|

|

市場調査レポート

商品コード

1397375

自動車用塗料の世界市場:塗料タイプ別、技術別、樹脂タイプ別、質感別、含有量別、塗装機器技術別、車両タイプ別、地域別-2028年までの予測Automotive Paints Market by Type (E-coat, Primer, Basecoat, Clearcoat), Resin (PU, Epoxy, Acrylic), Technology (Solvent, Water, Powder), Paint Equipment (Airless, Electrostatic), Texture, Content, ICE & EVs, Refinish and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用塗料の世界市場:塗料タイプ別、技術別、樹脂タイプ別、質感別、含有量別、塗装機器技術別、車両タイプ別、地域別-2028年までの予測 |

|

出版日: 2023年12月12日

発行: MarketsandMarkets

ページ情報: 英文 307 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

| 調査範囲 | |

|---|---|

| 調査対象年 | 2023年~2028年 |

| 基準年 | 2022年 |

| 予測期間 | 2023年~2028年 |

| 検討単位 | 金額(100万米ドル/10億米ドル) |

| セグメント別 | 塗料タイプ別、技術別、樹脂タイプ別、テクスチャー別、含有量別、塗装機器技術別、車両タイプ別、地域別 |

| 対象地域 | アジア太平洋地域、北米、欧州、その他の地域 |

自動車用塗料の市場規模は2023年に84億米ドルと予測され、3.2%のCAGRで拡大し、2028年には99億米ドルに達すると予測されています。

自動車用塗料は電気自動車やSUVの販売増が原動力であり、水系塗料技術は環境規制が原動力です。また、再仕上げ塗料では組織化された参入企業が拡大しています。しかし、自動車の安全性に関する自動車産業の進歩により、事故件数が減少し、それが自動車用再塗装塗料市場の抑制要因となっています。

水系塗料は水性であるため、従来の溶剤系塗料に比べて環境への害が大幅に少なく、スモッグやその他の環境問題の原因となる有害な大気汚染物質である揮発性有機化合物(VOC)の排出量もはるかに少なくなっています。環境規制が厳しくなり、自動車業界が持続可能性を追求するにつれて、水性塗料の魅力はますます高まっています。

当レポートでは、世界の自動車用塗料市場について調査し、塗料タイプ別、技術別、樹脂タイプ別、質感別、含有量別、塗装機器技術別、車両タイプ別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 顧客のビジネスに影響を与える動向と混乱

- 技術分析

- ケーススタディ

- 世界の自動車の色の人気

- 特許分析

- 貿易分析

- サプライチェーン分析

- 生態系マッピング

- 価格分析

- 関税と規制状況

- 主要な利害関係者と購入基準

- 2023年~2024年の主要な会議とイベント

第6章 自動車塗料市場、塗料タイプ別

- イントロダクション

- エレクトロコート

- プライマー

- ベースコート

- クリアコート

第7章 自動車用塗料市場、技術別

- イントロダクション

- 溶剤系

- 水性

- パウダーコーティング

第8章 自動車用塗料市場、樹脂タイプ別

- イントロダクション

- ポリウレタン

- エポキシ

- アクリル

- その他

第9章 自動車用塗料市場、質感別

- イントロダクション

- ソリッド

- メタリック

- マット仕上げ

- パールの香り

- 太陽光反射

第10章 自動車用塗料市場、含有量別

- イントロダクション

- 電着塗装、含有量別

- 溶剤系塗料、含有量別

- 水性塗料、含有量別

第11章 自動車用塗料市場、塗装設備技術別

- イントロダクション

- エアレススプレーガン

- 静電スプレーガン

第12章 自動車用塗料市場、車両タイプ別

- イントロダクション

- 乗用車

- 小型商用車(LCV)

- トラック

- バス

第13章 電気自動車およびハイブリッド自動車用塗料市場、車両タイプ別

- イントロダクション

- バッテリー電気自動車(BEV)

- 燃料電池電気自動車(FCEV)

- プラグインハイブリッド車(PHEV)

第14章 自動車用仕上げ塗料市場、樹脂タイプ別

- イントロダクション

- ポリウレタン

- エポキシ

- アクリル

- その他

第15章 自動車用塗料市場、地域別

- イントロダクション

- 北米

- アジア太平洋

- 欧州

- その他の地域

第16章 競合情勢

- 概要

- 市場シェア分析、2022年

- 収益分析、2020年と2022年

- 自動車用塗料市場:企業評価マトリックス、2022年

- 企業のフットプリント

- 自動車補修用塗料市場:企業評価マトリックス、2022年

- 企業のフットプリント

- 競合シナリオ

- 有力企業、2022-2023

第17章 企業プロファイル

- 主要参入企業

- PPG INDUSTRIES, INC.

- BASF SE

- AXALTA COATING SYSTEMS, LLC

- AKZO NOBEL N.V.

- THE SHERWIN-WILLIAMS COMPANY

- KANSAI PAINT CO., LTD.

- SOLVAY

- NIPPON PAINT HOLDINGS CO., LTD.

- COVESTRO AG

- CLARIANT

- その他の企業

- JOTUN

- SKSHU PAINT CO., LTD.

- KCC CORPORATION

- DONGLAI COATING TECHNOLOGY(SHANGHAI)CO., LTD.

- DUPONT

- STANDOX

- NEXA AUTOCOLOR

- 3M

- WACKER CHEMIE AG

- PPG ASIANPAINTS

第18章 提言

第19章 付録

Report Description

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By Paint type, By Technology type, By Resin type, By Texture type, By Electric & Hybrid Vehicle type, By Vehicle type, By Content type, By Resin Refinish Paint type, By Painting Equipment |

| Regions covered | Asia Pacific, North America, Europe, and Rest of the World. |

The automotive paints market is estimated to be USD 8.4 billion in 2023 and is projected to reach USD 9.9 billion by 2028, at a CAGR of 3.2%.

The automotive paint is driven by increase in sales of electric vehicles and SUVs while the water borne paint technologies is driven by the environmental regulations. Also, there is expansion of organized players in refinish paints. However, due to advancements in automotive industry regarding safety in vehicles which has resulted in the reduction of number of accidents, which in turn, has become a restraint in the automotive refinish paints market.

"The water borne technology is the fastest-growing segment in the automotive paints market."

Waterborne paints are water-based, making them significantly less harmful to the environment than traditional solvent-based paints. They emit far fewer volatile organic compounds (VOCs), which are harmful air pollutants that contribute to smog and other environmental problems. As environmental regulations become stricter and the automotive industry strives for sustainability, waterborne paints are becoming increasingly attractive.

Considering the automotive industry, water borne paint technology do not contain hazardous solvents which can pose health risks to workers, such as respiratory problems and skin irritation. This makes waterborne paints a more desirable choice for automotive manufacturers concerned about the health and safety of their employees. Key players of automotive paints manufacturer are manufacturing water borne paint technology for OEMs. For instance, PPG Industries LLC. Has invested USD 10 million to expand the automotive OEM coatings production in its site in Weingarten, Germany. The expansion will increase the facility's capacity to produce waterborne basecoats by more than 5,000 metric tons per year.

Hence, the tightening of environmental regulations and need for more sustainable solutions is driving the waterborne paints to the fastest growing technology in automotive painting.

"Basecoat segment is dominating the automotive paints market in paint type."

Basecoat serves as the foundation for the overall paint finish on a vehicle. It provides the primary color and establishes the underlying layer upon which the clearcoat, the final protective layer, is applied. Basecoat plays a crucial role in determining the vehicle's aesthetic appeal and ensuring consistent color tone across different panels and components. Also, it is available in a wide range of colors and finishes to cater to the diverse preferences and styles of vehicle owners.

Manufacturers offer basecoats in various shades, metallic effects, and pearlescent options, enabling them to create unique and eye-catching design. To stay ahead in the competition of automotive painting types, key players are investing heavily in developing new basecoat technology in paint types. For instance on August 2022, Axalta Coating Systems launched its next-generation basecoat technology, Cromax® Gen, specifically tailored for the automotive refinish market in Latin America. It was designed to enhance productivity, optimize costs, and elevate color accuracy for body shops across the region. Hence in general, basecoat is the most widely used paint type on automotives, and it typically accounts for about 60% of the total paint used, so holds the largest market share in automotive paints type.

"North America is the second fastest growing market."

North America has major key players of the world's largest automakers, including General Motors, Ford, and Chrysler. These manufacturers are constantly ramping up production to meet the growing demand for vehicles, fueling the consumption of automotive paints. According to International Organization of Motor Vehicle Manufacturers (OICA) in 2022, US produced over 9.2 million vehicles, accounting for a significant portion of global automotive production. This robust production is expected to continue in the coming years, driving the demand for automotive paints in North America.

The increasing number of vehicles on North American roads is also creating a surge in the demand for refinish paints. As vehicles age, they require refinishing to maintain their appearance, protect them from wear and tear, and enhance their resale value. In Canada, a study by the Automotive Industries Association of Canada revealed that over 20 million vehicles were in operation in 2022. This vast fleet of vehicles requires regular maintenance and refinishing, creating opportunities for refinish paints in the country.

Also, North America has implemented various VOC regulations to curb air pollution and its detrimental effects on public health. These regulations have significantly impacted the automotive paint industry, prompting manufacturers to develop innovative solutions to comply with the stringent standards. For instance, California's Air Resources Board (CARB) has a ban on solvent-based automotive paints for passenger cars, which means that all automotive paints used on passenger cars in California must have a density of VOC solvent content up to 880 g/L or less and VOC content less than 2.5 g/L. Also the Northeast and Mid-Atlantic Ozon Transport Commission (OTC) has a VOC emission limit of 250 g/L for automotive paints used on passenger cars and light-duty trucks.

In response to these pressing concerns, automotive paint manufacturers have embraced various strategies to develop low-VOC paints and developing and using new products of waterborne paints for the vehicles. Hence these factors has made North America the second fastest growing region in automotive paints market.

The break-up of the profile of primary participants in the automotive paint market:

By Companies: Tier 1 - 60%, OEMs - 40%

By Designation: Directors- 10%, C-Level Executives - 70%, others - 20%

By Region: North America - 10%, APAC - 80% and MEA - 10%

Global players dominate the automotive paints market and comprise several regional players. The key players in the automotive paints market are PPG industries, Inc. (US), BASF SE (Germany), Axalta Coating Systems LLC (US), Akzo Nobel N.V. (Netherlands), and The Sherwin Williams Company (US), Kansai Paints Co,. Ltd (Japan), Solvay (Germany), Nippon Paint Holding Co., Ltd., (Japan) and Covestro AG (Germany)

Research Coverage:

The automotive paints market is segmented by Paint type (Electrocoat, Primer, Basecoat, Clearcoat), by Technology type (Solventborne, Waterborne, Powder coating), by Resin type (Polyurethane, Epoxy, Acrylic, Other Resins), by Texture type (Solid, Metallic, Pearlescent, Matte Finish, Solar Reflective Paints), by Content (Water, Petroleum-based solvents, Resins and Binders, Silicone Polymers, Pigments and Colorants, Other additives), by Painting equipment (Airless, Electrostatic),Refinish paints market by Resin type (Polyurethane, Epoxy, Acrylic, Other Resins), by Vehicle type (Passenger Car, LCV, HCV), by Electric & Hybrid vehicle type (BEV, FCEV, PHEV), by Region (Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific); Europe (Germany, Spain, Italy, France, Russia, UK, Europe, Rest of Europe); North America (Canada, Mexico, US); Row (Brazil, South Africa, Rest of RoW)).

The report's scope covers detailed information regarding the major factors, such as influencing factors for the growth of the automotive paints market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products, and services; key strategies; contracts, partnerships, agreements, new product & service launches, mergers and acquisitions, recession impact, and recent developments associated with the automotive paints market.

Key Benefits of Buying the Report:

The report will help the market leaders/new entrants in this market with the information on the closest approximations of the revenue numbers for the overall automotive paints market and the sub-segments. This report will help stakeholders understand the competitive landscape and gain insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Stringent emission regulations has forced key players to produce sustainable and low-VOC paints; Expansion of organized players in refinish paint market), restraints (Advancements in autonomous technologies reduce accidents, restricting refinish market), opportunities (Emergence of innovative paint technologies; Booming sales of SUVs), and challenges (Automotive paint wastage in developing country at OEM and refinish level; Rapidly changing consumer preferences; Decline in vehicle sales) influencing the growth of the automotive paints market.

- Product Development/Innovation: Detailed insights on upcoming technologies, and new product & service launches in the automotive paints market.

- Market Development: Comprehensive information about the markets - the report analyses the authentication and brand protection market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in automotive paints market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like PPG industries, Inc. (US), BASF SE (Germany), Axalta Coating Systems LLC (US), Akzo Nobel N.V. (Netherlands), and The Sherwin Williams Company (US), among others in automotive paints market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- TABLE 1 AUTOMOTIVE PAINTS MARKET DEFINITION, BY PAINT TYPE

- TABLE 2 AUTOMOTIVE PAINTS MARKET DEFINITION, BY TECHNOLOGY

- TABLE 3 AUTOMOTIVE PAINTS MARKET DEFINITION, BY RESIN TYPE

- TABLE 4 AUTOMOTIVE PAINTS MARKET DEFINITION, BY TEXTURE

- TABLE 5 AUTOMOTIVE PAINTS MARKET DEFINITION, BY CONTENT

- TABLE 6 AUTOMOTIVE PAINTS MARKET DEFINITION, BY PAINTING EQUIPMENT TECHNIQUE

- TABLE 7 AUTOMOTIVE PAINTS MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 8 ELECTRIC & HYBRID VEHICLE PAINTS MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 9 AUTOMOTIVE REFINISH PAINTS MARKET DEFINITION, BY RESIN TYPE

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- TABLE 10 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- FIGURE 1 AUTOMOTIVE PAINTS MARKET SEGMENTATION

- 1.3.1 REGIONS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 11 CURRENCY EXCHANGE RATES

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

- 1.7.1 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 RESEARCH DESIGN

- FIGURE 3 RESEARCH DESIGN MODEL

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS

- 2.1.2.1 Primary participants

- 2.1.3 SAMPLING TECHNIQUES AND DATA COLLECTION METHODS

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 5 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 6 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- FIGURE 7 DATA TRIANGULATION

- 2.4 FACTOR ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RECESSION IMPACT ANALYSIS

3 EXECUTIVE SUMMARY

- FIGURE 8 AUTOMOTIVE PAINTS MARKET OUTLOOK

- FIGURE 9 WATER-BORNE SEGMENT TO GROW RAPIDLY DURING FORECAST PERIOD

- FIGURE 10 POLYURETHANE TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 11 METALLIC TO SURPASS OTHER SEGMENTS DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE PAINTS MARKET

- FIGURE 12 INCREASE IN VEHICLE PRODUCTION TO DRIVE GROWTH

- 4.2 AUTOMOTIVE PAINTS MARKET, BY PAINT TYPE

- FIGURE 13 BASE COAT TO ACQUIRE MAXIMUM MARKET SHARE BY VALUE IN 2028

- 4.3 AUTOMOTIVE PAINTS MARKET, BY TECHNOLOGY

- FIGURE 14 SOLVENT-BORNE TO BE LARGEST SEGMENT BY VALUE DURING FORECAST PERIOD

- 4.4 AUTOMOTIVE PAINTS MARKET, BY RESIN TYPE

- FIGURE 15 POLYURETHANE TO HOLD LARGEST MARKET SHARE BY VALUE IN 2028

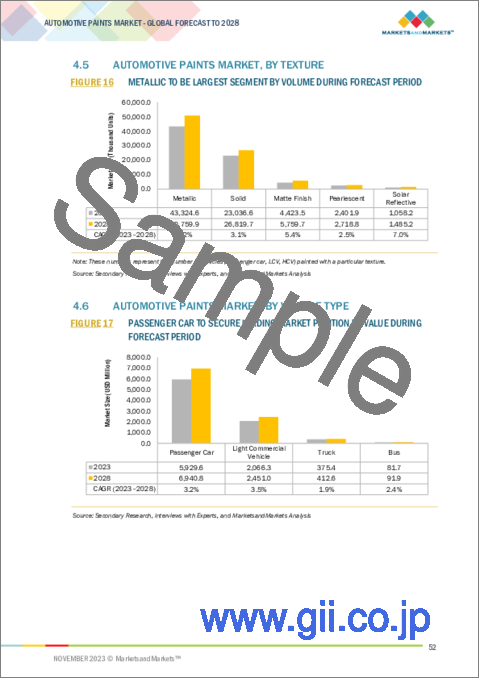

- 4.5 AUTOMOTIVE PAINTS MARKET, BY TEXTURE

- FIGURE 16 METALLIC TO BE LARGEST SEGMENT BY VOLUME DURING FORECAST PERIOD

- 4.6 AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE

- FIGURE 17 PASSENGER CAR TO SECURE LEADING MARKET POSITION BY VALUE DURING FORECAST PERIOD

- 4.7 AUTOMOTIVE PAINTS MARKET, BY CONTENT

- FIGURE 18 PIGMENT & COLORANT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- 4.8 ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY VEHICLE TYPE

- FIGURE 19 BEV TO SURPASS OTHER SEGMENTS BY VALUE DURING FORECAST PERIOD

- 4.9 AUTOMOTIVE PAINTS MARKET, BY REGION

- FIGURE 20 ASIA PACIFIC TO BE LARGEST MARKET DURING FORECAST PERIOD

- 4.10 AUTOMOTIVE REFINISH PAINTS MARKET, BY RESIN TYPE

- FIGURE 21 POLYURETHANE TO SECURE LEADING MARKET POSITION DURING FORECAST PERIOD

- 4.11 AUTOMOTIVE PAINTS EQUIPMENT MARKET, BY REGION

- FIGURE 22 ASIA PACIFIC TO BE LARGEST MARKET FOR ELECTROSTATIC SPRAY GUNS DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 23 AUTOMOTIVE PAINTS MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising production of sustainable automotive paints due to stringent emission regulations

- TABLE 12 VOC CONTENT LIMITS IN AUTOMOTIVE COATINGS

- 5.2.1.2 Expansion of established players in refinish paints market

- 5.2.2 RESTRAINTS

- 5.2.2.1 Reduced number of accidents and refinish jobs due to advancements in autonomous technologies

- TABLE 13 SAFETY FEATURES IMPOSED BY KEY COUNTRIES

- 5.2.3 OPPORTUNITY

- 5.2.3.1 Emergence of innovative paint technologies

- FIGURE 24 AUTOMOTIVE COAT PROCESS: CONVENTIONAL VS. ADVANCED

- 5.2.3.2 Growing popularity of SUVs

- FIGURE 25 GLOBAL SUV PRODUCTION DATA, 2018-2022

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of adequate waste management infrastructure in developing countries

- 5.2.4.2 Rapidly changing consumer preferences

- 5.2.4.3 Decline in vehicle sales

- 5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 26 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 TECHNOLOGY ANALYSIS

- 5.4.1 NANO-CERAMIC COATINGS

- 5.4.2 SMART PAINTS

- 5.4.3 SELF-CLEANING PAINTS

- 5.4.4 DRESS UP

- 5.4.5 SELF-HEALING WRAPS

- 5.4.6 PAINT ATOMIZERS

- 5.4.7 SMART AUTOMOTIVE PAINT BOOTHS

- 5.4.8 ANTIMICROBIAL COATINGS

- 5.4.9 IMPACT OF ELECTRIC VEHICLES ON AUTOMOTIVE PAINTS MARKET

- 5.5 CASE STUDIES

- 5.5.1 MITSUBISHI CHEMICAL GROUP

- 5.5.2 POPULAR PAINTS

- 5.5.3 TWIN CITY FAN

- 5.6 POPULARITY OF AUTOMOTIVE COLORS WORLDWIDE

- 5.6.1 POPULAR AUTOMOTIVE COLORS

- FIGURE 27 COLORS SOLD GLOBALLY

- FIGURE 28 COLORS WIDELY USED IN AUTOMOBILES (%)

- FIGURE 29 NORTH AMERICA: COLOR PREFERENCES, BY VEHICLE TYPE

- FIGURE 30 EUROPE: COLOR PREFERENCES, BY VEHICLE TYPE

- 5.6.2 VEHICLE DEPRECIATION VALUE BASED ON COLORS

- TABLE 14 VEHICLE DEPRECIATION VALUE BASED ON COLORS

- 5.6.3 NEW COLOR TRENDS BY AUTOMAKERS

- TABLE 15 NEW VEHICLE COLOR TRENDS BY AUTOMAKERS

- 5.7 PATENT ANALYSIS

- TABLE 16 INNOVATIONS AND PATENTS, 2020-2023

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT DATA

- TABLE 17 US: IMPORT, BY COUNTRY (%)

- TABLE 18 CHINA: IMPORT, BY COUNTRY (%)

- TABLE 19 GERMANY: IMPORT, BY COUNTRY (%)

- TABLE 20 BELGIUM: IMPORT, BY COUNTRY (%)

- TABLE 21 NETHERLANDS: IMPORT, BY COUNTRY (%)

- TABLE 22 CANADA: IMPORT, BY COUNTRY (%)

- 5.8.2 EXPORT DATA

- TABLE 23 GERMANY: EXPORT, BY COUNTRY (%)

- TABLE 24 JAPAN: EXPORT, BY COUNTRY (%)

- TABLE 25 US: EXPORT, BY COUNTRY (%)

- TABLE 26 BELGIUM: EXPORT, BY COUNTRY (%)

- TABLE 27 NETHERLANDS: EXPORT, BY COUNTRY (%)

- 5.9 SUPPLY CHAIN ANALYSIS

- FIGURE 31 SUPPLY CHAIN ANALYSIS

- TABLE 28 ROLE OF COMPANIES IN SUPPLY CHAIN

- 5.10 ECOSYSTEM MAPPING

- FIGURE 32 ECOSYSTEM MAPPING

- 5.11 PRICING ANALYSIS

- TABLE 29 AVERAGE SELLING PRICE TREND OF AUTOMOTIVE PAINTS, BY VEHICLE TYPE, 2022 (USD)

- TABLE 30 AVERAGE SELLING PRICE TREND OF AUTOMOTIVE PAINTS, BY REGION, 2022 (USD)

- 5.12 TARIFF AND REGULATORY LANDSCAPE

- 5.12.1 TARIFF RELATED TO AUTOMOTIVE PAINTS

- TABLE 31 TARIFF RELATED TO AUTOMOTIVE PAINTS

- 5.12.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 32 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 STAKEHOLDERS IN BUYING PROCESS

- TABLE 33 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR AUTOMOTIVE PAINTS

- 5.13.2 KEY BUYING CRITERIA

- FIGURE 33 KEY BUYING CRITERIA FOR AUTOMOTIVE PAINTS

- TABLE 34 KEY BUYING CRITERIA FOR AUTOMOTIVE PAINTS

- 5.14 KEY CONFERENCES AND EVENTS, 2023-2024

- TABLE 35 KEY CONFERENCES AND EVENTS, 2023-2024

6 AUTOMOTIVE PAINTS MARKET, BY PAINT TYPE

- 6.1 INTRODUCTION

- 6.1.1 INDUSTRY INSIGHTS

- FIGURE 34 AVERAGE THICKNESS OF AUTOMOTIVE PAINTS, BY LAYER (µM)

- FIGURE 35 AUTOMOTIVE REFINISH PAINT SINGLE STAGING PROCESS, BY LAYER (µM)

- FIGURE 36 AUTOMOTIVE PAINTS MARKET, BY PAINT TYPE, 2023-2028 (USD MILLION)

- TABLE 36 AUTOMOTIVE PAINTS MARKET, BY PAINT TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 37 AUTOMOTIVE PAINTS MARKET, BY PAINT TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 38 AUTOMOTIVE PAINTS MARKET, BY PAINT TYPE, 2019-2022 (USD MILLION)

- TABLE 39 AUTOMOTIVE PAINTS MARKET, BY PAINT TYPE, 2023-2028 (USD MILLION)

- 6.2 ELECTROCOAT

- 6.2.1 FOCUS ON REDUCING VOC EMISSIONS TO DRIVE GROWTH

- TABLE 40 ELECTROCOAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 41 ELECTROCOAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 42 ELECTROCOAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 43 ELECTROCOAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3 PRIMER

- 6.3.1 SHIFT TOWARD WATER-BORNE FORMULATIONS TO DRIVE GROWTH

- TABLE 44 PRIMER: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 45 PRIMER: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 46 PRIMER: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 47 PRIMER: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4 BASE COAT

- 6.4.1 UPCOMING INNOVATIVE TECHNOLOGIES TO DRIVE GROWTH

- TABLE 48 VEHICLES WITH SPECIAL EFFECT FINISHES

- TABLE 49 BASE COAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 50 BASE COAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 51 BASE COAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 52 BASE COAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.5 CLEAR COAT

- 6.5.1 INCREASING USE OF LIGHTWEIGHT MATERIALS TO DRIVE GROWTH

- TABLE 53 CLEAR COAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 54 CLEAR COAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 55 CLEAR COAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 56 CLEAR COAT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

7 AUTOMOTIVE PAINTS MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- TABLE 57 COMPARISON BETWEEN AUTOMOTIVE PAINT TECHNOLOGIES

- 7.1.1 INDUSTRY INSIGHTS

- FIGURE 37 AUTOMOTIVE PAINTS MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 58 AUTOMOTIVE PAINTS MARKET, BY TECHNOLOGY, 2019-2022 (THOUSAND GALLONS)

- TABLE 59 AUTOMOTIVE PAINTS MARKET, BY TECHNOLOGY, 2023-2028 (THOUSAND GALLONS)

- TABLE 60 AUTOMOTIVE PAINTS MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 61 AUTOMOTIVE PAINTS MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 7.2 SOLVENT-BORNE

- 7.2.1 AVAILABILITY OF DIVERSE COLORS AND FINISHES TO DRIVE GROWTH

- TABLE 62 SOLVENT-BORNE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 63 SOLVENT-BORNE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 64 SOLVENT-BORNE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 65 SOLVENT-BORNE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.3 WATER-BORNE

- 7.3.1 RISE IN ENVIRONMENTAL CONCERNS TO DRIVE GROWTH

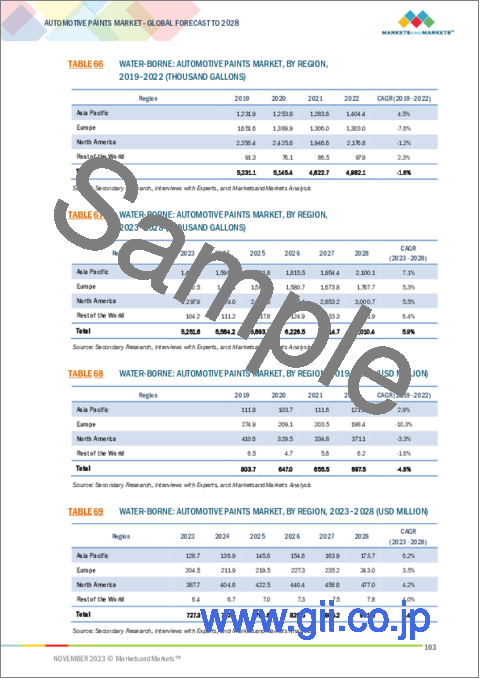

- TABLE 66 WATER-BORNE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 67 WATER-BORNE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 68 WATER-BORNE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 69 WATER-BORNE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.4 POWDER COATING

- 7.4.1 COST-EFFECTIVENESS AND LESS MAINTENANCE REQUIREMENTS TO DRIVE GROWTH

- TABLE 70 POWDER COATING: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 71 POWDER COATING: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 72 POWDER COATING: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 73 POWDER COATING: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

8 AUTOMOTIVE PAINTS MARKET, BY RESIN TYPE

- 8.1 INTRODUCTION

- FIGURE 38 AUTOMOTIVE PAINTS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- TABLE 74 AUTOMOTIVE PAINTS MARKET, BY RESIN TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 75 AUTOMOTIVE PAINTS MARKET, BY RESIN TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 76 AUTOMOTIVE PAINTS MARKET, BY RESIN TYPE, 2019-2022 (USD MILLION)

- TABLE 77 AUTOMOTIVE PAINTS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- 8.2 POLYURETHANE

- 8.2.1 DURABILITY AND CORROSION RESISTANCE PROPERTIES TO DRIVE GROWTH

- TABLE 78 POLYURETHANE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 79 POLYURETHANE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 80 POLYURETHANE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 81 POLYURETHANE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.3 EPOXY

- 8.3.1 EXTENSIVE USE IN VEHICLE REFINISHING TO DRIVE GROWTH

- TABLE 82 EPOXY: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 83 EPOXY: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 84 EPOXY: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 85 EPOXY: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.4 ACRYLIC

- 8.4.1 INCREASING DEMAND FOR WATER-BORNE COATINGS TO DRIVE GROWTH

- TABLE 86 ACRYLIC: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 87 ACRYLIC: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 88 ACRYLIC: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 89 ACRYLIC: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.5 OTHER RESINS

- TABLE 90 OTHER RESINS: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 91 OTHER RESINS: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 92 OTHER RESINS: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 93 OTHER RESINS: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

9 AUTOMOTIVE PAINTS MARKET, BY TEXTURE

- 9.1 INTRODUCTION

- 9.1.1 INDUSTRY INSIGHTS

- FIGURE 39 AUTOMOTIVE PAINTS MARKET, BY TEXTURE, 2023-2028 (THOUSAND UNITS)

- TABLE 94 AUTOMOTIVE PAINTS MARKET, BY TEXTURE, 2019-2022 (THOUSAND UNITS)

- TABLE 95 AUTOMOTIVE PAINTS MARKET, BY TEXTURE, 2023-2028 (THOUSAND UNITS)

- 9.2 SOLID

- 9.2.1 DEVELOPMENT OF NEW PIGMENT TECHNOLOGIES TO DRIVE GROWTH

- TABLE 96 VEHICLES WITH SOLID TEXTURE, 2023

- TABLE 97 SOLID: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND UNITS)

- TABLE 98 SOLID: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND UNITS)

- 9.3 METALLIC

- 9.3.1 RISING PREMIUM CAR SALES TO DRIVE GROWTH

- TABLE 99 VEHICLES WITH METALLIC TEXTURE, 2023

- TABLE 100 METALLIC: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND UNITS)

- TABLE 101 METALLIC: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND UNITS)

- 9.4 MATTE FINISH

- 9.4.1 CONSUMER PREFERENCE FOR LIMITED-EDITION VEHICLES TO DRIVE GROWTH

- TABLE 102 VEHICLES WITH MATTE FINISH TEXTURE, 2023

- TABLE 103 MATTE FINISH: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND UNITS)

- TABLE 104 MATTE FINISH: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND UNITS)

- 9.5 PEARLESCENT

- 9.5.1 PERSONALIZATION TREND IN HIGH-PERFORMANCE VEHICLES TO DRIVE GROWTH

- TABLE 105 PEARLESCENT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND UNITS)

- TABLE 106 PEARLESCENT: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND UNITS)

- 9.6 SOLAR REFLECTIVE

- 9.6.1 INNOVATIONS FOR SOLAR HEAT REDUCTION IN AUTOMOTIVE PAINTS TO DRIVE GROWTH

- TABLE 107 SOLAR REFLECTIVE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND UNITS)

- TABLE 108 SOLAR REFLECTIVE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND UNITS)

10 AUTOMOTIVE PAINTS MARKET, BY CONTENT

- 10.1 INTRODUCTION

- 10.2 ELECTROCOAT, BY CONTENT

- FIGURE 40 AUTOMOTIVE ELECTROCOAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- TABLE 109 AUTOMOTIVE ELECTROCOAT MARKET, BY CONTENT, 2019-2022 (THOUSAND GALLONS)

- TABLE 110 AUTOMOTIVE ELECTROCOAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- 10.3 SOLVENT-BORNE PAINT, BY CONTENT

- FIGURE 41 AUTOMOTIVE SOLVENT-BORNE BASE COAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- TABLE 111 AUTOMOTIVE SOLVENT-BORNE BASE COAT MARKET, BY CONTENT, 2019-2022 (THOUSAND GALLONS)

- TABLE 112 AUTOMOTIVE SOLVENT-BORNE BASE COAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- FIGURE 42 AUTOMOTIVE SOLVENT-BORNE CLEAR COAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- TABLE 113 AUTOMOTIVE SOLVENT-BORNE CLEAR COAT MARKET, BY CONTENT, 2019-2022 (THOUSAND GALLONS)

- TABLE 114 AUTOMOTIVE SOLVENT-BORNE CLEAR COAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- 10.4 WATER-BORNE PAINT, BY CONTENT

- FIGURE 43 AUTOMOTIVE WATER-BORNE BASE COAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- TABLE 115 AUTOMOTIVE WATER-BORNE BASE COAT MARKET, BY CONTENT, 2019-2022 (THOUSAND GALLONS)

- TABLE 116 AUTOMOTIVE WATER-BORNE BASE COAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- FIGURE 44 AUTOMOTIVE WATER-BORNE CLEAR COAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

- TABLE 117 AUTOMOTIVE WATER-BORNE CLEAR COAT MARKET, BY CONTENT, 2019-2022 (THOUSAND GALLONS)

- TABLE 118 AUTOMOTIVE WATER-BORNE CLEAR COAT MARKET, BY CONTENT, 2023-2028 (THOUSAND GALLONS)

11 AUTOMOTIVE PAINTS MARKET, BY PAINTING EQUIPMENT TECHNIQUE

- 11.1 INTRODUCTION

- 11.1.1 INDUSTRY INSIGHTS

- FIGURE 45 AUTOMOTIVE PAINTS EQUIPMENT MARKET, BY REGION, 2023-2028 (UNITS)

- TABLE 119 AUTOMOTIVE PAINTS EQUIPMENT MARKET, BY REGION, 2019-2022 (UNITS)

- TABLE 120 AUTOMOTIVE PAINTS EQUIPMENT MARKET, BY REGION, 2023-2028 (UNITS)

- 11.2 AIRLESS SPRAY GUN

- 11.2.1 GROWING POPULARITY OF WATER-BORNE PAINTS TO DRIVE GROWTH

- TABLE 121 AIRLESS SPRAY GUN: AUTOMOTIVE PAINTS EQUIPMENT MARKET, BY REGION, 2019-2022 (UNITS)

- TABLE 122 AIRLESS SPRAY GUN: AUTOMOTIVE PAINTS EQUIPMENT MARKET, BY REGION, 2023-2028 (UNITS)

- 11.3 ELECTROSTATIC SPRAY GUN

- 11.3.1 STRICT ENVIRONMENTAL REGULATIONS TO DRIVE GROWTH

- TABLE 123 ELECTROSTATIC SPRAY GUN: AUTOMOTIVE PAINTS EQUIPMENT MARKET, BY REGION, 2019-2022 (UNITS)

- TABLE 124 ELECTROSTATIC SPRAY GUN: AUTOMOTIVE PAINTS EQUIPMENT MARKET, BY REGION, 2023-2028 (UNITS)

12 AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE

- 12.1 INTRODUCTION

- 12.1.1 INDUSTRY INSIGHTS

- FIGURE 46 AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- TABLE 125 AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 126 AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 127 AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 128 AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 12.2 PASSENGER CAR

- 12.2.1 RISE IN DEMAND FOR COMPACT AND MID-SIZED SUVS TO DRIVE GROWTH

- TABLE 129 PASSENGER CAR: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 130 PASSENGER CAR: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 131 PASSENGER CAR: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 132 PASSENGER CAR: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.3 LIGHT COMMERCIAL VEHICLE (LCV)

- 12.3.1 BOOMING E-COMMERCE AND LOGISTICS INDUSTRIES TO DRIVE GROWTH

- TABLE 133 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 134 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 135 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE PAINTS MARKET, BY REGION 2019-2022 (USD MILLION)

- TABLE 136 LIGHT COMMERCIAL VEHICLE: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.4 TRUCK

- 12.4.1 INCREASE IN VEHICLE SALES AND MAINTENANCE SERVICES TO DRIVE GROWTH

- TABLE 137 TRUCK: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 138 TRUCK: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 139 TRUCK: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 140 TRUCK: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.5 BUS

- 12.5.1 EXPANDING TOURISM INDUSTRY TO DRIVE GROWTH

- TABLE 141 BUS: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND GALLONS)

- TABLE 142 BUS: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND GALLONS)

- TABLE 143 BUS: AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 144 BUS: AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

13 ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY VEHICLE TYPE

- 13.1 INTRODUCTION

- 13.1.1 INDUSTRY INSIGHTS

- FIGURE 47 ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD BILLION)

- TABLE 145 ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND UNITS)

- TABLE 146 ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND UNITS)

- TABLE 147 ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 148 ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 13.2 BATTERY ELECTRIC VEHICLE (BEV)

- 13.2.1 GOVERNMENT INCENTIVES AND POLICIES TO DRIVE GROWTH

- TABLE 149 BEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND UNITS)

- TABLE 150 BEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND UNITS)

- TABLE 151 BEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 152 BEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 13.3 FUEL CELL ELECTRIC VEHICLE (FCEV)

- 13.3.1 HYDROGEN FUEL INFRASTRUCTURE DEVELOPMENT TO DRIVE GROWTH

- TABLE 153 FCEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND UNIT)

- TABLE 154 FCEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND UNIT)

- TABLE 155 FCEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 156 FCEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 13.4 PLUG-IN HYBRID VEHICLE (PHEV)

- 13.4.1 CHANGING CUSTOMER PREFERENCES TO DRIVE GROWTH

- TABLE 157 PHEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2019-2022 (THOUSAND UNITS)

- TABLE 158 PHEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2023-2028 (THOUSAND UNITS)

- TABLE 159 PHEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 160 PHEV: ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

14 AUTOMOTIVE REFINISH PAINTS MARKET, BY RESIN TYPE

- 14.1 INTRODUCTION

- FIGURE 48 AUTOMOTIVE REFINISH PAINTS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- TABLE 161 AUTOMOTIVE REFINISH PAINTS MARKET, BY RESIN TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 162 AUTOMOTIVE REFINISH PAINTS MARKET, BY RESIN TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 163 AUTOMOTIVE REFINISH PAINTS MARKET, BY RESIN TYPE, 2019-2022 (USD MILLION)

- TABLE 164 AUTOMOTIVE REFINISH PAINTS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- 14.2 POLYURETHANE

- 14.2.1 DIY CAR CARE TREND TO DRIVE GROWTH

- TABLE 165 POLYURETHANE: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 166 POLYURETHANE: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 167 POLYURETHANE: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 168 POLYURETHANE: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 14.3 EPOXY

- 14.3.1 RESTORATION OF CLASSIC CARS AND SPECIAL PERFORMANCE VEHICLES TO DRIVE GROWTH

- TABLE 169 EPOXY: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 170 EPOXY: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 171 EPOXY: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 172 EPOXY: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 14.4 ACRYLIC

- 14.4.1 REGULATORY COMPLIANCE TO LOWER DEMAND

- TABLE 173 ACRYLIC: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 174 ACRYLIC: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 175 ACRYLIC: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 176 ACRYLIC: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 14.5 OTHER RESINS

- TABLE 177 OTHER RESINS: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 178 OTHER RESINS: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 179 OTHER RESINS: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 180 OTHER RESINS: AUTOMOTIVE REFINISH PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

15 AUTOMOTIVE PAINTS MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.1.1 INDUSTRY INSIGHTS

- FIGURE 49 AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 181 AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 182 AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 183 AUTOMOTIVE PAINTS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 184 AUTOMOTIVE PAINTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 15.2 NORTH AMERICA

- FIGURE 50 NORTH AMERICA: AUTOMOTIVE PAINTS MARKET SNAPSHOT

- TABLE 185 NORTH AMERICA: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2019-2022 (THOUSAND GALLONS)

- TABLE 186 NORTH AMERICA: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2023-2028 (THOUSAND GALLONS)

- TABLE 187 NORTH AMERICA: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 188 NORTH AMERICA: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 15.2.1 US

- 15.2.1.1 Rise of electric and autonomous vehicles to drive growth

- TABLE 189 US: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 190 US: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 191 US: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 192 US: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.2.2 MEXICO

- 15.2.2.1 Robust automotive manufacturing base to drive growth

- TABLE 193 MEXICO: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 194 MEXICO: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 195 MEXICO: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 196 MEXICO: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.2.3 CANADA

- 15.2.3.1 Extreme climatic conditions to drive growth

- TABLE 197 CANADA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 198 CANADA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 199 CANADA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 200 CANADA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.3 ASIA PACIFIC

- FIGURE 51 ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET SNAPSHOT

- TABLE 201 ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2019-2022 (THOUSAND GALLONS)

- TABLE 202 ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2023-2028 (THOUSAND GALLONS)

- TABLE 203 ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 204 ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 15.3.1 CHINA

- 15.3.1.1 Large-scale vehicle production to drive growth

- TABLE 205 CHINA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 206 CHINA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 207 CHINA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 208 CHINA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.3.2 JAPAN

- 15.3.2.1 Rising popularity of Kei cars to drive growth

- TABLE 209 JAPAN: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 210 JAPAN: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 211 JAPAN: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 212 JAPAN: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.3.3 SOUTH KOREA

- 15.3.3.1 Presence of prominent automotive paint manufacturers to drive growth

- TABLE 213 SOUTH KOREA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 214 SOUTH KOREA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 215 SOUTH KOREA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 216 SOUTH KOREA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.3.4 INDIA

- 15.3.4.1 Vehicle Scrappage Policy to drive growth

- TABLE 217 INDIA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 218 INDIA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 219 INDIA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 220 INDIA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.3.5 REST OF ASIA PACIFIC

- TABLE 221 REST OF ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 222 REST OF ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 223 REST OF ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 224 REST OF ASIA PACIFIC: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.4 EUROPE

- TABLE 225 EUROPE: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2019-2022 (THOUSAND GALLONS)

- TABLE 226 EUROPE: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2023-2028 (THOUSAND GALLONS)

- TABLE 227 EUROPE: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 228 EUROPE: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 15.4.1 GERMANY

- 15.4.1.1 Rising production of premium cars to drive growth

- TABLE 229 GERMANY: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 230 GERMANY: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 231 GERMANY: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 232 GERMANY: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.4.2 FRANCE

- 15.4.2.1 Favorable government policies for electric vehicles to drive growth

- TABLE 233 FRANCE: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 234 FRANCE: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 235 FRANCE: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 236 FRANCE: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.4.3 UK

- 15.4.3.1 Zero Emission Vehicle mandate to drive growth

- TABLE 237 UK: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 238 UK: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 239 UK: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 240 UK: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.4.4 ITALY

- 15.4.4.1 Aging fleet renewal to drive growth

- TABLE 241 ITALY: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 242 ITALY: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 243 ITALY: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 244 ITALY: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.4.5 SPAIN

- 15.4.5.1 Tourism and recreational activities to drive growth

- TABLE 245 SPAIN: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 246 SPAIN: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 247 SPAIN: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 248 SPAIN: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.4.6 RUSSIA

- 15.4.6.1 Robust automobile manufacturing industry to drive growth

- TABLE 249 RUSSIA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 250 RUSSIA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 251 RUSSIA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 252 RUSSIA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.4.7 REST OF EUROPE

- TABLE 253 REST OF EUROPE: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 254 REST OF EUROPE: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 255 REST OF EUROPE: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 256 REST OF EUROPE: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.5 REST OF THE WORLD (ROW)

- TABLE 257 REST OF THE WORLD: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2019-2022 (THOUSAND GALLONS)

- TABLE 258 REST OF THE WORLD: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2023-2028 (THOUSAND GALLONS)

- TABLE 259 REST OF THE WORLD: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 260 REST OF THE WORLD: AUTOMOTIVE PAINTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 15.5.1 BRAZIL

- 15.5.1.1 Increasing sales of ethanol-based vehicles to drive growth

- TABLE 261 BRAZIL: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 262 BRAZIL: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 263 BRAZIL: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 264 BRAZIL: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.5.2 SOUTH AFRICA

- 15.5.2.1 Emergence of digital design tools and customization services to drive growth

- TABLE 265 SOUTH AFRICA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 266 SOUTH AFRICA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 267 SOUTH AFRICA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 268 SOUTH AFRICA: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 15.5.3 OTHERS

- TABLE 269 OTHERS: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (THOUSAND GALLONS)

- TABLE 270 OTHERS: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (THOUSAND GALLONS)

- TABLE 271 OTHERS: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 272 OTHERS: AUTOMOTIVE PAINTS MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 MARKET SHARE ANALYSIS, 2022

- FIGURE 52 MARKET SHARE OF KEY PLAYERS, 2022

- 16.3 REVENUE ANALYSIS, 2020 VS. 2022

- FIGURE 53 REVENUE ANALYSIS OF KEY PLAYERS, 2020 VS. 2022

- 16.4 AUTOMOTIVE PAINTS MARKET: COMPANY EVALUATION MATRIX, 2022

- 16.4.1 STARS

- 16.4.2 EMERGING LEADERS

- 16.4.3 PERVASIVE PLAYERS

- 16.4.4 PARTICIPANTS

- FIGURE 54 AUTOMOTIVE PAINTS MARKET: COMPANY EVALUATION MATRIX, 2022

- 16.5 COMPANY FOOTPRINT

- TABLE 273 AUTOMOTIVE PAINTS MARKET: COMPANY FOOTPRINT, 2022

- TABLE 274 AUTOMOTIVE PAINTS MARKET: TECHNOLOGY FOOTPRINT, 2022

- TABLE 275 AUTOMOTIVE PAINTS MARKET: REGION FOOTPRINT, 2022

- 16.6 AUTOMOTIVE REFINISH PAINTS MARKET: COMPANY EVALUATION MATRIX, 2022

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- FIGURE 55 AUTOMOTIVE REFINISH PAINTS MARKET: COMPANY EVALUATION MATRIX, 2022

- 16.7 COMPANY FOOTPRINT

- TABLE 276 AUTOMOTIVE REFINISH PAINTS MARKET: COMPANY FOOTPRINT, 2022

- TABLE 277 AUTOMOTIVE REFINISH PAINTS MARKET: TECHNOLOGY FOOTPRINT, 2022

- TABLE 278 AUTOMOTIVE REFINISH PAINTS MARKET: REGION FOOTPRINT, 2022

- 16.8 COMPETITIVE SCENARIO

- 16.8.1 PRODUCT DEVELOPMENTS, 2022-2023

- TABLE 279 PRODUCT DEVELOPMENTS, 2022-2023

- 16.8.2 DEALS, 2022-2023

- TABLE 280 DEALS, 2022-2023

- 16.8.3 OTHERS, 2022-2023

- TABLE 281 OTHERS, 2022-2023

- 16.9 RIGHT TO WIN, 2022-2023

- TABLE 282 RIGHT TO WIN, 2022-2023

17 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 17.1 KEY PLAYERS

- 17.1.1 PPG INDUSTRIES, INC.

- TABLE 283 PPG INDUSTRIES, INC.: COMPANY OVERVIEW

- FIGURE 56 PPG INDUSTRIES, INC.: COMPANY SNAPSHOT

- TABLE 284 PPG INDUSTRIES, INC.: PRODUCTS OFFERED

- TABLE 285 PPG INDUSTRIES, INC.: PRODUCT DEVELOPMENTS

- TABLE 286 PPG INDUSTRIES, INC.: DEALS

- TABLE 287 PPG INDUSTRIES, INC.: OTHERS

- 17.1.2 BASF SE

- TABLE 288 BASF SE: COMPANY OVERVIEW

- FIGURE 57 BASF SE: COMPANY SNAPSHOT

- TABLE 289 BASF SE: PRODUCTS OFFERED

- TABLE 290 BASF SE: PRODUCT DEVELOPMENTS

- TABLE 291 BASF SE: DEALS

- TABLE 292 BASF SE: OTHERS

- 17.1.3 AXALTA COATING SYSTEMS, LLC

- TABLE 293 AXALTA COATING SYSTEMS, LLC: COMPANY OVERVIEW

- FIGURE 58 AXALTA COATING SYSTEMS, LLC: COMPANY SNAPSHOT

- TABLE 294 AXALTA COATING SYSTEMS, LLC: PRODUCTS OFFERED

- TABLE 295 AXALTA COATING SYSTEMS, LLC: PRODUCT DEVELOPMENTS

- TABLE 296 AXALTA COATING SYSTEMS, LLC: DEALS

- TABLE 297 AXALTA COATING SYSTEMS, LLC: OTHERS

- 17.1.4 AKZO NOBEL N.V.

- TABLE 298 AKZO NOBEL N.V.: COMPANY OVERVIEW

- FIGURE 59 AKZO NOBEL N.V.: COMPANY SNAPSHOT

- TABLE 299 AKZO NOBEL N.V.: PRODUCTS OFFERED

- TABLE 300 AKZO NOBEL N.V.: PRODUCT DEVELOPMENTS

- TABLE 301 AKZO NOBEL N.V.: DEALS

- TABLE 302 AKZO NOBEL N.V.: OTHERS

- 17.1.5 THE SHERWIN-WILLIAMS COMPANY

- TABLE 303 THE SHERWIN-WILLIAMS COMPANY: COMPANY OVERVIEW

- FIGURE 60 THE SHERWIN-WILLIAMS COMPANY: COMPANY SNAPSHOT

- TABLE 304 THE SHERWIN-WILLIAMS COMPANY: PRODUCTS OFFERED

- TABLE 305 THE SHERWIN-WILLIAMS COMPANY: PRODUCT DEVELOPMENTS

- TABLE 306 THE SHERWIN-WILLIAMS COMPANY: DEALS

- TABLE 307 THE SHERWIN-WILLIAMS COMPANY: OTHERS

- 17.1.6 KANSAI PAINT CO., LTD.

- TABLE 308 KANSAI PAINT CO., LTD.: COMPANY OVERVIEW

- FIGURE 61 KANSAI PAINT CO., LTD.: COMPANY SNAPSHOT

- TABLE 309 KANSAI PAINT CO., LTD.: PRODUCTS OFFERED

- TABLE 310 KANSAI PAINT CO., LTD.: DEALS

- 17.1.7 SOLVAY

- TABLE 311 SOLVAY: COMPANY OVERVIEW

- FIGURE 62 SOLVAY: COMPANY SNAPSHOT

- TABLE 312 SOLVAY: PRODUCTS OFFERED

- TABLE 313 SOLVAY: PRODUCT DEVELOPMENTS

- TABLE 314 SOLVAY: OTHERS

- 17.1.8 NIPPON PAINT HOLDINGS CO., LTD.

- TABLE 315 NIPPON PAINT HOLDINGS CO., LTD.: COMPANY OVERVIEW

- FIGURE 63 NIPPON PAINT HOLDINGS CO., LTD.: COMPANY SNAPSHOT

- TABLE 316 NIPPON PAINT HOLDINGS CO., LTD.: PRODUCTS OFFERED

- TABLE 317 NIPPON PAINT HOLDINGS CO., LTD.: PRODUCT DEVELOPMENTS

- TABLE 318 NIPPON PAINT HOLDINGS CO., LTD.: DEALS

- 17.1.9 COVESTRO AG

- TABLE 319 COVESTRO AG: COMPANY OVERVIEW

- FIGURE 64 COVESTRO AG: COMPANY SNAPSHOT

- TABLE 320 COVESTRO AG: PRODUCTS OFFERED

- TABLE 321 COVESTRO AG: PRODUCT DEVELOPMENTS

- TABLE 322 COVESTRO AG: OTHERS

- 17.1.10 CLARIANT

- TABLE 323 CLARIANT: COMPANY OVERVIEW

- FIGURE 65 CLARIANT: COMPANY SNAPSHOT

- TABLE 324 CLARIANT: PRODUCTS OFFERED

- TABLE 325 CLARIANT: PRODUCT DEVELOPMENTS

- 17.2 OTHER PLAYERS

- 17.2.1 JOTUN

- TABLE 326 JOTUN: COMPANY OVERVIEW

- 17.2.2 SKSHU PAINT CO., LTD.

- TABLE 327 SKSHU PAINT CO., LTD.: COMPANY OVERVIEW

- 17.2.3 KCC CORPORATION

- TABLE 328 KCC CORPORATION: COMPANY OVERVIEW

- 17.2.4 DONGLAI COATING TECHNOLOGY (SHANGHAI) CO., LTD.

- TABLE 329 DONGLAI COATING TECHNOLOGY (SHANGHAI) CO., LTD.: COMPANY OVERVIEW

- 17.2.5 DUPONT

- TABLE 330 DUPONT: COMPANY OVERVIEW

- 17.2.6 STANDOX

- TABLE 331 STANDOX: COMPANY OVERVIEW

- 17.2.7 NEXA AUTOCOLOR

- TABLE 332 NEXA AUTOCOLOR: COMPANY OVERVIEW

- 17.2.8 3M

- TABLE 333 3M: COMPANY OVERVIEW

- 17.2.9 WACKER CHEMIE AG

- TABLE 334 WACKER CHEMIE AG: COMPANY OVERVIEW

- 17.2.10 PPG ASIANPAINTS

- TABLE 335 PPG ASIANPAINTS: COMPANY OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

18 RECOMMENDATIONS BY MARKETSANDMARKETS

- 18.1 ASIA PACIFIC TO BE MAJOR MARKET FOR AUTOMOTIVE PAINTS

- 18.2 ENVIRONMENT FRIENDLINESS AND BETTER STRENGTH-TO-WEIGHT RATIO TO DRIVE POLYURETHANE SEGMENT

- 18.3 CONCLUSION

19 APPENDIX

- 19.1 INSIGHTS FROM INDUSTRY EXPERTS

- 19.2 DISCUSSION GUIDE

- 19.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.4 CUSTOMIZATION OPTIONS

- 19.4.1 ADDITIONAL COMPANY PROFILES

- 19.4.2 ELECTRIC & HYBRID VEHICLE PAINTS MARKET, BY VEHICLE TYPE, AT COUNTRY LEVEL

- 19.4.2.1 BEV

- 19.4.2.2 FCEV

- 19.4.2.3 PHEV

- 19.5 RELATED REPORTS

- 19.6 AUTHOR DETAILS