|

|

市場調査レポート

商品コード

1350665

塩素化ポリ塩化ビニル (CPVC) の世界市場 (~2028年):グレード (射出・押出)・形状 (ペレット・粉末)・販売チャネル (直接販売・間接販売)・製造プロセス・エンドユーザー産業 (住宅・商用・産業用)・地域別Chlorinated Polyvinyl Chloride Market by Grade (Injection, Extrusion), Form (Pellet, Powder), Sales Channel (Direct Sales, Indirect Sales), Production Process, End-use Industry( Residential, Commercial, Industrial), & Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 塩素化ポリ塩化ビニル (CPVC) の世界市場 (~2028年):グレード (射出・押出)・形状 (ペレット・粉末)・販売チャネル (直接販売・間接販売)・製造プロセス・エンドユーザー産業 (住宅・商用・産業用)・地域別 |

|

出版日: 2023年09月20日

発行: MarketsandMarkets

ページ情報: 英文 236 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

塩素化ポリ塩化ビニル (CPVC) の市場規模は、2022年の16億米ドルから、予測期間中は11.1%のCAGRで推移し、2028年には27億米ドルの規模に成長すると予測されています。

同市場の成長は、配管システム、防火、化学・産業機器、その他の最終用途からのCPVC需要の増加が牽引しています。CPVCの需要においては、既存の規制問題やリサイクルを取り巻く環境問題が課題となっていましたが、2021年には回復を示しています。建設、工業、その他の業界がパンデミックの影響から回復し、製造活動を再開しつつあるため、CPVCの需要が伸びています。

グレード別で見ると、押出グレードの部門が金額と数量の両面で最速成長を示しており、予測期間中は最大のCAGRを記録すると予測されています。

また、製造プロセス別では、固相法の部門が金額・数量ともに最も急成長しています。固相法では、塩素化プロセスをよりよく制御することができ、さまざまな用途に適した特性を持つCPVCを製造することができます。

当レポートでは、世界の塩素化ポリ塩化ビニル (CPVC) の市場を調査し、市場概要、市場影響因子および市場機会の分析、技術・特許の動向、ケーススタディ、法規制環境、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ポーターのファイブフォース分析

- サプライチェーン分析

- 価格分析

- 平均販売価格:用途別

- 平均販売価格:地域別

- 主要ステークホルダーと購入基準

- 技術分析

- エコシステム

- バリューチェーン分析

- ケーススタディ分析

- 顧客の事業に影響を与える動向とディスラプション

- 輸出入シナリオ

- 規制状況

- 主要な会議とイベント

- 特許分析

第6章 塩素化ポリ塩化ビニル (CPVC) 市場:製造プロセス別

- 水懸濁法

- 溶剤法

- 固相法

第7章 塩素化ポリ塩化ビニル (CPVC) 市場:形状別

- ペレット

- 粉末

第8章 塩素化ポリ塩化ビニル (CPVC) 市場:グレード別

- 射出グレード

- 押出グレード

第9章 塩素化ポリ塩化ビニル (CPVC) 市場:販売チャネル別

- 直接販売

- 間接販売

第10章 塩素化ポリ塩化ビニル (CPVC) 市場:用途別

- 配管システム

- 防火システム

- 化学・産業機器

- 電源ケーブルケーシング

- 接着剤・コーティング

- その他

第11章 塩素化ポリ塩化ビニル (CPVC) 市場:エンドユーザー産業別

- 住宅用

- 商用

- 産業用

- 電気・電子

- 化学薬品・石油化学製品

- 医薬品

- 発電

- 食品・飲料

- 農業・灌漑

- 紙パルプ

- その他

第12章 塩素化ポリ塩化ビニル (CPVC) 市場:地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第13章 競合情勢

- 市場シェア分析

- 市場ランキング

- 主要企業の収益分析

- 企業の製品フットプリント分析

- 主要企業の企業評価マトリックス

- 競合ベンチマーキング

- スタートアップ/中小企業の企業評価マトリクス

- 競合状況・動向

第14章 企業プロファイル

- 主要企業

- THE LUBRIZOL CORPORATION

- SEKISUI CHEMICAL CO., LTD.

- MEGHMANI FINECHEM LIMITED

- SHANGDONG NOVISTA CHEMICAL CO., LTD.

- SHANDONG PUJIE RUBBER & PLASTIC CO., LTD.

- KANEKA CORPORATION

- SHANGDONG YADA NEW MATERIAL CO., LTD.

- KEM ONE

- SHANDONG XUYE NEW MATERIALS CO., LTD.

- DCW LIMITED

- 主要企業

- SUNDOW POLYMERS CO., LTD.

- MITSUI & CO., LTD.

- SHANGHAI CHLOR-ALKALI CHEMICAL CO., LTD.

- その他の企業

- SHANDONG GAOXIN CHEMICAL CO., LTD.

- HANWHA SOLUTIONS

- HANGZHOU ELECTROCHEMICAL GROUP CO. LTD.

- EN-DOOR

- WEIFANG YADA PLASTIC CO., LTD.

- SHANDONG KETIAN CHEMICAL CO., LTD.

- VIA CHEMICAL CO., LTD.

- JIANGSU TIANTENG CHEMICAL CO., LTD.

- AVIENT CORPORATION

- KUNSHAN MAIJISEN COMPOSITE MATERIALS CO., LTD.

- ZHONGTAI IMPORT & EXPORT CORPORATION

第15章 付録

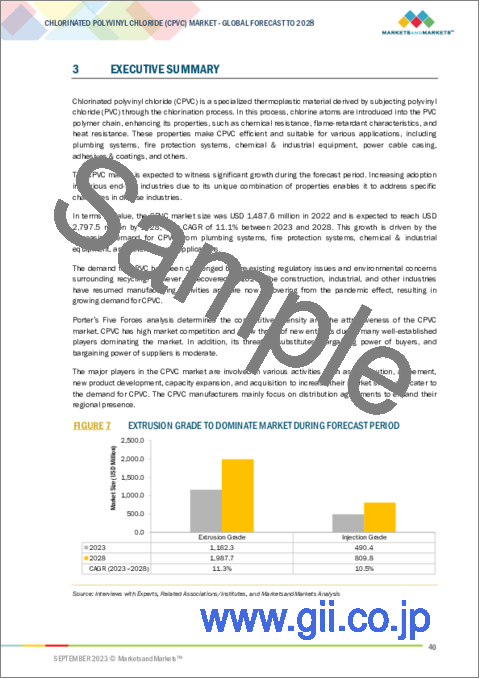

In terms of value, the CPVC market size was USD 1.6 billion in 2022 and is expected to reach USD 2.7 billion by 2028, at a CAGR of 11.1% between 2023 and 2028. This growth is driven by the increasing demand for CPVC from plumbing systems, fire protection, chemical & industrial equipment, and other end-use applications. The demand for CPVC has been challenged by pre-existing regulatory issues and environmental concerns surrounding recycling. However, it recovered in 2021. The construction, industrial, and other industries have resumed manufacturing activities and are now recovering from the pandemic effect, resulting in growing demand for CPVC.

''The extrusion grade segment is the fastest-growing grade segment of CPVC in terms of value and volume.''

Based on the grade, the CPVC market has been segmented into extrusion grade and injection grade. During forecasted years, extrusion grade segment is forecasted to register highest CAGR. CPVC extrusion is mainly used to create continuous, long shapes, whereas CPVC injection grade is used to manufacture shorter CPVC products. The grade of CPVC mainly refers to the polymer characteristics such as chemical resistance, impact strength, heat resistance, and others.

"The pellet form segment is the second-fastest growing form of CPVC in terms of both, value and volume.''

During the forecasted years, pellet form is expected to grow with a significant CAGR during forecasted years. Pellet CPVC is widely used for producing small, customized products that meet specific end-user requirements, in addition to long continuous products like sheets and pipes. To make CPVC products from pellets, an injection molding process is utilized.

"The Indirect sales segment is the second-fastest growing sales channel of CPVC in terms of both, value and volume.''

Indirect distribution involves third parties, like warehouses, wholesalers, and retailers, focusing on their core business while outsourcing distribution to an expert. Sales through distributors involve purchasing raw materials from manufacturers or suppliers, breaking them into smaller units, and selling them to multiple customers while ensuring prompt delivery. Distributors benefit customers by giving them pricing updates and suppliers by providing knowledge of numerous customers.

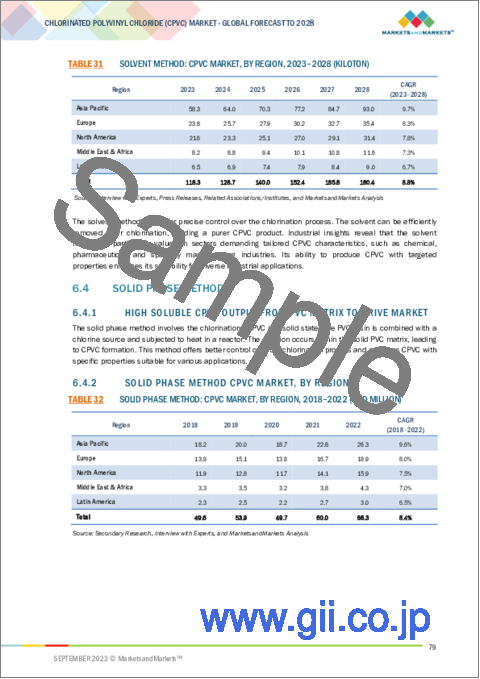

"The Solid phase segment is the fastest growing production process of CPVC in terms of both, value and volume.''

The solid phase method involves the chlorination of PVC in a solid state. The PVC resin is combined with a chlorine source and subjected to heat in a reactor. The reaction occurs within the solid PVC matrix, leading to CPVC formation. This method offers better control over the chlorination process and produces CPVC with specific properties suitable for various applications.

''The Fire protection systems segment is the third-fastest-growing application segment of CPVC in terms of both value and volume.''

CPVC pipes and components have a continued demand for use in fire protection systems in residential and other light-hazard settings. The advantages are straightforward: the material is cheaper and offers quicker and safer assembly than metal alternatives because installers do not need flame or heavy equipment to join components. It is sturdy and reliable, has a 50-year life expectancy, and is resistant to corrosion and deposits that could block water flow. Due to its superior corrosion resistance at high temperatures, CPVC is suited for self-supporting constructions at temperatures up to 200°F (93.3°C).

''The industrial segment is the second-fastest-growing end-use industry segment of CPVC in terms of both value and volume.''

CPVC plays a vital role in various industrial sectors. It finds applications in electronics, wherein its chemical resistance protects components. In the chemical industry, the ability of CPVC to withstand corrosive chemicals ensures safe transportation. In pharmaceuticals, it maintains its integrity when exposed to pharmaceutical substances, and in the food industry, it handles hot liquids and corrosive substances. Attributes such as chemical resistance, thermal stability, and durability make CPVC an indispensable material across these industries, contributing to safety, efficiency, and product quality.

"North America region is estimated to be the third largest CPVC market during the forecast period, in terms of both value, and volume."

The market growth in the North America region can be attributed to the rise in residential construction activities and construction spending. For instance, Eleven Park Mixed-Use Complex is one of the large projects in the US that involves the construction of a mixed-use complex in Indianapolis, Indiana, US. Construction work commenced in Q2 2023 and is expected to finish in Q4 2027. The project aims to provide better residential facilities. It will improve the quality of the place in Indianapolis by creating an entirely new neighbourhood that will help attract and retain quality workers and families. Such developments are fueling the CPVC market in the region.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 37%, Tier 2- 33%, and Tier 3- 30%

- By Designation- C Level- 33%, Director Level- 27%, Executives- 30% and Others- 10%

- By Region- North America- 22%, Europe- 40%, Asia Pacific - 20%, Latin America- 3%, Middle East & Africa- 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies in the CPVC market include The Lubrizol Corporation (US), Sekisui Chemical Co., Ltd. (Japan), Meghmani Finechem Limited (India), Shandong Novista Chemical Co., Ltd. (China), Shandong Pujie Rubber & Plastic Co., Ltd. (China), Kaneka Corporation (Japan), Shandong Yada New Material Co., Ltd. (China), KEM ONE (France), Shandong Xuye New Materials Co., Ltd. (China), DCW Limited (India), Sundow Polymers Co., Ltd. (China), Mitsui & Co., Ltd. (Japan), Shanghai Chlor-Alkali Chemical Co., Ltd. (China), Shandong Gaoxin Chemical Co., Ltd. (China) and others.

Research Coverage

This report covers the global CPVC market and forecasts the market size until 2028. It includes the following market segmentation- By Grade (Injection Grade, and Extrusion Grade), By Form (Pellet and Powder), By Sales Channel (Direct Sales, and Indirect Sales), By Production Process (Aqueous Suspension Methos, Solvent Method, and Solid Phase Method), By Application (Plumbing Systems, Fire Protection Systems, Chemical & Industrial Equipment, Power & Cable Casing, Adhesives & Coatings, and Others)m By End-use Industry (Residential, Commercial, and Industrial), and By Region (North America, Europe, Asia Pacific, Middle East & Africa, Latin America).

Porter's Five Forces Analysis, along with the drivers, restraints, opportunities, and challenges, have been discussed in the report. It also provides company profiles and competitive strategies adopted by the major players in the global CPVC market.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall CPVC market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing construction industry), restraints (high material cost), opportunities (retrofitting and upgrading of existing infrastructure), and challenges (supply chain disruptions and consumer spending patterns) influencing the growth of the CPVC market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the CPVC market

- Market Development: Comprehensive information about lucrative markets - the report analyses the CPVC market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the CPVC market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like The Lubrizol Corporation (US), Sekisui Chemical Co., Ltd. (Japan), Meghmani Finechem Limited (India), Shandong Novista Chemical Co., Ltd. (China), Shandong Pujie Rubber & Plastic Co., Ltd. (China), Kaneka Corporation (Japan), Shandong Yada New Material Co., Ltd. (China), KEM ONE (France), and others among others in the CPVC market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.4 MARKET SCOPE

- FIGURE 1 CPVC MARKET SEGMENTATION

- 1.4.1 REGIONS COVERED

- 1.4.2 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- FIGURE 2 CPVC MARKET: RESEARCH DESIGN

- 2.2 RESEARCH DATA

- 2.2.1 SECONDARY DATA

- 2.2.1.1 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 Key data from primary sources

- 2.2.2.2 Key primary participants

- 2.2.2.3 Breakdown of primary interviews

- 2.2.2.4 Key industry insights

- 2.2.1 SECONDARY DATA

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- 2.4 BASE NUMBER CALCULATION

- 2.4.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 2.4.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 2.5 FORECAST NUMBER CALCULATION

- 2.5.1 SUPPLY SIDE

- 2.5.2 DEMAND SIDE

- 2.6 DATA TRIANGULATION

- FIGURE 5 CPVC MARKET: DATA TRIANGULATION

- 2.7 ASSUMPTIONS

- 2.8 GROWTH FORECAST

- 2.9 RESEARCH LIMITATIONS

- 2.9.1 CPVC MARKET: RESEARCH LIMITATIONS

- 2.10 RISKS

- 2.11 RECESSION IMPACT

- FIGURE 6 RECESSION IMPACT ON CPVC MARKET

3 EXECUTIVE SUMMARY

- FIGURE 7 EXTRUSION GRADE TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 8 POWDER FORM TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 9 DIRECT SALES CHANNEL TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 10 AQUEOUS SUSPENSION METHOD TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 11 PLUMBING SYSTEMS DOMINATED MARKET IN 2022

- FIGURE 12 RESIDENTIAL END-USE INDUSTRY LED MARKET IN 2022

- FIGURE 13 ASIA PACIFIC TO LEAD MARKET DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CPVC MARKET

- FIGURE 14 SIGNIFICANT GROWTH IN CPVC MARKET BETWEEN 2023 AND 2028

- 4.2 CPVC MARKET, BY END-USE INDUSTRY AND REGION, 2022

- FIGURE 15 RESIDENTIAL AND ASIA PACIFIC WERE LARGEST MARKET SEGMENTS IN 2022

- 4.3 CPVC MARKET, BY GRADE

- FIGURE 16 EXTRUSION GRADE SEGMENT DOMINATED MARKET IN 2022

- 4.4 CPVC MARKET, BY FORM

- FIGURE 17 POWDER FORM SEGMENT T0 LEAD MARKET DURING FORECAST PERIOD

- 4.5 CPVC MARKET, BY DIRECT SALES CHANNEL

- FIGURE 18 DIRECT SALES CHANNEL TO ACCOUNT FOR LARGER MARKET SHARE IN 2028

- 4.6 CPVC MARKET, BY MANUFACTURING PROCESS

- FIGURE 19 AQUEOUS SUSPENSION METHOD DOMINATED MARKET IN 2022

- 4.7 CPVC MARKET, BY APPLICATION

- FIGURE 20 PLUMBING SYSTEMS APPLICATION REGISTERED HIGHEST GROWTH IN 2022

- 4.8 CPVC MARKET, BY KEY COUNTRY

- FIGURE 21 CHINA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 22 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN CPVC MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Resistance to chemicals and high temperatures

- 5.2.1.2 Growth of construction sector

- TABLE 1 CONTRIBUTION TO GROWTH IN GLOBAL CONSTRUCTION OUTPUT, BY COUNTRY (2019-2030)

- 5.2.2 RESTRAINTS

- 5.2.2.1 High processing temperature of CPVC than conventional PVC

- 5.2.2.2 High material cost

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rapid urbanization and infrastructure development

- 5.2.3.2 Retrofitting and upgrading of existing infrastructure

- 5.2.4 CHALLENGES

- 5.2.4.1 Increase in CPVC waste and microplastic pollution

- 5.2.4.2 Supply chain disruptions and consumer spending patterns

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 23 CPVC MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF BUYERS

- 5.3.4 BARGAINING POWER OF SUPPLIERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- TABLE 2 CPVC MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- TABLE 3 CPVC MARKET: COMPANIES AND THEIR ROLE IN ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY END-USE INDUSTRY

- FIGURE 24 AVERAGE SELLING PRICE BY KEY PLAYERS FOR TOP THREE END-USE INDUSTRIES (USD/KG)

- TABLE 4 AVERAGE SELLING PRICE TREND BY KEY PLAYERS, BY END-USE INDUSTRY (USD/KG)

- 5.6 AVERAGE SELLING PRICE, BY APPLICATION

- FIGURE 25 AVERAGE SELLING PRICE BASED ON APPLICATION (USD/KG)

- 5.7 AVERAGE SELLING PRICE, BY REGION

- TABLE 5 CPVC AVERAGE SELLING PRICE, BY REGION

- 5.8 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.8.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

- TABLE 6 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

- 5.8.2 BUYING CRITERIA

- FIGURE 27 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

- TABLE 7 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

- 5.9 TECHNOLOGY ANALYSIS

- TABLE 8 COMPARATIVE STUDY OF CPVC MANUFACTURING PROCESSES

- 5.10 ECOSYSTEM

- 5.11 VALUE CHAIN ANALYSIS

- FIGURE 28 VALUE CHAIN ANALYSIS: CPVC MARKET

- 5.12 CASE STUDY ANALYSIS

- 5.13 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 29 REVENUE SHIFT AND NEW REVENUE POCKETS FOR CPVC MARKET

- 5.14 IMPORT-EXPORT SCENARIO

- 5.14.1 CHINA

- 5.14.2 US

- 5.14.3 INDIA

- 5.14.4 JAPAN

- 5.15 REGULATORY LANDSCAPE

- 5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15.2 STANDARDS IN CPVC MARKET

- TABLE 13 CURRENT STANDARD CODES FOR CPVC

- 5.16 KEY CONFERENCES AND EVENTS, 2023-2024

- TABLE 14 CPVC MARKET: KEY CONFERENCES AND EVENTS, 2023-2024

- 5.17 PATENT ANALYSIS

- 5.17.1 INTRODUCTION

- 5.17.2 METHODOLOGY

- 5.17.3 DOCUMENT TYPES

- TABLE 15 CPVC MARKET: GLOBAL PATENT COUNT

- FIGURE 30 GLOBAL PATENT ANALYSIS, BY DOCUMENT TYPE

- FIGURE 31 GLOBAL PATENT PUBLICATION TREND, 2017-2022

- 5.17.4 INSIGHTS

- 5.17.5 LEGAL STATUS

- FIGURE 32 CPVC MARKET: LEGAL STATUS OF PATENTS

- 5.17.6 JURISDICTION ANALYSIS

- FIGURE 33 GLOBAL JURISDICTION ANALYSIS

- 5.17.7 TOP APPLICANTS

- FIGURE 34 LUBRIZOL ADVANCED MATERIALS INC REGISTERED HIGHEST PATENT COUNT

- TABLE 16 PATENTS BY LUBRIZOL ADVANCED MATERIALS INC

- TABLE 17 PATENTS BY SEKISUI CHEMICAL CO LTD.

- TABLE 18 PATENTS BY HUAYA IND PLASTIC TAICANG CO LTD.

- TABLE 19 TOP 10 PATENT OWNERS (US) IN LAST 10 YEARS

6 CPVC MARKET, BY PRODUCTION PROCESS

- 6.1 INTRODUCTION

- FIGURE 35 AQUEOUS SUSPENSION METHOD TO LEAD CPVC MARKET DURING FORECAST PERIOD

- TABLE 20 CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (USD MILLION)

- TABLE 21 CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (KILOTON)

- TABLE 22 CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (USD MILLION)

- TABLE 23 CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (KILOTON)

- 6.2 AQUEOUS SUSPENSION METHOD

- 6.2.1 LARGEST PRODUCTION PROCESS IMPARTING CHEMICAL RESISTANCE TO DRIVE MARKET

- FIGURE 36 ASIA PACIFIC TO LEAD AQUEOUS SUSPENSION SEGMENT DURING FORECAST PERIOD

- 6.2.2 AQUEOUS SUSPENSION METHOD CPVC MARKET, BY REGION

- TABLE 24 AQUEOUS SUSPENSION METHOD: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 25 AQUEOUS SUSPENSION METHOD: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 26 AQUEOUS SUSPENSION METHOD: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 27 AQUEOUS SUSPENSION METHOD: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

- 6.3 SOLVENT METHOD

- 6.3.1 EFFICIENT REMOVAL OF SOLVENTS AFTER CHLORINATION TO DRIVE MARKET

- 6.3.2 SOLVENT METHOD CPVC MARKET, BY REGION

- TABLE 28 SOLVENT METHOD: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 29 SOLVENT METHOD: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 30 SOLVENT METHOD: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 31 SOLVENT METHOD: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

- 6.4 SOLID PHASE METHOD

- 6.4.1 HIGH SOLUBLE CPVC OUTPUT FROM PVC MATRIX TO DRIVE MARKET

- 6.4.2 SOLID PHASE METHOD CPVC MARKET, BY REGION

- TABLE 32 SOLID PHASE METHOD: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 33 SOLID PHASE METHOD: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 34 SOLID PHASE METHOD: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 35 SOLID PHASE METHOD: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

7 CPVC MARKET, BY FORM

- 7.1 INTRODUCTION

- FIGURE 37 POWDER FORM TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 36 CPVC MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 37 CPVC MARKET, BY FORM, 2018-2022 (KILOTON)

- TABLE 38 CPVC MARKET, BY FORM, 2023-2028 (USD MILLION)

- TABLE 39 CPVC MARKET, BY FORM, 2023-2028 (KILOTON)

- 7.2 PELLET FORM

- 7.2.1 EXTENSIVE USE IN PIPES AND FITTINGS TO DRIVE SEGMENT

- FIGURE 38 ASIA PACIFIC TO BE LARGEST MARKET FOR PELLETS DURING FORECAST PERIOD

- 7.2.2 PELLET CPVC MARKET, BY REGION

- TABLE 40 PELLET: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 41 PELLET: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 42 PELLET: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 43 PELLET: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.3 POWDER FORM

- 7.3.1 CHEMICAL RESISTANCE AND FLAME RETARDANCE TO DRIVE APPLICATION

- 7.3.2 POWDER CPVC MARKET, BY REGION

- TABLE 44 POWDER: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 45 POWDER: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 46 POWDER: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 47 POWDER: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

8 CPVC MARKET, BY GRADE

- 8.1 INTRODUCTION

- FIGURE 39 EXTRUSION GRADE TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 48 CPVC MARKET, BY GRADE, 2018-2022 (USD MILLION)

- TABLE 49 CPVC MARKET, BY GRADE, 2018-2022 (KILOTON)

- TABLE 50 CPVC MARKET, BY GRADE, 2023-2028 (USD MILLION)

- TABLE 51 CPVC MARKET, BY GRADE, 2023-2028 (KILOTON)

- 8.2 INJECTION GRADE

- 8.2.1 GROWING APPLICATION IN VALVES, FITTINGS, AND FLANGE ADAPTERS TO DRIVE MARKET

- FIGURE 40 ASIA PACIFIC TO BE LARGEST MARKET OF INJECTION GRADE CPVC DURING FORECAST PERIOD

- 8.2.2 INJECTION GRADE CPVC MARKET, BY REGION

- TABLE 52 INJECTION GRADE: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 53 INJECTION GRADE: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 54 INJECTION GRADE: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 55 INJECTION GRADE: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

- 8.3 EXTRUSION GRADE

- 8.3.1 RISING USE TO MANUFACTURE SHEETS AND PIPES TO DRIVE SEGMENT

- 8.3.2 EXTRUSION GARDE CPVC, BY REGION

- TABLE 56 EXTRUSION GRADE: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 57 EXTRUSION GRADE: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 58 EXTRUSION GRADE: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 59 EXTRUSION GRADE: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

9 CPVC MARKET, BY SALES CHANNEL

- 9.1 INTRODUCTION

- FIGURE 41 INDIRECT SALES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 60 CPVC MARKET, BY SALES CHANNEL, 2018-2022 (USD MILLION)

- TABLE 61 CPVC MARKET, BY SALES CHANNEL, 2018-2022 (KILOTON)

- TABLE 62 CPVC MARKET, BY SALES CHANNEL, 2023-2028 (USD MILLION)

- TABLE 63 CPVC MARKET, BY SALES CHANNEL, 2023-2028 (KILOTON)

- 9.2 DIRECT SALES

- 9.2.1 CONTROL OVER ENTIRE PROCESS TO INCREASE DEMAND

- 9.2.2 DIRECT SALES CPVC MARKET, BY REGION

- TABLE 64 DIRECT SALES: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 65 DIRECT SALES: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 66 DIRECT SALES: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 67 DIRECT SALES: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

- 9.3 INDIRECT SALES

- 9.3.1 FOCUS ON CORE BUSINESS TO DRIVE MARKET

- FIGURE 42 EUROPE TO BE SECOND-LARGEST MARKET FOR INDIRECT SALES SEGMENT DURING FORECAST PERIOD

- 9.3.2 INDIRECT SALES CPVC MARKET, BY REGION

- TABLE 68 INDIRECT SALES: CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 69 INDIRECT SALES: CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 70 INDIRECT SALES: CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 71 INDIRECT SALES: CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

10 CPVC MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- FIGURE 43 PLUMBING SYSTEMS SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 72 CPVC MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 73 CPVC MARKET, BY APPLICATION, 2018-2022 (KILOTON)

- TABLE 74 CPVC MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 75 CPVC MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- 10.2 PLUMBING SYSTEMS

- 10.2.1 INCREASING DEMAND FOR EXTENDED LIFESPAN PRODUCTS TO DRIVE DEMAND

- 10.2.2 INDUSTRIAL PIPING

- 10.2.3 RECLAIMED WATER PIPING

- 10.2.4 POOL & SPA PIPING

- 10.2.5 RESIDENTIAL PIPING

- 10.2.6 FITTINGS, VALVES, & CONNECTORS

- FIGURE 44 ASIA PACIFIC TO BE LARGEST CPVC MARKET DURING FORECAST PERIOD

- 10.2.7 CPVC MARKET IN PLUMBING SYSTEMS, BY REGION

- TABLE 76 CPVC MARKET IN PLUMBING SYSTEMS APPLICATION, BY REGION, 2018-2022 (USD MILLION)

- TABLE 77 CPVC MARKET IN PLUMBING SYSTEMS APPLICATION, BY REGION, 2018-2022 (KILOTON)

- TABLE 78 CPVC MARKET IN PLUMBING SYSTEMS APPLICATION, BY REGION, 2023-2028 (USD MILLION)

- TABLE 79 CPVC MARKET IN PLUMBING SYSTEMS APPLICATION, BY REGION, 2023-2028 (KILOTON)

- 10.3 FIRE PROTECTION SYSTEMS

- 10.3.1 SAFER ASSEMBLY THAN METAL ALTERNATIVES TO DRIVE MARKET

- 10.3.2 INDUSTRIAL FIRE SUPPRESSION

- 10.3.3 FIRE SPRINKLER SYSTEMS

- 10.3.4 FIRE HYDRANT SYSTEMS

- 10.3.5 CPVC MARKET IN FIRE PROTECTION SYSTEMS APPLICATION, BY REGION

- TABLE 80 CPVC MARKET IN FIRE PROTECTION SYSTEMS APPLICATION, BY REGION, 2018-2022 (USD MILLION)

- TABLE 81 CPVC MARKET IN FIRE PROTECTION SYSTEMS APPLICATION, BY REGION, 2018-2022 (KILOTON)

- TABLE 82 CPVC MARKET IN FIRE PROTECTION SYSTEMS APPLICATION, BY REGION, 2023-2028 (USD MILLION)

- TABLE 83 CPVC MARKET IN FIRE PROTECTION SYSTEMS APPLICATION, BY REGION, 2023-2028 (KILOTON)

- 10.4 CHEMICAL & INDUSTRIAL EQUIPMENT

- 10.4.1 LOWER INSTALLATION COSTS TO FUEL MARKET GROWTH

- 10.4.2 CORROSION-RESISTANT COMPONENTS

- 10.4.3 INDUSTRIAL FLUID HANDLING COMPONENTS

- 10.4.4 CHEMICAL PROCESSING EQUIPMENT

- 10.4.5 CPVC MARKET IN CHEMICAL & INDUSTRIAL EQUIPMENT APPLICATION, BY REGION

- TABLE 84 CPVC MARKET IN CHEMICAL & INDUSTRIAL EQUIPMENT APPLICATION, BY REGION, 2018-2022 (USD MILLION)

- TABLE 85 CPVC MARKET IN CHEMICAL & INDUSTRIAL EQUIPMENT APPLICATION, BY REGION, 2018-2022 (KILOTON)

- TABLE 86 CPVC MARKET IN CHEMICAL & INDUSTRIAL EQUIPMENT APPLICATION, BY REGION, BY REGION, 2023-2028 (USD MILLION)

- TABLE 87 CPVC MARKET IN CHEMICAL & INDUSTRIAL EQUIPMENT APPLICATION, BY REGION, BY REGION, 2023-2028 (KILOTON)

- 10.5 POWER CABLE CASING

- 10.5.1 SELF-EXTINGUISHING PROPERTIES TO DRIVE MARKET

- 10.5.2 CABLE CONDUITS

- 10.5.3 PROTECTIVE ENCLOSURES

- 10.5.4 CPVC MARKET IN POWER CABLE CASING APPLICATION, BY REGION

- TABLE 88 CPVC MARKET IN POWER CABLE CASING APPLICATION, BY REGION, 2018-2022 (USD MILLION)

- TABLE 89 CPVC MARKET IN POWER CABLE CASING APPLICATION, BY REGION, 2018-2022 (KILOTON)

- TABLE 90 CPVC MARKET IN POWER CABLE CASING APPLICATION, BY REGION, 2023-2028 (USD MILLION)

- TABLE 91 CPVC MARKET IN POWER CABLE CASING APPLICATION, BY REGION, 2023-2028 (KILOTON)

- 10.6 ADHESIVES & COATINGS

- 10.6.1 HIGHER SOLUBILITY THAN PVC IN ORGANIC SOLVENTS TO DRIVE MARKET

- 10.6.2 CPVC MARKET IN ADHESIVES & COATINGS APPLICATION, BY REGION

- TABLE 92 CPVC MARKET IN ADHESIVES & COATINGS APPLICATION, BY REGION, 2018-2022 (USD MILLION)

- TABLE 93 CPVC MARKET IN ADHESIVES & COATINGS APPLICATION, BY REGION, 2018-2022 (KILOTON)

- TABLE 94 CPVC MARKET IN ADHESIVES & COATINGS APPLICATION, BY REGION, 2023-2028 (USD MILLION)

- TABLE 95 CPVC MARKET IN ADHESIVES & COATINGS APPLICATION, BY REGION, 2023-2028 (KILOTON)

- 10.7 OTHER APPLICATIONS

- 10.7.1 CPVC MARKET SIZE IN OTHER APPLICATIONS, BY REGION

- TABLE 96 CPVC MARKET IN OTHER APPLICATIONS, BY REGION, 2018-2022 (USD MILLION)

- TABLE 97 CPVC MARKET IN OTHER APPLICATIONS, BY REGION, 2018-2022 (KILOTON)

- TABLE 98 CPVC MARKET IN OTHER APPLICATIONS, BY REGION, 2023-2028 (USD MILLION)

- TABLE 99 CPVC MARKET IN OTHER APPLICATIONS, BY REGION, 2023-2028 (KILOTON)

11 CPVC MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- FIGURE 45 RESIDENTIAL INDUSTRY SEGMENT TO LEAD CPVC MARKET DURING FORECAST PERIOD

- TABLE 100 CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 101 CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 102 CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 103 CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- 11.2 RESIDENTIAL

- 11.2.1 DURABLE AND EFFICIENT PLUMBING SOLUTIONS TO DRIVE MARKET

- FIGURE 46 ASIA PACIFIC TO LEAD CPVC MARKET IN RESIDENTIAL SEGMENT DURING FORECAST PERIOD

- 11.2.2 CPVC MARKET IN RESIDENTIAL END-USE INDUSTRY, BY REGION

- TABLE 104 CPVC MARKET IN RESIDENTIAL END-USE INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 105 CPVC MARKET IN RESIDENTIAL END-USE INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 106 CPVC MARKET IN RESIDENTIAL END-USE INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 107 CPVC MARKET IN RESIDENTIAL END-USE INDUSTRY, BY REGION, 2023-2028 (KILOTON)

- 11.3 COMMERCIAL

- 11.3.1 SAFETY, RELIABILITY, AND DURABILITY TO DRIVE MARKET

- 11.3.2 CPVC MARKET IN COMMERCIAL END-USE INDUSTRY, BY REGION

- TABLE 108 CPVC MARKET IN COMMERCIAL END-USE INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 109 CPVC MARKET IN COMMERCIAL END-USE INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 110 CPVC MARKET IN COMMERCIAL END-USE INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 111 CPVC MARKET IN COMMERCIAL END-USE INDUSTRY, BY REGION, 2023-2028 (KILOTON)

- 11.4 INDUSTRIAL

- 11.4.1 DEMAND FROM VARIOUS INDUSTRIAL SECTORS TO DRIVE MARKET

- 11.4.2 ELECTRICAL & ELECTRONICS

- 11.4.3 CHEMICALS & PETROCHEMICALS

- 11.4.4 PHARMACEUTICALS

- 11.4.5 POWER GENERATION

- 11.4.6 FOOD & BEVERAGE

- 11.4.7 AGRICULTURE & IRRIGATION

- 11.4.8 PULP & PAPER

- 11.4.9 OTHERS

- 11.4.9.1 Fertilizer, oil & gas

- 11.4.10 CPVC MARKET IN INDUSTRIAL END-USE INDUSTRY, BY REGION

- TABLE 112 CPVC MARKET IN INDUSTRIAL END-USE INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 113 CPVC MARKET IN INDUSTRIAL END-USE INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 114 CPVC MARKET IN INDUSTRIAL END-USE INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 115 CPVC MARKET IN INDUSTRIAL END-USE INDUSTRY, BY REGION, 2023-2028 (KILOTON)

12 CPVC MARKET, BY REGION

- 12.1 INTRODUCTION

- FIGURE 47 UK TO BE FASTEST-GROWING CPVC MARKET DURING FORECAST PERIOD

- TABLE 116 CPVC MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 117 CPVC MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 118 CPVC MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 119 CPVC MARKET, BY REGION, 2023-2028 (KILOTON)

- 12.2 NORTH AMERICA

- 12.2.1 RECESSION IMPACT ON NORTH AMERICA

- FIGURE 48 NORTH AMERICA: CPVC MARKET SNAPSHOT

- 12.2.2 NORTH AMERICA: CPVC MARKET, BY GRADE

- TABLE 120 NORTH AMERICA: PHYSICAL CPVC MARKET, BY GRADE, 2018-2022 (USD MILLION)

- TABLE 121 NORTH AMERICA: CPVC MARKET, BY GRADE, 2018-2022 (KILOTON)

- TABLE 122 NORTH AMERICA: CPVC MARKET, BY GRADE, 2023-2028 (USD MILLION)

- TABLE 123 NORTH AMERICA: CPVC MARKET, BY GRADE, 2023-2028 (KILOTON)

- 12.2.3 NORTH AMERICA: CPVC MARKET, BY FORM

- TABLE 124 NORTH AMERICA: CPVC MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 125 NORTH AMERICA: CPVC MARKET, BY FORM, 2018-2022 (KILOTON)

- TABLE 126 NORTH AMERICA: CPVC MARKET, BY FORM, 2023-2028 (USD MILLION)

- TABLE 127 NORTH AMERICA: CPVC MARKET, BY FORM, 2023-2028 (KILOTON)

- 12.2.4 NORTH AMERICA: CPVC MARKET, BY SALES CHANNEL

- TABLE 128 NORTH AMERICA: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (USD MILLION)

- TABLE 129 NORTH AMERICA: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (KILOTON)

- TABLE 130 NORTH AMERICA: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (USD MILLION)

- TABLE 131 NORTH AMERICA: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (KILOTON)

- 12.2.5 NORTH AMERICA: CPVC MARKET, BY PRODUCTION PROCESS

- TABLE 132 NORTH AMERICA: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (USD MILLION)

- TABLE 133 NORTH AMERICA: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (KILOTON)

- TABLE 134 NORTH AMERICA: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (USD MILLION)

- TABLE 135 NORTH AMERICA: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (KILOTON)

- 12.2.6 NORTH AMERICA: CPVC MARKET, BY APPLICATION

- TABLE 136 NORTH AMERICA: CPVC MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 137 NORTH AMERICA: CPVC MARKET, BY APPLICATION, 2018-2022 (KILOTON)

- TABLE 138 NORTH AMERICA: CPVC MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 139 NORTH AMERICA: CPVC MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- 12.2.7 NORTH AMERICA: CPVC MARKET, BY END-USE INDUSTRY

- TABLE 140 NORTH AMERICA: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 141 NORTH AMERICA: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 142 NORTH AMERICA: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 143 NORTH AMERICA: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- 12.2.8 NORTH AMERICA: CPVC MARKET, BY COUNTRY

- TABLE 144 NORTH AMERICA: CPVC MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 145 NORTH AMERICA: CPVC MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 146 NORTH AMERICA: CPVC MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 147 NORTH AMERICA: CPVC MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 12.2.8.1 US

- 12.2.8.1.1 Growth in construction sector to drive market

- 12.2.8.2 Canada

- 12.2.8.2.1 Upcoming building and construction projects to drive growth

- 12.2.8.1 US

- 12.3 EUROPE

- 12.3.1 RECESSION IMPACT ON EUROPE

- FIGURE 49 EUROPE: CPVC MARKET SNAPSHOT

- 12.3.2 EUROPE: CPVC MARKET, BY GRADE

- TABLE 148 EUROPE: PHYSICAL CPVC MARKET, BY GRADE, 2018-2022 (USD MILLION)

- TABLE 149 EUROPE: CPVC MARKET, BY GRADE, 2018-2022 (KILOTON)

- TABLE 150 EUROPE: CPVC MARKET, BY GRADE, 2023-2028 (USD MILLION)

- TABLE 151 EUROPE: CPVC MARKET, BY GRADE, 2023-2028 (KILOTON)

- 12.3.3 EUROPE: CPVC MARKET, BY FORM

- TABLE 152 EUROPE: CPVC MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 153 EUROPE: CPVC MARKET, BY FORM, 2018-2022 (KILOTON)

- TABLE 154 EUROPE: CPVC MARKET, BY FORM, 2023-2028 (USD MILLION)

- TABLE 155 EUROPE: CPVC MARKET, BY FORM, 2023-2028 (KILOTON)

- 12.3.4 EUROPE: CPVC MARKET, BY SALES CHANNEL

- TABLE 156 EUROPE: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (USD MILLION)

- TABLE 157 EUROPE: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (KILOTON)

- TABLE 158 EUROPE: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (USD MILLION)

- TABLE 159 EUROPE: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (KILOTON)

- 12.3.5 EUROPE: CPVC MARKET, BY PRODUCTION PROCESS

- TABLE 160 EUROPE: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (USD MILLION)

- TABLE 161 EUROPE: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (KILOTON)

- TABLE 162 EUROPE: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (USD MILLION)

- TABLE 163 EUROPE: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (KILOTON)

- 12.3.6 EUROPE: CPVC MARKET, BY APPLICATION

- TABLE 164 EUROPE: CPVC MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 165 EUROPE: CPVC MARKET, BY APPLICATION, 2018-2022 (KILOTON)

- TABLE 166 EUROPE: CPVC MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 167 EUROPE: CPVC MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- 12.3.7 EUROPE: CPVC MARKET, BY END-USE INDUSTRY

- TABLE 168 EUROPE: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 169 EUROPE: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 170 EUROPE: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 171 EUROPE: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- 12.3.8 EUROPE: CPVC MARKET, BY COUNTRY

- TABLE 172 EUROPE: CPVC MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 173 EUROPE: CPVC MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 174 EUROPE: CPVC MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 175 EUROPE: CPVC MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 12.3.8.1 Germany

- 12.3.8.1.1 Growing development in residential industry to drive demand

- 12.3.8.2 UK

- 12.3.8.2.1 Increasing residential construction projects to drive market

- 12.3.8.3 France

- 12.3.8.3.1 Rapid development in metropolitan areas to drive market

- 12.3.8.4 Italy

- 12.3.8.4.1 Commercial and industrial construction projects to drive growth

- 12.3.8.5 Spain

- 12.3.8.5.1 Rising foreign investment in construction sector to drive market

- 12.3.8.6 Rest of Europe

- 12.3.8.1 Germany

- 12.4 ASIA PACIFIC

- 12.4.1 RECESSION IMPACT ON ASIA PACIFIC

- FIGURE 50 ASIA PACIFIC: CPVC MARKET SNAPSHOT

- 12.4.2 ASIA PACIFIC: CPVC MARKET, BY GRADE

- TABLE 176 ASIA PACIFIC: CPVC MARKET, BY GRADE, 2018-2022 (USD MILLION)

- TABLE 177 ASIA PACIFIC: CPVC MARKET, BY GRADE, 2018-2022 (KILOTON)

- TABLE 178 ASIA PACIFIC: CPVC MARKET, BY GRADE, 2023-2028 (USD MILLION)

- TABLE 179 ASIA PACIFIC: CPVC MARKET, BY GRADE, 2023-2028 (KILOTON)

- 12.4.3 ASIA PACIFIC: CPVC MARKET, BY FORM

- TABLE 180 ASIA PACIFIC: CPVC MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 181 ASIA PACIFIC: CPVC MARKET, BY FORM, 2018-2022 (KILOTON)

- TABLE 182 ASIA PACIFIC: CPVC MARKET, BY FORM, 2023-2028 (USD MILLION)

- TABLE 183 ASIA PACIFIC: CPVC MARKET, BY FORM, 2023-2028 (KILOTON)

- 12.4.4 ASIA PACIFIC: CPVC MARKET, BY SALES CHANNEL

- TABLE 184 ASIA PACIFIC: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (USD MILLION)

- TABLE 185 ASIA PACIFIC: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (KILOTON)

- TABLE 186 ASIA PACIFIC: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (USD MILLION)

- TABLE 187 ASIA PACIFIC: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (KILOTON)

- 12.4.5 ASIA PACIFIC: CPVC MARKET, BY PRODUCTION PROCESS

- TABLE 188 ASIA PACIFIC: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (USD MILLION)

- TABLE 189 ASIA PACIFIC: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (KILOTON)

- TABLE 190 ASIA PACIFIC: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (USD MILLION)

- TABLE 191 ASIA PACIFIC: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (KILOTON)

- 12.4.6 ASIA PACIFIC: CPVC MARKET, BY APPLICATION

- TABLE 192 ASIA PACIFIC: CPVC MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 193 ASIA PACIFIC: CPVC MARKET, BY APPLICATION, 2018-2022 (KILOTON)

- TABLE 194 ASIA PACIFIC: CPVC MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 195 ASIA PACIFIC: CPVC MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- 12.4.7 ASIA PACIFIC: CPVC MARKET, BY END-USE INDUSTRY

- TABLE 196 ASIA PACIFIC: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 197 ASIA PACIFIC: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 198 ASIA PACIFIC: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 199 ASIA PACIFIC: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- 12.4.8 ASIA PACIFIC: CPVC MARKET, BY COUNTRY

- TABLE 200 ASIA PACIFIC: CPVC MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 201 ASIA PACIFIC: CPVC MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 202 ASIA PACIFIC: CPVC MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 203 ASIA PACIFIC: CPVC MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 12.4.8.1 China

- 12.4.8.1.1 Huge government investments in construction sector to drive market

- 12.4.8.2 India

- 12.4.8.2.1 Improving business conditions across sectors to boost market

- 12.4.8.3 South Korea

- 12.4.8.3.1 Residential construction industry to drive market

- 12.4.8.4 Japan

- 12.4.8.4.1 Increasing government support for construction sector to drive market

- 12.4.8.5 Rest of Asia Pacific

- 12.4.8.1 China

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 RECESSION IMPACT ON MIDDLE EAST & AFRICA

- 12.5.2 MIDDLE EAST & AFRICA: CPVC MARKET, BY GRADE

- TABLE 204 MIDDLE EAST & AFRICA: CPVC MARKET, BY GRADE, 2018-2022 (USD MILLION)

- TABLE 205 MIDDLE EAST & AFRICA: CPVC MARKET, BY GRADE, 2018-2022 (KILOTON)

- TABLE 206 MIDDLE EAST & AFRICA: CPVC MARKET, BY GRADE, 2023-2028 (USD MILLION)

- TABLE 207 MIDDLE EAST & AFRICA: CPVC MARKET, BY GRADE, 2023-2028 (KILOTON)

- 12.5.3 MIDDLE EAST & AFRICA: CPVC MARKET, BY FORM

- TABLE 208 MIDDLE EAST & AFRICA: CPVC MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 209 MIDDLE EAST & AFRICA: CPVC MARKET, BY FORM, 2018-2022 (KILOTON)

- TABLE 210 MIDDLE EAST & AFRICA: CPVC MARKET, BY FORM, 2023-2028 (USD MILLION)

- TABLE 211 MIDDLE EAST & AFRICA: CPVC MARKET, BY FORM, 2023-2028 (KILOTON)

- 12.5.4 MIDDLE EAST & AFRICA: CPVC MARKET, BY SALES CHANNEL

- TABLE 212 MIDDLE EAST & AFRICA: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (USD MILLION)

- TABLE 213 MIDDLE EAST & AFRICA: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (KILOTON)

- TABLE 214 MIDDLE EAST & AFRICA: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (USD MILLION)

- TABLE 215 MIDDLE EAST & AFRICA: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (KILOTON)

- 12.5.5 MIDDLE EAST & AFRICA: CPVC MARKET, BY PRODUCTION PROCESS

- TABLE 216 MIDDLE EAST & AFRICA: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (USD MILLION)

- TABLE 217 MIDDLE EAST & AFRICA: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (KILOTON)

- TABLE 218 MIDDLE EAST & AFRICA: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (USD MILLION)

- TABLE 219 MIDDLE EAST & AFRICA: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (KILOTON)

- 12.5.6 MIDDLE EAST & AFRICA: CPVC MARKET, BY APPLICATION

- TABLE 220 MIDDLE EAST & AFRICA: CPVC MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 221 MIDDLE EAST & AFRICA: CPVC MARKET, BY APPLICATION, 2018-2022 (KILOTON)

- TABLE 222 MIDDLE EAST & AFRICA: CPVC MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 223 MIDDLE EAST & AFRICA: CPVC MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- 12.5.7 MIDDLE EAST & AFRICA: CPVC MARKET, BY END-USE INDUSTRY

- TABLE 224 MIDDLE EAST & AFRICA: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 225 MIDDLE EAST & AFRICA: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 226 MIDDLE EAST & AFRICA: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 227 MIDDLE EAST & AFRICA: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- 12.5.8 MIDDLE EAST & AFRICA: CPVC MARKET, BY COUNTRY

- TABLE 228 MIDDLE EAST & AFRICA: CPVC MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 229 MIDDLE EAST & AFRICA: CPVC MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 230 MIDDLE EAST & AFRICA: CPVC MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 231 MIDDLE EAST & AFRICA: CPVC MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 12.5.8.1 Saudi Arabia

- 12.5.8.1.1 Vision 2030 to drive market

- 12.5.8.2 UAE

- 12.5.8.2.1 Government initiatives to boost market

- 12.5.8.3 Rest of Middle East & Africa

- 12.5.8.1 Saudi Arabia

- 12.6 LATIN AMERICA

- 12.6.1 RECESSION IMPACT ON LATIN AMERICA

- 12.6.2 LATIN AMERICA: CPVC MARKET, BY GRADE

- TABLE 232 LATIN AMERICA: CPVC MARKET, BY GRADE, 2018-2022 (USD MILLION)

- TABLE 233 LATIN AMERICA: CPVC MARKET, BY GRADE, 2018-2022 (KILOTON)

- TABLE 234 LATIN AMERICA: CPVC MARKET, BY GRADE, 2023-2028 (USD MILLION)

- TABLE 235 LATIN AMERICA: CPVC MARKET, BY GRADE, 2023-2028 (KILOTON)

- 12.6.3 LATIN AMERICA: CPVC MARKET, BY FORM

- TABLE 236 LATIN AMERICA: CPVC MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 237 LATIN AMERICA: CPVC MARKET, BY FORM, 2018-2022 (KILOTON)

- TABLE 238 LATIN AMERICA: CPVC MARKET, BY FORM, 2023-2028 (USD MILLION)

- TABLE 239 LATIN AMERICA: CPVC MARKET, BY FORM, 2023-2028 (KILOTON)

- 12.6.4 LATIN AMERICA: CPVC MARKET, BY SALES CHANNEL

- TABLE 240 LATIN AMERICA: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (USD MILLION)

- TABLE 241 LATIN AMERICA: CPVC MARKET, BY SALES CHANNEL, 2018-2022 (KILOTON)

- TABLE 242 LATIN AMERICA: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (USD MILLION)

- TABLE 243 LATIN AMERICA: CPVC MARKET, BY SALES CHANNEL, 2023-2028 (KILOTON)

- 12.6.5 LATIN AMERICA: CPVC MARKET, BY PRODUCTION PROCESS

- TABLE 244 LATIN AMERICA: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (USD MILLION)

- TABLE 245 LATIN AMERICA: CPVC MARKET, BY PRODUCTION PROCESS, 2018-2022 (KILOTON)

- TABLE 246 LATIN AMERICA: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (USD MILLION)

- TABLE 247 LATIN AMERICA: CPVC MARKET, BY PRODUCTION PROCESS, 2023-2028 (KILOTON)

- 12.6.6 LATIN AMERICA: CPVC MARKET, BY APPLICATION

- TABLE 248 LATIN AMERICA: CPVC MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 249 LATIN AMERICA: CPVC MARKET, BY APPLICATION, 2018-2022 (KILOTON)

- TABLE 250 LATIN AMERICA: CPVC MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 251 LATIN AMERICA: CPVC MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- 12.6.7 LATIN AMERICA: CPVC MARKET, BY END-USE INDUSTRY

- TABLE 252 LATIN AMERICA: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 253 LATIN AMERICA: CPVC MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 254 LATIN AMERICA: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 255 LATIN AMERICA: CPVC MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- 12.6.8 LATIN AMERICA: CPVC MARKET, BY COUNTRY

- TABLE 256 LATIN AMERICA: CPVC MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 257 LATIN AMERICA: CPVC MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 258 LATIN AMERICA: CPVC MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 259 LATIN AMERICA: CPVC MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 12.6.8.1 Mexico

- 12.6.8.1.1 Water treatment and construction projects to drive market

- 12.6.8.2 Brazil

- 12.6.8.2.1 Growing tourist activities to drive market

- 12.6.8.3 Rest of Latin America

- 12.6.8.1 Mexico

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 MARKET SHARE ANALYSIS

- FIGURE 51 SHARES OF TOP COMPANIES IN CPVC MARKET

- TABLE 260 DEGREE OF COMPETITION: CPVC MARKET

- 13.3 MARKET RANKING

- FIGURE 52 RANKING OF TOP SIX PLAYERS IN CPVC MARKET

- 13.4 REVENUE ANALYSIS OF TOP MARKET PLAYERS

- 13.5 COMPANY PRODUCT FOOTPRINT ANALYSIS

- TABLE 261 COMPANY PRODUCT FOOTPRINT

- TABLE 262 COMPANY GRADE FOOTPRINT

- TABLE 263 COMPANY SALES CHANNEL FOOTPRINT

- TABLE 264 COMPANY APPLICATION FOOTPRINT

- TABLE 265 COMPANY END-USE INDUSTRY FOOTPRINT

- TABLE 266 COMPANY REGION FOOTPRINT

- 13.6 COMPANY EVALUATION MATRIX FOR KEY PLAYERS

- 13.6.1 STARS

- 13.6.2 PERVASIVE PLAYERS

- 13.6.3 PARTICIPANTS

- 13.6.4 EMERGING LEADERS

- FIGURE 53 COMPANY EVALUATION MATRIX FOR CPVC MARKET (GLOBAL), 2022

- 13.7 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 267 CPVC MARKET: KEY STARTUPS/SMES

- TABLE 268 CPVC MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 13.8 COMPANY EVALUATION MATRIX FOR STARTUPS/SMES

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- FIGURE 54 STARTUPS/SMES EVALUATION MATRIX FOR CPVC MARKET, 2022

- 13.9 COMPETITIVE SITUATIONS AND TRENDS

- TABLE 269 CPVC MARKET: DEALS, 2018-2023

- TABLE 270 CPVC MARKET: OTHER DEVELOPMENTS, 2018-2023

14 COMPANY PROFILES

- (Business overview, Products/Solutions/Services offered, Recent Developments, Deals, Other developments, MnM view, Right to win, Strategic choices, Weaknesses and competitive threats)**

- 14.1 KEY PLAYERS

- 14.1.1 THE LUBRIZOL CORPORATION

- TABLE 271 THE LUBRIZOL CORPORATION: COMPANY OVERVIEW

- 14.1.2 SEKISUI CHEMICAL CO., LTD.

- TABLE 272 SEKISUI CHEMICAL CO., LTD.: COMPANY OVERVIEW

- FIGURE 55 SEKISUI CHEMICAL CO., LTD.: COMPANY SNAPSHOT

- 14.1.3 MEGHMANI FINECHEM LIMITED

- TABLE 273 MEGHMANI FINECHEM LIMITED: COMPANY OVERVIEW

- FIGURE 56 MEGHMANI FINECHEM LIMITED: COMPANY SNAPSHOT

- 14.1.4 SHANGDONG NOVISTA CHEMICAL CO., LTD.

- TABLE 274 SHANDONG NOVISTA CHEMICAL CO., LTD.: COMPANY OVERVIEW

- 14.1.5 SHANDONG PUJIE RUBBER & PLASTIC CO., LTD.

- TABLE 275 SHANDONG PUJIE RUBBER & PLASTIC CO., LTD.: COMPANY OVERVIEW

- 14.1.6 KANEKA CORPORATION

- TABLE 276 KANEKA CORPORATION: COMPANY OVERVIEW

- FIGURE 57 KANEKA CORPORATION: COMPANY SNAPSHOT

- 14.1.7 SHANGDONG YADA NEW MATERIAL CO., LTD.

- TABLE 277 SHANDONG YADA NEW MATERIAL CO., LTD.: COMPANY OVERVIEW

- 14.1.8 KEM ONE

- TABLE 278 KEM ONE: COMPANY OVERVIEW

- 14.1.9 SHANDONG XUYE NEW MATERIALS CO., LTD.

- TABLE 279 SHANDONG XUYE NEW MATERIALS CO., LTD.: COMPANY OVERVIEW

- 14.1.10 DCW LIMITED

- TABLE 280 DCW LIMITED: COMPANY OVERVIEW

- FIGURE 58 DCW LIMITED: COMPANY SNAPSHOT

- 14.2 KEY COMPANIES

- 14.2.1 SUNDOW POLYMERS CO., LTD.

- TABLE 281 SUNDOW POLYMERS CO., LTD.: COMPANY OVERVIEW

- 14.2.2 MITSUI & CO., LTD.

- TABLE 282 MITSUI & CO., LTD.: COMPANY OVERVIEW

- FIGURE 59 MITSUI & CO., LTD.: COMPANY SNAPSHOT

- 14.2.3 SHANGHAI CHLOR-ALKALI CHEMICAL CO., LTD.

- TABLE 283 SHANGHAI CHLOR-ALKALI CHEMICAL CO., LTD.: COMPANY OVERVIEW

- FIGURE 60 SHANGHAI CHLOR-ALKALI CHEMICAL CO., LTD.: COMPANY SNAPSHOT

- *Details on Business overview, Products/Solutions/Services offered, Recent Developments, Deals, Other developments, MnM view, Right to win, Strategic choices, Weaknesses and competitive threats might not be captured in case of unlisted companies.

- 14.3 OTHER COMPANIES

- 14.3.1 SHANDONG GAOXIN CHEMICAL CO., LTD.

- TABLE 284 SHANDONG GAOXIN CHEMICAL CO., LTD.: COMPANY OVERVIEW

- 14.3.2 HANWHA SOLUTIONS

- TABLE 285 HANWHA SOLUTIONS: COMPANY OVERVIEW

- 14.3.3 HANGZHOU ELECTROCHEMICAL GROUP CO. LTD.

- TABLE 286 HANGZHOU ELECTROCHEMICAL GROUP CO. LTD.: COMPANY OVERVIEW

- 14.3.4 EN-DOOR

- TABLE 287 EN-DOOR: COMPANY OVERVIEW

- 14.3.5 WEIFANG YADA PLASTIC CO., LTD.

- TABLE 288 WEIFANG YADA PLASTIC CO., LTD.: COMPANY OVERVIEW

- 14.3.6 SHANDONG KETIAN CHEMICAL CO., LTD.

- TABLE 289 SHANDONG KETIAN CHEMICAL CO., LTD..: COMPANY OVERVIEW

- 14.3.7 VIA CHEMICAL CO., LTD.

- TABLE 290 VIA CHEMICAL CO., LTD.: COMPANY OVERVIEW

- 14.3.8 JIANGSU TIANTENG CHEMICAL CO., LTD.

- TABLE 291 JIANGSU TIANTENG CHEMICAL INDUSTRY CO., LTD.: COMPANY OVERVIEW

- 14.3.9 AVIENT CORPORATION

- TABLE 292 AVIENT CORPORATION: COMPANY OVERVIEW

- 14.3.10 KUNSHAN MAIJISEN COMPOSITE MATERIALS CO., LTD.

- TABLE 293 KUNSHAN MAIJISEN COMPOSITE MATERIALS CO., LTD.: COMPANY OVERVIEW

- 14.3.11 ZHONGTAI IMPORT & EXPORT CORPORATION

- TABLE 294 ZHONGTAI IMPORT & EXPORT CORPORATION: COMPANY OVERVIEW

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS