLAY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 34 3D DISPLAY MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3 SOFTWARE

- 6.3.1 INCREASING REQUIREMENTS FOR ADVANCED SOFTWARE TO FUEL EVOLUTION OF 3D IMAGING

- FIGURE 38 3D MODELING SOFTWARE SEGMENT TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- TABLE 35 3D IMAGING MARKET, BY SOFTWARE, 2018-2022 (USD MILLION)

- TABLE 36 3D IMAGING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- 6.3.2 SOFTWARE, BY TYPE

- 6.3.2.1 3D modeling software

- 6.3.2.1.1 Rising need to create digital 3D representation used in multiple industries to drive growth

- 6.3.2.1 3D modeling software

- TABLE 37 3D MODELING SOFTWARE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 38 3D MODELING SOFTWARE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3.2.2 3D scanning software

- 6.3.2.2.1 Growing demand for 3D scanning in diverse industries and role of advanced software solutions to boost growth

- 6.3.2.2 3D scanning software

- TABLE 39 3D SCANNING SOFTWARE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 40 3D SCANNING SOFTWARE MARKET, BY REGION, 2023-2028 (USD MILLION)

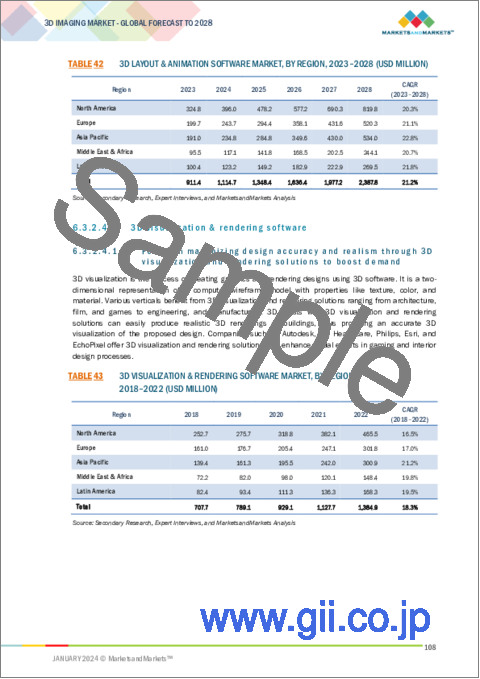

- 6.3.2.3 3D layout & animation software

- 6.3.2.3.1 Need for enhancing animation and motion picture quality to fuel market growth

- 6.3.2.3 3D layout & animation software

- TABLE 41 3D LAYOUT & ANIMATION SOFTWARE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 42 3D LAYOUT & ANIMATION SOFTWARE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3.2.4 3D visualization & rendering software

- 6.3.2.4.1 Focus on maximizing design accuracy and realism through 3D visualization and rendering solutions to boost demand

- 6.3.2.4 3D visualization & rendering software

- TABLE 43 3D VISUALIZATION & RENDERING SOFTWARE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 44 3D VISUALIZATION & RENDERING SOFTWARE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3.2.5 Image reconstruction software

- 6.3.2.5.1 Emphasis on improving medical imaging with image reconstruction software to drive market expansion

- 6.3.2.5 Image reconstruction software

- TABLE 45 IMAGE RECONSTRUCTION SOFTWARE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 46 IMAGE RECONSTRUCTION SOFTWARE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3.3 SOFTWARE, BY DEPLOYMENT MODE

- TABLE 47 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 48 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2028 (USD MILLION)

- 6.3.3.1 On-premises

- 6.3.3.1.1 Rapid growth in on-premises 3D imaging solutions and hardware adoption for better patient record management to propel growth

- 6.3.3.1 On-premises

- TABLE 49 ON-PREMISES: 3D IMAGING SOFTWARE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 50 ON-PREMISES: 3D IMAGING SOFTWARE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3.3.2 Cloud

- 6.3.3.2.1 Benefits of cloud-based 3D imaging solutions for efficient management and cost-effective operations to drive their adoption

- 6.3.3.2 Cloud

- TABLE 51 CLOUD: 3D IMAGING SOFTWARE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 52 CLOUD: 3D IMAGING SOFTWARE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4 SERVICES

- FIGURE 39 MANAGED SERVICES SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 53 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 54 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- TABLE 55 SERVICES: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 56 SERVICES: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4.1 PROFESSIONAL SERVICES

- 6.4.1.1 Vital role of professional services in navigating complex technological landscapes to drive market

- FIGURE 40 DEPLOYMENT & INTEGRATION SEGMENT TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- TABLE 57 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2018-2022 (USD MILLION)

- TABLE 58 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2023-2028 (USD MILLION)

- TABLE 59 PROFESSIONAL SERVICES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 60 PROFESSIONAL SERVICES MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4.1.2 Consulting services

- TABLE 61 CONSULTING SERVICES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 62 CONSULTING SERVICES MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4.1.3 Deployment & integration

- TABLE 63 DEPLOYMENT & INTEGRATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 64 DEPLOYMENT & INTEGRATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4.1.4 Support & maintenance

- TABLE 65 SUPPORT & MAINTENANCE MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 66 SUPPORT & MAINTENANCE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4.2 MANAGED SERVICES

- 6.4.2.1 Need for understanding importance of managed services for enhancing client experience to boost growth

- TABLE 67 MANAGED SERVICES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 68 MANAGED SERVICES MARKET, BY REGION, 2023-2028 (USD MILLION)

7 3D IMAGING MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.1.1 TECHNOLOGIES: 3D IMAGING MARKET DRIVERS

- FIGURE 41 STEREOSCOPIC IMAGING SEGMENT TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- TABLE 69 3D IMAGING MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 70 3D IMAGING MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 7.2 STEREOSCOPIC IMAGING

- 7.2.1 INCREASING APPLICATION OF STEREOSCOPIC IMAGING IN VARIOUS INDUSTRIES TO IMPROVE WORK QUALITY

- TABLE 71 STEREOSCOPIC IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 72 STEREOSCOPIC IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.2.2 ANAGLYPHIC 3D

- 7.2.3 POLARIZED 3D

- 7.2.4 SHUTTER GLASSES

- 7.2.5 AUTOSTEREOSCOPY

- 7.3 STRUCTURED LIGHT IMAGING

- 7.3.1 HIGH ACCURACY AND ROBUSTNESS OF STRUCTURED LIGHT IMAGING TO BOOST ITS POPULARITY

- TABLE 73 STRUCTURED LIGHT IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 74 STRUCTURED LIGHT IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.3.2 TRIANGULATION METHOD

- 7.3.3 PATTERN PROJECTION

- 7.3.4 DEATH MAPPING AND RECONSTRUCTION

- 7.3.5 OBJECT SCANNING AND MEASUREMENT

- 7.4 LASER-BASED IMAGING

- 7.4.1 LASER-BASED IMAGING DRIVES INNOVATION AND PRECISION ACROSS VARIOUS INDUSTRIES

- TABLE 75 LASER-BASED IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 76 LASER-BASED IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.4.2 LIDAR

- 7.4.3 LASER SCANNING

- 7.4.4 LASER PROFILING

- 7.4.5 LASER HOLOGRAPHY

- 7.5 HOLOGRAPHIC IMAGING

- 7.5.1 FOCUS ON ENHANCING VISUALIZATION AND DECISION-MAKING PROCESSES IN DIVERSE INDUSTRIES TO PROPEL GROWTH

- TABLE 77 HOLOGRAPHIC IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 78 HOLOGRAPHIC IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.5.2 HOLOGRAPHIC DISPLAYS

- 7.5.3 HOLOGRAPHIC PROJECTION

- 7.5.4 HOLOGRAPHIC CAPTURE AND RECORDING

- 7.5.5 HOLOGRAPHIC INTERFEROMETRY

- 7.6 TIME-OF-FLIGHT (TOF) IMAGING

- 7.6.1 INCREASING USE OF TOF SENSORS IN ENHANCING SAFETY AND EFFICIENCY IN AUTOMOTIVE AND INDUSTRIAL SECTORS TO ENCOURAGE GROWTH

- TABLE 79 TIME-OF-FLIGHT IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 80 TIME-OF-FLIGHT IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.6.2 DEPTH SENSING & MAPPING

- 7.6.3 GESTURE RECOGNITION

- 7.6.4 3D SCANNING

- 7.6.5 FACIAL RECOGNITION

8 3D IMAGING MARKET, BY VERTICAL

- 8.1 INTRODUCTION

- 8.1.1 VERTICALS: 3D IMAGING MARKET DRIVERS

- FIGURE 42 MANUFACTURING SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 81 3D IMAGING MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 82 3D IMAGING MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 8.2 AEROSPACE & DEFENSE

- 8.2.1 NEED FOR INTEGRATING 3D IMAGING SOLUTIONS TO REVOLUTIONIZE AEROSPACE & DEFENSE SECTOR

- TABLE 83 AEROSPACE & DEFENSE: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 84 AEROSPACE & DEFENSE: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.2.2 AEROSPACE & DEFENSE: 3D IMAGING APPLICATIONS

- 8.2.2.1 Wing and airframe analysis

- 8.2.2.2 Surveillance & reconnaissance

- 8.2.2.3 Target area visualization

- 8.2.2.4 Flight simulators & virtual reality training

- 8.2.2.5 Others

- 8.3 AUTOMOTIVE

- 8.3.1 NEED FOR ASSESSING DRIVERS' ATTENTIVENESS AND ENHANCING PARKING ASSISTANCE SYSTEMS TO DRIVE MARKET

- TABLE 85 AUTOMOTIVE: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 86 AUTOMOTIVE: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.3.2 AUTOMOTIVE: 3D IMAGING APPLICATIONS

- 8.3.2.1 Automated parking systems

- 8.3.2.2 Collision avoidance systems

- 8.3.2.3 Driver assistance systems

- 8.3.2.4 Autonomous vehicles

- 8.3.2.5 Others

- 8.4 MANUFACTURING

- 8.4.1 3D IMAGING TECHNOLOGY TO REVOLUTIONIZE MANUFACTURING SECTOR WITH ITS TRANSFORMATIVE INFLUENCE

- TABLE 87 MANUFACTURING: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 88 MANUFACTURING: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.4.2 MANUFACTURING: 3D IMAGING APPLICATIONS

- 8.4.2.1 Defect detection

- 8.4.2.2 Assembly line optimization

- 8.4.2.3 Inventory management

- 8.4.2.4 Manufacturing process optimization

- 8.4.2.5 Others

- 8.5 HEALTHCARE & LIFE SCIENCES

- 8.5.1 DEMAND FOR ADVANCED DIAGNOSTICS, PERSONALIZED TREATMENT, AND PATIENT ENGAGEMENT TO DRIVE 3D IMAGING TECHNOLOGY

- TABLE 89 HEALTHCARE & LIFE SCIENCES: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 90 HEALTHCARE & LIFE SCIENCES: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.5.2 HEALTHCARE & LIFE SCIENCES: 3D IMAGING APPLICATIONS

- 8.5.2.1 Medical imaging

- 8.5.2.2 Surgical planning

- 8.5.2.3 Patient monitoring

- 8.5.2.4 Diagnostic imaging

- 8.5.2.5 Others

- 8.6 ARCHITECTURE & CONSTRUCTION

- 8.6.1 RISING NEED TO PROVIDE COMPREHENSIVE VISUALIZATIONS THAT GUIDE ON-SITE ACTIVITIES TO BOOST MARKET DEMAND

- TABLE 91 ARCHITECTURE & CONSTRUCTION: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 92 ARCHITECTURE & CONSTRUCTION: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.6.2 ARCHITECTURE & CONSTRUCTION: 3D IMAGING APPLICATIONS

- 8.6.2.1 Architectural visualization

- 8.6.2.2 Building information modeling (BIM)

- 8.6.2.3 Site analysis & surveying

- 8.6.2.4 Restoration & preservation

- 8.6.2.5 Others

- 8.7 MEDIA & ENTERTAINMENT

- 8.7.1 EMPHASIS ON REDEFINING ENTERTAINMENT AND GAMING WITH UNPRECEDENTED REALISM AND ENGAGEMENT THROUGH 3D IMAGING TO DRIVE MARKET

- TABLE 93 MEDIA & ENTERTAINMENT: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 94 MEDIA & ENTERTAINMENT: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.7.2 MEDIA & ENTERTAINMENT: 3D IMAGING APPLICATIONS

- 8.7.2.1 Character modeling and animation

- 8.7.2.2 Gaming

- 8.7.2.3 Visual effects (VFX)

- 8.7.2.4 Augmented reality & virtual reality

- 8.7.2.5 Others

- 8.8 RETAIL & ECOMMERCE

- 8.8.1 GROWING DEMAND FOR ENHANCED CUSTOMER EXPERIENCE TO DRIVE POPULARITY OF 3D IMAGING SOLUTIONS

- TABLE 95 RETAIL & ECOMMERCE: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 96 RETAIL & ECOMMERCE: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.8.2 RETAIL & ECOMMERCE: 3D IMAGING APPLICATIONS

- 8.8.2.1 Virtual try-ons

- 8.8.2.2 Product visualization

- 8.8.2.3 Customization & personalization

- 8.8.2.4 AR-based shopping experiences

- 8.8.2.5 Others

- 8.9 GOVERNMENT

- 8.9.1 ABILITY TO CREATE DETAILED TOPOGRAPHIC MAPS AND MODELING STRUCTURES TO DRIVE DEMAND

- TABLE 97 GOVERNMENT: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 98 GOVERNMENT: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.9.2 GOVERNMENT: 3D IMAGING APPLICATIONS

- 8.9.2.1 Urban planning & development

- 8.9.2.2 Environmental analysis

- 8.9.2.3 Disaster management

- 8.9.2.4 Archaeology & cultural preservation

- 8.9.2.5 Others

- 8.10 ENERGY & UTILITIES

- 8.10.1 RISING NEED TO EXTRACT RESOURCES BY CREATING DETAILED VISUALIZATIONS OF GEOLOGICAL FORMATIONS TO DRIVE MARKET

- TABLE 99 ENERGY & UTILITIES: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 100 ENERGY & UTILITIES: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.10.2 ENERGY & UTILITIES: 3D IMAGING APPLICATIONS

- 8.10.2.1 Pipeline integrity assessments

- 8.10.2.2 Renewable energy site planning

- 8.10.2.3 Oil and gas exploration

- 8.10.2.4 Asset mapping & management

- 8.10.2.5 Others

- 8.11 OTHER VERTICALS

- TABLE 101 OTHER VERTICALS: 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 102 OTHER VERTICALS: 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

9 3D IMAGING MARKET, BY REGION

- 9.1 INTRODUCTION

- FIGURE 43 ASIA PACIFIC TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 44 INDIA TO ACHIEVE HIGHEST GROWTH DURING FORECAST PERIOD

- TABLE 103 3D IMAGING MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 104 3D IMAGING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: 3D IMAGING MARKET DRIVERS

- 9.2.2 NORTH AMERICA: RECESSION IMPACT ANALYSIS

- FIGURE 45 NORTH AMERICAN 3D IMAGING MARKET SNAPSHOT

- TABLE 105 NORTH AMERICA: 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 106 NORTH AMERICA: 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 107 NORTH AMERICA: 3D IMAGING MARKET, BY HARDWARE, 2018-2022 (USD MILLION)

- TABLE 108 NORTH AMERICA: 3D IMAGING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 109 NORTH AMERICA: 3D IMAGING MARKET, BY SOFTWARE, 2018-2022 (USD MILLION)

- TABLE 110 NORTH AMERICA: 3D IMAGING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 111 NORTH AMERICA: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 112 NORTH AMERICA: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2028 (USD MILLION)

- TABLE 113 NORTH AMERICA: 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 114 NORTH AMERICA: 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- TABLE 115 NORTH AMERICA: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2018-2022 (USD MILLION)

- TABLE 116 NORTH AMERICA: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2023-2028 (USD MILLION)

- TABLE 117 NORTH AMERICA: 3D IMAGING MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 118 NORTH AMERICA: 3D IMAGING MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 119 NORTH AMERICA: 3D IMAGING MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 120 NORTH AMERICA: 3D IMAGING MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 121 NORTH AMERICA: 3D IMAGING MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 122 NORTH AMERICA: 3D IMAGING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.2.3 US

- 9.2.3.1 Rise of 3D printing technologies to rely on 3D imaging for creating digital models

- TABLE 123 US: 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 124 US: 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 125 US: 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 126 US: 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- 9.2.4 CANADA

- 9.2.4.1 Emphasis on research and development to drive growth

- 9.3 EUROPE

- 9.3.1 EUROPE: 3D IMAGING MARKET DRIVERS

- 9.3.2 EUROPE: RECESSION IMPACT ANALYSIS

- TABLE 127 EUROPE: 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 128 EUROPE: 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 129 EUROPE: 3D IMAGING MARKET, BY HARDWARE, 2018-2022 (USD MILLION)

- TABLE 130 EUROPE: 3D IMAGING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 131 EUROPE: 3D IMAGING MARKET, BY SOFTWARE, 2018-2022 (USD MILLION)

- TABLE 132 EUROPE: 3D IMAGING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 133 EUROPE: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 134 EUROPE: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2028 (USD MILLION)

- TABLE 135 EUROPE: 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 136 EUROPE: 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- TABLE 137 EUROPE: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2018-2022 (USD MILLION)

- TABLE 138 EUROPE: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2023-2028 (USD MILLION)

- TABLE 139 EUROPE: 3D IMAGING MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 140 EUROPE: 3D IMAGING MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 141 EUROPE: 3D IMAGING MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 142 EUROPE: 3D IMAGING MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 143 EUROPE: 3D IMAGING MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 144 EUROPE: 3D IMAGING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.3.3 UK

- 9.3.3.1 Demand for precise medical imaging techniques to propel growth

- TABLE 145 UK: 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 146 UK: 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 147 UK: 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 148 UK: 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- 9.3.4 GERMANY

- 9.3.4.1 Growing demand for immersive experiences in gaming, entertainment, and virtual experiences to fuel market

- 9.3.5 FRANCE

- 9.3.5.1 Robust growth in entertainment and gaming industries to drive market

- 9.3.6 ITALY

- 9.3.6.1 Need for preserving historical artifacts, artworks, and monuments to drive adoption of 3D imaging solutions

- 9.3.7 SPAIN

- 9.3.7.1 Strong demand for advanced geospatial solutions to drive growth

- 9.3.8 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: 3D IMAGING MARKET DRIVERS

- 9.4.2 ASIA PACIFIC: RECESSION IMPACT ANALYSIS

- FIGURE 46 ASIA PACIFIC 3D IMAGING MARKET SNAPSHOT

- TABLE 149 ASIA PACIFIC: 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 150 ASIA PACIFIC: 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 151 ASIA PACIFIC: 3D IMAGING MARKET, BY HARDWARE, 2018-2022 (USD MILLION)

- TABLE 152 ASIA PACIFIC: 3D IMAGING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 153 ASIA PACIFIC: 3D IMAGING MARKET, BY SOFTWARE, 2018-2022 (USD MILLION)

- TABLE 154 ASIA PACIFIC: 3D IMAGING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 155 ASIA PACIFIC: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 156 ASIA PACIFIC: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2028 (USD MILLION)

- TABLE 157 ASIA PACIFIC: 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 158 ASIA PACIFIC: 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- TABLE 159 ASIA PACIFIC: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2018-2022 (USD MILLION)

- TABLE 160 ASIA PACIFIC: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2023-2028 (USD MILLION)

- TABLE 161 ASIA PACIFIC: 3D IMAGING MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 162 ASIA PACIFIC: 3D IMAGING MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 163 ASIA PACIFIC: 3D IMAGING MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 164 ASIA PACIFIC: 3D IMAGING MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 165 ASIA PACIFIC: 3D IMAGING MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 166 ASIA PACIFIC: 3D IMAGING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.4.3 CHINA

- 9.4.3.1 Rising demand for cutting-edge imaging technologies to fuel growth

- TABLE 167 CHINA: 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 168 CHINA: 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 169 CHINA: 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 170 CHINA: 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- 9.4.4 JAPAN

- 9.4.4.1 Growing demand for comprehensive metaverse experience to boost demand for 3D imaging software

- 9.4.5 INDIA

- 9.4.5.1 Growing initiatives taken by government to support digital innovation to propel growth

- 9.4.6 ANZ

- 9.4.6.1 Rapid adoption of 3D technologies for high-fidelity imaging, intricate modeling, and immersive environment to drive growth

- 9.4.7 SOUTH KOREA

- 9.4.7.1 Rising need to broaden global access to diagnostics to drive market growth

- 9.4.8 REST OF ASIA PACIFIC

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 MIDDLE EAST & AFRICA: 3D IMAGING MARKET DRIVERS

- 9.5.2 MIDDLE EAST & AFRICA: RECESSION IMPACT ANALYSIS

- TABLE 171 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 172 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 173 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY HARDWARE, 2018-2022 (USD MILLION)

- TABLE 174 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 175 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY SOFTWARE, 2018-2022 (USD MILLION)

- TABLE 176 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 177 MIDDLE EAST & AFRICA: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 178 MIDDLE EAST & AFRICA: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2028 (USD MILLION)

- TABLE 179 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 180 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- TABLE 181 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2018-2022 (USD MILLION)

- TABLE 182 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2023-2028 (USD MILLION)

- TABLE 183 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 184 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 185 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 186 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 187 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 188 MIDDLE EAST & AFRICA: 3D IMAGING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.5.3 SAUDI ARABIA

- 9.5.3.1 Need to embrace innovation and 3D imaging for enhanced diagnosis and treatment to propel demand

- 9.5.4 UAE

- 9.5.4.1 Ability to restore and preserve cultural heritage to drive adoption of 3D imaging solutions

- 9.5.5 SOUTH AFRICA

- 9.5.5.1 Increasing investments by businesses to adopt cutting-edge technologies to encourage market expansion

- 9.5.6 TURKEY

- 9.5.6.1 Need for revolutionizing production processes and enabling rapid prototyping to support market growth

- 9.5.7 REST OF MIDDLE EAST & AFRICA

- 9.6 LATIN AMERICA

- 9.6.1 LATIN AMERICA: 3D IMAGING MARKET DRIVERS

- 9.6.2 LATIN AMERICA: RECESSION IMPACT ANALYSIS

- TABLE 189 LATIN AMERICA: 3D IMAGING MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 190 LATIN AMERICA: 3D IMAGING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 191 LATIN AMERICA: 3D IMAGING MARKET, BY HARDWARE, 2018-2022 (USD MILLION)

- TABLE 192 LATIN AMERICA: 3D IMAGING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 193 LATIN AMERICA: 3D IMAGING MARKET, BY SOFTWARE, 2018-2022 (USD MILLION)

- TABLE 194 LATIN AMERICA: 3D IMAGING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 195 LATIN AMERICA: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 196 LATIN AMERICA: 3D IMAGING SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2028 (USD MILLION)

- TABLE 197 LATIN AMERICA: 3D IMAGING MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 198 LATIN AMERICA: 3D IMAGING MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- TABLE 199 LATIN AMERICA: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2018-2022 (USD MILLION)

- TABLE 200 LATIN AMERICA: 3D IMAGING MARKET, BY PROFESSIONAL SERVICE, 2023-2028 (USD MILLION)

- TABLE 201 LATIN AMERICA: 3D IMAGING MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 202 LATIN AMERICA: 3D IMAGING MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 203 LATIN AMERICA: 3D IMAGING MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 204 LATIN AMERICA: 3D IMAGING MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 205 LATIN AMERICA: 3D IMAGING MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 206 LATIN AMERICA: 3D IMAGING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.6.3 BRAZIL

- 9.6.3.1 Strategic technological integration to propel Brazil's 3D imaging market expansion across industries

- 9.6.4 MEXICO

- 9.6.4.1 Leveraging cutting-edge technologies and integrating 3D technologies to boost growth

- 9.6.5 ARGENTINA

- 9.6.5.1 Rising demand for integrating 3D imaging to spur technological growth across sectors

- 9.6.6 REST OF LATIN AMERICA

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES

- TABLE 207 OVERVIEW OF STRATEGIES ADOPTED BY KEY 3D IMAGING VENDORS

- 10.3 REVENUE ANALYSIS

- FIGURE 47 REVENUE ANALYSIS FOR KEY PLAYERS, 2018-2022 (USD BILLION)

- 10.4 MARKET SHARE ANALYSIS

- FIGURE 48 MARKET SHARE ANALYSIS, 2022

- TABLE 208 3D IMAGING MARKET: INTENSITY OF COMPETITIVE RIVALRY

- 10.5 BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 49 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 10.6 COMPANY EVALUATION MATRIX

- 10.6.1 STARS

- 10.6.2 EMERGING LEADERS

- 10.6.3 PERVASIVE PLAYERS

- 10.6.4 PARTICIPANTS

- FIGURE 50 COMPANY EVALUATION MATRIX, 2022

- 10.6.5 COMPANY FOOTPRINT

- TABLE 209 COMPONENT FOOTPRINT (17 COMPANIES)

- TABLE 210 VERTICAL FOOTPRINT (17 COMPANIES)

- TABLE 211 REGIONAL FOOTPRINT (17 COMPANIES)

- TABLE 212 COMPANY FOOTPRINT (17 COMPANIES)

- 10.7 STARTUP/SME EVALUATION MATRIX

- 10.7.1 PROGRESSIVE COMPANIES

- 10.7.2 RESPONSIVE COMPANIES

- 10.7.3 DYNAMIC COMPANIES

- 10.7.4 STARTING BLOCKS

- FIGURE 51 STARTUP/SME EVALUATION MATRIX, 2022

- 10.7.5 COMPETITIVE BENCHMARKING

- TABLE 213 3D IMAGING MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 214 3D IMAGING MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2022

- 10.8 COMPETITIVE SCENARIO AND TRENDS

- 10.8.1 PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 215 3D IMAGING MARKET: PRODUCT LAUNCHES & ENHANCEMENTS, JULY 2019-NOVEMBER 2023

- 10.8.2 DEALS

- TABLE 216 3D IMAGING MARKET: DEALS, JANUARY 2019-NOVEMBER 2023

- 10.9 VALUATION AND FINANCIAL METRICS OF KEY VENDORS

- FIGURE 52 VALUATION AND FINANCIAL METRICS OF KEY VENDORS

- FIGURE 53 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

11 COMPANY PROFILES

- (Business overview, Products/Solutions/Services offered, Recent Developments, MnM view, Right to win, Strategic choices made, Weaknesses and competitive threats) **

- 11.1 INTRODUCTION

- 11.2 KEY PLAYERS

- 11.2.1 GE HEALTHCARE

- TABLE 217 GE HEALTHCARE: BUSINESS OVERVIEW

- FIGURE 54 GE HEALTHCARE: COMPANY SNAPSHOT

- TABLE 218 GE HEALTHCARE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 219 GE HEALTHCARE: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 220 GE HEALTHCARE: DEALS

- TABLE 221 GE HEALTHCARE: OTHERS

- 11.2.2 AUTODESK

- TABLE 222 AUTODESK: BUSINESS OVERVIEW

- FIGURE 55 AUTODESK: COMPANY SNAPSHOT

- TABLE 223 AUTODESK: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 224 AUTODESK: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 225 AUTODESK: DEALS

- 11.2.3 STMICROELECTRONICS

- TABLE 226 STMICROELECTRONICS: BUSINESS OVERVIEW

- FIGURE 56 STMICROELECTRONICS: COMPANY SNAPSHOT

- TABLE 227 STMICROELECTRONICS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 228 STMICROELECTRONICS: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 229 STMICROELECTRONICS: DEALS

- 11.2.4 PANASONIC

- TABLE 230 PANASONIC: BUSINESS OVERVIEW

- FIGURE 57 PANASONIC: COMPANY SNAPSHOT

- TABLE 231 PANASONIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 232 PANASONIC: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 233 PANASONIC: DEALS

- 11.2.5 SONY

- TABLE 234 SONY: BUSINESS OVERVIEW

- FIGURE 58 SONY: COMPANY SNAPSHOT

- TABLE 235 SONY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 236 SONY: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 237 SONY: DEALS

- 11.2.6 TRIMBLE

- TABLE 238 TRIMBLE: BUSINESS OVERVIEW

- FIGURE 59 TRIMBLE: COMPANY SNAPSHOT

- TABLE 239 TRIMBLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 240 TRIMBLE: PRODUCT LAUNCHES & ENHANCEMENTS

- 11.2.7 FARO

- TABLE 241 FARO: BUSINESS OVERVIEW

- FIGURE 60 FARO: COMPANY SNAPSHOT

- TABLE 242 FARO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 243 FARO: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 244 FARO: DEALS

- 11.2.8 PHILIPS

- TABLE 245 PHILIPS: BUSINESS OVERVIEW

- FIGURE 61 PHILIPS: COMPANY SNAPSHOT

- TABLE 246 PHILIPS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 247 PHILIPS: PRODUCT LAUNCHES & ENHANCEMENTS

- 11.2.9 GOOGLE

- TABLE 248 GOOGLE: BUSINESS OVERVIEW

- FIGURE 62 GOOGLE: COMPANY SNAPSHOT

- TABLE 249 GOOGLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 250 GOOGLE: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 251 GOOGLE: DEALS

- 11.2.10 ADOBE

- TABLE 252 ADOBE: BUSINESS OVERVIEW

- FIGURE 63 ADOBE: COMPANY SNAPSHOT

- TABLE 253 ADOBE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 254 ADOBE: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 255 ADOBE: DEALS

- 11.2.11 HP

- TABLE 256 HP: BUSINESS OVERVIEW

- FIGURE 64 HP: COMPANY SNAPSHOT

- TABLE 257 HP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 258 HP: DEALS

- 11.2.12 DASSAULT SYSTEMES

- TABLE 259 DASSAULT SYSTEMES: BUSINESS OVERVIEW

- FIGURE 65 DASSAULT SYSTEMES: COMPANY SNAPSHOT

- TABLE 260 DASSAULT SYSTEMES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 261 DASSAULT SYSTEMES: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 262 DASSAULT SYSTEMES: DEALS

- 11.2.13 BENTLEY SYSTEMS

- TABLE 263 BENTLEY SYSTEMS: COMPANY OVERVIEW

- FIGURE 66 BENTLEY SYSTEMS: COMPANY SNAPSHOT

- TABLE 264 BENTLEY SYSTEMS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 265 BENTLEY SYSTEMS: PRODUCT LAUNCHES & ENHANCEMENTS

- TABLE 266 BENTLEY SYSTEMS: DEALS

- *Details on Business overview, Products/Solutions/Services offered, Recent Developments, MnM view, Right to win, Strategic choices made, Weaknesses and competitive threats might not be captured in case of unlisted companies.

- 11.3 OTHER KEY PLAYERS

- 11.3.1 LOCKHEED MARTIN

- 11.3.2 ESRI

- 11.3.3 TOPCON

- 11.3.4 ABLE SOFTWARE

- 11.4 STARTUPS/SMES

- 11.4.1 MAXON

- 11.4.2 ESRI

- 11.4.3 ARCHILOGIC

- 11.4.4 PIX4D

- 11.4.5 BRAINKEY

- 11.4.6 PRECISMO

- 11.4.7 KAARTA

- 11.4.8 LIGTHCODE PHOTONICS

- 11.4.9 VZENSE TECHNOLOGY

- 11.4.10 CAPOOM

- 11.4.11 ATOMONTAGE

- 11.4.12 HIVEMAPPER

- 11.4.13 SHAPR3D

- 11.4.14 INNERSIGHT

12 ADJACENT & RELATED MARKETS

- 12.1 INTRODUCTION

- 12.2 3D MAPPING AND MODELING MARKET

- 12.2.1 MARKET DEFINITION

- 12.2.2 MARKET OVERVIEW

- 12.2.2.1 3D mapping and modeling market, by offering

- TABLE 267 3D MAPPING AND MODELING MARKET, BY OFFERING, 2017-2022 (USD MILLION)

- TABLE 268 3D MAPPING AND MODELING MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- 12.2.2.2 3D mapping and modeling market, by deployment mode

- TABLE 269 3D MAPPING AND MODELING MARKET, BY DEPLOYMENT MODE, 2017-2022 (USD MILLION)

- TABLE 270 3D MAPPING AND MODELING MARKET, BY DEPLOYMENT MODE, 2023-2028 (USD MILLION)

- 12.2.2.3 3D mapping and modeling market, by technology

- TABLE 271 3D MAPPING AND MODELING MARKET, BY TECHNOLOGY, 2017-2022 (USD MILLION)

- TABLE 272 3D MAPPING AND MODELING MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 12.2.2.4 3D mapping and modeling market, by vertical

- TABLE 273 3D MAPPING AND MODELING MARKET, BY VERTICAL, 2017-2022 (USD MILLION)

- TABLE 274 3D MAPPING AND MODELING MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 12.2.2.5 3D mapping and modeling market, by region

- TABLE 275 3D MAPPING AND MODELING MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 276 3D MAPPING AND MODELING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.3 3D ANIMATION MARKET

- 12.3.1 MARKET DEFINITION

- 12.3.2 MARKET OVERVIEW

- 12.3.2.1 3D animation market, by component

- TABLE 277 3D ANIMATION MARKET, BY COMPONENT, 2015-2022 (USD MILLION)

- 12.3.2.2 3D animation market, by technology

- TABLE 278 3D ANIMATION MARKET, BY TECHNOLOGY, 2015-2022 (USD MILLION)

- 12.3.2.3 3D animation market, by vertical

- TABLE 279 3D ANIMATION MARKET, BY VERTICAL, 2015-2022 (USD MILLION)

- 12.3.2.4 3D animation market, by region

- TABLE 280 3D ANIMATION MARKET, BY REGION, 2015-2022 (USD MILLION)

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS