|

|

市場調査レポート

商品コード

1274190

自動マテリアルハンドリング機器の世界市場:製品別(ロボット、ASRS、コンベヤ・仕分けシステム、クレーン、WMS、AGV)、システムタイプ別(ユニットロード用、バルクロード用)、産業別、地域別 - 2028年までの予測Automated Material Handling Equipment Market by Product (Robots, ASRS, Conveyors And Sortation Systems, Cranes, WMS, AGV), System Type (Unit Load, Bulk Load), Industry (Automotive, E-Commerce, Food & Beverage) and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 自動マテリアルハンドリング機器の世界市場:製品別(ロボット、ASRS、コンベヤ・仕分けシステム、クレーン、WMS、AGV)、システムタイプ別(ユニットロード用、バルクロード用)、産業別、地域別 - 2028年までの予測 |

|

出版日: 2023年05月03日

発行: MarketsandMarkets

ページ情報: 英文 308 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の自動マテリアルハンドリング機器の市場規模は、2023年の306億米ドルから、2028年までに457億米ドルに達し、2023年から2028年までのCAGRで8.3%の成長が予測されています。

この市場の成長は、多様な産業における自動マテリアルハンドリング機器の需要の高まりと、倉庫オートメーションのためのロボットソリューションを提供するスタートアップ企業の増加に起因しています。

"ユニットロード用セグメントは、2023年から2028年の間、より高いCAGRで成長すると予測される"

ユニットロード用マテリアルハンドリングシステムは、適切な大きさの物品を1つのユニットにまとめ、容易に移動させることができるシステムです。大量に輸送されたり、寸法が大きくなったりした場合でも、さまざまなアイテムやユニットを単独で取り扱うことができるのが特徴です。1度に複数の物品を移動させることができ、迅速かつ経済的なシステムです。破損やハンドリングコストの低減に貢献します。ハンドリング、保管、流通の効率化に貢献します。ユニットロード用の管理に使用されるAMHEには、AGV、ASRS、ロボットなどの種類があります。

"2023年、自動車産業が市場の最大シェアを占める"

自動車産業の関係者は、自動化された効率的なプロセスによる製造の改善を求めています。これらの企業は、さまざまな部品を慎重に扱い、それを追跡することで、製造や組み立ての作業を効率的に行う必要があります。この業界におけるAMHEの導入は、自動車部品の損傷を防ぎ、在庫の取り扱いによる非生産的な労働時間のコストを削減し、利用可能な床面積内で保管能力を最大化することに役立ちます。

"予測期間中、アジア太平洋地域が市場で最大のシェアを占めると予想される"

アジア太平洋地域は、中国、日本、インドなどの急成長している経済圏で構成されています。国内での製品需要が大きく、ビジネスの成長機会も大きいことから、これらの国ではさまざまな産業の製造工場や倉庫が数多く設立されています。これらの工場は、自動車、金属・重機、半導体・エレクトロニクスなど、この地域の主要産業で使用されています。このことが、アジア太平洋地域の自動マテリアルハンドリング機器市場に有利な機会を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 顧客のビジネスに影響を与える動向/混乱

- 技術分析

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- ケーススタディ分析

- 貿易分析

- 特許分析

- 主要な会議とイベント(2023年~2025年)

- 規制状況

第6章 自動マテリアルハンドリング機器に関連する新興技術と応用

- イントロダクション

- 自動マテリアルハンドリング機器市場における提供

- ASRSの新興応用

- AGVの新興応用

- AGVで使用する新興技術

- 自動マテリアルハンドリングの未来を形成する技術動向

- インダストリー4.0フレームワークに関連する新興マテリアルハンドリング技術

第7章 屋外マテリアルハンドリング機器(定性)

- イントロダクション

- フォークリフト

- AGV

- 牽引車両

- ユニットロードキャリア

第8章 自動マテリアルハンドリング機器市場に影響を与える倉庫技術の最新動向

- イントロダクション

- 集中フルフィルメントセンター(CFC)

- マイクロフルフィルメントセンター(MFC)

- 自律型マシン

- 倉庫オートメーション

- ダークストア

第9章 自動マテリアルハンドリング機器市場:製品別

- イントロダクション

- ロボット

- 自動保管・検索システム(ASRS)

- コンベヤ・仕分けシステム

- クレーン

- 無人搬送車(AGV)

- 倉庫管理システム(WMS)

- リアルタイム位置情報システム(RLTS)

第10章 自動マテリアルハンドリング機器市場:システムタイプ別

- イントロダクション

- ユニットロード用

- バルクロード用

第11章 自動マテリアルハンドリング機器市場:産業別

- イントロダクション

- 自動車

- 化学

- 航空

- 半導体・エレクトロニクス

- Eコマース

- 食品・飲料

- 医療

- 医薬品

- 医療機器

- 金属・重機

- サードパーティロジスティクス(3PL)

- その他

第12章 自動マテリアルハンドリング機器市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋地域

- 中国

- 日本

- オーストラリア

- インド

- マレーシア

- 台湾

- インドネシア

- 韓国

- その他のアジア太平洋地域

- その他の地域

- 南米

- 中東

- アフリカ

第13章 競合情勢

- 概要

- 主要企業が採用した戦略

- 上位企業の収益分析

- 市場シェア分析

- 競合の評価象限

- 中小企業(SMES)の評価象限

- 自動マテリアルマテリアルハンドリング機器市場:企業のフットプリント

- 競合ベンチマーキング

- 競合シナリオ

第14章 企業プロファイル

- 主要企業

- DAIFUKU

- KION

- SSI SCHAEFER

- TOYOTA INDUSTRIES

- HONEYWELL INTERNATIONAL

- HYSTER-YALE MATERIAL HANDLING

- JUNGHEINRICH

- HANWHA

- JBT

- KUKA

- BEUMER

- KNAPP

- MURATA MACHINERY

- TGW LOGISTICS

- VIASTORE

- その他の企業

- ADDVERB TECHNOLOGIES

- AUTOCRIB

- AUTOMATION LOGISTIC

- AVANCON

- FERRETTO

- GRABIT

- INVATA INTRALOGISTICS

- INVIA ROBOTICS

- LOCUS ROBOTICS

- MEIDEN AMERICA

- MOBILE INDUSTRIAL ROBOTS

- WESTFALIA TECHNOLOGIES

第15章 隣接市場

- RFID市場

- イントロダクション

- タグ

- リーダー

- ソフトウェア・サービス

第16章 付録

The automated material handling equipment market is projected to reach USD 45.7 billion by 2028 from USD 30.6 billion in 2023, at a CAGR of 8.3% from 2023 to 2028. The growth of this market is attributed to the rising demand for automated material handling equipment among diverse industries and the growing number of startups offering robotics solutions for warehouse automation.

"Unit Load segment is projected to grow at a higher CAGR during 2023-2028."

Unit load material handling systems involve appropriately sized items organized into a single unit that can be moved easily. It consists in handling various items or unit formats independently, even when they are transported in large quantities or are significant in dimension. These systems are quick and economical to move several items in a single run. These systems help reduce damages and handling costs. Such systems make handling, storage, and distribution more efficient. The types of AMHE used to manage unit loads include AGVs, ASRS, and robots.

"Automotive Industry to account for the largest share of market in 2023."

The automotive industry players seek improvements in manufacturing through automated and efficient processes. These companies need to carry out their manufacturing and assembling operations efficiently by carefully handling various components and keeping track of it. The deployment of AMHE in this industry helps prevent damage to auto parts, reduce the cost of unproductive labor hours by handling inventory, and maximize storage capacity within the available floor space.

"Asia Pacific is anticipated to contribute the largest share of the market during the forecast period."

Asia Pacific consists of some of the fastest-growing economies-such as China, Japan, and India. Substantial domestic demand for products and significant business growth opportunities have led to the establishment of number of manufacturing and warehousing plants of various industries in the countries. These plants are of major industries such as automotive, metals & heavy machinery, and semiconductor & electronics, in the region. This in turn is offering lucrative opportunities for the automated material handling equipment market in Asia Pacific.

The break-up of the profiles of primary participants:

- By Company Type - Tier 1 - 45%, Tier 2 - 30%, and Tier 3 - 25%

- By Designation - C-level Executives - 35%, Directors - 45%, and Others - 20%

- By Region - North America - 30%, Europe - 25%, Asia Pacific - 35%, and Rest of the World - 10%

Major players in the automated material handling equipment market include Daifuku (Japan), KION (Germany), SSI Schaefer (Germany), Toyota Industries (Japan), and Honeywell International (US).

Research Coverage

The report segments the automated material handling equipment market into product, system type, industry, and region. The report also comprehensively reviews drivers, restraints, opportunities, and challenges influencing market growth. The report also covers qualitative aspects in addition to the quantitative aspects of the market.

Reasons to buy the report:

The report will help the market leaders/new entrants with information on the closest approximate revenues for the overall automated material handling equipment market and related segments. This report will help stakeholders understand the competitive landscape and gain more insights to strengthen their position in the market and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing penetration of ASRS in the e-commerce industry, growing number of startups offering robotic solutions for warehouse automation, high labor costs, and safety concerns, paradigm shift from mass production to mass customization), restraints (Requirement for significant capital, high integration, and switching costs), opportunities (Substantial industrial growth in emerging economies, existence of huge intralogistics sector in Southeast Asia, growing extent of order customization and personalization), and challenges (immense technical challenges related to sensing elements, production and revenue losses due to unwanted equipment downtime) influencing the growth of the automated material handling equipment market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the automated material handling equipment market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the automated material handling equipment market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the automated material handling equipment market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players like Daifuku (Japan), KION (Germany), SSI Schaefer (Germany), Toyota Industries (Japan), and Honeywell International (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.4 STUDY SCOPE

- 1.4.1 MARKETS COVERED

- FIGURE 1 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: SEGMENTATION

- 1.4.2 REGIONAL SCOPE

- 1.4.3 YEARS CONSIDERED

- 1.5 CURRENCY

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews with experts

- 2.1.2.2 Breakdown of primaries

- 2.1.2.3 Key data from primary sources

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.3.1 Key industry insights

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to derive market size using bottom-up analysis

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to derive market size using bottom-up analysis

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY (SUPPLY SIDE): REVENUE GENERATED BY KEY PLAYERS FROM AGV BUSINESS

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 6 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 PARAMETERS CONSIDERED TO ANALYZE IMPACT OF RECESSION ON AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- 2.6 LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 7 ASRS SEGMENT HELD LARGEST SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET IN 2022

- FIGURE 8 UNIT LOAD MATERIAL HANDLING SYSTEM SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 9 AUTOMOTIVE SEGMENT HELD LARGEST MARKET SHARE IN 2022

- FIGURE 10 ASIA PACIFIC HELD LARGEST MARKET SHARE IN 2022

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- FIGURE 11 RISING DEPLOYMENT OF AUTOMATION SOLUTIONS IN WAREHOUSES

- 4.2 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT

- FIGURE 12 ASRS SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.3 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET FOR AGV, BY TYPE

- FIGURE 13 TOW VEHICLE SEGMENT HELD LARGEST SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET FOR AGV IN 2022

- 4.4 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY

- FIGURE 14 AUTOMOTIVE SEGMENT TO HOLD LARGEST SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET IN 2023

- 4.5 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY REGION

- FIGURE 15 CANADA TO REGISTER HIGHEST CAGR IN AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 16 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing penetration of automated storage and retrieval systems into e-commerce industry

- 5.2.1.2 Increasing number of startups offering robotic solutions for warehouse automation

- 5.2.1.3 Rising demand for automated material handling equipment in various industries

- FIGURE 17 GLOBAL VEHICLE PRODUCTION, 2017-2021 (MILLION UNITS)

- 5.2.1.4 High labor costs and safety concerns

- 5.2.1.5 Paradigm shift toward mass customization from mass production

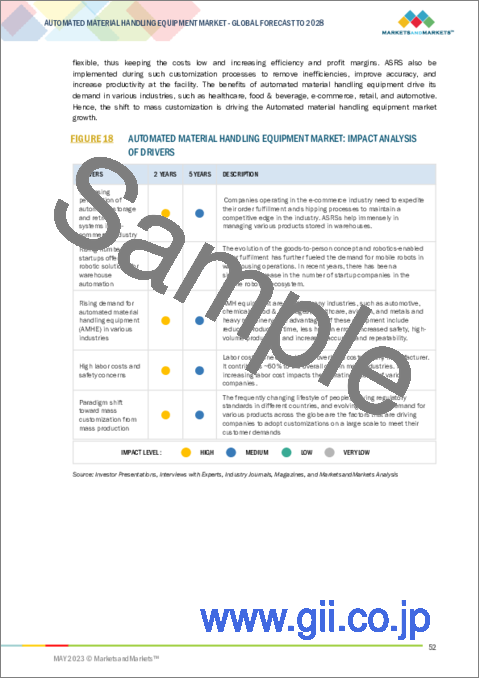

- FIGURE 18 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: IMPACT ANALYSIS OF DRIVERS

- 5.2.2 RESTRAINTS

- 5.2.2.1 Requirement for high capital by small and medium-sized enterprises (SMEs) to deploy automated material handling equipment

- 5.2.2.2 High integration and switching costs

- 5.2.2.3 Inadequate technical expertise to manage system operations

- FIGURE 19 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: IMPACT ANALYSIS OF RESTRAINTS

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing extent of order customization and personalization

- 5.2.3.2 Digitalization of supply chain processes with integration of Internet of Things (IoT) and automated material handling equipment

- 5.2.3.3 Substantial industrial growth in emerging economies

- 5.2.3.4 Expanding intralogistics sector in Southeast Asia

- 5.2.3.5 Potential growth prospects in healthcare industry

- FIGURE 20 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: IMPACT ANALYSIS OF OPPORTUNITIES

- 5.2.4 CHALLENGES

- 5.2.4.1 Production and revenue losses attributed to unwanted equipment downtime

- 5.2.4.2 Technical challenges related to sensing elements

- 5.2.4.3 Development of flexible and scalable automated material equipment with constant technological advancements

- FIGURE 21 AUTOMATED MATERIAL HANDLING SYSTEM MARKET: IMPACT ANALYSIS OF CHALLENGES

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 22 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- FIGURE 23 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: ECOSYSTEM ANALYSIS

- TABLE 1 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF ASRS OFFERED BY KEY PLAYERS, BY TYPE

- FIGURE 24 AVERAGE PROJECT COST OF ASRS BASED ON TYPE, BY COMPANY

- TABLE 2 AVERAGE PROJECT COST OF ASRS BASED ON TYPE, BY COMPANY (USD)

- 5.5.2 AVERAGE SELLING PRICE OF COLLABORATIVE ROBOTS BASED ON PAYLOAD, BY KEY PLAYER

- FIGURE 25 AVERAGE SELLING PRICE OF COLLABORATIVE ROBOTS BASED ON PAYLOAD, BY KEY PLAYERS

- TABLE 3 AVERAGE SELLING PRICE OF COLLABORATIVE ROBOTS BASED ON PAYLOAD, BY KEY PLAYERS

- 5.5.3 AVERAGE SELLING PRICE TREND

- TABLE 4 AVERAGE SELLING PRICE OF AGVS

- TABLE 5 AVERAGE SELLING PRICE OF AGVS, BY REGION

- FIGURE 26 AVERAGE SELLING PRICE OF AGVS, 2019-2028

- TABLE 6 AVERAGE SELLING PRICE OF ROBOTS

- TABLE 7 AVERAGE SELLING PRICE OF SORTATION SYSTEMS

- TABLE 8 AVERAGE SELLING PRICE OF CONVEYOR SYSTEMS

- TABLE 9 AVERAGE SELLING PRICE OF CRANES

- TABLE 10 PRICING OF WAREHOUSE MANAGEMENT SYSTEMS

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 27 REVENUE SHIFT FOR AUTOMATED MATERIAL HANDLING EQUIPMENT PROVIDERS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 WEARABLE TECHNOLOGY

- 5.7.2 PREDICTIVE ANALYTICS

- 5.7.3 MACHINE LEARNING PLATFORM

- 5.7.4 DIGITAL TWIN MODEL BUILDER

- 5.7.5 VOICE RECOGNITION TECHNOLOGY

- 5.7.6 5G

- 5.7.7 IOT

- 5.7.8 INDUSTRY 4.0

- 5.7.9 ROBOTIC PROCESS AUTOMATION

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 28 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 11 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE INDUSTRIES

- TABLE 12 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE INDUSTRIES (%)

- 5.9.2 BUYING CRITERIA

- FIGURE 30 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- TABLE 13 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- 5.10 CASE STUDY ANALYSIS

- TABLE 14 ASSESSMENT OF FEINTOOL SYSTEM PARTS OBERTSHAUSEN

- TABLE 15 ASSESSMENT OF REITAN DISTRIBUTION

- TABLE 16 ASSESSMENT OF RM RESOURCES

- TABLE 17 ASSESSMENT FOR LARGE AGV FLEET

- TABLE 18 ASSESSMENT FOR CUSTOM-ENGINEERED AGVS

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT SCENARIO

- FIGURE 31 IMPORT DATA, BY KEY COUNTRY, 2017-2021 (USD MILLION)

- 5.11.2 EXPORT SCENARIO

- FIGURE 32 EXPORT DATA, BY KEY COUNTRY, 2017-2021 (USD MILLION)

- 5.12 PATENT ANALYSIS

- FIGURE 33 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS IN LAST 10 YEARS

- TABLE 19 TOP 20 PATENT OWNERS IN US IN LAST 10 YEARS

- FIGURE 34 NUMBER OF PATENTS GRANTED PER YEAR FROM 2012 TO 2022

- TABLE 20 LIST OF PATENTS RELATED TO AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- 5.13 KEY CONFERENCES AND EVENTS, 2023-2025

- TABLE 21 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: CONFERENCES AND EVENTS

- 5.14 REGULATORY LANDSCAPE

- 5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 22 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 24 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 25 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.2 STANDARDS AND REGULATIONS RELATED TO AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- 5.14.3 SAFETY STANDARDS FOR ASRS

- TABLE 26 SAFETY STANDARDS FOR ASRS

- 5.14.4 SAFETY STANDARDS FOR AGVS

- TABLE 27 SAFETY STANDARDS FOR AGVS

6 EMERGING TECHNOLOGIES AND APPLICATIONS RELATED TO AUTOMATED MATERIAL HANDLING EQUIPMENT

- 6.1 INTRODUCTION

- 6.2 OFFERINGS IN AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- FIGURE 35 OFFERINGS IN AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- 6.2.1 HARDWARE

- 6.2.2 SOFTWARE

- FIGURE 36 WES INTEGRATES KEY FUNCTIONALITIES OF WMS AND WES

- 6.2.2.1 Services

- 6.2.2.2 Maintenance and repair

- 6.2.2.3 Training

- 6.2.2.4 Software upgrade

- 6.3 EMERGING APPLICATIONS OF ASRS

- 6.3.1 HOSPITALS

- 6.3.2 ACADEMIC INSTITUTIONS

- 6.4 EMERGING APPLICATIONS OF AGVS

- 6.4.1 HOSPITALS

- 6.4.2 THEME PARKS

- 6.5 EMERGING TECHNOLOGIES USED IN AGVS

- 6.5.1 LIDAR SENSORS

- 6.5.2 CAMERA VISION

- 6.5.3 DUAL-MODE AGVS

- 6.6 TECHNOLOGICAL TRENDS SHAPING FUTURE OF AUTOMATED MATERIAL HANDLING

- 6.6.1 BIG DATA AND ANALYTICS

- 6.6.2 INTERNET OF THINGS (IOT)

- 6.6.3 MOBILE TECHNOLOGY

- 6.6.4 VOICE PICKING

- 6.6.5 ADVANCED ROBOTICS

- 6.6.6 AUTONOMOUS VEHICLES

- 6.7 EMERGING MATERIAL HANDLING TECHNOLOGIES ASSOCIATED WITH INDUSTRY 4.0 FRAMEWORK

- 6.7.1 AUTONOMOUS MOBILE ROBOT (AMR)

- 6.7.2 COBOT

- 6.7.3 3D MOBILE ROBOT

7 OUTDOOR MATERIAL HANDLING EQUIPMENT (QUALITATIVE)

- 7.1 INTRODUCTION

- 7.2 FORKLIFT

- 7.3 AGV

- 7.3.1 TOW VEHICLE

- 7.3.2 UNIT LOAD CARRIER

8 LATEST TRENDS IN WAREHOUSING TECHNOLOGIES IMPACTING AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- 8.1 INTRODUCTION

- 8.2 CENTRALIZED FULFILLMENT CENTER (CFC)

- 8.3 MICRO FULFILLMENT CENTER (MFC)

- 8.3.1 DEVELOPMENTS IN MICRO FULFILLMENT CENTERS (MFCS)

- FIGURE 37 KEY ELEMENTS POWERING DEVELOPMENTS IN MICRO FULFILLMENT CENTERS (MFCS)

- 8.3.2 ADVANTAGES ASSOCIATED WITH MICRO FULFILLMENT CENTERS (MFCS) OVER CENTRALIZED FULFILMENT CENTERS (CFCS)

- 8.3.3 MICRO FULFILLMENT CENTER (MFC): ECOSYSTEM ANALYSIS

- FIGURE 38 ECOSYSTEM OF MICRO FULFILLMENT CENTER (MFC)

- 8.3.4 MAJOR COMPANIES LEADING WAYS TO MICRO FULFILLMENT CENTERS (MFCS)

- 8.3.5 KEY TECHNOLOGIES USED IN MICRO FULFILLMENT CENTERS (MFCS)

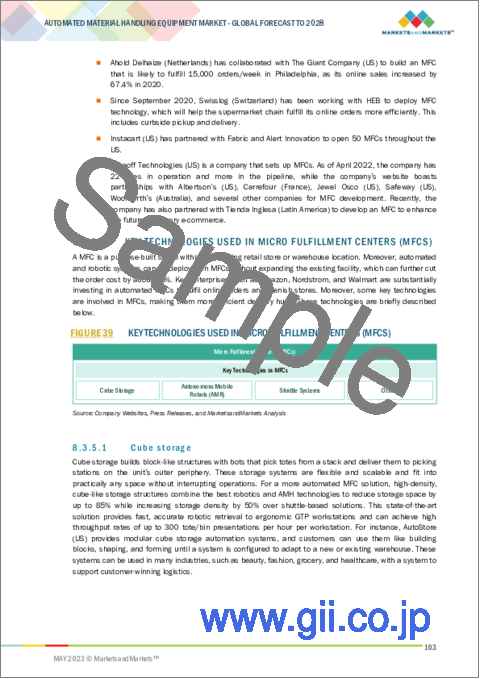

- FIGURE 39 KEY TECHNOLOGIES USED IN MICRO FULFILLMENT CENTERS (MFCS)

- 8.3.5.1 Cube storage

- 8.3.5.2 Autonomous mobile robot (AMR)

- 8.3.5.3 Shuttle system

- 8.3.5.4 Others

- 8.3.6 FUNDING IN MICRO FULFILLMENT CENTERS (MFCS)

- TABLE 28 OVERVIEW OF RECENT MAJOR FUNDING FOR MICRO FULFILLMENT CENTERS (MFCS)

- 8.4 AUTONOMOUS MACHINES

- 8.5 WAREHOUSE AUTOMATION

- 8.6 DARK STORES

9 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- FIGURE 40 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT

- FIGURE 41 ASRS SEGMENT TO HOLD LARGEST SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET DURING FORECAST PERIOD

- TABLE 29 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 30 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 9.2 ROBOT

- TABLE 31 ROBOT: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 32 ROBOT: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 33 ROBOT: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 34 ROBOT: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 35 ROBOT: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 36 ROBOT: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 9.2.1 TRADITIONAL ROBOT

- 9.2.1.1 Articulated robot

- 9.2.1.1.1 Used for inspection, testing, and packaging in automotive and metals industries

- 9.2.1.1 Articulated robot

- FIGURE 42 ILLUSTRATION OF 6-AXIS ARTICULATED ROBOT

- TABLE 37 ADVANTAGES, DISADVANTAGES, AND APPLICATIONS OF ARTICULATED ROBOTS

- 9.2.1.2 Cylindrical robot

- 9.2.1.2.1 Ensures high accuracy and repeatability in industrial operations

- 9.2.1.3 Selective compliance assembly robot arm (SCARA) robot

- 9.2.1.3.1 Used for faster assembly and palletizing applications

- 9.2.1.2 Cylindrical robot

- FIGURE 43 ILLUSTRATION OF 4-AXIS SCARA ROBOT

- TABLE 38 ADVANTAGES, DISADVANTAGES, AND APPLICATIONS OF SCARA ROBOTS

- 9.2.1.4 Delta robot

- 9.2.1.4.1 Used for fast pick-and-place operations in process industries

- 9.2.1.4 Delta robot

- FIGURE 44 ILLUSTRATION OF PARALLEL ROBOT

- TABLE 39 PARALLEL ROBOT: SUMMARY TABLE 126 9.2.1.5 Cartesian robot

- 9.2.1.5.1 Easily configured for precision applications

- FIGURE 45 ILLUSTRATION OF CARTESIAN ROBOT

- TABLE 40 ADVANTAGES, DISADVANTAGES, AND APPLICATIONS OF CARTESIAN ROBOTS

- 9.2.2 COLLABORATIVE ROBOT

- 9.2.2.1 Used to achieve higher efficiency in production

- 9.2.3 AUTONOMOUS MOBILE ROBOT (AMR)

- 9.2.3.1 Offers efficient and flexible route for navigation

- 9.3 AUTOMATED STORAGE AND RETRIEVAL SYSTEM (ASRS)

- TABLE 41 ASRS: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 42 ASRS: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 43 ASRS: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 44 ASRS: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2023-2028 (USD MILLION)

- FIGURE 46 UNIT LOAD SEGMENT TO ACCOUNT FOR LARGEST SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET FOR ASRS DURING FORECAST PERIOD

- TABLE 45 ASRS: AUTOMATED MATERIAL HANDLING MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 46 ASRS: AUTOMATED MATERIAL HANDLING MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 9.3.1 UNIT LOAD AUTOMATED STORAGE AND RETRIEVAL SYSTEM (ASRS)

- 9.3.1.1 Used to resolve operational and productivity issues

- 9.3.2 MINI LOAD AUTOMATED STORAGE AND RETRIEVAL SYSTEM (ASRS)

- 9.3.2.1 Widely used in pharmaceutical and medical industries

- 9.3.3 VERTICAL LIFT MODULE (VLM)

- 9.3.3.1 Increases productivity and improves accuracy levels

- 9.3.4 CAROUSEL

- 9.3.4.1 Vertical carousel

- 9.3.4.1.1 Improves inventory accuracy and productivity

- 9.3.4.2 Horizontal carousel

- 9.3.4.2.1 Improves flexibility and efficiency in picking

- 9.3.4.1 Vertical carousel

- 9.3.5 MID LOAD AUTOMATED STORAGE AND RETRIEVAL SYSTEM (ASRS)

- 9.3.5.1 Equipped with features of mini load and unit load ASRS

- 9.4 CONVEYOR & SORTATION SYSTEM

- 9.4.1 BELT CONVEYOR

- 9.4.1.1 Most economical conveyor used across various industries

- 9.4.2 ROLLER CONVEYOR

- 9.4.2.1 Used in warehouses and manufacturing facilities

- 9.4.3 OVERHEAD CONVEYOR

- 9.4.3.1 Well-suited for e-commerce and retail applications

- 9.4.4 SCREW CONVEYOR

- 9.4.4.1 Widely used in food & beverage and chemical industries

- TABLE 47 CONVEYOR & SORTATION SYSTEM: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 48 CONVEYOR & SORTATION SYSTEM: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 49 CONVEYOR & SORTATION SYSTEM: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 50 CONVEYOR & SORTATION SYSTEM: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 51 CONVEYOR & SORTATION SYSTEM: AUTOMATED MATERIAL HANDLING MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 52 CONVEYOR & SORTATION SYSTEM: AUTOMATED MATERIAL HANDLING MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 9.4.1 BELT CONVEYOR

- 9.5 CRANE

- 9.5.1 USED TO MOVE MATERIALS OVER VARIABLE PATHS AUTOMATICALLY

- FIGURE 47 AUTOMOTIVE SEGMENT TO HOLD LARGEST SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET FOR CRANE DURING FORECAST PERIOD

- TABLE 53 CRANE: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 54 CRANE: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 55 CRANE: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 56 CRANE: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.6 AUTOMATED GUIDED VEHICLE (AGV)

- TABLE 57 AGV: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 58 AGV: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 59 AGV: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 60 AGV: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.6.1 AUTOMATIC GUIDED VEHICLE (AGV) MARKET, BY TYPE

- 9.6.1.1 Tow vehicle

- 9.6.1.1.1 Prominently used in automotive industry

- 9.6.1.2 Unit load carrier

- 9.6.1.2.1 Widely adopted in heavy manufacturing industries

- 9.6.1.3 Pallet truck

- 9.6.1.3.1 Widely used in warehouses

- 9.6.1.4 Assembly line vehicle

- 9.6.1.4.1 Assists in transportation for serial assembly operations

- 9.6.1.5 Forklift truck

- 9.6.1.5.1 Used to pick and transport pallets

- 9.6.1.6 Others

- 9.6.1.1 Tow vehicle

- TABLE 61 AGV: AUTOMATED MATERIAL HANDLING MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 62 AGV: AUTOMATED MATERIAL HANDLING MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 63 LIST OF MAJOR AGV VENDORS

- 9.6.2 AUTOMATIC GUIDED VEHICLE (AGV) MARKET, BY NAVIGATION TECHNOLOGY

- FIGURE 48 NAVIGATION TECHNOLOGIES USED IN AGVS

- 9.6.2.1 Laser guidance

- 9.6.2.1.1 Offers accurate navigation

- 9.6.2.2 Magnetic guidance

- 9.6.2.2.1 Easy to install and reliable

- 9.6.2.3 Inductive guidance

- 9.6.2.3.1 Works in harsh environments and heavy traffic

- 9.6.2.4 Optical tape guidance

- 9.6.2.4.1 Uses colored floor linings to provide path for AGVs

- 9.6.2.5 Vision guidance

- 9.6.2.5.1 Helps manufacturers in supply chain management

- 9.6.2.6 Others

- 9.6.2.1 Laser guidance

- TABLE 64 AGV: AUTOMATED MATERIAL HANDLING MARKET, BY NAVIGATION TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 65 AGV: AUTOMATED MATERIAL HANDLING MARKET, BY NAVIGATION TECHNOLOGY, 2023-2028 (USD MILLION)

- 9.7 WAREHOUSE MANAGEMENT SYSTEM (WMS)

- TABLE 66 WMS: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 67 WMS: AUTOMATED MATERIAL HANDLING MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 68 WMS: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 69 WMS: AUTOMATED MATERIAL HANDLING MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.7.1 WAREHOUSE MANAGEMENT SYSTEM (WMS) MARKET, BY DEPLOYMENT TYPE

- 9.7.1.1 On-premises

- 9.7.1.1.1 Provides complete control and security to organizations

- 9.7.1.2 Cloud

- 9.7.1.2.1 Offers low-cost, scalable, and faster solutions to various organizations

- 9.7.1.1 On-premises

- TABLE 70 WMS: AUTOMATED MATERIAL HANDLING MARKET, BY DEPLOYMENT TYPE, 2019-2022 (USD MILLION)

- TABLE 71 WMS: AUTOMATED MATERIAL HANDLING MARKET, BY DEPLOYMENT TYPE, 2023-2028 (USD MILLION)

- 9.8 REAL-TIME LOCATION SYSTEMS (RLTS)

- TABLE 72 REAL-TIME LOCATION SYSTEM (RTLS) MARKET FOR WAREHOUSE MANAGEMENT, 2019-2022 (USD MILLION)

- TABLE 73 REAL-TIME LOCATION SYSTEM (RTLS) MARKET FOR WAREHOUSE MANAGEMENT, 2023-2028 (USD MILLION)

10 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY SYSTEM TYPE

- 10.1 INTRODUCTION

- FIGURE 49 UNIT LOAD SEGMENT TO HOLD LARGER SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET DURING FORECAST PERIOD

- TABLE 74 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY SYSTEM TYPE, 2019-2022 (USD MILLION)

- TABLE 75 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY SYSTEM TYPE, 2023-2028 (USD MILLION)

- 10.2 UNIT LOAD MATERIAL HANDLING SYSTEM

- 10.2.1 ADVANTAGES ASSOCIATED WITH UNIT LOAD MATERIAL HANDLING SYSTEMS

- 10.2.2 DISADVANTAGES ASSOCIATED WITH UNIT LOAD MATERIAL HANDLING SYSTEMS

- 10.3 BULK LOAD MATERIAL HANDLING SYSTEM

- 10.3.1 ADVANTAGES ASSOCIATED WITH BULK LOAD MATERIAL HANDLING SYSTEMS

- 10.3.2 DISADVANTAGES ASSOCIATED WITH BULK LOAD MATERIAL HANDLING SYSTEMS

11 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY

- 11.1 INTRODUCTION

- FIGURE 50 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY

- FIGURE 51 AUTOMOTIVE SEGMENT TO HOLD LARGEST SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET FROM 2023 TO 2028

- TABLE 76 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 77 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- 11.2 AUTOMOTIVE

- 11.2.1 RISING USE OF AUTOMATED GUIDED VEHICLES (AGVS) AND AUTOMATED STORAGE AND RETRIEVAL SYSTEMS (ASRS) TO ENHANCE MANUFACTURING PROCESSES

- TABLE 78 AUTOMOTIVE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 79 AUTOMOTIVE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 11.3 CHEMICAL

- 11.3.1 INCLINATION OF CHEMICAL INDUSTRY PLAYERS TOWARD DIGITALIZATION

- TABLE 80 CHEMICAL: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 81 CHEMICAL: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 11.4 AVIATION

- 11.4.1 GROWING NEED FOR SYSTEMATIC MANUFACTURING AND ASSEMBLY OPERATIONS IN AVIATION INDUSTRY

- TABLE 82 AVIATION: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 83 AVIATION: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 11.5 SEMICONDUCTOR & ELECTRONICS

- 11.5.1 GROWING NEED FOR ACCURACY IN SEMICONDUCTOR AND ELECTRONICS MANUFACTURING

- TABLE 84 SEMICONDUCTOR & ELECTRONICS: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 85 SEMICONDUCTOR & ELECTRONICS: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 11.6 E-COMMERCE

- 11.6.1 GROWING USE OF ROBOTS AND AUTOMATED GUIDED VEHICLES (AGVS) IN E-COMMERCE INDUSTRY TO REDUCE TRANSIT TIME

- TABLE 86 E-COMMERCE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 87 E-COMMERCE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 11.7 FOOD & BEVERAGE

- 11.7.1 CONSTANT NEED FOR EFFICIENT STORAGE, RETRIEVAL, AND TRANSIT SOLUTIONS

- FIGURE 52 WMS SEGMENT TO REGISTER HIGHEST CAGR IN AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET FOR FOOD & BEVERAGE INDUSTRY DURING FORECAST PERIOD

- TABLE 88 FOOD & BEVERAGE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 89 FOOD & BEVERAGE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 11.8 HEALTHCARE

- 11.8.1 INCREASED USE OF AUTOMATED MATERIAL HANDLING EQUIPMENT FOR MANUFACTURING, STORING, AND DISTRIBUTION BY HEALTHCARE COMPANIES

- TABLE 90 HEALTHCARE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 91 HEALTHCARE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- FIGURE 53 PHARMACEUTICAL SEGMENT TO HOLD LARGER SHARE OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET FOR HEALTHCARE INDUSTRY DURING FORECAST PERIOD

- TABLE 92 HEALTHCARE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY TYPE, 2019-2022 (USD MILLION)

- TABLE 93 HEALTHCARE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY TYPE, 2023-2028 (USD MILLION)

- 11.8.2 PHARMACEUTICAL

- 11.8.2.1 AGV, ASRS, and conveyors majorly used in pharmaceutical industry

- 11.8.3 MEDICAL DEVICE

- 11.8.3.1 Automated material handling equipment find applications in medical device manufacturing

- 11.9 METALS & HEAVY MACHINERY

- 11.9.1 RISING USE OF AUTOMATED MATERIAL HANDLING EQUIPMENT TO EASE WORKFLOW IN METALS & HEAVY MACHINERY INDUSTRIES

- TABLE 94 METALS & HEAVY MACHINERY: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 95 METALS & HEAVY MACHINERY: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 11.10 THIRD-PARTY LOGISTICS (3PL)

- 11.10.1 OPTIMIZATION OF LOGISTICS PROCESSES USING AUTOMATED MATERIAL HANDLING EQUIPMENT

- TABLE 96 3PL: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 97 3PL: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- 11.11 OTHERS

- TABLE 98 OTHERS: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 99 OTHERS: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

12 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY REGION

- 12.1 INTRODUCTION

- FIGURE 54 CANADA TO REGISTER HIGHEST CAGR IN AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET FROM 2023 TO 2028

- TABLE 100 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 101 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.2 NORTH AMERICA

- 12.2.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 55 NORTH AMERICA: SNAPSHOT OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- TABLE 102 NORTH AMERICA: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 103 NORTH AMERICA: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- TABLE 104 NORTH AMERICA: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 105 NORTH AMERICA: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 106 NORTH AMERICA: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 107 NORTH AMERICA: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 12.2.2 US

- 12.2.2.1 Booming e-commerce industry

- 12.2.3 CANADA

- 12.2.3.1 Expanding automotive industry

- 12.2.4 MEXICO

- 12.2.4.1 Rapid industrial developments

- 12.3 EUROPE

- 12.3.1 EUROPE: RECESSION IMPACT

- FIGURE 56 EUROPE: SNAPSHOT OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- TABLE 108 EUROPE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 109 EUROPE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- TABLE 110 EUROPE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 111 EUROPE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 112 EUROPE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 113 EUROPE: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 12.3.2 GERMANY

- 12.3.2.1 Rising demand for automated material handling equipment in automotive industry

- 12.3.3 UK

- 12.3.3.1 Rising adoption of warehouse automation solutions in various industries

- 12.3.4 FRANCE

- 12.3.4.1 Increased use in e-commerce industry

- 12.3.5 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 57 ASIA PACIFIC: SNAPSHOT OF AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET

- TABLE 114 ASIA PACIFIC: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 115 ASIA PACIFIC: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- TABLE 116 ASIA PACIFIC: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 117 ASIA PACIFIC: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 118 ASIA PACIFIC: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 119 ASIA PACIFIC: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 12.4.2 CHINA

- 12.4.2.1 Expanding automotive and electronics industries

- 12.4.3 JAPAN

- 12.4.3.1 Thriving e-commerce industry

- 12.4.4 AUSTRALIA

- 12.4.4.1 Substantial adoption of automated material handling equipment in manufacturing sector

- 12.4.5 INDIA

- 12.4.5.1 Rapid industrial development

- 12.4.6 MALAYSIA

- 12.4.6.1 Growing use of automated material handling equipment in warehouses of e-commerce companies

- 12.4.7 TAIWAN

- 12.4.7.1 Rising adoption of automation technologies in industrial manufacturing

- 12.4.8 INDONESIA

- 12.4.8.1 Healthy growth of e-commerce industry

- 12.4.9 SOUTH KOREA

- 12.4.9.1 Technological advancements and high focus on development of quality products in semiconductor & electronics industry

- 12.4.10 REST OF ASIA PACIFIC

- 12.5 ROW

- 12.5.1 ROW: RECESSION IMPACT

- TABLE 120 ROW: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2019-2022 (USD MILLION)

- TABLE 121 ROW: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY PRODUCT, 2023-2028 (USD MILLION)

- TABLE 122 ROW: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 123 ROW: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 124 ROW: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 125 ROW: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.5.2 SOUTH AMERICA

- 12.5.2.1 Rising adoption of warehouse automation solutions in various industries

- 12.5.3 MIDDLE EAST

- TABLE 126 MIDDLE EAST: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 127 MIDDLE EAST: AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 12.5.3.1 UAE

- 12.5.3.1.1 Rising demand in manufacturing and healthcare sectors

- 12.5.3.2 Saudi Arabia

- 12.5.3.2.1 Constant developments in aviation, food & beverage, and pharmaceutical industries

- 12.5.3.3 Rest of Middle East

- 12.5.3.1 UAE

- 12.5.4 AFRICA

- 12.5.4.1 High focus on warehouse automation

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 128 OVERVIEW OF STRATEGIES ADOPTED BY AUTOMATED MATERIAL HANDLING EQUIPMENT VENDORS

- 13.3 REVENUE ANALYSIS OF TOP COMPANIES

- FIGURE 58 FIVE-YEAR REVENUE ANALYSIS OF TOP FIVE PLAYERS IN AGV MARKET

- FIGURE 59 FIVE-YEAR REVENUE ANALYSIS OF TOP TWO PLAYERS IN ASRS MARKET

- 13.4 MARKET SHARE ANALYSIS

- TABLE 129 AGV MARKET SHARE ANALYSIS (2022)

- FIGURE 60 AGV MARKET: SHARE OF KEY PLAYERS

- TABLE 130 ASRS MARKET SHARE ANALYSIS (2022)

- FIGURE 61 ASRS MARKET: SHARE OF KEY PLAYERS

- 13.5 COMPETITIVE EVALUATION QUADRANT

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- FIGURE 62 AGV MARKET (GLOBAL): COMPETITIVE EVALUATION QUADRANT, 2022

- FIGURE 63 ASRS MARKET (GLOBAL): COMPETITIVE EVALUATION QUADRANT, 2022

- 13.6 SMALL AND MEDIUM-SIZED ENTERPRISES (SMES) EVALUATION QUADRANT

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- FIGURE 64 AGV MARKET (GLOBAL): SME EVALUATION QUADRANT, 2022

- FIGURE 65 ASRS MARKET (GLOBAL): SME EVALUATION QUADRANT, 2022

- 13.7 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: COMPANY FOOTPRINT

- TABLE 131 COMPANY FOOTPRINT

- TABLE 132 PRODUCT: COMPANY FOOTPRINT

- TABLE 133 INDUSTRY: COMPANY FOOTPRINT

- TABLE 134 REGION: COMPANY FOOTPRINT

- 13.8 COMPETITIVE BENCHMARKING

- TABLE 135 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: LIST OF KEYS STARTUPS/SMES

- TABLE 136 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 13.9 COMPETITIVE SCENARIO

- TABLE 137 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: PRODUCT LAUNCHES, 2021-2022

- TABLE 138 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: DEALS, 2020-2022

- TABLE 139 AUTOMATED MATERIAL HANDLING EQUIPMENT MARKET: OTHERS, 2022

14 COMPANY PROFILES

(Business Overview, Products Offered, Recent Developments, MnM View Right to win, Strategic choices made, Weaknesses and competitive threats)

- 14.1 KEY PLAYERS

- 14.1.1 DAIFUKU

- TABLE 140 DAIFUKU: COMPANY OVERVIEW

- FIGURE 66 DAIFUKU: COMPANY SNAPSHOT

- TABLE 141 DAIFUKU: PRODUCTS OFFERED

- TABLE 142 DAIFUKU: DEALS

- TABLE 143 DAIFUKU: OTHERS

- 14.1.2 KION

- TABLE 144 KION: COMPANY OVERVIEW

- FIGURE 67 KION: COMPANY SNAPSHOT

- TABLE 145 KION: PRODUCTS OFFERED

- TABLE 146 KION: DEALS

- TABLE 147 KION: OTHERS

- 14.1.3 SSI SCHAEFER

- TABLE 148 SSI SCHAEFER: COMPANY OVERVIEW

- TABLE 149 SSI SCHAEFER: PRODUCTS OFFERED

- TABLE 150 SSI SCHAEFER: OTHERS

- 14.1.4 TOYOTA INDUSTRIES

- TABLE 151 TOYOTA INDUSTRIES: COMPANY OVERVIEW

- FIGURE 68 TOYOTA INDUSTRIES: COMPANY SNAPSHOT

- TABLE 152 TOYOTA INDUSTRIES: PRODUCTS OFFERED

- TABLE 153 TOYOTA INDUSTRIES: PRODUCT LAUNCHES

- TABLE 154 TOYOTA INDUSTRIES: DEALS

- TABLE 155 TOYOTA INDUSTRIES: OTHERS

- 14.1.5 HONEYWELL INTERNATIONAL

- TABLE 156 HONEYWELL INTERNATIONAL: COMPANY OVERVIEW

- FIGURE 69 HONEYWELL INTERNATIONAL: COMPANY SNAPSHOT

- TABLE 157 HONEYWELL INTERNATIONAL: PRODUCTS OFFERED

- 14.1.6 HYSTER-YALE MATERIAL HANDLING

- TABLE 158 HYSTER-YALE MATERIAL HANDLING: COMPANY OVERVIEW

- FIGURE 70 HYSTER-YALE MATERIAL HANDLING: COMPANY SNAPSHOT

- TABLE 159 HYSTER-YALE MATERIAL HANDLING: PRODUCTS OFFERED

- TABLE 160 HYSTER-YALE MATERIAL HANDLING: PRODUCT LAUNCHES

- TABLE 161 HYSTER-YALE OTHERS

- 14.1.7 JUNGHEINRICH

- TABLE 162 JUNGHEINRICH: COMPANY OVERVIEW

- FIGURE 71 JUNGHEINRICH: COMPANY SNAPSHOT

- TABLE 163 JUNGHEINRICH: PRODUCTS OFFERED

- TABLE 164 JUNGHEINRICH: DEALS

- TABLE 165 JUNGHEINRICH: OTHERS

- 14.1.8 HANWHA

- TABLE 166 HANWHA: COMPANY OVERVIEW

- FIGURE 72 HANWHA: COMPANY SNAPSHOT

- TABLE 167 HANWHA: PRODUCTS OFFERED

- TABLE 168 HANWHA: DEALS

- TABLE 169 HANWHA: OTHERS

- 14.1.9 JBT

- TABLE 170 JBT: COMPANY OVERVIEW

- FIGURE 73 JBT: COMPANY SNAPSHOT

- TABLE 171 JBT: PRODUCTS OFFERED

- 14.1.10 KUKA

- TABLE 172 KUKA: COMPANY OVERVIEW

- FIGURE 74 KUKA: COMPANY SNAPSHOT

- TABLE 173 KUKA: PRODUCTS OFFERED

- TABLE 174 KUKA: OTHERS

- 14.1.11 BEUMER

- TABLE 175 BEUMER: COMPANY OVERVIEW

- TABLE 176 BEUMER: PRODUCTS OFFERED

- TABLE 177 BEUMER: PRODUCT LAUNCHES

- TABLE 178 BEUMER: DEALS

- TABLE 179 BEUMER: OTHERS

- 14.1.12 KNAPP

- TABLE 180 KNAPP: COMPANY OVERVIEW

- TABLE 181 KNAPP: PRODUCTS OFFERED

- TABLE 182 KNAPP: DEALS

- TABLE 183 KNAPP: OTHERS

- 14.1.13 MURATA MACHINERY

- TABLE 184 MURATA MACHINERY: COMPANY OVERVIEW

- TABLE 185 MURATA MACHINERY: PRODUCTS OFFERED

- TABLE 186 MURATA MACHINERY: DEALS

- TABLE 187 MURATA MACHINERY: OTHERS

- 14.1.14 TGW LOGISTICS

- TABLE 188 TGW LOGISTICS: COMPANY OVERVIEW

- TABLE 189 TGW LOGISTICS: PRODUCTS OFFERED

- TABLE 190 TGW LOGISTICS: PRODUCT LAUNCHES

- TABLE 191 TGW LOGISTICS: DEALS

- TABLE 192 TGW LOGISTICS: OTHERS

- 14.1.15 VIASTORE

- TABLE 193 VIASTORE: COMPANY OVERVIEW

- TABLE 194 VIASTORE: PRODUCTS OFFERED

- TABLE 195 VIASTORE: DEALS

- TABLE 196 VIASTORE: OTHERS

- 14.2 OTHER PLAYERS

- 14.2.1 ADDVERB TECHNOLOGIES

- TABLE 197 ADDVERB TECHNOLOGIES: COMPANY OVERVIEW

- 14.2.2 AUTOCRIB

- TABLE 198 AUTOCRIB: COMPANY OVERVIEW

- 14.2.3 AUTOMATION LOGISTIC

- TABLE 199 AUTOMATION LOGISTIC: COMPANY OVERVIEW

- 14.2.4 AVANCON

- TABLE 200 AVANCON: COMPANY OVERVIEW

- 14.2.5 FERRETTO

- TABLE 201 FERRETTO: COMPANY OVERVIEW

- 14.2.6 GRABIT

- TABLE 202 GRABIT: COMPANY OVERVIEW

- 14.2.7 INVATA INTRALOGISTICS

- TABLE 203 INVATA INTRALOGISTICS: COMPANY OVERVIEW

- 14.2.8 INVIA ROBOTICS

- TABLE 204 INVIA ROBOTICS: COMPANY OVERVIEW

- 14.2.9 LOCUS ROBOTICS

- TABLE 205 LOCUS ROBOTICS: COMPANY OVERVIEW

- 14.2.10 MEIDEN AMERICA

- TABLE 206 MEIDEN AMERICA: COMPANY OVERVIEW

- 14.2.11 MOBILE INDUSTRIAL ROBOTS

- TABLE 207 MOBILE INDUSTRIAL ROBOTS: COMPANY OVERVIEW

- 14.2.12 WESTFALIA TECHNOLOGIES

- TABLE 208 WESTFALIA TECHNOLOGIES: COMPANY OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, MnM View, Right to win, Strategic choices made, Weaknesses and competitive threats might not be captured in case of unlisted companies.

15 ADJACENT MARKET

- 15.1 RFID MARKET

- 15.2 INTRODUCTION

- FIGURE 75 RFID MARKET, BY OFFERING

- FIGURE 76 TAGS SEGMENT TO ACCOUNT FOR LARGEST SHARE OF RFID MARKET DURING FORECAST PERIOD

- TABLE 209 RFID MARKET, BY OFFERING, 2018-2021 (USD MILLION)

- TABLE 210 RFID MARKET, BY OFFERING, 2022-2030 (USD MILLION)

- 15.3 TAGS

- 15.3.1 USED TO IDENTIFY ASSETS OR PERSON

- 15.4 READERS

- 15.4.1 FIXED READER

- 15.4.1.1 Rugged and cost-efficient

- 15.4.2 HANDHELD READER

- 15.4.2.1 Mainly adopted due to mobility feature

- 15.4.1 FIXED READER

- 15.5 SOFTWARE & SERVICES

- 15.5.1 VITAL FOR DATA ANALYSIS AND CLOUD-BASED DATA STORAGE

16 APPENDIX

- 16.1 INSIGHTS FROM INDUSTRY EXPERTS

- 16.2 DISCUSSION GUIDE

- 16.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.4 CUSTOMIZATION OPTIONS

- 16.5 RELATED REPORTS

- 16.6 AUTHOR DETAILS