|

|

市場調査レポート

商品コード

1446313

ポイントオブケア診断の世界市場 (~2028年):製品・プラットフォーム・サンプル・購入形態・エンドユーザー別Point of Care Diagnostics Market by Product, Platform, Sample, Purchase, End User - Global Forecast to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ポイントオブケア診断の世界市場 (~2028年):製品・プラットフォーム・サンプル・購入形態・エンドユーザー別 |

|

出版日: 2024年03月04日

発行: MarketsandMarkets

ページ情報: 英文 314 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

ポイントオブケア診断の市場規模は、497億米ドルから、予測期間中は9.4%のCAGRで推移し、2028年には778億米ドルの規模に成長すると予測されています。

糖尿病、心血管疾患、感染症など、さまざまな疾病の負担が増加しており、これらの疾病の早期発見とモニタリングに対する需要が高まっていることがPOC検査機器の採用を後押ししています。さらに、技術的な進歩、分散型検査を促進する医療政策、新興国における小規模POCメーカーの出現も予測期間中の市場成長を後押しする可能性が高いと考えられています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021-2028年 |

| 基準年 | 2023年 |

| 予測期間 | 2023-2028年 |

| 単位 | 金額 (米ドル) |

| セグメント | 製品・プラットフォーム・購入形態・サンプル・エンドユーザー・地域 |

| 対象地域 | 北米・欧州・アジア太平洋・ラテンアメリカ・中東&アフリカ |

製品別では、感染症検査製品の部門が予測期間中にもっとも高いCAGRで成長を示す見通しです。HIV、結核、呼吸器感染症などの感染症数の増加と、感染症に対するPOC検査のアベイラビリティと認知度の向上が、同部門の成長を促進する見通しです。

エンドユーザー別では、臨床ラボの部門が2022年に最大のシェアを示しています。臨床ラボは大量の検査を取り扱うことから、POC診断機器への需要が加速しています。さらに、臨床ラボの急速な拡大と、臨床ラボ環境向けの高度なPOC製品の存在も成長を促進すると考えられています。

地域別では北米が最大のシェアを占めています。北米はPOC製品およびサービスにとって最大の地域市場であり、アジア太平洋市場は予測期間中にもっとも高いCAGRで成長すると予測されています。北米の最大のシェアは、高度な診断技術の急速な採用、迅速キットメーカーと医療施設間の協力の増加、有利な償還モデル、確立された医療インフラに起因しています。

当レポートでは、世界のポイントオブケア診断の市場を調査し、市場概要、市場影響因子および市場機会の分析、技術・特許の動向、法規制・償還環境、ケーススタディ、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 技術分析

- 規制状況

- バリューチェーン分析

- サプライチェーン分析

- ポーターのファイブフォース分析

- 貿易データ

- 償還シナリオ

- 特許分析

- ケーススタディ分析

- 顧客のビジネスに影響を与える動向/ディスラプショ

- 主なステークホルダーと購入基準

- 購入基準

第6章 ポイントオブケア診断市場:購入形態別

- OTC検査製品

- 処方箋ベースの検査製品

第7章 ポイントオブケア診断市場:プラットフォーム別

- ラテラルフローアッセイ

- 免疫学的検査

- マイクロ流体工学

- ディップスティック

- 分子診断

- RT-PCR

- INAAT

- その他

第8章 ポイントオブケア診断市場:サンプル別

- 血液サンプル

- 尿サンプル

- 鼻および口腔咽頭スワブ

- その他

第9章 ポイントオブケア診断市場:製品別

- 血糖値モニタリング製品

- ストリップ

- メートル

- ランセットおよび穿刺装置

- COVID-19検査製品

- 心血管代謝モニタリング製品

- 心臓マーカー検査製品

- 血液ガス/電解質検査製品

- HBA1C検査製品

- 感染症検査製品

- HIV検査製品

- 呼吸器感染症検査製品

- C型肝炎検査製品

- ヘルスケア関連の感染検査製品

- インフルエンザ検査製品

- 熱帯病検査製品

- 性感染症検査製品

- 結核

- クロストリジウム・ディフィシル感染症検査製品

- その他の感染症検査製品

- 凝固モニタリング製品

- PT/INR試験製品

- ACT/APTTテスト製品

- 妊娠および生殖能力検査製品

- 妊娠検査薬

- 不妊検査製品

- 腫瘍/癌マーカー検査製品

- 尿検査製品

- コレステロール検査製品

- 血液検査製品

- 乱用薬物検査製品

- 甲状腺刺激ホルモン (TSH) 検査製品

- 便潜血検査製品

- その他の製品

第10章 ポイントオブケア診断市場:エンドユーザー別

- 臨床ラボ

- 外来診療施設および医師診療所

- 薬局・小売クリニック・eコマースプラットフォーム

- 病院・救命救急センター・救急治療センター

- 在宅ケア・セルフテスト

- 他のエンドユーザー

第11章 ポイントオブケア診断市場:地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第12章 競合情勢

- 主要企業の戦略/有力企業

- 収益シェア分析

- 市場シェア分析

- 企業評価マトリックス

- 新興企業/中小企業の評価マトリックス

- 競合シナリオ

第13章 企業プロファイル

- 主要企業

- ABBOTT LABORATORIES

- F. HOFFMANN-LA ROCHE LTD.

- SIEMENS HEALTHINEERS

- QUIDELORTHO CORPORATION

- DANAHER CORPORATION

- BECTON, DICKINSON AND COMPANY

- THERMO FISHER SCIENTIFIC INC.

- BIOMERIEUX

- CHEMBIO DIAGNOSTICS, INC.

- EKF DIAGNOSTICS HOLDINGS PLC

- TRINITY BIOTECH PLC

- WERFEN, S.A.

- NOVA BIOMEDICAL

- PTS DIAGNOSTICS

- SEKISUI DIAGNOSTICS

- EUROLYSER DIAGNOSTICA GMBH

- RESPONSE BIOMEDICAL

- ALFA SCIENTIFIC DESIGNS, INC.

- BODITECH MED INC.

- BTNX INC.

- その他の企業

- LIFESCAN IP HOLDINGS, LLC

- ASCENSIA DIABETES CARE HOLDINGS AG

- FLUXERGY

- PRECISION BIOSENSOR, INC.

- ACON LABORATORIES, INC.

- A. MENARINI DIAGNOSTICS S.R.L.

- ORASURE TECHNOLOGIES, INC.

- MANKIND PHARMA

- GRIFOLS, S.A.

- DIASORIN S.P.A.

第14章 付録

The point of care diagnostics market is epected to reach USD 77.8 billion by 2028 from an estimated USD 49.7 billion at a CAGR of 9.4% during the forecast period (2023-2028).The gobal rising burden of various helath conditions including diabetes, cardiovascular diseases, infectious diseases and the growing demand for early detection and monitoring of these of these diseases are likely to boost the adoption of PoC tetsing devices. Additionally, technological adcamcements, hleathacre policies promoting decentralized testing and emergence of small PoC manufacturers in emerging countries are likely to booost the growth of market during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2028 |

| Base Year | 2023 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD) Billion |

| Segments | Product, Platform, Mode of Purchase, Sample, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

"Infectious disease testing products segment of point of care diagnostics market to grow with the highest CAGR in the forecast period."

Based on products, the infectious disease tetsing products segemnet is anticipated to grow at a signficant rate during the forecast period.Increasing number of infectious disease such as HIV, tuberculosis, respiratory infections, coupled with the growing availability & awareness of POC testing for infectious diseases are likely to prope the segment growth

"The clinical laboratories segment captired the largest market share of point of care diagnostics market in 2022"

On the basis of end users, the point-of-care and rapid diagnostics market is segmented into clinical laboratories; ambulatory care facilities and physicians' offices; pharmacies, retail clinics, and E-commerce platforms; hospitals, critical care centers, and urgent care centers; home care & self-testing; and other end users.

Clinical laboratories are the primary end users of point-of-care testing a they handle hgh volume of testing, accelerating the demand for point of care diagnostics devices.Moreover, the rapid exoansion of clinical laboratories and presence of advanced PoC products in cinical laboratory settings are likely to promote the growth of the segment

North America accounted for the largest share of the point of care diagnostics market by region.

The global rpoint of care diagnostics market is segmented into five major regions, namely, North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. North America is the largest regional market for PoC products and services , whereas the Asia Pacific market is estimated to grow at the highest CAGR during the forecast period. The largest share of North America can be attributed to the rapid adoption of advanced diagnostic technologies, increases collaboration among rapid kits manufacturers and healthacre facilities, favorable reimbursement models, and well established healthacre infrastructure

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-48%, Tier 2-36%, and Tier 3- 16%

- By Designation: C-level-10%, Director-level-14%, and Others-76%

- By Region: North America-40%, Europe-32%, Asia Pacific-20%, Latin America-5%, and the Middle East & Africa-3%

The major players operating in the point-of-care diagnostics market are Abbott Laboratories (US), F. Hoffmann-La Roche Ltd. (Switzerland), Siemens Healthineers (Germany), Danaher Corporation (US), and Becton, Dickinson and Company (US), QuidelOrtho Corporation (US), Chembio Diagnostics, Inc. (US), EKF Diagnostics Holdings plc)

Research Coverage

This report studies the point-of-care diagnostics market based on product, platform, mode of purchase, sample, end user and region. The report also studies factors (such as drivers, restraints, opportunities, and challenges) affecting market growth and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets with respect to their individual growth trends and forecasts the revenue of the market segments with respect to five major regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them to garner a larger market share. Firms purchasing the report could use one or a combination of the below-mentioned strategies for strengthening their market presence.

This report provides insights on the following pointers:

- Analayis of Key divers (rising prevalnce of infectious and chronic disease, growing adoption of self tetssing kits, helathacre decentralization, rising number of CLIA-wavier Poc Tests), restriants (rising pricing pressure on PoC manufactures, stringent regulatory approval procedures for new PoC devices), Opportunities (emerging markets, emerging technologies, sucha s mucrofuidics) , Challenge (Training & education in low resource countries)

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the point-of-care diagnostics market

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the point-of-care diagnostics market

- Market Development: Comprehensive information on lucrative emerging regions

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the point-of-care diagnostics market

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 KEY STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

- 1.6 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 RESEARCH DESIGN

- 2.1.1 SECONDARY RESEARCH

- 2.1.2 PRIMARY RESEARCH

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- FIGURE 2 BREAKDOWN OF PRIMARY INTERVIEWS: SUPPLY-SIDE AND DEMAND-SIDE PARTICIPANTS

- FIGURE 3 BREAKDOWN OF PRIMARIES

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 4 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- 2.2.1 VENDOR REVENUE MAPPING-BASED MARKET ESTIMATION

- 2.2.2 END-USER ASSESSMENT-BASED MARKET ESTIMATION

- FIGURE 5 POINT-OF-CARE DIAGNOSTICS MARKET: MARKET SIZE ESTIMATION METHODOLOGY

- 2.2.3 PRIMARY RESEARCH VALIDATION

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 6 DATA TRIANGULATION METHODOLOGY

- 2.4 RESEARCH LIMITATIONS

- 2.5 RECESSION IMPACT ANALYSIS

- TABLE 1 GLOBAL INFLATION RATE PROJECTIONS, 2021-2027 (% GROWTH)

3 EXECUTIVE SUMMARY

- FIGURE 7 POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2023 VS. 2028 (USD MILLION)

- FIGURE 8 POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM, 2023 VS. 2028 (USD MILLION)

- FIGURE 9 POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE, 2023 VS. 2028 (USD MILLION)

- FIGURE 10 POINT-OF-CARE DIAGNOSTICS MARKET, BY END USER, 2023 VS. 2028 (USD MILLION)

- FIGURE 11 GEOGRAPHIC SNAPSHOT OF POINT-OF-CARE DIAGNOSTICS MARKET

4 PREMIUM INSIGHTS

- 4.1 POINT-OF-CARE DIAGNOSTICS MARKET OVERVIEW

- FIGURE 12 INCREASING INCIDENCE OF INFECTIOUS DISEASES TO DRIVE MARKET

- 4.2 POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2023 VS. 2028 (USD MILLION)

- FIGURE 13 INFECTIOUS DISEASE TESTING PRODUCTS TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- 4.3 POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE (2022)

- FIGURE 14 OTC TESTING PRODUCTS ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

- 4.4 POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM, 2023 VS. 2028

- FIGURE 15 LATERAL FLOW ASSAYS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.5 POINT-OF-CARE DIAGNOSTICS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- FIGURE 16 CHINA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 17 POINT-OF-CARE DIAGNOSTICS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Rising incidence of infectious diseases

- FIGURE 18 REGIONAL INCIDENCE OF HIV (2022)

- 5.2.1.2 Increasing prevalence of target conditions

- 5.2.1.3 Favorable government initiatives for POC testing

- 5.2.1.4 Rising number of CLIA-waived POC tests

- TABLE 2 RECENT WAIVERS FOR PRODUCTS

- 5.2.2 RESTRAINTS

- 5.2.2.1 Pricing pressure on POC manufacturers

- 5.2.2.2 Stringent regulatory approval process for product commercialization

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 High growth potential of emerging markets

- 5.2.3.2 Decentralization of healthcare

- 5.2.3.3 Innovative product development

- 5.2.4 CHALLENGES

- 5.2.4.1 Inadequate standardization with centralized lab methods

- 5.2.4.2 Limited awareness in emerging markets

- 5.2.4.3 Premium pricing of novel platforms

- 5.3 TECHNOLOGY ANALYSIS

- 5.3.1 POC TESTS WITH MULTIPLEXING CAPABILITIES

- 5.3.2 STROKE/CARDIAC MARKERS

- 5.3.3 THYROID TESTING

- 5.3.4 DNA TESTING

- 5.3.5 ENDOCRINE TESTING

- 5.3.6 RESPIRATORY DIAGNOSTICS

- 5.4 REGULATORY LANDSCAPE

- TABLE 3 REGULATORY BODIES AND GOVERNMENT AGENCIES

- 5.4.1 KEY REGULATORY GUIDELINES

- 5.4.1.1 US

- FIGURE 19 US: REGULATORY PROCESS FOR IVD DEVICES

- 5.4.1.2 Canada

- FIGURE 20 CANADA: REGULATORY PROCESS FOR IVD DEVICES

- 5.4.1.3 Europe

- FIGURE 21 EUROPE: REGULATORY PROCESS FOR IVD DEVICES

- 5.4.1.4 Japan

- FIGURE 22 JAPAN: REGULATORY PROCESS FOR IVD DEVICES

- 5.4.1.5 China

- TABLE 4 CHINA: TIME, COST, AND COMPLEXITY OF REGISTRATION PROCESS

- 5.4.1.6 India

- FIGURE 23 INDIA: REGULATORY PROCESS FOR IVD DEVICES

- 5.4.1.7 Brazil

- FIGURE 24 BRAZIL: REGULATORY PROCESS FOR IVD DEVICES

- 5.5 VALUE CHAIN ANALYSIS

- FIGURE 25 VALUE CHAIN ANALYSIS-MAXIMUM VALUE ADDED DURING REGULATION & DISTRIBUTION STAGES

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.6.1 PROMINENT COMPANIES

- 5.6.2 SMALL & MEDIUM-SIZED ENTERPRISES

- 5.6.3 END USERS

- FIGURE 26 SUPPLY CHAIN ANALYSIS

- 5.6.4 PRICING ANALYSIS

- TABLE 5 AVERAGE SELLING PRICE OF LEADING PRODUCTS, BY KEY PLAYER (USD)

- FIGURE 27 AVERAGE SELLING PRICE OF TOP 2 LEADING PRODUCTS, BY KEY PLAYER

- 5.6.4.1 Average selling price trend

- TABLE 6 AVERAGE PRICE OF GLUCOSE MONITORING & CARDIOMETABOLIC MONITORING PRODUCTS, BY COUNTRY, 2022 (USD)

- TABLE 7 AVERAGE PRICE OF INFECTIOUS DISEASE TESTING PRODUCTS, BY COUNTRY, 2022 (USD)

- TABLE 8 AVERAGE PRICE OF OTHER POINT-OF-CARE TESTING PRODUCTS, BY COUNTRY, 2022 (USD)

- 5.7 PORTER'S FIVE FORCES ANALYSIS

- TABLE 9 POINT-OF-CARE DIAGNOSTICS MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.7.1 BARGAINING POWER OF BUYERS

- 5.7.2 BARGAINING POWER OF SUPPLIERS

- 5.7.3 THREAT OF NEW ENTRANTS

- 5.7.4 THREAT OF SUBSTITUTES

- 5.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.8 TRADE DATA

- TABLE 10 IMPORT DATA FOR MALARIA DIAGNOSTICS KITS (HS CODE 300211), BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 11 EXPORT DATA FOR MALARIA DIAGNOSTICS KITS (HS CODE 300211), BY COUNTRY, 2018-2021 (USD MILLION)

- 5.9 REIMBURSEMENT SCENARIO

- TABLE 12 KEY MEDICARE CLINICAL LAB FEE SCHEDULE (CLFS) CODES FOR COVID-19 TESTING

- TABLE 13 MEDICARE HCPCS CODES FOR HIV TESTING

- 5.10 PATENT ANALYSIS

- FIGURE 28 TOP 10 PATENT OWNERS FOR POINT-OF-CARE DIAGNOSTICS (JANUARY 2012-DECEMBER 2023)

- 5.10.1 ECOSYSTEM/MARKET MAP

- FIGURE 29 ANALYSIS OF PARENT MARKET: IN VITRO DIAGNOSTICS MARKET

- 5.10.2 KEY CONFERENCES & EVENTS

- TABLE 14 POINT-OF-CARE DIAGNOSTICS MARKET: LIST OF KEY CONFERENCES & EVENTS (2023-2024)

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 DEVELOPMENT OF HIGH-SENSITIVITY TROPONIN I

- TABLE 15 CASE 1: DIAGNOSING LOWER LEVELS OF TROPONIN IN CARDIAC PATIENTS

- 5.12 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 30 EMERGING TRENDS AND OPPORTUNITIES AFFECTING FUTURE REVENUE MIX

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF POINT-OF-CARE TESTING KITS & INSTRUMENTS

- TABLE 16 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR POINT-OF-CARE TESTING KITS AND INSTRUMENTS (%)

- 5.14 BUYING CRITERIA

- FIGURE 32 KEY BUYING CRITERIA FOR POINT-OF-CARE TESTING KITS & INSTRUMENTS

- TABLE 17 KEY BUYING CRITERIA FOR POC PRODUCTS

6 POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE

- 6.1 INTRODUCTION

- TABLE 18 POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE, 2021-2028 (USD MILLION)

- 6.2 OTC TESTING PRODUCTS

- 6.2.1 GROWING PATIENT PREFERENCE FOR REMOTE HEALTHCARE TO PROPEL MARKET

- TABLE 19 OTC TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 6.3 PRESCRIPTION-BASED TESTING PRODUCTS

- 6.3.1 RISING INCIDENCE OF CHRONIC DISEASES TO DRIVE MARKET

- TABLE 20 PRESCRIPTION-BASED TESTING PRODUCTS MARKET, BY REGION, 2021-2028 (USD MILLION)

7 POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM

- 7.1 INTRODUCTION

- TABLE 21 POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM, 2021-2028 (USD MILLION)

- 7.2 LATERAL FLOW ASSAYS

- 7.2.1 RISING ADOPTION OF TESTING PRODUCTS IN HOME CARE SETTINGS TO DRIVE MARKET

- TABLE 22 POINT-OF-CARE DIAGNOSTICS MARKET FOR LATERAL FLOW ASSAYS, BY REGION, 2021-2028 (USD MILLION)

- 7.3 IMMUNOASSAYS

- 7.3.1 UTILIZATION IN INFECTIOUS DISEASE TESTING TO SUPPORT MARKET GROWTH

- TABLE 23 POINT-OF-CARE DIAGNOSTICS MARKET FOR IMMUNOASSAYS, BY REGION, 2021-2028 (USD MILLION)

- 7.4 MICROFLUIDICS

- 7.4.1 GROWING TREND OF MINIATURIZATION AND RISING TECHNOLOGICAL ADVANCEMENTS TO PROPEL MARKET

- TABLE 24 POINT-OF-CARE DIAGNOSTICS MARKET FOR MICROFLUIDICS, BY REGION, 2021-2028 (USD MILLION)

- 7.5 DIPSTICKS

- 7.5.1 QUALITATIVE ANALYSIS OF MEDICAL CONDITIONS TO SUPPORT MARKET GROWTH

- TABLE 25 POINT-OF-CARE DIAGNOSTICS MARKET FOR DIPSTICKS, BY REGION, 2021-2028 (USD MILLION)

- 7.6 MOLECULAR DIAGNOSTICS

- TABLE 26 POINT-OF-CARE DIAGNOSTICS MARKET FOR MOLECULAR DIAGNOSTICS, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 27 POINT-OF-CARE DIAGNOSTICS MARKET FOR MOLECULAR DIAGNOSTICS, BY REGION, 2021-2028 (USD MILLION)

- 7.6.1 RT-PCR

- 7.6.1.1 Rising cases of COVID-19 to boost demand

- TABLE 28 POINT-OF-CARE DIAGNOSTICS MARKET FOR RT-PCR, BY REGION, 2021-2028 (USD MILLION)

- 7.6.2 INAAT

- 7.6.2.1 Cost benefits of INAAT to propel segment growth

- TABLE 29 POINT-OF-CARE DIAGNOSTICS MARKET FOR INAAT, BY REGION, 2021-2028 (USD MILLION)

- 7.6.3 OTHER TECHNOLOGIES

- TABLE 30 POINT-OF-CARE DIAGNOSTICS MARKET FOR OTHER TECHNOLOGIES, BY REGION, 2021-2028 (USD MILLION)

8 POINT-OF-CARE DIAGNOSTICS MARKET, BY SAMPLE

- 8.1 INTRODUCTION

- TABLE 31 POINT-OF-CARE DIAGNOSTICS MARKET, BY SAMPLE, 2021-2028 (USD MILLION)

- 8.2 BLOOD SAMPLES

- 8.2.1 HIGH UTILIZATION IN DISEASE DETECTION TO DRIVE MARKET

- TABLE 32 POINT-OF-CARE DIAGNOSTICS MARKET FOR BLOOD SAMPLES, BY REGION, 2021-2028 (USD MILLION)

- 8.3 URINE SAMPLES

- 8.3.1 INCREASING PREVALENCE OF KIDNEY DISORDERS AND WIDE RANGE OF DIAGNOSTIC TARGETS TO BOOST DEMAND

- TABLE 33 POINT-OF-CARE DIAGNOSTICS MARKET FOR URINE SAMPLES, BY REGION, 2021-2028 (USD MILLION)

- 8.4 NASAL & OROPHARYNGEAL SWABS

- 8.4.1 RISING INCIDENCE OF RESPIRATORY INFECTIONS TO PROPEL MARKET

- TABLE 34 POINT-OF-CARE DIAGNOSTICS MARKET FOR NASAL & OROPHARYNGEAL SWABS, BY REGION, 2021-2028 (USD MILLION)

- 8.5 OTHER SAMPLES

- TABLE 35 POINT-OF-CARE DIAGNOSTICS MARKET FOR OTHER SAMPLES, BY REGION, 2021-2028 (USD MILLION)

9 POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- TABLE 36 POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 9.2 GLUCOSE MONITORING PRODUCTS

- TABLE 37 POINT-OF-CARE DIAGNOSTICS MARKET FOR GLUCOSE MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 38 POINT-OF-CARE DIAGNOSTICS MARKET FOR GLUCOSE MONITORING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.2.1 STRIPS

- 9.2.1.1 Ability to provide single-use measurement testing to drive market

- TABLE 39 GLUCOSE MONITORING STRIPS MARKET, BY REGION, 2021-2028 (USD MILLION)

- 9.2.2 METERS

- 9.2.2.1 Ability to adjust therapeutic regimens daily to support market growth

- TABLE 40 GLUCOSE MONITORING METERS MARKET, BY REGION, 2021-2028 (USD MILLION)

- 9.2.3 LANCETS & LANCING DEVICES

- 9.2.3.1 Provision of multiple depth penetration settings to boost demand

- TABLE 41 GLUCOSE MONITORING LANCETS & LANCING DEVICES MARKET, BY REGION, 2021-2028 (USD MILLION)

- 9.3 COVID-19 TESTING PRODUCTS

- 9.3.1 RISING UPTAKE OF RT-PCR RAPID TESTS TO BOOST DEMAND

- TABLE 42 POINT-OF-CARE DIAGNOSTICS MARKET FOR COVID-19 TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

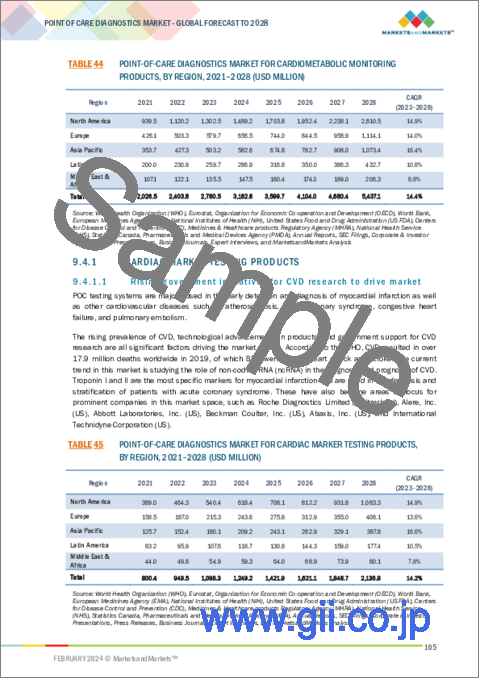

- 9.4 CARDIOMETABOLIC MONITORING PRODUCTS

- TABLE 43 POINT-OF-CARE DIAGNOSTICS MARKET FOR CARDIOMETABOLIC MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 44 POINT-OF-CARE DIAGNOSTICS MARKET FOR CARDIOMETABOLIC MONITORING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.4.1 CARDIAC MARKER TESTING PRODUCTS

- 9.4.1.1 Rising government initiatives for CVD research to drive market

- TABLE 45 POINT-OF-CARE DIAGNOSTICS MARKET FOR CARDIAC MARKER TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.4.2 BLOOD GAS/ELECTROLYTE TESTING PRODUCTS

- 9.4.2.1 Technological advancements in monitoring products to support market growth

- TABLE 46 POINT-OF-CARE DIAGNOSTICS MARKET FOR BLOOD GAS/ELECTROLYTE TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.4.3 HBA1C TESTING PRODUCTS

- 9.4.3.1 Favorable clinical outcomes with long-term monitoring to drive market

- TABLE 47 POINT-OF-CARE DIAGNOSTICS MARKET FOR HBA1C TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5 INFECTIOUS DISEASE TESTING PRODUCTS

- TABLE 48 POINT-OF-CARE DIAGNOSTICS MARKET FOR INFECTIOUS DISEASE TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 49 POINT-OF-CARE DIAGNOSTICS MARKET FOR INFECTIOUS DISEASE TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.1 HIV TESTING PRODUCTS

- 9.5.1.1 Rising prevalence of HIV to drive market

- TABLE 50 POINT-OF-CARE DIAGNOSTICS MARKET FOR HIV TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.2 RESPIRATORY INFECTION TESTING PRODUCTS

- 9.5.2.1 Rising incidence of respiratory infections to drive market

- TABLE 51 POINT-OF-CARE DIAGNOSTICS MARKET FOR RESPIRATORY INFECTION TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.3 HEPATITIS C TESTING PRODUCTS

- 9.5.3.1 Increasing prevalence of viral hepatitis to support market growth

- TABLE 52 POINT-OF-CARE DIAGNOSTICS MARKET FOR HEPATITIS C TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.4 HEALTHCARE-ASSOCIATED INFECTION TESTING PRODUCTS

- 9.5.4.1 High incidence of UTIs and surgical-site infections to boost demand

- TABLE 53 POINT-OF-CARE DIAGNOSTICS MARKET FOR HEALTHCARE-ASSOCIATED INFECTION TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.5 INFLUENZA TESTING PRODUCTS

- 9.5.5.1 Ability to identify A & B viral nucleoprotein antigens to drive market

- TABLE 54 POINT-OF-CARE DIAGNOSTICS MARKET FOR INFLUENZA TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.6 TROPICAL DISEASE TESTING PRODUCTS

- 9.5.6.1 Rising incidence of malaria and dengue to support market growth

- TABLE 55 POINT-OF-CARE DIAGNOSTICS MARKET FOR TROPICAL DISEASE TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.7 SEXUALLY TRANSMITTED DISEASE TESTING PRODUCTS

- TABLE 56 POINT-OF-CARE DIAGNOSTICS MARKET FOR STD TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 57 POINT-OF-CARE DIAGNOSTICS MARKET FOR STD TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.7.1 Syphilis testing products

- 9.5.7.1.1 Introduction of rapid tests to boost demand

- 9.5.7.1 Syphilis testing products

- TABLE 58 POINT-OF-CARE DIAGNOSTICS MARKET FOR SYPHILIS TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.7.2 Human papillomavirus (HPV) testing products

- 9.5.7.2.1 Rising uptake of HPV diagnostics and RT-PCR to support market growth

- 9.5.7.2 Human papillomavirus (HPV) testing products

- TABLE 59 POINT-OF-CARE DIAGNOSTICS MARKET FOR HPV TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.7.3 Chlamydia trachomatis testing products

- 9.5.7.3.1 Growing awareness of STI detection to boost demand

- 9.5.7.3 Chlamydia trachomatis testing products

- TABLE 60 POINT-OF-CARE DIAGNOSTICS MARKET FOR CHLAMYDIA TRACHOMATIS TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.7.4 Herpes simplex virus (HSV) testing products

- 9.5.7.4.1 Increasing incidence of HSV to support market growth

- 9.5.7.4 Herpes simplex virus (HSV) testing products

- TABLE 61 POINT-OF-CARE DIAGNOSTICS MARKET FOR HSV TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.8 TUBERCULOSIS

- 9.5.8.1 Rising prevalence of TB in underserved areas to support market growth

- TABLE 62 POINT-OF-CARE DIAGNOSTICS MARKET FOR TUBERCULOSIS, BY REGION, 2021-2028 (USD MILLION)

- 9.5.9 CLOSTRIDIUM DIFFICILE INFECTION TESTING PRODUCTS

- 9.5.9.1 Rising cases among hospitalized patients to boost demand

- TABLE 63 POINT-OF-CARE DIAGNOSTICS MARKET FOR CDI, BY REGION, 2021-2028 (USD MILLION)

- 9.5.10 OTHER INFECTIOUS DISEASE TESTING PRODUCTS

- TABLE 64 POINT-OF-CARE DIAGNOSTICS MARKET FOR OTHER INFECTIOUS DISEASE TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.6 COAGULATION MONITORING PRODUCTS

- TABLE 65 POINT-OF-CARE DIAGNOSTICS MARKET FOR COAGULATION MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 66 POINT-OF-CARE DIAGNOSTICS MARKET FOR COAGULATION MONITORING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.6.1 PT/INR TESTING PRODUCTS

- 9.6.1.1 Ability to detect blood clots to support market growth

- TABLE 67 POINT-OF-CARE DIAGNOSTICS MARKET FOR PT/INR TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.6.2 ACT/APTT TESTING PRODUCTS

- 9.6.2.1 Rising cases of dialysis and ESRD to boost demand

- TABLE 68 POINT-OF-CARE DIAGNOSTICS MARKET FOR ACT/APTT TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.7 PREGNANCY & FERTILITY TESTING PRODUCTS

- TABLE 69 POINT-OF-CARE DIAGNOSTICS MARKET FOR PREGNANCY & FERTILITY TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 70 POINT-OF-CARE DIAGNOSTICS MARKET FOR PREGNANCY & FERTILITY TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.7.1 PREGNANCY TESTING PRODUCTS

- 9.7.1.1 Growing preference for home care testing to drive market

- TABLE 71 POINT-OF-CARE DIAGNOSTICS MARKET FOR PREGNANCY TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.7.2 FERTILITY TESTING PRODUCTS

- 9.7.2.1 Growing focus on family planning to boost demand

- TABLE 72 POINT-OF-CARE DIAGNOSTICS MARKET FOR FERTILITY TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.8 TUMOR/CANCER MARKER TESTING PRODUCTS

- 9.8.1 INCREASING INCIDENCE OF CANCER AND RISING UPTAKE OF IMMUNOASSAYS TO PROPEL MARKET

- TABLE 73 POINT-OF-CARE DIAGNOSTICS MARKET FOR TUMOR/CANCER MARKER TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.9 URINALYSIS TESTING PRODUCTS

- 9.9.1 HIGH INCIDENCE OF RECURRENT UTIS TO DRIVE MARKET

- TABLE 74 POINT-OF-CARE DIAGNOSTICS MARKET FOR URINALYSIS TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.10 CHOLESTEROL TESTING PRODUCTS

- 9.10.1 RISING OBESITY LEVELS AND INCIDENCE OF CVD TO BOOST DEMAND

- TABLE 75 POINT-OF-CARE DIAGNOSTICS MARKET FOR CHOLESTEROL TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.11 HEMATOLOGY TESTING PRODUCTS

- 9.11.1 PREFERENCE FOR LABORATORY-BASED TESTS TO RESTRAIN MARKET

- TABLE 76 POINT-OF-CARE DIAGNOSTICS MARKET FOR HEMATOLOGY TESTING PRODUCTS, BY REGION, 2021-2028(USD MILLION)

- 9.12 DRUGS-OF-ABUSE TESTING PRODUCTS

- 9.12.1 RISING CONSUMPTION OF ILLICIT DRUGS TO FUEL MARKET

- TABLE 77 POINT-OF-CARE DIAGNOSTICS MARKET FOR DRUGS-OF-ABUSE TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.13 THYROID-STIMULATING HORMONE (TSH) TESTING PRODUCTS

- 9.13.1 RISING CASES OF THYROID TO BOOST DEMAND

- TABLE 78 POINT-OF-CARE DIAGNOSTICS MARKET FOR TSH TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.14 FECAL OCCULT TESTING PRODUCTS

- 9.14.1 INCREASING AWARENESS ON EARLY DISEASE DETECTION TO SUPPORT MARKET GROWTH

- TABLE 79 POINT-OF-CARE DIAGNOSTICS MARKET FOR FECAL OCCULT TESTING PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

- 9.15 OTHER PRODUCTS

- TABLE 80 POINT-OF-CARE DIAGNOSTICS MARKET FOR OTHER PRODUCTS, BY REGION, 2021-2028 (USD MILLION)

10 POINT-OF-CARE DIAGNOSTICS MARKET, BY END USER

- 10.1 INTRODUCTION

- TABLE 81 POINT-OF-CARE DIAGNOSTICS MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.2 CLINICAL LABORATORIES

- 10.2.1 IMPROVEMENTS IN AUTOMATED TESTING SERVICES TO BOOST DEMAND

- TABLE 82 POINT-OF-CARE DIAGNOSTICS MARKET FOR CLINICAL LABORATORIES, BY REGION, 2021-2028 (USD MILLION)

- 10.3 AMBULATORY CARE FACILITIES AND PHYSICIANS' OFFICES

- 10.3.1 RAPID RESULT GENERATION AND AVAILABILITY OF IMMEDIATE PATIENT CARE TO DRIVE MARKET

- TABLE 83 POINT-OF-CARE DIAGNOSTICS MARKET FOR AMBULATORY CARE FACILITIES AND PHYSICIANS' OFFICES, BY REGION, 2021-2028 (USD MILLION)

- 10.4 PHARMACIES, RETAIL CLINICS, AND E-COMMERCE PLATFORMS

- 10.4.1 ABILITY TO SUPPORT CHRONIC DISEASE MANAGEMENT TO BOOST DEMAND

- TABLE 84 POINT-OF-CARE DIAGNOSTICS MARKET FOR PHARMACIES, RETAIL CLINICS, AND E-COMMERCE PLATFORMS, BY REGION, 2021-2028 (USD MILLION)

- 10.5 HOSPITALS, CRITICAL CARE CENTERS, AND URGENT CARE CENTERS

- 10.5.1 RAPID RESULTS AND END USERS OF POC DIAGNOSTICS

- TABLE 85 POINT-OF-CARE DIAGNOSTICS MARKET FOR HOSPITALS, CRITICAL CARE CENTERS, AND URGENT CARE CENTERS, BY REGION, 2021-2028 (USD MILLION)

- 10.6 HOME CARE SETTINGS AND SELF-TESTING

- 10.6.1 GROWING INCLINATION TOWARDS REMOTE-BASED CARE TO DRIVE MARKET

- TABLE 86 POINT-OF-CARE DIAGNOSTICS MARKET FOR HOME CARE SETTINGS AND SELF-TESTING, BY REGION, 2021-2028 (USD MILLION)

- 10.7 OTHER END USERS

- TABLE 87 POINT-OF-CARE DIAGNOSTICS MARKET FOR OTHER END USERS, BY REGION, 2021-2028 (USD MILLION)

11 POINT-OF-CARE DIAGNOSTICS MARKET, BY REGION

- 11.1 INTRODUCTION

- TABLE 88 POINT-OF-CARE DIAGNOSTICS MARKET, BY REGION, 2021-2028 (USD MILLION)

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 33 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET SNAPSHOT

- TABLE 89 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 90 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- TABLE 91 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR GLUCOSE MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 92 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR CARDIOMETABOLIC MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 93 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR INFECTIOUS DISEASE TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 94 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR COAGULATION MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 95 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR PREGNANCY & FERTILITY TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 96 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM, 2021-2028 (USD MILLION)

- TABLE 97 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE, 2021-2028 (USD MILLION)

- TABLE 98 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 99 NORTH AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY SAMPLE, 2021-2028 (USD MILLION)

- 11.2.2 US

- 11.2.2.1 Favorable government support and medical reimbursements to boost demand

- TABLE 100 US: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.2.3 CANADA

- 11.2.3.1 Rising incidence of diabetes and cancer to support market growth

- TABLE 101 CANADA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.3 EUROPE

- 11.3.1 EUROPE: RECESSION IMPACT

- TABLE 102 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 103 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- TABLE 104 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET FOR GLUCOSE MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 105 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET FOR CARDIOMETABOLIC MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 106 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET FOR INFECTIOUS DISEASE TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 107 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET FOR COAGULATION MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 108 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET FOR PREGNANCY & FERTILITY TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 109 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM, 2021-2028 (USD MILLION)

- TABLE 110 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE, 2021-2028 (USD MILLION)

- TABLE 111 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 112 EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET, BY SAMPLE, 2021-2028 (USD MILLION)

- 11.3.2 GERMANY

- 11.3.2.1 Rising demand for innovative technologies to propel market

- TABLE 113 GERMANY: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.3.3 FRANCE

- 11.3.3.1 Growing public-private collaborations for product development to drive market

- TABLE 114 FRANCE: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.3.4 UK

- 11.3.4.1 Growing number of accredited diagnostic & hospital laboratories to propel market

- TABLE 115 UK: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.3.5 ITALY

- 11.3.5.1 Increasing adoption of infectious disease diagnostics to drive market

- TABLE 116 ITALY: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.3.6 SPAIN

- 11.3.6.1 Rising incidence of chronic diseases to support market growth

- TABLE 117 SPAIN: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.3.7 REST OF EUROPE

- TABLE 118 REST OF EUROPE: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 34 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET SNAPSHOT

- TABLE 119 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 120 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- TABLE 121 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET FOR GLUCOSE MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 122 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET FOR CARDIOMETABOLIC MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 123 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET FOR INFECTIOUS DISEASE TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 124 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET FOR COAGULATION MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 125 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET FOR PREGNANCY & FERTILITY TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 126 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM, 2021-2028 (USD MILLION)

- TABLE 127 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE, 2021-2028 (USD MILLION)

- TABLE 128 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 129 ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET, BY SAMPLE, 2021-2028 (USD MILLION)

- 11.4.2 JAPAN

- 11.4.2.1 Availability of advanced rapid flu tests to drive market

- TABLE 130 JAPAN: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.4.3 CHINA

- 11.4.3.1 Rising incidence of infectious diseases to drive market

- TABLE 131 CHINA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.4.4 INDIA

- 11.4.4.1 High burden of chronic diseases to propel market

- TABLE 132 INDIA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.4.5 AUSTRALIA

- 11.4.5.1 Increasing research investments for next-gen POC devices to fuel market

- TABLE 133 AUSTRALIA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION

- 11.4.6 SOUTH KOREA

- 11.4.6.1 Growing awareness about advanced POC devices to boost demand

- TABLE 134 SOUTH KOREA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.4.7 REST OF ASIA PACIFIC

- TABLE 135 REST OF ASIA PACIFIC: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.5 LATIN AMERICA

- 11.5.1 LATIN AMERICA: RECESSION IMPACT

- TABLE 136 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 137 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- TABLE 138 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR GLUCOSE MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 139 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR CARDIOMETABOLIC MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 140 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR INFECTIOUS DISEASE TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 141 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR COAGULATION MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 142 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR PREGNANCY & FERTILITY TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 143 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM, 2021-2028 (USD MILLION)

- TABLE 144 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE, 2021-2028 (USD MILLION)

- TABLE 145 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 146 LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY SAMPLE, 2021-2028 (USD MILLION)

- 11.5.2 BRAZIL

- 11.5.2.1 Rising prevalence of diabetes to support market growth

- TABLE 147 BRAZIL: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.5.3 MEXICO

- 11.5.3.1 Rising incidence of cancer to drive market

- TABLE 148 MEXICO: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.5.4 REST OF LATIN AMERICA

- TABLE 149 REST OF LATIN AMERICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 MIDDLE EAST & AFRICA: RECESSION IMPACT

- TABLE 150 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 151 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- TABLE 152 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR GLUCOSE MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 153 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR CARDIOMETABOLIC MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 154 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR INFECTIOUS DISEASE TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 155 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR COAGULATION MONITORING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 156 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET FOR PREGNANCY & FERTILITY TESTING PRODUCTS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 157 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PLATFORM, 2021-2028 (USD MILLION)

- TABLE 158 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY MODE OF PURCHASE, 2021-2028 (USD MILLION)

- TABLE 159 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 160 MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY SAMPLE, 2021-2028 (USD MILLION)

- 11.6.1.1 GCC Countries

- 11.6.1.1.1 Improvements in healthcare infrastructure to drive market

- 11.6.1.1 GCC Countries

- TABLE 161 GCC COUNTRIES: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- 11.6.2 REST OF MIDDLE EAST & AFRICA

- TABLE 162 REST OF AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

- TABLE 163 REST OF MIDDLE EAST & AFRICA: POINT-OF-CARE DIAGNOSTICS MARKET, BY PRODUCT, 2021-2028 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- FIGURE 35 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN POINT-OF-CARE DIAGNOSTICS MARKET

- 12.3 REVENUE SHARE ANALYSIS

- FIGURE 36 REVENUE ANALYSIS OF TOP FIVE PLAYERS IN POINT-OF-CARE DIAGNOSTICS MARKET (2022)

- 12.4 MARKET SHARE ANALYSIS

- FIGURE 37 POINT-OF-CARE DIAGNOSTICS MARKET SHARE, BY KEY PLAYER (2022)

- 12.5 COMPANY EVALUATION MATRIX

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- FIGURE 38 COMPANY EVALUATION MATRIX

- 12.5.5 COMPANY FOOTPRINT

- 12.5.5.1 Product & regional footprint

- TABLE 164 OVERALL FOOTPRINT

- TABLE 165 PRODUCT FOOTPRINT

- TABLE 166 REGIONAL FOOTPRINT

- 12.6 START-UP/SME EVALUATION MATRIX

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- FIGURE 39 START-UP/SME EVALUATION MATRIX

- 12.6.5 COMPETITIVE BENCHMARKING

- TABLE 167 POINT-OF-CARE DIAGNOSTICS MARKET: DETAILED LIST OF KEY START-UPS/SMES

- 12.7 COMPETITIVE SCENARIO

- 12.7.1 PRODUCT LAUNCHES & APPROVALS

- TABLE 168 POINT-OF-CARE DIAGNOSTICS MARKET: PRODUCT LAUNCHES & APPROVALS (JANUARY 2020-NOVEMBER 2023)

- 12.7.2 DEALS

- TABLE 169 POINT-OF-CARE DIAGNOSTICS MARKET: DEALS (JANUARY 2020-NOVEMBER 2023)

- 12.7.3 OTHER DEVELOPMENTS

- TABLE 170 POINT-OF-CARE DIAGNOSTICS MARKET: OTHER DEVELOPMENTS (JANUARY 2020-NOVEMBER 2023)

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

(Business Overview, Products/Services/Solutions Offered, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats, Recent Developments)**

- 13.1.1 ABBOTT LABORATORIES

- TABLE 171 ABBOTT LABORATORIES: COMPANY OVERVIEW

- FIGURE 40 ABBOTT LABORATORIES: COMPANY SNAPSHOT (2022)

- 13.1.2 F. HOFFMANN-LA ROCHE LTD.

- TABLE 172 F. HOFFMANN-LA ROCHE LTD.: COMPANY OVERVIEW

- FIGURE 41 F. HOFFMANN-LA ROCHE LTD.: COMPANY SNAPSHOT (2022)

- 13.1.3 SIEMENS HEALTHINEERS

- TABLE 173 SIEMENS HEALTHINEERS: COMPANY OVERVIEW

- FIGURE 42 SIEMENS HEALTHINEERS: COMPANY SNAPSHOT (2023)

- 13.1.4 QUIDELORTHO CORPORATION

- TABLE 174 QUIDELORTHO CORPORATION: COMPANY OVERVIEW

- FIGURE 43 QUIDELORTHO CORPORATION: COMPANY SNAPSHOT (2022)

- 13.1.5 DANAHER CORPORATION

- TABLE 175 DANAHER CORPORATION: COMPANY OVERVIEW

- FIGURE 44 DANAHER CORPORATION: COMPANY SNAPSHOT (2022)

- 13.1.6 BECTON, DICKINSON AND COMPANY

- TABLE 176 BECTON, DICKINSON AND COMPANY: COMPANY OVERVIEW

- FIGURE 45 BECTON, DICKINSON AND COMPANY: COMPANY SNAPSHOT (2023)

- 13.1.7 THERMO FISHER SCIENTIFIC INC.

- TABLE 177 THERMO FISHER SCIENTIFIC INC.: COMPANY OVERVIEW

- FIGURE 46 THERMO FISHER SCIENTIFIC INC.: COMPANY SNAPSHOT (2022)

- TABLE 178 PRODUCT LAUNCHES, ENHANCEMENTS, AND APPROVALS

- 13.1.8 BIOMERIEUX

- TABLE 179 BIOMERIEUX : COMPANY OVERVIEW

- FIGURE 47 BIOMERIEUX : COMPANY SNAPSHOT (2022)

- 13.1.9 CHEMBIO DIAGNOSTICS, INC.

- TABLE 180 CHEMBIO DIAGNOSTICS, INC.: COMPANY OVERVIEW

- FIGURE 48 CHEMBIO DIAGNOSTICS, INC.: COMPANY SNAPSHOT (2022)

- 13.1.10 EKF DIAGNOSTICS HOLDINGS PLC

- TABLE 181 EKF DIAGNOSTICS HOLDINGS PLC: COMPANY OVERVIEW

- FIGURE 49 EKF DIAGNOSTICS HOLDINGS PLC: COMPANY SNAPSHOT (2022)

- 13.1.11 TRINITY BIOTECH PLC

- TABLE 182 TRINITY BIOTECH PLC: COMPANY OVERVIEW

- FIGURE 50 TRINITY BIOTECH PLC: COMPANY SNAPSHOT (2022)

- 13.1.12 WERFEN, S.A.

- TABLE 183 WERFEN: COMPANY OVERVIEW

- FIGURE 51 WERFEN, S.A.: COMPANY SNAPSHOT (2022)

- 13.1.13 NOVA BIOMEDICAL

- TABLE 184 NOVA BIOMEDICAL: COMPANY OVERVIEW

- 13.1.14 PTS DIAGNOSTICS

- TABLE 185 PTS DIAGNOSTICS: COMPANY OVERVIEW

- 13.1.15 SEKISUI DIAGNOSTICS

- TABLE 186 SEKISUI DIAGNOSTICS: COMPANY OVERVIEW

- 13.1.16 EUROLYSER DIAGNOSTICA GMBH

- TABLE 187 EUROLYSER DIAGNOSTICA GMBH: COMPANY OVERVIEW

- 13.1.17 RESPONSE BIOMEDICAL

- TABLE 188 RESPONSE BIOMEDICAL: COMPANY OVERVIEW

- 13.1.18 ALFA SCIENTIFIC DESIGNS, INC.

- TABLE 189 ALFA SCIENTIFIC DESIGNS, INC: COMPANY OVERVIEW

- 13.1.19 BODITECH MED INC.

- TABLE 190 BODITECH MED INC.: COMPANY OVERVIEW

- 13.1.20 BTNX INC.

- TABLE 191 BTNX INC.: COMPANY OVERVIEW

- *Business Overview, Products/Services/Solutions Offered, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats, Recent Developments might not be captured in case of unlisted companies.

- 13.2 OTHER PLAYERS

- 13.2.1 LIFESCAN IP HOLDINGS, LLC

- 13.2.2 ASCENSIA DIABETES CARE HOLDINGS AG

- 13.2.3 FLUXERGY

- 13.2.4 PRECISION BIOSENSOR, INC.

- 13.2.5 ACON LABORATORIES, INC.

- 13.2.6 A. MENARINI DIAGNOSTICS S.R.L.

- 13.2.7 ORASURE TECHNOLOGIES, INC.

- 13.2.8 MANKIND PHARMA

- 13.2.9 GRIFOLS, S.A.

- 13.2.10 DIASORIN S.P.A.

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS