|

|

市場調査レポート

商品コード

1359920

金融クラウドの世界市場 (~2028年):提供区分 (ソリューション (財務予測・財務報告&分析・セキュリティ・GRC)・サービス)・用途・展開モデル、組織規模 (大企業・中小企業)・エンドユーザー・地域別Finance Cloud Market by Offering (Solutions (Financial Forecasting, Financial Reporting & Analysis, Security, GRC) and Services), Application, Deployment Model, Organization Size (Large Enterprises, SMEs), End User and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 金融クラウドの世界市場 (~2028年):提供区分 (ソリューション (財務予測・財務報告&分析・セキュリティ・GRC)・サービス)・用途・展開モデル、組織規模 (大企業・中小企業)・エンドユーザー・地域別 |

|

出版日: 2023年10月05日

発行: MarketsandMarkets

ページ情報: 英文 278 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

金融クラウドの市場規模は、2023年の1,356億米ドルから、予測期間中は14.6%のCAGRで推移し、2028年には2,681億米ドルの規模に成長すると予測されています。

デジタルサービス、コスト削減、拡張性、革新的技術へのアクセス、インダストリー4.0に対する需要の急増などの要因が同市場の成長機会をしh召しています。一方で、熟練の労働力の不足が市場成長の大きな課題となっています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2019-2028年 |

| 基準年 | 2022年 |

| 予測期間 | 2023-2028年 |

| 単位 | 金額 (米ドル) |

| 部門別 | 提供区分・用途・展開モデル・組織規模・エンドユーザー・地域別 |

| 対象地域 | 北米・欧州・アジア太平洋・ラテンアメリカ・中東&アフリカ |

ソリューション別で見ると、財務予測の部門が予測期間中に市場シェアを拡大する見通しです。財務予測ソリューションでは、クラウドベースの技術やツールを使って組織の将来の財務実績を予測します。このプロセスには、過去の財務データ、市場動向、経済指標、さまざまな財務指標を分析し、正確な収益、費用、利益、キャッシュフロー予測を作成することが含まれます。クラウドベースのプラットフォームは、さまざまなソースからの膨大な財務情報を管理するための、一元化されたスケーラブルな環境を提供します。リアルタイムのデータアクセス、自動化、高度な分析機能を提供することで、財務担当者は正確なレポートを作成し、詳細な財務分析を行い、意思決定をサポートする貴重な洞察を引き出すことができます。

用途別では、顧客管理の部門が予測期間中に最も高いCAGRを記録すると予測されています。金融クラウドにおける顧客管理では、クラウドベースの技術やツールを使用して、金融機関の顧客や顧客を効果的に監督し、やり取りします。これらのソリューションは、顧客の情報や取引を安全に管理するための一元化されたプラットフォームを提供します。クラウドベースの顧客管理システムには、顧客データの保存、連絡先管理、コミュニケーション追跡、口座履歴などの機能が含まれていることが多いです。クラウドの拡張性とアクセシビリティにより、金融機関はパーソナライズされた迅速な顧客サービスを提供し、顧客のオンボーディングを合理化し、顧客に財務情報へのリアルタイムアクセスを提供することができます。

当レポートでは、世界の金融クラウドの市場を調査し、市場概要、市場影響因子および市場機会の分析、技術・特許動向、ケーススタディ、法規制環境、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要・産業動向

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ケーススタディ分析

- エコシステム

- バリューチェーン分析

- 技術分析

- 価格分析

- ビジネスモデル分析

- 特許分析

- ポーターのファイブフォース分析

- 規則

- 主な会議とイベント

- カンファレンスおよびイベントの詳細リスト

- 新たな動向

- 主要なステークホルダーと購入基準

第6章 金融クラウド市場:提供区分別

- ソリューション

- 財務予測

- 財務報告・分析

- 安全

- ガバナンス・リスク・コンプライアンス (GRC)

- その他

- サービス

- プロフェッショナルサービス

- マネージドサービス

第7章 金融クラウド市場:用途別

- 収益管理

- 請求

- サブスクリプション管理

- 収益予測・分析

- その他

- 資産管理

- ポートフォリオ管理

- 財務計画

- リスク&コンプライアンス管理

- その他

- 口座管理

- クライアントオンボーディング

- 口座保守・サポート

- 口座分析・報告

- その他

- 顧客管理

- 顧客関係管理 (CRM)

- マーケティングオートメーション

- 顧客サポート&サービス

- その他

- その他

第8章 金融クラウド市場:組織規模別

- 大企業

- 中小企業

第9章 金融クラウド市場:導入モデル別

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

第10章 金融クラウド市場:エンドユーザー別

- 銀行

- 小売銀行および商業銀行

- 中央銀行

- 投資銀行

- 信用組合およびノンバンク金融会社

- 金融サービスプロバイダー

- アセット&ウェルス管理会社

- 決済処理会社

- その他

- 保険会社

- 生命保険会社

- 健康保険会社

- 損害保険 (P&C) 保険会社

- その他

第11章 金融クラウド市場:地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第12章 競合情勢

- 概要

- 主要企業の採用した戦略/有力企業

- 収益分析

- 企業の財務指標

- 主要参入企業のスナップショット

- 市場シェア分析

- ベンダー製品/ブランドの比較

- 企業評価マトリックス

- スタートアップ/中小企業の評価マトリックス

- 市場の主要な展開

第13章 企業プロファイル

- 主要企業

- MICROSOFT

- AWS

- IBM

- TENCENT CLOUD

- SALESFORCE

- ORACLE

- ALIBABA CLOUD

- WORKDAY

- SAP

- その他の企業

- HPE

- VMWARE

- CISCO

- HUAWEI

- SERVICENOW

- DXC TECHNOLOGY

- UNIT4

- SAGE GROUP

- SNOWFLAKE

- NUTANIX

- ACUMATICA

- RAPIDSCALE

- ATEMISCLOUD

- RAMBASE

- OVHCLOUD

- FREEAGENT

- FRESHBOOKS

- WAVE

- KASHOO

第14章 隣接市場および関連市場

第15章 付録

The Finance Cloud market size is expected to grow from USD 135.6 billion in 2023 to USD 268.1 billion by 2028 at a Compound Annual Growth Rate (CAGR) of 14.6% during the forecast period. The surge in demand for digital services, cost savings, scalability, access to innovative technologies, and Industry 4.0 offer opportunities to grow the Finance Cloud market. The lack of a skilled workforce poses a significant challenge to the growth of the Finance Cloud market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD) Million |

| Segments | By Offering, Application, Deployment Model, Organization Size, End User and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

"By deployment model, the private cloud segment to have the second highest growth rate during the forecast period."

A private cloud deployment model is a cloud computing environment exclusively used by a single organization or entity. Unlike public clouds, private clouds are not shared with other organizations and can be hosted on-premises or by a third-party cloud provider. Private clouds provide greater control, security, and customization than public clouds, making them ideal for organizations with specific data privacy, security, and compliance requirements. An example of a private cloud solution is VMware Cloud Foundation, which enables organizations to create a software-defined data center (SDDC) using their hardware or a partner's infrastructure. This private cloud offering includes virtualization, computing, storage, and network resources, all managed through VMware's software stack.

"By solutions, the financial forecasting segment is projected to witness a higher market share during the forecast period. "

Financial forecasting solutions involve predicting an organization's future financial performance using cloud-based technologies and tools. This process includes analyzing historical financial data, market trends, economic indicators, and various financial metrics to generate accurate revenues, expenses, profits, and cash flow projections. Cloud-based platforms offer a centralized and scalable environment for managing vast financial information from various sources. They provide real-time data access, automation, and advanced analytics capabilities; this enables finance professionals to generate accurate reports, perform in-depth financial analysis, and extract valuable insights to support decision-making. Cloud computing solutions for financial services are scalable and cost-effective, making it possible to store vast amounts of data generated by financial transactions, reports, and documents. These solutions offer features like data encryption, access controls, and versioning to ensure data security.

"By application, the customer management segment is projected to record the highest CAGR during the forecast period."

Managing customers in the finance cloud involves using cloud-based technologies and tools to effectively oversee and interact with clients or customers of financial institutions. These solutions provide a centralized platform for securely managing client information, interactions, and transactions. Cloud-based customer management systems often include features such as client data storage, contact management, communication tracking, and account history. With the scalability and accessibility of the cloud, financial institutions can offer personalized and responsive customer service, streamline client onboarding, and provide clients with real-time access to their financial information. The goal of customer management in the finance cloud is to enhance client satisfaction, foster long-term relationships, and provide clients with the tools and resources they need to manage their finances effectively.

The breakup of the profiles of the primary participants is below:

- By Company Type: Tier I: 22%, Tier II: 30%, and Tier III: 48%

- By Designation: C-Level Executives: 30%, Director Level: 45%, and *Others: 25%

- By Region: North America: 28%, Europe: 25%, Asia Pacific: 35%, **RoW: 12%

- Others include sales managers, marketing managers, and product managers

*RoW include Middle East & Africa and Latin America

Note: Tier 1 companies have revenues of more than USD 100 million; tier 2 companies' revenue ranges from USD 10 million to USD 100 million; and tier 3 companies' revenue is less than 10 million

Source: Secondary Literature, Expert Interviews, and MarketsandMarkets Analysis

Some of the key players operating in the Finance Cloud market are - IBM (US), SAP (Germany), Google (US), Microsoft (US), Salesforce (US), AWS (US), Oracle (US), Alibaba Cloud (China), Tencent Cloud (China), and Workday (US).

Research coverage:

The market study covers the Finance Cloud market across segments. It aims to estimate the market size and the growth potential of this market across different segments, such as offering, deployment model, organization size, end user, and region. It includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Reasons to buy this report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall Finance Cloud market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (increased adoption of cloud computing services due to rise in remote workforce count, personalized customer experience, requirement for disaster recovery and contingency plan), restraints (protection of Intellectual Property Rights (IPR), lack of appropriate technical knowledge and expertise), opportunities (increasing government initiatives boosting innovations and implementation of the offerings of financial cloud market, deployment of applications over cloud), and challenges (higher dependence on network, issues with interoperability and flexibility) influencing the growth of the Finance Cloud market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the Finance Cloud market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the Finance Cloud market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the Finance Cloud market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like AWS, IBM, Google, Salesforce, Microsoft, and SAP in the Finance Cloud market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY

- TABLE 1 USD EXCHANGE RATES, 2018-2022

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 FINANCE CLOUD MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- FIGURE 2 BREAKUP OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.1.2.2 Key industry insights

- 2.2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- FIGURE 3 FINANCE CLOUD MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 4 APPROACH 1 (SUPPLY SIDE): REVENUE OF SERVICES FROM FINANCE CLOUD VENDORS

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY - BOTTOM-UP APPROACH (SUPPLY SIDE): COLLECTIVE REVENUE OF FINANCE CLOUD VENDORS

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY - (SUPPLY SIDE): ILLUSTRATION OF VENDOR REVENUE ESTIMATION

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 2 (DEMAND SIDE): REVENUE GENERATED FROM FINANCE CLOUD OFFERINGS

- FIGURE 8 APPROACH 2 (DEMAND SIDE): REVENUE GENERATED FROM DIFFERENT SEGMENTS

- 2.4 MARKET FORECAST

- TABLE 2 FACTOR ANALYSIS

- 2.5 IMPACT OF RECESSION

- TABLE 3 RECESSION IMPACT

- 2.6 ASSUMPTIONS

- 2.7 LIMITATIONS

3 EXECUTIVE SUMMARY

- 3.1 OVERVIEW OF RECESSION IMPACT

- FIGURE 9 FINANCE CLOUD MARKET: RECESSION IMPACT

- FIGURE 10 TOP-GROWING SEGMENTS IN FINANCE CLOUD MARKET

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE GROWTH OPPORTUNITIES FOR KEY PLAYERS IN FINANCE CLOUD MARKET

- FIGURE 11 FOCUS ON ENHANCING ENTERPRISE CUSTOMER EXPERIENCE AND SIMPLIFYING INFORMATION TECHNOLOGY OPERATIONS WORKFLOW TO DRIVE ADOPTION OF FINANCE CLOUD

- 4.2 FINANCE CLOUD MARKET, BY OFFERING, 2023 VS. 2028

- FIGURE 12 SOLUTIONS SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- 4.3 FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023 VS. 2028

- FIGURE 13 PUBLIC CLOUD SEGMENT TO HOLD LARGEST MARKET SHARE IN 2023

- 4.4 FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023 VS. 2028

- FIGURE 14 LARGE ENTERPRISES SEGMENT TO HOLD LARGER MARKET SHARE IN 2023

- 4.5 FINANCE CLOUD MARKET, BY END USER, 2023 VS. 2028

- FIGURE 15 BANKS TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.6 FINANCE CLOUD MARKET: REGIONAL SCENARIO, 2023-2028

- FIGURE 16 ASIA PACIFIC TO EMERGE AS BEST MARKET FOR INVESTMENTS IN NEXT FIVE YEARS

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 17 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: FINANCE CLOUD MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Rising adoption of cloud computing services due to growing remote workforce count

- 5.2.1.2 Compliance with stringent industry regulations

- 5.2.1.3 Personalized customer experience

- 5.2.1.4 Need for disaster recovery and contingency plans

- 5.2.2 RESTRAINTS

- 5.2.2.1 Protection of Intellectual Property Rights (IPR)

- FIGURE 18 ENTERPRISE SECURITY ISSUES

- 5.2.2.2 Rise in new regulations and financial standards

- 5.2.2.3 Lack of technical knowledge and expertise

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing government initiatives

- 5.2.3.2 Evolution of AI and ML

- 5.2.3.3 Deployment of applications via cloud

- 5.2.4 CHALLENGES

- 5.2.4.1 High dependency on networks

- 5.2.4.2 Issues with interoperability and flexibility

- 5.2.4.3 Effective management of associated cost

- 5.3 CASE STUDY ANALYSIS

- 5.3.1 CASE STUDY 1: ORACLE HELPED FINANCIAL INSTITUTION TO BUILD UNIFIED PLATFORM

- 5.3.2 CASE STUDY 2: MICROSOFT RENOVATED BANKING ARCHITECTURE AND CUSTOMER UI/UX CAPABILITIES

- 5.3.3 CASE STUDY 3: HUAWEI ENABLED BFSI GIANT TO STREAMLINE OPERATIONS

- 5.3.4 CASE STUDY 4: CAPGEMINI ENABLED EFFECTIVE AND EFFICIENT AUTOMATION FOR CONSTRUCTION VENDOR

- 5.3.5 CASE STUDY 5: ALIBABA ENABLED OPTIMIZATION OF RESOURCES AND FLASH TURNAROUND TIME TO PSX

- 5.4 ECOSYSTEM

- FIGURE 19 FINANCE CLOUD MARKET: ECOSYSTEM

- TABLE 4 FINANCE CLOUD MARKET: COMPANIES AND THEIR ROLE IN ECOSYSTEM

- 5.5 VALUE CHAIN ANALYSIS

- FIGURE 20 FINANCE CLOUD MARKET: VALUE CHAIN

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 ARTIFICIAL INTELLIGENCE

- 5.6.2 BIG DATA

- 5.6.3 INTERNET OF THINGS

- 5.6.4 DATA ANALYTICS

- 5.6.5 MACHINE LEARNING

- 5.6.6 5G

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE TREND

- 5.8 FINANCE CLOUD MARKET: BUSINESS MODEL ANALYSIS

- FIGURE 21 BUSINESS MODEL: FINANCE CLOUD MARKET

- 5.9 PATENT ANALYSIS

- FIGURE 22 NUMBER OF PATENTS PUBLISHED, 2012-2023

- FIGURE 23 TOP FIVE PATENT OWNERS (GLOBAL)

- TABLE 5 TOP TEN PATENT OWNERS

- TABLE 6 PATENTS GRANTED TO VENDORS IN FINANCE CLOUD MARKET

- 5.10 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 24 FINANCE CLOUD MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 7 FINANCE CLOUD MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 THREAT OF NEW ENTRANTS

- 5.10.2 THREAT OF SUBSTITUTES

- 5.10.3 BARGAINING POWER OF SUPPLIERS

- 5.10.4 BARGAINING POWER OF BUYERS

- 5.10.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.11 REGULATIONS

- 5.11.1 NORTH AMERICA

- TABLE 8 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.2 EUROPE

- TABLE 9 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.3 ASIA PACIFIC

- TABLE 10 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.4 REST OF THE WORLD

- TABLE 11 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12 KEY CONFERENCES AND EVENTS IN 2023-2024

- 5.13 FINANCE CLOUD MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2023-2024

- 5.14 EMERGING TRENDS IN FINANCE CLOUD MARKET

- FIGURE 25 MAJOR YCC TRENDS TO DRIVE FUTURE REVENUE PROSPECTS IN FINANCE CLOUD MARKET

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS

- TABLE 12 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS (IN %)

- 5.15.2 BUYING CRITERIA

- FIGURE 27 KEY BUYING CRITERIA FOR TOP END USERS

- TABLE 13 KEY BUYING CRITERIA FOR TOP END USERS

6 FINANCE CLOUD MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: FINANCE CLOUD MARKET DRIVERS

- FIGURE 28 SERVICES SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 14 FINANCE CLOUD MARKET, BY OFFERING, 2019-2022 (USD MILLION)

- TABLE 15 FINANCE CLOUD MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- 6.2 SOLUTIONS

- FIGURE 29 SECURITY SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 16 FINANCE CLOUD MARKET, BY SOLUTION, 2019-2022 (USD MILLION)

- TABLE 17 FINANCE CLOUD MARKET, BY SOLUTION, 2023-2028 (USD MILLION)

- TABLE 18 SOLUTIONS: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 19 SOLUTIONS: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.2.1 FINANCIAL FORECASTING

- 6.2.1.1 Organizations to utilize financial forecasting to make data-driven decisions that can impact financial health positively

- TABLE 20 FINANCIAL FORECASTING: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 21 FINANCIAL FORECASTING: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.2.1.2 Budgeting & Planning

- 6.2.1.3 Cash Flow Forecasting

- 6.2.1.4 Revenue Forecasting

- 6.2.1.5 Other Financial Forecasting Solutions

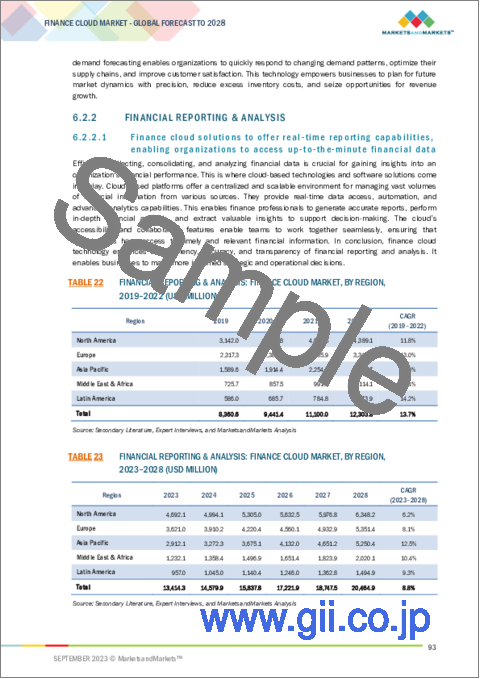

- 6.2.2 FINANCIAL REPORTING & ANALYSIS

- 6.2.2.1 Finance cloud solutions to offer real-time reporting capabilities, enabling organizations to access up-to-the-minute financial data

- TABLE 22 FINANCIAL REPORTING & ANALYSIS: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 23 FINANCIAL REPORTING & ANALYSIS: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.2.2.2 Financial Reporting

- 6.2.2.3 Business Intelligence (BI) & Analytics

- 6.2.2.4 Performance Analytics

- 6.2.2.5 Other Financial Reporting & Analysis Solutions

- 6.2.3 SECURITY

- 6.2.3.1 Financial organizations to adopt advanced security solutions to combat evolving cybersecurity threats

- TABLE 24 SECURITY: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 25 SECURITY: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.2.3.2 Data Encryption & Protection

- 6.2.3.3 Identity & Access Management (IAM)

- 6.2.3.4 Security Information & Event Management (SIEM)

- 6.2.3.5 Other Security Solutions

- 6.2.4 GOVERNANCE, RISK, AND COMPLIANCE (GRC)

- 6.2.4.1 GRC solutions to enable organizations to stay up-to-date with regulatory changes and streamline compliance efforts

- TABLE 26 GOVERNANCE, RISK, AND COMPLIANCE (GRC): FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 27 GOVERNANCE, RISK, AND COMPLIANCE (GRC): FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.2.4.2 Risk Management

- 6.2.4.3 Compliance Management

- 6.2.4.4 Audit Management

- 6.2.4.5 Other GRC Solutions

- 6.2.5 OTHER SOLUTIONS

- TABLE 28 OTHER SOLUTIONS: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 29 OTHER SOLUTIONS: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3 SERVICES

- FIGURE 30 MANAGED SERVICES SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 30 FINANCE CLOUD MARKET, BY SERVICE, 2019-2022 (USD MILLION)

- TABLE 31 FINANCE CLOUD MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- TABLE 32 SERVICES: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 33 SERVICES: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3.1 PROFESSIONAL SERVICES

- 6.3.1.1 Lack of in-house expertise and increasing complexity of cloud ecosystems to fuel demand for professional services

- TABLE 34 PROFESSIONAL SERVICES: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 35 PROFESSIONAL SERVICES: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3.1.2 Consulting

- 6.3.1.3 Deployment & Integration

- 6.3.1.4 Training & Support

- 6.3.2 MANAGED SERVICES

- 6.3.2.1 Managed services to enable financial organizations to focus on core competencies instead of managing complex IT infrastructure

- TABLE 36 MANAGED SERVICES: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 37 MANAGED SERVICES: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3.2.2 Managed Cloud Infrastructure Services

- 6.3.2.3 Managed Network Services

- 6.3.2.4 Managed Security Services

- 6.3.2.5 Other Managed Services

7 FINANCE CLOUD MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.1.1 APPLICATION: FINANCE CLOUD MARKET DRIVERS

- FIGURE 31 CUSTOMER MANAGEMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 38 FINANCE CLOUD MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 39 FINANCE CLOUD MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 7.2 REVENUE MANAGEMENT

- 7.2.1 BUSINESSES INCREASINGLY RELYING ON DATA-DRIVEN REVENUE MANAGEMENT TO INCREASE PROFITABILITY AND COMPETITIVENESS

- TABLE 40 REVENUE MANAGEMENT: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 41 REVENUE MANAGEMENT: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.2.2 BILLING & INVOICING

- 7.2.3 SUBSCRIPTION MANAGEMENT

- 7.2.4 REVENUE FORECASTING & ANALYSIS

- 7.2.5 OTHER REVENUE MANAGEMENT APPLICATIONS

- 7.3 WEALTH MANAGEMENT

- 7.3.1 CLIENTS' DEMAND FOR TAILORED INVESTMENT STRATEGIES AND FINANCIAL ADVICE TO DRIVE GROWTH OF WEALTH MANAGEMENT

- TABLE 42 WEALTH MANAGEMENT: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 43 WEALTH MANAGEMENT: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.3.2 PORTFOLIO MANAGEMENT

- 7.3.3 FINANCIAL PLANNING

- 7.3.4 RISK & COMPLIANCE MANAGEMENT

- 7.3.5 OTHER WEALTH MANAGEMENT APPLICATIONS

- 7.4 ACCOUNT MANAGEMENT

- 7.4.1 DEMAND FOR MORE CONVENIENT AND SELF-SERVICE ACCOUNT MANAGEMENT WITH INCREASING DIGITALIZATION OF FINANCIAL SERVICES TO DRIVE GROWTH

- TABLE 44 ACCOUNT MANAGEMENT: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 45 ACCOUNT MANAGEMENT: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.4.2 CLIENT ONBOARDING

- 7.4.3 ACCOUNT MAINTENANCE & SUPPORT

- 7.4.4 ACCOUNT ANALYTICS & REPORTING

- 7.4.5 OTHER ACCOUNT MANAGEMENT APPLICATIONS

- 7.5 CUSTOMER MANAGEMENT

- 7.5.1 CUSTOMER EXPECTATIONS FOR SEAMLESS INTERACTIONS WITH FINANCIAL INSTITUTIONS TO DRIVE GROWTH OF CUSTOMER MANAGEMENT

- TABLE 46 CUSTOMER MANAGEMENT: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 47 CUSTOMER MANAGEMENT: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.5.2 CUSTOMER RELATIONSHIP MANAGEMENT (CRM)

- 7.5.3 MARKETING AUTOMATION

- 7.5.4 CUSTOMER SUPPORT & SERVICE

- 7.5.5 OTHER CUSTOMER MANAGEMENT APPLICATIONS

- 7.6 OTHER APPLICATIONS

- TABLE 48 OTHER APPLICATIONS: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 49 OTHER APPLICATIONS: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

8 FINANCE CLOUD MARKET, BY ORGANIZATION SIZE

- 8.1 INTRODUCTION

- 8.1.1 ORGANIZATION SIZE: FINANCE CLOUD MARKET DRIVERS

- FIGURE 32 SMES TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 50 FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 51 FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 8.2 LARGE ENTERPRISES

- 8.2.1 RISING DIGITAL TRANSFORMATION TO MODERNIZE OPERATIONS AND STAY COMPETITIVE TO DRIVE FINANCE CLOUD ADOPTION

- TABLE 52 LARGE ENTERPRISES: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 53 LARGE ENTERPRISES: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.3 SMALL AND MEDIUM-SIZED ENTERPRISES

- 8.3.1 SMES TO ADOPT FINANCE CLOUD SOLUTIONS DUE TO AVAILABILITY OF COST-EFFECTIVE SCALABILITY OPTIONS

- TABLE 54 SMES: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 55 SMES: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

9 FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL

- 9.1 INTRODUCTION

- 9.1.1 DEPLOYMENT MODEL: FINANCE CLOUD MARKET DRIVERS

- FIGURE 33 HYBRID CLOUD SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 56 FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 57 FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- 9.2 PUBLIC CLOUD

- 9.2.1 PAY-AS-YOU-GO PRICING MODEL OF PUBLIC CLOUD TO HELP CONTROL EXPENSES AND IMPROVE BUDGET MANAGEMENT

- TABLE 58 PUBLIC CLOUD: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 59 PUBLIC CLOUD: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3 PRIVATE CLOUD

- 9.3.1 ABILITY TO CUSTOMIZE SECURITY MEASURES AND COMPLIANCE CONTROLS TO MEET INDUSTRY-SPECIFIC AND REGIONAL REQUIREMENTS TO DRIVE GROWTH

- TABLE 60 PRIVATE CLOUD: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 61 PRIVATE CLOUD: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.4 HYBRID CLOUD

- 9.4.1 FINANCIAL INSTITUTIONS TO UTILIZE HYBRID CLOUD MODEL TO SEGMENT AND PRIORITIZE DATA TO REDUCE STORAGE COST

- TABLE 62 HYBRID CLOUD: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 63 HYBRID CLOUD: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

10 FINANCE CLOUD MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.1.1 END USER: FINANCE CLOUD MARKET DRIVERS

- FIGURE 34 INSURANCE COMPANIES TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 64 FINANCE CLOUD MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 65 FINANCE CLOUD MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.2 BANKS

- 10.2.1 BANKS ADOPT FINANCE CLOUD TO REDUCE OPERATIONAL COSTS WHILE MAINTAINING SERVICE QUALITY

- TABLE 66 BANKS: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 67 BANKS: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.2.2 RETAIL & COMMERCIAL BANKS

- 10.2.3 CENTRAL BANKS

- 10.2.4 INVESTMENT BANKS

- 10.2.5 CREDIT UNIONS & NON-BANKING FINANCIAL COMPANIES

- 10.3 FINANCIAL SERVICE PROVIDERS

- 10.3.1 FINANCE CLOUD TO ENABLE FINANCIAL SERVICE PROVIDERS TO SCALE UP RESOURCES DURING PEAK PERIODS AND DOWN DURING SLOWER TIMES

- TABLE 68 FINANCIAL SERVICE PROVIDERS: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 69 FINANCIAL SERVICE PROVIDERS: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.3.2 ASSET & WEALTH MANAGEMENT COMPANIES

- 10.3.3 PAYMENT PROCESSING COMPANIES

- 10.3.4 OTHER FINANCIAL SERVICE PROVIDERS

- 10.4 INSURANCE COMPANIES

- 10.4.1 FINANCE CLOUD TO ENHANCE CUSTOMER EXPERIENCES, STREAMLINE CLAIMS PROCESSING, AND OFFER INNOVATIVE INSURANCE PRODUCTS

- TABLE 70 INSURANCE COMPANIES: FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 71 INSURANCE COMPANIES: FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.4.2 LIFE INSURANCE COMPANIES

- 10.4.3 HEALTH INSURANCE COMPANIES

- 10.4.4 PROPERTY & CASUALTY (P&C) INSURANCE COMPANIES

- 10.4.5 OTHER INSURANCE COMPANIES

11 FINANCE CLOUD MARKET, BY REGION

- 11.1 INTRODUCTION

- FIGURE 35 ASIA PACIFIC TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 72 FINANCE CLOUD MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 73 FINANCE CLOUD MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: FINANCE CLOUD MARKET DRIVERS

- 11.2.2 NORTH AMERICA: RECESSION IMPACT

- FIGURE 36 NORTH AMERICA: MARKET SNAPSHOT

- TABLE 74 NORTH AMERICA: FINANCE CLOUD MARKET, BY OFFERING, 2019-2022 (USD MILLION)

- TABLE 75 NORTH AMERICA: FINANCE CLOUD MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- TABLE 76 NORTH AMERICA: FINANCE CLOUD MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 77 NORTH AMERICA: FINANCE CLOUD MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 78 NORTH AMERICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 79 NORTH AMERICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- TABLE 80 NORTH AMERICA: FINANCE CLOUD MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 81 NORTH AMERICA: FINANCE CLOUD MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 82 NORTH AMERICA: FINANCE CLOUD MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 83 NORTH AMERICA: FINANCE CLOUD MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.2.3 US

- 11.2.3.1 Convergence of finance cloud with IoT to encourage US service providers to scale

- TABLE 84 US: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 85 US: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 86 US: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 87 US: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.2.4 CANADA

- 11.2.4.1 Emerging startups to provide innovative platforms and solutions catering to Canadian market

- TABLE 88 CANADA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 89 CANADA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 90 CANADA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 91 CANADA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.3 EUROPE

- 11.3.1 EUROPE: FINANCE CLOUD MARKET DRIVERS

- 11.3.2 EUROPE: RECESSION IMPACT

- TABLE 92 EUROPE: FINANCE CLOUD MARKET, BY OFFERING, 2019-2022 (USD MILLION)

- TABLE 93 EUROPE: FINANCE CLOUD MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- TABLE 94 EUROPE: FINANCE CLOUD MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 95 EUROPE: FINANCE CLOUD MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 96 EUROPE: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 97 EUROPE: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- TABLE 98 EUROPE: FINANCE CLOUD MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 99 EUROPE: FINANCE CLOUD MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 100 EUROPE: FINANCE CLOUD MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 101 EUROPE: FINANCE CLOUD MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.3.3 UK

- 11.3.3.1 Companies in UK to adopt finance cloud solutions to enhance operational efficiency

- TABLE 102 UK: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 103 UK: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 104 UK: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 105 UK: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.3.4 GERMANY

- 11.3.4.1 German finance cloud and telecom companies to witness increased collaborations to build robust finance cloud solutions

- TABLE 106 GERMANY: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 107 GERMANY: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 108 GERMANY: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 109 GERMANY: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.3.5 FRANCE

- 11.3.5.1 Huge investments by global finance cloud providers because of changing customer behavior to drive growth in France

- TABLE 110 FRANCE: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 111 FRANCE: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 112 FRANCE: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 113 FRANCE: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.3.6 REST OF EUROPE

- TABLE 114 REST OF EUROPE: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 115 REST OF EUROPE: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 116 REST OF EUROPE: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 117 REST OF EUROPE: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: FINANCE CLOUD MARKET DRIVERS

- 11.4.2 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 37 ASIA PACIFIC: MARKET SNAPSHOT

- TABLE 118 ASIA PACIFIC: FINANCE CLOUD MARKET, BY OFFERING, 2019-2022 (USD MILLION)

- TABLE 119 ASIA PACIFIC: FINANCE CLOUD MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- TABLE 120 ASIA PACIFIC: FINANCE CLOUD MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 121 ASIA PACIFIC: FINANCE CLOUD MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 122 ASIA PACIFIC: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 123 ASIA PACIFIC: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- TABLE 124 ASIA PACIFIC: FINANCE CLOUD MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 125 ASIA PACIFIC: FINANCE CLOUD MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 126 ASIA PACIFIC: FINANCE CLOUD MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 127 ASIA PACIFIC: FINANCE CLOUD MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.4.3 CHINA

- 11.4.3.1 Adoption of finance cloud in China to help achieve resiliency and scalability

- TABLE 128 CHINA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 129 CHINA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 130 CHINA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 131 CHINA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.4.4 JAPAN

- 11.4.4.1 Technology providers in Japan to introduce cutting-edge finance cloud technologies

- TABLE 132 JAPAN: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 133 JAPAN: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 134 JAPAN: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 135 JAPAN: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.4.5 INDIA

- 11.4.5.1 Cloud-computing for financial services to enhance capabilities for Indian market

- TABLE 136 INDIA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 137 INDIA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 138 INDIA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 139 INDIA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.4.6 REST OF ASIA PACIFIC

- TABLE 140 REST OF ASIA PACIFIC: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 141 REST OF ASIA PACIFIC: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 142 REST OF ASIA PACIFIC: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 143 REST OF ASIA PACIFIC: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET DRIVERS

- 11.5.2 MIDDLE EAST & AFRICA: RECESSION IMPACT

- TABLE 144 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY OFFERING, 2019-2022 (USD MILLION)

- TABLE 145 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- TABLE 146 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY SOLUTION, 2019-2022 (USD MILLION)

- TABLE 147 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY SOLUTION, 2023-2028 (USD MILLION)

- TABLE 148 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY SERVICE, 2019-2022 (USD MILLION)

- TABLE 149 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY SERVICE, 2023-2028 (USD MILLION)

- TABLE 150 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 151 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 152 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 153 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 154 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 155 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- TABLE 156 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 157 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 158 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 159 MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.5.3 SAUDI ARABIA

- 11.5.3.1 Increase in purchasing power and inclination toward advanced technologies to propel market growth in KSA

- TABLE 160 SAUDI ARABIA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 161 SAUDI ARABIA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 162 SAUDI ARABIA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 163 SAUDI ARABIA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.5.4 UAE

- 11.5.4.1 IT resource deployment, intelligent storage services, and remote monitoring capabilities drive adoption of finance cloud in UAE

- TABLE 164 UAE: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 165 UAE: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 166 UAE: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 167 UAE: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.5.5 REST OF MIDDLE EAST & AFRICA

- TABLE 168 REST OF MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 169 REST OF MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 170 REST OF MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 171 REST OF MIDDLE EAST & AFRICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.6 LATIN AMERICA

- 11.6.1 LATIN AMERICA: FINANCE CLOUD MARKET DRIVERS

- 11.6.2 LATIN AMERICA: RECESSION IMPACT

- TABLE 172 LATIN AMERICA: FINANCE CLOUD MARKET, BY OFFERING, 2019-2022 (USD MILLION)

- TABLE 173 LATIN AMERICA: FINANCE CLOUD MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- TABLE 174 LATIN AMERICA: FINANCE CLOUD MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 175 LATIN AMERICA: FINANCE CLOUD MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 176 LATIN AMERICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 177 LATIN AMERICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- TABLE 178 LATIN AMERICA: FINANCE CLOUD MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 179 LATIN AMERICA: FINANCE CLOUD MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 180 LATIN AMERICA: FINANCE CLOUD MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 181 LATIN AMERICA: FINANCE CLOUD MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.6.3 BRAZIL

- 11.6.3.1 Rising technology assimilation among enterprises and consumers to present significant opportunity for Brazil

- TABLE 182 BRAZIL: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 183 BRAZIL: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 184 BRAZIL: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 185 BRAZIL: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.6.4 MEXICO

- 11.6.4.1 Migration of applications and IT infrastructure to cloud to drive demand for finance cloud solutions in Mexico

- TABLE 186 MEXICO: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 187 MEXICO: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 188 MEXICO: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 189 MEXICO: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- 11.6.5 REST OF LATIN AMERICA

- TABLE 190 REST OF LATIN AMERICA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2019-2022 (USD MILLION)

- TABLE 191 REST OF LATIN AMERICA: FINANCE CLOUD MARKET, BY DEPLOYMENT MODEL, 2023-2028 (USD MILLION)

- TABLE 192 REST OF LATIN AMERICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2019-2022 (USD MILLION)

- TABLE 193 REST OF LATIN AMERICA: FINANCE CLOUD MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 STRATEGIES ADOPTED BY KEY PLAYERS/RIGHT TO WIN

- TABLE 194 OVERVIEW OF STRATEGIES ADOPTED BY KEY FINANCE CLOUD VENDORS

- 12.3 REVENUE ANALYSIS

- FIGURE 38 HISTORICAL FIVE-YEAR REVENUE ANALYSIS OF LEADING PLAYERS, 2018-2022 (USD MILLION)

- 12.4 FINANCIAL METRICS OF COMPANIES

- FIGURE 39 TRADING COMPARABLES, 2023 (EV/EBITDA)

- 12.5 GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS

- FIGURE 40 FINANCE CLOUD MARKET: GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS, 2022

- 12.6 MARKET SHARE ANALYSIS

- FIGURE 41 FINANCE CLOUD MARKET SHARE ANALYSIS, 2022

- TABLE 195 FINANCE CLOUD MARKET: DEGREE OF COMPETITION

- 12.7 FINANCE CLOUD MARKET: VENDOR PRODUCTS/BRANDS COMPARISON

- TABLE 196 VENDOR PRODUCTS/BRANDS COMPARISON

- 12.8 COMPANY EVALUATION MATRIX

- FIGURE 42 COMPANY EVALUATION MATRIX FOR KEY PLAYERS: CRITERIA WEIGHTAGE

- 12.8.1 STARS

- 12.8.2 EMERGING LEADERS

- 12.8.3 PERVASIVE PLAYERS

- 12.8.4 PARTICIPANTS

- FIGURE 43 FINANCE CLOUD MARKET: COMPANY EVALUATION MATRIX, 2022 (KEY PLAYERS)

- 12.8.5 COMPANY PRODUCT FOOTPRINT ANALYSIS

- TABLE 197 GLOBAL COMPANY FOOTPRINT

- 12.9 STARTUP/SME EVALUATION MATRIX

- FIGURE 44 STARTUP/SME EVALUATION MATRIX: CRITERIA WEIGHTAGE

- 12.9.1 PROGRESSIVE COMPANIES

- 12.9.2 RESPONSIVE COMPANIES

- 12.9.3 DYNAMIC COMPANIES

- 12.9.4 STARTING BLOCKS

- FIGURE 45 FINANCE CLOUD MARKET: STARTUP/SME EVALUATION MATRIX, 2022

- 12.9.5 COMPETITIVE BENCHMARKING

- TABLE 198 FINANCE CLOUD MARKET: DETAILED LIST OF KEY STARTUP/SMES

- TABLE 199 STARTUP/SME FOOTPRINT

- 12.10 KEY MARKET DEVELOPMENTS

- 12.10.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 200 PRODUCT LAUNCHES AND ENHANCEMENTS, 2021-2023

- 12.10.2 DEALS

- TABLE 201 DEALS, 2021-2023

13 COMPANY PROFILES

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS

(Business Overview, Products/Solutions/Services offered, Recent Developments, MnM View)**

- 13.2.1 MICROSOFT

- TABLE 202 MICROSOFT: BUSINESS OVERVIEW

- FIGURE 46 MICROSOFT: COMPANY SNAPSHOT

- TABLE 203 MICROSOFT: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 204 MICROSOFT: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 205 MICROSOFT: DEALS

- 13.2.2 GOOGLE

- TABLE 206 GOOGLE: BUSINESS OVERVIEW

- FIGURE 47 GOOGLE: COMPANY SNAPSHOT

- TABLE 207 GOOGLE: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 208 GOOGLE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 209 GOOGLE: DEALS

- 13.2.3 AWS

- TABLE 210 AWS: BUSINESS OVERVIEW

- FIGURE 48 AWS: COMPANY SNAPSHOT

- TABLE 211 AWS: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 212 AWS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 213 AWS: DEALS

- 13.2.4 IBM

- TABLE 214 IBM: BUSINESS OVERVIEW

- FIGURE 49 IBM: COMPANY SNAPSHOT

- TABLE 215 IBM: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 216 IBM: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 217 IBM: DEALS

- 13.2.5 TENCENT CLOUD

- TABLE 218 TENCENT CLOUD: BUSINESS OVERVIEW

- FIGURE 50 TENCENT CLOUD: COMPANY SNAPSHOT

- TABLE 219 TENCENT CLOUD: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 220 TENCENT CLOUD: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 221 TENCENT CLOUD: DEALS

- 13.2.6 SALESFORCE

- TABLE 222 SALESFORCE: BUSINESS OVERVIEW

- FIGURE 51 SALESFORCE: COMPANY SNAPSHOT

- TABLE 223 SALESFORCE: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 224 SALESFORCE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 225 SALESFORCE: DEALS

- 13.2.7 ORACLE

- TABLE 226 ORACLE: BUSINESS OVERVIEW

- FIGURE 52 ORACLE: COMPANY SNAPSHOT

- TABLE 227 ORACLE: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 228 ORACLE: PRODUCT LAUNCHES AND ENHANCEMENTS

- 13.2.8 ALIBABA CLOUD

- TABLE 229 ALIBABA CLOUD: BUSINESS OVERVIEW

- FIGURE 53 ALIBABA CLOUD: COMPANY SNAPSHOT

- TABLE 230 ALIBABA CLOUD: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 231 ALIBABA CLOUD: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 232 ALIBABA CLOUD: DEALS

- 13.2.9 WORKDAY

- TABLE 233 WORKDAY: BUSINESS OVERVIEW

- FIGURE 54 WORKDAY: COMPANY SNAPSHOT

- TABLE 234 WORKDAY: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 235 WORKDAY: DEALS

- 13.2.10 SAP

- TABLE 236 SAP: BUSINESS OVERVIEW

- FIGURE 55 SAP: COMPANY SNAPSHOT

- TABLE 238 SAP: PRODUCT LAUNCHES AND ENHANCEMENTS

- *Details on Business Overview, Products/Solutions/Services offered, Recent Developments, MnM View might not be captured in case of unlisted companies.

- 13.3 OTHER COMPANIES

- 13.3.1 HPE

- 13.3.2 VMWARE

- 13.3.3 CISCO

- 13.3.4 HUAWEI

- 13.3.5 SERVICENOW

- 13.3.6 DXC TECHNOLOGY

- 13.3.7 UNIT4

- 13.3.8 SAGE GROUP

- 13.3.9 SNOWFLAKE

- 13.3.10 NUTANIX

- 13.3.11 ACUMATICA

- 13.3.12 RAPIDSCALE

- 13.3.13 ATEMISCLOUD

- 13.3.14 RAMBASE

- 13.3.15 OVHCLOUD

- 13.3.16 FREEAGENT

- 13.3.17 FRESHBOOKS

- 13.3.18 WAVE

- 13.3.19 KASHOO

14 ADJACENT AND RELATED MARKETS

- 14.1 INTRODUCTION

- 14.1.1 RELATED MARKETS

- 14.2 CLOUD COMPUTING MARKET

- TABLE 239 CLOUD COMPUTING MARKET, BY SERVICE MODEL, 2017-2021 (USD BILLION)

- TABLE 240 CLOUD COMPUTING MARKET, BY SERVICE MODEL, 2022-2027 (USD BILLION)

- TABLE 241 CLOUD COMPUTING MARKET, BY IAAS, 2017-2021 (USD BILLION)

- TABLE 242 CLOUD COMPUTING MARKET, BY IAAS, 2022-2027 (USD BILLION)

- TABLE 243 CLOUD COMPUTING MARKET, BY PAAS, 2017-2021 (USD BILLION)

- TABLE 244 CLOUD COMPUTING MARKET, BY PAAS, 2022-2027 (USD BILLION)

- TABLE 245 CLOUD COMPUTING MARKET, BY SAAS, 2017-2021 (USD BILLION)

- TABLE 246 CLOUD COMPUTING MARKET, BY SAAS, 2022-2027 (USD BILLION)

- TABLE 247 CLOUD COMPUTING MARKET, BY DEPLOYMENT MODEL, 2017-2021 (USD BILLION)

- TABLE 248 CLOUD COMPUTING MARKET, BY DEPLOYMENT MODEL, 2022-2027 (USD BILLION)

- TABLE 249 CLOUD COMPUTING MARKET, BY ORGANIZATION SIZE, 2017-2021 (USD BILLION)

- TABLE 250 CLOUD COMPUTING MARKET, BY ORGANIZATION SIZE, 2022-2027 (USD BILLION)

- TABLE 251 CLOUD COMPUTING MARKET, BY VERTICAL, 2017-2021 (USD BILLION)

- TABLE 252 CLOUD COMPUTING MARKET, BY VERTICAL, 2022-2027 (USD BILLION)

- TABLE 253 CLOUD COMPUTING MARKET, BY REGION, 2017-2021 (USD BILLION)

- TABLE 254 CLOUD COMPUTING MARKET, BY REGION, 2022-2027 (USD BILLION)

- 14.3 FINANCIAL ANALYTICS MARKET

- TABLE 255 FINANCIAL ANALYTICS MARKET, BY COMPONENT, 2016-2023 (USD MILLION)

- TABLE 256 FINANCIAL ANALYTICS MARKET, BY APPLICATION, 2016-2023 (USD MILLION)

- TABLE 257 FINANCIAL ANALYTICS MARKET, BY DEPLOYMENT MODEL, 2016-2023 (USD MILLION)

- TABLE 258 FINANCIAL ANALYTICS MARKET, BY ORGANIZATION SIZE, 2016-2023 (USD MILLION)

- TABLE 259 FINANCIAL ANALYTICS MARKET, BY VERTICAL, 2016-2023 (USD MILLION)

- TABLE 260 FINANCIAL ANALYTICS MARKET, BY REGION, 2016-2023 (USD MILLION)

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS