農業機械の世界市場:出力別、設備タイプ別、機能別、推進方式別、駆動タイプ別、製品タイプ別、地域別 - 2033年までの予測

Farm Equipment Market by Power, Type (Tractors, Balers, Sprayers, Harvesters), Function, & Propulsion, and Region - Global Forecast to 2033- 発行日

- ページ情報

- 英文 446 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 2076888

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

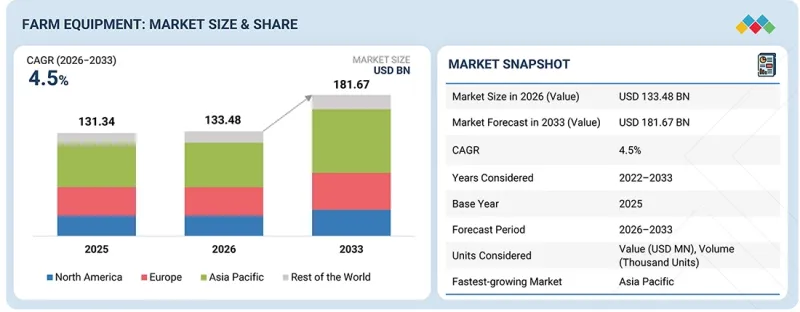

農業機械の市場規模は、2026年の1,334億8,000万米ドルから2033年までに1,816億7,000万米ドルへと成長し、CAGRは4.5%になると予測されています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2026年~2033年 |

| 基準年 | 2025年 |

| 予測期間 | 2026年~2033年 |

| 対象単位 | 10億米ドル |

| セグメント | 出力別、設備タイプ別、機能別、推進方式別、駆動タイプ別、製品タイプ別、地域別 |

| 対象地域 | アジア・オセアニア、欧州、北米、その他の地域 |

2025年、世界の農業用トラクター市場では、主に農家の所得低迷、高金利、および買い替えサイクルの遅れにより、主要地域全体で需要が緩やかに減少しました。AEM、CEMA、および各地域の農業機関による業界見通しによると、トラクターの販売台数は北米で約7~9%、欧州で約22~24%、アジア・オセアニアで約4~6%減少したと推定されています。アジア・オセアニア地域では、政府の補助金や堅調な内需(特にインド)が、販売の減速を食い止める一助となりました。農家が新規機械の購入を控え、既存機器の耐用年数を延ばす傾向にあるため、この影響は高馬力トラクターやコンバインのセグメントでより顕著に表れています。さらに、イスラエルとイランの紛争により、中東の供給ルートの混乱が懸念され、燃料費や物流コストの不確実性が高まっていることから、短期的な圧力がさらに強まっています。これにより、特に価格に敏感な市場において、農家の収益性が低下し、機械の購入が先送りされています。しかし、その影響は間接的かつ短期的なものに留まっており、世界の食料需要や進行中の機械化の動向により、長期的な需要は安定しています。

「レンタル市場における収穫・脱穀セグメントは、予測期間において最も急速に成長するセグメントです。」

収穫・脱穀機器は、農業用機械市場において最大のセグメントの一つを占めています。これは、作物生産において最も労働集約的で時間的制約の厳しい段階、すなわち作物の収穫や、損失を最小限に抑えながら販売可能な穀粒をわらから分離する作業に直接対応するからです。特に、アジア太平洋地域(中国、インド、東南アジア)、北米、欧州、ラテンアメリカといった主要な穀物生産地域では需要が旺盛です。これらの地域では、農業賃金の上昇、労働力不足、農場の規模拡大、収穫適期の短縮などが相まって、機械化が加速しています。これらの機械は、小麦、米、トウモロコシ、大麦、大豆、その他の穀物作物の収穫に広く使用されており、農家は穀物の損失を削減し、穀物の品質を向上させ、労働力への依存度を低減し、悪天候が収量に影響を与える前に収穫作業を完了させることができます。

最近の技術革新により、導入はさらに加速しています。例えば、2025年2月には、John Deereが、作物の捕捉と収穫効率を向上させるよう設計された先進的な作物供給システムを備えた次世代コンバインを導入しました。また、2025年6月には、自動化の強化、精密農業技術、および作業生産性の向上を特徴とする自走式飼料収穫機「F8」および「F9」を発売しました。また、インドの稲作地域向けにコンバイン「PRO588i-G」を発売しました。この機種には、日本が設計した特殊な脱穀機構が組み込まれており、バスマティ米の穀粒破損を低減すると同時に、残渣管理を支援し、刈り株の焼却を削減します。同様に、OEM各社は、生産性を最大化し、オペレーターの介入を削減するために、GPSガイダンス、収穫調整の自動化、テレマティクス、AIによる機械の最適化をコンバインや収穫機にますます統合しています。世界の穀物生産量が増加し続け、農場の規模が拡大し商業化が進むにつれ、収穫・脱穀機器への需要は引き続き堅調であると予想され、この分野は世界の農業機械化の最も重要な促進要因の一つとなるでしょう。

「バッテリー式電気トラクターが、農業用トラクター業界の未来を牽引するでしょう。」

電気トラクターは主に、排出ガス、騒音、運用コストを最小限に抑える必要がある、低出力、精密作業、および管理された環境での用途に使用されています。主な用途には、果樹園、ブドウ園、園芸、温室栽培、畜産農場、自治体農業、および日常的な稼働時間における軽~中程度の畑作業が含まれます。欧州や米国では、小型のEVトラクターが特にブドウ園で人気を博しています。これは、狭い列の間でも効率的に作業できる上、土壌への影響を軽減し、排気ガスをゼロにできるためです。また、騒音レベルが低く、メンテナンスの手間も少ないことから、自治体でも都市の維持管理作業にこれらを活用するケースが増えています。代表的なモデルとしては、Monarch Tractor MK-V(バッテリー容量約70 kWh)、Solectrac e25およびe70(約22~70 kWh)、Fendt e100 V Vario(約100 kWh)、そしてアジア・オセアニア市場向けのクボタ製コンパクト電動トラクターなどが挙げられます。農場内での夜間充電、太陽光発電による充電システム、作業の合間を利用した短時間の補充充電といった先進的な充電戦略により、電動農業機械の実用性と普及が進んでいます。さらに、政府が支援する農業ローンの免除措置、低金利の農業融資制度、および機械購入資金の融資プログラムが、農家の近代的な機械への投資を後押ししており、農業の機械化と先進的な農業技術の導入をさらに加速させています。

政府の支援は、導入を加速させる主要な要因です。カリフォルニア州では、COREプログラムが販売時点でのインセンティブを提供しており、電気トラクターの初期費用を大幅に削減しています。支援額は通常、小型コンパクトトラクターで約16,000米ドルから、中型農業機械で43,000~130,000米ドルに及び、一部の大型カテゴリーでは適格条件に応じてさらに高額になる場合もあります。欧州では、EUグリーンディール、共通農業政策(CAP)のエコ・スキーム、およびドイツやフランスなどの各国の補助金プログラムを通じて導入が支援されており、カナダやアジア太平洋地域(APAC)の一部でも同様のクリーン機器向け資金援助が存在します。電気トラクターは従来のディーゼルモデルよりも初期費用が高くなりますが、燃料費や維持費の削減、エネルギー効率の向上、排出ガスの削減を通じて、長期的には大幅なコスト削減が期待できます。政府によるインセンティブ、有利な融資プログラム、充電インフラの拡充、そしてますます厳格化する排出規制に支えられ、主要な農業市場、特に持続可能性への取り組みが活発で農業の機械化が進んでいる地域において、電気トラクターの需要は着実に拡大すると予想されます。

「フォワーダー分野は、林業機械市場において最も急速に成長している分野であると推定されています。」

フォワーダーは、機械化林業機器において最も重要な成長セグメントの一つとして台頭しており、需要と技術導入の面では欧州が明らかに主導的な立場にあります。スウェーデン、フィンランド、中央欧州などの国々では、フォワーダーがカット・トゥ・レングス(CTL)伐採システムで広く使用されています。このシステムは、厳しい環境規制、FSC/PEFC認証要件、および木材1立方メートルあたりの土壌損傷と炭素排出量の削減への強い重視により、現代の持続可能な林業において主流となっています。OEMからの需要は、積載量12~20トン以上の範囲に集中しており、コマツの845/855/875/895や、ポンッセのバッファローおよびエレファントシリーズなど、高い生産性、急勾配地での作業、継続的な間伐サイクルを想定して設計されたモデルが人気を博しています。欧州のフォワーダー市場は、旧式のスキッダーベースのシステムが、より高精度で環境に優しく、デジタル接続された機械へと置き換えられる「フリート更新」によって牽引されています。北米では、カナダおよび米国の特定の林業地域において、特にカット・トゥ・レングス(CTL)作業向けに導入が徐々に拡大している一方、大規模な伐採作業では依然としてスキッダーが主流を占めています。John DeereやKomatsu Forestといった主要OEM各社は、テレマティクス、低燃費の油圧システム、オペレーター支援技術などを活用してフォワーダーの性能向上を図っており、今後の開発では、半自律運転、AIを活用した積載量の最適化、ハイブリッド動力システムに焦点が当てられると見込まれています。

「欧州は、地域別市場として第2位の規模になると予測されています。」

CEMAおよびVDMAによると、欧州のトラクター市場は2025年に2024年比で約22%縮小し、これは近年で最も急激な縮小の一つとなりました。フランスでは、農業所得の低迷、高金利、および買い替えサイクルの遅れにより、17.2%(27,844台)の減少となりました。トルコでは、通貨安、インフレ、購買力の低下により、36.3%(40,505台)という大幅な減少を記録し、ロシアでは供給制約や貿易制限により、31%(24,150台)減少しました。対照的に、イタリアでは、ブドウ園や果樹園における補助金主導の買い替え需要に支えられ、+14.1%(17,573台)の増加となりました。一方、ポーランドでは、EUの共通農業政策(CAP)による強力な資金援助、農場の統合、および車両の近代化の加速により、+22.1%(10,433台)の増加となりました。

トラクターの馬力別に見ると、131~250 HPのセグメントは、複合農業や請負業務における中核的な需要基盤であり続けていますが、250 HP超のセグメントは、農地の統合や生産性向上の要求が高まっていることから、フランス、ドイツ、東欧でより急速に成長しています。この移行は、EUステージV規制、2027年機械規制の枠組み、グリーン・ディールといった政策やコスト面での圧力によって、より強く推進されています。欧州における100~200 HPのEVトラクターは、依然として初期段階にあるもの急速に台頭しているセグメントであり、主にブドウ園、果樹園、温室、および自治体での用途で利用されています。これらの場面では、高出力よりも低騒音、ゼロエミッション、および精密作業が重視されています。

農業機械市場は、Deere &Company(米国)、AGCO Corporation(米国)、CNH Industrial N.V.(オランダ)、クボタ(日本)、CLAAS KGaA mbH(ドイツ)、Mahindra&Mahindra Ltd.(インド)、ISEKI(日本)、Escorts Kubota Limited(インド)、SDF Group(ドイツ)、Yanmar Holdings(日本)といった世界の企業が主導しています。これらの企業は、市場での存在感を高めるため、製品開発や提携などの戦略を採用しました。

調査範囲:

本調査では、農業機械市場をセグメント化し、出力別、駆動タイプ別、設備タイプ別、機能別、推進方式別、および地域別に分析しています。また、農業機械市場エコシステムにおける主要企業の競合情勢や企業プロファイルについても網羅しています。

当レポートの主なメリット

当レポートは、市場をリードする企業や新規参入企業に対し、農業機械市場およびそのサブセグメントにおける売上高の最も正確な推計値を提供します。当レポートは、利害関係者が競合情勢を理解し、自社のビジネスをより良い位置づけに導き、適切な市場参入戦略を策定するための洞察を得るのに役立ちます。また、当レポートは利害関係者が市場の動向を把握するのに役立ち、主要な市場促進要因、市場抑制要因、課題、および機会に関する情報を提供します。

当レポートでは、以下の点に関する洞察を提供します:

- 主要な促進要因の分析(農家向け融資免除・信用融資別政府支援、ディーラーのサービスおよびレンタル事業を支援するためのOEM/販売インセンティブ、契約農業、農業の機械化の進展)、制約要因(レンタル市場の拡大、新興国における機器の高コスト)、機会(精密農業の普及拡大、研究開発の強化および電気トラクターの導入拡大)、ならびに課題(急速に変化する排出ガス規制および義務)について、農業機械市場の成長に影響を与える要因を分析しています。

- 製品開発・イノベーション:農業機械市場における今後の技術、研究開発活動、および新製品の発売に関する詳細な洞察

- 市場開発:収益性の高い市場に関する包括的な情報-当レポートでは、さまざまな地域における農業機械市場を分析しています。

- 市場の多様化:農業機械市場における新製品、未開拓地域、最近の動向、および投資に関する網羅的な情報

- 競合分析:Deere &Company(米国)、AGCO Corporation(米国)、CNH Industrial N.V.(オランダ)、Kubota Corporation(日本)、CLAAS KGaA mbH(ドイツ)、Mahindra &Mahindra(インド)、ISEKI &(日本)、Escorts Kubota Limited(インド)、SDF Group(ドイツ)、Yanmar Holdings(日本)など、農業機械市場における主要企業の市場シェア、成長戦略、サービス提供内容について詳細に評価します。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズと未開拓分野

- 相互接続された市場と異業種間の機会

- ティア1/2/3企業による戦略的な動き

第5章 業界動向

- マクロ経済指標

- サプライチェーン分析

- エコシステム分析

- 価格分析

- 2026年~2027年の主な会議およびイベント

- 貿易分析

- 顧客ビジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ

- 事例研究分析

- 総所有コスト

- OEM分析

- 主要OEMメーカー別トラクター価格帯

- イラン・イスラエル戦争が農業機械市場に与える影響

- 主要国におけるブランド別トラクター販売台数

- OEM別トラクター生産能力

- トラクター生産能力増強のための将来投資

第6章 技術進歩、特許、イノベーション、そして将来の応用

- 主要技術

- 補完的な技術

- 隣接技術

- 特許分析

- 将来の応用

- 成功事例と実世界での応用例

第7章 規制状況

- 地域規制および遵守事項

- 規制機関、政府機関、その他の組織

- 業界標準

- 非道路移動機械排出ガス規制(NRMM)の見通し

- 北米

- 欧州

- アジア・オセアニア

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 主要な利害関係者と購入基準

- 導入における障壁と内部課題

- 最終用途産業におけるアンメットニーズ

- 市場収益性

第9章 農業用トラクター市場(出力別)

- 30馬力未満

- 30~70馬力

- 71~130馬力

- 131~250馬力

- 250馬力以上

- 業界洞察

第10章 農業機械市場(設備タイプ別)

- 穀物コンバイン

- 非穀物用コンバイン

- ベーラー

- 自走式噴霧器

- トラクター搭載型噴霧器

- 業界洞察

第11章 農業機械市場(機能別)

- 耕作と耕うん

- 種まきと植え付け

- 植物保護と施肥

- 収穫と脱穀

- その他の機能

- 業界洞察

第12章 電動農業用トラクター市場(推進方式別)

- バッテリー式電気自動車

- ハイブリッド電気自動車

- 水素

- 業界洞察

第13章 農業用トラクターレンタル市場概要

- 賃貸経済学と資産活用分析

- 農業機械レンタル事業モデルの進化

- OEM向けレンタルプログラムと戦略

- 将来の収益分析

第14章 農業用トラクターレンタル市場(駆動タイプ別)

- 二輪駆動(2WD)

- 四輪駆動(4WD)

- 業界洞察

第15章 農業機械レンタル市場(設備タイプ別)

- トラクター

- コンバイン

- 噴霧器

- ベーラー

- その他

- 業界洞察

第16章 林業機械市場(製品タイプ別)

- フェラーバンチャー

- 収穫機

- フォワーダー

- ローダー

- スキッダー

- スイングマシン

- その他

- 業界洞察

第17章 農業用トラクター市場(地域別)

- アジア・オセアニア

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- その他

- 欧州

- フランス

- ドイツ

- イタリア

- ポーランド

- ロシア

- スペイン

- トルコ

- 英国

- その他

- 北米

- 米国

- カナダ

- メキシコ

- 世界のその他の地域

- アルゼンチン

- ブラジル

- その他

- 業界洞察

第18章 競合情勢

- 概要

- 主要参入企業の戦略/強み、2022年~2026年

- 収益分析、2021年~2025年

- 市場シェア分析、2025年

- 企業評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要企業、2025年

- 企業評価マトリックス:スタートアップ/中小企業、2025年

- 競合シナリオ

第19章 企業プロファイル

- 主要参入企業

- DEERE & COMPANY

- CNH INDUSTRIAL

- MAHINDRA & MAHINDRA

- AGCO CORPORATION

- KUBOTA CORPORATION

- CLAAS KGAA

- ISEKI & CO., LTD.

- ESCORTS KUBOTA LIMITED

- SDF GROUP

- YANMAR HOLDINGS CO., LTD.

- その他の企業

- JCB

- TRACTORS AND FARM EQUIPMENT

- SONALIKA

- TYM CORPORATION

- DAEDONG CORPORATION

- EXEL INDUSTRIES LTD.

- BUCHER INDUSTRIES AG

- ZETOR TRACTORS A.S.

- ARGO TRACTORS S.P.A.

- CONCERN TRACTOR PLANTS

- AMAZONE H. DREYER GMBH & CO. KG

- BUHLER INDUSTRIES INC.

- AUTONOMOUS TRACTOR CORPORATION

- CHANGZHOU DONGFENG AGRICULTURAL MACHINERY GROUP CO., LTD.

- CHINA NATIONAL MACHINERY INDUSTRY CORPORATION

- WEICHAI LOVOL HEAVY INDUSTRY CO., LTD.

- BERNARD KRONE HOLDING SE & CO.

- VERMEER CORPORATION

- POTTINGER LANDTECHNIK GMBH

- MINSK TRACTOR WORKS

- HENAN QIANLI MACHINERY CO., LTD.

- MASCHIO GASPARDO S.P.A.

- ALAMO GROUP INC.

- KOMATSU LTD.

- CATERPILLAR INC.

- PONSSE PLC

- TIGERCAT INTERNATIONAL INC.

第20章 調査手法

第21章 市場における提言

第22章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 446 Pages

- 納期

- 即納可能