|

|

市場調査レポート

商品コード

1099312

端子台市場:タイプ別(バリア・バリアストリップ、セクション端子台、PCBマウント端子台、電源端子台)、産業別(HVACシステム、産業制御、プロセス制御機器)-2027年までの世界予測Terminal Block Market by Type (Barriers or Barrier Strips, Sectional Terminal Blocks, PCB Mount Terminal Blocks, Power Terminal Blocks), Industry (HVAC Systems, Industrial Controls, Process Control Instruments) - Global Forecast to 2027 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 端子台市場:タイプ別(バリア・バリアストリップ、セクション端子台、PCBマウント端子台、電源端子台)、産業別(HVACシステム、産業制御、プロセス制御機器)-2027年までの世界予測 |

|

出版日: 2022年07月06日

発行: MarketsandMarkets

ページ情報: 英文 219 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

端子台の市場規模は、2022年の39億米ドルから2027年には52億米ドルに拡大すると予測されており、2022年から2027年までのCAGRは5.7%と予想されています。

端子台市場の成長の主な要因は、さまざまな産業からのPCB端子台に対する需要の急増と、端子台で展開される接続技術に見られる進歩であり、したがって産業にさまざまな利点を提供することです。

"PCBマウント端子台は2022年から2027年にかけて高い成長率が見込まれる"

PCBマウント端子台は、信頼性の高い接続を提供するモジュール式の絶縁デバイスです。これらの端子台はプリント基板(PCB)に取り付けられ、さまざまなピッチサイズとワイヤサイズでプラグ式と固定式の構成があり、信号、データ、電力を安全に伝送するために使用されます。これらの端子台は、家庭用充電スタンド、流量計、コントローラー、電源など、さまざまな用途で使用されています。現在、PCB端子台には、ワイヤーケージ型、フロントエントリー型、ワイヤープロテクター型など、さまざまなモデルがあります。PCBマウント端子台の絶え間ない進歩により、産業界がより速いスピードでPCBマウント端子台を採用するようになったため、PCBマウント端子台は近年人気を博しているのです。

"2021年、産業用制御機器が最大シェアを占める"

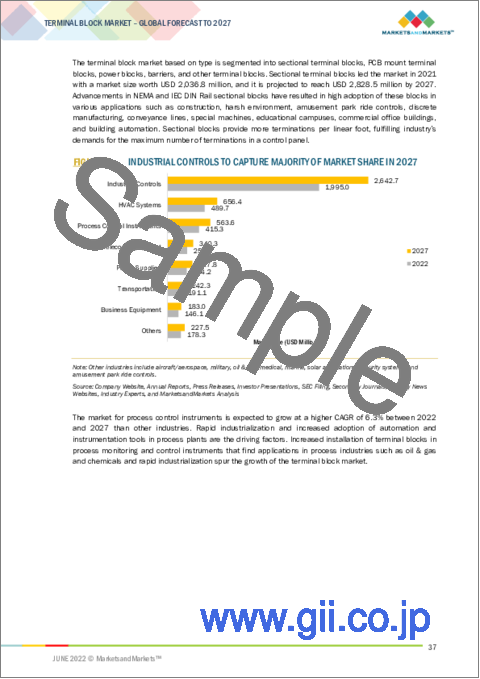

2021年の端子台市場で最大のシェアを占めるのは、産業用制御機器分野です。米国、カナダ、英国、ドイツなどのほとんどの先進国や、中国、インドなどの一部の新興国において、製造装置における自動化装置やインダストリー4.0の採用が増加していることが、世界の産業制御および工場自動化市場の成長を後押ししています。製造装置における高度なツールや技術の使用が増加していることが、端子台の需要を高めています。また、端子台はスイッチギア、機械制御、配電盤、測定器などの産業用機器で一般的に使用されており、産業用制御機器向け端子台市場の成長を加速させています。

"予測期間中、アジア太平洋地域が最大の市場成長率を獲得する見込み"

アジア太平洋地域は、予測期間中、端子台市場の最大の市場成長率を占めると予想されます。急速な都市化と高い可処分所得が、この地域の人々のライフスタイルを向上させています。その結果、プレミアムカー、ハイエンド電子機器、HVACシステムに対する高い需要があります。このため、自動車、通信機器、HVACシステムの各業界から端子台に対する強い需要が生まれています。また、アジア太平洋地域の新興国は、予測期間中に端子台市場に大きく貢献すると思われます。中国、インド、日本、インドネシアでの産業活動の増加が、アジア太平洋地域の端子台市場の成長を牽引しています。

本レポートの主要参加企業のプロファイルの内訳は以下の通りです:

- 企業タイプ別:Tier 1=52%, Tier 2=31%, and Tier 3=17%

- 役職別:C-Level Executives=47%, Directors=31%, and Others=22%

- 地域別:North America=31%, Europe=29%, Asia Pacific=34%, and RoW=06%

端子台市場に参入している主な企業は、WAGO Kontakttechnik GmbH &Co.KG(ドイツ)、TE Connectivity(スイス)、Weidmuller Interface GmbH &Co.KG(ドイツ)、オムロン株式会社(日本)、Eaton Corporation(アイルランド)、PHOENIX CONTACT(ドイツ)、Rockwell Automation, Inc(米国)、Molex, LLC(米国)、Wieland Electric GmbH(ドイツ)などがあります。

調査対象:

この調査レポートは、端子台の世界市場を、タイプ、産業、構造、機能タイプ、接続タイプによる端子台の分類、取り付けタイプ、地域に基づいて調査しています。タイプ別では、バリアまたはバリアストリップ、セクショナル端子台、PCBマウント端子台、パワー端子台、その他の端子台に分類されます。産業別では、ビジネス機器、HVACシステム、電源、産業制御、プロセス制御機器、通信機器、輸送機器、その他の産業に分類されます。端子台の構造、機能タイプ、接続タイプによる分類に基づき、市場は構造と機能に基づく端子台に区分されます。構造および機能には、1段貫通端子台、2段端子台、3段端子台、接地回路端子、断路・ナイフ断路・スイッチ端子台、ヒューズ端子台、熱電対端子、I/O端子、センサー専用端子台があります。一方、接続技術による端子台は、スプリング(ケージクランプ)式端子台、ネジ式端子台、圧接接続式端子台、プッシュイン式端子台、特殊接続(スリップオンプラグン接続、TERMI-POINT接続)などがあります。取り付けタイプにより、市場はDINレールマウントとPCBマウントに分類されます。本レポートは、北米、欧州、アジア太平洋地域、その他の諸国(RoW)の4つの主要地域を対象としています。

レポートを購入する主な利点:

本レポートは、端子台市場を包括的にセグメント化し、全体的な市場規模だけでなく、異なるタイプ、産業、構造、機能タイプ、接続タイプによる端子台の分類、実装タイプ、地域にわたるサブセグメントの規模を最も近似値で提供するものです。

このレポートは、利害関係者が市場の脈動、予想される市場シナリオを理解するのに役立ち、主要な市場促進要因・阻害要因・課題・機会に関する情報を提供します。

また、COVID-19が端子台市場に与える影響を把握するのに役立ちます。

目次

第1章 イントロダクション

- 調査目的

- 市場の定義

- 包含と除外

- 調査範囲

- 対象となる市場

- 考慮される年

- 通貨

- 制限

- 利害関係者

- 変更の概要

第2章 調査手法

- 調査データ

- 二次および1次調査

- 二次データ

- 主要な二次資料のリスト

- 二次資料からの重要なデータ

- 一次データ

- 専門家への一次インタビュー

- 一次資料からの主要なデータ

- 業界の重要な洞察

- 予備選挙の内訳

- 市場規模の見積もり

- ボトムアップアプローチ

- ボトムアップ分析(需要側)でシェアを獲得するためのアプローチ

- トップダウンアプローチ

- トップダウン分析別シェア獲得アプローチ(供給側)

- ボトムアップアプローチ

- 市場の内訳とデータの三角測量

- 研究の仮定

- リスクアセスメント

第3章 エグゼクティブサマリー

第4章 重要考察

- 端子台市場のプレーヤー成長機会

- タイプ別の端子台市場

- 業界別の端子台市場

- 地域別の端子台市場

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- さまざまな業界からのPCB端子台の急増

- 接続技術の継続的な進歩

- 電気通信セクターにおける高度な端子台の実装の拡大

- 電気自動車の採用の増加

- 抑制要因

- アプリケーションに応じて適切な端子台を選択するのが難しい

- 市場機会

- 新興諸国における急速な都市化と工業化

- 超小型端子台の必要性の高まり

- 課題

- 表面実装技術ベースの端子台を開発する際の設計関連の課題

- 促進要因

- バリューチェーン分析

- エコシステム

- 価格分析

- キープレーヤーが提供する端子台のタイプ別の平均販売価格

- 動向のビジネスに影響を与える傾向/混乱

- テクノロジー分析

- プッシュイン接続

- ピアス接続

- 圧着接続

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争力のある競争企業間の敵対関係

- 主要な利害関係者と購入基準

- 購入プロセスの主要な利害関係者

- 購入基準

- ケーススタディ

- PHOENIX CONTACTは、HMIソリューションを使用してI/O端子台を統合することにより、イオンが照明システムをリモートで制御するのに役立ちます

- WAGO別スプリング圧力接続技術により、K-LITEの照明接続が簡単になります

- CONNECTWELLは、ハラマイン高速鉄道が直面する信号中断の問題を、スプリングクランプシリーズの展開で解決します

- CHETTINAD CEMENTのワゴンティプラーアンロードシステムは、CONNECTWELLからの省スペースの端子台を使用します

- 貿易分析

- 特許分析

- 主要な特許のリスト

- 2022年と2023年の主要な会議とイベント

- 関税と規制の規制状況

- 規制機関、政府機関、およびその他の組織

- 市場基準

- UL 1059

- CSAC22.2番号158

- NEMA ICS 4

- UL 486E

- EN 60947-7-2

- IEC 60947-7-1:2009

- EN 60934

- EN 50019

第6章 構造別、機能別、接続タイプ別の端子台の分類

- イントロダクション

- 構造と機能に基づく端子台

- シングルレベルのフィードスルー端子台

- ダブルレベルの端子台

- トリプルレベルの端子台

- 接地回路端子

- 断路/ナイフ状断路/スイッチ端子台

- ヒューズ端子台

- 熱電対ブロック

- I/Oブロック

- センサー固有の端子台

- 接続技術に基づく端子台

- スプリング型(ケージクランプ)端子台

- ネジ型端子台

- 絶縁-圧接接続タイプの端子台

- プッシュイン端子台

- 特殊接続(スリップオンプラグイン接続、端子点接続)端子台

第7章 端子台の取り付けタイプ

- イントロダクション

- DINレール

- DINレールは、信頼性の高い接続を確立するために機械的なサポートを必要とします

- ミニチュアシルクハットレール

- G32レール

- シルクハットレール

- PCBマウント

- PCB端子台により、信号とデータの安全で簡単な送信が可能になります

第8章 タイプ別の端子台市場

- イントロダクション

- バリア・バリアストリップ

- 電源およびHVACシステムに主に配備されるバリア

- 単列バリア

- 二重列バリア

- セクション端子台

- ワイヤの電気的終端のために構築されたセクション端子台

- NEMA(アメリカンスタイル)およびIEC(欧州スタイル)端子台の概要

- NEMAセクション端子台

- IEC DINレールセクション端子台

- PCBマウント端子台

- 家庭用充電ステーション、流量計、照明制御などのために設計されたPCBマウント端子台

- 固定PCB端子台

- プラグ可能なPCB端子台

- 電源端子台

- 産業用制御盤、デッドフロント配電盤、ビジネス機器などに適した電源端子台

- その他

第9章 業界別の端子台市場

- イントロダクション

- ビジネス機器

- 効率的な作業スペースを作成するための最新のオフィス機器の優先度の向上は、端子台の要件を後押しします

- HVAC(暖房、換気、空調)システム

- 端子台市場の成長を加速するための商業ビルへのHVACシステムの設置の増加

- 電源装置

- さまざまな回路を燃料市場の成長に接続するための端子台の採用の急増

- 産業制御

- 端子台の需要を刺激するために企業を製造すること別デジタルテクノロジーと自動化ツールの実装の増加

- プロセス制御機器

- 安全なプロセス制御システムの要件を引き上げることで、信頼性の高い端子台が必要になります

- 通信機器

- 高度な通信機器の急増する使用により、端子台の需要が増加します

- 輸送

- 端子台プロバイダーの機会を創出するために、EV充電インフラストラクチャを構築する必要性が高まっています

- その他

第10章 地域別の端子台市場

- イントロダクション

- 北米

- 米国

- 市場の成長を推進するための自動車、エネルギー、通信会社別高度な接続技術の高い採用

- カナダ

- 市場機会を創出するための電源および自動機器アプリケーションでの端子台の使用の増加

- メキシコ

- 端子台の市場の成長を刺激するための国への巨額の投資

- 米国

- 欧州

- ドイツ

- ドイツは今後数年間で欧州の端子台市場で主導的な地位を保持します

- 英国

- 巨大な通信会社と自動車ブランドの存在は、端子台市場の成長機会を生み出します

- フランス

- 電気通信、自動車、防衛セクターが端子台の需要を刺激

- その他欧州

- ドイツ

- アジア太平洋地域

- 中国

- 端子台の高い採用につながる急速な工業化

- 日本

- 家庭用電化製品および自動車産業に対する国の人気は、端子台市場の成長機会を生み出します

- インド

- 堅牢な自動車セクターは端子台の使用を促進します

- その他アジア太平洋地域

- 中国

- 他の国々 (RoW)

- 南米

- インフラストラクチャの近代化と端子台市場の成長をサポートするための新技術の採用

- 中東・アフリカ

- 端子台市場の成長の可能性を生み出すための新しい建設プロジェクトでのHVACシステムの展開

- 南米

第11章 競合情勢

- イントロダクション

- トップ企業の収益分析

- トップ企業の市場シェア分析、2021年

- 会社評価象限、2021年

- 星

- 新興リーダー

- 普及して

- 参加者

- 中小企業(SMES)評価象限、2021年

- プログレッシブカンパニー

- レスポンシブ企業

- ダイナミックカンパニー

- スターティングブロック

- 端子台市場:会社のフットプリント

- 競合ベンチマーキング

- 競合シナリオと動向

- 製品の発売

- 取引

第12章 企業プロファイル

- KEY PLAYERS

- ADVANTECH

- ANYTEK ELECTRONIC TECHNOLOGY(SZ)CO., LTD.

- EATON CORPORATION PLC

- IDEC CORPORATION

- MOLEX, LLC

- NINGBO DEGSON ELECTRICAL CO., LTD.

- OMRON CORPORATION

- PHOENIX CONTACT

- ROCKWELL AUTOMATION, INC.

- SIEMENS AG

- TE CONNECTIVITY

- WAGO KONTAKTTECHNIK GMBH & CO. KG

- WECO ELECTRICAL CONNECTORS INC.

- WEIDMULLER INTERFACE GMBH & CO. KG

- WIELAND ELECTRIC GMBH

- OTHER PLAYERS

- AUTONICS CORPORATION

- CABUR

- CHENGDU RELIANCE ELECTRIC CO., LTD.

- CHINT

- CONNECTWELL INDUSTRIES PVT. LTD.

- CONTA-CLIP VERBINDUNGSTECHNIK GMBH

- CUI DEVICES

- DINKLE INTERNATIONAL CO., LTD.

- ELMEX CONTROLS PVT. LTD.

- KLEMSAN

- LEGRAND

- LITTELFUSE, INC.

- METZ CONNECT

- NINGBO SUPU ELECTRONICS CO., LTD

- PENN UNION

- RENHOTEC GROUP LTD.

- UPUN ELECTRIC

第13章 隣接および関連市場

- イントロダクション

- 制限

- アプリケーション別のHVACシステム市場

- 商業

- HVACシステム市場を後押しするための商業スペースにおけるエネルギー効率の高い機器に対する高い要件

- 住宅

- 住宅用途での住宅システムの使用を促進するための政府規制および税額控除プログラム

- 工業

- 運用コストを削減し、エネルギーを節約して市場の成長を加速するための、産業用スペースでのエネルギー効率の高いHVACシステムの導入の増加

第14章 付録

The terminal block market size is expected to grow from USD 3.9 billion in 2022 to USD 5.2 billion by 2027; it is expected to grow at a CAGR of 5.7% from 2022 to 2027. The key factors driving the growth of the terminal block market are surging demand for PCB terminal blocks from various industries and advancements observed in connection technologies which is deployed in terminal blocks; and thus provides various advantages to the industries.

"PCB mount terminal blocks is expected to grow at higher rate from 2022 to 2027"

PCB mount terminal blocks are modular and insulated devices that provide reliable connections. These blocks are mounted on printed circuit boards (PCBs), which come in pluggable and fixed configurations in various pitch sizes and wire sizes and are used to transmit signals, data, and power safely. These terminal blocks are used in various applications, such as home charging stations, flow meters, controllers, power supplies, etc. Nowadays, PCB blocks are available in different models, including wire cage models, front entry models, and wire protector types. The PCB mount terminal blocks is gaining popularity in the recent years, as constant advancements in PCB mount terminal blocks prompt industries to adopt them at a faster rate.

"Industrial controls to hold largest share in 2021"

The industrial controls segment holds the largest share of terminal block market in 2021. The rising adoption of automation devices and industry 4.0 in manufacturing units in most developed countries such as the US, Canada, the UK, and Germany, as well as in some developing countries such as China and India, has propelled the growth of the global industrial controls and factory automation market. The increasing use of advanced tools and technologies in manufacturing units elevates the demand for terminal blocks. Besides, terminal blocks are commonly used in industrial equipment such as switchgear, machine controls, distribution panels, and measuring devices, there by accelerating the growth of the terminal block market for industrial controls.

"Asia Pacific is expected to capture largest market growth rateduring forecast period"

The Asia Pacific region is expected to hold the largest market growth rate of the terminal block market during the forecast period. Rapid urbanization and high disposable income are improving the lifestyles of people in this region. As a result, there is a high demand for premium cars, high-end electronic devices, and HVAC systems. This creates a strong demand for terminal blocks from the automotive, telecom equipment, and HVAC systems industries. Besides, the emerging economies in Asia Pacific would majorly contribute to the terminal block market in the forecast period. Increasing industrial activities in China, India, Japan, and Indonesia drive the growth of the terminal block market in Asia Pacific.

The break-up of the profiles of primary participants for the report has been given below:

- By Company Type: Tier 1 = 52%, Tier 2 = 31%, and Tier 3 = 17%

- By Designation: C-Level Executives = 47%, Directors= 31%, and Others= 22%

- By Region: North America = 31%, Europe = 29%, Asia Pacific = 34%, and RoW = 06%

Major players operating in the terminal block market include WAGO Kontakttechnik GmbH & Co. KG (Germany), TE Connectivity (Switzerland), Weidmuller Interface GmbH & Co. KG (Germany), OMRON Corporation (Japan), Eaton Corporation (Ireland), PHOENIX CONTACT (Germany), Rockwell Automation, Inc. (US), Molex, LLC (US), Wieland Electric GmbH (Germany), among others.

Research Coverage:

The research report on the global terminal block market covers the market based on type, industry, classification of terminal blocks according to their structure, function type, and connection type; mounting type,and region. Based on type, the market has been segmented into barriers or barrier strips, sectional terminal blocks, PCB mount terminal blocks, power terminal blocks, and other terminal blocks. Based on industry, the market has been segmented into business equipment, HVAC systems, power supplies, industrial control, process control instruments, telecom equipment, transportation, and other industries. Based on classification of terminal blocks according to their structure, function type, and connection type, the market has been segmented into terminal blocks based on structure and function which includes single-level feed-through terminal blocks, double-level terminal blocks, triple-level terminal blocks, ground circuit terminals, disconnect/knife disconnect/switch terminal blocks, fuse terminal blocks, thermocouple blocks, I/O blocks, and sensor-specific terminal blocks; whereas terminal blocks on connection technologies includes spring (cage clamp)-type terminal blocks, screw-type terminal blocks, insulation displacement connection-type terminal blocks, push-in-type terminal blocks, and special connections (slip-on plug-in connection, TERMI-POINT connection). Based on mounting type, the market has been segmented into DIN rail and PCB mount. The report covers four major regions, namely,North America, Europe, AsiaPacific (APAC), and Rest of the World (RoW).

Key Benefits of Buying the Report:

This report segments the terminal block market comprehensively and provides the closest approximations of the overall market size, as well as that of the subsegments across different type, industry, classification of terminal blocks according to their structure, function type, and connection type; mounting type,and region.

The report helps stakeholders understand the pulse of the market, expected market scenario and provides information on key market drivers, restraints, challenges, and opportunities.

The report helps to understand the COVID-19 impact on the terminal block market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 TERMINAL BLOCK MARKET SEGMENTATION

- FIGURE 2 GEOGRAPHIC SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 3 TERMINAL BLOCK MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY AND PRIMARY RESEARCH

- 2.1.2 SECONDARY DATA

- 2.1.2.1 List of major secondary sources

- 2.1.2.2 Key data from secondary sources

- 2.1.3 PRIMARY DATA

- 2.1.3.1 Primary interviews with experts

- 2.1.3.2 Key data from primary sources

- 2.1.3.3 Key industry insights

- 2.1.3.4 Breakdown of primaries

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH (SUPPLY-SIDE): REVENUE GENERATED THROUGH SALES OF PRODUCTS/SOLUTIONS/SERVICES PERTAINING TO TERMINAL BLOCKS

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach for arriving at market share by bottom-up analysis (demand side)

- FIGURE 5 TERMINAL BLOCK MARKET: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach for capturing market share by top-down analysis (supply side)

- FIGURE 6 TERMINAL BLOCK MARKET: TOP-DOWN APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 7 DATA TRIANGULATION

- 2.4 STUDY ASSUMPTIONS

- 2.5 RISK ASSESSMENT

- TABLE 1 RISKS AND ASSOCIATED RESULTS

3 EXECUTIVE SUMMARY

- FIGURE 8 SECTIONAL TERMINAL BLOCKS TO DOMINATE MARKET IN 2022

- FIGURE 9 INDUSTRIAL CONTROLS TO CAPTURE MAJORITY OF MARKET SHARE IN 2027

- FIGURE 10 ASIA PACIFIC TO WITNESS HIGHEST CAGR IN TERMINAL BLOCK MARKET DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE GROWTH OPPORTUNITIES FOR PLAYERS IN TERMINAL BLOCK MARKET

- FIGURE 11 RAPID INDUSTRIALIZATION IN ASIA PACIFIC COUNTRIES LIKELY TO DRIVE MARKET GROWTH

- 4.2 TERMINAL BLOCK MARKET, BY TYPE

- FIGURE 12 SECTIONAL TERMINAL BLOCKS TO HOLD LARGEST MARKET SHARE IN 2027

- 4.3 TERMINAL BLOCK MARKET, BY INDUSTRY

- FIGURE 13 PROCESS CONTROL INSTRUMENTS TO RECORD HIGHEST CAGR IN TERMINAL BLOCK MARKET DURING FORECAST PERIOD

- 4.4 TERMINAL BLOCK MARKET, BY REGION

- FIGURE 14 ASIA PACIFIC EXPECTED TO COMMAND TERMINAL BLOCK MARKET THROUGHOUT FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 15 GLOBAL TERMINAL BLOCK MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Surging demand for PCB terminal blocks from various industries

- 5.2.1.2 Ongoing advancements in connection technologies

- 5.2.1.3 Growing implementation of advanced terminal blocks in telecom sector

- 5.2.1.4 Rising adoption of electric vehicles

- FIGURE 16 IMPACT OF DRIVERS ON TERMINAL BLOCK MARKET

- 5.2.2 RESTRAINTS

- 5.2.2.1 Difficulty in selecting right terminal block according to applications

- FIGURE 17 IMPACT OF RESTRAINTS ON TERMINAL BLOCK MARKET

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rapid urbanization and industrialization in developing countries

- 5.2.3.2 Increased need for micro-miniature terminal blocks

- FIGURE 18 IMPACT OF OPPORTUNITIES ON TERMINAL BLOCK MARKET

- 5.2.4 CHALLENGES

- 5.2.4.1 Design-related challenges while developing surface-mount technology-based terminal blocks

- FIGURE 19 IMPACT OF CHALLENGES ON TERMINAL BLOCK MARKET

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 20 TERMINAL BLOCK MARKET: VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM

- FIGURE 21 GLOBAL TERMINAL BLOCK MARKET: ECOSYSTEM

- TABLE 2 COMPANIES AND THEIR ROLES IN TERMINAL BLOCK ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF TERMINAL BLOCKS OFFERED BY KEY PLAYERS, BY TYPE

- FIGURE 22 AVERAGE SELLING PRICE OF TERMINAL BLOCKS PROVIDED BY KEY PLAYERS, BY TYPE

- TABLE 3 AVERAGE SELLING PRICE OF TERMINAL BLOCKS PROVIDED BY KEY PLAYERS, BY TYPE (USD)

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESS

- FIGURE 23 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 PUSH-IN CONNECTION

- 5.7.2 PIERCE CONNECTION

- 5.7.3 CRIMP CONNECTION

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 TERMINAL BLOCK MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 BARGAINING POWER OF SUPPLIERS

- 5.8.2 BARGAINING POWER OF BUYERS

- 5.8.3 THREAT OF SUBSTITUTES

- 5.8.4 THREAT OF NEW ENTRANTS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 24 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP 3 INDUSTRIES

- TABLE 5 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP 3 INDUSTRIES (%)

- 5.9.2 BUYING CRITERIA

- FIGURE 25 KEY BUYING CRITERIA FOR TOP 3 INDUSTRIES

- TABLE 6 KEY BUYING CRITERIA FOR TOP 3 INDUSTRIES

- 5.10 CASE STUDY

- 5.10.1 PHOENIX CONTACT HELPS AEON TO CONTROL LIGHTING SYSTEM REMOTELY BY INTEGRATING I/O TERMINALS BLOCKS WITH HMI SOLUTION

- 5.10.2 SPRING PRESSURE CONNECTION TECHNOLOGY BY WAGO MAKES LIGHTING CONNECTION EASY FOR K-LITE

- 5.10.3 CONNECTWELL RESOLVES SIGNAL INTERRUPTION ISSUE FACED BY HARAMAIN RAILWAY WITH DEPLOYMENT OF SPRING CLAMP SERIES

- 5.10.4 CHETTINAD CEMENT'S WAGON TIPPLER UNLOADING SYSTEM USES SPACE-SAVING TERMINAL BLOCKS FROM CONNECTWELL

- 5.11 TRADE ANALYSIS

- FIGURE 26 IMPORT DATA FOR HS CODE 8536, BY KEY COUNTRY, 2017-2021 (USD MILLION)

- FIGURE 27 EXPORT DATA FOR HS CODE 8536, BY KEY COUNTRY, 2017-2021 (USD MILLION)

- 5.12 PATENT ANALYSIS

- FIGURE 28 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS IN LAST 10 YEARS

- FIGURE 29 ANALYSIS OF PATENTS RELATED TO TERMINAL BLOCKS, 2012-2021

- TABLE 7 NUMBER OF PATENTS FILED BY TOP 20 MARKET PLAYERS

- 5.12.1 LIST OF MAJOR PATENTS

- 5.13 KEY CONFERENCES AND EVENTS IN 2022 AND 2023

- TABLE 8 TERMINAL BLOCK MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

- 5.14 TARIFF AND REGULATORY LANDSCAPE

- 5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.2 MARKET STANDARDS

- 5.14.2.1 UL 1059

- 5.14.2.2 CSA C22.2 no. 158

- 5.14.2.3 NEMA ICS 4

- 5.14.2.4 UL 486E

- 5.14.2.5 EN 60947-7-2

- 5.14.2.6 IEC 60947-7-1:2009

- 5.14.2.7 EN 60934

- 5.14.2.8 EN 50019

6 CLASSIFICATION OF TERMINAL BLOCKS ACCORDING TO STRUCTURE, FUNCTION, AND CONNECTION TYPE

- 6.1 INTRODUCTION

- FIGURE 30 CLASSIFICATION OF TERMINAL BLOCKS BY STRUCTURE, FUNCTION, AND CONNECTION TYPE

- 6.2 TERMINAL BLOCKS BASED ON STRUCTURE AND FUNCTION

- 6.2.1 SINGLE-LEVEL FEED-THROUGH TERMINAL BLOCKS

- 6.2.2 DOUBLE-LEVEL TERMINAL BLOCKS

- 6.2.3 TRIPLE-LEVEL TERMINAL BLOCKS

- 6.2.4 GROUND CIRCUIT TERMINALS

- 6.2.5 DISCONNECT/KNIFE-DISCONNECT/SWITCH TERMINAL BLOCKS

- 6.2.6 FUSE TERMINAL BLOCKS

- 6.2.7 THERMOCOUPLE BLOCKS

- 6.2.8 I/O BLOCKS

- 6.2.9 SENSOR-SPECIFIC TERMINAL BLOCKS

- 6.3 TERMINAL BLOCKS BASED ON CONNECTION TECHNOLOGIES

- 6.3.1 SPRING-TYPE (CAGE CLAMP) TERMINAL BLOCKS

- 6.3.2 SCREW-TYPE TERMINAL BLOCKS

- 6.3.3 INSULATION-DISPLACEMENT CONNECTION-TYPE TERMINAL BLOCKS

- 6.3.4 PUSH-IN TERMINAL BLOCKS

- 6.3.5 SPECIAL CONNECTION (SLIP-ON PLUG-IN CONNECTION, TERMI-POINT CONNECTION) TERMINAL BLOCKS

7 MOUNTING TYPES OF TERMINAL BLOCKS

- 7.1 INTRODUCTION

- FIGURE 31 MOUNTING TYPES OF TERMINAL BLOCKS

- FIGURE 32 TERMINAL BLOCKS ARE MOUNTED ON DIN RAIL

- 7.2 DIN RAIL

- 7.2.1 DIN RAIL REQUIRES MECHANICAL SUPPORT TO MAKE RELIABLE CONNECTIONS

- 7.2.2 MINIATURE TOP-HAT RAILS

- 7.2.3 G32 RAILS

- 7.2.4 TOP-HAT RAILS

- 7.3 PCB MOUNT

- 7.3.1 PCB TERMINAL BLOCKS ALLOW SAFE AND EASY TRANSMISSION OF SIGNALS AND DATA

8 TERMINAL BLOCK MARKET, BY TYPE

- 8.1 INTRODUCTION

- FIGURE 33 TERMINAL BLOCK MARKET, BY TYPE

- FIGURE 34 PCB MOUNT TERMINAL BLOCKS TO EXHIBIT HIGHEST CAGR FROM 2022 TO 2027

- TABLE 13 TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 14 TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- 8.2 BARRIERS OR BARRIER STRIPS

- 8.2.1 BARRIERS PRIMARILY DEPLOYED IN POWER SUPPLIES AND HVAC SYSTEMS

- TABLE 15 BARRIERS: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 16 BARRIERS: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 17 BARRIERS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 18 BARRIERS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 19 BARRIERS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 20 BARRIERS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.2.2 SINGLE-ROW BARRIERS

- 8.2.3 DOUBLE-ROW BARRIERS

- 8.3 SECTIONAL TERMINAL BLOCKS

- 8.3.1 SECTIONAL TERMINAL BLOCKS BUILT FOR ELECTRICAL TERMINATION OF WIRES

- TABLE 21 SECTIONAL TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 22 SECTIONAL TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 23 SECTIONAL TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 24 SECTIONAL TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 25 SECTIONAL TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 26 SECTIONAL TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.3.2 OVERVIEW OF NEMA (AMERICAN STYLE) AND IEC (EUROPEAN STYLE) TERMINAL BLOCKS

- 8.3.3 NEMA SECTIONAL TERMINAL BLOCKS

- 8.3.4 IEC DIN RAIL SECTIONAL TERMINAL BLOCKS

- 8.4 PCB MOUNT TERMINAL BLOCKS

- 8.4.1 PCB MOUNT TERMINAL BLOCKS DESIGNED FOR HOME CHARGING STATIONS, FLOW METERS, LIGHTING CONTROLS, ETC.

- TABLE 27 PCB MOUNT TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 28 PCB MOUNT TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 29 PCB MOUNT TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 30 PCB MOUNT TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 31 PCB MOUNT TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 32 PCB MOUNT TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.4.2 FIXED PCB TERMINAL BLOCKS

- 8.4.3 PLUGGABLE PCB TERMINAL BLOCKS

- 8.5 POWER TERMINAL BLOCKS

- 8.5.1 POWER TERMINAL BLOCKS SUITABLE FOR INDUSTRIAL CONTROL PANELS, DEAD-FRONT SWITCHBOARDS, BUSINESS EQUIPMENT, ETC.

- TABLE 33 POWER TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 34 POWER TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 35 POWER TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 36 POWER TERMINAL BLOCKS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.6 OTHERS

- TABLE 37 OTHERS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 38 OTHERS: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- TABLE 39 OTHERS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 40 OTHERS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

9 TERMINAL BLOCK MARKET, BY INDUSTRY

- 9.1 INTRODUCTION

- FIGURE 35 TERMINAL BLOCK MARKET, BY INDUSTRY

- FIGURE 36 INDUSTRIAL CONTROLS SEGMENT HELD LARGEST SHARE OF TERMINAL BLOCK MARKET IN 2021

- TABLE 41 TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 42 TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- 9.2 BUSINESS EQUIPMENT

- 9.2.1 INCREASING PREFERENCE FOR MODERN OFFICE EQUIPMENT TO CREATE EFFICIENT WORKING SPACE BOOSTS REQUIREMENT FOR TERMINAL BLOCKS

- TABLE 43 BUSINESS EQUIPMENT: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 44 BUSINESS EQUIPMENT: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 45 BUSINESS EQUIPMENT: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 46 BUSINESS EQUIPMENT: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.3 HVAC (HEATING, VENTILATION, AND AIR CONDITIONING) SYSTEMS

- 9.3.1 INCREASING INSTALLATION OF HVAC SYSTEMS IN COMMERCIAL BUILDINGS TO ACCELERATE TERMINAL BLOCK MARKET GROWTH

- TABLE 47 HVAC SYSTEMS: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 48 HVAC SYSTEMS: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 49 HVAC SYSTEMS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 50 HVAC SYSTEMS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.4 POWER SUPPLIES

- 9.4.1 SURGING ADOPTION OF TERMINAL BLOCKS TO CONNECT DIFFERENT CIRCUITRIES TO FUEL MARKET GROWTH

- TABLE 51 POWER SUPPLIES: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 52 POWER SUPPLIES: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 53 POWER SUPPLIES: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 54 POWER SUPPLIES: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.5 INDUSTRIAL CONTROLS

- 9.5.1 RISING IMPLEMENTATION OF DIGITAL TECHNOLOGY AND AUTOMATED TOOLS BY MANUFACTURING FIRMS TO STIMULATE DEMAND FOR TERMINAL BLOCKS

- TABLE 55 INDUSTRIAL CONTROLS: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 56 INDUSTRIAL CONTROLS: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 57 INDUSTRIAL CONTROLS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 58 INDUSTRIAL CONTROLS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.6 PROCESS CONTROL INSTRUMENTS

- 9.6.1 ELEVATING REQUIREMENT FOR SAFE PROCESS CONTROL SYSTEMS GENERATES NEED FOR RELIABLE TERMINAL BLOCKS

- TABLE 59 PROCESS CONTROL INSTRUMENTS: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 60 PROCESS CONTROL INSTRUMENTS: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 61 PROCESS CONTROL INSTRUMENTS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 62 PROCESS CONTROL INSTRUMENTS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.7 TELECOM EQUIPMENT

- 9.7.1 SURGING USE OF HIGHLY ADVANCED TELECOM EQUIPMENT INCREASES DEMAND FOR TERMINAL BLOCKS

- TABLE 63 TELECOM EQUIPMENT: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 64 TELECOM EQUIPMENT: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 65 TELECOM EQUIPMENT: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 66 TELECOM EQUIPMENT: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.8 TRANSPORTATION

- 9.8.1 RISING NEED TO BUILD EV CHARGING INFRASTRUCTURE TO CREATE OPPORTUNITIES FOR TERMINAL BLOCK PROVIDERS

- TABLE 67 TRANSPORTATION: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 68 TRANSPORTATION: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 69 TRANSPORTATION: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 70 TRANSPORTATION: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.9 OTHERS

- TABLE 71 OTHERS: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 72 OTHERS: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 73 OTHERS: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 74 OTHERS: TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

10 TERMINAL BLOCK MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 37 TERMINAL BLOCK MARKET, BY GEOGRAPHY

- FIGURE 38 GEOGRAPHIC SNAPSHOT FOR TERMINAL BLOCK MARKET, 2022-2027

- TABLE 75 TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 76 TERMINAL BLOCK MARKET, BY REGION, 2022-2027 (USD MILLION)

- 10.2 NORTH AMERICA

- FIGURE 39 NORTH AMERICA: TERMINAL BLOCK MARKET SNAPSHOT

- FIGURE 40 US LIKELY TO DOMINATE NORTH AMERICAN TERMINAL BLOCK MARKET DURING FORECAST PERIOD

- TABLE 77 NORTH AMERICA: TERMINAL BLOCK MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 78 NORTH AMERICA: TERMINAL BLOCK MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- TABLE 79 NORTH AMERICA: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 80 NORTH AMERICA: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 81 NORTH AMERICA: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 82 NORTH AMERICA: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- 10.2.1 US

- 10.2.1.1 High adoption of advanced connection technologies by automobile, energy, and telecom companies to propel market growth

- 10.2.2 CANADA

- 10.2.2.1 Increased use of terminal blocks in power supplies and automated equipment applications to create market opportunities

- 10.2.3 MEXICO

- 10.2.3.1 Huge investments in country to stimulate growth of market for terminal blocks

- 10.3 EUROPE

- FIGURE 41 EUROPE: TERMINAL BLOCK MARKET SNAPSHOT

- FIGURE 42 GERMANY TO DOMINATE EUROPEAN TERMINAL BLOCK MARKET THROUGHOUT FORECAST PERIOD

- TABLE 83 EUROPE: TERMINAL BLOCK MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 84 EUROPE: TERMINAL BLOCK MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- TABLE 85 EUROPE: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 86 EUROPE: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 87 EUROPE: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 88 EUROPE: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- 10.3.1 GERMANY

- 10.3.1.1 Germany to hold leading position in European terminal block market in coming years

- 10.3.2 UK

- 10.3.2.1 Presence of giant telecom companies and automobile brands creates growth opportunities for terminal block market

- 10.3.3 FRANCE

- 10.3.3.1 Telecom, automotive, and defense sectors stimulate demand for terminal blocks

- 10.3.4 REST OF EUROPE

- 10.4 ASIA PACIFIC

- FIGURE 43 ASIA PACIFIC: TERMINAL BLOCK MARKET SNAPSHOT

- FIGURE 44 CHINA TO LEAD TERMINAL BLOCK MARKET IN ASIA PACIFIC FROM 2022 TO 2027

- TABLE 89 ASIA PACIFIC: TERMINAL BLOCK MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 90 ASIA PACIFIC: TERMINAL BLOCK MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- TABLE 91 ASIA PACIFIC: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 92 ASIA PACIFIC: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 93 ASIA PACIFIC: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 94 ASIA PACIFIC: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- 10.4.1 CHINA

- 10.4.1.1 Rapid industrialization to lead to high adoption of terminal blocks

- 10.4.2 JAPAN

- 10.4.2.1 Popularity of nation for its consumer electronics and automotive industries creates growth opportunities for terminal block market

- 10.4.3 INDIA

- 10.4.3.1 Robust automotive sector promotes use of terminal blocks

- 10.4.4 REST OF ASIA PACIFIC

- 10.5 REST OF THE WORLD (ROW)

- FIGURE 45 MIDDLE EAST & AFRICA TO LEAD TERMINAL BLOCK MARKET IN ROW REGION BETWEEN 2022 AND 2027

- TABLE 95 ROW: TERMINAL BLOCK MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 96 ROW: TERMINAL BLOCK MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- TABLE 97 ROW: TERMINAL BLOCK MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 98 ROW: TERMINAL BLOCK MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 99 ROW: TERMINAL BLOCK MARKET, BY INDUSTRY, 2018-2021 (USD MILLION)

- TABLE 100 ROW: TERMINAL BLOCK MARKET, BY INDUSTRY, 2022-2027 (USD MILLION)

- 10.5.1 SOUTH AMERICA

- 10.5.1.1 Modernization of infrastructure and adoption of new technologies to support terminal block market growth

- 10.5.2 MIDDLE EAST & AFRICA

- 10.5.2.1 Deployment of HVAC systems in new construction projects to create growth potential for terminal block market

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- TABLE 101 KEY DEVELOPMENTS IN TERMINAL BLOCK MARKET (2019-2022)

- 11.2 REVENUE ANALYSIS OF TOP COMPANIES

- FIGURE 46 TERMINAL BLOCK MARKET: REVENUE ANALYSIS (2021)

- 11.3 MARKET SHARE ANALYSIS OF TOP PLAYERS, 2021

- TABLE 102 TERMINAL BLOCK MARKET: DEGREE OF COMPETITION

- 11.4 COMPANY EVALUATION QUADRANT, 2021

- 11.4.1 STAR

- 11.4.2 EMERGING LEADER

- 11.4.3 PERVASIVE

- 11.4.4 PARTICIPANT

- FIGURE 47 TERMINAL BLOCK MARKET (GLOBAL): COMPANY EVALUATION QUADRANT, 2021

- 11.5 SMALL AND MEDIUM-SIZED ENTERPRISES (SMES) EVALUATION QUADRANT, 2021

- 11.5.1 PROGRESSIVE COMPANY

- 11.5.2 RESPONSIVE COMPANY

- 11.5.3 DYNAMIC COMPANY

- 11.5.4 STARTING BLOCK

- FIGURE 48 TERMINAL BLOCK MARKET (GLOBAL): SME EVALUATION QUADRANT, 2021

- 11.6 TERMINAL BLOCK MARKET: COMPANY FOOTPRINT

- TABLE 103 COMPANY TYPE FOOTPRINT

- TABLE 104 COMPANY INDUSTRY FOOTPRINT

- TABLE 105 COMPANY REGION FOOTPRINT

- TABLE 106 COMPANY FOOTPRINT

- 11.7 COMPETITIVE BENCHMARKING

- TABLE 107 TERMINAL BLOCK MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 108 TERMINAL BLOCK MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 11.8 COMPETITIVE SCENARIO AND TRENDS

- 11.8.1 PRODUCT LAUNCHES

- TABLE 109 TERMINAL BLOCK MARKET: PRODUCT LAUNCHES, MARCH 2019-AUGUST 2021

- 11.8.2 DEALS

- TABLE 110 TERMINAL BLOCK MARKET: DEALS, JANUARY 2020-FEBRUARY 2022

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- (Business overview. Products offered, Recent developments, Product launches, Deals, MnM view, Key strengths/right to win, Strategic choices made, and Weaknesses and competitive threats)**

- 12.1.1 ADVANTECH

- TABLE 111 ADVANTECH: BUSINESS OVERVIEW

- FIGURE 49 ADVANTECH: COMPANY SNAPSHOT

- TABLE 112 ADVANTECH: PRODUCT OFFERINGS

- 12.1.2 ANYTEK ELECTRONIC TECHNOLOGY (SZ) CO., LTD.

- TABLE 113 ANYTEK ELECTRONIC TECHNOLOGY (SZ) CO., LTD.: BUSINESS OVERVIEW

- TABLE 114 ANYTEK ELECTRONIC TECHNOLOGY (SZ) CO., LTD.: PRODUCT OFFERINGS

- 12.1.3 EATON CORPORATION PLC

- TABLE 115 EATON CORPORATION PLC: BUSINESS OVERVIEW

- FIGURE 50 EATON CORPORATION PLC: COMPANY SNAPSHOT

- TABLE 116 EATON CORPORATION PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.4 IDEC CORPORATION

- TABLE 117 IDEC CORPORATION: BUSINESS OVERVIEW

- FIGURE 51 IDEC CORPORATION: COMPANY SNAPSHOT

- TABLE 118 IDEC CORPORATION: PRODUCT OFFERINGS

- 12.1.5 MOLEX, LLC

- TABLE 119 MOLEX, LLC: BUSINESS OVERVIEW

- TABLE 120 MOLEX, LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.6 NINGBO DEGSON ELECTRICAL CO., LTD.

- TABLE 121 NINGBO DEGSON ELECTRICAL CO., LTD: BUSINESS OVERVIEW

- TABLE 122 NINGBO DEGSON ELECTRICAL CO., LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.7 OMRON CORPORATION

- TABLE 123 OMRON CORPORATION: BUSINESS OVERVIEW

- FIGURE 52 OMRON CORPORATION: COMPANY SNAPSHOT

- TABLE 124 OMRON CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.8 PHOENIX CONTACT

- TABLE 125 PHOENIX CONTACT: BUSINESS OVERVIEW

- TABLE 126 PHOENIX CONTACT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.9 ROCKWELL AUTOMATION, INC.

- TABLE 127 ROCKWELL AUTOMATION, INC.: BUSINESS OVERVIEW

- FIGURE 53 ROCKWELL AUTOMATION, INC.: COMPANY SNAPSHOT

- TABLE 128 ROCKWELL AUTOMATION, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.10 SIEMENS AG

- TABLE 129 SIEMENS AG: BUSINESS OVERVIEW

- FIGURE 54 SIEMENS AG: COMPANY SNAPSHOT

- TABLE 130 SIEMENS AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.11 TE CONNECTIVITY

- TABLE 131 TE CONNECTIVITY: BUSINESS OVERVIEW

- FIGURE 55 TE CONNECTIVITY: COMPANY SNAPSHOT

- TABLE 132 TE CONNECTIVITY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 133 TE CONNECTIVITY: PRODUCT LAUNCHES

- 12.1.12 WAGO KONTAKTTECHNIK GMBH & CO. KG

- TABLE 134 WAGO KONTAKTTECHNIK GMBH & CO. KG: BUSINESS OVERVIEW

- TABLE 135 WAGO KONTAKTTECHNIK GMBH & CO. KG.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 136 WAGO KONTAKTTECHNIK GMBH & CO. KG: PRODUCT LAUNCHES

- 12.1.13 WECO ELECTRICAL CONNECTORS INC.

- TABLE 137 WECO ELECTRICAL CONNECTORS INC.: BUSINESS OVERVIEW

- TABLE 138 WECO ELECTRICAL CONNECTORS INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.14 WEIDMULLER INTERFACE GMBH & CO. KG

- TABLE 139 WEIDMULLER INTERFACE GMBH & CO. KG: BUSINESS OVERVIEW

- TABLE 140 WEIDMULLER INTERFACE GMBH & CO. KG.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 141 WEIDMULLER INTERFACE GMBH & CO. KG.: PRODUCT LAUNCHES

- 12.1.15 WIELAND ELECTRIC GMBH

- TABLE 142 WIELAND ELECTRIC GMBH: BUSINESS OVERVIEW

- TABLE 143 WIELAND ELECTRIC GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2 OTHER PLAYERS

- 12.2.1 AUTONICS CORPORATION

- 12.2.2 CABUR

- 12.2.3 CHENGDU RELIANCE ELECTRIC CO., LTD.

- 12.2.4 CHINT

- 12.2.5 CONNECTWELL INDUSTRIES PVT. LTD.

- 12.2.6 CONTA-CLIP VERBINDUNGSTECHNIK GMBH

- 12.2.7 CUI DEVICES

- 12.2.8 DINKLE INTERNATIONAL CO., LTD.

- 12.2.9 ELMEX CONTROLS PVT. LTD.

- 12.2.10 KLEMSAN

- 12.2.11 LEGRAND

- 12.2.12 LITTELFUSE, INC.

- 12.2.13 METZ CONNECT

- 12.2.14 NINGBO SUPU ELECTRONICS CO., LTD

- 12.2.15 PENN UNION

- 12.2.16 RENHOTEC GROUP LTD.

- 12.2.17 UPUN ELECTRIC

- *Details on Business overview. Products offered, Recent developments, Product launches, Deals, MnM view, Key strengths/right to win, Strategic choices made, and Weaknesses and competitive threats might not be captured in case of unlisted companies.

13 ADJACENT & RELATED MARKETS

- 13.1 INTRODUCTION

- 13.2 LIMITATIONS

- 13.3 HVAC SYSTEM MARKET, BY APPLICATION

- TABLE 144 INDUSTRY-STANDARD RATING PARAMETERS RELATED TO HVAC SYSTEMS

- TABLE 145 HVAC SYSTEM MARKET, BY APPLICATION, 2017-2020 (USD BILLION)

- TABLE 146 HVAC SYSTEM MARKET, BY APPLICATION, 2021-2026 (USD BILLION)

- 13.4 COMMERCIAL

- 13.4.1 HIGH REQUIREMENT FOR ENERGY-EFFICIENT EQUIPMENT IN COMMERCIAL SPACES TO BOOST HVAC SYSTEM MARKET

- TABLE 147 HVAC SYSTEM MARKET, BY COMMERCIAL APPLICATION, 2017-2020 (USD BILLION)

- TABLE 148 HVAC SYSTEM MARKET, BY COMMERCIAL APPLICATION, 2021-2026 (USD BILLION)

- TABLE 149 COMMERCIAL: HVAC SYSTEM MARKET, BY COOLING EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 150 COMMERCIAL: HVAC SYSTEM MARKET, BY COOLING EQUIPMENT, 2021-2026 (USD BILLION)

- TABLE 151 COMMERCIAL: HVAC SYSTEM MARKET, BY HEATING EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 152 COMMERCIAL: HVAC SYSTEM MARKET, BY HEATING EQUIPMENT, 2021-2026 (USD BILLION)

- TABLE 153 COMMERCIAL: HVAC SYSTEM MARKET, BY VENTILATION EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 154 COMMERCIAL: HVAC SYSTEM MARKET, BY VENTILATION EQUIPMENT, 2021-2026 (USD BILLION)

- 13.5 RESIDENTIAL

- 13.5.1 GOVERNMENT REGULATIONS AND TAX CREDIT PROGRAMS TO PROMOTE USE OF HVAC SYSTEMS IN RESIDENTIAL APPLICATIONS

- TABLE 155 RESIDENTIAL: HVAC SYSTEM MARKET, BY COOLING EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 156 RESIDENTIAL: HVAC SYSTEM MARKET, BY COOLING EQUIPMENT, 2021-2026 (USD BILLION)

- TABLE 157 RESIDENTIAL: HVAC SYSTEM MARKET, BY HEATING EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 158 RESIDENTIAL: HVAC SYSTEM MARKET, BY HEATING EQUIPMENT, 2021-2026 (USD BILLION)

- TABLE 159 RESIDENTIAL: HVAC SYSTEM MARKET, BY VENTILATION EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 160 RESIDENTIAL: HVAC SYSTEM MARKET, BY VENTILATION EQUIPMENT, 2021-2026 (USD BILLION)

- 13.6 INDUSTRIAL

- 13.6.1 INCREASED DEPLOYMENT OF ENERGY-EFFICIENT HVAC SYSTEMS IN INDUSTRIAL SPACES TO REDUCE OPERATIONAL COST AND SAVE ENERGY TO ACCELERATE MARKET GROWTH

- TABLE 161 INDUSTRIAL: HVAC SYSTEM MARKET, BY COOLING EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 162 INDUSTRIAL: HVAC SYSTEM MARKET, BY COOLING EQUIPMENT, 2021-2026 (USD BILLION)

- TABLE 163 INDUSTRIAL: HVAC SYSTEM MARKET, BY HEATING EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 164 INDUSTRIAL: HVAC SYSTEM MARKET, BY HEATING EQUIPMENT, 2021-2026 (USD BILLION)

- TABLE 165 INDUSTRIAL: HVAC SYSTEM MARKET, BY VENTILATION EQUIPMENT, 2017-2020 (USD BILLION)

- TABLE 166 INDUSTRIAL: HVAC SYSTEM MARKET, BY VENTILATION EQUIPMENT, 2021-2026 (USD BILLION)

14 APPENDIX

- 14.1 INSIGHTS FROM INDUSTRY EXPERTS

- 14.2 DISCUSSION GUIDE

- 14.3 KNOWLEDGE STORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.4 AVAILABLE CUSTOMIZATION

- 14.5 RELATED REPORTS

- 14.6 AUTHOR DETAILS