|

|

市場調査レポート

商品コード

1118549

フレキシブルヒーターの世界市場:種類別 (シリコーンゴム、ポリイミド、ポリエステル、マイカ)・業種別 (電子機器・半導体、医療、航空宇宙、自動車・輸送、食品・飲料、石油・ガス)・地域別の将来予測 (2027年まで)Flexible Heater Market by Type (Silicone Rubber, Polyimide, Polyester, Mica), Industry (Electronics & Semiconductor, Medical, Aerospace, Automotive & Transportation, Food & Beverages, Oil & Gas) and Region - Global Forecast to 2027 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| フレキシブルヒーターの世界市場:種類別 (シリコーンゴム、ポリイミド、ポリエステル、マイカ)・業種別 (電子機器・半導体、医療、航空宇宙、自動車・輸送、食品・飲料、石油・ガス)・地域別の将来予測 (2027年まで) |

|

出版日: 2022年08月18日

発行: MarketsandMarkets

ページ情報: 英文 193 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

フレキシブルヒーターの世界市場規模は、2022年の12億米ドルから2027年には17億米ドルに達し、2022年から2027年にかけて7.2%のCAGRで成長すると予測されています。

各種産業 (医療、電子機器・半導体、航空宇宙、自動車・輸送など) での技術進歩によるフレキシブルヒーターの需要増大や、プロセス熱や凍結防止を必要とする革新的製品の発売、新しいタイプのフレキシブルヒーターの継続的研究開発は、フレキシブルヒーター市場の成長を推進する主要因の一部となっています。

"マイカベースのフレキシブルヒーターが、2022年から2027年にかけて大幅なCAGRで成長する"

マイカベースのフレキシブルヒーターは、エネルギー効率とコスト効率が高く、極端な温度でも優れた加熱性能を発揮します。マイカベースのフレキシブルヒーターは、通常より高いワット密度と速い温度回復が必要な用途向けに設計されています。これらの特徴から、マイカベースのフレキシブルヒーターは、予測期間中に大きなCAGRで成長することが期待されています。

"電子機器・半導体業界は、予測期間中に最大の市場シェアを獲得する"

電子機器・半導体業界向けのフレキシブルヒーター市場は、最大の市場シェアを占めており、予測期間中に最も速いCAGRで成長すると予測されています。フレキシブルヒーターは、プラズマエッチシステム、プロービングステーション、ICテストハンドリング装置、フォトレジストトラックシステム、LCDスクリーン (プリヒート時) 、半導体テストモジュールなどの半導体製造装置で使用されています。また、冷凍機、コーヒーメーカー、ワックスメーカーなどの電子機器にも使用されています。

"予測期間中、アジアが最大の市場シェアを占める"

アジア太平洋は予測期間中、フレキシブルヒーター市場で最大の市場規模を獲得すると予想されます。また、最も高いCAGRで成長するとも予想されています。アジア太平洋では電子機器・半導体・自動車産業が主導的な地位にあり、今後数年間は医療機器や食品機械製造の市場が最も速い速度で成長すると予想されています。

目次

第1章 イントロダクション

第2章 調査方法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概略

- イントロダクション

- 市場力学

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 顧客に影響を与える動向/混乱

- 技術分析

- フレキシブルプリントヒーター

- 電化・自動化技術

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- ケーススタディ分析

- 貿易分析

- 特許分析

- 主な会議とイベント (2022年~2023年)

- 規制状況

第6章 フレキシブルヒーターの流通チャネル

- イントロダクション

- 直接販売

- 間接販売

第7章 フレキシブルヒーター市場:種類別

- イントロダクション

- シリコーンゴムベース

- ポリイミドベース

- ポリエステルベース

- マイカベース

- その他

第8章 フレキシブルヒーター市場:業種別

- イントロダクション

- 電子機器・半導体

- 医療

- 航空宇宙

- 食品・飲料

- 自動車・輸送

- 石油・ガス

- その他

第9章 フレキシブルヒーター市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- 他の欧州諸国

- アジア太平洋

- 中国

- 日本

- インド

- 他のアジア太平洋諸国

- 他の国々 (RoW)

- 中東

- アフリカ

- 南米

第10章 競合情勢

- 概要

- 主要企業の戦略/勝つ権利

- 上位5社の収益分析

- 市場シェア分析

- 競合評価クアドラント

- 中小企業 (SME) の評価クアドラント (2021年)

- フレキシブルヒーター市場:企業のフットプリント

- 競合ベンチマーキング

- 競合シナリオ

第11章 企業プロファイル

- 主要企業

- HONEYWELL INTERNATIONAL

- NIBE INDUSTRIER

- OMEGA ENGINEERING

- WATLOW ELECTRIC MANUFACTURING

- SMITHS GROUP

- ALL FLEX FLEXIBLE CIRCUITS

- CHROMALOX

- MINCO

- ROGERS CORPORATION

- ZOPPAS INDUSTRIES

- その他の企業

- BIRK MANUFACTURING INC

- BUCAN

- DELTA/ACRA

- DUREX INDUSTRIES

- EPEC ENGINEERED TECHNOLOGIES

- HOLROYD COMPONENTS

- HOTSET

- KLC CORPORATION

- MIYO TECHNOLOGY

- NATIONAL PLASTIC HEATER

- NEL TECHNOLOGIES

- SINOMAS

- TEMPCO ELECTRIC HEATER

- THERMO HEATING ELEMENTS

- THERMOCOAX

第12章 隣接市場

- 床暖房市場

- イントロダクション

- 温水循環式床暖房 (湿式)

- 電気式床暖房 (乾式)

第13章 付録

The global flexible heater market size is anticipated to grow from USD 1.2 billion in 2022 to USD 1.7 billion by 2027, at a CAGR of 7.2% from 2022 to 2027. Rising requirements of flexible heaters due to technological advancement in several industries such as medical, electronics & semiconductor, aerospace, automotive & transportation, launch of innovative products which require process heat and freeze protection, and continuous research and development of new types of flexible heater are some of the major factors propelling the growth of flexible heater market.

"Mica-based flexible heater type to grow at a significant CAGRfrom 2022 to 2027"

Mica-based flexible heaters are energy-efficient and cost-effective, and they provide excellent heating performance even at extreme temperatures.The mica-based flexible heaters are designed for application that require higher than normal watt densities and fast temperature recovery. They are economical and have high operating temperatures, for which they are used in air heaters, enclosure systems, food service equipment, packing equipment, and various other places.As a results of these features, mica-based flexible heaters are expected to grow at a significant CAGR during the forecast period.

"Electronics & semiconductor industry is expected to contribute largest market share of the flexible heater market during the forecast period."

The flexible heater market for the electronics & semiconductor industry accounts the largest markets share and is expected to grow at the fastest CAGR during the forecast period. Flexible heaters are used in semiconductor manufacturing equipment such as plasma etch systems, probing stations, IC test handling equipment, photo-resist track systems, LCD screen (in preheating), and semiconductor test modules. These heaters also find applications in electronics such as in refrigeration equipment, coffee maker, wax maker, and various other electronic products. The increase in demand for such products is expected to drive the market for flexible heaters in the electronics & semiconductor industry.

"Asia is expected to account for the largest share of market during the forecast period."

Asia Pacific is expected to contribute the largest size of the flexible heater market during forecast period. Asia Pacific is expected to contribute to the largest market share in the flexible heater market. The region is also expected to grow at the highest CAGR during the forecast period. The increasing demand for flexible heaters in various medical equipment, analytical instruments, avionics and defense systems, semiconductor processes, and commercial food equipment is driving the growth of the flexible heater market. The electronics, semiconductor, and automotive industries are in the leading position in Asia Pacific, and the market for the medical device and food equipment manufacturing is expected to grow at the fastest rate in this region in the upcoming years.

Break-up of the profiles ofprimary participants:

- By Company Type -Tier 1 - 40%, Tier 2 - 25%, and Tier 3 - 35%

- By Designation - C-level Executives - 25%, Directors - 40%, and Others - 35%

- By Region- North America - 45%, Europe - 35%, Asia Pacific - 15%, and RoW - 5%

Research Coverage:

Theflexible heater market has been segmented into type, distribution channel, industry and region. The flexible heater market has been studied for North America, Europe, Asia Pacific, and the Rest of the World (RoW).

Reasons to buy the report:

- Illustrative segmentation, analysis, and forecast of the market based ontype, distribution channel, industry and region have been conducted to give an overall view of the flexible heater market.

- Avalue chain analysis has been performed to provide in-depth insights into the flexible heater market.

- The key drivers, restraints, opportunities, and challenges pertaining to the flexible heater market have been detailed in this report.

- The report includes a detailed competitive landscape of the market, along with key players, as well as an in-depth analysis of their revenues

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.4 STUDY SCOPE

- 1.4.1 MARKETS COVERED

- FIGURE 1 FLEXIBLE HEATER MARKET: SEGMENTATION

- 1.4.2 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 INTRODUCTION

- FIGURE 2 FLEXIBLE HEATER MARKET: RESEARCH DESIGN

- 2.2 RESEARCH DATA

- 2.2.1 SECONDARY DATA

- 2.2.1.1 List of major secondary sources

- 2.2.1.2 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 Primary interviews with experts

- 2.2.2.2 Key data from primary sources

- 2.2.2.3 Key industry insights

- 2.2.2.4 Breakdown of primaries

- 2.2.1 SECONDARY DATA

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Approach for arriving at market size using bottom-up analysis

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- 2.3.2.1 Approach for arriving at market size using top-down analysis

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

- 2.3.1 BOTTOM-UP APPROACH

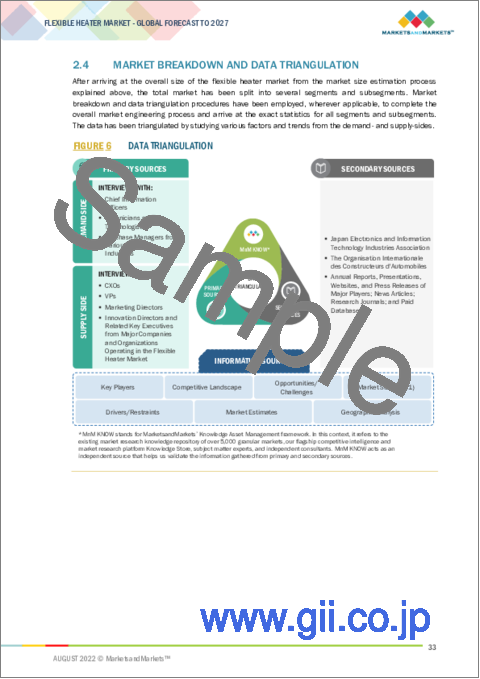

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 6 DATA TRIANGULATION

- 2.5 ASSUMPTIONS

- 2.5.1 RESEARCH ASSUMPTIONS

- 2.5.2 RESEARCH LIMITATIONS

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 7 FLEXIBLE HEATER MARKET, 2018-2027 (USD MILLION)

- FIGURE 8 SILICONE RUBBER-BASED FLEXIBLE HEATERS TO ACCOUNT FOR LARGEST SHARE IN 2022

- FIGURE 9 ELECTRONICS & SEMICONDUCTORS INDUSTRY TO GROW AT HIGHEST CAGR

- FIGURE 10 ASIA PACIFIC ACCOUNTED FOR LARGEST SHARE IN 2021

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN FLEXIBLE HEATER MARKET

- FIGURE 11 MEDICAL INDUSTRY TO GROW AT SIGNIFICANT RATE

- 4.2 FLEXIBLE HEATER MARKET, BY TYPE (2022-2027)

- FIGURE 12 SILICONE RUBBER-BASED FLEXIBLE HEATERS TO LEAD MARKET

- 4.3 FLEXIBLE HEATER MARKET, BY INDUSTRY

- FIGURE 13 ELECTRONICS & SEMICONDUCTORS INDUSTRY TO ACCOUNT FOR MAJOR SHARE

- 4.4 FLEXIBLE HEATER MARKET, BY REGION

- FIGURE 14 MARKET IN CHINA TO GROW AT HIGHEST CAGR

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 15 FLEXIBLE HEATER MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Broad scope in various industries

- FIGURE 16 PRIVATE AND COMMERCIAL VEHICLE PRODUCTION, BY COUNTRY, 2021 (UNITS)

- 5.2.1.2 Technological advancements, innovative products, and flexible form factor

- 5.2.1.3 Surging adoption in medical applications

- FIGURE 17 IMPACT ANALYSIS OF DRIVERS

- 5.2.2 RESTRAINTS

- 5.2.2.1 Extensive operational costs

- FIGURE 18 IMPACT ANALYSIS OF RESTRAINTS

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Investments in IT sector and demand in electronics & semiconductors industry

- 5.2.3.2 Applications in oil & gas and petrochemical industries

- 5.2.3.3 Surging demand for electric mobility

- FIGURE 19 IMPACT ANALYSIS OF OPPORTUNITIES

- 5.2.4 CHALLENGES

- 5.2.4.1 Deployment in rugged environments

- FIGURE 20 IMPACT ANALYSIS OF CHALLENGES

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 21 VALUE CHAIN ANALYSIS: FLEXIBLE HEATER MARKET

- 5.4 ECOSYSTEM ANALYSIS

- FIGURE 22 ECOSYSTEM: FLEXIBLE HEATER MARKET

- TABLE 1 FLEXIBLE HEATER MARKET: ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 ASP ANALYSIS OF KEY PLAYERS

- FIGURE 23 ASP OF FLEXIBLE HEATERS BASED ON TYPE

- TABLE 2 APPROXIMATE ASPS OF FLEXIBLE HEATERS BASED ON TYPE, BY COMPANY (USD)

- 5.5.2 ASP TRENDS

- TABLE 3 AVERAGE SELLING PRICES OF FLEXIBLE HEATERS

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS

- FIGURE 24 REVENUE SHIFT IN FLEXIBLE HEATER MARKET

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 FLEXIBLE PRINTED HEATERS

- 5.7.2 ELECTRIFICATION AND AUTOMATION TECHNOLOGIES

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 FLEXIBLE HEATER MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 25 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP THREE INDUSTRIES

- TABLE 5 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP THREE INDUSTRIES (%)

- 5.9.2 BUYING CRITERIA

- FIGURE 26 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- TABLE 6 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- 5.10 CASE STUDY ANALYSIS

- TABLE 7 DUREX INDUSTRIES PROVIDED FLEXIBLE HEATERS TO MAJOR OIL FIELD GAS ANALYZER MANUFACTURER TO ENSURE TEMPERATURE UNIFORMITY AND PREVENT PREMATURE HEATER FAILURE

- TABLE 8 FLEXIBLE HEATERS PROVIDED BY CHROMALOX MEET STRINGENT DEMANDS IN THERMAL VACUUM TESTING CHAMBER (TVC)

- TABLE 9 HIGH TEMPERATURE CONTROL WITH REDUCED PROFILE THERMOCOUPLE AND FLEXIBLE HEATER

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT SCENARIO

- FIGURE 27 IMPORTS, BY KEY COUNTRY, 2017-2021 (USD MILLION)

- 5.11.2 EXPORT SCENARIO

- FIGURE 28 EXPORTS, BY KEY COUNTRY, 2017-2021 (USD MILLION)

- 5.12 PATENT ANALYSIS

- FIGURE 29 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS (2012-2021)

- TABLE 10 TOP 20 PATENT OWNERS IN US (2012-2021)

- FIGURE 30 NUMBER OF PATENTS GRANTED PER YEAR FROM 2012 TO 2021

- TABLE 11 LIST OF SOME PATENTS IN FLEXIBLE HEATER MARKET

- 5.13 KEY CONFERENCES AND EVENTS (2022-2023)

- TABLE 12 FLEXIBLE HEATER MARKET: CONFERENCES AND EVENTS

- 5.14 REGULATORY LANDSCAPE

- 5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS RELATED TO FLEXIBLE HEATERS

- TABLE 13 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

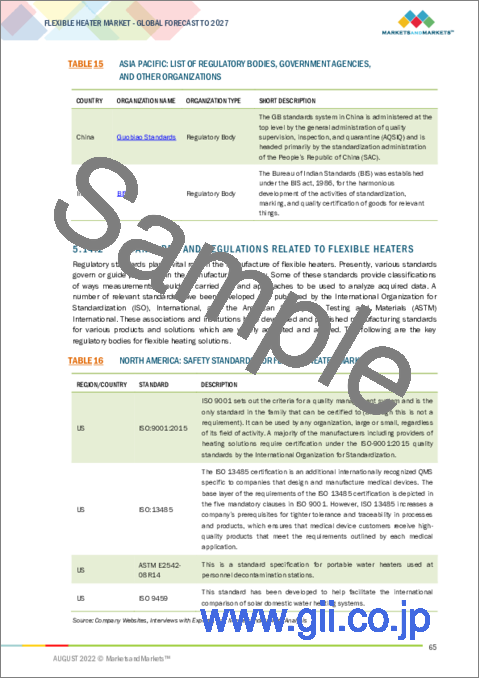

- TABLE 15 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.2 STANDARDS AND REGULATIONS RELATED TO FLEXIBLE HEATERS

- TABLE 16 NORTH AMERICA: SAFETY STANDARDS FOR FLEXIBLE HEATER MARKET

- TABLE 17 EUROPE: SAFETY STANDARDS FOR FLEXIBLE HEATER MARKET

6 DISTRIBUTION CHANNELS FOR FLEXIBLE HEATERS

- 6.1 INTRODUCTION

- FIGURE 31 DISTRIBUTION CHANNELS FOR FLEXIBLE HEATERS

- FIGURE 32 DISTRIBUTION CHANNEL ENTITIES IN FLEXIBLE HEATER MARKET

- 6.2 DIRECT

- 6.2.1 DIRECT DISTRIBUTION CHANNEL GENERATES MAJOR PROFITS

- 6.3 INDIRECT

- 6.3.1 GLOBAL DEMAND TO INCREASE DISTRIBUTORS AND INTERMEDIARIES

7 FLEXIBLE HEATER MARKET, BY TYPE

- 7.1 INTRODUCTION

- FIGURE 33 FLEXIBLE HEATER MARKET, BY TYPE

- FIGURE 34 SILICONE RUBBER-BASED SEGMENT TO LEAD AND GROW AT HIGHEST CAGR

- TABLE 18 FLEXIBLE HEATER MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 19 FLEXIBLE HEATER MARKET, BY TYPE, 2022-2027 (USD MILLION)

- 7.2 SILICONE RUBBER-BASED

- 7.2.1 SIGNIFICANT APPLICATIONS IN ELECTRONICS & SEMICONDUCTORS INDUSTRY

- FIGURE 35 ELECTRONICS & SEMICONDUCTORS SEGMENT TO GROW AT HIGHEST CAGR IN SILICONE RUBBER-BASED MARKET

- TABLE 20 SILICONE RUBBER-BASED FLEXIBLE HEATER MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 21 SILICONE RUBBER-BASED FLEXIBLE HEATER MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 22 SILICONE RUBBER-BASED FLEXIBLE HEATER MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 23 SILICONE RUBBER-BASED FLEXIBLE HEATER MARKET, BY REGION, 2022-2027 (USD MILLION)

- 7.3 POLYIMIDE-BASED

- 7.3.1 DEMAND FOR MEDICAL, ANALYTICAL, AND ELECTRONIC INSTRUMENTS

- TABLE 24 POLYIMIDE-BASED FLEXIBLE HEATER MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 25 POLYIMIDE-BASED FLEXIBLE HEATER MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 26 POLYIMIDE-BASED FLEXIBLE HEATER MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 27 POLYIMIDE-BASED FLEXIBLE HEATER MARKET, BY REGION, 2022-2027 (USD MILLION)

- 7.4 POLYESTER-BASED

- 7.4.1 TECHNOLOGICAL ADVANCEMENTS IN ELECTRONICS, AUTOMOTIVE, AND MEDICAL FIELDS

- TABLE 28 POLYESTER-BASED FLEXIBLE HEATER MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 29 POLYESTER-BASED FLEXIBLE HEATER MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 30 POLYESTER-BASED FLEXIBLE HEATER MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 31 POLYESTER-BASED FLEXIBLE HEATER MARKET, BY REGION, 2022-2027 (USD MILLION)

- 7.5 MICA-BASED

- 7.5.1 DEMAND FROM ELECTRONICS & SEMICONDUCTORS AND AEROSPACE INDUSTRIES

- TABLE 32 MICA-BASED FLEXIBLE HEATER MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 33 MICA-BASED FLEXIBLE HEATER MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 34 MICA-BASED FLEXIBLE HEATER MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 35 MICA-BASED FLEXIBLE HEATER MARKET, BY REGION, 2022-2027 (USD MILLION)

- 7.6 OTHERS

- TABLE 36 FLEXIBLE HEATER MARKET FOR OTHER TYPES, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 37 FLEXIBLE HEATER MARKET FOR OTHER TYPES, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 38 FLEXIBLE HEATER MARKET FOR OTHER TYPES, BY REGION, 2018-2021 (USD MILLION)

- TABLE 39 FLEXIBLE HEATER MARKET FOR OTHER TYPES, BY REGION, 2022-2027 (USD MILLION)

8 FLEXIBLE HEATER MARKET, BY INDUSTRY

- 8.1 INTRODUCTION

- FIGURE 36 FLEXIBLE HEATER MARKET, BY INDUSTRY

- FIGURE 37 ELECTRONICS & SEMICONDUCTORS SEGMENT TO LEAD AND GROW AT HIGHEST CAGR

- TABLE 40 FLEXIBLE HEATER MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 41 FLEXIBLE HEATER MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- 8.2 ELECTRONICS & SEMICONDUCTORS

- 8.2.1 SEMICONDUCTOR MANUFACTURING EQUIPMENT AND GENERAL ELECTRONICS TO DRIVE MARKET

- FIGURE 38 SILICONE RUBBER-BASED SEGMENT TO BE LARGEST IN ELECTRONICS & SEMICONDUCTORS

- TABLE 42 FLEXIBLE HEATER MARKET FOR ELECTRONICS & SEMICONDUCTORS, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 43 FLEXIBLE HEATER MARKET FOR ELECTRONICS & SEMICONDUCTORS, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 44 FLEXIBLE HEATER MARKET FOR ELECTRONICS & SEMICONDUCTORS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 45 FLEXIBLE HEATER MARKET FOR ELECTRONICS & SEMICONDUCTORS, BY REGION, 2022-2027 (USD MILLION)

- 8.3 MEDICAL

- 8.3.1 MARKET IN ASIA PACIFIC TO GROW AT HIGHEST CAGR

- FIGURE 39 MICA-BASED SEGMENT TO GROW AT HIGHEST CAGR IN MEDICAL

- TABLE 46 FLEXIBLE HEATER MARKET FOR MEDICAL, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 47 FLEXIBLE HEATER MARKET FOR MEDICAL, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 48 FLEXIBLE HEATER MARKET FOR MEDICAL, BY REGION, 2018-2021 (USD MILLION)

- TABLE 49 FLEXIBLE HEATER MARKET FOR MEDICAL, BY REGION, 2022-2027 (USD MILLION)

- 8.4 AEROSPACE

- 8.4.1 NORTH AMERICA TO ACCOUNT FOR LARGEST SHARE

- TABLE 50 FLEXIBLE HEATER MARKET FOR AEROSPACE, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 51 FLEXIBLE HEATER MARKET FOR AEROSPACE, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 52 FLEXIBLE HEATER MARKET FOR AEROSPACE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 53 FLEXIBLE HEATER MARKET FOR AEROSPACE, BY REGION, 2022-2027 (USD MILLION)

- 8.5 FOOD & BEVERAGES

- 8.5.1 THERMAL PROCESSING, FREEZE PROTECTION, AND VISCOSITY CONTROL TO INCREASE DEMAND

- TABLE 54 FLEXIBLE HEATER MARKET FOR FOOD & BEVERAGES, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 55 FLEXIBLE HEATER MARKET FOR FOOD & BEVERAGES, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 56 FLEXIBLE HEATER MARKET FOR FOOD & BEVERAGES, BY REGION, 2018-2021 (USD MILLION)

- TABLE 57 FLEXIBLE HEATER MARKET FOR FOOD & BEVERAGES, BY REGION, 2022-2027 (USD MILLION)

- 8.6 AUTOMOTIVE & TRANSPORTATION

- 8.6.1 RISING TREND IN ELECTRIFICATION

- TABLE 58 FLEXIBLE HEATER MARKET FOR AUTOMOTIVE & TRANSPORTATION, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 59 FLEXIBLE HEATER MARKET FOR AUTOMOTIVE & TRANSPORTATION, BY TYPE, 2022-2027 (USD MILLION)

- FIGURE 40 AUTOMOTIVE & TRANSPORTATION SEGMENT TO GROW AT HIGHEST CAGR IN ASIA PACIFIC

- TABLE 60 FLEXIBLE HEATER MARKET FOR AUTOMOTIVE & TRANSPORTATION, BY REGION, 2018-2021 (USD MILLION)

- TABLE 61 FLEXIBLE HEATER MARKET FOR AUTOMOTIVE & TRANSPORTATION, BY REGION, 2022-2027 (USD MILLION)

- 8.7 OIL & GAS

- 8.7.1 INCREASING GLOBAL OIL CONSUMPTION

- TABLE 62 FLEXIBLE HEATER MARKET FOR OIL & GAS, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 63 FLEXIBLE HEATER MARKET FOR OIL & GAS, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 64 FLEXIBLE HEATER MARKET FOR OIL & GAS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 65 FLEXIBLE HEATER MARKET FOR OIL & GAS, BY REGION, 2022-2027 (USD MILLION)

- 8.8 OTHERS

- TABLE 66 FLEXIBLE HEATER MARKET FOR OTHER INDUSTRIES, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 67 FLEXIBLE HEATER MARKET FOR OTHER INDUSTRIES, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 68 FLEXIBLE HEATER MARKET FOR OTHER INDUSTRIES, BY REGION, 2018-2021 (USD MILLION)

- TABLE 69 FLEXIBLE HEATER MARKET FOR OTHER INDUSTRIES, BY REGION, 2022-2027 (USD MILLION)

9 FLEXIBLE HEATER MARKET, BY REGION

- 9.1 INTRODUCTION

- FIGURE 41 MARKET IN CHINA TO GROW AT HIGHEST CAGR

- TABLE 70 FLEXIBLE HEATER MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 71 FLEXIBLE HEATER MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.2 NORTH AMERICA

- FIGURE 42 NORTH AMERICA: FLEXIBLE HEATER MARKET SNAPSHOT

- TABLE 72 FLEXIBLE HEATER MARKET IN NORTH AMERICA, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 73 FLEXIBLE HEATER MARKET IN NORTH AMERICA, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 74 FLEXIBLE HEATER MARKET IN NORTH AMERICA, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 75 FLEXIBLE HEATER MARKET IN NORTH AMERICA, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 76 FLEXIBLE HEATER MARKET IN NORTH AMERICA, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 77 FLEXIBLE HEATER MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2027 (USD MILLION)

- 9.2.1 US

- 9.2.1.1 Aerospace and medical industries to drive market

- 9.2.2 CANADA

- 9.2.2.1 Medical and automotive industries drive market

- 9.2.3 MEXICO

- 9.2.3.1 Growth of automotive and electronics industries

- 9.3 EUROPE

- FIGURE 43 EUROPE: FLEXIBLE HEATER MARKET SNAPSHOT

- TABLE 78 FLEXIBLE HEATER MARKET IN EUROPE, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 79 FLEXIBLE HEATER MARKET IN EUROPE, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 80 FLEXIBLE HEATER MARKET IN EUROPE, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 81 FLEXIBLE HEATER MARKET IN EUROPE, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 82 FLEXIBLE HEATER MARKET IN EUROPE, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 83 FLEXIBLE HEATER MARKET IN EUROPE, BY COUNTRY, 2022-2027 (USD MILLION)

- 9.3.1 GERMANY

- 9.3.1.1 Largest share of European market

- 9.3.2 FRANCE

- 9.3.2.1 Booming aerospace and other industries

- 9.3.3 UK

- 9.3.3.1 Automotive industry to witness rapid growth

- 9.3.4 REST OF EUROPE

- 9.4 ASIA PACIFIC

- FIGURE 44 ASIA PACIFIC: FLEXIBLE HEATER MARKET SNAPSHOT

- TABLE 84 FLEXIBLE HEATER MARKET IN ASIA PACIFIC, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 85 FLEXIBLE HEATER MARKET IN ASIA PACIFIC, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 86 FLEXIBLE HEATER MARKET IN ASIA PACIFIC, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 87 FLEXIBLE HEATER MARKET IN ASIA PACIFIC, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 88 FLEXIBLE HEATER MARKET IN ASIA PACIFIC, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 89 FLEXIBLE HEATER MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2027 (USD MILLION)

- 9.4.1 CHINA

- 9.4.1.1 Largest share of Asia Pacific market

- 9.4.2 JAPAN

- 9.4.2.1 Automotive and medical industries to drive growth

- TABLE 90 LIST OF MAJOR LOCAL MANUFACTURERS/SUPPLIERS OF FLEXIBLE HEATERS IN JAPAN

- 9.4.3 INDIA

- 9.4.3.1 Automotive and semiconductors & electronics to drive demand

- 9.4.4 REST OF ASIA PACIFIC

- 9.5 REST OF THE WORLD (ROW)

- FIGURE 45 MARKET IN SOUTH AMERICA TO GROW AT HIGHEST CAGR

- TABLE 91 FLEXIBLE HEATER MARKET IN ROW, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 92 FLEXIBLE HEATER MARKET IN ROW, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 93 FLEXIBLE HEATER MARKET IN ROW, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 94 FLEXIBLE HEATER MARKET IN ROW, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 95 FLEXIBLE HEATER MARKET IN ROW, BY REGION, 2018-2021 (USD MILLION)

- TABLE 96 FLEXIBLE HEATER MARKET IN ROW, BY REGION, 2022-2027 (USD MILLION)

- 9.5.1 MIDDLE EAST

- 9.5.1.1 Saudi Arabia

- 9.5.1.1.1 Key contributor to growth in Middle East

- 9.5.1.2 UAE

- 9.5.1.2.1 Major oil & gas companies to support growth

- 9.5.1.3 Rest of Middle East

- 9.5.1.1 Saudi Arabia

- TABLE 97 FLEXIBLE HEATER MARKET IN MIDDLE EAST, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 98 FLEXIBLE HEATER MARKET IN MIDDLE EAST, BY COUNTRY, 2022-2027 (USD MILLION)

- 9.5.2 AFRICA

- 9.5.2.1 Demand from various industries to drive market

- 9.5.3 SOUTH AMERICA

- 9.5.3.1 Market driven by major industries

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES/RIGHT-TO-WIN

- TABLE 99 OVERVIEW OF STRATEGIES BY KEY FLEXIBLE HEATER MANUFACTURERS

- 10.3 REVENUE ANALYSIS FOR TOP FIVE COMPANIES

- FIGURE 46 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2017-2021

- 10.4 MARKET SHARE ANALYSIS

- TABLE 100 MARKET SHARE OF TOP FIVE PLAYERS IN 2021

- 10.5 COMPETITIVE EVALUATION QUADRANT

- 10.5.1 STAR PLAYERS

- 10.5.2 EMERGING LEADERS

- 10.5.3 PERVASIVE PLAYERS

- 10.5.4 PARTICIPANTS

- FIGURE 47 FLEXIBLE HEATER MARKET (GLOBAL) COMPANY EVALUATION QUADRANT, 2021

- 10.6 SMALL AND MEDIUM-SIZED ENTERPRISES (SMES) EVALUATION QUADRANT, 2021

- 10.6.1 PROGRESSIVE COMPANIES

- 10.6.2 RESPONSIVE COMPANIES

- 10.6.3 DYNAMIC COMPANIES

- 10.6.4 STARTING BLOCKS

- FIGURE 48 FLEXIBLE HEATER MARKET (GLOBAL) SME EVALUATION QUADRANT, 2021

- 10.7 FLEXIBLE HEATER MARKET: COMPANY FOOTPRINT

- TABLE 101 OVERALL COMPANY FOOTPRINT

- TABLE 102 COMPANY PRODUCT FOOTPRINT

- TABLE 103 COMPANY INDUSTRY FOOTPRINT

- TABLE 104 COMPANY REGION FOOTPRINT

- 10.8 COMPETITIVE BENCHMARKING

- TABLE 105 FLEXIBLE HEATER MARKET: KEY STARTUPS/SMES

- TABLE 106 FLEXIBLE HEATER MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 10.9 COMPETITIVE SCENARIO

- TABLE 107 FLEXIBLE HEATER MARKET: PRODUCT LAUNCHES, 2020-2021

- TABLE 108 FLEXIBLE HEATER MARKET: DEALS, 2020-2021

11 COMPANY PROFILES

- (Business Overview, Products/Solutions/Services Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 11.1 KEY PLAYERS

- 11.1.1 HONEYWELL INTERNATIONAL

- TABLE 109 HONEYWELL INTERNATIONAL: BUSINESS OVERVIEW

- FIGURE 49 HONEYWELL INTERNATIONAL: COMPANY SNAPSHOT

- TABLE 110 HONEYWELL INTERNATIONAL: PRODUCT OFFERINGS

- 11.1.2 NIBE INDUSTRIER

- TABLE 111 NIBE INDUSTRIER: BUSINESS OVERVIEW

- FIGURE 50 NIBE INDUSTRIER: COMPANY SNAPSHOT

- TABLE 112 NIBE INDUSTRIER: PRODUCT OFFERINGS

- TABLE 113 NIBE INDUSTRIER: DEALS

- 11.1.3 OMEGA ENGINEERING

- TABLE 114 OMEGA ENGINEERING: BUSINESS OVERVIEW

- FIGURE 51 OMEGA ENGINEERING: COMPANY SNAPSHOT

- TABLE 115 OMEGA ENGINEERING: PRODUCT OFFERINGS

- 11.1.4 WATLOW ELECTRIC MANUFACTURING

- TABLE 116 WATLOW ELECTRIC MANUFACTURING: BUSINESS OVERVIEW

- TABLE 117 WATLOW ELECTRIC MANUFACTURING: PRODUCT OFFERINGS

- TABLE 118 WATLOW ELECTRIC MANUFACTURING: DEALS

- 11.1.5 SMITHS GROUP

- TABLE 119 SMITHS GROUP: BUSINESS OVERVIEW

- FIGURE 52 SMITHS GROUP: COMPANY SNAPSHOT

- TABLE 120 SMITHS GROUP: PRODUCT OFFERINGS

- TABLE 121 SMITHS GROUP: DEALS

- 11.1.6 ALL FLEX FLEXIBLE CIRCUITS

- TABLE 122 ALL FLEX FLEXIBLE CIRCUITS: BUSINESS OVERVIEW

- TABLE 123 ALL FLEX FLEXIBLE CIRCUITS: PRODUCT OFFERINGS

- TABLE 124 ALL FLEX FLEXIBLE CIRCUITS: PRODUCT LAUNCHES AND DEVELOPMENTS

- 11.1.7 CHROMALOX

- TABLE 125 CHROMALOX: BUSINESS OVERVIEW

- TABLE 126 CHROMALOX: PRODUCT OFFERINGS

- 11.1.8 MINCO

- TABLE 127 MINCO: BUSINESS OVERVIEW

- TABLE 128 MINCO: PRODUCT OFFERINGS

- 11.1.9 ROGERS CORPORATION

- TABLE 129 ROGERS CORPORATION: BUSINESS OVERVIEW

- FIGURE 53 ROGERS CORPORATION: COMPANY SNAPSHOT

- TABLE 130 ROGERS CORPORATION: PRODUCT OFFERINGS

- TABLE 131 ROGERS CORPORATION: PRODUCT LAUNCHES

- TABLE 132 ROGERS CORPORATION: DEALS

- 11.1.10 ZOPPAS INDUSTRIES

- TABLE 133 ZOPPAS INDUSTRIES: BUSINESS OVERVIEW

- TABLE 134 ZOPPAS INDUSTRIES: PRODUCT OFFERINGS

- 11.2 OTHER PLAYERS

- 11.2.1 BIRK MANUFACTURING INC

- TABLE 135 BIRK MANUFACTURING INC: COMPANY OVERVIEW

- 11.2.2 BUCAN

- TABLE 136 BUCAN: COMPANY OVERVIEW

- 11.2.3 DELTA/ACRA

- TABLE 137 DELTA/ACRA: COMPANY OVERVIEW

- 11.2.4 DUREX INDUSTRIES

- TABLE 138 DUREX INDUSTRIES: COMPANY OVERVIEW

- 11.2.5 EPEC ENGINEERED TECHNOLOGIES

- TABLE 139 EPEC ENGINEERED TECHNOLOGIES: COMPANY OVERVIEW

- 11.2.6 HOLROYD COMPONENTS

- TABLE 140 HOLROYD COMPONENTS: COMPANY OVERVIEW

- 11.2.7 HOTSET

- TABLE 141 HOTSET: COMPANY OVERVIEW

- 11.2.8 KLC CORPORATION

- TABLE 142 KLC CORPORATION: COMPANY OVERVIEW

- 11.2.9 MIYO TECHNOLOGY

- TABLE 143 MIYO TECHNOLOGY: COMPANY OVERVIEW

- 11.2.10 NATIONAL PLASTIC HEATER

- TABLE 144 NATIONAL PLASTIC HEATER: COMPANY OVERVIEW

- 11.2.11 NEL TECHNOLOGIES

- TABLE 145 NEL TECHNOLOGIES: COMPANY OVERVIEW

- 11.2.12 SINOMAS

- TABLE 146 SINOMAS: COMPANY OVERVIEW

- 11.2.13 TEMPCO ELECTRIC HEATER

- TABLE 147 TEMPCO ELECTRIC HEATER: COMPANY OVERVIEW

- 11.2.14 THERMO HEATING ELEMENTS

- TABLE 148 THERMO HEATING ELEMENTS: COMPANY OVERVIEW

- 11.2.15 THERMOCOAX

- TABLE 149 THERMOCOAX: COMPANY OVERVIEW

- *Details on Business Overview, Products/Solutions/Services Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

12 ADJACENT MARKETS

- 12.1 UNDERFLOOR HEATING SYSTEM MARKET

- 12.2 INTRODUCTION

- FIGURE 54 MARKET FOR HYDRONIC UNDERFLOOR HEATING TO LEAD

- TABLE 150 UNDERFLOOR HEATING MARKET, BY PRODUCT TYPE, 2018-2021 (USD MILLION)

- TABLE 151 UNDERFLOOR HEATING MARKET, BY PRODUCT TYPE, 2022-2027 (USD MILLION)

- 12.3 HYDRONIC UNDERFLOOR HEATING (WET SYSTEM)

- FIGURE 55 MANIFOLDS AND VALVES TO HOLD LARGEST SHARE OF HYDRONIC UNDERFLOOR HEATING HARDWARE MARKET IN 2022

- TABLE 152 HYDRONIC UNDERFLOOR HEATING MARKET FOR HARDWARE, BY COMPONENTS, 2018-2021 (USD MILLION)

- TABLE 153 HYDRONIC UNDERFLOOR HEATING MARKET FOR HARDWARE, BY COMPONENTS, 2022-2027 (USD MILLION)

- TABLE 154 HYDRONIC UNDERFLOOR HEATING MARKET, BY INSTALLATION, 2018-2021 (USD MILLION)

- TABLE 155 HYDRONIC UNDERFLOOR HEATING MARKET, BY INSTALLATION, 2022-2027 (USD MILLION)

- TABLE 156 HYDRONIC UNDERFLOOR HEATING MARKET, BY APPLICATION, 2018-2021 (USD MILLION)

- TABLE 157 HYDRONIC UNDERFLOOR HEATING MARKET, BY APPLICATION, 2022-2027 (USD MILLION)

- TABLE 158 HYDRONIC UNDERFLOOR HEATING MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 159 HYDRONIC UNDERFLOOR HEATING MARKET, BY REGION, 2022-2027 (USD MILLION)

- TABLE 160 HYDRONIC UNDERFLOOR HEATING MARKET FOR RESIDENTIAL APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 161 HYDRONIC UNDERFLOOR HEATING MARKET FOR RESIDENTIAL APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 162 HYDRONIC UNDERFLOOR HEATING MARKET FOR COMMERCIAL APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 163 HYDRONIC UNDERFLOOR HEATING MARKET, FOR COMMERCIAL APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 164 HYDRONIC UNDERFLOOR HEATING MARKET FOR INDUSTRIAL APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 165 HYDRONIC UNDERFLOOR HEATING MARKET, FOR INDUSTRIAL APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 166 HYDRONIC UNDERFLOOR HEATING MARKET, FOR HEALTHCARE APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 167 HYDRONIC UNDERFLOOR HEATING MARKET, FOR HEALTHCARE APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 168 HYDRONIC UNDERFLOOR HEATING MARKET, FOR SPORTS & ENTERTAINMENT APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 169 HYDRONIC UNDERFLOOR HEATING MARKET, FOR SPORTS & ENTERTAINMENT APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 170 HYDRONIC UNDERFLOOR HEATING MARKET, FOR OTHER APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 171 HYDRONIC UNDERFLOOR HEATING MARKET, FOR OTHER APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- 12.3.1 HEATING PIPES

- 12.3.1.1 Heating pipes installed within floor structures

- 12.3.2 THERMOSTATS AND SENSORS

- 12.3.2.1 Thermostats and sensors measure temperature to control flow of heating medium

- 12.3.3 THERMAL ACTUATORS

- 12.3.3.1 Thermal actuators are used to sense temperature

- 12.3.4 ZONE VALVES

- 12.3.4.1 Zone valves used to control heating operations of different zones of buildings

- 12.3.5 WIRING CENTERS

- 12.3.5.1 Wiring centers as hubs to control heating systems and thermostats

- 12.3.6 MANIFOLDS AND VALVES

- 12.3.6.1 Manifolds control temperatures in rooms by opening and closing valves according to requirements

- 12.4 ELECTRIC UNDERFLOOR HEATING (DRY SYSTEM)

- FIGURE 56 HEATING MATS TO ACCOUNT FOR LARGEST MARKET SHARE

- TABLE 172 ELECTRIC UNDERFLOOR HEATING MARKET FOR HARDWARE, BY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 173 ELECTRIC UNDERFLOOR HEATING MARKET FOR HARDWARE, BY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 174 ELECTRIC UNDERFLOOR HEATING MARKET, BY INSTALLATION TYPE, 2018-2021 (USD MILLION)

- TABLE 175 ELECTRIC UNDERFLOOR HEATING MARKET, BY INSTALLATION TYPE, 2022-2027 (USD MILLION)

- TABLE 176 ELECTRIC UNDERFLOOR HEATING MARKET, BY APPLICATION, 2018-2021 (USD MILLION)

- TABLE 177 ELECTRIC UNDERFLOOR HEATING MARKET, BY APPLICATION, 2022-2027 (USD MILLION)

- TABLE 178 ELECTRIC UNDERFLOOR HEATING MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 179 ELECTRIC UNDERFLOOR HEATING MARKET, BY REGION, 2022-2027 (USD MILLION)

- TABLE 180 ELECTRIC UNDERFLOOR HEATING MARKET FOR RESIDENTIAL APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 181 ELECTRIC UNDERFLOOR HEATING MARKET FOR RESIDENTIAL APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 182 ELECTRIC UNDERFLOOR HEATING MARKET FOR COMMERCIAL APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 183 ELECTRIC UNDERFLOOR HEATING MARKET FOR COMMERCIAL APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 184 ELECTRIC UNDERFLOOR HEATING MARKET FOR INDUSTRIAL APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 185 ELECTRIC UNDERFLOOR HEATING MARKET FOR INDUSTRIAL APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 186 ELECTRIC UNDERFLOOR HEATING MARKET FOR HEALTHCARE APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 187 ELECTRIC UNDERFLOOR HEATING MARKET FOR HEALTHCARE APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 188 ELECTRIC UNDERFLOOR HEATING MARKET FOR SPORTS & ENTERTAINMENT APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 189 ELECTRIC UNDERFLOOR HEATING MARKET FOR SPORTS & ENTERTAINMENT APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- TABLE 190 ELECTRIC UNDERFLOOR HEATING MARKET FOR OTHER APPLICATIONS, BY REGION, 2018-2021 (USD MILLION)

- TABLE 191 ELECTRIC UNDERFLOOR HEATING MARKET FOR OTHER APPLICATIONS, BY REGION, 2022-2027 (USD MILLION)

- 12.4.1 HEATING CABLE

- 12.4.1.1 Heating cables laid in screed or beneath tiled floors

- 12.4.2 HEATING MATS

- 12.4.2.1 Heating mats utilized in DIY-based underfloor heating systems

- 12.4.3 THERMOSTATS AND SENSORS

- 12.4.3.1 Thermostats and sensors utilized to monitor and maintain floor temperature

13 APPENDIX

- 13.1 INSIGHTS OF INDUSTRY EXPERTS

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 CUSTOMIZATION OPTIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS