|

|

市場調査レポート

商品コード

1295439

赤外線検出器の世界市場:種類別 (テルル化カドミウム水銀、InGaAs、パイロエレクトリック、サーモパイル、マイクロボロメーター)・技術別 (冷却型、非冷却型)・波長別 (NIR・SWIR、MWIR、LWIR)・用途別・業種別・地域別の将来予測 (2028年まで)Infrared Detector Market by Type (Mercury Cadmium Telluride, INGaas, Pyroelectric, Thermopile, Microbolometer), Technology (Cooled and Uncooled), Wavelength (NIR & SWIR, MWIR, LWIR), Application, Vertical and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 赤外線検出器の世界市場:種類別 (テルル化カドミウム水銀、InGaAs、パイロエレクトリック、サーモパイル、マイクロボロメーター)・技術別 (冷却型、非冷却型)・波長別 (NIR・SWIR、MWIR、LWIR)・用途別・業種別・地域別の将来予測 (2028年まで) |

|

出版日: 2023年06月14日

発行: MarketsandMarkets

ページ情報: 英文 229 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の赤外線検出器の市場規模は、2023年の5億3,500万米ドルから7億5,100万米ドルへと、7.0%のCAGRで成長すると予測されています。

非冷却型赤外線検出器の人気拡大、画像診断用途における赤外線検出器の需要増加、人物・動作検出ソリューションにおける赤外線検出器の採用拡大が市場を牽引しています。

"NIR・SWIRが、予測期間中に最高のCAGRで成長する"

近赤外光 (NIR) は、電磁スペクトルのうち可視光域のすぐ先にある部分を指し、波長は約700~2,500ナノメートル (nm) です。人間の目には見えませんが、近赤外光はそのユニークな特性により、様々な用途や産業で一般的に利用されています。近赤外光は、透過性、反射性、吸収性、熱感知性、通信性、多様な産業への応用という点でユニークな利点を提供します。その特性により、様々な科学、工業、医療、技術目的のための貴重なツールとなっています。

SWIR (短波長赤外線) 検出器は、赤外線スペクトルの短波長領域の光を検出・捕捉するように設計されています。SWIR検出器は一般的に、約900~2,500ナノメートル (nm) の波長の赤外線を感知するために使用されます。これらの検出器はSWIR放射を検出し、電気信号に変換してさらなる分析・処理を行うことができます。NIRおよびSWIR検出器の主要メーカーには、Excelitas Technologies Corp. (米国)、Hamamatsu Photonics K.K. (日本)、Teledyne FLIR LLC (米国)、Lynred (フランス) などがあります。

"非冷却型赤外線検出器市場が、2022年に最大のシェアを占める"

非冷却型赤外線検出器のセグメントが、2022年に主導権を握り、約77%の市場シェアを占めています。非冷却型赤外線検出器は、極低温や熱電冷却を必要とせず、室温やわずかに上昇した温度で動作する赤外線センサであり、赤外線にさらされると電気的特性が変化する感温材料や構造を採用しています。しかし、一般的に冷却型検出器よりも低い感度と空間分解能を示します。現在進行中の技術進歩により、非冷却型検出器の性能と能力は継続的に向上しており、赤外線画像・監視・工業検査・自動車安全・医療機器など幅広い用途に適しています。

"北米が予測期間中に最大の市場となる"

北米 (米国、カナダ、メキシコ) では、政府・防衛・商業・住宅など多様な分野で、セキュリティ・監視システムの需要が発生しています。これらの用途では、夜間の監視を容易にし、状況認識を強化し、光が限られた環境や厳しい条件下でも信頼できる検出能力を提供する赤外線検出器が極めて重要です。さらに北米では、特に製造、自動車、航空宇宙分野で産業オートメーションとロボットの導入が急増しています。赤外線検出器は、これらの産業におけるマシンビジョンシステム、品質管理、プロセスモニタリングに採用され、生産プロセスの最適化や最終製品の信頼性確保に役立っています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- バリューチェーン分析

- エコシステム分析

- 顧客のビジネスに影響を与える動向/混乱

- 技術分析

- ポーターのファイブフォース分析

- 価格分析

- 主要な利害関係者と購入基準

- ケーススタディ分析

- 貿易分析

- 特許分析

- 主要な会議とイベント (2023年~2024年)

- 規制と基準

第6章 赤外線検出器市場:種類別

- イントロダクション

- テルル化カドミウム水銀 (MCT)

- ヒ化インジウムガリウム (InGaAs)

- パイロエレクトリック (焦電型)

- サーモパイル

- マイクロボロメーター

- その他

第7章 赤外線検出器市場:波長別

- イントロダクション

- 近赤外線 (NIR)・短波赤外線 (SWIR)

- 中波赤外線 (MWIR)

- 長波赤外線 (LWIR)

第8章 赤外線検出器市場:技術別

- イントロダクション

- 冷却型

- 非冷却型

第9章 赤外線検出器市場:業種別

- イントロダクション

- 工業用

- 自動車

- 航空宇宙

- 半導体・エレクトロニクス

- 石油・ガス

- その他

- 非工業用

- 軍事・防衛

- 住宅用・商業用

- 医療

- 科学研究

第10章 赤外線検出器市場:用途別

- イントロダクション

- 人物・動作検出

- 温度測定

- セキュリティ・監視

- ガス・火災検知

- 分光学・生体医用画像

- その他

第11章 赤外線検出器市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他の欧州

- アジア太平洋

- 日本

- 中国

- 台湾

- その他のアジア太平洋

- その他の地域

- 南米

- 中東

- アフリカ

第12章 競合情勢

- 概要

- 市場シェア分析

- 赤外線検出器市場:上位企業の収益分析

- 企業評価クアドラント (2022年)

- 企業のフットプリント

- スタートアップ/中小企業 (SME) の評価クアドラント (2022年)

- 競合ベンチマーキング

- 競争シナリオと動向

第13章 企業プロファイル

- 主要企業

- EXCELITAS TECHNOLOGIES CORP.

- HAMAMATSU PHOTONICS K.K.

- MURATA MANUFACTURING CO., LTD.

- TELEDYNE FLIR LLC

- TEXAS INSTRUMENTS INCORPORATED

- NIPPON CERAMIC CO., LTD.

- OMRON CORPORATION

- INFRATEC GMBH

- LYNRED

- TE CONNECTIVITY

- その他の企業

- HONEYWELL INTERNATIONAL INC.

- RAYTHEON TECHNOLOGIES CORPORATION

- LASER COMPONENTS

- DRAGERWERK AG & CO. KGAA

- VIGO PHOTONICS S.A.

- XENICS NV.

- MELEXIS

- FAGUS-GRECON

- THORLABS, INC.

- SEMITEC CORPORATION

- IRNOVA AB

- GLOBAL SENSOR TECHNOLOGY CO., LTD.

- DIAS INFRARED GMBH

- SENSORS UNLIMITED, INC.

- IRAY TECHNOLOGY CO., LTD. (INFIRAY)

第14章 隣接・関連市場

- イントロダクション

- 研究の限界

- ガスセンサー市場:技術別

- 電気化学

- 光イオン化検出器

- 固体/金属酸化物半導体

- 触媒

- 赤外線

- レーザー

- ジルコニア

- ホログラフィック

- その他

第15章 付録

The Infrared detector market is expected to grow at a CAGR of 7.0% from USD 535 million in 2023 to USD 751 million. The growing popularity of uncooled infrared detectors and increasing demand for infrared detectors in imaging applications, and growing adoption of infrared detectors in motion and

people-sensing solutions are driving the market.

"Infrared detector market for NIR & SWIR is expected to grow at highest CAGR during the forecast period"

Near-infrared light (NIR) refers to the portion of the electromagnetic spectrum that lies just beyond the visible light range, with wavelengths ranging from approximately 700 to 2500 nanometers (nm). Although invisible to the human eye, NIR light is commonly utilized in various applications and industries due to its unique properties. Near-infrared light offers unique advantages in terms of penetration, reflectance, absorption, thermal sensing, communication, and applications in diverse industries. Its properties make it a valuable tool for various scientific, industrial, medical, and technological purposes.

The SWIR (Short-Wave Infrared) detector is designed to detect and capture light in the short-wavelength region of the infrared spectrum. SWIR detectors are typically used to sense infrared radiation with wavelengths ranging from approximately 900 to 2500 nanometers (nm). These detectors can detect and convert SWIR radiation into electrical signals for further analysis and processing. Some of the prominent manufacturers of NIR and SWIR detectors are Excelitas Technologies Corp. (US), Hamamatsu Photonics K.K. (Japan), Teledyne FLIR LLC (US), and Lynred (France).

"Infrared detector market for uncooled accounted for the largest share in 2022"

The uncooled infrared detector segment held the leading position, accounting for ~77% of the infrared detector market in 2022. An uncooled infrared detector is an infrared sensor that operates at room temperature or slightly elevated temperatures without the need for cryogenic or thermoelectric cooling, employing temperature-sensitive materials or structures that change electrical properties when exposed to infrared radiation, thus offering advantages such as lower cost, reduced power consumption, compact size, and portability. However, they generally exhibit lower sensitivity and spatial resolution than cooled detectors. Ongoing technological advancements continuously improve the performance and capabilities of uncooled detectors, making them suitable for a wide range of applications, including thermal imaging, surveillance, industrial inspection, automotive safety, and medical devices, enabling functions such as non-contact temperature measurement, night vision, object detection, and heat signature monitoring.

"North America is expected to hold the largest market for Infrared detectors during the forecast period"

The infrared detector market in North America has been further classified into the US, Canada, and Mexico. The demand for security and surveillance systems is substantial across diverse sectors such as government, defense, commercial, and residential in North America. In these applications, infrared detectors are pivotal as they facilitate nighttime surveillance, bolster situational awareness, and offer dependable detection capabilities in environments with limited light or challenging conditions. Furthermore, there is a notable surge in the implementation of industrial automation and robotics in North America, particularly in the manufacturing, automotive, and aerospace sectors. Infrared detectors are employed in machine vision systems, quality control, and process monitoring within these industries, aiding in optimizing production processes and ensuring the reliability of the final products.

Breakdown of the profile of primary participants:

- By Company Type: Tier 1 - 35 %, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-level Executives - 35%, Managers - 25%, and Others -40%

- By Region: North America- 45%, Europe- 20%, Asia Pacific - 30%, and RoW - 5%

Major players profiled in this report are as follows: Excelitas Technologies Corp. (US), Hamamatsu Photonics K.K. (Japan), Murata Manufacturing Co., Ltd. (Japan), Teledyne FLIR LLC (US), and Nippon Ceramic Co., Ltd. (Japan), Texas Instruments Incorporated (US), OMRON Corporation (Japan), InfraTec GmbH (Germany), Lynred (France), and TE Connectivity (Switzerland)and others.

Research Coverage

The study segments the Infrared detector market report into technology (cooled, uncooled), working principle (absorption, reflection, transmission, emission), wavelength (near and short-wave infrared, mid-wave infrared, long-wave infrared), type (mercury cadmium telluride, indium gallium arsenide, pyroelectric, thermopile, microbolometer, PIR motion sensor, IR photodiode sensor, IR imaging sensor), application (people and motion sensing, temperature measurement, security and surveillance, gas and fire detection, spectroscopy and biomedical imaging, scientific applications, and smart buildings) and vertical (industrial, nonindustrial). The study also provides market size for various segments regarding four main regions-North America, Europe, Asia Pacific (APAC), and the Rest of the World (RoW).

Reasons to buy the report

The report will help the market leaders/new entrants in this market with information on the closest approximate revenues for the overall infrared detector and related segments. This report will help stakeholders understand the competitive landscape and gain more insights to strengthen their position in the market and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Rapid Adoption of Infrared Detectors in Non-Contact Temperature Measurement, Gas Analysis, Astronomy, and Fire Detection applications, Growing popularity of uncooled infrared detectors and increasing demand for infrared detectors in industrial and manufacturing application, Increasing Utilization of Infrared Detectors in Security and Surveillance), restraints (Stringent regulations pertaining to import and export of cameras), opportunities (Rising demand for infrared detectors in emerging countries; Growing Demand for Infrared Detectors in the Automotive Industry), and challenges (Detection of objects/substances placed beyond wavelength range).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the infrared detector market

- Market Development: Comprehensive information about lucrative markets - the report analyses the infrared detector market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the infrared detector market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and product offerings of leading players like Excelitas Technologies Corp. (US), Hamamatsu Photonics K.K. (Japan), Murata Manufacturing Co., Ltd. (Japan), Teledyne FLIR LLC (US), and Nippon Ceramic Co., Ltd. (Japan) among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 INFRARED DETECTOR MARKET SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.8.1 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 INFRARED DETECTOR MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews with experts

- TABLE 1 INFRARED DETECTOR MARKET: PRIMARY INTERVIEWS

- TABLE 2 PARTICIPANTS FOR PRIMARY INTERVIEWS

- 2.1.2.2 Key data from primary sources

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.3.1 Key industry insights

- 2.1.3.2 Breakdown of primaries

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE): REVENUE GENERATED BY KEY PLAYERS FROM INFRARED DETECTOR MARKET

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2 (DEMAND SIDE): BOTTOM-UP ESTIMATION OF INFRARED DETECTOR MARKET, BY TYPE

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to derive market size using bottom-up analysis (demand side)

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to derive market size using top-down analysis (supply side)

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 7 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- FIGURE 8 RESEARCH ASSUMPTIONS

- 2.5 APPROACH TO UNDERSTAND RECESSION IMPACT ON INFRARED DETECTOR MARKET

- 2.6 RISK ASSESSMENT

- TABLE 3 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 9 PYROELECTRIC INFRARED DETECTOR SEGMENT TO HOLD MAJOR MARKET SHARE DURING FORECAST PERIOD

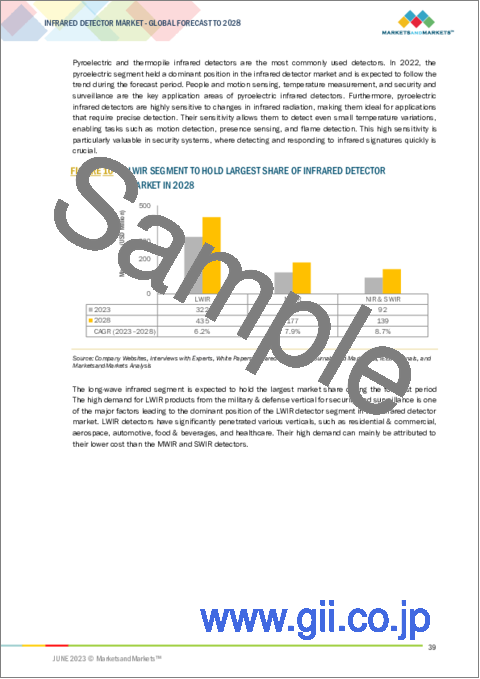

- FIGURE 10 LWIR SEGMENT TO HOLD LARGEST SHARE OF INFRARED DETECTOR MARKET IN 2028

- FIGURE 11 PEOPLE & MOTION SENSING SEGMENT TO WITNESS FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 12 NORTH AMERICA HELD LARGEST SHARE OF INFRARED DETECTOR MARKET IN 2022

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INFRARED DETECTOR MARKET

- FIGURE 13 GROWING ADOPTION OF INFRARED TECHNOLOGY IN PEOPLE & MOTION SENSING AND TEMPERATURE MEASUREMENT APPLICATIONS

- 4.2 INFRARED DETECTOR MARKET, BY WAVELENGTH

- FIGURE 14 LWIR SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.3 NORTH AMERICAN INFRARED DETECTOR MARKET, BY COUNTRY AND APPLICATION

- FIGURE 15 US AND SECURITY & SURVEILLANCE SEGMENT TO HOLD LARGEST SHARES OF NORTH AMERICAN INFRARED DETECTOR MARKET IN 2028

- 4.4 INFRARED DETECTOR MARKET FOR PEOPLE & MOTION SENSING, BY WAVELENGTH

- FIGURE 16 LWIR SEGMENT TO HOLD LARGEST SHARE OF INFRARED DETECTOR MARKET FOR PEOPLE & MOTION SENSING APPLICATION FROM 2023 TO 2028

- 4.5 INFRARED DETECTOR MARKET, BY COUNTRY

- FIGURE 17 CHINA TO RECORD HIGHEST CAGR IN INFRARED DETECTOR MARKET FROM 2023 TO 2028

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 18 INFRARED DETECTOR MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Increased adoption of infrared detectors in non-contact temperature measurement, gas analysis, astronomy, and fire detection applications

- FIGURE 19 FIRE INCIDENTS AND DIRECT PROPERTY DAMAGES IN US, 2016-2022

- 5.2.1.2 Growing popularity of uncooled infrared detectors and increasing demand for infrared detectors in industrial and manufacturing sectors

- 5.2.1.3 Rising use of infrared detectors in security and surveillance

- FIGURE 20 INFRARED DETECTOR MARKET: IMPACT ANALYSIS OF DRIVERS

- 5.2.2 RESTRAINTS

- 5.2.2.1 Stringent regulations pertaining to import and export of cameras

- FIGURE 21 INFRARED DETECTOR MARKET: IMPACT ANALYSIS OF RESTRAINTS

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising demand for infrared detectors in emerging economies

- 5.2.3.2 Growing adoption of infrared spectroscopy

- 5.2.3.3 Rising demand for infrared detectors in automotive industry

- FIGURE 22 INFRARED DETECTOR MARKET: IMPACT ANALYSIS OF OPPORTUNITIES

- 5.2.4 CHALLENGES

- 5.2.4.1 Detection of objects/substances placed beyond wavelength range

- 5.2.4.2 Availability of substitute technologies for chemical and petrochemical plants

- FIGURE 23 INFRARED DETECTOR MARKET: IMPACT ANALYSIS OF CHALLENGES

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 24 INFRARED DETECTOR MARKET: VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- FIGURE 25 INFRARED DETECTOR MARKET: ECOSYSTEM ANALYSIS

- TABLE 4 INFRARED DETECTOR MARKET: ECOSYSTEM ANALYSIS

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 26 REVENUE SHIFT AND NEW REVENUE POCKETS FOR PLAYERS IN INFRARED DETECTOR MARKET

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 SMALLER PIXEL PITCHES

- 5.6.2 ARTIFICIAL INTELLIGENCE (AI)

- 5.6.3 ADVANCEMENTS IN HIGH-OPERATING-TEMPERATURE INFRARED DETECTORS

- 5.7 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 27 INFRARED DETECTOR MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.7.1 THREAT OF NEW ENTRANTS

- 5.7.2 THREAT OF SUBSTITUTES

- 5.7.3 BARGAINING POWER OF SUPPLIERS

- 5.7.4 BARGAINING POWER OF BUYERS

- 5.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE (ASP) OF INFRARED DETECTORS OFFERED BY TOP THREE PLAYERS

- FIGURE 28 AVERAGE SELLING PRICE (ASP) OF INFRARED DETECTORS OFFERED BY TOP THREE PLAYERS

- TABLE 5 AVERAGE SELLING PRICE (ASP) OF INFRARED DETECTORS OFFERED BY TOP THREE PLAYERS (USD)

- TABLE 6 AVERAGE SELLING PRICE (ASP) OF INFRARED DETECTORS, BY REGION

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VERTICAL

- TABLE 7 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VERTICAL (%)

- 5.9.2 BUYING CRITERIA

- FIGURE 30 KEY BUYING CRITERIA FOR DIFFERENT VERTICALS

- TABLE 8 KEY BUYING CRITERIA FOR DIFFERENT VERTICALS

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 INFRATEC GMBH (GERMANY)

- TABLE 9 INFRATEC GMBH PROVIDES RELIABLE THERMOGRAPHIC COMPLETE SOLUTIONS FOR AUTOMATIC LADLE MONITORING

- 5.10.2 MURATA MANUFACTURING CO., LTD. (JAPAN)

- TABLE 10 MURATA MANUFACTURING PROVIDES PYROELECTRIC INFRARED SENSORS TO ACHIEVE DESIRED SECURITY

- 5.10.3 TELEDYNE FLIR LLC (US)

- TABLE 11 TELEDYNE FLIR LLC PROVIDES INFRARED DETECTOR-BASED THERMAL IMAGING SOLUTIONS TO PREVENT FIRE BREAKOUTS IN INDUSTRIAL FACILITIES

- 5.10.4 MURATA MANUFACTURING CO., LTD. (JAPAN)

- TABLE 12 MURATA MANUFACTURING PROVIDES DIGITAL SIGNAGE EQUIPPED WITH PYROELECTRIC INFRARED SENSORS TO CLIENT

- 5.11 TRADE ANALYSIS

- FIGURE 31 IMPORT DATA, BY COUNTRY, 2018-2022 (USD MILLION)

- FIGURE 32 EXPORT DATA, BY COUNTRY, 2018-2022 (USD MILLION)

- 5.12 PATENT ANALYSIS

- FIGURE 33 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS IN LAST 10 YEARS

- TABLE 13 TOP 20 PATENT OWNERS IN LAST 10 YEARS

- FIGURE 34 NUMBER OF PATENTS GRANTED, 2013-2022

- TABLE 14 INFRARED DETECTOR MARKET: PATENT ANALYSIS, JUNE 2021-AUGUST 2022

- 5.13 KEY CONFERENCES AND EVENTS, 2023-2024

- TABLE 15 INFRARED DETECTOR MARKET: LIST OF CONFERENCES AND EVENTS

- 5.14 REGULATIONS AND STANDARDS

- 5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.2 STANDARDS

- TABLE 20 INFRARED DETECTOR MARKET: STANDARDS

6 INFRARED DETECTOR MARKET, BY TYPE

- 6.1 INTRODUCTION

- FIGURE 35 INFRARED DETECTOR MARKET, BY TYPE

- FIGURE 36 PYROELECTRIC INFRARED DETECTOR SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- TABLE 21 INFRARED DETECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 22 INFRARED DETECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 6.2 MERCURY CADMIUM TELLURIDE (MCT)

- 6.2.1 HIGH DEMAND IN TEMPERATURE & MEASUREMENT APPLICATION

- TABLE 23 MERCURY CADMIUM TELLURIDE (MCT): INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 24 MERCURY CADMIUM TELLURIDE (MCT): INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 25 MERCURY CADMIUM TELLURIDE (MCT): INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 26 MERCURY CADMIUM TELLURIDE (MCT): INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3 INDIUM GALLIUM ARSENIDE (INGAAS)

- 6.3.1 INCREASED DEMAND IN IMAGING APPLICATIONS ATTRIBUTED TO LOW NOISE FEATURE

- TABLE 27 INDIUM GALLIUM ARSENIDE (INGAAS): INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 28 INDIUM GALLIUM ARSENIDE (INGAAS): INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 29 INDIUM GALLIUM ARSENIDE (INGAAS): INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 30 INDIUM GALLIUM ARSENIDE (INGAAS): INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4 PYROELECTRIC

- 6.4.1 RISING DEMAND IN PEOPLE & MOTION SENSING APPLICATION

- TABLE 31 PYROELECTRIC: INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 32 PYROELECTRIC: INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 33 PYROELECTRIC: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 34 PYROELECTRIC: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.5 THERMOPILE

- 6.5.1 REVOLUTIONIZING NON-CONTACT TEMPERATURE MEASUREMENT, GAS ANALYSIS, AND THERMAL IMAGING APPLICATIONS

- TABLE 35 THERMOPILE: INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 36 THERMOPILE INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 37 THERMOPILE: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 38 THERMOPILE: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.6 MICROBOLOMETER

- 6.6.1 RISING DEMAND IN MEDICAL IMAGING, ENVIRONMENTAL MONITORING, AND INDUSTRIAL INSPECTION

- TABLE 39 MICROBOLOMETER: INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 40 MICROBOLOMETER: INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 41 MICROBOLOMETER: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 42 MICROBOLOMETER: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.7 OTHERS

- TABLE 43 OTHERS: INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 44 OTHERS: INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 45 OTHERS: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 46 OTHERS: INFRARED DETECTOR MARKET FOR OTHERS, BY REGION, 2023-2028 (USD MILLION)

7 INFRARED DETECTOR MARKET, BY WAVELENGTH

- 7.1 INTRODUCTION

- FIGURE 37 INFRARED DETECTOR MARKET, BY WAVELENGTH

- FIGURE 38 NIR & SWIR INFRARED DETECTOR SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 47 INFRARED DETECTOR MARKET, BY WAVELENGTH, 2019-2022 (USD MILLION)

- TABLE 48 INFRARED DETECTOR MARKET, BY WAVELENGTH, 2023-2028 (USD MILLION)

- 7.2 NEAR-INFRARED (NIR) AND SHORT-WAVE INFRARED (SWIR)

- 7.2.1 GROWING POPULARITY OF INGAAS AND MCT-BASED INFRARED DETECTORS

- TABLE 49 NEAR-INFRARED (NIR) AND SHORT-WAVE INFRARED (SWIR): INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 50 NEAR-INFRARED (NIR) AND SHORT-WAVE INFRARED (SWIR): INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 7.3 MID-WAVE INFRARED (MWIR)

- 7.3.1 HIGH APPLICATIONS OF MWIR DETECTORS IN SECURITY & SURVEILLANCE

- TABLE 51 MID-WAVE INFRARED (MWIR): INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 52 MID-WAVE INFRARED (MWIR): INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 7.4 LONG-WAVE INFRARED (LWIR)

- 7.4.1 SURGING DEMAND FOR LWIR DETECTORS IN MILITARY & DEFENSE VERTICAL

- 7.4.1.1 Key properties of LWIR

- TABLE 53 LONG-WAVE INFRARED (LWIR): INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 54 LONG-WAVE INFRARED (LWIR): INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 7.4.1 SURGING DEMAND FOR LWIR DETECTORS IN MILITARY & DEFENSE VERTICAL

8 INFRARED DETECTOR MARKET, BY TECHNOLOGY

- 8.1 INTRODUCTION

- FIGURE 39 INFRARED DETECTOR MARKET, BY TECHNOLOGY

- FIGURE 40 UNCOOLED INFRARED DETECTOR SEGMENT TO HOLD LARGER MARKET SHARE DURING FORECAST PERIOD

- TABLE 55 INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 56 INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 8.2 COOLED

- 8.2.1 HIGH DEMAND IN SPECTROSCOPY, GAS ANALYSIS, AND THERMAL IMAGING APPLICATIONS

- 8.3 UNCOOLED

- 8.3.1 RISING DEMAND ATTRIBUTED TO COST-EFFECTIVENESS AND LOW POWER CONSUMPTION FEATURES

9 INFRARED DETECTOR MARKET, BY VERTICAL

- 9.1 INTRODUCTION

- FIGURE 41 INFRARED DETECTOR MARKET, BY VERTICAL

- FIGURE 42 NONINDUSTRIAL SEGMENT TO REGISTER HIGHER CAGR IN INFRARED DETECTOR MARKET DURING FORECAST PERIOD

- TABLE 57 INFRARED DETECTOR MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 58 INFRARED DETECTOR MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 9.2 INDUSTRIAL

- 9.2.1 AUTOMOTIVE

- 9.2.1.1 Enhances safety and functionality of automobiles

- 9.2.2 AEROSPACE

- 9.2.2.1 Used in security & surveillance, quality inspection, and vision enhancement applications

- 9.2.3 SEMICONDUCTOR & ELECTRONICS

- 9.2.3.1 Used in quality control and inspection of manufacturing processes

- 9.2.4 OIL & GAS

- 9.2.4.1 Deployed for gas & fire detection

- 9.2.5 OTHERS

- 9.2.1 AUTOMOTIVE

- 9.3 NONINDUSTRIAL

- 9.3.1 MILITARY & DEFENSE

- 9.3.1.1 Employed for vision enhancement

- 9.3.2 RESIDENTIAL & COMMERCIAL

- 9.3.2.1 Used for security & surveillance

- 9.3.3 MEDICAL

- 9.3.3.1 Highly used for non-contact temperature measurement

- 9.3.4 SCIENTIFIC RESEARCH

- 9.3.4.1 Used to inspect and analyze material properties

- 9.3.1 MILITARY & DEFENSE

10 INFRARED DETECTOR MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- FIGURE 43 INFRARED DETECTOR MARKET, BY APPLICATION

- FIGURE 44 PEOPLE & MOTION SENSING SEGMENT TO HOLD LARGER MARKET SHARE IN INFRARED DETECTOR MARKET DURING FORECAST PERIOD

- TABLE 59 INFRARED DETECTOR MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 60 INFRARED DETECTOR MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 10.2 PEOPLE & MOTION SENSING

- 10.2.1 PLAY CRUCIAL ROLE IN SECURITY SYSTEMS BY DETECTING HUMAN MOVEMENT OR PRESENCE IN RESTRICTED AREAS

- TABLE 61 PEOPLE & MOTION SENSING: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2019-2022 (USD MILLION)

- TABLE 62 PEOPLE & MOTION SENSING: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2023-2028 (USD MILLION)

- TABLE 63 PEOPLE & MOTION SENSING: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 64 PEOPLE & MOTION SENSING: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 65 PEOPLE & MOTION SENSING: INFRARED DETECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 66 PEOPLE AND MOTION SENSING: INFRARED DETECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 67 PEOPLE & MOTION SENSING: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 68 PEOPLE & MOTION SENSING: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.3 TEMPERATURE MEASUREMENT

- 10.3.1 HIGH DEMAND IN RESIDENTIAL, COMMERCIAL, AND MEDICAL VERTICALS

- TABLE 69 TEMPERATURE MEASUREMENT: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2019-2022 (USD MILLION)

- TABLE 70 TEMPERATURE MEASUREMENT: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2023-2028 (USD MILLION)

- TABLE 71 TEMPERATURE MEASUREMENT: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 72 TEMPERATURE MEASUREMENT: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 73 TEMPERATURE MEASUREMENT: INFRARED DETECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 74 TEMPERATURE MEASUREMENT: INFRARED DETECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 75 TEMPERATURE MEASUREMENT: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 76 TEMPERATURE MEASUREMENT: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.4 SECURITY & SURVEILLANCE

- 10.4.1 WIDELY USED IN SECURITY & SURVEILLANCE ATTRIBUTED TO NIGHT VISION, COVERT MONITORING, AND EXTENDED DETECTION RANGE CAPABILITIES

- TABLE 77 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2019-2022 (USD MILLION)

- TABLE 78 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2023-2028 (USD MILLION)

- TABLE 79 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 80 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 81 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 82 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 83 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 84 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.5 GAS & FIRE DETECTION

- 10.5.1 HELPS DETECT LEAKAGE OF HAZARDOUS GASES

- TABLE 85 GAS & FIRE DETECTION: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2019-2022 (USD MILLION)

- TABLE 86 GAS & FIRE DETECTION: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2023-2028 (USD MILLION)

- TABLE 87 GAS & FIRE DETECTION: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 88 GAS & FIRE DETECTION: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 89 GAS & FIRE DETECTION: INFRARED DETECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 90 GAS & FIRE DETECTION: INFRARED DETECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 91 GAS & FIRE DETECTION: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 92 GAS & FIRE DETECTION: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.6 SPECTROSCOPY & BIOMEDICAL IMAGING

- 10.6.1 USED TO IDENTIFY AND DETECT MEDICINE AND BIOMEDICAL COMPOSITIONS

- TABLE 93 SPECTROSCOPY & BIOMEDICAL IMAGING: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2019-2022 (USD MILLION)

- TABLE 94 SPECTROSCOPY & BIOMEDICAL IMAGING: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2023-2028 (USD MILLION)

- TABLE 95 SPECTROSCOPY & BIOMEDICAL IMAGING: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 96 SPECTROSCOPY & BIOMEDICAL IMAGING: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 97 SPECTROSCOPY & BIOMEDICAL IMAGING: INFRARED DETECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 98 SPECTROSCOPY & BIOMEDICAL IMAGING: INFRARED DETECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 99 SPECTROSCOPY & BIOMEDICAL IMAGING: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 100 SPECTROSCOPY & BIOMEDICAL IMAGING: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.7 OTHERS

- TABLE 101 OTHERS: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2019-2022 (USD MILLION)

- TABLE 102 OTHERS: INFRARED DETECTOR MARKET, BY WAVELENGTH, 2023-2028 (USD MILLION)

- TABLE 103 OTHERS: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 104 OTHERS: INFRARED DETECTOR MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 105 OTHERS: INFRARED DETECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 106 OTHERS: INFRARED DETECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 107 OTHERS: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 108 OTHERS: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

11 INFRARED DETECTOR MARKET, BY REGION

- 11.1 INTRODUCTION

- FIGURE 45 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN INFRARED DETECTOR MARKET DURING FORECAST PERIOD

- TABLE 109 INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 110 INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 46 NORTH AMERICA: SNAPSHOT OF INFRARED DETECTOR MARKET

- TABLE 111 NORTH AMERICA: INFRARED DETECTOR MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 112 NORTH AMERICA: INFRARED DETECTOR MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.2.2 US

- 11.2.2.1 Presence of several prominent automobile, aircraft, electronics, and healthcare companies

- 11.2.3 CANADA

- 11.2.3.1 High investments in defense modernization programs

- 11.2.4 MEXICO

- 11.2.4.1 Rising structural reforms

- 11.3 EUROPE

- 11.3.1 EUROPE: RECESSION IMPACT

- FIGURE 47 EUROPE: SNAPSHOT OF INFRARED DETECTOR MARKET

- TABLE 113 EUROPE: INFRARED DETECTOR MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 114 EUROPE: INFRARED DETECTOR MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.3.2 UK

- 11.3.2.1 High demand for infrared detectors in people & motion sensing and temperature measurement applications

- 11.3.3 GERMANY

- 11.3.3.1 Growing use in industrial sector to ensure product quality and process control

- 11.3.4 FRANCE

- 11.3.4.1 Increasing demand for infrared detectors in aerospace & defense industry

- 11.3.5 ITALY

- 11.3.5.1 Rising demand in temperature measurement and thermal imaging applications

- 11.3.6 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 48 ASIA PACIFIC: SNAPSHOT OF INFRARED DETECTOR MARKET

- TABLE 115 ASIA PACIFIC: INFRARED DETECTOR MARKET, 2019-2022 (USD MILLION)

- TABLE 116 ASIA PACIFIC: INFRARED DETECTOR MARKET, 2023-2028 (USD MILLION)

- 11.4.2 JAPAN

- 11.4.2.1 Booming manufacturing vertical

- 11.4.3 CHINA

- 11.4.3.1 High potential in industrial vertical and nonindustrial verticals

- 11.4.4 TAIWAN

- 11.4.4.1 Expanding electronics and information & communication technology verticals

- 11.4.5 REST OF ASIA PACIFIC

- 11.5 ROW

- 11.5.1 ROW: RECESSION IMPACT

- TABLE 117 ROW: INFRARED DETECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 118 ROW: INFRARED DETECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.5.2 SOUTH AMERICA

- 11.5.2.1 Increasing adoption of cutting-edge wireless communication and networking technologies

- 11.5.3 MIDDLE EAST

- 11.5.3.1 Booming oil & gas and automotive verticals

- 11.5.4 AFRICA

- 11.5.4.1 Growing commercial, residential, mining, and oil & gas verticals

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- TABLE 119 KEY STRATEGIES ADOPTED BY MAJOR MARKET PLAYERS, 2021-2022

- 12.2 MARKET SHARE ANALYSIS

- TABLE 120 INFRARED DETECTOR MARKET: DEGREE OF COMPETITION

- FIGURE 49 MARKET SHARE ANALYSIS: INFRARED DETECTOR MARKET, 2022

- 12.3 REVENUE ANALYSIS OF TOP PLAYERS IN INFRARED DETECTOR MARKET

- FIGURE 50 FIVE-YEAR REVENUE ANALYSIS OF TOP PLAYERS IN INFRARED DETECTOR MARKET

- 12.4 COMPANY EVALUATION QUADRANT, 2022

- 12.4.1 STARS

- 12.4.2 PERVASIVE PLAYERS

- 12.4.3 EMERGING LEADERS

- 12.4.4 PARTICIPANTS

- FIGURE 51 INFRARED DETECTOR MARKET (GLOBAL): COMPANY EVALUATION QUADRANT, 2022

- 12.5 COMPANY FOOTPRINT

- TABLE 121 COMPANY FOOTPRINT

- TABLE 122 WAVELENGTH: COMPANY FOOTPRINT

- TABLE 123 APPLICATION: COMPANY FOOTPRINT

- TABLE 124 REGION: COMPANY FOOTPRINT

- 12.6 STARTUPS/SMALL AND MEDIUM-SIZED ENTREPRISES (SMES) EVALUATION QUADRANT, 2022

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- FIGURE 52 INFRARED DETECTOR MARKET: STARTUPS/SMES EVALUATION QUADRANT, 2022

- 12.7 COMPETITIVE BENCHMARKING

- TABLE 125 INFRARED DETECTOR MARKET: KEY STARTUPS/SMES

- TABLE 126 INFRARED DETECTOR MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 12.8 COMPETITIVE SCENARIOS AND TRENDS

- 12.8.1 PRODUCT LAUNCHES

- TABLE 127 INFRARED DETECTOR MARKET: PRODUCT LAUNCHES, NOVEMBER 2021-APRIL 2023

- 12.8.2 DEALS

- TABLE 128 INFRARED DETECTOR MARKET: DEALS, MAY 2021-SEPTEMBER 2022

- 12.8.3 OTHERS

- TABLE 129 INFRARED DETECTOR MARKET: OTHERS, JUNE 2022-MARCH 2023

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- (Business Overview, Products Offered, Recent Developments, and MnM View)**

- 13.1.1 EXCELITAS TECHNOLOGIES CORP.

- TABLE 130 EXCELITAS TECHNOLOGIES CORP.: COMPANY OVERVIEW

- TABLE 131 EXCELITAS TECHNOLOGIES CORP.: PRODUCT OFFERING

- TABLE 132 EXCELITAS TECHNOLOGIES CORP.: PRODUCT LAUNCHES

- TABLE 133 EXCELITAS TECHNOLOGIES CORP.: DEALS

- 13.1.2 HAMAMATSU PHOTONICS K.K.

- TABLE 134 HAMAMATSU PHOTONICS K.K.: COMPANY OVERVIEW

- FIGURE 53 HAMAMATSU PHOTONICS K.K.: COMPANY SNAPSHOT

- TABLE 135 HAMAMATSU PHOTONICS K.K.: PRODUCT OFFERING

- TABLE 136 HAMAMATSU PHOTONICS K.K.: PRODUCT LAUNCHES

- 13.1.3 MURATA MANUFACTURING CO., LTD.

- TABLE 137 MURATA MANUFACTURING CO., LTD.: COMPANY OVERVIEW

- FIGURE 54 MURATA MANUFACTURING CO., LTD.: COMPANY SNAPSHOT

- TABLE 138 MURATA MANUFACTURING CO., LTD.: PRODUCT OFFERING

- TABLE 139 MURATA MANUFACTURING CO., LTD.: OTHERS

- 13.1.4 TELEDYNE FLIR LLC

- TABLE 140 TELEDYNE FLIR LLC: COMPANY OVERVIEW

- TABLE 141 TELEDYNE FLIR LLC: PRODUCT OFFERING

- TABLE 142 TELEDYNE FLIR LLC: PRODUCT LAUNCHES

- 13.1.5 TEXAS INSTRUMENTS INCORPORATED

- TABLE 143 TEXAS INSTRUMENTS INCORPORATED: COMPANY OVERVIEW

- FIGURE 55 TEXAS INSTRUMENTS INCORPORATED: COMPANY SNAPSHOT

- TABLE 144 TEXAS INSTRUMENTS INCORPORATED: PRODUCT OFFERING

- TABLE 145 TEXAS INSTRUMENTS INCORPORATED: PRODUCT LAUNCHES

- TABLE 146 TEXAS INSTRUMENTS INCORPORATED: DEALS

- 13.1.6 NIPPON CERAMIC CO., LTD.

- TABLE 147 NIPPON CERAMIC CO., LTD.: COMPANY OVERVIEW

- FIGURE 56 NIPPON CERAMIC CO., LTD.: COMPANY SNAPSHOT

- TABLE 148 NIPPON CERAMIC CO., LTD.: PRODUCT OFFERING

- 13.1.7 OMRON CORPORATION

- TABLE 149 OMRON CORPORATION: COMPANY OVERVIEW

- FIGURE 57 OMRON CORPORATION: COMPANY SNAPSHOT

- TABLE 150 OMRON CORPORATION: PRODUCT OFFERING

- TABLE 151 OMRON CORPORATION: PRODUCT LAUNCHES

- 13.1.8 INFRATEC GMBH

- TABLE 152 INFRATEC GMBH: COMPANY OVERVIEW

- TABLE 153 INFRATEC GMBH: PRODUCT OFFERING

- TABLE 154 INFRATEC GMBH: PRODUCT LAUNCHES

- 13.1.9 LYNRED

- TABLE 155 LYNRED: BUSINESS OVERVIEW

- TABLE 156 LYNRED: PRODUCT OFFERING

- TABLE 157 LYNRED: PRODUCT LAUNCHES

- TABLE 158 LYNRED: DEALS

- 13.1.10 TE CONNECTIVITY

- TABLE 159 TE CONNECTIVITY: COMPANY OVERVIEW

- FIGURE 58 TE CONNECTIVITY: COMPANY SNAPSHOT

- TABLE 160 TE CONNECTIVITY: PRODUCT OFFERING

- TABLE 161 TE CONNECTIVITY: PRODUCT LAUNCHES

- TABLE 162 TE CONNECTIVITY: DEALS

- TABLE 163 TE CONNECTIVITY: OTHERS

- * Business Overview, Products Offered, Recent Developments, and MnM View might not be captured in case of unlisted companies.

- 13.2 OTHER COMPANIES

- 13.2.1 HONEYWELL INTERNATIONAL INC.

- 13.2.2 RAYTHEON TECHNOLOGIES CORPORATION

- 13.2.3 LASER COMPONENTS

- 13.2.4 DRAGERWERK AG & CO. KGAA

- 13.2.5 VIGO PHOTONICS S.A.

- 13.2.6 XENICS NV.

- 13.2.7 MELEXIS

- 13.2.8 FAGUS-GRECON

- 13.2.9 THORLABS, INC.

- 13.2.10 SEMITEC CORPORATION

- 13.2.11 IRNOVA AB

- 13.2.12 GLOBAL SENSOR TECHNOLOGY CO., LTD.

- 13.2.13 DIAS INFRARED GMBH

- 13.2.14 SENSORS UNLIMITED, INC.

- 13.2.15 IRAY TECHNOLOGY CO., LTD. (INFIRAY)

14 ADJACENT AND RELATED MARKETS

- 14.1 INTRODUCTION

- 14.2 STUDY LIMITATIONS

- 14.3 GAS SENSOR MARKET, BY TECHNOLOGY

- FIGURE 59 GAS SENSOR MARKET, BY TECHNOLOGY

- FIGURE 60 ELECTROCHEMICAL SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- TABLE 164 GAS SENSOR MARKET, BY TECHNOLOGY, 2018-2021 (USD MILLION)

- TABLE 165 GAS SENSOR MARKET, BY TECHNOLOGY, 2022-2027 (USD MILLION)

- 14.4 ELECTROCHEMICAL

- 14.4.1 USED IN LOW-CONCENTRATION GAS RANGES

- FIGURE 61 SCHEMATIC OF ELECTROCHEMICAL GAS SENSORS IN CLEAN AIR

- 14.5 PHOTOIONIZATION DETECTORS

- 14.5.1 WIDELY USED IN GAS CHROMATOGRAPHY

- 14.6 SOLID-STATE/METAL-OXIDE-SEMICONDUCTOR

- 14.6.1 LIGHTWEIGHT AND OFFERS HIGH SENSITIVITY AND FAST RESPONSE TIME

- 14.7 CATALYTIC

- 14.7.1 SURGING ADOPTION OF AMMONIA AND METHANE GAS SENSORS

- FIGURE 62 OPERATING PRINCIPLE OF CATALYTIC GAS SENSORS IN CLEAN AIR

- 14.8 INFRARED

- 14.8.1 USED IN INDUSTRIAL, HVAC, AND IQM APPLICATIONS

- FIGURE 63 OPERATING PRINCIPLE OF INFRARED GAS SENSORS

- 14.9 LASER

- 14.9.1 ENABLES LONG-RANGE DETECTION OF GASES

- 14.10 ZIRCONIA

- 14.10.1 MAINLY USED IN OXYGEN GAS SENSORS

- 14.11 HOLOGRAPHIC

- 14.11.1 USED FOR GAS DETECTION TO MEASURE REFLECTION PROPERTIES

- 14.12 OTHERS

15 APPENDIX

- 15.1 INSIGHTS FROM INDUSTRY EXPERTS

- 15.2 DISCUSSION GUIDE

- 15.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.4 CUSTOMIZATION OPTIONS

- 15.5 RELATED REPORTS

- 15.6 AUTHOR DETAILS