|

|

市場調査レポート

商品コード

1280002

ゲーム用メタバースの世界市場:コンポーネント別・ハードウェア別・ソフトウェア別 (XRソフトウェア、ゲームエンジン、メタバースプラットフォーム、金融プラットフォーム)・ゲームジャンル別・地域別の将来予測 (2028年まで)Metaverse in Gaming Market by Component Hardware (AR Devices, VR Devices, MR Devices, Displays), Software (Extended Reality Software, Gaming Engines, Metaverse Platforms, Financial Platforms), Game Genre and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| ゲーム用メタバースの世界市場:コンポーネント別・ハードウェア別・ソフトウェア別 (XRソフトウェア、ゲームエンジン、メタバースプラットフォーム、金融プラットフォーム)・ゲームジャンル別・地域別の将来予測 (2028年まで) |

|

出版日: 2023年05月22日

発行: MarketsandMarkets

ページ情報: 英文 247 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界のゲーム用メタバースの市場規模は、2023年には227億米ドル、2028年には1,192億米ドルへと、39.3%のCAGRで成長すると予測されます。

ゲーム用メタバース市場の成長を促進する主な要因としては、XR (Extended Reality:VR、AR、MRほか) などの隣接技術市場における強固で変化する成長状況などが挙げられます。ブロックチェーン技術や、ゲーミングメタバース市場におけるゲーマー向け報酬用の金融モデル (暗号通貨など)、仮想化、5G、IoTなどもまた、ゲーミングメタバース市場における到達や普及、ひいては需要を後押しする触媒として主要な促進要因であると考えられています。さらに、従来型ゲームからVRベースゲームへの移行、複合現実 (MR) の出現、マルチプレイヤーゲームにおける分散化の需要は、この市場のベンダーに十分な機会を提供しています。

"予測期間中、サービスのセグメントが顕著な成長を遂げる"

サービスは、あらゆるソリューションの展開ライフサイクルの重要な部分を占めています。そのため、さまざまなベンダーがメタバースに関連するサービスを提供し、企業がメタバースベースのビジネス慣行や戦略を効果的に実行できるように支援しています。メタバースサービスには、アプリケーション開発、システムインテグレーション、戦略・ビジネスコンサルティングサービスなどがあります。これらのサービスは、販売前の要件評価から販売後の製品展開や実行まで、さまざまな段階で必要とされるため、クライアントは最大限の投資収益率 (RoI) を得ることが可能になっています。開発サービスは、より速く機能をリリースでき、拡張性があり、楽しい顧客体験を提供する世界クラスのWeb・モバイルアプリケーションを提供するのに役立ちます。メタバース開発サービスには、メタバースゲーム開発、メタバースNFTマーケットプレース開発、メタバース不動産プラットフォーム開発、メタバースアプリ開発、メタバースソーシャルメディアプラットフォーム開発、メタバース教育プラットフォーム開発、メタバースイベントプラットフォーム開発、などがあります。サービス分野のコンポーネントには、ゲーミングメタバース市場、ゲームローンチパッド開発、NFTゲーム開発、プレイトゥイヤーモデルゲーム開発などが含まれます。

"予測期間中、欧州が2番目に高いCAGRで成長する"

英国、ドイツ、フランスは、西欧で新技術の開発に多額の投資を行っている数少ない国です。ロシアとスペインは、さまざまな用途に使用される新しいディスプレイ技術を採用することで、徐々に人気を集めています。欧州における仮想世界没入型インタラクティブゲーム産業の大幅な成長は、この地域のゲーミングメタバース市場の重要な促進要因となっています。AR/VR/MR技術は、同地域のエンターテインメント (ゲーミングメタバース) 部門から大きな需要を示すことが期待されます。

この地域のEuroVR (European Association for Virtual Reality and Augmented Reality) は、さまざまな用途で使用するXRに関連した新しい開発をもたらすのに役立っています。このことは、この地域におけるゲーム用メタバース市場の成長に貢献すると予測されます。欧州連合は、Augmented HeritageやInternational Augmented Med (I AM) などのプロジェクトを立ち上げており、これらは市場の成長に貢献すると予想されます。International Augmented Medプロジェクトは、XR技術を用いた地中海地域の観光振興に各国が参加するものです。スペイン、ポルトガル、マルタ、キプロス、フランス、ギリシャ、イタリアがこのプロジェクトに参加しています。スウェーデンではXR関連のスタートアップが増加しており、2026年には欧州でゲーム用メタバース市場がより高い成長を遂げると予想されます。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要と業界動向

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ケーススタディ分析

- エコシステム

- バリューチェーン分析

- エンドユーザーの好みと傾向分析:年齢層別

- 技術分析

- 価格分析

- 特許分析

- ポーターのファイブフォースモデル

- 主要な利害関係者と購入基準

- 規制状況

- 主な会議とイベント (2023年~2024年)

- バイヤーに影響を与える動向/混乱

第6章 ゲーム用メタバース市場:コンポーネント別

- イントロダクション

- ハードウェア

- ソフトウェア

- サービス

第7章 ゲーム用メタバース市場:ハードウェア別

- イントロダクション

- ARデバイス

- VRデバイス

- MRデバイス

- ディスプレイ

第8章 ゲーム用メタバース市場:ソフトウェア別

- イントロダクション

- XRソフトウェア

- ゲームエンジン

- 3Dマッピング、モデリング、再構築

- 金融プラットフォーム

- メタバースプラットフォーム

第9章 ゲーム用メタバース市場:ゲームジャンル別

- イントロダクション

- アクション

- アドベンチャー

- カジュアル

- ロールプレイング

- シミュレーション

- スポーツ・レース

- 戦略

第10章 ゲーム用メタバース市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア王国

- その他の中東・アフリカ

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

第11章 競合情勢

- イントロダクション

- 上位ベンダーの市場シェア

- 上位ベンダー5社の収益分析

- 企業評価クアドラント (2022年)

- 企業評価クアドラント:スタートアップ/中小企業向け (2022年)

- 競合ベンチマーキング:スタートアップ/中小企業向け

- 企業の財務指標

- 主要な市場参入企業:世界のスナップショット

- 競合シナリオ

第12章 企業プロファイル

- イントロダクション

- 主要企業

- META (FORMERLY FACEBOOK)

- ACTIVISION BLIZZARD

- NETEASE

- ELECTRONIC ARTS

- TAKE-TWO

- TENCENT

- NEXON

- EPIC GAMES

- UNITY

- VALVE

- その他の企業

- ACCENTURE

- ADOBE

- HPE

- DELOITTE

- ANSYS

- AUTODESK INC.

- INTEL

- TECH MAHINDRA

- BYTEDANCE

- NVIDIA

- MICROSOFT

- SAMSUNG

- SONY

- HTC

- SEIKO EPSON

- APPLE

- QUALCOMM

- PANASONIC

- EON REALITY

- ROBLOX

- LENOVO

- RAZER

- NEXTECH AR SOLUTIONS

- ZQGAME

- TALECRAFT

- VR CHAT

- DECENTRALAND

- SOMNIUM SPACE

- SANDBOX VR

第13章 隣接・関連市場

- イントロダクション

- 制限事項

- メタバース市場

- AR (拡張現実) 市場

- VR (仮想現実) 市場

第14章 付録

The global metaverse in gaming market size is estimated at USD 22.7 billion in 2023 and is projected to reach USD 119.2 billion by 2028 at a CAGR of 39.3%. Major factors expected to fuel the growth of the metaverse in gaming market include robust and transforming growth landscape in the adjacent technology markets such as the extended reality which includes VR, AR, MR. Blockchain technology, financial model for rewarding gamers in the gaming metaverse market such as cryptocurrency, virtualization, 5G, Internet of Things (IoT), and few others are also the major boosting factors which as a catalyst drive the reach, penetration and eventually the demand in the gaming metaverse market. Further, the shift from traditional gaming to VR-based gaming, the advent of mixed reality, and the demand for decentralization in multiplayer games have provided ample opportunities for vendors in this market.

By Component, the services segment to showcase rising growth in the gaming metaverse development sector during the forecast period

Services are an important part of any solution's deployment life cycle. Hence, various vendors offer services associated with the metaverse to help companies effectively implement their metaverse-based business practices and strategies. The metaverse services involve application development, system integration, and strategy and business consulting services. These services are required at various stages, from pre-sales requirement assessment to post-sales product deployment and execution, thus enabling the client to get maximum Return on Investment (RoI). Development services help in delivering world-class web and mobile applications that can release features faster, are scalable and provide a delightful customer experience. The metaverse development services include Metaverse Game Development, Metaverse NFT Marketplace Development, Metaverse Real Estate Platform Development, Metaverse App Development, Metaverse Social Media Platform Development, Metaverse Education Platform Development, Metaverse Event Platform Development, among others. Components in the services segment include gaming metaverse marketplace, games launchpad development, NFT game development, and play-to-earn model game development, among others.

Europe to record the second highest CAGR during the forecast period

The UK, Germany, and France are a few countries in Western Europe that invest heavily in developing new technologies. Russia and Spain are slowly gaining traction by adopting new display technologies for use in various applications. The substantial growth of the virtual world immersive interactive gaming industry in Europe is a crucial driver for the gaming metaverse market in this region. The AR/VR/MR technologies are expected to witness significant demand from the entertainment (gaming metaverse) sector in the region.

The European Association for Virtual Reality and Augmented Reality (EuroVR) in the region helps bring new developments related to extended reality for use in various applications. This is projected to help the metaverse in gaming market grow in this region. The European Union has taken up projects such as Augmented Heritage and International Augmented Med (I AM), which are anticipated to contribute to the market's growth. The International Augmented Med project involves countries' participation in promoting tourism in the Mediterranean region using extended reality technologies. Spain, Portugal, Malta, Cyprus, France, Greece, and Italy are involved in this project. There is an increase in the number of startups related to extended reality in Sweden; as a result, the metaverse in gaming market is expected to witness higher growth in Europe by 2026.

In the process of evaluating, validating, and verifying the market size for several segments and subsegments collected/figured out through extensive secondary research, primary interviews were conducted with the Chief Executive Officers (CEOs), Chief Marketing Officers (CMO), Vice Presidents (VPs), Managing Directors (MDs), Chief Technology Officer [CTO], technology and innovation directors, and related key executives from various vendor companies and organizations operating in the metaverse in gaming market.

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: C-level executives- 40%, Director Level - 25%, and Others - 35%

- By Region: North America - 45%, Europe - 30%, Asia Pacific - 20%, Rest of World (RoW) - 5%

Note: Others include sales managers, marketing managers, and product managers

Note: Rest of the World includes the Middle East & Africa and Latin America

Note: Tier 1 companies have revenues more than USD 100 million; tier 2 companies' revenue ranges from USD 10 million to USD 100 million; and tier 3 companies' revenue is less than 10 million

Source: Secondary Literature, Expert Interviews, and MarketsandMarkets Analysis

The report profiles the following key vendors:

- Meta (US)

- Microsoft (US)

- NetEase (China)

- Electronic Arts (US)

- Take-Two (US)

- Tencent (China)

- Nexon (Japan)

- Epic games (US)

- Unity (US)

- Valve (US)

- Accenture (Ireland)

- Adobe (US)

- HPE (US)

- Deloitte (UK)

- Ansys (US)

- Autodesk (US)

- Intel (US)

- Tech Mahindra (India)

- ByteDance (China)

- Nvidia (US)

- Activision Blizzard (US)

- Samsung (South Korea)

- Google (US)

- Sony (Japan)

- HTC (Taiwan)

- Seiko Epson (Japan)

- Apple (US)

- Qualcomm (US)

- Panasonic (Japan)

- Eon Reality (US)

- Roblox (US)

- Lenovo (Hong Kong)

- Razer (US)

- Nextech AR Solutions (Canada)

- ZQGame (China)

- Talecraft (Marshall islands)

- VR Chat (US)

- Decentraland (Argentina)

- Somnium Space (UK)

- Sandbox VR (US)

Research Coverage

The metaverse in gaming market is segmented by component, hardware, software, game genre, and region. A detailed analysis of the key industry players has been undertaken to provide insights into their business overviews; solutions and services; key strategies; new product launches and product enhancements; partnerships, acquisitions, and collaborations; agreements and business expansions; and competitive landscape associated within the market.

Key Benefits of Buying the Report

The report would help the market leaders and new entrants in the following ways:

- The report comprehensively and exhaustively segments the metaverse in gaming market and provides the closest approximations of the revenue numbers for the overall market and its subsegments across different regions.

- It provides impact of recession on the market, among top vendors worldwide along with figures which are the closest approximations, estimated and projected.

- It would help stakeholders understand the pulse of the market as analyzed information is provided basis the key market drivers, restraints, challenges, and opportunities in the market.

- It would help stakeholders understand the market dynamics better, their competitors better and gain more insights to uplift their positions in the market. The competitive landscape section includes a competitor ecosystem, market diversification parameters such as new product launch, product enhancement, partnerships, agreement, integration, collaborations, and acquisitions.

- Market quadrant of metaverse in gaming vendors have been precisely incorporated as a figure which helps readers understand market players categorization and their performance.

- In-depth exhaustive assessment of market shares, growth strategies and service offerings of leading players in the metaverse in gaming market strategies.

- The report also helps stakeholders understand the competitive analysis by these market players via competitive benchmarking, heat map.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATES, 2019-2022

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 METAVERSE IN GAMING MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- TABLE 2 LIST OF KEY SECONDARY SOURCES

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primaries

- 2.1.2.2 Primary respondents

- TABLE 3 PRIMARY RESPONDENTS: METAVERSE IN GAMING MARKET

- 2.1.2.3 Key industry insights

- 2.2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- FIGURE 2 METAVERSE IN GAMING MARKET: TOP-DOWN AND BOTTOM-UP APPROACH

- 2.3.1 SUPPLY-SIDE APPROACH

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 1 (SUPPLY SIDE): REVENUE OF METAVERSE IN GAMING FROM VENDORS

- FIGURE 4 BOTTOM-UP APPROACH (SUPPLY SIDE): COLLECTIVE REVENUE OF METAVERSE IN GAMING VENDORS

- FIGURE 5 MARKET PROJECTIONS FROM SUPPLY SIDE

- 2.3.2 DEMAND-SIDE APPROACH

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY ̶ APPROACH 2 (DEMAND SIDE): REVENUE OF VENDORS FROM VARIOUS GAME PLAYERS

- FIGURE 7 MARKET PROJECTIONS FROM DEMAND SIDE

- 2.4 MARKET FORECAST

- TABLE 4 FACTOR ANALYSIS

- 2.4.1 RECESSION IMPACT ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- TABLE 5 ASSUMPTIONS

- 2.6 LIMITATIONS

3 EXECUTIVE SUMMARY

- FIGURE 8 GLOBAL METAVERSE IN GAMING MARKET, 2020-2028 (USD MILLION)

- FIGURE 9 FASTEST-GROWING SEGMENTS IN METAVERSE IN GAMING MARKET, 2023-2028

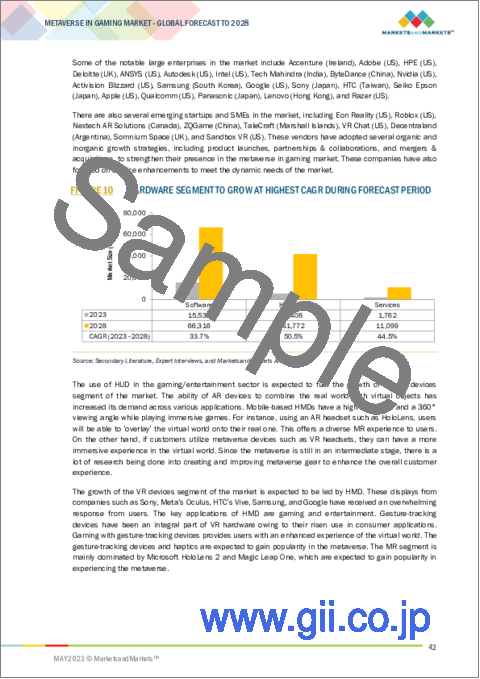

- FIGURE 10 HARDWARE SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 11 AR DEVICES SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 FINANCIAL PLATFORMS SEGMENT TO GROW AT HIGHEST CAGR BY 2028

- FIGURE 13 STRATEGY SEGMENT TO GROW AT HIGHEST CAGR TILL 2028

- FIGURE 14 METAVERSE IN GAMING MARKET: REGIONAL SNAPSHOT

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR COMPANIES IN METAVERSE IN GAMING MARKET

- FIGURE 15 STRONG VR, MR LIVESTREAMING, AND INTERACTIVE GAMING INTEREST AMONG YOUTH TO DRIVE MARKET

- 4.2 METAVERSE IN GAMING MARKET, BY COMPONENT, 2023 VS. 2028

- FIGURE 16 SOFTWARE SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.3 METAVERSE IN GAMING MARKET, BY HARDWARE, 2023 VS. 2028

- FIGURE 17 AR DEVICES SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.4 METAVERSE IN GAMING MARKET, BY SOFTWARE, 2023 VS. 2028

- FIGURE 18 EXTENDED REALITY SOFTWARE SEGMENT TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- 4.5 METAVERSE IN GAMING MARKET, BY GAME GENRE, 2023 VS. 2028

- FIGURE 19 ADVENTURE SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.6 METAVERSE IN GAMING MARKET: REGIONAL SCENARIO, 2023-2028

- FIGURE 20 ASIA PACIFIC TO EMERGE AS BEST MARKET FOR INVESTMENTS IN NEXT FIVE YEARS

- FIGURE 21 METAVERSE IN GAMING MARKET IN SOUTH KOREA TO GROW AT HIGHEST RATE DURING FORECAST PERIOD

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 22 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: METAVERSE IN GAMING MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing demand in entertainment and gaming industries

- 5.2.1.2 VR gaming becoming more immersive, interactive, and real

- 5.2.1.3 Emerging opportunities from adjacent markets

- TABLE 6 MARKET SIZE AND GROWTH RATES OF ADJACENT MARKETS

- 5.2.1.4 Brand promotions using gamification and virtual world simulators

- 5.2.1.5 Availability of affordable hardware

- 5.2.2 RESTRAINTS

- 5.2.2.1 High installation and maintenance costs of high-end metaverse in gaming components

- 5.2.2.2 Health and mental issues from excessive use

- 5.2.2.3 Regulating metaverse in gaming with respect to cybersecurity, privacy, and usage standards

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Easier hosting of events and better engagement

- 5.2.3.2 Significant growth opportunities despite possible economic slowdown

- 5.2.4 CHALLENGES

- 5.2.4.1 Regional government regulations, coupled with environmental impact

- 5.3 CASE STUDY ANALYSIS

- 5.3.1 CASE STUDY 1: UNITY ENGINE LEVERAGED LAUNCH OF MULTIPLATFORM GAMING SERVICE

- 5.3.2 CASE STUDY 2: TENCENT CLOUD AMPLIFIED MILDOM'S LIVESTREAMING USER EXPERIENCE

- 5.4 ECOSYSTEM

- FIGURE 23 METAVERSE IN GAMING MARKET: ECOSYSTEM

- TABLE 7 METAVERSE IN GAMING MARKET: COMPANIES AND THEIR ROLE IN ECOSYSTEM

- 5.5 VALUE CHAIN ANALYSIS

- FIGURE 24 VALUE CHAIN ANALYSIS: METAVERSE IN GAMING MARKET

- 5.5.1 SUPPLIERS

- 5.5.2 HARDWARE MANUFACTURERS

- 5.5.3 SOFTWARE VENDORS

- 5.5.4 END USERS

- 5.6 END-USER PREFERENCES AND TREND ANALYSIS, BY AGE GROUP

- 5.6.1 11 TO 19 YEARS

- 5.6.2 20 TO 35 YEARS

- 5.6.3 36 YEARS & ABOVE

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 TECHNOLOGY STACK

- FIGURE 25 METAVERSE IN GAMING MARKET: TECHNOLOGIES

- 5.7.2 INFRASTRUCTURE LEVEL

- 5.7.2.1 5G network

- 5.7.2.2 Internet of things

- 5.7.2.3 Cloud and edge computing

- 5.7.3 DESIGN AND DEVELOPMENT LEVEL

- 5.7.3.1 Blockchain

- 5.7.3.2 3D modeling and real-time rendering

- 5.7.3.3 Artificial intelligence, natural language processing, and computer vision

- 5.7.4 HUMAN INTERACTION LEVEL

- 5.7.4.1 Virtual reality

- 5.7.4.2 Augmented reality

- 5.7.4.2.1 Mobile augmented reality

- 5.7.4.2.2 Monitor-based AR technology

- 5.7.4.2.3 Near-eye-based AR technology

- 5.7.4.2.4 Web AR

- 5.7.4.3 Mixed reality

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE TREND

- 5.9 PATENT ANALYSIS

- FIGURE 26 NUMBER OF PATENTS PUBLISHED, 2012-2022

- FIGURE 27 TOP FIVE PATENT OWNERS (GLOBAL)

- TABLE 8 TOP TEN PATENT OWNERS (US)

- TABLE 9 KEY PATENTS IN METAVERSE IN GAMING MARKET

- 5.10 PORTER'S FIVE FORCES MODEL

- FIGURE 28 METAVERSE IN GAMING MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 10 METAVERSE IN GAMING MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.10.2 BARGAINING POWER OF SUPPLIERS

- 5.10.3 BARGAINING POWER OF BUYERS

- 5.10.4 THREAT OF NEW ENTRANTS

- 5.10.5 THREAT OF SUBSTITUTES

- 5.11 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS

- TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS (%)

- 5.11.2 BUYING CRITERIA

- FIGURE 30 KEY BUYING CRITERIA FOR TOP END USERS

- TABLE 12 KEY BUYING CRITERIA FOR TOP END USERS

- 5.12 REGULATORY LANDSCAPE

- 5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12.2 REGULATORY IMPLICATIONS AND INDUSTRY STANDARDS

- 5.13 KEY CONFERENCES AND EVENTS IN 2023-2024

- TABLE 17 METAVERSE IN GAMING MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

- 5.14 TRENDS/DISRUPTIONS IMPACTING BUYERS

- FIGURE 31 METAVERSE IN GAMING MARKET: TRENDS/DISRUPTIONS IMPACTING BUYERS

6 METAVERSE IN GAMING MARKET, BY COMPONENT

- 6.1 INTRODUCTION

- 6.1.1 COMPONENT: METAVERSE IN GAMING MARKET DRIVERS

- FIGURE 32 SOFTWARE SEGMENT TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- TABLE 18 METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 19 METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 6.2 HARDWARE

- 6.2.1 RISING YOUTH INTEREST TO FUEL DEMAND FOR GAMING HARDWARE DEVICES

- TABLE 20 HARDWARE: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 21 HARDWARE: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3 SOFTWARE

- 6.3.1 REQUIREMENT OF GAMING ENGINE AND RT3D SOFTWARE AMONG GAMERS TO FUEL MARKET GROWTH

- TABLE 22 SOFTWARE: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 23 SOFTWARE: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4 SERVICES

- 6.4.1 INTEGRATION OF ONLINE GAMING, SOCIAL NETWORKING, AR, AND VR TECHNOLOGIES TO BOOST MARKET GROWTH

- TABLE 24 SERVICES: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 25 SERVICES: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

7 METAVERSE IN GAMING MARKET, BY HARDWARE

- 7.1 INTRODUCTION

- 7.1.1 HARDWARE: METAVERSE IN GAMING MARKET DRIVERS

- FIGURE 33 AR DEVICES SEGMENT TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- TABLE 26 METAVERSE IN GAMING MARKET, BY HARDWARE, 2019-2022 (USD MILLION)

- TABLE 27 METAVERSE IN GAMING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- 7.2 AR DEVICES

- 7.2.1 LIVESTREAM GAMING AND ENTERTAINMENT TO FUEL DEMAND FOR AR DEVICE PRODUCTION AND TECHNOLOGY ADVANCEMENTS

- TABLE 28 AR DEVICES: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 29 AR DEVICES: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.3 VR DEVICES

- 7.3.1 SIGNIFICANT IMPROVEMENTS VIS-A-VIS MASS, COST, VOLUME, SIMPLICITY, AND OPTICAL PERFORMANCE TO FUEL VR DEVICE ADOPTION

- TABLE 30 VR DEVICES: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 31 VR DEVICES: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.4 MR DEVICES

- 7.4.1 RISE IN BODY GESTURE SENSING IN GAMING METAVERSE TO SUPPORT GROWING ADOPTION OF MR DEVICES

- TABLE 32 MR DEVICES: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 33 MR DEVICES: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.5 DISPLAYS

- 7.5.1 ENHANCED SCREEN RESOLUTION, REAL-TIME AMBIENCE EXPERIENCE, AND HIGHER QUALITY VIDEO TO PUSH VENDORS TO MANUFACTURE STATE-OF-THE-ART DISPLAYS

- TABLE 34 DISPLAYS: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 35 DISPLAYS: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

8 METAVERSE IN GAMING MARKET, BY SOFTWARE

- 8.1 INTRODUCTION

- 8.1.1 SOFTWARE: METAVERSE IN GAMING MARKET DRIVERS

- FIGURE 34 EXTENDED REALITY SOFTWARE SEGMENT TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- TABLE 36 METAVERSE IN GAMING MARKET, BY SOFTWARE, 2019-2022 (USD MILLION)

- TABLE 37 METAVERSE IN GAMING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- 8.1.2 EXTENDED REALITY SOFTWARE

- 8.1.2.1 SDK development to become need of hour

- TABLE 38 EXTENDED REALITY SOFTWARE: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 39 EXTENDED REALITY SOFTWARE: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.1.3 GAMING ENGINES

- 8.1.3.1 Transforming gamers' ecosystem to fuel demand for innovation and R&D for gaming engine vendors

- TABLE 40 GAMING ENGINES: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 41 GAMING ENGINES: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.1.4 3D MAPPING, MODELING, AND RECONSTRUCTION

- 8.1.4.1 Emerging use of 3D software for expressive avatar creation and 3D world design to drive market

- TABLE 42 3D MAPPING, MODELING, AND RECONSTRUCTION: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 43 3D MAPPING, MODELING, AND RECONSTRUCTION: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.1.5 FINANCIAL PLATFORMS

- 8.1.5.1 NFT and cryptocurrency rewards, along with tokenization model, to attract gamers in metaverse

- TABLE 44 FINANCIAL PLATFORMS: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 45 FINANCIAL PLATFORMS: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.1.6 METAVERSE PLATFORMS

- 8.1.6.1 Building effective and desired avatars to create interest among gamers in RT3D ecosystem

- TABLE 46 METAVERSE PLATFORMS: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 47 METAVERSE PLATFORMS: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

9 METAVERSE IN GAMING MARKET, BY GAME GENRE

- 9.1 INTRODUCTION

- 9.1.1 GAME GENRE: METAVERSE IN GAMING MARKET DRIVERS

- FIGURE 35 STRATEGY SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 48 METAVERSE IN GAMING MARKET, BY GAME GENRE, 2019-2022 (USD MILLION)

- TABLE 49 METAVERSE IN GAMING MARKET, BY GAME GENRE, 2023-2028 (USD MILLION)

- 9.2 ACTION

- 9.2.1 POPULARITY OF LIVESTREAMING AND ESPORTS GAME TOURNAMENTS TO FUEL DEMAND FOR THIS GENRE

- TABLE 50 ACTION: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 51 ACTION: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3 ADVENTURE

- 9.3.1 METAVERSE TO PROVIDE ENHANCEMENTS IN COMBAT, EXPLORATION, AND SURVIVAL GAMES

- TABLE 52 ADVENTURE: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 53 ADVENTURE: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.4 CASUAL

- 9.4.1 INCREASING USE OF VR IN COLLABORATIVE FAMILY AND CHILDREN GAMES TO DRIVE MARKET

- TABLE 54 CASUAL: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 55 CASUAL: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.5 ROLE-PLAYING

- 9.5.1 METAVERSE TO PROVIDE HIGHLY DETAILED AND VISUALLY STUNNING EXPERIENCE IN ROLE-PLAYING GAMES

- TABLE 56 ROLE-PLAYING: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 57 ROLE-PLAYING: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.6 SIMULATION

- 9.6.1 EMERGING USE OF EXTENDED REALITY IN FLIGHT AND TRUCK SIMULATION GAMES TO DRIVE MARKET

- TABLE 58 SIMULATION: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 59 SIMULATION: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.7 SPORTS & RACING

- 9.7.1 RISING POPULARITY OF METAVERSE IN MULTIPLAYER SPORTS & RACING GAMES TO DRIVE MARKET

- TABLE 60 SPORTS & RACING: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 61 SPORTS & RACING: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.8 STRATEGY

- 9.8.1 INCREASING POPULARITY OF USER-GENERATED CONTENT IN MULTIPLAYER STRATEGY GAMES TO DRIVE MARKET

- TABLE 62 STRATEGY: METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 63 STRATEGY: METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

10 METAVERSE IN GAMING MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 36 ASIA PACIFIC TO GROW AT HIGHEST RATE DURING FORECAST PERIOD

- TABLE 64 METAVERSE IN GAMING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 65 METAVERSE IN GAMING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: METAVERSE IN GAMING MARKET DRIVERS

- 10.2.2 NORTH AMERICA: RECESSION IMPACT

- FIGURE 37 NORTH AMERICA: MARKET SNAPSHOT

- TABLE 66 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 67 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 68 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 69 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 70 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY HARDWARE, 2019-2022 (USD MILLION)

- TABLE 71 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 72 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2019-2022 (USD MILLION)

- TABLE 73 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 74 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2019-2022 (USD MILLION)

- TABLE 75 NORTH AMERICA: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2023-2028 (USD MILLION)

- 10.2.3 US

- TABLE 76 US: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 77 US: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.2.4 CANADA

- TABLE 78 CANADA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 79 CANADA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.3 EUROPE

- 10.3.1 EUROPE: METAVERSE IN GAMING MARKET DRIVERS

- 10.3.2 EUROPE: RECESSION IMPACT

- TABLE 80 EUROPE: METAVERSE IN GAMING MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 81 EUROPE: METAVERSE IN GAMING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 82 EUROPE: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 83 EUROPE: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 84 EUROPE: METAVERSE IN GAMING MARKET, BY HARDWARE, 2019-2022 (USD MILLION)

- TABLE 85 EUROPE: METAVERSE IN GAMING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 86 EUROPE: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2019-2022 (USD MILLION)

- TABLE 87 EUROPE: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 88 EUROPE: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2019-2022 (USD MILLION)

- TABLE 89 EUROPE: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2023-2028 (USD MILLION)

- 10.3.3 UK

- TABLE 90 UK: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 91 UK: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.3.4 GERMANY

- TABLE 92 GERMANY: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 93 GERMANY: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.3.5 FRANCE

- TABLE 94 FRANCE: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 95 FRANCE: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.3.6 REST OF EUROPE

- TABLE 96 REST OF EUROPE: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 97 REST OF EUROPE: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: METAVERSE IN GAMING MARKET DRIVERS

- 10.4.2 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 38 ASIA PACIFIC: REGIONAL SNAPSHOT

- TABLE 98 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 99 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 100 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 101 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 102 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY HARDWARE, 2019-2022 (USD MILLION)

- TABLE 103 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 104 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2019-2022 (USD MILLION)

- TABLE 105 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 106 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2019-2022 (USD MILLION)

- TABLE 107 ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2023-2028 (USD MILLION)

- 10.4.3 CHINA

- TABLE 108 CHINA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 109 CHINA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.4.4 JAPAN

- TABLE 110 JAPAN: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 111 JAPAN: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.4.5 SOUTH KOREA

- TABLE 112 SOUTH KOREA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 113 SOUTH KOREA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.4.6 REST OF ASIA PACIFIC

- TABLE 114 REST OF ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 115 REST OF ASIA PACIFIC: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET DRIVERS

- 10.5.2 MIDDLE EAST & AFRICA: RECESSION IMPACT

- TABLE 116 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 117 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 118 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 119 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 120 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY HARDWARE, 2019-2022 (USD MILLION)

- TABLE 121 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 122 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2019-2022 (USD MILLION)

- TABLE 123 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 124 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2019-2022 (USD MILLION)

- TABLE 125 MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2023-2028 (USD MILLION)

- 10.5.3 KINGDOM OF SAUDI ARABIA

- TABLE 126 KINGDOM OF SAUDI ARABIA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 127 KINGDOM OF SAUDI ARABIA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.5.4 REST OF MIDDLE EAST & AFRICA

- TABLE 128 REST OF MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 129 REST OF MIDDLE EAST & AFRICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.6 LATIN AMERICA

- 10.6.1 LATIN AMERICA: METAVERSE IN GAMING MARKET DRIVERS

- 10.6.2 LATIN AMERICA: RECESSION IMPACT

- TABLE 130 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 131 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 132 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 133 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 134 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY HARDWARE, 2019-2022 (USD MILLION)

- TABLE 135 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY HARDWARE, 2023-2028 (USD MILLION)

- TABLE 136 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2019-2022 (USD MILLION)

- TABLE 137 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY SOFTWARE, 2023-2028 (USD MILLION)

- TABLE 138 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2019-2022 (USD MILLION)

- TABLE 139 LATIN AMERICA: METAVERSE IN GAMING MARKET, BY GAME GENRE, 2023-2028 (USD MILLION)

- 10.6.3 BRAZIL

- TABLE 140 BRAZIL: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 141 BRAZIL: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 10.6.4 REST OF LATIN AMERICA

- TABLE 142 REST OF LATIN AMERICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 143 REST OF LATIN AMERICA: METAVERSE IN GAMING MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 MARKET SHARE OF TOP VENDORS

- TABLE 144 INTENSITY OF COMPETITIVE RIVALRY

- FIGURE 39 MARKET SHARE ANALYSIS, 2022

- 11.3 REVENUE ANALYSIS OF TOP FIVE VENDORS

- FIGURE 40 REVENUE ANALYSIS OF TOP FIVE VENDORS, 2018-2022 (USD BILLION)

- 11.4 COMPANY EVALUATION QUADRANT, 2022

- 11.4.1 DEFINITIONS AND METHODOLOGY

- FIGURE 41 KEY PLAYER EVALUATION QUADRANT: CRITERIA WEIGHTAGE

- 11.4.2 STARS

- 11.4.3 EMERGING LEADERS

- 11.4.4 PERVASIVE PLAYERS

- 11.4.5 PARTICIPANTS

- FIGURE 42 COMPANY EVALUATION QUADRANT, 2022

- TABLE 145 COMPANY FOOTPRINT (TOP 10 PLAYERS)

- 11.5 COMPANY EVALUATION QUADRANT FOR STARTUPS/SMES, 2022

- 11.5.1 DEFINITION AND METHODOLOGY

- FIGURE 43 COMPANY EVALUATION QUADRANT FOR STARTUPS/SMES: CRITERIA WEIGHTAGE

- 11.5.2 PROGRESSIVE COMPANIES

- 11.5.3 RESPONSIVE COMPANIES

- 11.5.4 DYNAMIC COMPANIES

- 11.5.5 STARTING BLOCKS

- FIGURE 44 COMPANY EVALUATION QUADRANT FOR STARTUPS/SMES, 2022

- 11.6 COMPETITIVE BENCHMARKING FOR STARTUPS/SMES

- TABLE 146 COMPETITIVE BENCHMARKING FOR STARTUPS/SMES

- TABLE 147 ANALYSIS OF KEY STARTUPS/SMES

- 11.7 COMPANY FINANCIAL METRICS

- FIGURE 45 COMPANY FINANCIAL METRICS, 2022

- 11.8 GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS

- FIGURE 46 METAVERSE IN GAMING: GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS, 2022

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 148 METAVERSE IN GAMING MARKET: PRODUCT LAUNCHES AND ENHANCEMENTS, JANUARY 2020-APRIL 2023

- 11.9.2 DEALS

- TABLE 149 METAVERSE IN GAMING MARKET: DEALS, JANUARY 2020-APRIL 2023

12 COMPANY PROFILES

- 12.1 INTRODUCTION

- 12.2 KEY PLAYERS

- (Business Overview, Products/Solutions/Services offered, Recent Developments, MnM View)**

- 12.2.1 META (FORMERLY FACEBOOK)

- TABLE 150 META: BUSINESS OVERVIEW

- FIGURE 47 META: COMPANY SNAPSHOT

- TABLE 151 META: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 152 META: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 153 META: DEALS

- 12.2.2 ACTIVISION BLIZZARD

- TABLE 154 ACTIVISION BLIZZARD: BUSINESS OVERVIEW

- FIGURE 48 ACTIVISION BLIZZARD: COMPANY SNAPSHOT

- TABLE 155 ACTIVISION BLIZZARD: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 156 ACTIVISION BLIZZARD: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 157 ACTIVISION BLIZZARD: DEALS

- 12.2.3 NETEASE

- TABLE 158 NETEASE: BUSINESS OVERVIEW

- FIGURE 49 NETEASE: COMPANY SNAPSHOT

- TABLE 159 NETEASE: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 160 NETEASE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 161 NETEASE: DEALS

- TABLE 162 NETEASE: OTHERS

- 12.2.4 ELECTRONIC ARTS

- TABLE 163 ELECTRONIC ARTS: BUSINESS OVERVIEW

- FIGURE 50 ELECTRONIC ARTS: COMPANY SNAPSHOT

- TABLE 164 ELECTRONIC ARTS: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 165 ELECTRONIC ARTS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 166 ELECTRONIC ARTS: DEALS

- 12.2.5 TAKE-TWO

- TABLE 167 TAKE-TWO: BUSINESS OVERVIEW

- FIGURE 51 TAKE-TWO: COMPANY SNAPSHOT

- TABLE 168 TAKE-TWO: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 169 TAKE-TWO: DEALS

- 12.2.6 TENCENT

- TABLE 170 TENCENT: BUSINESS OVERVIEW

- FIGURE 52 TENCENT: COMPANY SNAPSHOT

- TABLE 171 TENCENT: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 172 TENCENT: DEALS

- 12.2.7 NEXON

- TABLE 173 NEXON: BUSINESS OVERVIEW

- FIGURE 53 NEXON: COMPANY SNAPSHOT

- TABLE 174 NEXON: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 175 NEXON: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 176 NEXON: DEALS

- 12.2.8 EPIC GAMES

- TABLE 177 EPIC GAMES: BUSINESS OVERVIEW

- TABLE 178 EPIC GAMES: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 179 EPIC GAMES: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 180 EPIC GAMES: DEALS

- 12.2.9 UNITY

- TABLE 181 UNITY: BUSINESS OVERVIEW

- FIGURE 54 UNITY: COMPANY SNAPSHOT

- TABLE 182 UNITY: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- TABLE 183 UNITY: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 184 UNITY: DEALS

- 12.2.10 VALVE

- TABLE 185 VALVE: BUSINESS OVERVIEW

- TABLE 186 VALVE: SOLUTIONS/SERVICES/PLATFORMS OFFERED

- *Details on Business Overview, Products/Solutions/Services offered, Recent Developments, MnM View might not be captured in case of unlisted companies.

- 12.3 OTHER COMPANIES

- 12.3.1 ACCENTURE

- 12.3.2 ADOBE

- 12.3.3 HPE

- 12.3.4 DELOITTE

- 12.3.5 ANSYS

- 12.3.6 AUTODESK INC.

- 12.3.7 INTEL

- 12.3.8 TECH MAHINDRA

- 12.3.9 BYTEDANCE

- 12.3.10 NVIDIA

- 12.3.11 MICROSOFT

- 12.3.12 SAMSUNG

- 12.3.13 GOOGLE

- 12.3.14 SONY

- 12.3.15 HTC

- 12.3.16 SEIKO EPSON

- 12.3.17 APPLE

- 12.3.18 QUALCOMM

- 12.3.19 PANASONIC

- 12.3.20 EON REALITY

- 12.3.21 ROBLOX

- 12.3.22 LENOVO

- 12.3.23 RAZER

- 12.3.24 NEXTECH AR SOLUTIONS

- 12.3.25 ZQGAME

- 12.3.26 TALECRAFT

- 12.3.27 VR CHAT

- 12.3.28 DECENTRALAND

- 12.3.29 SOMNIUM SPACE

- 12.3.30 SANDBOX VR

13 ADJACENT & RELATED MARKETS

- 13.1 INTRODUCTION

- 13.1.1 RELATED MARKETS

- TABLE 187 RELATED MARKETS

- 13.2 LIMITATIONS

- 13.3 METAVERSE MARKET

- 13.3.1 INTRODUCTION

- 13.3.2 METAVERSE MARKET, BY COMPONENT

- TABLE 188 METAVERSE MARKET, BY COMPONENT, 2018-2021 (USD BILLION)

- TABLE 189 METAVERSE MARKET, BY COMPONENT, 2022-2027 (USD BILLION)

- 13.3.3 METAVERSE MARKET, BY VERTICAL

- TABLE 190 METAVERSE MARKET, BY VERTICAL, 2018-2021 (USD BILLION)

- TABLE 191 METAVERSE MARKET, BY VERTICAL, 2022-2027 (USD BILLION)

- 13.3.4 METAVERSE MARKET, BY REGION

- TABLE 192 METAVERSE MARKET, BY REGION, 2018-2021 (USD BILLION)

- TABLE 193 METAVERSE MARKET, BY REGION, 2022-2027 (USD BILLION)

- 13.4 AUGMENTED REALITY MARKET

- 13.4.1 INTRODUCTION

- 13.4.2 AUGMENTED REALITY MARKET, BY DEVICE TYPE

- TABLE 194 AUGMENTED REALITY MARKET, BY DEVICE TYPE, 2021-2026 (USD MILLION)

- 13.4.3 AUGMENTED REALITY MARKET, BY OFFERING

- TABLE 195 AUGMENTED REALITY MARKET, BY OFFERING, 2021-2026 (USD MILLION)

- 13.4.4 AUGMENTED REALITY MARKET, BY REGION

- TABLE 196 AUGMENTED REALITY MARKET, BY REGION, 2021-2026 (USD MILLION)

- 13.5 VIRTUAL REALITY MARKET

- 13.5.1 INTRODUCTION

- 13.5.2 VIRTUAL REALITY MARKET, BY OFFERING

- TABLE 197 VR MARKET, BY OFFERING, 2016-2019 (USD MILLION)

- TABLE 198 VR MARKET, BY OFFERING, 2020-2025 (USD MILLION)

- 13.5.3 VIRTUAL REALITY MARKET, BY REGION

- TABLE 199 VR MARKET, BY REGION, 2016-2019 (USD MILLION)

- TABLE 200 VR MARKET, BY REGION, 2020-2025 (USD MILLION)

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS