|

|

市場調査レポート

商品コード

1305955

自動車用シリコーンの世界市場:種類別 (エラストマー、樹脂、ジェル、流体)・用途別 (内装材・外装材、エンジン、電気、タイヤ)・地域別 (北米、欧州、アジア太平洋、中東・アフリカ、南米) の将来予測 (2028年まで)Automotive Silicone Market by Type (Elastomers, Resins, Gels, Fluids), Application (Interior & Exterior, Engines, Electrical, Tires) and Region (North America, Europe, Asia Pacific, Middle East & Africa, South America) - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用シリコーンの世界市場:種類別 (エラストマー、樹脂、ジェル、流体)・用途別 (内装材・外装材、エンジン、電気、タイヤ)・地域別 (北米、欧州、アジア太平洋、中東・アフリカ、南米) の将来予測 (2028年まで) |

|

出版日: 2023年06月27日

発行: MarketsandMarkets

ページ情報: 英文 173 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の自動車用シリコーンの市場規模は、2023年の24億米ドルから、2028年には34億米ドルに達し、7.3%のCAGRで成長すると予測されています。

自動車産業の成長は、自動車用シリコーン市場拡大の重要な触媒です。この需要急増の主な要因は、産業成長、インフラプロジェクトの投資拡大、スマートシティ、技術進歩などです。さらに、世界人口の増加、中間所得層の増加、耐久消費財に対する消費者の嗜好の変化なども、自動車分野における自動車用シリコーン需要の拡大に寄与しています。

"電気向けのセグメントが、2022年に第2位のシェアを占める"

自動車用シリコーンは、自動車の電気分野で重要な役割を果たしており、信頼性の高い送電、卓越した減衰、絶縁特性を提供しています。イグニッションケーブル、スパークプラグブーツ、ハイテンション (HT) ケーブルに広く採用され、スムーズな電気接続を確保し、熱や環境要因から保護しています。自動車用シリコーンは、送電効率を最適化し、電気システムの性能を高め、電圧の乱れや漏れを防ぎます。自動車用シリコーンは、その優れた特性により、信頼性が高く効率的な電気システムの維持に不可欠であり、自動車の信頼性と性能を向上させます。

"地域別では、アジア太平洋が2022年に金額ベースで最大の市場となる"

アジア太平洋は、2022年に金額ベースで世界最大の自動車用シリコーン市場となっています。アジア太平洋市場は技術革新が牽引役となっています。同地域の産業拡大と自動車産業の成長が自動車用シリコーンの消費を促進しています。また、世界経済の改善も市場の成長を後押しすると予想されます。中国はアジア太平洋地域の主要市場であり、予測期間中に高い成長が見込まれます。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ポーターのファイブフォース分析

- バリューチェーン分析

- マクロ経済分析

- 景気後退の評価

第6章 自動車用シリコーン市場:用途別

- イントロダクション

- 内装材・外装材

- エアバッグ

- 排気用ハンガー

- 外装用トリム

- ヘッドランプ

- ホース

- 内装用トリム

- メンブレン

- ショックアブソーバー

- グロメット

- エンジン

- 封止・ポッティング・接合

- 濾過

- ガスケット

- ラジエーターシール

- 振動減衰

- 電気

- 送電

- 減衰・絶縁

- 点火ケーブル

- スパークプラグブーツ

- HTケーブル

- タイヤ

- その他

第7章 自動車用シリコーン市場:種類別

- イントロダクション

- エラストマー

- 樹脂

- ジェル

- 流体

第8章 自動車用シリコーン市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

第9章 競合情勢

- 概要

- 主要市場プレーヤーのランキング分析 (2022年)

- 市場評価マトリックス

- 企業評価マトリックス:ティア1 (2022年)

- スタートアップ・中小企業 (SME) の評価マトリックス

- 競合シナリオ

第10章 企業プロファイル

- 主要企業

- THE DOW CHEMICAL COMPANY

- WACKER CHEMIE AG

- MOMENTIVE

- SHIN-ETSU CHEMICAL CO. LTD.

- ELKEM ASA

- EVONIK INDUSTRIES AG

- GELEST INC.

- HENKEL

- PRIMASIL SILICONES

- SILTECH CORPORATION

- その他の主な企業

- CHT GROUP

- BRB INTERNATIONAL

- NOLATO

- REISS MANUFACTURING

- KIBARU MANUFACTURING SDN. BHD.

- MCCOY PERFORMANCE SILICONES

- MILLIKEN

- NOVAGUARD SOLUTIONS

- PERMATEX

- ROGERS CORPORATION

- MESGO

- SILICONE SOLUTIONS

- SIMTECH SILICONE PARTS

- SPECIALTY SILICONE PRODUCTS INC.

- WYNCA TINYO SILICONE

第11章 付録

The automotive silicone market is projected to reach USD 3.4 billion by 2028, at a CAGR of 7.3% from USD 2.4 billion in 2023. The growing automotive industry is a key catalyst for the expansion of the automotive silicone market. This demand surge is primarily propelled by factors like the growth of industries, increased investments in infrastructure projects, smart cities, and advancements in technology. Additionally, increasing global population, rising middle-class incomes, and changing consumer preferences for durable goods contribute to the growing demand for automotive silicone in automotive sector.

"Electrical application segment is expected to account for the second-largest share in 2022."

Automotive silicone plays a critical role in the automotive electrical segment, offering dependable power transmission, exceptional damping, and insulation characteristics. It is extensively employed in ignition cables, spark plug boots, and high-tension (HT) cables to ensure smooth electrical connectivity and protection from heat and environmental factors. Automotive silicone optimizes power transfer efficiency, enhances electrical system performance, and safeguards against voltage disruptions or leaks. With its remarkable attributes, automotive silicone is indispensable for maintaining reliable and efficient electrical systems, thereby bolstering vehicle reliability and performance.

"Based on region, Asia Pacific region was the largest market for automotive silicone in 2022, in terms of value."

Asia Pacific was the largest market for global automotive silicone, in terms of value, in 2022. The market in Asia Pacific is driven by innovation. Industrial expansion and growing automotive indsutry in the region are driving the consumption of automotive silicone. The growth of the market is also expected to be supported by the improving global economy. China is the key market in Asia Pacific and is expected to witness high growth during the forecast period because of the high use of automotive silicone in various automotive silicone in the region.

In the process of determining and verifying the market size for several segments and subsegments identified through secondary research, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees are as follows:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-Level - 35%, Director Level - 25%, and Others - 40%

- By Region: Asia Pacific - 40%, North America - 30%, Europe - 20%, Middle East & Africa-5%, and Latin America-5%

The key players in this market are include The Dow Chemical Company (US), Wacker Chemie AG ( Germany), Momentive (US), Shin-Etsu Chemical Co. Ltd. (Japan), Elkem ASA (Norway), Evonik Industries AG (Germany), Gelest Inc.(US), Henkel (Germany), Primasil Silicones (UK), and Slitch Corporation (Canada).

Research Coverage

This report segments the market for automotive siliconemarket on the basis of filter type, filter media, application , region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and mergers & acquisition associated with the market for automotive siliconemarket.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view on the competitive landscape; emerging and high-growth segments of the automotive silicone market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing automotive industry in Asia Pacific, Increasing demand for high efficiency and lightweight materials in the automotive industry, Superior properties of silicone), restraints (Growing use of electric vehicles ), opportunities (High growth opportunities in the emerging economies in Asia Pacific, Growing demand in the transportation industry, Advancements in autonomous technology), and challenges (Fluctuating raw material prices, Supply chain challenges in the automotive silicone market) influencing the growth of the automotive silicone market

- Market Penetration: Comprehensive information on automotive silicone market offered by top players in the global automotive silicone market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the automotive silicone market.

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for automotive silicone market across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global automotive silicone market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the automotive silicone market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.4 REGIONS COVERED

- 1.4.1 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNIT CONSIDERED

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 AUTOMOTIVE SILICONE MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primary interviews

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 2 AUTOMOTIVE SILICONE MARKET: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 3 AUTOMOTIVE SILICONE MARKET: TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- FIGURE 4 AUTOMOTIVE SILICONE MARKET: DATA TRIANGULATION

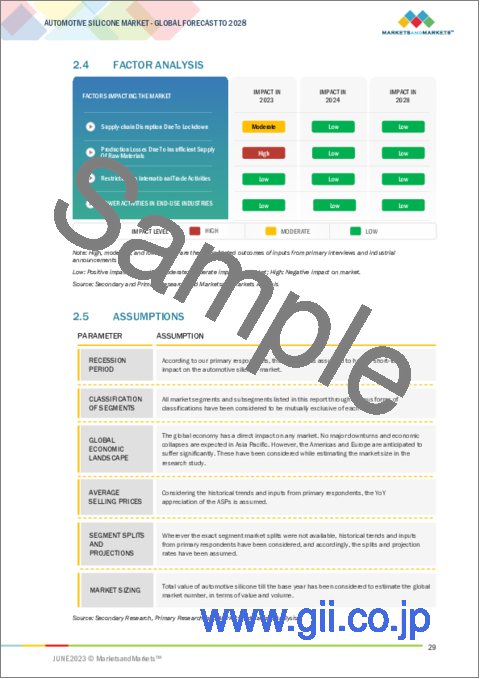

- 2.4 FACTOR ANALYSIS

- 2.5 ASSUMPTIONS

3 EXECUTIVE SUMMARY

- FIGURE 5 ELECTRICAL APPLICATION TO WITNESS FASTEST GROWTH BETWEEN 2023 AND 2028

- FIGURE 6 ASIA PACIFIC LED AUTOMOTIVE SILICONE MARKET IN 2022

4 PREMIUM INSIGHTS

- 4.1 SIGNIFICANT OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE SILICONE MARKET

- FIGURE 7 HIGH GROWTH POTENTIAL IN ASIA PACIFIC TO DRIVE MARKET

- 4.2 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION AND COUNTRY, 2022

- FIGURE 8 INTERIOR & EXTERIOR APPLICATION DOMINATED MARKET IN ASIA PACIFIC

- 4.3 AUTOMOTIVE SILICONE MARKET, BY APPLICATION

- FIGURE 9 INTERIOR & EXTERIOR APPLICATION TO LEAD AUTOMOTIVE SILICONE MARKET DURING FORECAST PERIOD

- 4.4 AUTOMOTIVE SILICONE MARKET, BY COUNTRY

- FIGURE 10 CHINA TO BE FASTEST-GROWING AUTOMOTIVE SILICONE MARKET

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 11 DRIVERS, RESTRAINTS, CHALLENGES, AND OPPORTUNITIES IN AUTOMOTIVE SILICONE MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Growing automotive industry in Asia Pacific

- 5.2.1.2 Increasing demand for high-efficiency and lightweight materials in automotive industry

- 5.2.1.3 Superior properties of silicone

- 5.2.2 RESTRAINTS

- 5.2.2.1 Growing use of electric vehicles

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 High growth opportunities in emerging economies of Asia Pacific

- 5.2.3.2 Growing demand in transportation industry

- 5.2.3.3 Advancements in autonomous driving technology

- 5.2.4 CHALLENGES

- 5.2.4.1 Fluctuating raw material prices

- 5.2.4.2 Supply chain challenges in automotive silicone market

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 12 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 BARGAINING POWER OF SUPPLIERS

- 5.3.2 BARGAINING POWER OF BUYERS

- 5.3.3 THREAT OF SUBSTITUTES

- 5.3.4 THREAT OF NEW ENTRANTS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- TABLE 1 AUTOMOTIVE SILICONE MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.4.1 RAW MATERIAL SUPPLIERS

- 5.4.2 MANUFACTURERS

- 5.4.3 DISTRIBUTORS

- 5.4.4 END CONSUMERS

- FIGURE 13 VALUE CHAIN ANALYSIS

- 5.5 MACROECONOMIC ANALYSIS

- TABLE 2 PROJECTED REAL GDP GROWTH (ANNUAL PERCENT CHANGE) OF KEY COUNTRIES, 2018-2025

- 5.6 ECONOMIC RECESSION ASSESSMENT

- 5.6.1 TRENDS IN AUTOMOTIVE INDUSTRY

- TABLE 3 VEHICLE PRODUCTION STATISTICS, BY COUNTRY, 2021-2022 (UNITS)

6 AUTOMOTIVE SILICONE MARKET, BY APPLICATION

- 6.1 INTRODUCTION

- FIGURE 14 INTERIOR & EXTERIOR APPLICATION SEGMENT TO ACCOUNT FOR LARGEST MARKET SIZE DURING FORECAST PERIOD

- TABLE 4 AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 5 AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 6 AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 7 AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 6.2 INTERIOR & EXTERIOR

- 6.2.1 HEAT RESISTANCE PROPERTY OF SILICONE TO DRIVE ITS USE

- 6.2.2 AIRBAGS

- 6.2.3 EXHAUST HANGERS

- 6.2.4 EXTERIOR TRIMS

- 6.2.5 HEADLAMPS

- 6.2.6 HOSES

- 6.2.7 INTERIOR TRIMS

- 6.2.8 MEMBRANES

- 6.2.9 SHOCK ABSORBERS

- 6.2.10 GROMMETS

- 6.3 ENGINES

- 6.3.1 SEALING AND BONDING PROPERTIES OF SILICONE TO DRIVE ITS USE

- 6.3.2 SEALING, POTTING & BONDING

- 6.3.3 FILTRATION

- 6.3.4 GASKETS

- 6.3.5 RADIATOR SEALS

- 6.3.6 VIBRATION DAMPENING

- 6.4 ELECTRICAL

- 6.4.1 DAMPING AND INSULATION PROPERTIES TO MAKE SILICONE FAVORABLE FOR USE IN ELECTRICAL CONNECTIONS

- 6.4.2 POWER TRANSMISSION

- 6.4.3 DAMPING & INSULATION

- 6.4.4 IGNITION CABLES

- 6.4.5 SPARK PLUG BOOTS

- 6.4.6 HT CABLES

- 6.5 TIRES

- 6.5.1 SEMI-PERMANENT FORMULATIONS OF SILICONE FILMS TO DRIVE THEIR APPLICATION

- 6.6 OTHERS

7 AUTOMOTIVE SILICONE MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 ELASTOMERS

- 7.3 RESINS

- 7.4 GELS

- 7.5 FLUIDS

8 AUTOMOTIVE SILICONE MARKET, BY REGION

- 8.1 INTRODUCTION

- FIGURE 15 ASIA PACIFIC TO ACCOUNT FOR LARGEST SHARE IN GLOBAL AUTOMOTIVE SILICONE MARKET

- TABLE 8 AUTOMOTIVE SILICONE MARKET, BY REGION, 2019-2022 (KILOTON)

- TABLE 9 AUTOMOTIVE SILICONE MARKET, BY REGION, 2023-2028 (KILOTON)

- TABLE 10 AUTOMOTIVE SILICONE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 11 AUTOMOTIVE SILICONE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.2 NORTH AMERICA

- FIGURE 16 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET SNAPSHOT

- TABLE 12 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 13 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 14 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 15 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 16 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 17 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 18 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 19 NORTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.2.1 RECESSION IMPACT

- 8.2.2 US

- 8.2.2.1 Demand to decline due to growing market maturity

- TABLE 20 US: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 21 US: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 22 US: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 23 US: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.2.3 CANADA

- 8.2.3.1 Robust automotive manufacturing and presence of key automotive manufacturers to drive growth

- TABLE 24 CANADA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 25 CANADA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 26 CANADA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 27 CANADA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.2.4 MEXICO

- 8.2.4.1 Significant government investments in automotive industry to drive market

- TABLE 28 MEXICO: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 29 MEXICO: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 30 MEXICO: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 31 MEXICO: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.3 EUROPE

- FIGURE 17 EUROPE: AUTOMOTIVE SILICONE MARKET SNAPSHOT

- TABLE 32 EUROPE: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 33 EUROPE: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 34 EUROPE: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 35 EUROPE: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 36 EUROPE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 37 EUROPE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 38 EUROPE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 39 EUROPE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.3.1 RECESSION IMPACT

- 8.3.2 GERMANY

- 8.3.2.1 Demand to grow in automotive electronics segment

- TABLE 40 GERMANY: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 41 GERMANY: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 42 GERMANY: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 43 GERMANY: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.3.3 FRANCE

- 8.3.3.1 Steady growth in automotive manufacturing to drive demand

- TABLE 44 FRANCE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 45 FRANCE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 46 FRANCE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 47 FRANCE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.3.4 UK

- 8.3.4.1 Presence of luxury car manufacturers to drive demand for automotive silicones

- TABLE 48 UK: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 49 UK: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 50 UK: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 51 UK: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.3.5 ITALY

- 8.3.5.1 Rebound of automotive manufacturing sector favorable for market growth

- TABLE 52 ITALY: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 53 ITALY: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 54 ITALY: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 55 ITALY: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.3.6 SPAIN

- 8.3.6.1 Immense growth potential of automotive industry lucrative for market growth

- TABLE 56 SPAIN: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 57 SPAIN: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 58 SPAIN: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 59 SPAIN: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.3.7 REST OF EUROPE

- TABLE 60 REST OF EUROPE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 61 REST OF EUROPE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 62 REST OF EUROPE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 63 REST OF EUROPE: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.4 ASIA PACIFIC

- FIGURE 18 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET SNAPSHOT

- TABLE 64 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 65 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 66 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 67 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 68 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 69 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 70 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 71 ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.4.1 RECESSION IMPACT

- 8.4.2 CHINA

- 8.4.2.1 Availability of cheap raw materials and moderately stringent regulatory framework to drive market

- TABLE 72 CHINA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 73 CHINA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 74 CHINA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 75 CHINA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.4.3 JAPAN

- 8.4.3.1 Increasing demand for automotive electronics to drive market

- TABLE 76 JAPAN: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 77 JAPAN: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 78 JAPAN: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 79 JAPAN: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.4.4 INDIA

- 8.4.4.1 Favorable location for low-cost automotive manufacturing

- TABLE 80 INDIA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 81 INDIA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 82 INDIA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 83 INDIA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.4.5 SOUTH KOREA

- 8.4.5.1 Development in automotive manufacturing industry to drive demand

- TABLE 84 SOUTH KOREA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 85 SOUTH KOREA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 86 SOUTH KOREA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 87 SOUTH KOREA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.4.6 REST OF ASIA PACIFIC

- TABLE 88 REST OF ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 89 REST OF ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 90 REST OF ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 91 REST OF ASIA PACIFIC: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.5 MIDDLE EAST & AFRICA

- TABLE 92 MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 93 MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 94 MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 95 MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 96 MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 97 MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 98 MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 99 MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.5.1 SAUDI ARABIA

- 8.5.1.1 Government initiatives to promote automotive manufacturing to drive demand

- TABLE 100 SAUDI ARABIA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 101 SAUDI ARABIA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 102 SAUDI ARABIA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 103 SAUDI ARABIA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.5.2 SOUTH AFRICA

- 8.5.2.1 Key players establishing automotive business to create demand for automotive silicone

- TABLE 104 SOUTH AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 105 SOUTH AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 106 SOUTH AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 107 SOUTH AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.5.3 REST OF MIDDLE EAST & AFRICA

- TABLE 108 REST OF MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 109 REST OF MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 110 REST OF MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 111 REST OF MIDDLE EAST & AFRICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.6 SOUTH AMERICA

- TABLE 112 SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 113 SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 114 SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 115 SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 116 SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 117 SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 118 SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 119 SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.6.1 BRAZIL

- 8.6.1.1 Favorable trade and investment policies to attract private investments

- TABLE 120 BRAZIL: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 121 BRAZIL: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 122 BRAZIL: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 123 BRAZIL: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.6.2 ARGENTINA

- 8.6.2.1 Improvements in country's automotive investment to drive market

- TABLE 124 ARGENTINA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 125 ARGENTINA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 126 ARGENTINA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 127 ARGENTINA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.6.3 REST OF SOUTH AMERICA

- TABLE 128 REST OF SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (KILOTON)

- TABLE 129 REST OF SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- TABLE 130 REST OF SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 131 REST OF SOUTH AMERICA: AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

9 COMPETITIVE LANDSCAPE

- 9.1 OVERVIEW

- FIGURE 19 COMPANIES ADOPTED ACQUISITIONS AND EXPANSIONS AS KEY GROWTH STRATEGIES BETWEEN 2018 AND 2023

- 9.2 RANKING ANALYSIS OF KEY MARKET PLAYERS, 2022

- FIGURE 20 RANKING OF TOP FIVE PLAYERS IN AUTOMOTIVE SILICONES MARKET, 2022

- 9.3 MARKET EVALUATION MATRIX

- TABLE 132 MARKET EVALUATION MATRIX

- 9.4 COMPANY EVALUATION MATRIX, 2022 (TIER 1)

- 9.4.1 STARS

- 9.4.2 EMERGING LEADERS

- 9.4.3 PERVASIVE PLAYERS

- 9.4.4 PARTICIPANTS

- FIGURE 21 COMPANY EVALUATION MATRIX, 2022

- 9.5 START-UPS AND SMALL & MEDIUM-SIZED ENTERPRISES (SMES) EVALUATION MATRIX

- 9.5.1 PROGRESSIVE COMPANIES

- 9.5.2 RESPONSIVE COMPANIES

- 9.5.3 STARTING BLOCKS

- 9.5.4 DYNAMIC COMPANIES

- FIGURE 22 STARTUPS AND SMES EVALUATION MATRIX, 2022

- 9.6 COMPETITIVE SCENARIO

- 9.6.1 PRODUCT LAUNCHES

- TABLE 133 PRODUCT LAUNCHES, 2018-2023

- TABLE 134 NEW TECHNOLOGY, 2018-2023

- 9.6.2 DEALS

- TABLE 135 DEALS, 2018-2022

- 9.6.3 OTHER DEVELOPMENTS

- TABLE 136 OTHER DEVELOPMENTS, 2018-2022

10 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, MnM View Right to win, Strategic choices made, Weaknesses and competitive threats) **

- 10.1 KEY PLAYERS

- 10.1.1 THE DOW CHEMICAL COMPANY

- TABLE 137 THE DOW CHEMICAL COMPANY: COMPANY OVERVIEW

- FIGURE 23 THE DOW CHEMICAL COMPANY: COMPANY SNAPSHOT

- TABLE 138 THE DOW CHEMICAL COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 139 THE DOW CHEMICAL COMPANY: PRODUCT LAUNCHES

- TABLE 140 THE DOW CHEMICAL COMPANY: OTHER DEVELOPMENTS

- 10.1.2 WACKER CHEMIE AG

- TABLE 141 WACKER CHEMIE AG: COMPANY OVERVIEW

- FIGURE 24 WACKER CHEMIE AG: COMPANY SNAPSHOT

- TABLE 142 WACKER CHEMIE AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 143 WACKER CHEMIE AG: PRODUCT LAUNCHES

- TABLE 144 WACKER CHEMIE AG: DEALS

- TABLE 145 WACKER CHEMIE AG: OTHER DEVELOPMENTS

- 10.1.3 MOMENTIVE

- TABLE 146 MOMENTIVE: COMPANY OVERVIEW

- TABLE 147 MOMENTIVE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 148 MOMENTIVE: PRODUCT LAUNCHES

- TABLE 149 MOMENTIVE: DEALS

- TABLE 150 MOMENTIVE: OTHER DEVELOPMENTS

- 10.1.4 SHIN-ETSU CHEMICAL CO. LTD.

- TABLE 151 SHIN-ETSU CHEMICAL CO., LTD.: COMPANY OVERVIEW

- FIGURE 25 SHIN-ETSU CHEMICAL CO. LTD.: COMPANY SNAPSHOT

- TABLE 152 SHIN-ETSU CHEMICAL CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 153 SHIN-ETSU CHEMICAL CO., LTD.: PRODUCT LAUNCHES

- TABLE 154 SHIN-ETSU CHEMICAL CO., LTD.: OTHER DEVELOPMENTS

- 10.1.5 ELKEM ASA

- TABLE 155 ELKEM ASA: COMPANY OVERVIEW

- FIGURE 26 ELKEM ASA: COMPANY SNAPSHOT

- TABLE 156 ELKEM ASA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 157 ELKEM ASA: PRODUCT LAUNCHES

- TABLE 158 ELKEM ASA: DEALS

- TABLE 159 ELKEM ASA: OTHER DEVELOPMENTS

- 10.1.6 EVONIK INDUSTRIES AG

- TABLE 160 EVONIK INDUSTRIES AG: COMPANY OVERVIEW

- FIGURE 27 EVONIK INDUSTRIES AG: COMPANY SNAPSHOT

- TABLE 161 EVONIK INDUSTRIES AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 162 EVONIK INDUSTRIES AG: OTHER DEVELOPMENTS

- 10.1.7 GELEST INC.

- TABLE 163 GELEST INC.: COMPANY OVERVIEW

- TABLE 164 GELEST INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 165 GELEST INC.: DEALS

- 10.1.8 HENKEL

- TABLE 166 HENKEL: COMPANY OVERVIEW

- FIGURE 28 HENKEL: COMPANY SNAPSHOT

- TABLE 167 HENKEL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 168 HENKEL: DEALS

- TABLE 169 HENKEL: OTHER DEVELOPMENTS

- 10.1.9 PRIMASIL SILICONES

- TABLE 170 PRIMASIL SILICONES: COMPANY OVERVIEW

- TABLE 171 PRIMASIL SILICONES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 172 PRIMASIL SILICONES: DEALS

- 10.1.10 SILTECH CORPORATION

- TABLE 173 SILTECH CORPORATION: COMPANY OVERVIEW

- TABLE 174 SILTECH CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 175 SILTECH CORPORATION: OTHER DEVELOPMENTS

- 10.3 OTHER KEY COMPANIES

- 10.3.1 CHT GROUP

- 10.3.2 BRB INTERNATIONAL

- 10.3.3 NOLATO

- 10.3.4 REISS MANUFACTURING

- 10.3.5 KIBARU MANUFACTURING SDN. BHD.

- 10.3.6 MCCOY PERFORMANCE SILICONES

- 10.3.7 MILLIKEN

- 10.3.8 NOVAGUARD SOLUTIONS

- 10.3.9 PERMATEX

- 10.3.10 ROGERS CORPORATION

- 10.3.11 MESGO

- 10.3.12 SILICONE SOLUTIONS

- 10.3.13 SIMTECH SILICONE PARTS

- 10.3.14 SPECIALTY SILICONE PRODUCTS INC.

- 10.3.15 WYNCA TINYO SILICONE

- *Details on Business Overview, Products Offered, Recent Developments, MnM View, Right to win, Strategic choices made, Weaknesses and competitive threats might not be captured in case of unlisted companies.

11 APPENDIX

- 11.1 INSIGHTS FROM INDUSTRY EXPERTS

- 11.2 DISCUSSION GUIDE

- 11.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 11.4 CUSTOMIZATION OPTIONS

- 11.5 RELATED REPORTS

- 11.6 AUTHOR DETAILS