|

|

市場調査レポート

商品コード

1105480

産業用蒸発器の世界市場:構造の種類別 (シェル・チューブ型、プレート型)・最終用途産業別 (食品・飲料、医薬品、化学・石油化学、自動車)・機能性別 (流下膜式、上昇膜式)・地域別の将来予測 (2027年まで)Industrial Evaporators Market by Construction Type (Shell & Tube, Plate), End-use Industry (Food & Beverage, Pharmaceutical, Chemical & Petrochemical, Automotive), Functionality (Falling Film, Rising Film) & Region - Global Forecast to 2027 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 産業用蒸発器の世界市場:構造の種類別 (シェル・チューブ型、プレート型)・最終用途産業別 (食品・飲料、医薬品、化学・石油化学、自動車)・機能性別 (流下膜式、上昇膜式)・地域別の将来予測 (2027年まで) |

|

出版日: 2022年07月19日

発行: MarketsandMarkets

ページ情報: 英文 203 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

産業用蒸発器の市場は、2022年の187億米ドルから2027年には237億米ドルへと、2022年から2027年までCAGR4.8%で成長すると予測されます。

産業用蒸発器の世界市場は、食品・飲料産業の成長や医薬品支出の増加、各地域でのZLDシステムの需要増加などの主要因によって牽引されています。

"構造の種類別では、プレート型蒸発器セグメントが2022年から2027年にかけて産業用蒸発器市場の最速成長セグメントとなる"

構造の種類別では、プレート型蒸発器が予測期間中に最も急成長するセグメントと推定されます。プレート型蒸発器は洗浄が容易で、高い衛生要件を満たしているため、乳製品、醸造所、食品加工用途に最適です。また、プレート型蒸発器は、シェル・チューブ型蒸発器と比較して様々な利点があります。そのため、多くの産業でプレート型蒸発器への需要が高まっています。

"機能別では、自己蒸気機械圧縮 (MVR) 分野が予測期間中に最も高いCAGRを記録する"

機能性では、自己蒸気機械圧縮が予測期間中に最も高いCAGRを記録すると予測されています。自己蒸気機械圧縮型蒸発器は、蒸気コストが高い地域での使用に最適です。また、エネルギー効率の高い蒸発器であるため、熱に敏感な材料に使用することができます。

"最終用途産業別では、2022年から2027年にかけて、食品・飲料セグメントが産業用蒸発器市場の最速成長セグメントとなる"

最終用途産業別では、食品・飲料分野が予測期間中に最も急成長する分野と推定されます。食品・飲料産業は、最も急速に成長している産業の1つであり、様々な食品・飲料の処理に蒸発器を使用しています。加工中に効果的な蒸発が行われないと、粘度の上昇や製品の不安定化を引き起こし、乾燥がより複雑になったり、最終製品にダメージを与える可能性があります。

"アジア太平洋の産業用蒸発器は、予測期間中に最も高いCAGRを記録する"

アジア太平洋は、2022年から2027年にかけて、産業用蒸発器市場で最も高いCAGRを記録すると予測されています。この地域は、さまざまな最終用途産業からの需要増加により、産業用蒸発器の需要が高いです。

目次

第1章 イントロダクション

第2章 調査方法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概略

- イントロダクション

- 市場力学

- ポーターのファイブフォース分析

- バリューチェーン分析

- 産業用蒸発器市場のエコシステム

- 特許分析

- ケーススタディ分析

- 主要な会議とイベント (2021年~2022年)

- 規制状況

- 技術分析

- 動向/混乱の影響

第6章 産業用蒸発器市場:構造の種類別

- イントロダクション

- シェル・チューブ型蒸発器

- プレート型蒸発器

第7章 産業用蒸発器市場:機能別

- イントロダクション

- 流下膜式蒸発器

- 上昇膜式蒸発器

- 強制循環式蒸発器

- 攪拌薄膜蒸発器

- 自己蒸気機械圧縮(MVR)型蒸発器

- その他

第8章 産業用蒸発器市場:最終用途産業別

- イントロダクション

- 医薬品

- 化学・石油化学

- エレクトロニクス・半導体

- パルプ・製紙

- 飲食品

- 自動車

- その他

第9章 産業用蒸発器市場:地域別

- イントロダクション

- アジア太平洋地域

- 中国

- 韓国

- 日本

- インド

- マレーシア

- オーストラリア

- 他のアジア太平洋諸国

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- ロシア

- フランス

- イタリア

- スペイン

- 他の欧州諸国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- 他の中東・アフリカ諸国

- 南米

- アルゼンチン

- ブラジル

- 他の南米諸国

第10章 競合情勢

- 概要

- 主要企業の戦略

- 市場シェア・収益の分析

- 産業用蒸発器の市場シェア分析

- 産業用蒸発器市場:大手企業の収益分析

- 競合情勢マッピング (2020年)

- 競合ベンチマーキング

- 製品ポートフォリオの強み

- 事業戦略の優秀性

- 中小企業のマトリックス (2020年)

- 市場の主な動向

第11章 企業プロファイル

- 主要企業

- VEOLIA WATER TECHNOLOGIES

- SUMITOMO HEAVY INDUSTRIES, LTD.

- SPX FLOW INC.

- JEOL LTD.

- CONDORCHEM ENVITECH

- ECO-TECHNO S.R.L.

- SUEZ WATER TECHNOLOGIES & SOLUTIONS

- GEA GROUP AG

- H2O GMBH

- DE DIETRICH PROCESS SYSTEMS

- BUCHER INDUSTRIES AG

- ALFA LAVAL

- SASAKURA ENGINEERING CO., LTD.

- PRAJ INDUSTRIES LTD.

- SANSHIN MFG. CO., LTD.

- APOLLOXSTILL

- COILMASTER CORPORATION

- COLMAC COIL MANUFACTURING, INC.

- EQUIPMENT MANUFACTURING CORPORATION

- IGEFA WEINBRENNER ENERGY SOLUTIONS GMBH

- その他の企業

- LENNTECH

- SALTWORKS TECHNOLOGIES INC.

- NOL-TEC EUROPE S.R.L.

- ZHEJIANG TAIKANG EVAPORATOR CO., LTD

- BELMAR TECHNOLOGIES LTD.

- HEBEI LEHENG ENERGY SAVING EQUIPMENT CO., LTD.

- UNITOP AQUACARE LTD.

- 3V TECH S.P.A.

- VILOKAN RECYCLING TECH

- SAMSCO CORPORATION

- 3R TECHNOLOGY

- KOVOFINIS

- ENCON EVAPORATORS

- S.A.I.T.A. SRL

- RELCO LLC

- SCHULZ+PARTNER GMBH

- SMI EVAPORATIVE SOLUTIONS

- KMU LOFT CLEANWATER GMBH

第12章 付録

The industrial evaporators market is projected to grow from USD 18.7 billion in 2022 to USD 23.7 billion by 2027, at a CAGR of 4.8% from 2022 to 2027. The global market for industrial evaporators are driven by major factors such as growth in food & beverage industry, increasing pharmaceutical spending and increasing demand of ZLD systems across various regions.

"By construction type, the plate evaporators segment is estimated to be the fastest-growing segment of industrial evaporators market during 2022 to 2027"

Based on construction type, the plate evaporators is estimated to be the fastest growing segment during the forecast period. The plate evaporators are easy to clean and meet high hygiene requirements that makes it ideal for dairy, brewery, and food-processing application. Plate evaporators has various advantages compared to shell & tube evaporators. The demand of many end-use industries is shifting to plate evaporators.

"The mechanical vapor recompression segment in functionality is projected to register the highest CAGR during the forecast period."

Based on functionality, the mechanical vapor recompression is projected to register the highest CAGR during the forecast period. Mechanical vapor recompression evaporators are ideal to be used in area where steam cost is high. These are energy efficient evaporators are can be used for heat sensitive materials.

"By end-use industry, the food & beverage segment is estimated to be the fastest-growing segment of industrial evaporators market during 2022 to 2027"

Based on end-use industry, the food & beverage is estimated to be the fastest-growing segment during the forecast period. Food & beverage industry is one of the fastest growing industry and uses evaporators in various food & beverage processing. Ineffective evaporation during processing can cause increased viscosity and product instability, making drying more complex or potentially causing damage to the end product.

The industrial evaporators in Asia Pacific region is projected to witness the highest CAGR during the forecast period."

Asia Pacific region is projected to register the highest CAGR in the industrial evaporators market from 2022 to 2027. Asia Pacific is one of the key market for industrial evaporators. The region has high demand for the industrial evaporatots due to rising demand from various end use industries.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1 - 40%, Tier 2 - 20%, and Tier 3 - 40%

- By Designation: C-level Executives - 10%, Directors - 70%, and Others - 20%

- By Region: Asia Pacific - 25%, North America - 20%, Europe - 45%, South America-5%, and Middle East & Africa- 5%

The industrial evaporators report is dominated by players, such as Veolia Water Technologies (France), Sumitomo Heavy Industries, Ltd. (Japan), SPX Flow Inc. (US), JEOL Ltd. (Japan), SUEZ Water Technologies & Solutions (France), GEA Group AG (Germany), De Dietrich Process Systems (France), Coilmaster Corporation (US), Colmac Coil Manufacturing, Inc. (US), Saltworks Technologies Inc. (Canada), Belmar Technologies Ltd. (England), Sasakura Engineering Co., Ltd. (Japan), Praj Industries Ltd. (India), SMI Evaporative Solutions (US), Alfa Laval (Sweden), RELCO LLC (US), and Hebei Leheng Energy Saving Equipment Co., Ltd. (China)

Research Coverage:

The report defines, segments, and projects the size of the industrial evaporators market based on construction type, functionality, end-use industry and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as agreements, acquisitions, contracts and partnerships, undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help the market leaders/new entrants in the market by providing them the closest approximations of revenue numbers of the industrial evaporators market and its segments. This report is also expected to help stakeholders obtain an improved understanding of the competitive landscape of the market, gain insights to improve the position of their businesses and make suitable go-to-market strategies. It also enables stakeholders to understand the pulse of the market and provide them information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVES OF THE STUDY

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS & EXCLUSIONS

- TABLE 1 INDUSTRIAL EVAPORATORS MARKET, BY FUNCTIONALITY: INCLUSIONS & EXCLUSIONS

- TABLE 2 INDUSTRIAL EVAPORATORS MARKET, BY END-USE INDUSTRY: INCLUSIONS & EXCLUSIONS

- TABLE 3 INDUSTRIAL EVAPORATORS MARKET, BY REGION: INCLUSIONS & EXCLUSIONS

- 1.4 MARKET SCOPE

- 1.4.1 MARKETS COVERED

- FIGURE 1 INDUSTRIAL EVAPORATORS MARKET SEGMENTATION

- 1.4.2 REGIONS COVERED

- 1.4.3 YEARS CONSIDERED

- 1.5 CURRENCY

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 INDUSTRIAL EVAPORATORS MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Participating companies in primary research

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primary interviews

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 3 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- 2.3 BASE NUMBER CALCULATION

- FIGURE 5 MARKET SIZE ESTIMATION (SUPPLY SIDE): INDUSTRIAL EVAPORATORS MARKET

- 2.4 DATA TRIANGULATION

- FIGURE 6 INDUSTRIAL EVAPORATORS MARKET: DATA TRIANGULATION

- 2.5 ASSUMPTIONS

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- TABLE 4 INDUSTRIAL EVAPORATORS MARKET SNAPSHOT, 2022 VS. 2027

- FIGURE 7 SHELL & TUBE EVAPORATORS ACCOUNTED FOR LARGER SHARE OF INDUSTRIAL EVAPORATORS MARKET IN 2021

- FIGURE 8 FALLING FILM EVAPORATORS ACCOUNTED FOR LARGEST MARKET SHARE IN 2021

- FIGURE 9 FOOD & BEVERAGE SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2021

- FIGURE 10 ASIA PACIFIC TO LEAD INDUSTRIAL EVAPORATORS MARKET IN 2021

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL EVAPORATORS MARKET

- FIGURE 11 RISING DEMAND FROM VARIOUS MANUFACTURING INDUSTRIES TO DRIVE MARKET GROWTH

- 4.2 INDUSTRIAL EVAPORATORS MARKET, BY REGION

- FIGURE 12 ASIA PACIFIC TO GROW AT HIGHEST RATE DURING FORECAST PERIOD

- 4.3 ASIA PACIFIC INDUSTRIAL EVAPORATORS MARKET, BY CONSTRUCTION TYPE AND COUNTRY

- FIGURE 13 SHELL & TUBE EVAPORATORS SEGMENT AND CHINA TO LEAD ASIA PACIFIC INDUSTRIAL EVAPORATORS MARKET

- 4.4 INDUSTRIAL EVAPORATORS MARKET: MAJOR COUNTRIES

- FIGURE 14 CHINA TO GROW AT HIGHEST RATE DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 15 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN INDUSTRIAL EVAPORATORS MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Growth in food & beverage industry

- FIGURE 16 REVENUE GROWTH IN FOOD & BEVERAGE INDUSTRY FOR NEXT FIVE YEARS

- 5.2.1.2 Rapid adoption of ZLD and MLD in global manufacturing industry

- 5.2.1.3 Increasing pharmaceutical R&D spending

- TABLE 5 R&D SPENDING OF LEADING PHARMACEUTICAL COMPANIES IN 2020

- 5.2.2 RESTRAINTS

- 5.2.2.1 High manufacturing and maintenance costs

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Industrialization in developing countries creating opportunities for industrial evaporator manufacturers

- 5.2.3.2 Rise in demand for desalination due to water crisis

- FIGURE 17 NUMBER OF DESALINATION PLANTS IN 2019

- 5.2.4 CHALLENGES

- 5.2.4.1 Shortage of skilled workforce

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 18 PORTER'S FIVE FORCES ANALYSIS: INDUSTRIAL EVAPORATORS MARKET

- TABLE 6 INDUSTRIAL EVAPORATORS MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 BARGAINING POWER OF SUPPLIERS

- 5.3.2 BARGAINING POWER OF BUYERS

- 5.3.3 THREAT OF SUBSTITUTES

- 5.3.4 THREAT OF NEW ENTRANTS

- 5.3.5 DEGREE OF COMPETITION

- 5.4 VALUE CHAIN ANALYSIS

- FIGURE 19 VALUE CHAIN ANALYSIS: HIGHEST VALUE ADDED DURING MANUFACTURING PHASE

- 5.5 ECOSYSTEM FOR INDUSTRIAL EVAPORATORS MARKET

- FIGURE 20 ECOSYSTEM MAP OF INDUSTRIAL EVAPORATORS MARKET

- TABLE 7 INDUSTRIAL EVAPORATORS MARKET: ECOSYSTEM

- 5.6 PATENT ANALYSIS

- 5.6.1 METHODOLOGY

- 5.6.2 PATENT PUBLICATION TRENDS

- FIGURE 21 NUMBER OF PATENTS YEAR-WISE DURING LAST TEN YEARS

- 5.6.3 INSIGHTS

- 5.6.4 JURISDICTION ANALYSIS

- FIGURE 22 CHINA ACCOUNTED FOR HIGHEST NUMBER OF PATENTS

- 5.6.5 TOP COMPANIES/APPLICANTS

- FIGURE 23 TOP TEN COMPANIES/APPLICANTS WITH HIGHEST NUMBER OF PATENTS

- 5.6.5.1 LIST OF MAJOR PATENTS

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 MULTIPLE-EFFECT EVAPORATORS: ENERGY INTEGRATION STUDY

- 5.7.1.1 Objective

- 5.7.1.2 Solution statement

- 5.7.2 EFFECT OF FOULING ON FALLING FILM EVAPORATOR

- 5.7.2.1 Objective

- 5.7.2.2 Solution statement

- 5.7.1 MULTIPLE-EFFECT EVAPORATORS: ENERGY INTEGRATION STUDY

- 5.8 KEY CONFERENCES & EVENTS IN 2021-2022

- TABLE 8 INDUSTRIAL EVAPORATORS MARKET: DETAILED LIST OF CONFERENCES & EVENTS

- 5.9 REGULATORY LANDSCAPE

- TABLE 9 STANDARDS FOR INDUSTRIAL EVAPORATORS

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 EVAPORATOR TECHNOLOGY

- 5.10.1.1 Falling film evaporators

- 5.10.1.2 Rising film evaporators

- 5.10.1.3 Forced circulation evaporators

- 5.10.1.4 Agitated thin film evaporators

- 5.10.1.5 Mechanical vapor recompression

- 5.10.1 EVAPORATOR TECHNOLOGY

- 5.11 TRENDS/DISRUPTION IMPACT

- FIGURE 24 REVENUE SHIFTS AND NEW REVENUE POCKETS FOR INDUSTRIAL EVAPORATORS MARKET

6 INDUSTRIAL EVAPORATORS MARKET, BY CONSTRUCTION TYPE

- 6.1 INTRODUCTION

- FIGURE 25 INDUSTRIAL EVAPORATORS MARKET, BY CONSTRUCTION TYPE, 2022-2027(USD MILLION)

- TABLE 10 INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- 6.2 SHELL & TUBE EVAPORATORS

- 6.2.1 TO CONTINUE THEIR DOMINANCE IN EVAPORATORS MARKET

- TABLE 11 SHELL & TUBE EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

- 6.3 PLATE EVAPORATORS

- 6.3.1 HIGH DEMAND FROM FOOD & BEVERAGE INDUSTRY TO DRIVE MARKET

- TABLE 12 PLATE EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

7 INDUSTRIAL EVAPORATORS MARKET, BY FUNCTIONALITY

- 7.1 INTRODUCTION

- FIGURE 26 INDUSTRIAL EVAPORATORS MARKET, BY FUNCTIONALITY, 2022-2027(USD MILLION)

- TABLE 13 INDUSTRIAL EVAPORATORS MARKET SIZE, BY FUNCTIONALITY, 2019-2027 (USD MILLION)

- 7.2 FALLING FILM EVAPORATORS

- 7.2.1 HIGH DEMAND FROM SEVERAL MAJOR INDUSTRIES

- TABLE 14 FALLING FILM EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

- 7.3 RISING FILM EVAPORATORS

- 7.3.1 IDEAL FOR LOW-SCALING FEEDS

- TABLE 15 RISING FILM EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

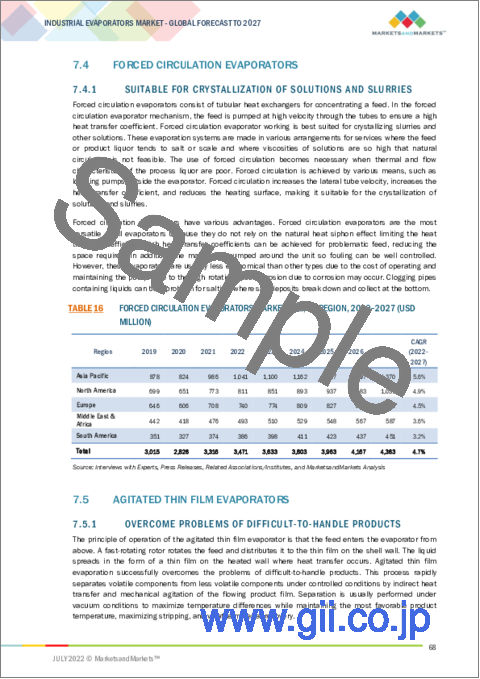

- 7.4 FORCED CIRCULATION EVAPORATORS

- 7.4.1 SUITABLE FOR CRYSTALLIZATION OF SOLUTIONS AND SLURRIES

- TABLE 16 FORCED CIRCULATION EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

- 7.5 AGITATED THIN FILM EVAPORATORS

- 7.5.1 OVERCOME PROBLEMS OF DIFFICULT-TO-HANDLE PRODUCTS

- TABLE 17 AGITATED THIN FILM EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

- 7.6 MECHANICAL VAPOR RECOMPRESSION (MVR)

- 7.6.1 MECHANICAL VAPOR EVAPORATORS CAN BE USED FOR HEAT-SENSITIVE MATERIALS

- TABLE 18 MECHANICAL VAPOR RECOMPRESSION EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

- 7.7 OTHERS

- TABLE 19 OTHER EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

8 INDUSTRIAL EVAPORATORS MARKET, BY END-USE INDUSTRY

- 8.1 INTRODUCTION

- FIGURE 27 INDUSTRIAL EVAPORATORS MARKET, BY END-USE INDUSTRY, 2022-2027(USD MILLION)

- TABLE 20 INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 8.2 PHARMACEUTICAL

- 8.2.1 EXTENSIVE USE OF THIN FILM EVAPORATORS DRIVING SEGMENT GROWTH

- TABLE 21 INDUSTRIAL EVAPORATORS MARKET SIZE IN PHARMACEUTICAL END-USE INDUSTRY, BY REGION, 2019-2027 (USD MILLION)

- 8.3 CHEMICAL & PETROCHEMICAL

- 8.3.1 WIDE USE OF VARIOUS EVAPORATION PROCESSES

- TABLE 22 INDUSTRIAL EVAPORATORS MARKET SIZE IN CHEMICAL & PETROCHEMICAL END-USE INDUSTRY, BY REGION, 2019-2027 (USD MILLION)

- 8.4 ELECTRONICS & SEMICONDUCTOR

- 8.4.1 PRIMARY APPLICATION OF EVAPORATORS FOR METAL DEPOSITION

- TABLE 23 INDUSTRIAL EVAPORATORS MARKET SIZE IN ELECTRONICS & SEMICONDUCTOR END-USE INDUSTRY, BY REGION, 2019-2027 (USD MILLION)

- 8.5 PULP & PAPER

- 8.5.1 USES OF EVAPORATORS TO CONCENTRATE BLACK LIQUOR

- TABLE 24 INDUSTRIAL EVAPORATORS MARKET SIZE IN PULP & PAPER END-USE INDUSTRY, BY REGION, 2019-2027 (USD MILLION)

- 8.6 FOOD & BEVERAGE

- 8.6.1 ONE OF THE LEADING MARKETS FOR EVAPORATORS

- TABLE 25 INDUSTRIAL EVAPORATORS MARKET SIZE IN FOOD & BEVERAGE END-USE INDUSTRY, BY REGION, 2019-2027 (USD MILLION)

- 8.7 AUTOMOTIVE

- 8.7.1 USE OF MULTIPLE-EFFECT EVAPORATORS FOR INDUSTRIAL PROCESSES

- TABLE 26 INDUSTRIAL EVAPORATORS MARKET SIZE IN AUTOMOTIVE END-USE INDUSTRY, BY REGION, 2019-2027 (USD MILLION)

- 8.8 OTHERS

- TABLE 27 INDUSTRIAL EVAPORATORS MARKET SIZE IN OTHER END-USE INDUSTRIES, BY REGION, 2019-2027 (USD MILLION)

9 INDUSTRIAL EVAPORATORS MARKET, BY REGION

- 9.1 INTRODUCTION

- FIGURE 28 ASIA PACIFIC TO SHOW HIGHEST GROWTH

- TABLE 28 INDUSTRIAL EVAPORATORS MARKET SIZE, BY REGION, 2019-2027 (USD MILLION)

- 9.2 ASIA PACIFIC

- FIGURE 29 ASIA PACIFIC: INDUSTRIAL EVAPORATORS MARKET SNAPSHOT

- TABLE 29 ASIA PACIFIC: INDUSTRIAL EVAPORATORS MARKET SIZE, BY COUNTRY, 2019-2027 (USD MILLION)

- TABLE 30 ASIA PACIFIC: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 31 ASIA PACIFIC: INDUSTRIAL EVAPORATORS MARKET SIZE, BY FUNCTIONALITY, 2019-2027 (USD MILLION)

- TABLE 32 ASIA PACIFIC: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.2.1 CHINA

- 9.2.1.1 Manufacturing hub leading to demand for industrial evaporators

- TABLE 33 CHINA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 34 CHINA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.2.2 SOUTH KOREA

- 9.2.2.1 Growing electronics and automobile sectors to create opportunities for industrial evaporator manufacturers

- TABLE 35 SOUTH KOREA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 36 SOUTH KOREA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.2.3 JAPAN

- 9.2.3.1 Leading end-use industries to create demand for industrial evaporators

- TABLE 37 JAPAN: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 38 JAPAN: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.2.4 INDIA

- 9.2.4.1 Initiative in food & beverage industries to generate demand for industrial evaporators

- TABLE 39 INDIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 40 INDIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.2.5 MALAYSIA

- 9.2.5.1 Expanding manufacturing sector to create opportunities for industrial evaporator manufacturers

- TABLE 41 MALAYSIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 42 MALAYSIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.2.6 AUSTRALIA

- 9.2.6.1 High demand for industrial evaporators in food & beverage sector

- TABLE 43 AUSTRALIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 44 AUSTRALIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.2.7 REST OF ASIA PACIFIC

- TABLE 45 REST OF ASIA PACIFIC: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 46 REST OF ASIA PACIFIC: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.3 NORTH AMERICA

- FIGURE 30 NORTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SNAPSHOT

- TABLE 47 NORTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY COUNTRY, 2019-2027 (USD MILLION)

- TABLE 48 NORTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 49 NORTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY FUNCTIONALITY, 2019-2027 (USD MILLION)

- TABLE 50 NORTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.3.1 US

- 9.3.1.1 Pharmaceutical growth to create demand for industrial evaporators

- TABLE 51 US: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 52 US: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.3.2 CANADA

- 9.3.2.1 Rising demand for industrial evaporators in automotive industry

- TABLE 53 CANADA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 54 CANADA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.3.3 MEXICO

- 9.3.3.1 Electronics industry to create demand for pure industrial water

- TABLE 55 MEXICO: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 56 MEXICO: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.4 EUROPE

- FIGURE 31 EUROPE: INDUSTRIAL EVAPORATORS MARKET SNAPSHOT

- TABLE 57 EUROPE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY COUNTRY, 2019-2027 (USD MILLION)

- TABLE 58 EUROPE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 59 EUROPE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY FUNCTIONALITY, 2019-2027 (USD MILLION)

- TABLE 60 EUROPE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.4.1 GERMANY

- 9.4.1.1 Pharmaceutical production and automotive industry to support market growth

- TABLE 61 GERMANY: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 62 GERMANY: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.4.2 UK

- 9.4.2.1 Rising demand for industrial evaporators in electrical and electronics industry

- TABLE 63 UK: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 64 UK: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.4.3 RUSSIA

- 9.4.3.1 Growth in food & beverage industry increasing demand

- TABLE 65 RUSSIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 66 RUSSIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.4.4 FRANCE

- 9.4.4.1 Water treatment infrastructure driving demand for industrial evaporators

- TABLE 67 FRANCE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 68 FRANCE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.4.5 ITALY

- 9.4.5.1 Growth in pharmaceutical and automotive industries to increase demand

- TABLE 69 ITALY: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 70 ITALY: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.4.6 SPAIN

- 9.4.6.1 Growth in food & beverage industry supporting market

- TABLE 71 SPAIN: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 72 SPAIN: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.4.7 REST OF EUROPE

- TABLE 73 REST OF EUROPE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 74 REST OF EUROPE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.5 MIDDLE EAST & AFRICA

- TABLE 75 MIDDLE EAST & AFRICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY COUNTRY, 2019-2027 (USD MILLION)

- TABLE 76 MIDDLE EAST & AFRICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 77 MIDDLE EAST & AFRICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY FUNCTIONALITY, 2019-2027 (USD MILLION)

- TABLE 78 MIDDLE EAST & AFRICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.5.1 SAUDI ARABIA

- 9.5.1.1 Growth in chemical industry to create demand for industrial evaporators

- TABLE 79 SAUDI ARABIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 80 SAUDI ARABIA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.5.2 UAE

- 9.5.2.1 Growing industrial evaporators demand in manufacturing sector

- TABLE 81 UAE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 82 UAE: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.5.3 SOUTH AFRICA

- 9.5.3.1 Biggest industrial sectors to create demand for industrial evaporators

- TABLE 83 SOUTH AFRICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 84 SOUTH AFRICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.5.4 REST OF THE MIDDLE EAST & AFRICA

- TABLE 85 REST OF MIDDLE EAST & AFRICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 86 REST OF MIDDLE EAST & AFRICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.6 SOUTH AMERICA

- TABLE 87 SOUTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY COUNTRY, 2019-2027 (USD MILLION)

- TABLE 88 SOUTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 89 SOUTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY FUNCTIONALITY, 2019-2027 (USD MILLION)

- TABLE 90 SOUTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.6.1 ARGENTINA

- 9.6.1.1 Growing food & beverage and electronics industries to boost market growth

- TABLE 91 ARGENTINA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 92 ARGENTINA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.6.2 BRAZIL

- 9.6.2.1 Automobile industries to create demand for industrial evaporators

- TABLE 93 BRAZIL: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 94 BRAZIL: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

- 9.7 REST OF SOUTH AMERICA

- TABLE 95 REST OF SOUTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY CONSTRUCTION TYPE, 2019-2027 (USD MILLION)

- TABLE 96 REST OF SOUTH AMERICA: INDUSTRIAL EVAPORATORS MARKET SIZE, BY END-USE INDUSTRY, 2019-2027 (USD MILLION)

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES

- TABLE 97 OVERVIEW OF STRATEGIES ADOPTED BY INDUSTRIAL EVAPORATORS MANUFACTURERS

- 10.3 MARKET SHARE AND REVENUE ANALYSIS

- 10.3.1 MARKET SHARE ANALYSIS OF INDUSTRIAL EVAPORATORS

- FIGURE 32 MARKET SHARE ANALYSIS

- 10.3.2 REVENUE ANALYSIS OF TOP PLAYERS IN INDUSTRIAL EVAPORATORS MARKET

- FIGURE 33 TOP PLAYERS - REVENUE ANALYSIS (2016-2020)

- 10.4 COMPETITIVE LANDSCAPE MAPPING, 2020

- 10.4.1 STAR

- 10.4.2 EMERGING LEADERS

- 10.4.3 PERVASIVE

- 10.4.4 PARTICIPANTS

- FIGURE 34 INDUSTRIAL EVAPORATORS MARKET: COMPETITIVE LANDSCAPE MAPPING

- 10.5 COMPETITIVE BENCHMARKING

- 10.5.1 STRENGTH OF PRODUCT PORTFOLIO

- FIGURE 35 PRODUCT PORTFOLIO ANALYSIS OF TOP PLAYERS IN INDUSTRIAL EVAPORATORS MARKET

- 10.5.2 BUSINESS STRATEGY EXCELLENCE

- FIGURE 36 BUSINESS STRATEGY EXCELLENCE OF TOP PLAYERS IN INDUSTRIAL EVAPORATORS MARKET

- 10.6 SME MATRIX, 2020

- 10.6.1 PROGRESSIVE COMPANIES

- 10.6.2 DYNAMIC COMPANIES

- 10.6.3 RESPONSIVE COMPANIES

- 10.6.4 STARTING BLOCKS

- FIGURE 37 INDUSTRIAL EVAPORATORS MARKET: COMPETITIVE LEADERSHIP MAPPING OF EMERGING COMPANIES

- TABLE 98 COMPANY END-USE INDUSTRY FOOTPRINT, 2021

- TABLE 99 COMPANY REGION FOOTPRINT, 2021

- TABLE 100 COMPANY APPLICATION FOOTPRINT, 2020

- TABLE 101 INDUSTRIAL EVAPORATORS: DETAILED LIST OF KEY STARTUP/SMES

- TABLE 102 INDUSTRIAL EVAPORATORS: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- 10.7 KEY MARKET DEVELOPMENTS

- TABLE 103 INDUSTRIAL EVAPORATORS MARKET: NEW PRODUCT LAUNCH, 2016-2022

- TABLE 104 INDUSTRIAL EVAPORATORS MARKET: DEALS, 2016-2022

11 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, MnM View Right to win, Strategic choices made, Weaknesses and competitive threats) **

- 11.1 MAJOR PLAYERS

- 11.1.1 VEOLIA WATER TECHNOLOGIES

- TABLE 105 VEOLIA WATER TECHNOLOGIES: COMPANY OVERVIEW

- FIGURE 38 VEOLIA WATER TECHNOLOGIES: COMPANY SNAPSHOT

- 11.1.2 SUMITOMO HEAVY INDUSTRIES, LTD.

- TABLE 106 SUMITOMO HEAVY INDUSTRIES, LTD.: COMPANY OVERVIEW

- FIGURE 39 SUMITOMO HEAVY INDUSTRIES, LTD.: COMPANY SNAPSHOT

- 11.1.3 SPX FLOW INC.

- TABLE 107 SPX FLOW INC.: COMPANY OVERVIEW

- FIGURE 40 SPX FLOW INC.: COMPANY SNAPSHOT

- 11.1.4 JEOL LTD.

- TABLE 108 JEOL LTD.: COMPANY OVERVIEW

- FIGURE 41 JEOL LTD.: COMPANY SNAPSHOT

- 11.1.5 CONDORCHEM ENVITECH

- TABLE 109 CONDORCHEM ENVITECH: COMPANY OVERVIEW

- 11.1.6 ECO-TECHNO S.R.L.

- TABLE 110 ECO-TECHNO S.R.L.: COMPANY OVERVIEW

- 11.1.7 SUEZ WATER TECHNOLOGIES & SOLUTIONS

- TABLE 111 SUEZ WATER TECHNOLOGIES & SOLUTIONS: COMPANY OVERVIEW

- FIGURE 42 SUEZ WATER TECHNOLOGIES & SOLUTIONS: COMPANY SNAPSHOT

- 11.1.8 GEA GROUP AG

- TABLE 112 GEA GROUP AG: COMPANY OVERVIEW

- FIGURE 43 GEA GROUP AG: COMPANY SNAPSHOT

- 11.1.9 H2O GMBH

- TABLE 113 H2O GMBH: COMPANY OVERVIEW

- 11.1.10 DE DIETRICH PROCESS SYSTEMS

- TABLE 114 DE DIETRICH PROCESS SYSTEMS: COMPANY OVERVIEW

- 11.1.11 BUCHER INDUSTRIES AG

- TABLE 115 BUCHER INDUSTRIES AG: COMPANY OVERVIEW

- FIGURE 44 BUCHER INDUSTRIES AG: COMPANY SNAPSHOT

- 11.1.12 ALFA LAVAL

- TABLE 116 ALFA LAVAL: COMPANY OVERVIEW

- FIGURE 45 ALFA LAVAL: COMPANY SNAPSHOT

- 11.1.13 SASAKURA ENGINEERING CO., LTD.

- TABLE 117 SASAKURA ENGINEERING CO., LTD.: COMPANY OVERVIEW

- FIGURE 46 SASAKURA ENGINEERING CO., LTD.: COMPANY SNAPSHOT

- 11.1.14 PRAJ INDUSTRIES LTD.

- TABLE 118 PRAJ INDUSTRIES LTD.: COMPANY OVERVIEW

- FIGURE 47 PRAJ INDUSTRIES LTD.: COMPANY SNAPSHOT

- 11.1.15 SANSHIN MFG. CO., LTD.

- TABLE 119 SANSHIN MFG. CO., LTD: COMPANY OVERVIEW

- 11.1.16 APOLLOXSTILL

- TABLE 120 APOLLOXSTILL: COMPANY OVERVIEW

- 11.1.17 COILMASTER CORPORATION

- TABLE 121 COILMASTER CORPORATION: COMPANY OVERVIEW

- 11.1.18 COLMAC COIL MANUFACTURING, INC.

- TABLE 122 COLMAC COIL MANUFACTURING, INC.: COMPANY OVERVIEW

- 11.1.19 EQUIPMENT MANUFACTURING CORPORATION

- TABLE 123 EQUIPMENT MANUFACTURING CORPORATION: COMPANY OVERVIEW

- 11.1.20 IGEFA WEINBRENNER ENERGY SOLUTIONS GMBH

- TABLE 124 IGEFA WEINBRENNER ENERGY SOLUTIONS GMBH: COMPANY OVERVIEW

- 11.2 OTHER PLAYERS

- 11.2.1 LENNTECH

- TABLE 125 LENNTECH: COMPANY OVERVIEW

- 11.2.2 SALTWORKS TECHNOLOGIES INC.

- TABLE 126 SALTWORKS TECHNOLOGIES INC.: COMPANY OVERVIEW

- 11.2.3 NOL-TEC EUROPE S.R.L.

- TABLE 127 NOL-TEC EUROPE S.R.L.: COMPANY OVERVIEW

- 11.2.4 ZHEJIANG TAIKANG EVAPORATOR CO., LTD

- TABLE 128 ZHEJIANG TAIKANG EVAPORATOR CO., LTD.: COMPANY OVERVIEW

- 11.2.5 BELMAR TECHNOLOGIES LTD.

- TABLE 129 BELMAR TECHNOLOGIES LTD.: COMPANY OVERVIEW

- 11.2.6 HEBEI LEHENG ENERGY SAVING EQUIPMENT CO., LTD.

- TABLE 130 HEBEI LEHENG ENERGY SAVING EQUIPMENT CO., LTD.: COMPANY OVERVIEW

- 11.2.7 UNITOP AQUACARE LTD.

- TABLE 131 UNITOP AQUACARE LTD.: COMPANY OVERVIEW

- 11.2.8 3V TECH S.P.A.

- TABLE 132 3V TECH S.P.A.: COMPANY OVERVIEW

- 11.2.9 VILOKAN RECYCLING TECH

- TABLE 133 VILOKAN RECYCLING TECH: COMPANY OVERVIEW

- 11.2.10 SAMSCO CORPORATION

- TABLE 134 SAMSCO CORPORATION: COMPANY OVERVIEW

- 11.2.11 3R TECHNOLOGY

- TABLE 135 3R TECHNOLOGY: COMPANY OVERVIEW

- 11.2.12 KOVOFINIS

- TABLE 136 KOVOFINIS: COMPANY OVERVIEW

- 11.2.13 ENCON EVAPORATORS

- TABLE 137 ENCON EVAPORATORS: COMPANY OVERVIEW

- 11.2.14 S.A.I.T.A. SRL

- TABLE 138 S.A.I.T.A. SRL COMPANY OVERVIEW

- 11.2.15 RELCO LLC

- TABLE 139 RELCO LLC: COMPANY OVERVIEW

- 11.2.16 SCHULZ+PARTNER GMBH

- TABLE 140 SCHULZ+PARTNER GMBH: COMPANY OVERVIEW

- 11.2.17 SMI EVAPORATIVE SOLUTIONS

- TABLE 141 SMI EVAPORATIVE SOLUTIONS: COMPANY OVERVIEW

- 11.2.18 KMU LOFT CLEANWATER GMBH

- TABLE 142 KMU LOFT CLEANWATER GMBH: COMPANY OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, MnM View, Right to win, Strategic choices made, Weaknesses and competitive threats might not be captured in case of unlisted companies.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGE STORE: MARKETSANDMARKETS SUBSCRIPTION PORTAL

- 12.3 AVAILABLE CUSTOMIZATIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS