|

|

市場調査レポート

商品コード

1393004

経皮吸収パッチの世界市場:タイプ別、粘着剤別、用途別、流通チャネル別、エンドユーザー別 - 予測(~2029年)Transdermal Patches Market by Type (Drug-in-adhesives, Matrix, Reservoir Membrane), Adhesive (Acrylic, Silicone, Hydrogel), Application (Pain, CVS, Hormonal), Distribution Channel (Pharmacy (Retail Online, Hospital)), End User - Global Forecast to 2029 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 経皮吸収パッチの世界市場:タイプ別、粘着剤別、用途別、流通チャネル別、エンドユーザー別 - 予測(~2029年) |

|

出版日: 2023年11月30日

発行: MarketsandMarkets

ページ情報: 英文 282 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

レポートの概要

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2029年 |

| 基準年 | 2022年 |

| 予測期間 | 2023年~2029年 |

| 単位 | 10億米ドル |

| セグメント | パッチタイプ、粘着剤タイプ、用途、流通チャネル、エンドユーザー |

| 対象地域 | 北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカ |

世界の経皮吸収パッチの市場規模は、2023年に62億米ドル、2029年までに80億米ドルに達し、2023年~2029年にCAGRで4.5%の成長が予測されています。

市場の成長促進要因は、慢性疾患の流行、鎮痛パッチ使用の拡大、経皮吸収パッチ技術の進歩、従来の注射から経皮吸収パッチへの移行などです。とはいえ、薬剤の不具合、経皮ドラッグデリバリーシステムのリコール、医療施設費の増加などの要因が、予測期間に市場の拡大をある程度抑制する見込みです。

「パッチタイプ別では、マトリクスパッチセグメントがもっとも高いCAGRで成長すると予測されます。」

パッチの魅力と有効性を高める多くの特徴により、マトリクスパッチセグメントが市場でもっとも高いCAGRで成長すると予測されます。マトリクスパッチの処方と製造における継続的な技術改良により、患者コンプライアンスとマトリクスパッチの有効性が高まっています。

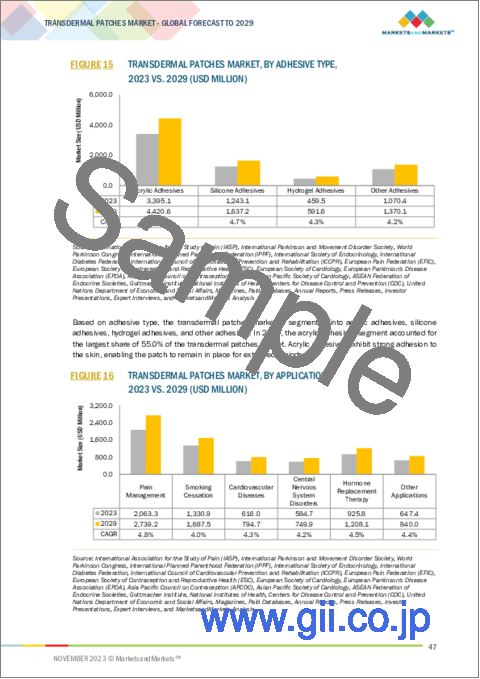

「粘着剤別では、シリコン粘着剤セグメントがもっとも高いCAGRで成長する見込みです。」

シリコン粘着剤は他の粘着剤と比較して特別な利点があるため、シリコン粘着パッチセグメントが市場でもっとも高いCAGRで成長すると予測されます。

「用途別では、疼痛管理セグメントが市場でもっとも高いCAGRで成長する見込みです。」

安全で非侵襲性の疼痛緩和の選択肢へのニーズの高まりにより、市場は疼痛管理セグメントでもっとも高い成長率となる見込みです。痛みを和らげる経皮吸収パッチは、鎮痛薬を標的を定めて調節しながら皮膚から放出することで、均一で安定した治療効果をもたらします。この方法は侵襲性の治療や従来の経口薬に代わる選択肢を提供し、慢性疼痛障害を抱える人々にとって特に魅力的なものとなっています。

「流通チャネル別では、オンライン薬局セグメントが市場でもっとも高いCAGRで成長する見込みです。」

これは一般的なデジタル化の動向と、医療商品のeコマースプラットフォームへの依存の高まりによるものです。顧客はオンライン薬局の助けを借りて、自宅から簡単かつ便利に経皮吸収パッチを入手することができます。eコマースの人気の高まりが、その便利な注文や宅配の機能とともに、医療への手間のかからないアクセスを求める患者のニーズの変化に対応しています。

「エンドユーザー別では、在宅ケア環境セグメントが市場でもっとも高いCAGRで成長する見込みです。」

患者中心の個別化医療を目指す動向の拡大から、在宅ケア環境セグメントがエンドユーザーとしてもっとも高い速度で成長すると予測されます。経皮吸収パッチは便利な非侵襲性の投薬方法を提供するため、家庭内での自己投与に特に適しています。高齢化と慢性疾患の増加により、利用しやすく長期的な代替の治療品へのニーズが高まっています。経皮吸収パッチは、この医療の新しいパラダイムに完璧に適合しています。

「予測期間にアジア太平洋が市場でもっとも高いCAGRで成長します。」

アジア太平洋市場は、同地域の医療情勢の変化を浮き彫りにするさまざまな要因により、もっとも高いCAGRで成長すると予測されます。慢性疾患の罹患率の上昇と非侵襲性のドラッグデリバリー技術に関する知識の高まりにより、経皮吸収パッチはますます普及しています。この地域の多数の人口と高齢化は医療コスト上昇の主要因であり、その結果、利用しやすく患者に優しい治療オプションに対する需要が高まっています。アジア太平洋市場もまた、医薬品研究開発のブレイクスルーや可処分所得の増加、医療インフラの改善により拡大が見込まれています。

当レポートでは、世界経皮吸収パッチの市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 経皮吸収パッチ市場の概要

- アジア太平洋の経皮吸収パッチ市場:パッチタイプ別、国別(2022年)

- 経皮吸収パッチ市場:地理的な成長機会

- 経皮吸収パッチ市場:地域別、構成(2021年~2029年)

- 経皮吸収パッチ市場:発展途上国市場 VS. 先進国市場

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 技術分析

- 産業の動向

- バリューチェーン分析

- サプライチェーン分析

- 貿易分析

- ポーターのファイブフォース分析

- 関税と規制情勢

- 規制分析

- 規制機関、政府機関、その他の組織

- 特許分析

- 価格分析

- 主な会議とイベント(2023年~2024年)

- 主なステークホルダーと購入基準

- エコシステム/市場マップ

- 隣接市場の分析

- 顧客のビジネスに影響を与える動向/混乱

- アンメットニーズ

第6章 経皮吸収パッチ市場:パッチタイプ別

- イントロダクション

- 薬剤入り粘着剤パッチ

- 単層薬剤入り粘着剤パッチ

- 多層薬剤入り粘着剤パッチ

- マトリクスパッチ

- リザーバー膜パッチ

- マイクロニードルパッチ

- イオン導入パッチ

- ベイパーパッチ

第7章 経皮吸収パッチ市場:粘着剤タイプ別

- イントロダクション

- アクリル粘着剤

- シリコン粘着剤

- ヒドロゲル粘着剤

- その他の粘着剤

第8章 経皮吸収パッチ市場:用途別

- イントロダクション

- 疼痛管理

- 禁煙

- ホルモン補充療法

- 経皮テストステロン療法

- 経皮エストロゲン療法

- 中枢神経系障害

- 心血管疾患

- その他の用途

第9章 経皮吸収パッチ市場:流通チャネル別

- イントロダクション

- 病院薬局

- 小売薬局

- オンライン薬局

第10章 経皮吸収パッチ市場:エンドユーザー別

- イントロダクション

- 在宅ケア環境

- 病院・診療所

第11章 経皮吸収パッチ市場:地域別

- イントロダクション

- 北米

- 北米の経皮吸収パッチ市場に対する景気後退の影響

- 米国

- カナダ

- 欧州

- 欧州経皮吸収パッチ市場に対する景気後退の影響

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- アジア太平洋経皮吸収パッチ市場に対する景気後退の影響

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ラテンアメリカの経皮吸収パッチ市場に対する景気後退の影響

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

第12章 競合情勢

- イントロダクション

- 主な市場企業の収益の分析

- 市場シェア分析

- 企業のフットプリント

- 経皮吸収パッチ市場:研究開発支出

- 企業の評価マトリクス

- 中小企業/スタートアップの評価マトリクス

- 競合状況と動向

第13章 企業プロファイル

- 主要企業

- HISAMITSU PHARMACEUTICAL CO., INC.

- VIATRIS INC.

- NOVARTIS AG

- BOEHRINGER INGELHEIM INTERNATIONAL GMBH

- JOHNSON & JOHNSON

- UCB S.A.

- ENDO INTERNATIONAL PLC

- LUYE PHARMA GROUP

- ABBVIE INC.

- NITTO DENKO CORPORATION

- CIPLA INC.

- TEVA PHARMACEUTICAL INDUSTRIES LTD.

- AGILE THERAPEUTICS

- BAYER AG

- AMNEAL PHARMACEUTICALS LLC

- HIKMA PHARMACEUTICALS PLC

- その他の企業

- ALVOGEN GROUP INC.

- SPARSHA PHARMA INTERNATIONAL PVT. LTD.

- IONTOPATCH

- MEDHERANT LIMITED

- ADHEXPHARMA

- EVERNOW

- LEAD CHEMICAL CO., LTD.

- PURDUE PHARMA L.P.

- MUNDIPHARMA INTERNATIONAL

- COMPANIES PROVIDING ADHESIVES FOR TRANSDERMAL PATCHES

- WACKER CHEMIE AG

- ELKEM ASA

- DUPONT DE NEMOURS, INC.

- KATECHO, LLC

- POLYMER SCIENCE, INC.

第14章 付録

Report Description

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2029 |

| Base Year | 2022 |

| Forecast Period | 2023-2029 |

| Units Considered | Value (USD) Billion |

| Segments | Patch Type, Adhesive Type, Application, Distribution Channel, End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

The global transdermal patches market is projected to reach 8.0 USD Billion by 2029 from USD 6.2 Billion in 2023, at a CAGR of 4.5% from 2023 to 2029. The factors driving the growth of the global transdermal patches market include the rising prevalence of chronic diseases, the expanding use of analgesic patches, technological advancements in transdermal patches, and the shift from traditional injections to transdermal patches. Nonetheless, during the anticipated period, factors such as drug failures, recalls of transdermal drug delivery systems, and increasing healthcare facility expenses will probably constrain market expansion to some degree.

"The matrix patches segment is expected to grow with the highest CAGR in patch type of the transdermal patches market."

Due to a number of characteristics that increase the patch's appeal and efficacy, the matrix patches segment is expected to grow at the highest CAGR in the transdermal patch market. In matrix patches, the medicine is evenly dispersed within a polymer matrix, providing a straightforward but effective design. This design promotes the best possible drug absorption via the skin by enabling a prolonged, regulated release of the medicinal substance. Due to its adaptability, matrix patches are widely used in a variety of therapeutic fields. This is because they may be used to administer a broad range of drugs. Patient compliance and matrix patch efficacy are increasing as a result of ongoing technological improvements in matrix patch formulation and manufacturing.

"The silicone adhesives segment is expected to grow with the highest CAGR in the adhesive type of the transdermal patches market."

Since silicone adhesives have particular advantages over other adhesives, it is expected that the silicone adhesive patches segment of the transdermal patch market will grow at the fastest CAGR. Silicone adhesives ensure patient comfort and adherence by forming a thin yet strong connection with the skin. Because they are biocompatible and hypoallergenic, they can be used by a wide range of patients with less chance of skin sensitivity or irritation. Silicone adhesive patches' conformability and flexibility make them more comfortable to wear and encourage prolonged and regular use.

"Based on the Application Type, the pain management segment is expected to grow by the highest CAGR in the transdermal patches market."

The market for transdermal patches is expected to grow at the fastest rate in the pain management segment due to the growing need for safe, non-invasive pain reduction options. Pain-relieving transdermal patches deliver an even and steady therapeutic impact by releasing analgesic drugs through the skin in a targeted and regulated manner. This method offers an alternative to invasive therapies and conventional oral drugs, making it especially tempting to people with chronic pain disorders.

"Based on the Distribution Channel, The online Pharmacies segment is expected to grow with the highest CAGR in the transdermal patches market."

As a distribution channel for transdermal patches, the online pharmacies segment is anticipated to grow at the fastest rate in the market. This is due to the general trend of digitalization and the growing dependence of healthcare items on e-commerce platforms. Customers can get transdermal patches easily and conveniently from the comfort of their homes with the help of online pharmacies. The increasing popularity of e-commerce, together with its convenient ordering and doorstep delivery features, corresponds with the changing needs of patients who want hassle-free access to healthcare.

"Based on the End User, The Homecare Settings segment is expected to grow with the highest CAGR in the transdermal patches market."

Given the growing trend towards patient-centered and personalized healthcare, the transdermal patch market's homecare settings sector is expected to grow at the fastest rate as an end-user. For self-administration in domestic settings, transdermal patches are especially well-suited since they offer a convenient and non-invasive way to administer medication. The need for accessible, long-term treatment alternatives is fueled by the aging population and the rise of chronic illnesses. Transdermal patches are a perfect fit with this new paradigm in healthcare since homecare settings provide people the freedom to take care of their healthcare needs on their own.

"Asia Pacific to grow with the highest CAGR in the transdermal patches market during the forecast period."

The transdermal patch market in Asia Pacific is expected to grow at the highest CAGR due to an array of factors that highlight the region's changing healthcare landscape. Transdermal patches are becoming more and more popular due to the rising incidence of chronic illnesses and rising knowledge of non-invasive medication delivery techniques. The huge and aging population in the area is a major factor in the rising cost of healthcare, which in turn is driving up demand for accessible and patient-friendly treatment choices. The transdermal patch market in Asia Pacific is also expected to rise as a result of breakthroughs in pharmaceutical research and development, rising disposable incomes, and improved healthcare infrastructure.

A breakdown of the primary participants (supply-side) for the transdermal patches market referred to for this report is provided below:

- By Company Type: Tier 1-45%, Tier 2-30%, and Tier 3-25%

- By Designation: C-level-42%, Director Level-29%, and Others-29%

- By Region: North America-30%, Europe-25%, Asia Pacific-30%, Latin America- 10%, Middle East & Africa-5%

The prominent players in the transdermal patches market include Johnson & Johnson (U.S.), Viatris Inc. (U.S.), Hisamatsu Pharmaceuticals Co. Ltd. (Japan), Cipla Inc. (India), Teva Pharmaceutical Industries Ltd. (Israel), Agile Therapeutics (U.S.), Bayer AG (Germany), Luye Pharma Group (China), Sparsha Pharma International Pvt Ltd (India), Iontopatch (U.S.), Medherant Limited (U.K.), AdhexPharma (France), Evernow (U.S.), Amneal Pharmaceuticals LLC. (U.S.), Hikma Pharmaceuticals PLC (U.K.), Alvogen Group Inc. (U.S.), Novartis AG (Switzerland), AbbVie Inc. (U.S.), Nitto Denko Corporation (Japan), USB S.A. (Belgium), Boehringer Ingelheim International GmbH (Germany), Endo International plc. (Ireland), LEAD CHEMICAL Co., Ltd. (Japan), Purdue Pharma L.P (U.S.) and Mundipharma International (U.K.).

Research Coverage:

The market study covers the transdermal patches market across various segments. It aims to estimate the market size and the growth potential of this market across different segments by patch type, adhesive type, application, distribution type, end-user, and region. The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their product and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall transdermal patches market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights on the following pointers:

- Analysis of key drivers (Increasing prevalence of chronic diseases, Growing adoption of analgesic patches, Technological advancements in transdermal patches, Switching from conventional needle injections to transdermal patches), restraints (High procedural cost of vascular surgeries and associated products, Drug failure and recalls of transdermal drug delivery systems, Rising cost of healthcare facilities), opportunities (Collaborations between pharmaceutical companies and drug delivery firms, Self-administration and home care drug delivery systems) and challenges (Technical barriers related to skin irritation and permeability, Lack of skilled professionals)

- Market Penetration: Comprehensive information on product portfolios offered by the top players in the global transdermal patches market. The report analyzes this market by patch type, adhesive type, application, distribution channel, end-user, and region.

- Product Enhancement/Innovation: Detailed insights on upcoming trends and product launches in the global transdermal patches market.

- Market Development: Comprehensive information on the lucrative emerging markets by patch type, adhesive type, application, distribution channel, end-user, and region.

- Market Diversification: Exhaustive information about new products and services, growing geographies, recent developments, and investments in the global transdermal patches market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product and service offerings, and capabilities of leading players in the global transdermal patches market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 INCLUSIONS AND EXCLUSIONS OF STUDY

- 1.3.2 MARKETS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY

- TABLE 1 STANDARD CURRENCY CONVERSION RATES

- 1.5 STAKEHOLDERS

- 1.6 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- FIGURE 2 PRIMARY SOURCES

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: SUPPLY-SIDE AND DEMAND-SIDE PARTICIPANTS

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS (SUPPLY SIDE): BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 5 BREAKDOWN OF PRIMARY INTERVIEWS (DEMAND SIDE): BY END USER, DESIGNATION, AND REGION

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 6 SUPPLY-SIDE MARKET SIZE ESTIMATION: REVENUE SHARE ANALYSIS

- FIGURE 7 REVENUE SHARE ANALYSIS ILLUSTRATION: JOHNSON & JOHNSON

- FIGURE 8 SUPPLY-SIDE MARKET SIZE ESTIMATION: TRANSDERMAL PATCHES MARKET (2022)

- FIGURE 9 BOTTOM-UP APPROACH

- FIGURE 10 TOP-DOWN APPROACH

- FIGURE 11 CAGR PROJECTIONS FROM DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES (2023-2029)

- FIGURE 12 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 13 DATA TRIANGULATION METHODOLOGY

- 2.4 MARKET SHARE ESTIMATION

- 2.5 ASSUMPTIONS FOR STUDY

- 2.6 RESEARCH LIMITATIONS

- 2.6.1 SCOPE-RELATED LIMITATIONS

- 2.6.2 METHODOLOGY-RELATED LIMITATIONS

- 2.7 RISK ASSESSMENT

- TABLE 2 RISK ASSESSMENT: TRANSDERMAL PATCHES MARKET

- 2.8 IMPACT OF RECESSION ON TRANSDERMAL PATCHES MARKET

3 EXECUTIVE SUMMARY

- FIGURE 14 TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2023 VS. 2029 (USD MILLION)

- FIGURE 15 TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2023 VS. 2029 (USD MILLION)

- FIGURE 16 TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2023 VS. 2029 (USD MILLION)

- FIGURE 17 TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2023 VS. 2029 (USD MILLION)

- FIGURE 18 TRANSDERMAL PATCHES MARKET, BY END USER, 2023 VS. 2029 (USD MILLION)

- FIGURE 19 GEOGRAPHICAL SNAPSHOT OF TRANSDERMAL PATCHES MARKET

4 PREMIUM INSIGHTS

- 4.1 TRANSDERMAL PATCHES MARKET OVERVIEW

- FIGURE 20 RISING PREVALENCE OF CHRONIC DISEASES TO DRIVE MARKET

- 4.2 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE AND COUNTRY (2022)

- FIGURE 21 DRUG-IN-ADHESIVE PATCHES SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

- 4.3 TRANSDERMAL PATCHES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- FIGURE 22 CHINA TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- 4.4 TRANSDERMAL PATCHES MARKET, REGIONAL MIX, 2021-2029

- FIGURE 23 NORTH AMERICA WILL CONTINUE TO DOMINATE TRANSDERMAL PATCHES MARKET DURING FORECAST PERIOD

- 4.5 TRANSDERMAL PATCHES MARKET: DEVELOPING VS. DEVELOPED MARKETS

- FIGURE 24 DEVELOPING MARKETS TO REGISTER HIGHER GROWTH DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 25 TRANSDERMAL PATCHES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing prevalence of chronic diseases

- 5.2.1.2 Growing adoption of analgesic patches

- 5.2.1.3 Technological advancements in transdermal patches

- 5.2.1.4 Switching from conventional needle injections to transdermal patches

- 5.2.2 RESTRAINTS

- 5.2.2.1 High procedural cost of transdermal surgeries and associated products

- 5.2.2.2 Drug failure and recalls of transdermal drug delivery systems

- 5.2.2.3 Rising cost of healthcare facilities

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Collaborations between pharmaceutical companies and drug delivery firms

- 5.2.3.2 Self-administration and home care drug delivery systems

- 5.2.4 CHALLENGES

- 5.2.4.1 Technical barriers related to skin irritation and permeability

- 5.2.4.2 Lack of skilled professionals

- 5.3 TECHNOLOGY ANALYSIS

- 5.4 INDUSTRY TRENDS

- 5.4.1 ADVANCEMENTS IN TRANSDERMAL DRUG DELIVERY SYSTEMS

- 5.5 VALUE CHAIN ANALYSIS

- FIGURE 26 TRANSDERMAL PATCHES MARKET: VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- FIGURE 27 TRANSDERMAL PATCHES MARKET: SUPPLY CHAIN ANALYSIS

- 5.7 TRADE ANALYSIS

- 5.7.1 TRADE ANALYSIS FOR TRANSDERMAL PATCHES

- TABLE 3 IMPORT AND EXPORT DATA FOR TRANSDERMAL PATCHES, BY COUNTRY, 2022

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 TRANSDERMAL PATCHES MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 THREAT OF NEW ENTRANTS

- 5.8.2 THREAT OF SUBSTITUTES

- 5.8.3 BARGAINING POWER OF BUYERS

- 5.8.4 BARGAINING POWER OF SUPPLIERS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 TARIFF AND REGULATORY LANDSCAPE

- 5.9.1 REGULATORY ANALYSIS

- 5.9.1.1 North America

- 5.9.1.1.1 US

- 5.9.1.1.2 Canada

- 5.9.1.2 Europe

- 5.9.1.3 Asia Pacific

- 5.9.1.3.1 China

- 5.9.1.3.2 Japan

- 5.9.1.3.3 India

- 5.9.1.4 Latin America

- 5.9.1.4.1 Brazil

- 5.9.1.4.2 Mexico

- 5.9.1.5 Middle East

- 5.9.1.6 Africa

- 5.9.1.1 North America

- 5.9.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 5 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 6 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.9.1 REGULATORY ANALYSIS

- 5.10 PATENT ANALYSIS

- 5.10.1 PATENT PUBLICATION TRENDS FOR TRANSDERMAL PATCHES

- FIGURE 28 PATENT PUBLICATION TRENDS (JANUARY 2015-DECEMBER 2022)

- 5.10.2 JURISDICTION ANALYSIS: TOP APPLICANTS FOR PATENTS IN TRANSDERMAL PATCHES MARKET

- FIGURE 29 TOP APPLICANTS & OWNERS (COMPANIES/INSTITUTES) FOR TRANSDERMAL PATCH PATENTS (JANUARY 2015-DECEMBER 2022)

- FIGURE 30 TOP APPLICANT COUNTRIES/REGIONS FOR TRANSDERMAL PATCHES (JANUARY 2015-APRIL 2022)

- 5.11 PRICING ANALYSIS

- TABLE 10 AVERAGE SELLING PRICE TRENDS OF KEY PLAYERS, BY APPLICATION

- TABLE 11 REGIONAL PRICING ANALYSIS OF TRANSDERMAL PATCHES, 2023 (USD)

- 5.12 KEY CONFERENCES & EVENTS IN 2023-2024

- TABLE 12 TRANSDERMAL PATCHES MARKET: DETAILED LIST OF CONFERENCES & EVENTS

- 5.13 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF TRANSDERMAL PATCHES

- TABLE 13 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF TRANSDERMAL PATCHES

- 5.13.2 BUYING CRITERIA

- FIGURE 32 KEY BUYING CRITERIA FOR TRANSDERMAL PATCHES

- TABLE 14 KEY BUYING CRITERIA FOR TRANSDERMAL PATCHES

- 5.14 ECOSYSTEM/MARKET MAP

- FIGURE 33 TRANSDERMAL PATCHES MARKET: ECOSYSTEM/MARKET MAP

- 5.15 ADJACENT MARKET ANALYSIS

- FIGURE 34 TRANSDERMAL PATCHES MARKET: ADJACENT MARKETS

- 5.16 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- FIGURE 35 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.17 UNMET NEEDS

6 TRANSDERMAL PATCHES MARKET, BY PATCH TYPE

- 6.1 INTRODUCTION

- TABLE 15 TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- 6.2 DRUG-IN-ADHESIVE PATCHES

- TABLE 16 DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 17 DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- 6.2.1 SINGLE-LAYER DRUG-IN-ADHESIVE PATCHES

- 6.2.1.1 Used to deliver wide range of medications

- TABLE 18 SINGLE-LAYER DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- 6.2.2 MULTI-LAYER DRUG-IN-ADHESIVE PATCHES

- 6.2.2.1 Enhanced drug release and reduced side effects to drive adoption

- TABLE 19 MULTI-LAYER DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- 6.3 MATRIX PATCHES

- 6.3.1 TECHNOLOGICAL ADVANCEMENTS IN NEW MATRIX MATERIALS TO SUPPORT MARKET GROWTH

- TABLE 20 MATRIX TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- 6.4 RESERVOIR MEMBRANE PATCHES

- 6.4.1 OFFER GREAT CONTROL OVER DRUG DELIVERY RATES

- TABLE 21 RESERVOIR MEMBRANE TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- 6.5 MICRONEEDLE PATCHES

- 6.5.1 ABILITY TO DELIVER ACTIVE PHARMACEUTICAL INGREDIENTS TO BOOST ADOPTION

- TABLE 22 MICRONEEDLE TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- 6.6 IONTOPHORESIS PATCHES

- 6.6.1 USED TO DELIVER MEDICINES WITH LOW MOLECULAR WEIGHT

- TABLE 23 IONTOPHORESIS TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- 6.7 VAPOR PATCHES

- 6.7.1 RELEASE ESSENTIAL OILS FOR UP TO 6 HOURS

- TABLE 24 VAPOR TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

7 TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE

- 7.1 INTRODUCTION

- TABLE 25 TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- 7.2 ACRYLIC ADHESIVES

- 7.2.1 HIGH DURABILITY TO BOOST DEMAND

- TABLE 26 TRANSDERMAL PATCHES MARKET FOR ACRYLIC ADHESIVES, BY COUNTRY, 2021-2029 (USD MILLION)

- 7.3 SILICONE ADHESIVES

- 7.3.1 LOW PEEL ADHESION PROPERTY MAKES IT IDEAL FOR MEDICAL APPLICATIONS

- TABLE 27 TRANSDERMAL PATCHES MARKET FOR SILICONE ADHESIVES, BY COUNTRY, 2021-2029 (USD MILLION)

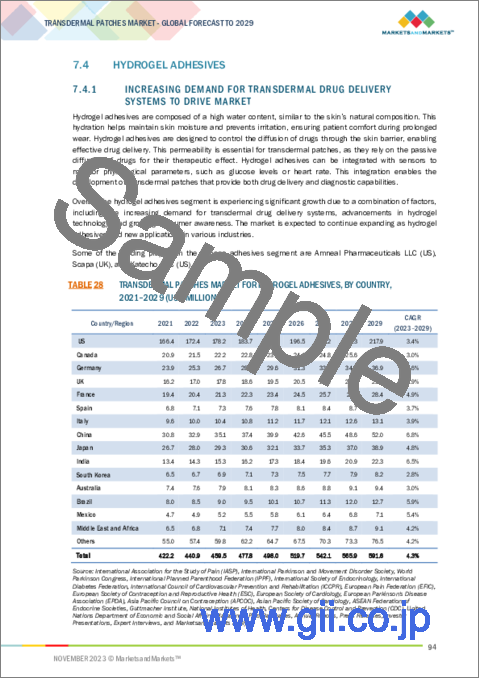

- 7.4 HYDROGEL ADHESIVES

- 7.4.1 INCREASING DEMAND FOR TRANSDERMAL DRUG DELIVERY SYSTEMS TO DRIVE MARKET

- TABLE 28 TRANSDERMAL PATCHES MARKET FOR HYDROGEL ADHESIVES, BY COUNTRY, 2021-2029 (USD MILLION)

- 7.5 OTHER ADHESIVES

- TABLE 29 TRANSDERMAL PATCHES MARKET FOR OTHER ADHESIVES, BY COUNTRY, 2021-2029 (USD MILLION)

8 TRANSDERMAL PATCHES MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- TABLE 30 TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- 8.2 PAIN MANAGEMENT

- 8.2.1 HIGH BURDEN OF CHRONIC PAIN WORLDWIDE TO DRIVE MARKET

- TABLE 31 TRANSDERMAL PATCHES AVAILABLE FOR PAIN MANAGEMENT

- TABLE 32 TRANSDERMAL PATCHES MARKET FOR PAIN MANAGEMENT, BY COUNTRY, 2021-2029 (USD MILLION)

- 8.3 SMOKING CESSATION

- 8.3.1 CONTROLLED DRUG DELIVERY AND REDUCED SIDE EFFECTS TO SUPPORT MARKET GROWTH

- TABLE 33 TRANSDERMAL PATCHES AVAILABLE FOR SMOKING CESSATION

- TABLE 34 TRANSDERMAL PATCHES MARKET FOR SMOKING CESSATION, BY COUNTRY, 2021-2029 (USD MILLION)

- 8.4 HORMONE REPLACEMENT THERAPY

- TABLE 35 TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 36 TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY COUNTRY, 2021-2029 (USD MILLION)

- 8.4.1 TRANSDERMAL TESTOSTERONE THERAPY

- 8.4.1.1 Increased bone density, better muscle development, and reduced risk factors to support market growth

- TABLE 37 TRANSDERMAL PATCHES AVAILABLE FOR TRANSDERMAL TESTOSTERONE THERAPY

- TABLE 38 TRANSDERMAL PATCHES MARKET FOR TRANSDERMAL TESTOSTERONE THERAPY, BY COUNTRY, 2021-2029 (USD MILLION)

- 8.4.2 TRANSDERMAL ESTROGEN THERAPY

- 8.4.2.1 Growing use of transdermal contraceptive patches to drive market

- TABLE 39 TRANSDERMAL PATCHES AVAILABLE FOR TRANSDERMAL ESTROGEN THERAPY

- TABLE 40 TRANSDERMAL PATCHES MARKET FOR TRANSDERMAL ESTROGEN THERAPY, BY COUNTRY, 2021-2029 (USD MILLION)

- 8.5 CENTRAL NERVOUS SYSTEM DISORDERS

- 8.5.1 EASE OF USE, SIMPLE TREATMENT REGIMEN, AND CONTINUOUS DELIVERY OF DRUGS TO DRIVE ADOPTION

- TABLE 41 TRANSDERMAL PATCHES AVAILABLE FOR CENTRAL NERVOUS SYSTEM DISORDERS

- TABLE 42 TRANSDERMAL PATCHES MARKET FOR CENTRAL NERVOUS SYSTEM DISORDERS, BY COUNTRY, 2021-2029 (USD MILLION)

- 8.6 CARDIOVASCULAR DISEASES

- 8.6.1 AVAILABILITY OF ALTERNATIVE AND ADVANCED DRUG DELIVERY OPTIONS TO LIMIT MARKET GROWTH

- TABLE 43 TRANSDERMAL PATCHES AVAILABLE FOR CARDIOVASCULAR DISEASES

- TABLE 44 TRANSDERMAL PATCHES MARKET FOR CARDIOVASCULAR DISEASES, BY COUNTRY, 2021-2029 (USD MILLION)

- 8.7 OTHER APPLICATIONS

- TABLE 45 TRANSDERMAL PATCHES AVAILABLE FOR OTHER APPLICATIONS

- TABLE 46 TRANSDERMAL PATCHES MARKET FOR OTHER APPLICATIONS, BY COUNTRY, 2021-2029 (USD MILLION)

9 TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL

- 9.1 INTRODUCTION

- TABLE 47 TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- 9.2 HOSPITAL PHARMACIES

- 9.2.1 LARGEST DISTRIBUTION CHANNEL FOR TRANSDERMAL PATCHES

- TABLE 48 TRANSDERMAL PATCHES MARKET FOR HOSPITAL PHARMACIES, BY COUNTRY, 2021-2029 (USD MILLION)

- 9.3 RETAIL PHARMACIES

- 9.3.1 IMPROVING HEALTHCARE INFRASTRUCTURE TO DRIVE MARKET

- TABLE 49 TRANSDERMAL PATCHES MARKET FOR RETAIL PHARMACIES, BY COUNTRY, 2021-2029 (USD MILLION)

- 9.4 ONLINE PHARMACIES

- 9.4.1 FASTEST-GROWING SEGMENT DUE TO EASY ACCESSIBILITY TO MEDICATIONS

- TABLE 50 TRANSDERMAL PATCHES MARKET FOR ONLINE PHARMACIES, BY COUNTRY, 2021-2029 (USD MILLION)

10 TRANSDERMAL PATCHES MARKET, BY END USER

- 10.1 INTRODUCTION

- TABLE 51 TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 10.2 HOME CARE SETTINGS

- 10.2.1 RAPID GROWTH IN GERIATRIC POPULATION TO SUPPORT MARKET GROWTH

- TABLE 52 TRANSDERMAL PATCHES MARKET FOR HOME CARE SETTINGS, BY COUNTRY, 2021-2029 (USD MILLION)

- 10.3 HOSPITALS & CLINICS

- 10.3.1 INCREASING PREVALENCE OF CHRONIC DISEASES TO DRIVE MARKET

- TABLE 53 TRANSDERMAL PATCHES MARKET FOR HOSPITALS & CLINICS, BY COUNTRY, 2021-2029 (USD MILLION)

11 TRANSDERMAL PATCHES MARKET, BY REGION

- 11.1 INTRODUCTION

- TABLE 54 TRANSDERMAL PATCHES MARKET, BY REGION, 2021-2029 (USD MILLION)

- 11.2 NORTH AMERICA

- 11.2.1 IMPACT OF RECESSION ON NORTH AMERICAN TRANSDERMAL PATCHES MARKET

- FIGURE 36 NORTH AMERICA: TRANSDERMAL PATCHES MARKET SNAPSHOT

- TABLE 55 NORTH AMERICA: TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- TABLE 56 NORTH AMERICA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 57 NORTH AMERICA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 58 NORTH AMERICA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 59 NORTH AMERICA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 60 NORTH AMERICA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 61 NORTH AMERICA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 62 NORTH AMERICA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.2.2 US

- 11.2.2.1 Largest market for transdermal patches

- TABLE 63 US: MACROECONOMIC INDICATORS

- TABLE 64 US: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 65 US: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 66 US: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 67 US: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 68 US: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 69 US: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 70 US: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.2.3 CANADA

- 11.2.3.1 Rising funding for transdermal drug delivery research to drive market

- TABLE 71 CANADA: MACROECONOMIC INDICATORS

- TABLE 72 CANADA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 73 CANADA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 74 CANADA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 75 CANADA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 76 CANADA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 77 CANADA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 78 CANADA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.3 EUROPE

- 11.3.1 IMPACT OF RECESSION ON EUROPEAN TRANSDERMAL PATCHES MARKET

- TABLE 79 EUROPE: TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- TABLE 80 EUROPE: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 81 EUROPE: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 82 EUROPE: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 83 EUROPE: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 84 EUROPE: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 85 EUROPE: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 86 EUROPE: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.3.2 GERMANY

- 11.3.2.1 Favorable government policies to aid market growth

- TABLE 87 GERMANY: MACROECONOMIC INDICATORS

- TABLE 88 GERMANY: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 89 GERMANY: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 90 GERMANY: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 91 GERMANY: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 92 GERMANY: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 93 GERMANY: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 94 GERMANY: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.3.3 UK

- 11.3.3.1 Increasing funding for R&D of innovative transdermal technologies to drive market

- TABLE 95 UK: MACROECONOMIC INDICATORS

- TABLE 96 UK: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 97 UK: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 98 UK: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 99 UK: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 100 UK: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 101 UK: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 102 UK: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.3.4 FRANCE

- 11.3.4.1 Development of transdermal drug delivery systems by local players to support market growth

- TABLE 103 FRANCE: MACROECONOMIC INDICATORS

- TABLE 104 FRANCE: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 105 FRANCE: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 106 FRANCE: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 107 FRANCE: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 108 FRANCE: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 109 FRANCE: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 110 FRANCE: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.3.5 ITALY

- 11.3.5.1 High burden of lung cancer to propel market

- TABLE 111 ITALY: MACROECONOMIC INDICATORS

- TABLE 112 ITALY: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 113 ITALY: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 114 ITALY: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 115 ITALY: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 116 ITALY: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 117 ITALY: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 118 ITALY: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.3.6 SPAIN

- 11.3.6.1 Growing demand for self-care and personalized medicine to drive market

- TABLE 119 SPAIN: MACROECONOMIC INDICATORS

- TABLE 120 SPAIN: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 121 SPAIN: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 122 SPAIN: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 123 SPAIN: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 124 SPAIN: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 125 SPAIN: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 126 SPAIN: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.3.7 REST OF EUROPE

- TABLE 127 REST OF EUROPE: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 128 REST OF EUROPE: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 129 REST OF EUROPE: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 130 REST OF EUROPE: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 131 REST OF EUROPE: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 132 REST OF EUROPE: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL 2021-2029 (USD MILLION)

- TABLE 133 REST OF EUROPE: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.4 ASIA PACIFIC

- 11.4.1 IMPACT OF RECESSION ON ASIA PACIFIC TRANSDERMAL PATCHES MARKET

- FIGURE 37 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET SNAPSHOT

- TABLE 134 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- TABLE 135 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 136 ASIA PACIFIC: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 137 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 138 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 139 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 140 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 141 ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.4.2 CHINA

- 11.4.2.1 Large diabetic population to drive market

- TABLE 142 CHINA: MACROECONOMIC INDICATORS

- TABLE 143 CHINA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 144 CHINA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 145 CHINA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 146 CHINA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 147 CHINA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 148 CHINA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 149 CHINA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.4.3 JAPAN

- 11.4.3.1 Increasing number of product approvals and growing focus of local players on R&D of transdermal systems to support market growth

- TABLE 150 JAPAN: MACROECONOMIC INDICATORS

- TABLE 151 JAPAN: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 152 JAPAN: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 153 JAPAN: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 154 JAPAN: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 155 JAPAN: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 156 JAPAN: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 157 JAPAN: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.4.4 INDIA

- 11.4.4.1 Increasing focus on noninvasive methods of drug delivery to drive market

- TABLE 158 INDIA: MACROECONOMIC INDICATORS

- TABLE 159 INDIA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 160 INDIA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 161 INDIA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 162 INDIA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 163 INDIA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 164 INDIA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 165 INDIA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.4.5 SOUTH KOREA

- 11.4.5.1 Rising healthcare spending and increasing government initiatives to propel market

- TABLE 166 SOUTH KOREA: MACROECONOMIC INDICATORS

- TABLE 167 SOUTH KOREA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 168 SOUTH KOREA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 169 SOUTH KOREA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 170 SOUTH KOREA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 171 SOUTH KOREA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 172 SOUTH KOREA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 173 SOUTH KOREA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.4.6 AUSTRALIA

- 11.4.6.1 Increasing number of smokers to drive market

- TABLE 174 AUSTRALIA: MACROECONOMIC INDICATORS

- TABLE 175 AUSTRALIA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 176 AUSTRALIA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 177 AUSTRALIA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 178 AUSTRALIA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 179 AUSTRALIA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 180 AUSTRALIA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 181 AUSTRALIA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.4.7 REST OF ASIA PACIFIC

- TABLE 182 REST OF ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 183 REST OF ASIA PACIFIC: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 184 REST OF ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 185 REST OF ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 186 REST OF ASIA PACIFIC: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 187 REST OF ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 188 REST OF ASIA PACIFIC: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.5 LATIN AMERICA

- 11.5.1 IMPACT OF RECESSION ON TRANSDERMAL PATCHES MARKET IN LATIN AMERICA

- TABLE 189 LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY COUNTRY, 2021-2029 (USD MILLION)

- TABLE 190 LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 191 LATIN AMERICA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 192 LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 193 LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 194 LATIN AMERICA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 195 LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 196 LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.5.2 BRAZIL

- 11.5.2.1 High prevalence of diabetes to propel market

- TABLE 197 BRAZIL: KEY MACROINDICATORS

- TABLE 198 BRAZIL: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 199 BRAZIL: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 200 BRAZIL: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 201 BRAZIL: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 202 BRAZIL: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 203 BRAZIL: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 204 BRAZIL: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.5.3 MEXICO

- 11.5.3.1 Government investments to drive transdermal drug delivery production

- TABLE 205 MEXICO: KEY MACROINDICATORS

- TABLE 206 MEXICO: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 207 MEXICO: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 208 MEXICO: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 209 MEXICO: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 210 MEXICO: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 211 MEXICO: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 212 MEXICO: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.5.4 REST OF LATIN AMERICA

- TABLE 213 REST OF LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 214 REST OF LATIN AMERICA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 215 REST OF LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 216 REST OF LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 217 REST OF LATIN AMERICA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 218 REST OF LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 219 REST OF LATIN AMERICA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GOVERNMENT SUPPORT TO BOOST LOCAL PRODUCTION TO OFFER GROWTH OPPORTUNITIES FOR TRANSDERMAL PATCH MANUFACTURERS

- 11.6.2 IMPACT OF RECESSION ON TRANSDERMAL PATCHES MARKET IN MIDDLE EAST AND AFRICA

- TABLE 220 MIDDLE EAST & AFRICA: TRANSDERMAL PATCHES MARKET, BY PATCH TYPE, 2021-2029 (USD MILLION)

- TABLE 221 MIDDLE EAST & AFRICA: DRUG-IN-ADHESIVE TRANSDERMAL PATCHES MARKET, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 222 MIDDLE EAST & AFRICA: TRANSDERMAL PATCHES MARKET, BY ADHESIVE TYPE, 2021-2029 (USD MILLION)

- TABLE 223 MIDDLE EAST & AFRICA: TRANSDERMAL PATCHES MARKET, BY APPLICATION, 2021-2029 (USD MILLION)

- TABLE 224 MIDDLE EAST & AFRICA: TRANSDERMAL PATCHES MARKET FOR HORMONE REPLACEMENT THERAPY, BY TYPE, 2021-2029 (USD MILLION)

- TABLE 225 MIDDLE EAST & AFRICA: TRANSDERMAL PATCHES MARKET, BY DISTRIBUTION CHANNEL, 2021-2029 (USD MILLION)

- TABLE 226 MIDDLE EAST & AFRICA: TRANSDERMAL PATCHES MARKET, BY END USER, 2021-2029 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- TABLE 227 KEY DEVELOPMENTS IN TRANSDERMAL PATCHES MARKET (JANUARY 2020-OCTOBER 2023)

- 12.2 REVENUE ANALYSIS OF KEY MARKET PLAYERS

- FIGURE 38 REVENUE ANALYSIS OF KEY PLAYERS IN TRANSDERMAL PATCHES MARKET

- 12.3 MARKET SHARE ANALYSIS

- FIGURE 39 TRANSDERMAL PATCHES MARKET SHARE, BY KEY PLAYER, 2022

- 12.4 COMPANY FOOTPRINT

- 12.4.1 FOOTPRINT OF COMPANIES IN TRANSDERMAL PATCHES MARKET

- 12.4.2 PATCH TYPE FOOTPRINT

- 12.4.3 ADHESIVE TYPE FOOTPRINT

- 12.4.4 APPLICATION FOOTPRINT

- 12.4.5 DISTRIBUTION CHANNEL FOOTPRINT

- 12.4.6 END-USER FOOTPRINT

- 12.4.7 REGIONAL FOOTPRINT

- 12.5 TRANSDERMAL PATCHES MARKET: R&D EXPENDITURE

- FIGURE 40 R&D EXPENDITURE OF KEY PLAYERS IN TRANSDERMAL PATCHES MARKET (2021 VS. 2022)

- 12.6 COMPANY EVALUATION MATRIX

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- FIGURE 41 TRANSDERMAL PATCHES MARKET: COMPANY EVALUATION MATRIX, 2022

- 12.7 SME/STARTUP EVALUATION MATRIX

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 STARTING BLOCKS

- 12.7.3 RESPONSIVE COMPANIES

- 12.7.4 DYNAMIC COMPANIES

- FIGURE 42 TRANSDERMAL PATCHES MARKET: SME/STARTUP EVALUATION MATRIX

- 12.7.5 COMPETITIVE BENCHMARKING

- TABLE 228 TRANSDERMAL PATCHES MARKET: DETAILED LIST OF KEY STARTUP/SMES

- 12.8 COMPETITIVE SITUATION AND TRENDS

- 12.8.1 PRODUCT LAUNCHES

- TABLE 229 TRANSDERMAL PATCHES MARKET: PRODUCT LAUNCHES, JANUARY 2020-OCTOBER 2023

- 12.8.2 DEALS

- TABLE 230 TRANSDERMAL PATCHES MARKET: DEALS, JANUARY 2020-OCTOBER 2023

- 12.8.3 OTHER DEVELOPMENTS

- TABLE 231 TRANSDERMAL PATCHES MARKET: OTHER DEVELOPMENTS, JANUARY 2020-OCTOBER 2023

13 COMPANY PROFILES

- (Business overview, Products offered, Recent developments & MnM View)**

- 13.1 KEY PLAYERS

- 13.1.1 HISAMITSU PHARMACEUTICAL CO., INC.

- TABLE 232 HISAMITSU PHARMACEUTICAL CO., INC.: BUSINESS OVERVIEW

- FIGURE 43 HISAMITSU PHARMACEUTICAL CO., INC.: COMPANY SNAPSHOT (2022)

- 13.1.2 VIATRIS INC.

- TABLE 233 VIATRIS INC.: BUSINESS OVERVIEW

- FIGURE 44 VIATRIS INC.: COMPANY SNAPSHOT (2022)

- 13.1.3 NOVARTIS AG

- TABLE 234 NOVARTIS AG: BUSINESS OVERVIEW

- FIGURE 45 NOVARTIS AG: COMPANY SNAPSHOT (2022)

- 13.1.4 BOEHRINGER INGELHEIM INTERNATIONAL GMBH

- TABLE 235 BOEHRINGER INGELHEIM INTERNATIONAL GMBH: BUSINESS OVERVIEW

- FIGURE 46 BOEHRINGER INGELHEIM INTERNATIONAL GMBH: COMPANY SNAPSHOT (2022)

- 13.1.5 JOHNSON & JOHNSON

- TABLE 236 JOHNSON & JOHNSON: BUSINESS OVERVIEW

- FIGURE 47 JOHNSON & JOHNSON: COMPANY SNAPSHOT (2022)

- 13.1.6 UCB S.A.

- TABLE 237 UCB S.A.: BUSINESS OVERVIEW

- FIGURE 48 UCB S.A.: COMPANY SNAPSHOT (2022)

- 13.1.7 ENDO INTERNATIONAL PLC

- TABLE 238 ENDO INTERNATIONAL PLC: BUSINESS OVERVIEW

- FIGURE 49 ENDO INTERNATIONAL PLC: COMPANY SNAPSHOT (2022)

- 13.1.8 LUYE PHARMA GROUP

- TABLE 239 LUYE PHARMA GROUP: BUSINESS OVERVIEW

- FIGURE 50 LUYE PHARMA GROUP: COMPANY SNAPSHOT (2022)

- 13.1.9 ABBVIE INC.

- TABLE 240 ABBVIE INC.: BUSINESS OVERVIEW

- FIGURE 51 ABBVIE INC.: COMPANY SNAPSHOT (2022)

- 13.1.10 NITTO DENKO CORPORATION

- TABLE 241 NITTO DENKO CORPORATION: BUSINESS OVERVIEW

- FIGURE 52 NITTO DENKO CORPORATION: COMPANY SNAPSHOT (2022)

- 13.1.11 CIPLA INC.

- TABLE 242 CIPLA INC.: BUSINESS OVERVIEW

- FIGURE 53 CIPLA INC.: COMPANY SNAPSHOT (2022)

- 13.1.12 TEVA PHARMACEUTICAL INDUSTRIES LTD.

- TABLE 243 TEVA PHARMACEUTICAL INDUSTRIES LTD.: BUSINESS OVERVIEW

- FIGURE 54 TEVA PHARMACEUTICAL INDUSTRIES LTD.: COMPANY SNAPSHOT (2022)

- 13.1.13 AGILE THERAPEUTICS

- TABLE 244 AGILE THERAPEUTICS: BUSINESS OVERVIEW

- FIGURE 55 AGILE THERAPEUTICS: COMPANY SNAPSHOT (2022)

- 13.1.14 BAYER AG

- TABLE 245 BAYER AG: BUSINESS OVERVIEW

- FIGURE 56 BAYER AG: COMPANY SNAPSHOT (2022)

- 13.1.15 AMNEAL PHARMACEUTICALS LLC

- TABLE 246 AMNEAL PHARMACEUTICALS LLC: BUSINESS OVERVIEW

- FIGURE 57 AMNEAL PHARMACEUTICALS LLC: COMPANY SNAPSHOT (2022)

- 13.1.16 HIKMA PHARMACEUTICALS PLC

- TABLE 247 HIKMA PHARMACEUTICALS PLC: BUSINESS OVERVIEW

- FIGURE 58 HIKMA PHARMACEUTICALS PLC: COMPANY SNAPSHOT (2022)

- *Details on Business overview, Products offered, Recent developments & MnM View might not be captured in case of unlisted companies.

- 13.2 OTHER PLAYERS

- 13.2.1 ALVOGEN GROUP INC.

- TABLE 248 ALVOGEN GROUP INC.: COMPANY OVERVIEW

- 13.2.2 SPARSHA PHARMA INTERNATIONAL PVT. LTD.

- TABLE 249 SPARSHA PHARMA INTERNATIONAL PVT. LTD.: COMPANY OVERVIEW

- 13.2.3 IONTOPATCH

- TABLE 250 IONTOPATCH: COMPANY OVERVIEW

- 13.2.4 MEDHERANT LIMITED

- TABLE 251 MEDHERANT LIMITED: COMPANY OVERVIEW

- 13.2.5 ADHEXPHARMA

- TABLE 252 ADHEXPHARMA: COMPANY OVERVIEW

- 13.2.6 EVERNOW

- TABLE 253 EVERNOW: COMPANY OVERVIEW

- 13.2.7 LEAD CHEMICAL CO., LTD.

- TABLE 254 LEAD CHEMICAL CO., LTD.: COMPANY OVERVIEW

- 13.2.8 PURDUE PHARMA L.P.

- TABLE 255 PURDUE PHARMA L.P.: COMPANY OVERVIEW

- 13.2.9 MUNDIPHARMA INTERNATIONAL

- TABLE 256 MUNDIPHARMA INTERNATIONAL: COMPANY OVERVIEW

- 13.3 COMPANIES PROVIDING ADHESIVES FOR TRANSDERMAL PATCHES

- 13.3.1 WACKER CHEMIE AG

- 13.3.1.1 Business overview

- TABLE 257 WACKER CHEMIE AG: BUSINESS OVERVIEW

- FIGURE 59 WACKER CHEMIE AG: COMPANY SNAPSHOT (2022)

- 13.3.1.2 Products offered

- 13.3.2 ELKEM ASA

- 13.3.2.1 Business overview

- TABLE 258 ELKEM ASA: BUSINESS OVERVIEW

- FIGURE 60 ELKEM ASA: COMPANY SNAPSHOT (2022)

- 13.3.2.2 Products offered

- 13.3.3 DUPONT DE NEMOURS, INC.

- 13.3.3.1 Business overview

- TABLE 259 DUPONT DE NEMOURS, INC.: BUSINESS OVERVIEW

- FIGURE 61 DUPONT DE NEMOURS, INC.: COMPANY SNAPSHOT (2022)

- 13.3.3.2 Products offered

- 13.3.4 KATECHO, LLC

- TABLE 260 KATECHO, LLC: COMPANY OVERVIEW

- 13.3.5 POLYMER SCIENCE, INC.

- TABLE 261 POLYMER SCIENCE, INC.: COMPANY OVERVIEW

- 13.3.1 WACKER CHEMIE AG

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS