|

|

市場調査レポート

商品コード

1745106

デジタル病理検査の世界市場:製品別、タイプ別、用途別、エンドユーザー別、地域別 - 2030年までの予測Digital Pathology Market by Product (Scanner, Software, Storage System), Type (Human, Veterinary), Application (Teleconsultation, Training, Disease Diagnosis, Drug Discovery), End User (Pharma & Biotech, Academia, Hospitals) - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| デジタル病理検査の世界市場:製品別、タイプ別、用途別、エンドユーザー別、地域別 - 2030年までの予測 |

|

出版日: 2025年06月03日

発行: MarketsandMarkets

ページ情報: 英文 283 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

デジタル病理検査の市場規模は、タイプ別にスキャナー、ストレージシステム、ソフトウェアの3つに区分されます。

デジタルパソロジーのワークフローにおけるこれらの機器の重要性を考えると、2024年にはスキャナーが製品カテゴリーで最大のシェアを占めています。スキャナは、病理医が組織サンプルをコンピュータ画面上で閲覧・分析するために不可欠であり、スキャナは物理的なスライドガラスを高解像度のデジタル画像に変換します。診断用リモートアクセスの開発は、病理医が物理的な場所を問わず症例を評価できるようにすることで、病理学サービスのアクセシビリティと効率性を向上させるために最も重要であり、そのためスキャナーの需要が高まっています。スキャニング速度の向上や高解像度のイメージングなど、スキャナ技術の進歩は、ワークフローの増加、診断精度の向上、検査室や医療施設の投資価値の向上をもたらしています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2024年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2024年~2030年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント | 製品別、タイプ別、用途別、エンドユーザー別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカ |

がん、心血管疾患、感染症など、タイムリーで正確な診断結果を必要とする複雑で慢性的な疾患の世界の負担が増加していることが主な理由です。

通常、顕微鏡の接眼レンズの下で行われるデジタル病理検査、検査、診断は、高解像度画像の生成、自動化された分析の提供、画像保存、クラウドストレージ、遠隔病理学スライド共有サービスの提供など、多くの面で有利です。同様に重要なのは、様々な施設での共同相談や調整、専門医によるセカンドオピニオンを含む遠隔コンサルテーションを提供できるという、他に類を見ない利点です。

さらに、デジタル病理検査は、人工知能(AI)、機械学習(ML)、ディープラーニング画像認識などの最新技術を統合するために急速に採用され、進化しています。これらはすべて、診断精度の向上、所要時間の短縮、さらには微妙な組織学的パターンの認識に役立っており、デジタル病理検査を世界中の検査室や病院における診療の基礎的要素にしています。

北米は、成熟したヘルスケアシステムとヘルスケア技術開拓に向けた大規模な財政投資により、2024年のデジタル病理検査市場をリードしました。北米、特に米国とカナダの規制環境は、新興のデジタル病理技術に対する比較的迅速な審査と承認プロセスをサポートしています。このことは、ヘルスケア提供者の意識の高まりや高度な診断ソリューションに対する需要の高まりと相まって、この地域全体におけるデジタル病理検査の強力な普及を後押ししています。

当レポートでは、世界のデジタル病理検査市場について調査し、製品別、タイプ別、用途別、エンドユーザー別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 業界動向

- 技術分析

- 価格分析

- バリューチェーン分析

- エコシステム分析

- ポーターのファイブフォース分析

- HSコード

- 規制状況

- 特許分析

- ケーススタディ分析

- 2025年~2026年の主な会議とイベント

- 主要な利害関係者と購入基準

- エンドユーザー分析

- ビジネスモデル分析

- 投資と資金調達のシナリオ

- AIがデジタル病理検査市場に与える影響

- 米国関税がデジタル病理検査市場に与える影響

- 価格影響分析

- 国/地域への影響

第6章 デジタル病理検査市場(製品別)

- イントロダクション

- スキャナー

- ソフトウェア

- ソフトウェア(導入モデル別)

- ストレージシステム

第7章 デジタル病理検査市場(タイプ別)

- イントロダクション

- ヒト

- 動物

第8章 デジタル病理検査市場(用途別)

- イントロダクション

- 創薬

- 病気の診断

- トレーニングと教育

第9章 デジタル病理検査市場(エンドユーザー別)

- イントロダクション

- 製薬・バイオテクノロジー企業

- 病院・検査機関

- 学術研究機関

- 診断検査室

- 獣医学研究所

第10章 デジタル病理検査市場(地域別)

- イントロダクション

- 北米

- 北米:マクロ経済見通し

- 米国

- カナダ

- 欧州

- 欧州:マクロ経済見通し

- ドイツ

- 英国

- スウェーデン

- フランス

- スペイン

- イタリア

- その他

- アジア太平洋

- アジア太平洋:マクロ経済見通し

- 中国

- 日本

- インド

- その他

- ラテンアメリカ

- ラテンアメリカ:マクロ経済見通し

- ブラジル

- メキシコ

- その他

- 中東・アフリカ

- 市場の成長を支えるヘルスケアインフラの改善

- 中東・アフリカのマクロ経済見通し

- GCC諸国

- その他

第11章 競合情勢

- 概要

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 企業評価と財務指標

- ブランド/ソフトウェア比較分析

- 競合シナリオ

第12章 企業プロファイル

- 主要参入企業

- DANAHER CORPORATION

- HOFFMANN-LA ROCHE LTD.

- SECTRA AB

- HAMAMATSU PHOTONICS K.K.

- KONINKLIJKE PHILIPS N.V.

- AKOYA BIOSCIENCES, INC.

- FUJIFILM HOLDINGS CORPORATION

- HOLOGIC, INC.

- 3DHISTECH LTD.

- APOLLO ENTERPRISE IMAGING CORP.

- XIFIN, INC.

- HURON DIGITAL PATHOLOGY

- INDICA LABS

- OPTRASCAN, INC.

- GLENCOE SOFTWARE, INC.

- AIFORIA TECHNOLOGIES OY

- PAIGE AI, INC.

- PROSCIA, INC.

- その他の企業

- QUEST DIAGNOSTICS

- KONFOONG BIOTECH INTERNATIONAL CO., LTD.

- MIKROSCAN TECHNOLOGIES, INC.

- MOTIC DIGITAL PATHOLOGY

- KANTERON SYSTEMS

- MORPHLE LABS INC.

- EW HEALTHCARE PARTNERS

第13章 付録

List of Tables

- TABLE 1 FACTOR ANALYSIS

- TABLE 2 RISK ASSESSMENT ANALYSIS

- TABLE 3 INCIDENCE OF CANCER, BY REGION, 2020 VS. 2030 VS. 2040 (MILLION)

- TABLE 4 AVERAGE SELLING PRICE TREND OF DIGITAL PATHOLOGY PRODUCTS, BY REGION

- TABLE 5 AVERAGE SELLING PRICE OF DIGITAL PATHOLOGY PRODUCTS

- TABLE 6 DIGITAL PATHOLOGY MARKET: PORTER'S FIVE FORCES

- TABLE 7 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 US FDA: MEDICAL DEVICE CLASSIFICATION

- TABLE 9 US: MEDICAL DEVICE REGULATORY APPROVAL PROCESS

- TABLE 10 CANADA: MEDICAL DEVICE REGULATORY APPROVAL PROCESS

- TABLE 11 EUROPE: CLASSIFICATION OF IVD DEVICES

- TABLE 12 JAPAN: MEDICAL DEVICE CLASSIFICATION UNDER PMDA

- TABLE 13 CHINA: CLASSIFICATION OF MEDICAL DEVICES

- TABLE 14 LIST OF PATENTS/PATENT APPLICATIONS

- TABLE 15 CASE STUDY 1: ASSESSING IMAGE QUALITY: A COMPARATIVE MULTI-ASSESSMENT EVALUATION OF APERIO GT 450 DX

- TABLE 16 CASE STUDY 2: HOW TO PROMOTE PATHOLOGY WORKFLOW EFFICIENCY

- TABLE 17 CASE STUDY 3: ARTIFICIAL INTELLIGENCE IN DIGITAL PATHOLOGY

- TABLE 18 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR DIGITAL PATHOLOGY PRODUCTS

- TABLE 19 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR DIGITAL PATHOLOGY, BY PRODUCT

- TABLE 20 KEY BUYING CRITERIA FOR DIGITAL PATHOLOGY PRODUCTS

- TABLE 21 UNMET NEEDS IN DIGITAL PATHOLOGY MARKET

- TABLE 22 END-USER EXPECTATIONS IN DIGITAL PATHOLOGY MARKET

- TABLE 23 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 24 DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 25 SCANNING MAGNIFICATION AND APPLICATIONS

- TABLE 26 DIGITAL PATHOLOGY SCANNERS OFFERED BY KEY MARKET PLAYERS

- TABLE 27 DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 28 DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 29 BRIGHTFIELD SCANNERS OFFERED BY KEY MARKET PLAYERS

- TABLE 30 BRIGHTFIELD SCANNERS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 31 FLUORESCENCE SCANNERS OFFERED BY KEY MARKET PLAYERS

- TABLE 32 FLUORESCENCE SCANNERS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 33 OTHER SCANNERS OFFERED BY KEY MARKET PLAYERS

- TABLE 34 OTHER SCANNERS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 35 DIGITAL PATHOLOGY SOFTWARE OFFERED BY KEY MARKET PLAYERS

- TABLE 36 DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 37 DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY REGION, 2023-2030 (USD MILLION)

- TABLE 38 INTEGRATED SOFTWARE OFFERED BY KEY MARKET PLAYERS

- TABLE 39 INTEGRATED SOFTWARE MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 40 STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 41 STANDALONE SOFTWARE MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 42 INFORMATION MANAGEMENT SOFTWARE OFFERED BY KEY MARKET PLAYERS

- TABLE 43 INFORMATION MANAGEMENT SOFTWARE MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 44 IMAGE ANALYSIS SOFTWARE OFFERED BY KEY MARKET PLAYERS

- TABLE 45 IMAGE ANALYSIS SOFTWARE MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 46 DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 47 CLOUD-BASED SOFTWARE OFFERED BY KEY MARKET PLAYERS

- TABLE 48 CLOUD-BASED MODEL MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 49 ON-PREMISE SOFTWARE OFFERED BY KEY MARKET PLAYERS

- TABLE 50 ON-PREMISE MODEL MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 51 HYBRID SOFTWARE OFFERED BY KEY MARKET PLAYERS

- TABLE 52 HYBRID MODEL MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 53 STORAGE SYSTEMS OFFERED BY KEY MARKET PLAYERS

- TABLE 54 DIGITAL PATHOLOGY MARKET FOR STORAGE SYSTEMS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 55 DIGITAL PATHOLOGY MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 56 HUMAN DIGITAL PATHOLOGY MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 57 VETERINARY DIGITAL PATHOLOGY MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 58 DIGITAL PATHOLOGY MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 59 SOFTWARE IMPACT ANALYSIS, BY APPLICATION

- TABLE 60 DIGITAL PATHOLOGY APPLICATIONS IN DRUG DISCOVERY

- TABLE 61 DIGITAL PATHOLOGY MARKET FOR DRUG DISCOVERY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 62 DIGITAL PATHOLOGY MARKET FOR DISEASE DIAGNOSIS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 63 DIGITAL PATHOLOGY MARKET FOR TRAINING & EDUCATION, BY REGION, 2023-2030 (USD MILLION)

- TABLE 64 DIGITAL PATHOLOGY MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 65 DIGITAL PATHOLOGY MARKET: SOFTWARE IMPACT ANALYSIS, BY END USER

- TABLE 66 DIGITAL PATHOLOGY MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 67 DEPLOYMENT OF DIGITAL PATHOLOGY SOLUTIONS, BY HOSPITAL

- TABLE 68 DIGITAL PATHOLOGY MARKET FOR HOSPITALS & REFERENCE LABORATORIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 69 DIGITAL PATHOLOGY MARKET FOR ACADEMIC & RESEARCH INSTITUTES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 70 DIGITAL PATHOLOGY MARKET FOR DIAGNOSTICS LABORATORIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 71 DIGITAL PATHOLOGY MARKET FOR VETERINARY LABORATORIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 72 DIGITAL PATHOLOGY MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 73 NORTH AMERICA: MACROECONOMIC OUTLOOK, 2024

- TABLE 74 NORTH AMERICA: DIGITAL PATHOLOGY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 75 NORTH AMERICA: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 76 NORTH AMERICA: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 77 NORTH AMERICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 78 NORTH AMERICA: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 79 NORTH AMERICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 80 NORTH AMERICA: DIGITAL PATHOLOGY MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 81 NORTH AMERICA: DIGITAL PATHOLOGY MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 82 NORTH AMERICA: DIGITAL PATHOLOGY MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 83 US: CANCER INCIDENCE, BY CANCER TYPE, 2022 VS. 2040

- TABLE 84 US: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 85 US: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 86 US: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 87 US: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 88 US: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 89 CANADA: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 90 CANADA: FUNDING INITIATIVES FOR DIGITAL PATHOLOGY

- TABLE 91 CANADA: KEY MACROINDICATORS

- TABLE 92 CANADA: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 93 CANADA: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 94 CANADA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 95 CANADA: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 96 CANADA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 97 EUROPE: MACROECONOMIC OUTLOOK

- TABLE 98 EUROPE: DIGITAL PATHOLOGY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 99 EUROPE: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 100 EUROPE: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 101 EUROPE: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 102 EUROPE: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 103 EUROPE: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 104 EUROPE: DIGITAL PATHOLOGY MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 105 EUROPE: DIGITAL PATHOLOGY MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 106 EUROPE: DIGITAL PATHOLOGY MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 107 GERMANY: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 108 GERMANY: KEY MACROINDICATORS

- TABLE 109 GERMANY: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 110 GERMANY: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 111 GERMANY: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 112 GERMANY: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 113 GERMANY: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 114 UK: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 115 UK: KEY MACROINDICATORS

- TABLE 116 UK: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 117 UK: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 118 UK: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 119 UK: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 120 UK: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 121 SWEDEN: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 122 SWEDEN: KEY MACROINDICATORS

- TABLE 123 SWEDEN: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 124 SWEDEN: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 125 SWEDEN: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 126 SWEDEN: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 127 SWEDEN: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 128 FRANCE: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 129 FRANCE: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 130 FRANCE: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 131 FRANCE: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 132 FRANCE: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 133 FRANCE: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 134 SPAIN: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 135 SPAIN: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 136 SPAIN: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 137 SPAIN: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 138 SPAIN: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 139 ITALY: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 140 ITALY: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 141 ITALY: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 142 ITALY: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 143 ITALY: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 144 REST OF EUROPE: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 145 REST OF EUROPE: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 146 REST OF EUROPE: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 147 REST OF EUROPE: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 148 REST OF EUROPE: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 149 ASIA PACIFIC: MACROINDICATORS

- TABLE 150 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 151 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 152 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 153 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 154 ASIA PACIFIC: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 155 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 156 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 157 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 158 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 159 CHINA: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 160 CHINA: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 161 CHINA: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 162 CHINA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 163 CHINA: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 164 CHINA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 165 JAPAN: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 166 JAPAN: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 167 JAPAN: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 168 JAPAN: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 169 JAPAN: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 170 JAPAN: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 171 INDIA: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 172 INDIA: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 173 INDIA: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 174 INDIA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 175 INDIA: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 176 INDIA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 177 REST OF ASIA PACIFIC: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 178 REST OF ASIA PACIFIC: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 179 REST OF ASIA PACIFIC: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 180 REST OF ASIA PACIFIC: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 181 REST OF ASIA PACIFIC: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 182 LATIN AMERICA: MACROINDICATORS

- TABLE 183 LATIN AMERICA: DIGITAL PATHOLOGY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 184 LATIN AMERICA: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 185 LATIN AMERICA: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 186 LATIN AMERICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 187 LATIN AMERICA: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 188 LATIN AMERICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 189 LATIN AMERICA: DIGITAL PATHOLOGY MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 190 LATIN AMERICA: DIGITAL PATHOLOGY MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 191 LATIN AMERICA: DIGITAL PATHOLOGY MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 192 BRAZIL: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 193 BRAZIL: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 194 BRAZIL: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 195 BRAZIL: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 196 BRAZIL: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 197 BRAZIL: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 198 MEXICO: CANCER INCIDENCE, BY CANCER TYPE, 2020 VS. 2040

- TABLE 199 MEXICO: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 200 MEXICO: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 201 MEXICO: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 202 MEXICO: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 203 MEXICO: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 204 REST OF LATIN AMERICA: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 205 REST OF LATIN AMERICA: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 206 REST OF LATIN AMERICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 207 REST OF LATIN AMERICA: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 208 REST OF LATIN AMERICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 209 MIDDLE EAST & AFRICA: KEY MACROINDICATORS

- TABLE 210 MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 211 MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 212 MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 213 MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 214 MIDDLE EAST & AFRICA: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 215 MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 216 MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 217 MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 218 MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 219 GCC: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 220 GCC: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 221 GCC: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 222 GCC: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 223 GCC: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 224 REST OF MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 225 REST OF MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET FOR SCANNERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 226 REST OF MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 227 REST OF MIDDLE EAST & AFRICA: STANDALONE SOFTWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 228 REST OF MIDDLE EAST & AFRICA: DIGITAL PATHOLOGY MARKET FOR SOFTWARE, BY DEPLOYMENT MODEL, 2023-2030 (USD MILLION)

- TABLE 229 OVERVIEW OF STRATEGIES DEPLOYED BY KEY MANUFACTURING COMPANIES

- TABLE 230 DIGITAL PATHOLOGY MARKET: DEGREE OF COMPETITION

- TABLE 231 DIGITAL PATHOLOGY MARKET: PRODUCT FOOTPRINT

- TABLE 232 DIGITAL PATHOLOGY MARKET: APPLICATION FOOTPRINT

- TABLE 233 DIGITAL PATHOLOGY MARKET: END-USER FOOTPRINT

- TABLE 234 DIGITAL PATHOLOGY MARKET: REGION FOOTPRINT

- TABLE 235 DIGITAL PATHOLOGY MARKET: DETAILED LIST OF KEY START-UPS/SMES

- TABLE 236 DIGITAL PATHOLOGY MARKET: COMPETITIVE BENCHMARKING OF KEY EMERGING PLAYERS/STARTUPS

- TABLE 237 DIGITAL PATHOLOGY MARKET: PRODUCT LAUNCHES, ENHANCEMENTS, AND APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 238 DIGITAL PATHOLOGY MARKET: DEALS, JANUARY 2022-JUNE 2025

- TABLE 239 DIGITAL PATHOLOGY MARKET: OTHER DEVELOPMENTS, JANUARY 2022-JUNE 2025

- TABLE 240 DANAHER CORPORATION: COMPANY OVERVIEW

- TABLE 241 DANAHER CORPORATION: PRODUCTS OFFERED

- TABLE 242 DANAHER CORPORATION: DEALS, JANUARY 2022-JUNE 2025

- TABLE 243 F. HOFFMANN-LA ROCHE LTD.: COMPANY OVERVIEW

- TABLE 244 F. HOFFMANN-LA ROCHE LTD.: PRODUCTS OFFERED

- TABLE 245 HOFFMANN-LA ROCHE LTD.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 246 HOFFMANN-LA ROCHE LTD.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 247 SECTRA AB: COMPANY OVERVIEW

- TABLE 248 SECTRA AB: PRODUCTS OFFERED

- TABLE 249 SECTRA AB: DEALS, JANUARY 2022-JUNE 2025

- TABLE 250 SECTRA AB: OTHER DEVELOPMENTS, JANUARY 2022-JUNE 2025

- TABLE 251 HAMAMATSU PHOTONICS K.K.: COMPANY OVERVIEW

- TABLE 252 HAMAMATSU PHOTONICS K.K.: PRODUCTS OFFERED

- TABLE 253 HAMAMATSU PHOTONICS K.K.: PRODUCT APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 254 HAMAMATSU PHOTONICS K.K.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 255 KONINKLIJKE PHILIPS N.V.: COMPANY OVERVIEW

- TABLE 256 KONINKLIJKE PHILIPS N.V.: PRODUCTS OFFERED

- TABLE 257 KONINKLIJKE PHILIPS N.V: PRODUCT APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 258 KONINKLIJKE PHILIPS N.V.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 259 AKOYA BIOSCIENCES, INC.: COMPANY OVERVIEW

- TABLE 260 AKOYA BIOSCIENCES INC.: PRODUCTS OFFERED

- TABLE 261 AKOYA BIOSCIENCES, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JUNE 2024

- TABLE 262 FUJIFILM HOLDINGS CORPORATION: COMPANY OVERVIEW

- TABLE 263 FUJIFILM HOLDINGS CORPORATION: PRODUCTS OFFERED

- TABLE 264 FUJIFILM HOLDINGS CORPORATION: DEALS, JANUARY 2022-JUNE 2025

- TABLE 265 HOLOGIC, INC.: COMPANY OVERVIEW

- TABLE 266 HOLOGIC, INC: PRODUCTS OFFERED

- TABLE 267 HOLOGIC, INC: PRODUCT APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 268 3DHISTECH LTD.: COMPANY OVERVIEW

- TABLE 269 3DHISTECH LTD.: PRODUCTS OFFERED

- TABLE 270 3DHISTECH LTD.: PRODUCT LAUNCHES & ENHANCEMENTS, JANUARY 2022-JUNE 2024

- TABLE 271 3DHISTECH LTD.: OTHER DEVELOPMENTS, JANUARY 2022-JUNE 2024

- TABLE 272 APOLLO ENTERPRISE IMAGING CORP.: COMPANY OVERVIEW

- TABLE 273 APOLLO ENTERPRISE IMAGING CORP.: PRODUCTS OFFERED

- TABLE 274 APOLLO ENTERPRISE IMAGING CORP.: PRODUCT ENHANCEMENTS, JANUARY 2022-JUNE 2025

- TABLE 275 APOLLO ENTERPRISE IMAGING CORP.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 276 XIFIN, INC.: COMPANY OVERVIEW

- TABLE 277 XIFIN, INC.: PRODUCTS OFFERED

- TABLE 278 XIFIN, INC.: PRODUCT LAUNCHES, JANUARY 2022-JUNE 2025

- TABLE 279 XIFIN, INC.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 280 HURON DIGITAL PATHOLOGY: COMPANY OVERVIEW

- TABLE 281 HURON DIGITAL PATHOLOGY: PRODUCTS OFFERED

- TABLE 282 HURON DIGITAL PATHOLOGY: DEALS, JANUARY 2022-JUNE 2025

- TABLE 283 INDICA LABS: COMPANY OVERVIEW

- TABLE 284 INDICA LABS: PRODUCTS OFFERED

- TABLE 285 INDICA LABS: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 286 INDICA LABS: DEALS, JANUARY 2022-JUNE 2025

- TABLE 287 OPTRASCAN, INC.: COMPANY OVERVIEW

- TABLE 288 OPTRASCAN, INC.: PRODUCTS OFFERED

- TABLE 289 OPTRASCAN, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 290 OPTRASCAN, INC.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 291 GLENCOE SOFTWARE, INC.: COMPANY OVERVIEW

- TABLE 292 GLENCOE SOFTWARE, INC.: PRODUCTS OFFERED

- TABLE 293 GLENCOE SOFTWARE, INC.: PRODUCT ENHANCEMENTS, JANUARY 2022-JUNE 2025

- TABLE 294 AIFORIA TECHNOLOGIES OY: COMPANY OVERVIEW

- TABLE 295 AIFORIA TECHNOLOGIES OY: PRODUCTS OFFERED

- TABLE 296 PAIGE AI, INC.: COMPANY OVERVIEW

- TABLE 297 PAIGE AI, INC.: PRODUCTS OFFERED

- TABLE 298 PAIGE AI, INC.: PRODUCT LAUNCHES & ENHANCEMENTS, JANUARY 2022-JUNE 2025

- TABLE 299 PAIGE AI, INC.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 300 PROSCIA, INC.: COMPANY OVERVIEW

- TABLE 301 PROSCIA, INC.: PRODUCTS OFFERED

- TABLE 302 PROSCIA, INC.: PRODUCT ENHANCEMENTS & APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 303 PROSCIA, INC.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 304 QUEST DIAGNOSTICS: COMPANY OVERVIEW

- TABLE 305 KONFOONG BIOTECH INTERNATIONAL CO., LTD.: COMPANY OVERVIEW

- TABLE 306 MIKROSCAN TECHNOLOGIES, INC.: COMPANY OVERVIEW

- TABLE 307 MOTIC DIGITAL PATHOLOGY: COMPANY OVERVIEW

- TABLE 308 KANTERON SYSTEMS: COMPANY OVERVIEW

- TABLE 309 MORPHLE LABS INC.: COMPANY OVERVIEW

- TABLE 310 EW HEALTHCARE PARTNERS: COMPANY OVERVIEW

List of Figures

- FIGURE 1 DIGITAL PATHOLOGY MARKET

- FIGURE 2 RESEARCH DESIGN

- FIGURE 3 PRIMARY SOURCES

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 5 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 6 MARKET SIZE ESTIMATION: REVENUE SHARE ANALYSIS

- FIGURE 7 DIGITAL PATHOLOGY MARKET: REVENUE SHARE ANALYSIS OF DANAHER CORPORATION

- FIGURE 8 BOTTOM-UP APPROACH

- FIGURE 9 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- FIGURE 10 CAGR PROJECTIONS FROM ANALYSIS OF DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN DIGITAL PATHOLOGY MARKET (2025-2030)

- FIGURE 11 DATA TRIANGULATION METHODOLOGY

- FIGURE 12 DIGITAL PATHOLOGY MARKET, BY PRODUCT, 2025 VS. 2030 (USD MILLION)

- FIGURE 13 DIGITAL PATHOLOGY MARKET, BY TYPE, 2025 VS. 2030 (USD MILLION)

- FIGURE 14 DIGITAL PATHOLOGY MARKET, BY APPLICATION, 2025 VS. 2030 (USD MILLION)

- FIGURE 15 DIGITAL PATHOLOGY MARKET, BY END USER, 2025 VS. 2030 (USD MILLION)

- FIGURE 16 GEOGRAPHIC SNAPSHOT OF DIGITAL PATHOLOGY MARKET

- FIGURE 17 RISING INCIDENCE OF CANCER AND GROWING ADOPTION OF PATHOLOGY SOLUTIONS FOR ENHANCED LAB EFFICIENCY TO DRIVE MARKET

- FIGURE 18 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 19 UK TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 20 ASIA PACIFIC SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 21 DIGITAL PATHOLOGY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 22 GLOBAL CANCER INCIDENCE, 2008-2030

- FIGURE 23 FDA-APPROVED PERSONALIZED MEDICINES, 2015-2022

- FIGURE 24 DIGITAL PATHOLOGY MARKET: VALUE CHAIN ANALYSIS

- FIGURE 25 DIGITAL PATHOLOGY MARKET: ECOSYSTEM ANALYSIS

- FIGURE 26 DIGITAL PATHOLOGY MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 27 EUROPE: IVDR TIMELINE

- FIGURE 28 JURISDICTION ANALYSIS: TOP APPLICANT COUNTRIES FOR DIGITAL PATHOLOGY PATENTS, 2014-2025

- FIGURE 29 MAJOR PATENTS FOR DIGITAL PATHOLOGY (2015-2025)

- FIGURE 30 KEY BUYING CRITERIA FOR DIGITAL PATHOLOGY PRODUCTS

- FIGURE 31 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 32 RECENT FUNDING OF PLAYERS IN DIGITAL PATHOLOGY MARKET

- FIGURE 33 NORTH AMERICA: DIGITAL PATHOLOGY MARKET SNAPSHOT

- FIGURE 34 ASIA PACIFIC: DIGITAL PATHOLOGY MARKET SNAPSHOT

- FIGURE 35 REVENUE ANALYSIS OF KEY PLAYERS IN DIGITAL PATHOLOGY MARKET

- FIGURE 36 DIGITAL PATHOLOGY MARKET SHARE ANALYSIS

- FIGURE 37 DIGITAL PATHOLOGY MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 38 DIGITAL PATHOLOGY MARKET: COMPANY FOOTPRINT

- FIGURE 39 DIGITAL PATHOLOGY MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 40 EV/EBITDA OF KEY VENDORS

- FIGURE 41 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF DIGITAL PATHOLOGY VENDORS

- FIGURE 42 DIGITAL PATHOLOGY MARKET: BRAND/SOFTWARE COMPARATIVE ANALYSIS

- FIGURE 43 DANAHER CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 44 F. HOFFMANN-LA ROCHE LTD.: COMPANY SNAPSHOT (2024)

- FIGURE 45 SECTRA AB: COMPANY SNAPSHOT (2024)

- FIGURE 46 HAMAMATSU PHOTONICS K.K.: COMPANY SNAPSHOT (2024)

- FIGURE 47 KONINKLIJKE PHILIPS N.V.: COMPANY SNAPSHOT (2024)

- FIGURE 48 AKOYA BIOSCIENCES, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 49 FUJIFILM HOLDINGS CORPORATION: COMPANY SNAPSHOT (2022)

- FIGURE 50 HOLOGIC, INC.: COMPANY SNAPSHOT (2024)

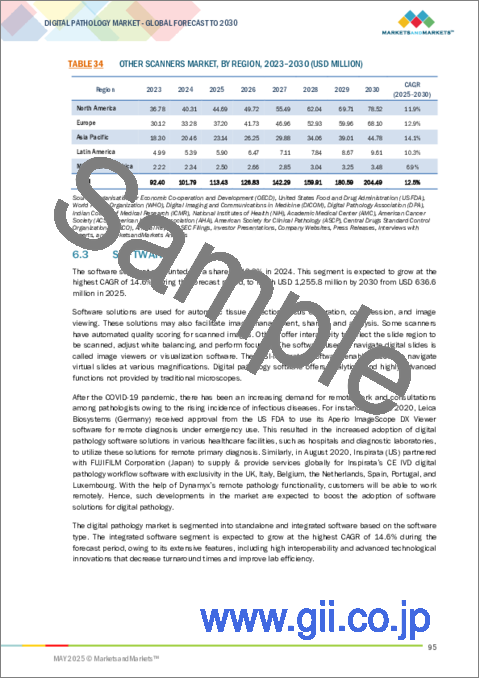

The market for digital pathology is segmented into three categories based on type: scanners, storage systems, and software. Given the significance of these devices in the digital pathology workflow, the scanners segment accounted for the largest share of the product category in 2024. Scanners are critical in enabling pathologists to view and analyze tissue samples on computer screens, as scanners convert physical glass slides to high-resolution digital images. The development of diagnostic remote access is paramount for improved accessibility and efficiency of pathology services by allowing pathologists to evaluate cases from any physical location, hence, the demand for scanners. The advancements in scanner technology, such as improved scanning rates and greater resolution imaging, have led to increased workflow, improved diagnostic accuracy, and value for investment for laboratories or medical facilities.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2024-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Type, Application, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

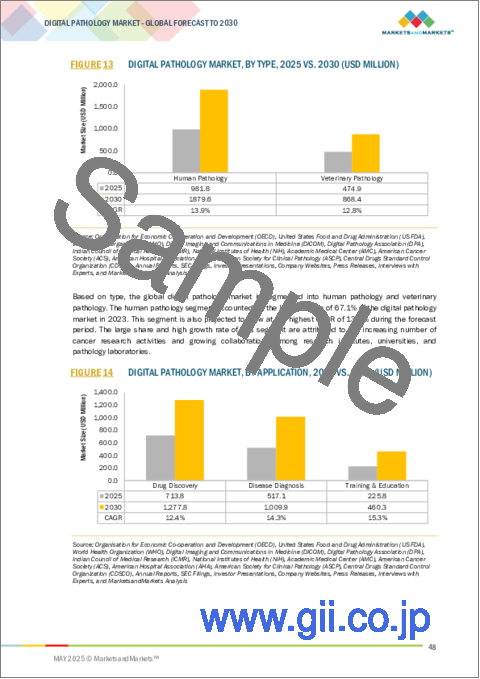

By type, the human pathology segment is expected to hold the largest share during the forecast period.

The human pathology segment is expected to occupy the largest share of the digital pathology market throughout the forecast period largely due to the rising global burden of complex and chronic diseases, including cancer, cardiovascular diseases, and infections, which demand timely and accurate diagnostic outcomes.

Digital pathology, examination, and diagnosis, typically performed under the eyepiece of a microscope, are advantageous in many aspects, such as producing high-resolution images, providing automated analytics, allowing for image storage, cloud storage, and telepathology slide-sharing services. Equally important is the unparalleled advantage of being able to provide remote consultation that may involve co-consultation and coordination at various sites and second opinions from specialists.

Furthermore, digital pathology is quickly being adopted and evolving to integrate the newest technologies such as artificial intelligence (AI), machine learning (ML), deep learning image recognition, which are all improving diagnostic accuracy, decreasing turnaround time, and even aiding in recognizing subtle histological patterns, which makes digital pathology a foundational element of practice in laboratories and hospitals around the world.

North America is expected to lead the global digital pathology market during the forecast period.

North America led the digital pathology market in 2024 due to a mature healthcare system and large financial investments toward developing healthcare technology. The regulatory environment in North America-especially in the US and Canada-supports a relatively faster review and approval process for emerging digital pathology technologies. This, combined with growing awareness among healthcare providers and rising demand for advanced diagnostic solutions, has driven strong adoption of digital pathology across the region.

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (35%), Tier 2 (45%), and Tier 3 (20%)

- By Designation: C-level (35%), Director-level (25%), and Others (40%)

- By Region: North America (40%), Europe (30%), Asia Pacific (20%), Latin America (5%), and Middle East & Africa (5%)

List of Companies Profiled in the Report

Danaher Corporation (US), Koninklijke Philips N.V. (Netherlands), Hamamatsu Photonics K.K. (Japan), F. Hoffmann-La Roche Ltd. (Switzerland), 3DHISTECH (Hungary), Apollo Enterprise Imaging (US), XIFIN, Inc. (US), Huron Digital Pathology (Canada), Hologic, Inc. (US), Corista (US), Indica Labs Inc. (US), Objective Pathology Services Limited (Canada), Sectra AB (Sweden), OptraSCAN (US), Akoya Biosciences, Inc. (US), Glencoe Software, Inc. (US), Aiforia (Finland), Paige AI, Inc. (US), Fujifilm Holdings Corporation (Japan), Proscia Inc. (US), KONFOONG BIOTECH INTERNATIONAL CO., LTD. (China), Mikroscan Technologies, Inc. (US), PathAI (US), Motic Digital Pathology (US), and Kanteron Systems (Spain)

Research Coverage

This report studies the digital pathology market based on product, type, application, end user, and region. The report also analyses factors (such as drivers, opportunities, and challenges) affecting market growth. It evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders. The report also studies micro markets with respect to their growth trends, prospects, and contributions to the total digital pathology market. The report forecasts the revenue of the market segments with respect to five major regions.

Reasons to Buy the Report

This report also includes.

- Analysis of key drivers (Growing adoption of AI-enabled digital pathology, rising burden of cancer, diabetes, and chronic diseases, expansion of digital pathology in drug discovery and biomarker validation, Cancer screening programs in emerging markets), restraints (High initial capital costs, Data interoperability issues with existing lab systems, regulatory and reimbursement uncertainty), opportunities (Affordable scanner development for low-resource settings, growing preference for personalized medicine, government-backed digitization in emerging economies) challenges (Shortage of skilled pathologists and technicians, algorithm validation issues, data security and patient privacy concerns), are contributing the growth of the digital pathology market.

- Product Development/Innovation: Detailed insights on upcoming trends, research & development activities, and new software launches in the digital pathology market

- Market Development: Comprehensive information about lucrative markets and analysis of the authentication and brand protection market across varied regions

- Market Diversification: Exhaustive information about the software portfolios, growing geographies, recent developments, and investments in the digital pathology market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, company evaluation quadrant, and capabilities of leading players in the global digital pathology market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 RESEARCH METHODOLOGY DESIGN

- 2.3 MARKET SIZE ESTIMATION

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 MARKET ASSUMPTIONS

- 2.6.1 OVERALL STUDY ASSUMPTIONS

- 2.7 RISK ASSESSMENT

- 2.8 RESEARCH LIMITATIONS

- 2.8.1 METHODOLOGY-RELATED LIMITATIONS

- 2.8.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 DIGITAL PATHOLOGY MARKET OVERVIEW

- 4.2 NORTH AMERICA: DIGITAL PATHOLOGY MARKET, BY END USER AND COUNTRY (2024)

- 4.3 DIGITAL PATHOLOGY MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 DIGITAL PATHOLOGY MARKET: REGIONAL MIX

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 AI-enabled digital pathology improving lab throughput

- 5.2.1.2 Rising burden of cancer, diabetes, and cardiovascular diseases

- 5.2.1.3 Expansion of digital pathology in drug discovery and biomarker validation

- 5.2.1.4 National cancer screening programs in emerging markets

- 5.2.2 RESTRAINTS

- 5.2.2.1 High initial capital cost of digital pathology systems

- 5.2.2.2 Data interoperability issues with existing lab systems

- 5.2.2.3 Regulatory and reimbursement uncertainty

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Affordable scanner development for low-resource settings

- 5.2.3.2 Personalized medicine driving precision diagnostics

- 5.2.3.3 Government-backed digitalization in emerging economies

- 5.2.4 CHALLENGES

- 5.2.4.1 Shortage of skilled pathologists and technicians

- 5.2.4.2 Algorithm validation and trust in AI-based diagnostics

- 5.2.4.3 Data security and privacy concerns

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 AI-POWERED DIAGNOSTICS GO MAINSTREAM

- 5.3.2 CLOUD-BASED PLATFORMS AND REMOTE ACCESS BECOME CRITICAL ENABLERS

- 5.4 TECHNOLOGY ANALYSIS

- 5.4.1 CLOUD STORAGE & ARCHIVING

- 5.4.2 WHOLE SLIDE IMAGING (WSI) SCANNERS

- 5.4.3 IMAGE MANAGEMENT SYSTEMS

- 5.4.4 ADJACENT TECHNOLOGIES

- 5.4.4.1 Genomic sequencing

- 5.4.4.2 Artificial Intelligence and Machine Learning

- 5.4.5 COMPLEMENTARY TECHNOLOGIES

- 5.4.5.1 LIS & PACS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 THREAT OF NEW ENTRANTS

- 5.8.2 THREAT OF SUBSTITUTES

- 5.8.3 BARGAINING POWER OF SUPPLIERS

- 5.8.4 BARGAINING POWER OF BUYERS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 HS CODES

- 5.10 REGULATORY LANDSCAPE

- 5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.10.2 REGULATORY ANALYSIS

- 5.10.2.1 North America

- 5.10.2.1.1 US

- 5.10.2.1.2 Canada

- 5.10.2.2 Europe

- 5.10.2.3 Asia Pacific

- 5.10.2.3.1 Japan

- 5.10.2.3.2 China

- 5.10.2.3.3 India

- 5.10.2.1 North America

- 5.11 PATENT ANALYSIS

- 5.11.1 PATENT PUBLICATION TRENDS

- 5.11.2 JURISDICTION ANALYSIS: TOP APPLICANT COUNTRIES FOR DIGITAL PATHOLOGY PATENTS

- 5.11.3 MAJOR PATENTS

- 5.12 CASE STUDY ANALYSIS

- 5.13 KEY CONFERENCES & EVENTS, 2025-2026

- 5.14 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.14.2 BUYING CRITERIA

- 5.14.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.15 END-USER ANALYSIS

- 5.15.1 UNMET NEEDS

- 5.15.2 END-USER EXPECTATIONS

- 5.16 BUSINESS MODEL ANALYSIS

- 5.17 INVESTMENT & FUNDING SCENARIO

- 5.18 IMPACT OF AI ON DIGITAL PATHOLOGY MARKET

- 5.19 IMPACT OF US TARIFF ON DIGITAL PATHOLOGY MARKET

- 5.19.1 INTRODUCTION

- 5.19.2 KEY TARIFF RATES

- 5.20 PRICE IMPACT ANALYSIS

- 5.21 IMPACT ON COUNTRY/REGION

- 5.21.1 US

- 5.21.2 EUROPE

- 5.21.3 ASIA PACIFIC

- 5.21.4 IMPACT ON END-USE INDUSTRIES

6 DIGITAL PATHOLOGY MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 SCANNERS

- 6.2.1 BRIGHTFIELD SCANNERS

- 6.2.1.1 Cost-efficient features to boost demand

- 6.2.2 FLUORESCENCE SCANNERS

- 6.2.2.1 Ability to detect cellular structures and biomarkers to fuel uptake

- 6.2.3 OTHER SCANNERS

- 6.2.1 BRIGHTFIELD SCANNERS

- 6.3 SOFTWARE

- 6.3.1 INTEGRATED SOFTWARE

- 6.3.1.1 Single & effective suite for multiple applications to propel market

- 6.3.2 STANDALONE SOFTWARE

- 6.3.2.1 Information management software

- 6.3.2.1.1 Management of image repositories to fuel uptake

- 6.3.2.2 Image analysis software

- 6.3.2.2.1 Ability to automate quantitative evaluation to support market growth

- 6.3.2.1 Information management software

- 6.3.1 INTEGRATED SOFTWARE

- 6.4 SOFTWARE, BY DEPLOYMENT MODEL

- 6.4.1 CLOUD-BASED MODEL

- 6.4.1.1 Facilitation of collaboration on a single platform to drive market

- 6.4.2 ON-PREMISE MODEL

- 6.4.2.1 High data security and integration with HCIT solutions to fuel uptake

- 6.4.3 HYBRID MODEL

- 6.4.3.1 Combined flexibility to support market growth

- 6.4.1 CLOUD-BASED MODEL

- 6.5 STORAGE SYSTEMS

- 6.5.1 GROWING FOCUS ON STORAGE OF HIGH-RESOLUTION IMAGES TO DRIVE MARKET

7 DIGITAL PATHOLOGY MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 HUMAN PATHOLOGY

- 7.2.1 INCREASING CANCER RESEARCH ACTIVITIES TO PROPEL MARKET

- 7.3 VETERINARY PATHOLOGY

- 7.3.1 IMPROVEMENTS IN ANIMAL DISEASE DIAGNOSTICS TO SUPPORT MARKET GROWTH

8 DIGITAL PATHOLOGY MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 DRUG DISCOVERY

- 8.2.1 INCREASING FOCUS ON LIFE SCIENCES R&D TO DRIVE MARKET

- 8.3 DISEASE DIAGNOSIS

- 8.3.1 INTEGRATION OF AI & ML IN COMPLEX DIAGNOSTICS TO BOOST DEMAND

- 8.4 TRAINING & EDUCATION

- 8.4.1 ABILITY TO PROVIDE REAL-TIME LEARNING EXPERIENCES TO SUPPORT MARKET GROWTH

9 DIGITAL PATHOLOGY MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 9.2.1 INCREASING FOCUS ON DRUG TOXICOLOGY TESTING AND RISING NUMBER OF PRECLINICAL TRIALS TO PROPEL MARKET

- 9.3 HOSPITALS & REFERENCE LABORATORIES

- 9.3.1 HIGH INCIDENCE OF INFECTIOUS DISEASES TO BOOST DEMAND

- 9.4 ACADEMIC & RESEARCH INSTITUTES

- 9.4.1 INCREASING PUBLIC & PRIVATE FUNDING INVESTMENTS TO SUPPORT MARKET GROWTH

- 9.5 DIAGNOSTICS LABORATORIES

- 9.5.1 INCREASING PUBLIC & PRIVATE FUNDING INVESTMENTS TO SUPPORT MARKET GROWTH

- 9.6 VETERINARY LABORATORIES

- 9.6.1 TECHNOLOGICAL ADVANCEMENTS, PARTICULARLY IN WHOLE-SLIDE IMAGING SYSTEMS AND AI-POWERED IMAGE ANALYSIS SOFTWARE, SUPPORT MARKET GROWTH

10 DIGITAL PATHOLOGY MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 10.2.2 US

- 10.2.2.1 Favorable reimbursements for diagnostics to drive market

- 10.2.3 CANADA

- 10.2.3.1 Growing awareness on early cancer detection & diagnosis to drive market

- 10.3 EUROPE

- 10.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 10.3.2 GERMANY

- 10.3.2.1 High healthcare expenditure and supportive research initiatives to drive market

- 10.3.3 UK

- 10.3.3.1 Government funding investments for pathology services to fuel market

- 10.3.4 SWEDEN

- 10.3.4.1 Increasing prevalence of chronic diseases to support market growth

- 10.3.5 FRANCE

- 10.3.5.1 Increasing government funding and favorable insurance system to drive adoption

- 10.3.6 SPAIN

- 10.3.6.1 Supportive collaborations among leading companies and hospitals to boost demand

- 10.3.7 ITALY

- 10.3.7.1 Integration of AI & ML to support market growth

- 10.3.8 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 10.4.2 CHINA

- 10.4.2.1 Increasing establishment of hospitals and reference laboratories to drive market

- 10.4.3 JAPAN

- 10.4.3.1 Advanced healthcare infrastructure to support market growth

- 10.4.4 INDIA

- 10.4.4.1 Growth in pharmaceutical industry to propel market

- 10.4.5 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 10.5.2 BRAZIL

- 10.5.2.1 High adoption of POC testing to drive market

- 10.5.3 MEXICO

- 10.5.3.1 Growth in companion diagnostics to fuel uptake

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 IMPROVEMENTS IN HEALTHCARE INFRASTRUCTURE TO SUPPORT MARKET GROWTH

- 10.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 10.6.3 GCC COUNTRIES

- 10.6.4 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN DIGITAL PATHOLOGY MARKET

- 11.3 REVENUE ANALYSIS

- 11.4 MARKET SHARE ANALYSIS

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Product footprint

- 11.5.5.3 Application footprint

- 11.5.5.4 End-user footprint

- 11.5.5.5 Region footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.7 COMPANY VALUATION AND FINANCIAL METRICS

- 11.8 BRAND/SOFTWARE COMPARATIVE ANALYSIS

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES, ENHANCEMENTS, AND APPROVALS

- 11.9.2 DEALS

- 11.9.3 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY COMPANIES

- 12.1.1 DANAHER CORPORATION

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 HOFFMANN-LA ROCHE LTD.

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches & approvals

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 SECTRA AB

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Deals

- 12.1.3.3.2 Other developments

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 HAMAMATSU PHOTONICS K.K.

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product approvals

- 12.1.4.3.2 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 KONINKLIJKE PHILIPS N.V.

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches & approvals

- 12.1.5.3.2 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 AKOYA BIOSCIENCES, INC.

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches & approvals

- 12.1.7 FUJIFILM HOLDINGS CORPORATION

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Deals

- 12.1.8 HOLOGIC, INC.

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product approvals

- 12.1.9 3DHISTECH LTD.

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches & enhancements

- 12.1.9.3.2 Other developments

- 12.1.10 APOLLO ENTERPRISE IMAGING CORP.

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product enhancements

- 12.1.10.3.2 Deals

- 12.1.11 XIFIN, INC.

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Product launches

- 12.1.11.3.2 Deals

- 12.1.12 HURON DIGITAL PATHOLOGY

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.12.2.1 Deals

- 12.1.13 INDICA LABS

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Product launches & approvals

- 12.1.13.3.2 Deals

- 12.1.14 OPTRASCAN, INC.

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Product launches & approvals

- 12.1.14.3.2 Deals

- 12.1.15 GLENCOE SOFTWARE, INC.

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.15.3 Recent developments

- 12.1.15.3.1 Product enhancements

- 12.1.16 AIFORIA TECHNOLOGIES OY

- 12.1.16.1 Business overview

- 12.1.16.2 Products offered

- 12.1.16.3 Recent developments

- 12.1.16.3.1 Deals

- 12.1.17 PAIGE AI, INC.

- 12.1.17.1 Business overview

- 12.1.17.2 Products offered

- 12.1.17.3 Recent developments

- 12.1.17.3.1 Product launches & enhancements

- 12.1.17.3.2 Deals

- 12.1.18 PROSCIA, INC.

- 12.1.18.1 Business overview

- 12.1.18.2 Products offered

- 12.1.18.3 Recent developments

- 12.1.18.3.1 Product enhancements & approvals

- 12.1.18.3.2 Deals

- 12.1.1 DANAHER CORPORATION

- 12.2 OTHER PLAYERS

- 12.2.1 QUEST DIAGNOSTICS

- 12.2.2 KONFOONG BIOTECH INTERNATIONAL CO., LTD.

- 12.2.3 MIKROSCAN TECHNOLOGIES, INC.

- 12.2.4 MOTIC DIGITAL PATHOLOGY

- 12.2.5 KANTERON SYSTEMS

- 12.2.6 MORPHLE LABS INC.

- 12.2.7 EW HEALTHCARE PARTNERS

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS