|

|

市場調査レポート

商品コード

1499311

ミリ波技術の世界市場:コンポーネント別、周波数帯域幅別、製品別、ライセンスタイプ別、最終用途別、地域別 - 2029年までの予測Millimeter Wave Technology Market by Product (Scanning System, Telecommunication Equipment, Radar and Satellite Communication System, Others), License Type, Component, Frequency Band, End Use and Region - Global Forecast to 2029 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ミリ波技術の世界市場:コンポーネント別、周波数帯域幅別、製品別、ライセンスタイプ別、最終用途別、地域別 - 2029年までの予測 |

|

出版日: 2024年06月06日

発行: MarketsandMarkets

ページ情報: 英文 251 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

ミリ波技術の市場規模は、2024年の30億米ドルから2029年には76億米ドルに成長し、予測期間中のCAGRは20.1%になると予測されています。

ミリ波技術市場の成長を促進する主な要因には、ブロードバンドとモバイルの高速化、ワイヤレスバックホールの普及と5Gネットワークの採用拡大、セキュリティとレーダー用途でのミリ波技術の需要の高さなどがあります。しかし、ミリ波の物理的特性に関連する課題は、今後の市場の課題として作用します。市場参入企業にとっての主な成長機会は、自律走行車の出現と5Gおよびミリ波技術の利用急増です。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント別 | コンポーネント別、周波数帯域幅別、製品別、ライセンスタイプ別、最終用途別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

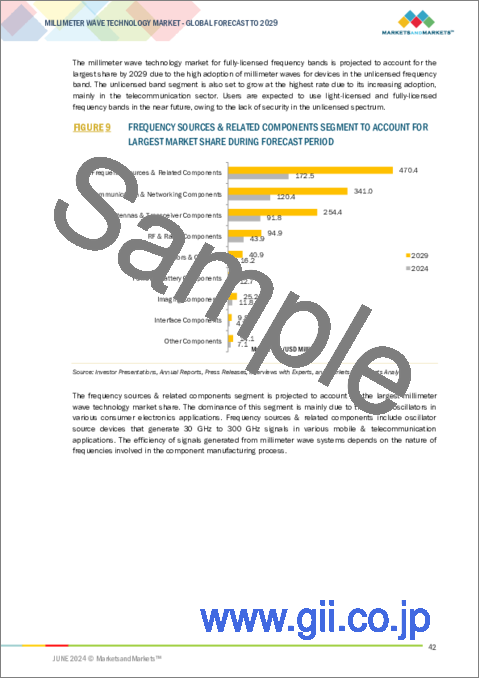

予測期間中、最もシェアが高いミリ波技術市場セグメントは、フルライセンスになると予測されています。8GHz~23GHz、23GHz~38GHz、38GHz~43GHzの周波数帯域が、フルライセンスのミリ波セクションを構成しています。この周波数帯域をアンライセンスおよびライトライセンス周波数帯域と比較すると、この周波数帯域が占める市場規模は小さいです。ポイント・ツー・ポイントの無線通信に使用される周波数帯は、完全にライセンスされています。電気通信業界で予想される発展のひとつは、5G技術に基づく周波数帯であり、これは完全にライセンスされたミリ波周波数帯の一部です。

予測期間中、ミリ波技術市場の通信機器セグメントが最も大きな複合年間成長率を記録すると予測されます。製品別では、ミリ波技術市場は通信機器セグメントによって支配されると予測されています。5Gバックホールへのミリ波コンポーネントの利用が増加していることが、このセグメントの優位性の理由です。さらに、屋内外を問わず、多くのスモールセルおよびマクロセル通信機器がミリ波コンポーネントを使用しています。空港、ショッピングセンター、その他の公共エリアでの人体検査に広く使用されているため、スキャナー・システムが市場の大きな部分を占めると予想されます。衛星・レーダー通信システム市場は、防衛・軍事用途での利用の結果、急速に拡大すると予想されます。

欧州は2023年にミリ波技術のCAGRが他の地域に次いで2番目に高くなると予想されています。5Gの実験とプロジェクトに関しては、欧州が先行しています。これらは現在、世界的に採用されつつあります。改善されたモバイル・ブロードバンド、大型マシン型通信、超高信頼性・低遅延通信などの5Gサービスは、欧州のさまざまなセクターから提供されています。このような商業的な5Gの開始には、新たな周波数帯、新たな機能、インフラストラクチャーに多額の費用を投じるとともに、通信事業者、ネットワークイネーブラー、政府機関の緊密な協力が必要です。欧州委員会はまた、健康と安全への懸念から、空港でのX線後方散乱装置の使用を禁止しました。これらすべての要因が、欧州におけるミリ波技術をベースとしたミリ波スキャナーの需要を後押ししています。

当レポートでは、世界のミリ波技術市場について調査し、コンポーネント別、周波数帯域幅別、製品別、ライセンスタイプ別、最終用途別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- バリューチェーン分析

- エコシステム分析

- 顧客ビジネスに影響を与える動向/混乱

- 価格分析

- 投資と資金調達のシナリオ

- 技術分析

- ケーススタディ分析

- 特許分析

- 貿易分析

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- 2024年~2025年の主な会議とイベント

- 規制状況

第6章 ミリ波技術に関連するソフトウェアとサービス

- ソフトウェア

- サービス

- デザインとコンサルティング

第7章 モバイルおよび無線バックホールにおけるミリ波技術

第8章 ミリ波技術市場(コンポーネント別)

- イントロダクション

- 部品セグメントの市場規模

- アンテナおよびトランシーバー部品

- 周波数源と関連コンポーネント

- 通信およびネットワークコンポーネント

- イメージングコンポーネント

- RFおよび無線コンポーネント

- センサーとコントロール

- インターフェースコンポーネント

- 電源およびバッテリーコンポーネント

- その他

第9章 ミリ波技術市場(周波数帯域幅別)

- イントロダクション

- 24~57GHZ

- 57~95GHZ

- 95~300GHZ

第10章 ミリ波技術市場(製品別)

- イントロダクション

- スキャナーシステム

- レーダーおよび衛星通信システム

- 通信機器

- その他

第11章 ミリ波技術市場(ライセンスタイプ別)

- イントロダクション

- ライトライセンス

- ライセンス無し

- フルライセンス

第12章 ミリ波技術市場(最終用途別)

- イントロダクション

- モバイル・通信

- 消費者・商業

- ヘルスケア

- 工業用

- 自動車・輸送

- 航空宇宙・防衛

- セキュリティ・監視

第13章 地域分析

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- その他の地域

第14章 競合情勢

- 主要参入企業が採用した主要戦略

- 収益分析

- 市場シェア分析、2023年

- 企業価値評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:2023年

- スタートアップ/中小企業評価マトリックス、2023年

- 競合シナリオ

第15章 企業プロファイル

- 主要参入企業

- AXXCSS WIRELESS SOLUTIONS

- NEC CORPORATION

- CERAGON

- L3HARRIS TECHNOLOGIES, INC.

- AVIAT NETWORKS

- SMITHS GROUP PLC

- ERAVANT

- FARRAN

- KEYSIGHT TECHNOLOGIES

- DUCOMMUN INCORPORATED

- MILLIMETER WAVE PRODUCTS INC.

- その他の企業

- VUBIQ NETWORKS, INC.

- ELVA-1

- VERANA NETWORKS

- CABLEFREE

- FASTBACK NETWORKS

- QUINSTAR TECHNOLOGY, INC.

- TREX ENTERPRISES CORPORATION

- NUCTECH

- KYOCERA CORPORATION

- RADWIN

- IGNITENET

- KRATOS DEFENSE & SECURITY SOLUTIONS, INC.

- ANOKIWAVE, INC

- SPACEK LABS INC.

- CAMBIUM NETWORKS, LTD.

第16章 付録

The millimeter wave technology market is projected to grow from USD 3.0 billion in 2024 to USD 7.6 billion by 2029, registering a CAGR of 20.1% during the forecast period. Some of the major factors driving the growth of the millimeter wave technology market include increase in broadband and mobile speeds, proliferation of wireless backhaul and growing adoption of 5G network, and high demand for millimeter wave technology in security and radar applications. However, challenges associated with physical properties of millimeter waves act as a challenge for the market in the future. The major growth opportunities for the market players are the emergence of autonomous vehicles and surging use of 5G and millimeter wave technologies.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Product, License Type, Component, Frequency Band, End Use and Region |

| Regions covered | North America, Europe, APAC, RoW |

"Market for fully licensed expected to have highest share during the forecast period."

Over the course of the forecast period, the millimeter wave technology market segment with the largest share is anticipated to be fully licensed. The frequency ranges between 8 GHz and 23 GHz, 23 GHz and 38 GHz, and 38 GHz and 43 GHz make up the fully licensed millimeter wave section. Comparing this frequency band to unlicensed and lightly licensed frequency bands, the market sector it occupies is smaller. The frequency bands utilized in point-to-point wireless communications are fully licensed. One of the anticipated developments in the telecom industry is the frequency spectrum based on 5G technology, which is a portion of the fully licensed millimeter wave spectrum.

"Telecommunication equipment segment expected to register the highest CAGR during the forecast period."

During the forecast period, the communications equipment segment of the millimeter wave technology market is anticipated to have the greatest compound annual growth rate. By product, the millimeter wave technology market is anticipated to be dominated by the telecommunication equipment segment. The increased utilization of millimeter wave components for 5G backhaul is the reason for this segment's supremacy. Additionally, a lot of small-cell and macrocell telecommunications equipment, both indoors and outdoors, uses millimeter wave components. Because they are widely used for people screening in airports, shopping centers, and other public areas, scanner systems are anticipated to hold a sizeable portion of the market. The market for satellite and radar communication systems is expected to expand rapidly as a result of its use in defense and military applications.

"Europe is expected to have second highest CAGR among other regions in forecast period."

Europe is expected to have second second-highest CAGR for millimeter wave technology in 2023. When it comes to 5G experiments and projects, Europe has led the way. These are currently being adopted globally. 5G services, such as improved mobile broadband, large machine-type communications, and ultra-reliable and low-latency communications, are being offered by a variety of sectors around Europe. Such commercial 5G launches necessitate significant expenditures for new spectrum, new capabilities, and infrastructure, as well as tight cooperation between telecom operators, network enablers, and government agencies. The European Commission also banned using X-ray backscatter machines at airports due to health and safety concerns. All these factors fuel the demand for millimeter wave scanners based on millimeter wave technology in Europe.

In determining and verifying the market size for several segments and subsegments gathered through extensive secondary research, primary interviews have been conducted with key industry experts in the millimeter wave technology market.

The break-up of primary participants for the report has been shown below:

- By company type: Tier 1 - 38%, Tier 2 - 28%, and Tier 3 - 34%

- By designation: C-Level Executives - 40%, Managers - 30%, and Others - 30%

- By region: North America - 35%, Europe - 20%, Asia Pacific - 35%, and RoW - 10%

The report profiles key players in the millimeter wave technologymarket with their respective market ranking analyses. Prominent players profiled in this report include Axxcss Wireless Solutions (US), NEC Corporation (Japan), Ceragon (Israel), L3Harris Technologies, Inc. (US), Aviat Networks (US), Smiths Group plc (UK), Eravant (US), Farran (Ireland), Keysight Technologies (US), Ducommun Incorporated (US), and Millimeter Wave Product, Inc, (US), among others.

Research Coverage

This research report categorizes the millimeter wave technology market based on technology, end-user industry, and region. The report describes the major drivers, restraints, challenges, and opportunities pertaining to the millimeter wave technology market and forecasts the same till 2029. The report also consists of leadership mapping and analysis of companies in the millimeter wave technology ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall millimeter wave technology market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (increase in broadband and mobile speeds, proliferation of Wireless Backhaul and growing adoption of 5G network, high demand for millimeter wave technology in security and radar applications, and growing need for faster data transmission), restraints (low penetration power and adverse impact on environment), opportunities (surging use of 5G and millimeter wave technologies, emergence of new applications in aerospace & defense industry, emergence of autonomous vehicles, and rising use of V-band millimeter waves for last-mile connectivity), and challenges (challenges associated with physical properties of millimeter waves) influencing the growth of the millimeter wave technology market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the millimeter wave technologymarket

- Market Development: Comprehensive information about lucrative markets - the report analyses the millimeter wave technology market across varied regions

- Market Diversification: Exhaustive information about new products & technologies, untapped geographies, recent developments, and investments in the millimeter wave technology market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product/service offerings of leading players like Axxcss Wireless Solutions (US), NEC Corporation (Japan), Ceragon (Israel), L3Harris Technologies, Inc. (US), Aviat Networks (US), Smiths Group plc (UK), Eravant (US), Farran (Ireland), Keysight Technologies (US), Ducommun Incorporated (US), and Millimeter Wave Product, Inc, (US), among others in the millimeter wave technology market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 MILLIMETER WAVE TECHNOLOGY: MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 UNITS CONSIDERED

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.8.1 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 MILLIMETER WAVE TECHNOLOGY MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews with experts

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Breakdown of primary interviews

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.3.1 Key industry insights

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.2.1.1 Approach for capturing market size from bottom-up analysis

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach for capturing market share by top-down analysis

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.3 MARKET BREAKDOWN & DATA TRIANGULATION

- FIGURE 5 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.4.1 IMPACT OF RECESSION

- 2.5 LIMITATIONS

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 6 57-95 GHZ FREQUENCY BAND TO ACCOUNT FOR HIGHEST SHARE IN 2024

- FIGURE 7 TELECOMMUNICATION EQUIPMENT PRODUCT SEGMENT TO LEAD MILLIMETER WAVE TECHNOLOGY MARKET DURING FORECAST PERIOD

- FIGURE 8 FULLY LICENSED FREQUENCY BANDS SEGMENT TO ACCOUNT FOR LARGEST SHARE OF MILLIMETER WAVE TECHNOLOGY MARKET

- FIGURE 9 FREQUENCY SOURCES & RELATED COMPONENTS SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 10 MOBILE & TELECOMMUNICATION END USE TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 11 NORTH AMERICA RECORDED HIGHEST MARKET SHARE IN 2023

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MILLIMETER WAVE TECHNOLOGY MARKET

- FIGURE 12 INCREASING USE OF MILLIMETER WAVE TECHNOLOGY IN VARIOUS INDUSTRIES AND SECTORS TO DRIVE MARKET

- 4.2 MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT

- FIGURE 13 TELECOMMUNICATION EQUIPMENT PRODUCT TO ACCOUNT FOR HIGHEST SHARE DURING FORECAST PERIOD

- 4.3 MILLIMETER WAVE TECHNOLOGY MARKET IN NORTH AMERICA, BY END USE AND COUNTRY

- FIGURE 14 US HELD LARGEST SHARE IN NORTH AMERICA MARKET IN 2023

- 4.4 MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY

- FIGURE 15 CHINA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 16 MILLIMETER WAVE TECHNOLOGY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- FIGURE 17 MILLIMETER WAVE TECHNOLOGY MARKET: IMPACT ANALYSIS OF DRIVERS

- 5.2.1.1 Increase in internet speeds boosting consumption of high-bandwidth content

- 5.2.1.2 Proliferation of wireless backhaul and growing adoption of 5G network

- FIGURE 18 GLOBAL MOBILE DATA TRAFFIC (EXABYTE PER MONTH)

- 5.2.1.3 High demand in security and radar applications

- TABLE 1 MILLIMETER-WAVE FREQUENCIES AND APPLICATIONS

- 5.2.1.4 Growing need for faster data transmission

- TABLE 2 DEVELOPMENTS IN 60 GHZ FWA SOLUTIONS

- 5.2.2 RESTRAINTS

- FIGURE 19 MILLIMETER WAVE TECHNOLOGY MARKET: IMPACT ANALYSIS OF RESTRAINTS

- 5.2.2.1 Low penetration power and adverse impact on environment

- 5.2.3 OPPORTUNITIES

- FIGURE 20 MILLIMETER WAVE TECHNOLOGY MARKET: IMPACT ANALYSIS OF OPPORTUNITIES

- 5.2.3.1 Surging use of 5G and millimeter wave technologies

- FIGURE 21 GLOBAL NUMBER OF 5G SUBSCRIBERS, 2020-2029 (BILLION)

- 5.2.3.2 Emergence of new applications in aerospace & defense industry

- 5.2.3.3 Emergence of autonomous vehicles

- 5.2.3.4 Rising use of V-band millimeter waves for last-mile connectivity

- 5.2.4 CHALLENGES

- FIGURE 22 MILLIMETER WAVE TECHNOLOGY MARKET: IMPACT ANALYSIS OF CHALLENGES

- 5.2.4.1 Challenges associated with physical properties of millimeter waves

- TABLE 3 CHALLENGES ASSOCIATED WITH PHYSICAL PARAMETERS OF MILLIMETER WAVES

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 23 MILLIMETER WAVE TECHNOLOGY MARKET: VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- FIGURE 24 KEY PARTICIPANTS IN MILLIMETER WAVE TECHNOLOGY MARKET: ECOSYSTEM

- TABLE 4 MILLIMETER WAVE TECHNOLOGY MARKET: ECOSYSTEM ANALYSIS

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 25 MILLIMETER WAVE TECHNOLOGY MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE, BY PRODUCT TYPE

- TABLE 5 AVERAGE SELLING PRICE OF VARIOUS PRODUCT TYPES

- FIGURE 26 AVERAGE SELLING PRICE TRENDS FOR MILLIMETER WAVE TECHNOLOGY, BY PRODUCT, 2020-2023

- FIGURE 27 AVERAGE SELLING PRICE OFFERED BY KEY PLAYERS, BY PRODUCT

- TABLE 6 AVERAGE SELLING PRICE OF PRODUCTS OFFERED BY THREE KEY PLAYERS (USD)

- TABLE 7 KEY PROVIDERS OF MILLIMETER-WAVE TELECOMMUNICATION PRODUCTS

- TABLE 8 KEY PROVIDERS OF MILLIMETER WAVE SCANNING PRODUCTS

- TABLE 9 KEY PROVIDERS OF MILLIMETER WAVE RADAR & SATELLITE PRODUCTS

- 5.6.2 AVERAGE SELLING PRICE TREND, BY REGION

- FIGURE 28 AVERAGE SELLING PRICE TREND OF SCANNER SYSTEMS, BY REGION

- 5.7 INVESTMENT AND FUNDING SCENARIO

- FIGURE 29 FUNDS AUTHORIZED BY VARIOUS MILLIMETRE WAVE TECHNOLOGY KEY PLAYERS

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Artificial intelligence and machine learning for beamforming

- 5.8.1.2 Monolithic microwave integrated circuits

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Gallium nitride (GaN) transistors

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Terahertz waves

- TABLE 10 MILLIMETER WAVE TECHNOLOGY VS. TERAHERTZ WAVE TECHNOLOGY

- 5.8.1 KEY TECHNOLOGIES

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 TELECOMMUNICATION

- 5.9.1.1 Skycom1 relies on HaulPass V60s V-Band Wireless links

- 5.9.2 IMAGING

- 5.9.2.1 First-to-market radio-wave breast imaging system achieved with network analyzer

- 5.9.3 AUTOMOTIVE & TRANSPORTATION

- 5.9.3.1 Proxim Solutions enabled seamless surveillance along Tenerife Tram Line in Spain

- 5.9.4 INDUSTRIAL

- 5.9.4.1 Kingston Technology deployed HaulPass V60s wireless broadband for disaster recovery and campus network expansion

- 5.9.5 CONSUMER & COMMERCIAL

- 5.9.5.1 City of Mission Viejo deployed cost-effective broadband wireless gigabit ethernet link at Potocki Conference Center

- 5.9.1 TELECOMMUNICATION

- 5.10 PATENT ANALYSIS

- FIGURE 30 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS IN LAST 10 YEARS

- TABLE 11 TOP 20 PATENT OWNERS IN LAST 10 YEARS

- 5.10.1 LIST OF MAJOR PATENTS

- TABLE 12 MILLIMETER WAVE TECHNOLOGY MARKET: LIST OF MAJOR PATENTS

- 5.11 TRADE ANALYSIS

- FIGURE 31 IMPORT DATA FOR HS CODE 851761, BY COUNTRY, 2019-2023 (USD THOUSAND)

- FIGURE 32 EXPORT DATA FOR HS CODE 851761, BY COUNTRY, 2019-2023 (USD THOUSAND)

- 5.12 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 33 MILLIMETER WAVE TECHNOLOGY MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 13 MILLIMETER WAVE TECHNOLOGY MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.12.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.12.2 THREAT OF SUBSTITUTES

- 5.12.3 BARGAINING POWER OF BUYERS

- 5.12.4 BARGAINING POWER OF SUPPLIERS

- 5.12.5 THREAT OF NEW ENTRANTS

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 34 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USES

- TABLE 14 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USES (%)

- 5.13.2 BUYING CRITERIA

- FIGURE 35 KEY BUYING CRITERIA FOR END USERS

- TABLE 15 KEY BUYING CRITERIA FOR END USE

- 5.14 KEY CONFERENCES AND EVENTS, 2024-2025

- TABLE 16 MILLIMETER WAVE TECHNOLOGY MARKET: KEY CONFERENCES AND EVENTS

- 5.15 REGULATORY LANDSCAPE

- 5.15.1 REGULATORY STANDARDS

- 5.15.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6 SOFTWARE AND SERVICES ASSOCIATED WITH MILLIMETER WAVE TECHNOLOGY

- 6.1 SOFTWARE

- 6.2 SERVICES

- 6.3 DESIGNING AND CONSULTING

- 6.3.1 INTEGRATION & DEPLOYMENT

- 6.3.2 SUPPORT & MAINTENANCE

7 MILLIMETER WAVE TECHNOLOGY IN MOBILE AND WIRELESS BACKHAUL

- 7.1 MOBILE AND WIRELESS BACKHAUL

8 MILLIMETER WAVE TECHNOLOGY MARKET, BY COMPONENT

- 8.1 INTRODUCTION

- 8.2 MARKET SIZE ESTIMATION FOR COMPONENT SEGMENTS

- FIGURE 36 MILLIMETER WAVE TECHNOLOGY MARKET, BY COMPONENT

- FIGURE 37 COMMUNICATION & NETWORKING COMPONENTS SEGMENT TO GROW AT HIGHEST RATE DURING FORECAST PERIOD

- TABLE 21 MILLIMETER WAVE TECHNOLOGY MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 22 MILLIMETER WAVE TECHNOLOGY MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- 8.3 ANTENNA & TRANSCEIVER COMPONENTS

- 8.3.1 ADVANCEMENTS IN PRECISION MANUFACTURING AND MINIATURIZATION TO DRIVE MARKET

- TABLE 23 MAJOR PROVIDERS OF MILLIMETER WAVE ANTENNAS

- 8.4 FREQUENCY SOURCES & RELATED COMPONENTS

- 8.4.1 INCREASING ADOPTION BY COMMUNICATION PROVIDERS TO DRIVE MARKET

- 8.5 COMMUNICATION & NETWORKING COMPONENTS

- 8.5.1 COMMUNICATION & NETWORKING COMPONENTS TO PLAY VITAL ROLE IN TELECOMMUNICATION DURING FORECAST PERIOD

- 8.6 IMAGING COMPONENTS

- 8.6.1 INCREASING APPLICATIONS IN AUTOMOTIVE, MEDICAL, AND INDUSTRIAL INSPECTION TO DRIVE MARKET

- 8.7 RF & RADIO COMPONENTS

- 8.7.1 PRESENCE OF KEY COMPANIES OFFERING RF & RADIO COMPONENTS TO DRIVE MARKET

- 8.8 SENSORS & CONTROLS

- 8.8.1 GROWING ADOPTION IN VARIOUS APPLICATIONS TO DRIVE MARKET

- 8.9 INTERFACE COMPONENTS

- 8.9.1 INCREASING DEVELOPMENTS BY MAJOR PLAYERS TO DRIVE MARKET

- 8.10 POWER & BATTERY COMPONENTS

- 8.10.1 MILLIMETER WAVE TECHNOLOGY TO PLAY IMPORTANT ROLE IN IMPLEMENTING WIRELESS POWER TRANSFER TECHNOLOGY

- 8.11 OTHER COMPONENTS

9 MILLIMETER WAVE TECHNOLOGY MARKET, BY FREQUENCY BAND

- 9.1 INTRODUCTION

- FIGURE 38 MILLIMETER WAVE TECHNOLOGY MARKET, BY FREQUENCY BAND

- FIGURE 39 57-95 GHZ FREQUENCY BAND TO REGISTER HIGHEST CAGR IN MILLIMETER WAVE TECHNOLOGY MARKET DURING FORECAST PERIOD

- TABLE 24 MILLIMETER WAVE TECHNOLOGY MARKET, BY FREQUENCY BAND, 2020-2023 (USD MILLION)

- TABLE 25 MILLIMETER WAVE TECHNOLOGY MARKET, BY FREQUENCY BAND, 2024-2029 (USD MILLION)

- 9.2 24-57 GHZ

- 9.2.1 INCREASING USE OF MILLIMETER WAVES WITH FREQUENCY BANDS BETWEEN 24 AND 57 GHZ IN TELECOMMUNICATIONS INDUSTRY TO DRIVE MARKET

- 9.3 57-95 GHZ

- 9.3.1 INCREASING APPLICATIONS OF MILLIMETER WAVES WITH FREQUENCY BANDS BETWEEN 57 AND 95 GHZ IN AUTOMOTIVE, HEALTHCARE, AND TELECOMMUNICATIONS INDUSTRIES TO DRIVE MARKET

- TABLE 26 CHARACTERISTICS OF V-BAND AND E-BAND

- 9.3.2 V-BAND

- 9.3.3 E-BAND

- 9.4 95-300 GHZ

- 9.4.1 RISING USE OF TELECOMMUNICATION IN AEROSPACE & DEFENSE INDUSTRY TO DRIVE MARKET

10 MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT

- 10.1 INTRODUCTION

- FIGURE 40 MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT

- FIGURE 41 TELECOMMUNICATION EQUIPMENT PRODUCT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 27 MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2020-2023 (USD MILLION)

- TABLE 28 MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 29 MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2020-2023 (THOUSAND UNITS)

- TABLE 30 MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2024-2029 (THOUSAND UNITS)

- 10.2 SCANNER SYSTEMS

- TABLE 31 SCANNER SYSTEMS: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 32 SCANNER SYSTEMS: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 33 SCANNER SYSTEMS: MILLIMETER WAVE TECHNOLOGY MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 34 SCANNER SYSTEMS: MILLIMETER WAVE TECHNOLOGY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.2.1 ACTIVE SCANNERS

- 10.2.1.1 Growing deployment for various applications, such as government screening systems to drive market

- 10.2.2 PASSIVE SCANNERS

- 10.2.2.1 Rising trend of vulnerability scanning to drive market

- 10.3 RADAR & SATELLITE COMMUNICATION SYSTEMS

- TABLE 35 RADAR & SATELLITE COMMUNICATION SYSTEMS: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 36 RADAR & SATELLITE COMMUNICATION SYSTEMS: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 37 RADAR & SATELLITE COMMUNICATION SYSTEMS: MILLIMETER WAVE TECHNOLOGY MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 38 RADAR & SATELLITE COMMUNICATION SYSTEMS: MILLIMETER WAVE TECHNOLOGY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.3.1 PERIMETER SURVEILLANCE RADAR SYSTEMS (PSRS)

- 10.3.1.1 Rising demand for critical and highly secure areas to drive market

- 10.3.2 APPLICATION-SPECIFIC RADAR SYSTEMS

- 10.3.2.1 Increasing use in automobile collision warning systems, wide area traffic monitoring and control systems to drive market

- 10.3.3 SATELLITE COMMUNICATION SYSTEMS

- 10.3.3.1 Increasing use of V- and E-bands to drive market

- 10.4 TELECOMMUNICATION EQUIPMENT

- 10.4.1 MOBILE BACKHAUL EQUIPMENT

- 10.4.1.1 Growing adoption by government agencies and academic institutions to drive market

- 10.4.2 SMALL-CELL EQUIPMENT

- 10.4.2.1 Increasing uses of unlicensed 60 GHz frequency band to drive market

- 10.4.3 MACROCELL EQUIPMENT

- 10.4.3.1 Use in wide outdoor coverage (3 to 5 km) to drive segment (1.8-3 miles)

- TABLE 39 TELECOMMUNICATION EQUIPMENT: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 40 TELECOMMUNICATION EQUIPMENT: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 41 TELECOMMUNICATION EQUIPMENT: MILLIMETER WAVE TECHNOLOGY MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 42 TELECOMMUNICATION EQUIPMENT: MILLIMETER WAVE TECHNOLOGY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.4.1 MOBILE BACKHAUL EQUIPMENT

- 10.5 OTHER PRODUCTS

- TABLE 43 OTHER PRODUCTS: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 44 OTHER PRODUCTS: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

11 MILLIMETER WAVE TECHNOLOGY MARKET, BY LICENSE TYPE

- 11.1 INTRODUCTION

- FIGURE 42 MILLIMETER WAVE TECHNOLOGY MARKET, BY LICENSE TYPE

- FIGURE 43 UNLICENSED SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 45 MILLIMETER WAVE TECHNOLOGY MARKET, BY LICENSE TYPE, 2020-2023 (USD MILLION)

- TABLE 46 MILLIMETER WAVE TECHNOLOGY MARKET, BY LICENSE TYPE, 2024-2029 (USD MILLION)

- 11.2 LIGHT LICENSED

- 11.2.1 POINT-TO-POINT WIRELESS COMMUNICATION TO DRIVE MARKET

- 11.3 UNLICENSED

- 11.3.1 IMMUNITY TO WIND AND SUNLIGHT TO DRIVE MARKET

- 11.4 FULLY LICENSED

- 11.4.1 WIDE ADOPTION IN TELECOMMUNICATIONS INDUSTRY TO DRIVE MARKET

12 MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE

- 12.1 INTRODUCTION

- FIGURE 44 MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE INDUSTRY

- FIGURE 45 MOBILE & TELECOMMUNICATION END USE TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 47 MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 48 MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 12.2 MOBILE & TELECOMMUNICATION

- 12.2.1 ADVANCEMENTS IN 5G TECHNOLOGY TO DRIVE MARKET

- TABLE 49 MOBILE & TELECOMMUNICATION: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 50 MOBILE & TELECOMMUNICATION: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 12.3 CONSUMER & COMMERCIAL

- 12.3.1 INCREASING DEMAND IN WIRELESS SENSORS AND WIRELESS SECURITY APPLICATIONS TO DRIVE MARKET

- TABLE 51 CONSUMER & COMMERCIAL: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 52 CONSUMER & COMMERCIAL: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 12.4 HEALTHCARE

- 12.4.1 RISING USE IN MEDICAL SCANNING AND IMAGING APPLICATIONS TO DRIVE MARKET

- TABLE 53 HEALTHCARE: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 54 HEALTHCARE: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 12.5 INDUSTRIAL

- 12.5.1 GROWING ADOPTION OF MILLIMETER WAVE TECHNOLOGY FOR LEVEL MEASUREMENTS TO DRIVE MARKET

- TABLE 55 INDUSTRIAL: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 56 INDUSTRIAL: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 12.6 AUTOMOTIVE & TRANSPORTATION

- 12.6.1 INCREASING INCORPORATION OF MILLIMETER WAVE RADARS INTO AUTONOMOUS VEHICLES TO DRIVE MARKET

- TABLE 57 AUTOMOTIVE & TRANSPORTATION: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 58 AUTOMOTIVE & TRANSPORTATION: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 12.7 AEROSPACE & DEFENSE

- 12.7.1 RISING USE OF MILLIMETER WAVE TECHNOLOGY IN AIRCRAFT AND SATELLITES TO DRIVE MARKET

- TABLE 59 AEROSPACE & DEFENSE: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 60 AEROSPACE & DEFENSE: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 12.8 SECURITY & SURVEILLANCE

- 12.8.1 RISING ADOPTION OF MILLIMETER WAVE-BASED IMAGING PRODUCTS AT AIRPORTS AND CONCERTS TO DRIVE MARKET

- TABLE 61 SECURITY & SURVEILLANCE: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 62 SECURITY & SURVEILLANCE: MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

13 REGIONAL ANALYSIS

- 13.1 INTRODUCTION

- FIGURE 46 MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION/COUNTRY

- FIGURE 47 ASIA PACIFIC TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 63 MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 64 MILLIMETER WAVE TECHNOLOGY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 13.2 NORTH AMERICA

- FIGURE 48 NORTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET SNAPSHOT

- TABLE 65 NORTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 66 NORTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 67 NORTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2020-2023 (USD MILLION)

- TABLE 68 NORTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 69 NORTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 70 NORTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.2.1 US

- 13.2.1.1 Large presence of key companies offering millimeter wave technology to drive market

- TABLE 71 US: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 72 US: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.2.2 CANADA

- 13.2.2.1 Rise in number of 5G rollouts to drive market

- TABLE 73 CANADA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 74 CANADA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.2.3 MEXICO

- 13.2.3.1 Expanding telecommunications industry with rising adoption of 5G technology to drive market

- TABLE 75 MEXICO: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 76 MEXICO: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.2.4 IMPACT OF RECESSION ON MILLIMETER WAVE TECHNOLOGY MARKET IN NORTH AMERICA

- 13.3 EUROPE

- FIGURE 49 EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET SNAPSHOT

- TABLE 77 EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 78 EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 79 EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2020-2023 (USD MILLION)

- TABLE 80 EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 81 EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 82 EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.3.1 UK

- 13.3.1.1 Increased government-led investments in telecommunications industry to drive market

- TABLE 83 UK: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 84 UK: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.3.2 GERMANY

- 13.3.2.1 Increased deployment of millimeter wave technology in various industries to drive market

- TABLE 85 GERMANY: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 86 GERMANY: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.3.3 FRANCE

- 13.3.3.1 Technological shift from 4G to 5G to drive market

- TABLE 87 FRANCE: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 88 FRANCE: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.3.4 ITALY

- 13.3.4.1 Increasing adoption in automotive sector to drive market

- TABLE 89 ITALY: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 90 ITALY: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.3.5 REST OF EUROPE

- TABLE 91 REST OF EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 92 REST OF EUROPE: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.3.6 IMPACT OF RECESSION ON MILLIMETER WAVE TECHNOLOGY MARKET IN EUROPE

- 13.4 ASIA PACIFIC

- FIGURE 50 ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET SNAPSHOT

- TABLE 93 ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 94 ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 95 ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2020-2023 (USD MILLION)

- TABLE 96 ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 97 ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 98 ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.4.1 CHINA

- 13.4.1.1 Large customer base of telecommunication services to drive market

- TABLE 99 CHINA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 100 CHINA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.4.2 JAPAN

- 13.4.2.1 Expanding mobile & telecommunications and automotive industries to drive market

- TABLE 101 JAPAN: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 102 JAPAN: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.4.3 SOUTH KOREA

- 13.4.3.1 Presence of strong telecommunication infrastructure and easy availability of 5G mobile phones to drive market

- TABLE 103 SOUTH KOREA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 104 SOUTH KOREA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.4.4 INDIA

- 13.4.4.1 Increasing investments in 5G infrastructure and rise in number of 5G mobile phone manufacturers to drive market

- TABLE 105 INDIA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 106 INDIA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.4.5 REST OF ASIA PACIFIC

- TABLE 107 REST OF ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 108 REST OF ASIA PACIFIC: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.4.6 IMPACT OF RECESSION ON MILLIMETER WAVE TECHNOLOGY MARKET IN ASIA PACIFIC

- 13.5 ROW

- TABLE 109 ROW: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 110 ROW: MILLIMETER WAVE TECHNOLOGY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 111 ROW: MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2020-2023 (USD MILLION)

- TABLE 112 ROW: MILLIMETER WAVE TECHNOLOGY MARKET, BY PRODUCT, 2024-2029 (USD MILLION)

- TABLE 113 ROW: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 114 ROW: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.5.1 SOUTH AMERICA

- 13.5.1.1 Rising 5G deployments and partnerships of local players with global players to drive market

- TABLE 115 SOUTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 116 SOUTH AMERICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.5.2 GCC COUNTRIES

- 13.5.2.1 Increasing implementation for smart grids and smart city projects to drive market

- TABLE 117 GCC COUNTRIES: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 118 GCC COUNTRIES: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- TABLE 119 REST OF MIDDLE EAST & AFRICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 120 REST OF MIDDLE EAST & AFRICA: MILLIMETER WAVE TECHNOLOGY MARKET, BY END USE, 2024-2029 (USD MILLION)

14 COMPETITIVE LANDSCAPE

- 14.1 KEY STRATEGIES ADOPTED BY MAJOR PLAYERS

- TABLE 121 MILLIMETER WAVE TECHNOLOGY MARKET: OVERVIEW OF STRATEGIES DEPLOYED BY KEY PLAYERS

- 14.2 REVENUE ANALYSIS

- FIGURE 51 REVENUE ANALYSIS OF KEY PLAYERS, 2019-2023

- 14.3 MARKET SHARE ANALYSIS, 2023

- FIGURE 52 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2023

- TABLE 122 MILLIMETER WAVE TECHNOLOGY MARKET SHARE ANALYSIS, 2023

- 14.3.1 MILLIMETER WAVE TECHNOLOGY MARKET: RANKING ANALYSIS, 2023

- FIGURE 53 RANKING OF TOP FIVE PLAYERS IN MILLIMETER WAVE TECHNOLOGY MARKET, 2023

- 14.4 COMPANY VALUATION AND FINANCIAL METRICS

- FIGURE 54 COMPANY VALUATION (USD BILLION), 2023

- FIGURE 55 FINANCIAL METRICS (ENTERPRISE VALUE/EBITDA), 2023

- 14.5 BRAND/PRODUCT COMPARISON

- FIGURE 56 MILLIMETER WAVE TECHNOLOGY MARKET: BRAND/PRODUCT COMPARISON

- 14.6 COMPANY EVALUATION MATRIX, 2023

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- FIGURE 57 MILLIMETER WAVE TECHNOLOGY MARKET: COMPANY EVALUATION MATRIX, 2023

- 14.6.5 COMPANY FOOTPRINT, KEY PLAYERS, 2023

- 14.6.5.1 Company footprint

- FIGURE 58 MILLIMETER WAVE TECHNOLOGY MARKET: COMPANY FOOTPRINT

- 14.6.5.2 Product footprint

- TABLE 123 MILLIMETER WAVE TECHNOLOGY MARKET: PRODUCT FOOTPRINT

- 14.6.5.3 Component footprint

- TABLE 124 MILLIMETER WAVE TECHNOLOGY MARKET: COMPONENT FOOTPRINT

- 14.6.5.4 End use footprint

- TABLE 125 MILLIMETER WAVE TECHNOLOGY MARKET: END USE FOOTPRINT

- 14.6.5.5 Region footprint

- TABLE 126 MILLIMETER WAVE TECHNOLOGY MARKET: REGION FOOTPRINT

- 14.7 STARTUPS/SMALL AND MEDIUM-SIZED ENTERPRISES EVALUATION (SMES) EVALUATION MATRIX, 2023

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- FIGURE 59 MILLIMETER WAVE TECHNOLOGY MARKET: STARTUPS/SMES EVALUATION MATRIX, 2023

- 14.7.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2023

- TABLE 127 MILLIMETER WAVE TECHNOLOGY MARKET: LIST OF KEY STARTUPS/SMES

- TABLE 128 MILLIMETER WAVE TECHNOLOGY MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 14.8 COMPETITIVE SCENARIO

- 14.8.1 PRODUCT LAUNCHES

- TABLE 129 MILLIMETER WAVE TECHNOLOGY MARKET: PRODUCT LAUNCHES, JANUARY 2020-FEBRUARY 2024

- 14.8.2 DEALS

- TABLE 130 MILLIMETER WAVE TECHNOLOGY MARKET: DEALS, JANUARY 2020-FEBRUARY 2024

- 14.8.3 OTHER DEVELOPMENTS

- TABLE 131 MILLIMETER WAVE TECHNOLOGY MARKET: OTHER DEVELOPMENTS, JANUARY 2020-FEBRUARY 2024

15 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 15.1 KEY PLAYERS

- 15.1.1 AXXCSS WIRELESS SOLUTIONS

- TABLE 132 AXXCSS WIRELESS SOLUTIONS: COMPANY OVERVIEW

- TABLE 133 AXXCSS WIRELESS SOLUTIONS: PRODUCTS OFFERED

- TABLE 134 AXXCSS WIRELESS SOLUTIONS: PRODUCTS LAUNCHES

- TABLE 135 AXXCSS WIRELESS SOLUTIONS: DEALS

- 15.1.2 NEC CORPORATION

- 15.1.2.1 Business overview

- TABLE 136 NEC CORPORATION: COMPANY OVERVIEW

- FIGURE 60 NEC CORPORATION: COMPANY SNAPSHOT

- TABLE 137 NEC CORPORATION: PRODUCTS OFFERED

- TABLE 138 NEC CORPORATION: PRODUCTS LAUNCHES

- TABLE 139 NEC CORPORATION: DEALS

- 15.1.3 CERAGON

- TABLE 140 CERAGON: COMPANY OVERVIEW

- FIGURE 61 CERAGON: COMPANY SNAPSHOT

- TABLE 141 CERAGON: PRODUCTS/SOLUTIONS OFFERED

- TABLE 142 CERAGON: PRODUCT LAUNCHES

- TABLE 143 CERAGON: DEALS

- 15.1.4 L3HARRIS TECHNOLOGIES, INC.

- TABLE 144 L3HARRIS TECHNOLOGIES, INC.: COMPANY OVERVIEW

- FIGURE 62 L3HARRIS TECHNOLOGIES, INC.: COMPANY SNAPSHOT

- TABLE 145 L3HARRIS TECHNOLOGIES, INC.: PRODUCTS OFFERED

- TABLE 146 L3HARRIS TECHNOLOGIES, INC.: DEALS

- 15.1.5 AVIAT NETWORKS

- TABLE 147 AVIAT NETWORKS: COMPANY OVERVIEW

- FIGURE 63 AVIAT NETWORKS: COMPANY SNAPSHOT

- TABLE 148 AVIAT NETWORKS: PRODUCTS OFFERED

- TABLE 149 AVIAT NETWORKS: DEALS

- 15.1.6 SMITHS GROUP PLC

- TABLE 150 SMITHS GROUP PLC: COMPANY OVERVIEW

- FIGURE 64 SMITHS GROUP PLC: COMPANY SNAPSHOT

- TABLE 151 SMITHS GROUP PLC: PRODUCTS OFFERED

- TABLE 152 SMITHS GROUP PLC: PRODUCT LAUNCHES

- TABLE 153 SMITHS GROUP PLC: OTHER DEVELOPMENTS

- 15.1.7 ERAVANT

- TABLE 154 ERAVANT: COMPANY OVERVIEW

- TABLE 155 ERAVANT: PRODUCTS OFFERED

- TABLE 156 ERAVANT: PRODUCT LAUNCHES

- TABLE 157 ERAVANT: DEALS

- 15.1.8 FARRAN

- TABLE 158 FARRAN: COMPANY OVERVIEW

- TABLE 159 FARRAN: PRODUCTS OFFERED

- 15.1.9 KEYSIGHT TECHNOLOGIES

- TABLE 160 KEYSIGHT TECHNOLOGIES: COMPANY OVERVIEW

- FIGURE 65 KEYSIGHT TECHNOLOGIES: COMPANY SNAPSHOT

- TABLE 161 KEYSIGHT TECHNOLOGIES: PRODUCTS OFFERED

- TABLE 162 KEYSIGHT TECHNOLOGIES: PRODUCT LAUNCHES

- TABLE 163 KEYSIGHT TECHNOLOGIES: DEALS

- 15.1.10 DUCOMMUN INCORPORATED

- TABLE 164 DUCOMMUN INCORPORATED: COMPANY OVERVIEW

- FIGURE 66 DUCOMMUN INCORPORATED: COMPANY SNAPSHOT

- TABLE 165 DUCOMMUN INCORPORATED: PRODUCTS OFFERED

- 15.1.11 MILLIMETER WAVE PRODUCTS INC.

- TABLE 166 MILLIMETER WAVE PRODUCTS: COMPANY OVERVIEW

- TABLE 167 MILLIMETER WAVE PRODUCTS: PRODUCTS OFFERED

- 15.2 OTHER PLAYERS

- 15.2.1 VUBIQ NETWORKS, INC.

- TABLE 168 VUBIQ NETWORKS, INC: COMPANY OVERVIEW

- 15.2.2 ELVA-1

- TABLE 169 ELVA-1: COMPANY OVERVIEW

- 15.2.3 VERANA NETWORKS

- TABLE 170 VERANA NETWORKS: COMPANY OVERVIEW

- 15.2.4 CABLEFREE

- TABLE 171 CABLEFREE: COMPANY OVERVIEW

- 15.2.5 FASTBACK NETWORKS

- TABLE 172 FASTBACK NETWORKS: COMPANY OVERVIEW

- 15.2.6 QUINSTAR TECHNOLOGY, INC.

- TABLE 173 QUINSTAR TECHNOLOGY, INC.: COMPANY OVERVIEW

- 15.2.7 TREX ENTERPRISES CORPORATION

- TABLE 174 TREX ENTERPRISES CORPORATION.: COMPANY OVERVIEW

- 15.2.8 NUCTECH

- TABLE 175 NUCTECH: COMPANY OVERVIEW

- 15.2.9 KYOCERA CORPORATION

- TABLE 176 KYOCERA CORPORATION: COMPANY OVERVIEW

- 15.2.10 RADWIN

- TABLE 177 RADWIN: COMPANY OVERVIEW

- 15.2.11 IGNITENET

- TABLE 178 IGNITENET: COMPANY OVERVIEW

- 15.2.12 KRATOS DEFENSE & SECURITY SOLUTIONS, INC.

- TABLE 179 KRATOS DEFENSE & SECURITY SOLUTIONS, INC.: COMPANY OVERVIEW

- 15.2.13 ANOKIWAVE, INC

- TABLE 180 ANOKIWAVE, INC: COMPANY OVERVIEW

- 15.2.14 SPACEK LABS INC.

- TABLE 181 SPACEK LABS INC.: COMPANY OVERVIEW

- 15.2.15 CAMBIUM NETWORKS, LTD.

- TABLE 182 CAMBIUM NETWORKS, LTD.: COMPANY OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS